examiners’ commentaries 2012 - wordpress.com · examiners’ commentaries 2012 1 ... information...

TRANSCRIPT

Examiners’ commentaries 2012

1

Examiners’ commentaries 2012

AC1025 Principles of accounting

Important note

This commentary reflects the examination and assessment arrangements for this course in the academic year 2011–12. The format and structure of the examination may change in future years, and any such changes will be publicised on the virtual learning environment (VLE).

Information about the subject guideUnless otherwise stated, all cross-references will be to the latest version of the subject guide (2012).

General remarks

Learning outcomes At the end of this course, and having completed the Essential reading and activities, you should be able to:

• distinguish between different uses of accounting information and relate these uses to the needs of different groups of users

• explain the limitations of such statements and their analysis

• categorise cost behaviour, and prepare and contrast inventory valuations under different costing methods

• describe the budgeting process and discuss the use of budgets in planning and control

• explain, discuss and apply relevant techniques to aid internal users in decision-making.

What the Examiners are looking forThe examination paper covers a range of financial and management accounting topics, all of which the well-prepared candidate will have studied. The questions are designed to encourage candidates to think about the theories and principles of accounting and to demonstrate their ability to apply relevant concepts in a variety of situations or to a given set of information. Where appropriate, questions are sub-divided to help candidates answer in a logical manner. The examination will always include questions designed to test candidates’ ability in interpretation and analysis of financial information.

The rubric of the examination paper is set out on the front cover and you should ensure that you precisely follow these instructions. It is very important that you do not waste time and effort in answering more questions than required, as marks will only be awarded to the correct number of questions. You are advised to read all of the questions before deciding which to answer in each section. Time allocation is an important factor in accounting examinations. You should decide how much time to spend on each question, based on the overall marks for the question and for each section, and should then adhere to these time allocations. The

AC1025 Principles of accounting

2

format of the examination requires you to answer question 1 of Section A, which is in four parts. It is important that you allocate your time on this question so that you attempt all of the four parts. You are then required to answer question 2 of Section B, and two further questions, one from Section C and one from either Sections B or C. Please note that failure to comply with these requirements may result in some of your work not being marked.

The rubric of the examination states that workings must be submitted for all questions requiring calculations. The importance of this cannot be overstated as, in the absence of workings, simple arithmetic errors cannot be distinguished from errors of principle and understanding. Thus the absence of workings will very often lead to an over-penalisation of errors. Of course, arithmetic errors may, in some instances, result in some loss of marks and you should always be careful to check your calculations. The rubric also states that any necessary assumptions introduced into answering a question should be stated. If you do not understand what a question is asking (a circumstance the Examiners endeavour to avoid), then you must state any consequent assumptions that you have made. Even if you do not answer in precisely the way the Examiners had hoped, you may get a good mark – providing your assumptions are reasonable.

The most frequent reason for failing to do well in the examination, apart from lack of knowledge, is not answering the question actually set. You should take time to read each question carefully, and then attempt to answer everything that the Examiners require. Far too many candidates include every scrap of knowledge they have on a topic without specifically addressing the question and this can have a disastrous effect on their marks. Read the question carefully and tailor your answer to precisely what it asks and you should do well.

Accounting is a progressive subject where it is essential to understand a particular topic before you go on to the next. Make sure that you understand the basic concepts and can apply them in an appropriate manner so that there is a logical structure to your answers. Do not write something that you do not understand for, if you do, you are likely to produce a muddled response. In answering computational questions, think carefully about the layout and logical progression of your answer before writing and set out your answer in a structured and easily readable format. You will be rewarded for an appropriate, logical and sensible method, even if the figures contain errors. The subject guide and textbook contain numerous worked examples, which you should have studied carefully, and practice questions with solutions, which should form a key part of your study and revision.

You will find 8-column accounting paper is incorporated into the answer booklet. It may be particularly useful where tables of figures are required because it keeps answers neat and saves ruling lines for different columns. You are strongly advised to practise using it while you are preparing answers as part of your study of accounting. A sheet is available to download from the AC1025 page on the VLE and you can print off as many sheets of the paper as you need.

This subject does not require a lot of reading beyond the core text of Perks, R. and D. Leiwy Accounting: understanding and practice. (Maidenhead: McGraw-Hill, 2010) third edition [ISBN 9780077124786], but it is essential that you adopt an approach of thorough study, plenty of practice answering questions and an ability and willingness to think logically.

Examiners’ commentaries 2012

3

All major topics are covered at the appropriate level in the recommended text by Perks and Leiwy and others are covered in the subject guide. References presented in the ‘Comments on specific questions’ for Zone A and Zone B indicate where certain topics may be found in the current edition of the subject guide (2012), which is an essential part of the study material for this course. You are also encouraged to read the financial press, including accounting journals and listen to, or watch, financial programmes and visit appropriate websites. This will enable you to keep abreast of current issues and help you to develop your ideas and opinions about them.

Question spotting

Many candidates are disappointed to find that their examination performance is poorer than they expected. This can be due to a number of different reasons and the Examiners’ commentaries suggest ways of addressing common problems and improving your performance. We want to draw your attention to one particular failing – ‘question spotting’, that is, confining your examination preparation to a few question topics which have come up in past papers for the course. This can have very serious consequences.

We recognise that candidates may not cover all topics in the syllabus in the same depth, but you need to be aware that Examiners are free to set questions on any aspect of the syllabus. This means that you need to study enough of the syllabus to enable you to answer the required number of examination questions.

The syllabus can be found in the Course information sheet in the section of the VLE dedicated to this course. You should read the syllabus very carefully and ensure that you cover sufficient material in preparation for the examination.

Examiners will vary the topics and questions from year to year and may well set questions that have not appeared in past papers – every topic on the syllabus is a legitimate examination target. So although past papers can be helpful in revision, you cannot assume that topics or specific questions that have come up in past examinations will occur again.

AC1025 Principles of accounting

4

Examiners’ commentaries 2012

AC1025 Principles of accounting – Zone A

Important note

This commentary reflects the examination and assessment arrangements for this course in the academic year 2011–12. The format and structure of the examination may change in future years, and any such changes will be publicised on the virtual learning environment (VLE).

Information about the subject guideUnless otherwise stated, all cross-references will be to the latest version of the subject guide (2012).

Comments on specific questions

Candidates should answer FOUR of the following SEVEN questions: QUESTION 1 of Section A, QUESTION 2 of Section B, ONE question from Section C and ONE further question from either Section B or C. All questions carry equal marks.

Section AAnswer Question 1 from this section.

Question 1

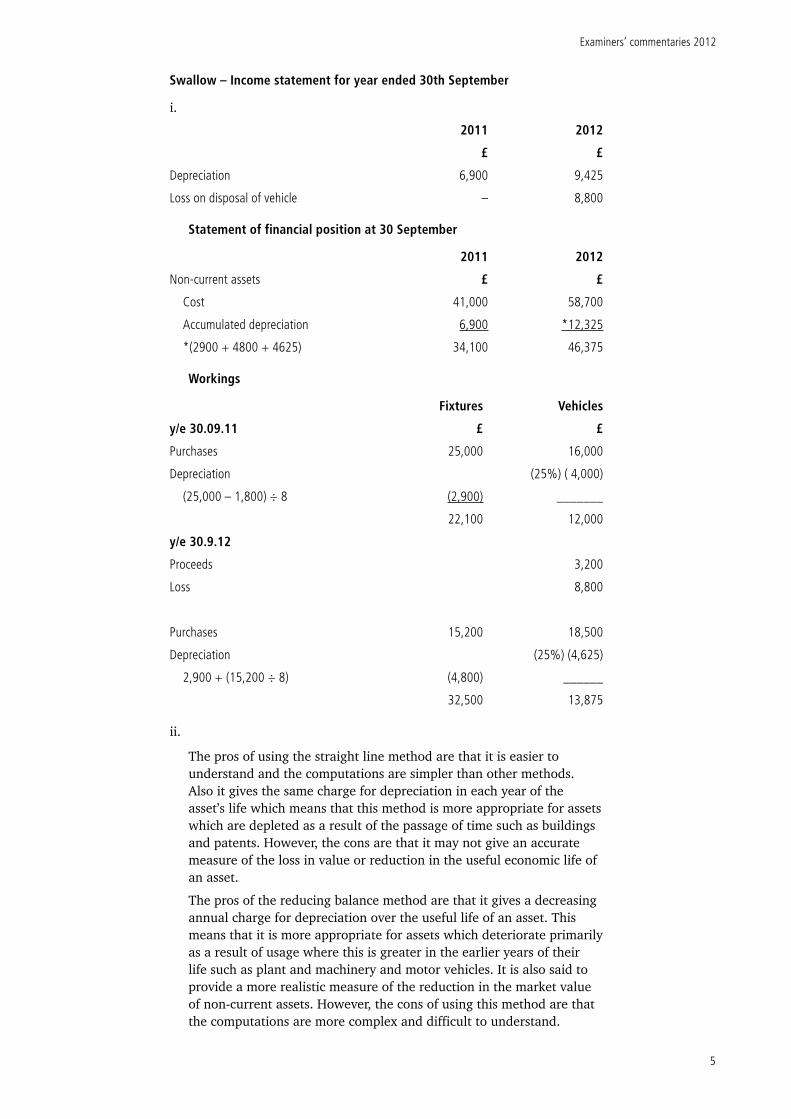

(a) Swallow commenced business on 1st October 2010 purchasing fixtures and fittings for £25,000 and a motor vehicle for £16,000. The fixtures and fittings were estimated to have a useful life of 8 years and a residual value of £1,800. Further fittings were purchased on 1 November 2011 for £15,200 with nil residual value and a useful life of 8 years.

During December 2011 the motor vehicle was involved in an accident and the insurance assessors considered it a write-off. A cheque for £3,200 was received in December from the insurers in full settlement. Another vehicle was purchased on 5 January 2012 at a cost of £18,500.

The depreciation policy of Swallow is to charge a full year’s depreciation in the year of purchase and none in the year of disposal, and to depreciate fixtures and fittings on a straight-line basis and vehicles by 25% reducing balance….

[For the full question please refer to the examination paper.]

Reading for this question

Subject guide, Chapter 4.

Perks, R. and D. Leiwy Accounting: understanding and practice. (Maidenhead: McGraw-Hill, 2010) third edition [ISBN 9780077124786] Chapter 1.

Approaching the question

One of the key aims of this course is to be able to apply financial accounting techniques and concepts to a set of data. Depreciation is a key accounting concept. Part (ii) requires a discussion of the advantages and disadvantages of the two methods of depreciation.

Examiners’ commentaries 2012

5

Swallow – Income statement for year ended 30th September

i.

2011 2012

£ £

Depreciation 6,900 9,425

Loss on disposal of vehicle – 8,800

Statement of financial position at 30 September

2011 2012

Non-current assets £ £

Cost 41,000 58,700

Accumulated depreciation 6,900 *12,325

*(2900 + 4800 + 4625) 34,100 46,375

Workings

Fixtures Vehicles

y/e 30.09.11 £ £

Purchases 25,000 16,000

Depreciation (25%) ( 4,000)

(25,000 – 1,800) ÷ 8 (2,900) _______

22,100 12,000

y/e 30.9.12

Proceeds 3,200

Loss 8,800

Purchases 15,200 18,500

Depreciation (25%) (4,625)

2,900 + (15,200 ÷ 8) (4,800) ______

32,500 13,875

ii.

The pros of using the straight line method are that it is easier to understand and the computations are simpler than other methods. Also it gives the same charge for depreciation in each year of the asset’s life which means that this method is more appropriate for assets which are depleted as a result of the passage of time such as buildings and patents. However, the cons are that it may not give an accurate measure of the loss in value or reduction in the useful economic life of an asset.

The pros of the reducing balance method are that it gives a decreasing annual charge for depreciation over the useful life of an asset. This means that it is more appropriate for assets which deteriorate primarily as a result of usage where this is greater in the earlier years of their life such as plant and machinery and motor vehicles. It is also said to provide a more realistic measure of the reduction in the market value of non-current assets. However, the cons of using this method are that the computations are more complex and difficult to understand.

AC1025 Principles of accounting

6

(b) Required:

Explain the objective of published financial statements and identify the two principal characteristics of financial statements which contribute to achieving this objective. (6 marks)

Reading for this question

Subject guide Chapter 1.

Perks and Leiwy (2010) Chapter 3.

Approaching the question

Understanding of the objectives and characteristics of financial statements is a fundamental conceptual underpinning to this course. Answers which discuss the content of financial statements (income, assets, etc.) or the format (income statement, cash flow statements, etc.) do not address the issue raised in the question.

Answers should explain that the objective of financial statements is to provide information that users (investors, lenders and creditors) need in making decisions about the reporting entity.

The two principal (qualitative) characteristics of financial statements are relevance and faithful representation (or reliability). Good answers will explain the predictive and confirmatory value of relevance, and the comparability and understandability of faithful representation.

(c) Required:

In the context of cost-volume-profit (CVP) analysis explain the meaning, and give an example of each of the following terms:

i. Non-linear variable costs

ii. Stepped fixed costs

iii. Relevant range (6 marks)

Reading for this question

Subject guide Chapter 10.

Perks and Leiwy (2010) Chapter 15.

Approaching the question

This question tests candidates’ ability to explain the three terms used in cost-volume-profit (CVP) analysis. An example of each of the terms should be used to demonstrate the meaning and application of the terms.

i. Non-linear variable costs vary with volume of activity but with a cost per unit which is different for different levels of activity.

Example Direct material where there are discounts available for larger orders.

ii. Stepped fixed costs are those which do not vary with volume of activity between two levels of activity but which, at the higher level, will require an extra resource.

Example Rental of storage facility which has a maximum capacity after which a new facility will have to be rented.

iii. The relevant range is the range of outputs over which the assumption that a cost-volume relationship is a linear relationship is realistic.

Example A firm may determine variable and fixed costs which will be realistic between 10,000 and 15,000 units; outside of this range these costs will no longer behave in the assumed linear fashion.

Examiners’ commentaries 2012

7

(d) Kestrel Ltd manufactures a single product which sells at £1.20 per unit. The variable cost of this product is 60p per unit. At present the fixed expenses of the company are £30,000 p.a. Kestrel is currently selling its full productive capacity of 100,000 units p.a. at what the company’s directors believe is the optimum price-volume relationship for the product. However, they are considering selling the product under an additional brand name. While being virtually identical from the manufacturing point of view, brands will be differentiated by the packaging and the marketing approaches adopted. Sales of the existing and the new brand when both are priced at 90p per unit are expected to total 250,000 units.

[For the full question please refer to the examination paper.]

Reading for this question

Subject guide Chapter 10.

Perks and Leiwy (2010) Chapter 15.

Approaching the question

A key learning outcome of this course is to apply decision-making techniques using accounting information. This question requires basic calculations of information which would be useful to a company in deciding between two schemes. Answers should show understanding of the techniques and an ability to assess the information and draw reasoned conclusions.

i. Existing Proposed scheme

• BEP 30,000 1.20 – 0.6

50,000 units 60,000 = 150,000 0.9 – 0.5

• Profit

(0.6 100,000) – 30,000 =

(0.4 250,000) – 60,000 =

£30,000

£40,000

• Margin of safety 50,000 units

= 50%

100,000 units

= 40%

ii. Existing profit level = £30,000

Sales volume at predicted sales price

= 60,000 + 30,000 = 0.4

225,000

Sales price at predicted volume

Cost = 60,000 + 30,000 = 36p

250,000

Price = 36 + 50 = 86p

iii. The proposed scheme

• gives 33% increase in profits if predictions are achieved

• has a higher break-even point but if predicted sales are achieved, a similar unit margin of safety – but in percentage terms it is riskier

• if the scheme is adopted the level of sales needed to at least achieve current profits is 90% of predicted levels

• Or, sales price can be dropped from 90p to 86p.

Overall the proposed scheme seems to give reasonably low risk with higher profits.

AC1025 Principles of accounting

8

Section BAnswer Question 2 from this section, and one further question from either Section B or C

Question 2

The following is the trial balance of Nightingale Ltd as at 30 April 2011:

£ £

100,000 equity shares of £1 each 100,000

50,000 7% preference shares of 50p each 25,000

Land and buildings, at valuation 240,000

Accumulated depreciation: Buildings 13,100

Plant and equipment, at cost 13,000

Accumulated depreciation: Plant and equipment 3,900

Inventory 9,400

Trade receivables 11,200

Trade payables 8,300

Bank overdraft 7,800

Purchases 49,700

Sales 135,900

Administrative expenses 28,400

Distribution costs 11,700

Interest on debentures 1,200

10% debentures 24,000

Investments (current assets) 8,000

Provision for bad debts 910

Share premium 35,000

General reserve 10,200

Interim dividend paid on equity shares 3,250

Bed debts written off 700

Revaluation reserve 9,860

Retained earnings 2,580

_______ ______

376,550 376,550

The following additonal information is available:

(1) Inventory at 30 April 2011 is valued at £13,480.

(2) Administrative expenses of £1,150 were prepaid on 30 April 2011.

(3) Depreciation on buildings is to be provided at a rate of 15% per annum on the carrying value of £80,000 and the plant and equipment should be depreciated to result in a net book value of £7,800 on 30 April 2011. Depreciation is to be included in administrative expenses.

(4) The provision for bad debts is to be adjusted to 10% of the trade receivables at the period end. Bad debts and changes to the provision are to be treated as administrative expenses.

Examiners’ commentaries 2012

9

(5) The corporation tax on this year’s profit of £6,370 is to be provided for.

(6) The preference share dividends are outstanding at the period end (30 April 2011) and the last half year’s interest on the debentures has not been paid.

(7) The directors propose to declare a final dividend on the equity shares of 13 pence per share and transfer £2,500 to general reserves.

(8) The account policies of Nightingale Ltd include the following:

• Preference shares are to be treated as a non-current liability and the preference dividend as a finance cost.

• Equity dividends are only accounted for when paid and are shown as part of the changes in equity.

[For the full question please refer to the examination paper.]

Reading for this question

Subject guide Chapters 5 and 6.

Perks and Leiwy (2010) Chapter 18.

Approaching the question

The preparation of final accounts from structured information is a key learning outcome. A trial balance with several adjusting items has been the format for the compulsory question over recent years. In answering this type of question a methodical and organised approach is needed. It is very important that detailed, legible workings are given in order that marks are awarded for all work which is correct. If figures in the final accounts comprise a number of items, marks will be awarded accordingly. Without workings one error may result in several marks being lost. The workings may be shown on the face of the accounts or separately but candidates should try and help the Examiners to award all appropriate marks by clear presentations. The 8-column accounting paper provided is particularly useful for presenting the financial statements. You should pay attention to the presentation of your answer, taking care to use the appropriate descriptions of line items in the income statement and statement of financial position. The format of the Statement of Changes in Equity should follow best practice.

(a)

i. Income statement for the year ended 30 April 2011

£

Sales revenue 135,900

Cost of sales [W1] (45,620)

Gross profit 90,280

Distribution costs (11,700)

Administrative expenses [W2] (41,460)

Profit before Interest and Tax 37,120

Finance costs [W6] (4,150)

Profit before tax 32,970

Taxation (6,370)

Profit for the year 26,600

AC1025 Principles of accounting

10

ii. Statement of changes in equity for the year ended 30 April 2011

Share capital

Share premium

Revaluation reserve

General reserve

Retained earnings

Total

£ £ £ £ £ £Balance at 1/5/10 100,000 35,000 9,860 10,200 2,580 157,640

Changes in equity:

Equity dividends paid

Total income (profit)

Transfer 2,500

(3,250)

26,600

(2,500)

(3,250)

26,600

Balance at 30/4/11 100,000 35,000 9,860 12.700 23,430 180,990

iii. Statement of financial position as at 30 April 2011

£ £ £ASSETSNon-current assets:

Land and buildings

Fixtures and fittings

240,000

13,000

25,100

5,200

214,900

7,800253,000 30,300 222,700

Current assets:

Inventory

Trade debtors

Less: provision for doubtful debts

Prepayments

Investments

11,200

(1,120)

13,480

10,080

1,150

8,000

Total assets 255,410

EQUITY AND LIABILITIESNon-current liabilities: 10% debentures 24,000 50,000 7% preference shares 25,000Total non-current liabilities 49,000Current liabilities: Bank overdraft 7,800 Trade creditors 8,300 Accrued tax 6,370 Accrued debenture interest 1,200 Preference dividend 1,750Total current liabilities 25,420Total liabilities: 74,420

Equity

Share capital

Reserves

100,000

80,990

180,990

Total equity and liabilities 255,410

Presentation

Examiners’ commentaries 2012

11

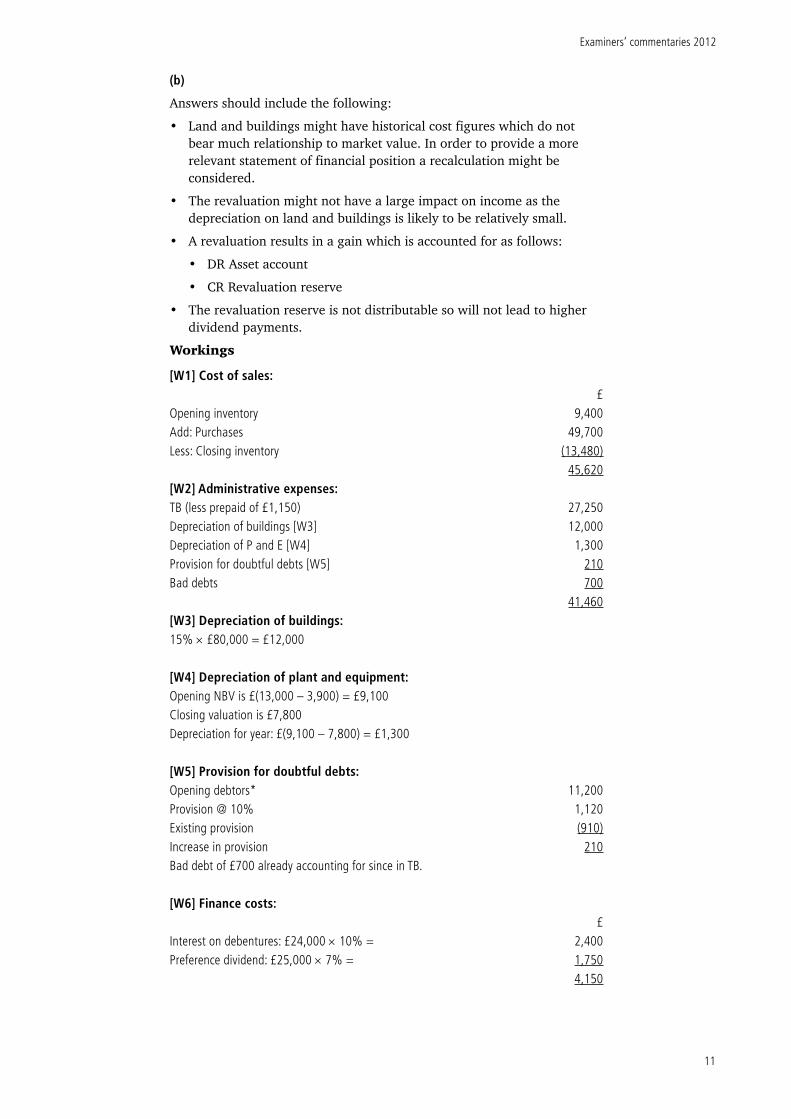

(b)

Answers should include the following:

• Land and buildings might have historical cost figures which do not bear much relationship to market value. In order to provide a more relevant statement of financial position a recalculation might be considered.

• The revaluation might not have a large impact on income as the depreciation on land and buildings is likely to be relatively small.

• A revaluation results in a gain which is accounted for as follows:

• DR Asset account

• CR Revaluation reserve

• The revaluation reserve is not distributable so will not lead to higher dividend payments.

Workings

[W1] Cost of sales:£

Opening inventory 9,400Add: Purchases 49,700Less: Closing inventory (13,480)

45,620[W2] Administrative expenses:TB (less prepaid of £1,150) 27,250Depreciation of buildings [W3] 12,000Depreciation of P and E [W4] 1,300Provision for doubtful debts [W5] 210Bad debts 700

41,460[W3] Depreciation of buildings:15% £80,000 = £12,000

[W4] Depreciation of plant and equipment:Opening NBV is £(13,000 – 3,900) = £9,100Closing valuation is £7,800Depreciation for year: £(9,100 – 7,800) = £1,300

[W5] Provision for doubtful debts:Opening debtors* 11,200Provision @ 10% 1,120Existing provision (910)Increase in provision 210Bad debt of £700 already accounting for since in TB.

[W6] Finance costs:£

Interest on debentures: £24,000 10% = 2,400Preference dividend: £25,000 7% = 1,750

4,150

AC1025 Principles of accounting

12

Question 3

The statement of financial position of Lapwing plc for the year ended 31 December 2011, together with comparative figures for the previous year, is shown below:

2011 2010£’000 £’000

ASSETSNon-current assetsProperty, plant and equipment – cost 270 180Accumulated depreciation (90) (56)

180 124Current assetsInventory 50 42Trade receivables 40 33Cash – 11

90 86Total assets 270 210

EQUITY AND LIABILITIESEquity Equity share capital £1 shares 25 20Share premium 10 8Retained earnings 93 81Total equity 128 109

Non-current liabilities15% debentures repayable 2015 80 60

Current liabilitiesTrade and operating payables 33 24Current tax payable 19 17Bank overdraft 10 –Total current liabilities 62 41Total liabilities 142 101Total equity and liabilities 270 210

Additional information:

(1) Plant had been sold during the year for £15,000 with a loss on disposal of £5,000. The cost of the plant sold was £27,000.

(2) The company declared a final dividend of £26,000 for 2011 (2010 was £28,000).This is paid immediately after the AGM that takes place after the year end.The company did not pay any interim dividends.

(3) New debentures and shares issued in 2011 were issued on 1 January.

(4) The taxation liability at each year end is settled in full in the following year.

[For the full question please refer to the examination paper.]

Reading for this question

Subject guide Chapter 6.

Perks and Leiwy (2010) Chapter 6.

Approaching the question

This question requires preparation of a cash flow statement (CFS). You should adopt a systematic approach which will enable you to extract the cash flows from the accruals based income statement and statement of

Examiners’ commentaries 2012

13

financial position. The resulting increase or decrease in cash balances should be reconciled to the relevant figures in the statement of financial position. Good answers will be well presented, correctly describing the component cash flows with well laid out workings. In 2012 part (c) was often not attempted and candidates should remember to attempt all sections of the questions in the paper.

(a) Computation of operating profit£’000

Increase in retained earnings (93–81) 12Dividends 28Taxation 19Operating profit 59

(b) Lapwing plcStatement of cash flows for the year ended 31 December 2011Cash flows from operating activities £’000 £’000Profit before taxation 59Depreciation charges 41Loss on disposal 5Loan interest (15% £800,000) 12Operating profit before working capital changes 117Increase in trade receivables (7)Increase in inventories (8)Increase in trade payables 9Cash generated from operations 111Interest paid (12)Taxation (17)Net cash from operating activities 82Cash flows from investing activitiesSale of property, plant and equipment 15Payments to acquire property, plant and equipment (117)Net cash from investing activities (102)Cash flows from financingIssue of debentures 20Issue of equity share capital 7Equity dividends paid (28)Net cash used in financing activities (1)Decrease in cash and cash equivalents (21)Net cash and cash equivalents at 12 January 2011 11Net cash and cash equivalents at 31 December 2011 (10)

Statement of cash and cash equivalents 2010 Cash flow 2011£’000 £’000 £’000

Cash at bank 11 (11) –Overdraft – (10) (10)Total cash and cash equivalents 11 (21) (10)

(c) A statement of cash flows presented under the direct method shows operating cash receipts and payments (including, in particular, cash receipts from customers, cash payments to suppliers and cash payments to and on behalf of employees), aggregating to the net cash flow from operating activities.

AC1025 Principles of accounting

14

The direct method shows actual inflows and outflows of activities.

The indirect method shows users can assess quality of earnings by referring to reconciliation of earnings/cash flows.

Workings

Cost A/c Depn1. PPE

As at 2010 180 56Disposal (27) (7)Additions (B/F) 117Depreciation (B/F) ___ 41As at 2011 270 90

Question 4

Osprey plc is a family-owned clothes manufacturer. For a number of years the chairman and managing director was David Bird. During his period of office, sales revenue had grown steadily at a rate of two to three per cent each year. David Bird retired on 30 November 2011 and was succeeded by his son Simon. Soon after taking office, Simon decided to expand the business. Within weeks he had successfully negotiated a five-year contract with a large clothes retailer to make a range of sports and leisurewear items. The contract will result in an additional £2m in sales revenue during each year of the contract. To fulfill the contract, Osprey Ltd acquired new equipment and premises.

Financial information concerning the business is given below.

Income statements for the year ended 30 November

2011 2012£000 £000

Revenue 9,482 11,365Operating profit 914 1,042Interest charges (22) (81)Profit before taxation 892 961Taxation (358) (386)Profit for the year 534 575

[For the full question please refer to the examination paper.]

Reading for this question

Subject guide Chapter 7.

Perks and Leiwy (2010) Chapters 4, 5 and 7.

Approaching the question

The learning outcomes for Chapter 7 of the subject guide include the ability to analyse, interpret and communicate the information contained in financial statements. The most common analytical technique is often testing by a mini-case study of the type used in this question. It is important that answers go beyond simply stating that a particular ratio has gone up or down; the interpretation should use the contextual information given in the question and make links between different ratios. Good answers will draw conclusions from the ratios and the background information, which provide insight into the financial position and performance of the companies.

Excellent answers will use the analysis to draw appropriate conclusions which will be discussed from the perspectives of the lenders and shareholders.

Examiners’ commentaries 2012

15

You should carefully read the requirements of the question which, in this case, specify the number and nature of the ratios to be calculated. If you do not follow these instructions your work may not be marked.

There are no absolute answers to this type of question and you will be rewarded for a logical and informed analytical approach to the case study described in the question. The answer below illustrates such an approach, but for completeness provides more ratios than the question requires.

Osprey plc

(a) 2011 2012i. Operating profit margin

914 1009482

1042 10011365

9.6%

9.2%

ii. Net profit margin

534 1009482

575 10011365

5.6%

5.1%

iii. Asset turnover

9482 12541 – 1508

11365 19117 – 5174

0.86 x

0.81 x

iv. ROCE

914 100 11033

1042 100 13943

8.28%

7.47%

v. Current ratio

4926 1508

7700 5174

3.3 : 1

1.5 : 1

vi. Quick assets

4926 – 2386 1508

7700 – 3420 5174

1.7 : 1

0.8 : 1

AC1025 Principles of accounting

16

vii. Receivables collection period

2540 365 9482

4280 365 11365

98 days

137 days

viii. Gearing

1120 100 11033

3675 100

13943

11.1%

26.4%

(b) The operating and net profit margins were slightly lower in 2012 than in 2011. Although there was an increase in sales revenue in 2012, this could not prevent a slight fall in return on capital employed (ROCE) in that year. The lower operating margin and increases in sales revenue may well be due to the new contract. The capital employed by the company increased in 2012 by a larger percentage than the increase in revenue. Hence, the sales revenue to capital employed ratio decreased over the period. The increase in capital during 2012 is largely due to an increase in borrowing. However, the gearing ratio is probably still low in comparison with other businesses. Comparison of the premises and borrowing figures indicates possible unused borrowing (debt) capacity.

The major cause for concern has been the dramatic decline in liquidity during 2012. The current ratio has decreased by more than half during the period. There has also been a similar decrease in the quick assets ratio. The balance sheet shows that the business now has a large overdraft and the trade payables outstanding have nearly doubled in 2012.

The trade receivables outstanding and inventories have increased much more than appears to be warranted by the increase in sales revenue. This may be due to the terms of the contract that has been negotiated and may be difficult to influence. If this is the case, the business should consider whether it is overtrading. If the conclusion is that it is, increasing its long-term funding may be a sensible policy.

Examiners’ commentaries 2012

17

Section CAnswer one question from this section, and one further question from either Section B or C

Question 5

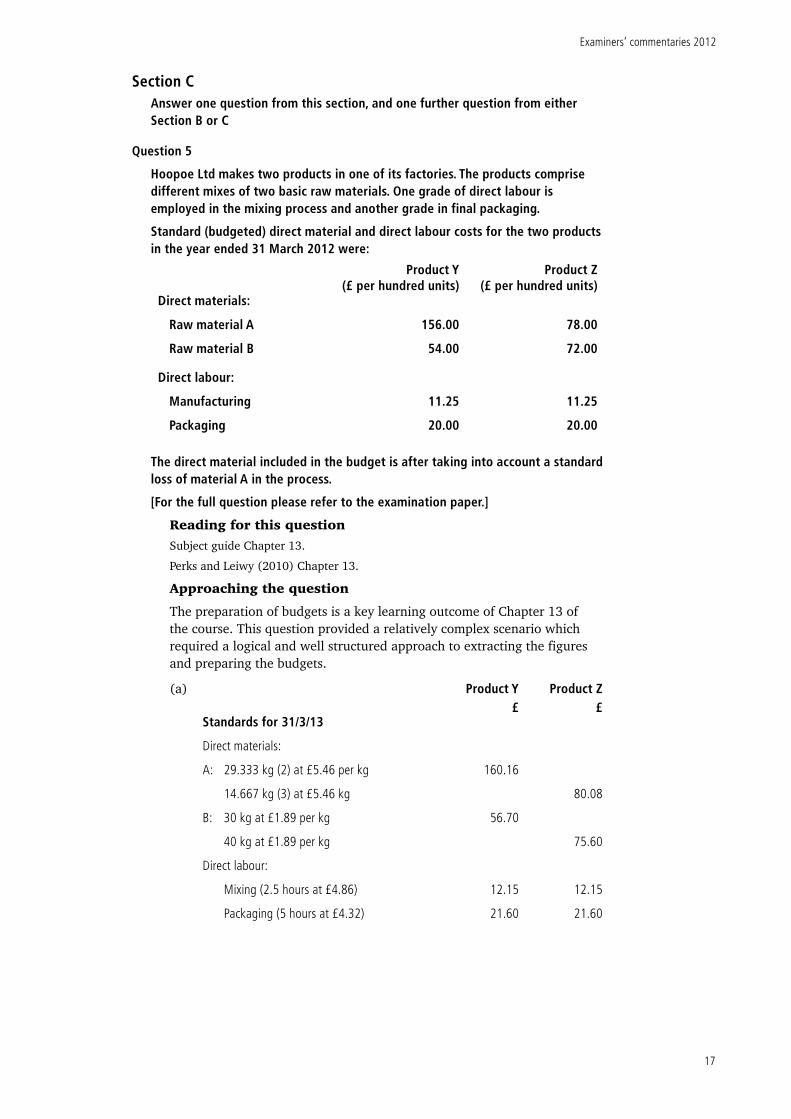

Hoopoe Ltd makes two products in one of its factories. The products comprise different mixes of two basic raw materials. One grade of direct labour is employed in the mixing process and another grade in final packaging.

Standard (budgeted) direct material and direct labour costs for the two products in the year ended 31 March 2012 were:

Product Y(£ per hundred units)

Product Z(£ per hundred units)

Direct materials:

Raw material A

Raw material B

156.00

54.00

78.00

72.00

Direct labour:

Manufacturing

Packaging

11.25

20.00

11.25

20.00

The direct material included in the budget is after taking into account a standard loss of material A in the process.

[For the full question please refer to the examination paper.]

Reading for this question

Subject guide Chapter 13.

Perks and Leiwy (2010) Chapter 13.

Approaching the question

The preparation of budgets is a key learning outcome of Chapter 13 of the course. This question provided a relatively complex scenario which required a logical and well structured approach to extracting the figures and preparing the budgets.

(a) Product Y Product Z£ £

Standards for 31/3/13

Direct materials:

A: 29.333 kg (2) at £5.46 per kg

14.667 kg (3) at £5.46 kg

B: 30 kg at £1.89 per kg

40 kg at £1.89 per kg

Direct labour:

Mixing (2.5 hours at £4.86)

Packaging (5 hours at £4.32)

160.16

56.70

12.15

21.60

80.08

75.60

12.15

21.60

AC1025 Principles of accounting

18

Notes:

1. Standards for 31/3/12

Direct materials:

A: 30 kg at £5.20 per kg

15 kg at £5.20 per kg

B: 30 kg at £1.80 per kg

40 kg at £1.80 per kg

Direct labour:

Mixing (2.5 hours at £4.50)

Packaging (5 hours at £4)

2. X- Revised input for material A = 30 (1.10/1.125) = 29.333

3. Y- Revised input for material A = 15 (1.10/1.125) =14.667

156.00

54.00

11.25

20.00

78.00

72.00

11.25

20.00

(b) i. Production budget: Product Y (units) Product Z (units) Sales

Add closing stock

1,700,000

200,000

950,000

125,000

Less closing stock

1,900,000

190,000

1,075,000

150,000 Production 1,710,000 925,000

Kilosii. Material B purchases budget: Required for production: Product Y: 1,710,000 units at 30 kg per hundred 513,000

Product Z: 925,000 units at 40 kg per hundred 370,000

883,000

Add: Closing stock

Less: Opening stock

90,000

(95,000)Required purchases 878,000Required purchase cost = £ 1,659,420

iii. Mixing labour budget:

Total production:

Product Y 1,710,000Product Z 925,000 2,635,000 units

at 2.5 hours per hundred

= 65,875 hours

Examiners’ commentaries 2012

19

Question 6

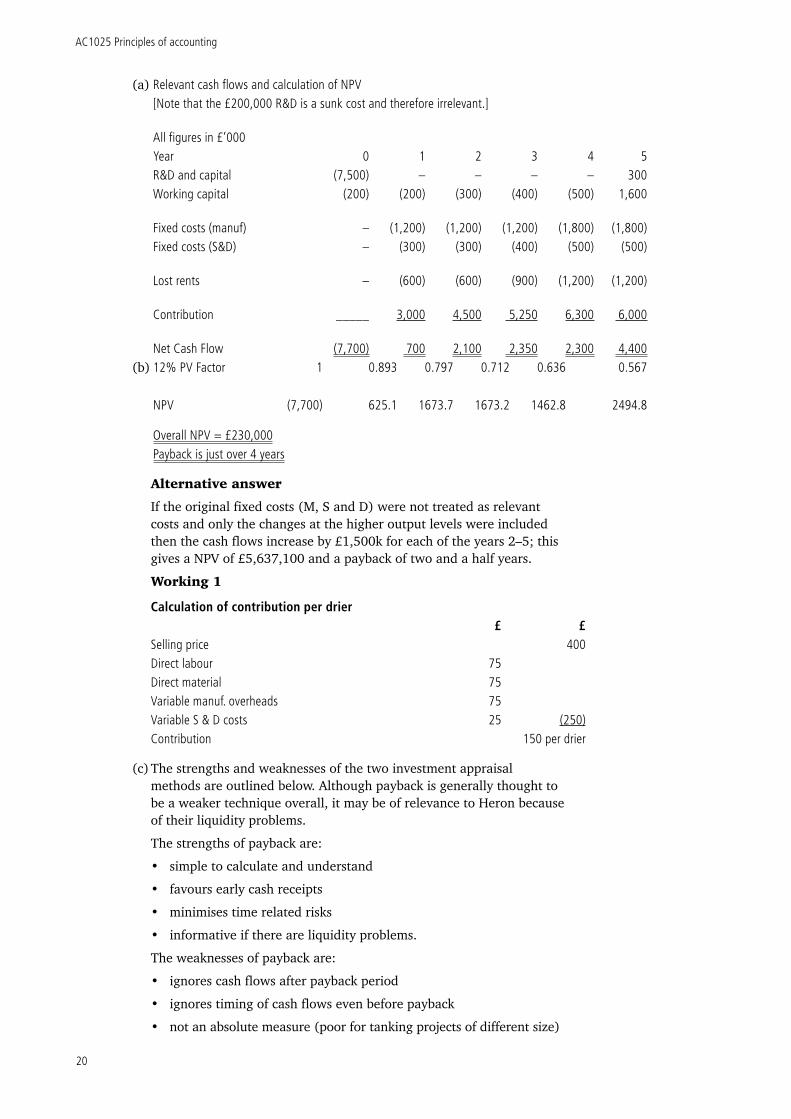

Heron Electronics Ltd is an established company which has continued to be profitable in recent years despite operating at below full capacity. Continued investment in research and development has produced a new innovative product, the microwave drier.

(1) Market research supports the proposed price of £400 per drier with the following predicted sales over the next five years:

Year Unit sales1 20,0002 30,0003 35,0004 42,0005 40,000

(2) The company accountant has collated the following costing information relating to the drier proposal:

[For the full question please refer to the examination paper.]

Reading for this question

Subject guide Chapter 12.

Perks and Leiwy (2010) Chapter 12.

Approaching the question

The application of capital investment techniques is an important element of the syllabus and the learning outcomes for Chapter 12 of the subject guide. The most effective approach to Part (a) is to construct a columnar table in which relevant cash flows can be inserted. It is important to give workings of all figures and to explain clearly treatment of all amounts, for example if a cost is to be treated as sunk and therefore not included as a relevant cost this should be stated. Having determined the net cash flow for each year, these are discounted using the discount factors taken from the tables provided. Thus a net present value and payback can be arrived at and a decision recommended and justified. This type of question requires use of a significant amount of data and it is very important that your work is clearly presented and that all workings are legible and understandable. The 8-column accounting paper can help in this respect. A suggested presentation of the answer is given below.

Part (b) was a fairly straightforward comparison of the strengths and weaknesses of NPV and Payback methods.

AC1025 Principles of accounting

20

(a) Relevant cash flows and calculation of NPV[Note that the £200,000 R&D is a sunk cost and therefore irrelevant.]

All figures in £’000Year 0 1 2 3 4 5R&D and capital (7,500) – – – – 300Working capital (200) (200) (300) (400) (500) 1,600

Fixed costs (manuf) – (1,200) (1,200) (1,200) (1,800) (1,800)Fixed costs (S&D) – (300) (300) (400) (500) (500)

Lost rents – (600) (600) (900) (1,200) (1,200)

Contribution _____ 3,000 4,500 5,250 6,300 6,000

Net Cash Flow (7,700) 700 2,100 2,350 2,300 4,400(b) 12% PV Factor 1 0.893 0.797 0.712 0.636 0.567

NPV (7,700) 625.1 1673.7 1673.2 1462.8 2494.8

Overall NPV = £230,000Payback is just over 4 years

Alternative answer

If the original fixed costs (M, S and D) were not treated as relevant costs and only the changes at the higher output levels were included then the cash flows increase by £1,500k for each of the years 2–5; this gives a NPV of £5,637,100 and a payback of two and a half years.

Working 1

Calculation of contribution per drier£ £

Selling price 400Direct labour 75Direct material 75Variable manuf. overheads 75Variable S & D costs 25 (250)Contribution 150 per drier

(c) The strengths and weaknesses of the two investment appraisal methods are outlined below. Although payback is generally thought to be a weaker technique overall, it may be of relevance to Heron because of their liquidity problems.

The strengths of payback are:

• simple to calculate and understand

• favours early cash receipts

• minimises time related risks

• informative if there are liquidity problems.

The weaknesses of payback are:

• ignores cash flows after payback period

• ignores timing of cash flows even before payback

• not an absolute measure (poor for tanking projects of different size)

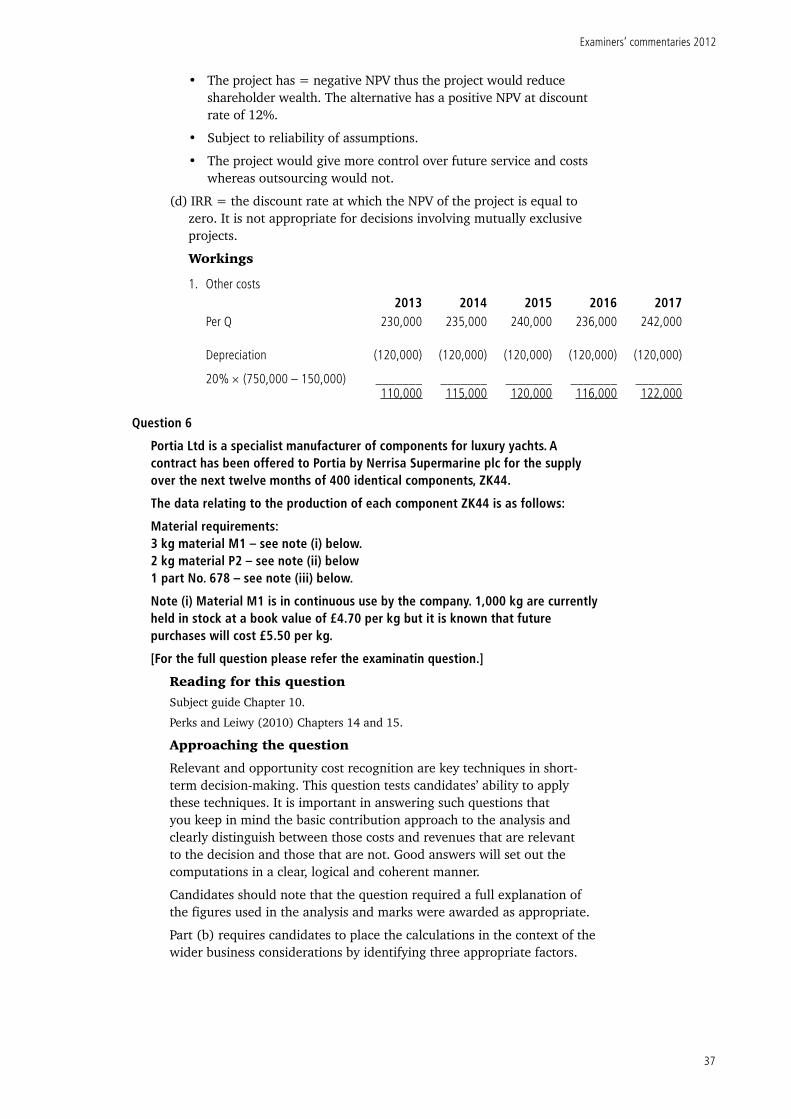

Examiners’ commentaries 2012

21

The strengths of NPV are:

• takes into account time value of money

• money sooner is better than money later because of:

1. Real Interest Rate (or opportunity cost).

2. Inflation

3. Risk

(1 and 2 are included in money interest rates)

• considers all cash flows and the whole life of the project

• an absolute measure (therefore good for ranking projects).

The weaknesses of NPV are:

• more complicated to calculate and understand

• may give impression of ‘accurate figures’ but only as good as the estimates of relevant cash flows

• has a long term view but does not consider liquidity and is not popular with managers who are assessed by short term performance measures.

Question 7

Dunnock Ltd manufactures a single product, a laminated kitchen unit, which has a standard cost of £80 made up as follows:

Direct material 15sq metres @ £3 per sq m £45Direct labour 5 hours @ £4 per hour £20Variable overheads 5 hours @ £2 per hour £10Fixed overheads £ 5

£80

• Variable overheads are charged on a direct labour hour rate.

• The standard selling price of the kitchen is £100.

• The month budget projects production and sales of 1,000 units.

• Actual figures for the month of April are as follows:

Sales 1,400 units @ £102

Production 1,400 units

Direct materials 22,000 sq metres @ £4 per sq m

Direct labour 6,800 hours @ £5

Variable overheads £11,000

Fixed overheads £6,000

There are no inventories of materials at the beginning or end of the period.

[For the full question please refer to the examination paper.]

Reading for this question

Subject guide Chapter 14.

Perks and Leiwy (2010) Chapter 16.

Approaching the question

This is a question which tests candidates’ ability to apply standard costing, budgeting and variance analysis to a given set of data. Your answer should set out clearly all of your workings and cross-refer these to the final operating statement and relevant variances. It is important that you identify variances as either favourable or adverse (unfavourable). These

AC1025 Principles of accounting

22

techniques are clearly demonstrated by examples in the subject guide and you should be prepared to apply them in questions at this level.

Part (b) tests your understanding of the variances and their interpretations. Good answers will provide a well-explained commentary for management.

(a)

Report on kitchen unit sales and production for April

£Budgeted profit 20,000 Sales variances – Price

Volume

2,800 F

10,000 F 32,800

Cost variances Fav AdvMaterials – Price – Efficiency

(22,000) (3,000)

Labour – Price – Efficiency 800

(6,800)

V. overhead – Price – Efficiency

2,600400

F. overhead – Spending _____ (1,000)3,800 32,800 (29,000)

Actual profit 3,800

(b) Commentary

• Overall budgeted profits of £20,000 have not been achieved due principally to material cost overruns.

• Sales volume has increased even after a 2p increase in sales price. If costs had been on target, a profit of £32,800 could have been achieved.

• Materials suffered a large price rise and management should investigate the cause of this; for example, have we changed supplier, purchased better quality or is this a result of a market price increase?

• Material usage was also worse than budget (which may mean better quality of material is unlikely). Management should investigate wastage and production processes.

• Labour rates have increased. This could be due to higher skilled staff mix, bonus schemes, overtime or a response to higher market rates.

• The efficiency of labour is better than anticipated; this could be due to higher skilled employees or production process efficiencies. The amount is relatively small compared to other cost variances.

• Variable overheads have cost less than anticipated. An analysis of the components would reveal where the reductions have occurred. The efficiency savings will relate to the labour efficiency referred to above.

• Fixed overheads have increased and management should investigate the components of this cost.

Examiners’ commentaries 2012

23

Workings

1. Budgeted and actual figures – AprilOriginal budget Flexed budget Actual

Materials 45,000 63,000 88,000Labour 20,000 28,000 34,000Variable overhead 10,000 14,000 11,000Fixed overhead 5,000 5,000 6,000

80,000 110,000 139,000Sales 100,000 140,000 142,800Profit 20,000 30,000 3,800

2. VariancesSales price

(AQ AP) – (AQ SP)

(1400 102) – (1400 100) = 2,800 F

Sales volume

30,000 – 20,000 =10,000 FMaterials price

(AQ AP) – (AQ SP)

(22,000 4) – (22,000 3) = 22,000 A

Materials efficiency

(AQ SP) – (SQ SP)

(22,000 3) – (21,000 3) = 3,000 A

Labour price

(AQ AP) – (AQ SP)

(6,800 5) – (6,800 4) = 6,800 A

Labour efficiency

(AQ SP) – (SQ SP)

(6,800 4) – (7,000 4) = 800 F

Variable overhead price

(AQ AP) – (AQ SP)

(11,000) – (6,800 2) = 2,600 F

Variable overhead efficiency

(AQ SP) – (SQ SP)

(6,800 2) – (7,000 2) = 400 F

Fixed overhead – spending 1000 A

AC1025 Principles of accounting

24

Examiners’ commentaries 2012

AC1025 Principles of accounting – Zone B

Important note

This commentary reflects the examination and assessment arrangements for this course in the academic year 2011–12. The format and structure of the examination may change in future years, and any such changes will be publicised on the virtual learning environment (VLE).

Information about the subject guideUnless otherwise stated, all cross-references will be to the latest version of the subject guide (2012).

Comments on specific questions

Candidates should answer FOUR of the following SEVEN questions: QUESTION 1 of Section A, QUESTION 2 of Section B, ONE question from Section C and ONE further question from either Section B or C. All questions carry equal marks.

Section AAnswer Question 1 from this section.

Question 1

(a) Required:

Explain the objective of published financial statements and identify the two principal characteristics of financial statements which contribute to achieving this objective. (6 marks)

Reading for this question

Subject guide, Chapter 1.

Perks, R. and D. Leiwy Accounting: understanding and practice. (Maidenhead: McGraw-Hill, 2010) third edition [ISBN 9780077124786] Chapter 3.

Approaching the question

Understanding of the objectives and characteristics of financial statements is a fundamental conceptual underpinning to this course. Answers which discuss the content of financial statements (income, assets, etc.) or the format (income statement, cash flow statements, etc.) do not address the issue raised in the question.

Answers should explain that the objective of financial statements provide information that users (investors, lenders and creditors) need in making decisions about the reporting entity.

The two principal (qualitative) characteristics of financial statements are relevance and faithful representation (or reliability). Good answers will explain the predictive and confirmatory value of relevance, and the comparability and understandability of faithful representation.

Examiners’ commentaries 2012

25

(b) The following data show the trading transactions of Othello Ltd for its first six months of trading. The company operates the weighted average assumption for calculation of cost of sales. Closing inventory and the cost of sales is calculated whenever a sale is made.

(1) 2011 Purchases SalesJuly 40 units at £1,000 eachAugust 80 units at £ 900 eachSeptember 50 units at £1,500October 40 units at £1,100 eachNovember 20 units at £ 700 eachDecember 20 units at £1,200 each 90 units at £1,700

The December sale occurred before the purchase in that month.

(2) The 20 units purchased in November incurred a transport charge of £2,500 to move them to the company premises. This amount is not included in the cost of £700 per unit.

(3) The 20 units purchased in December had been made to order for a customer who has now gone into liquidation. Othello Ltd can only sell these for a price of £1,000 per unit after a modification costing £150 per unit.

(4) Operating expenses for the six months amounted to 10% of sales revenue.

Required:

Prepare the Income Statement for Othello Ltd for the six months to 31st December 2011 from the above information. (6 marks)

Reading for this question

Subject guide Chapter 4.

Perks and Leiwy (2010) Chapters 1 and 2.

Approaching the question

The learning outcomes in Chapter 9 require candidates to be able to prepare and contrast stock valuations under different costing methods. This question tests the use of one method. It is important to set out the statements and calculations in a clear and organised manner. The most common failures were the incorrect treatment of the transport costs and using a periodic valuation rather than, as the question required, using a transaction-based valuation.

Othello Ltd

Income Statement for the six months to 31 December 2011

£ £Sales 228,000Purchases (196,500)Less: Closing inventory 55,718 (140,782)

________Gross profit 87,218Operating expenses (10% 228,000) (22,800)Operating profit 64,418

AC1025 Principles of accounting

26

Workings

1. Purchases

Cost 194,000 Transport costs 2,500 196,500

2. Inventory valuation Units CostAt 31 August 120 112,000Sale (50) (46,667)

70 65,333Purchases (October – November) 60 60,500*

130 125,833Sale (90) (87,115)

40 38,718December (NRV) 20 17,000

60 55,718

3. Net Realisable Value Sale price 1,000 Less: costs 150

850 20 units = 17,000

(c) Required:

Outline the main purposes and benefits of budgeting. (6 marks)

Reading for this question

Subject guide Chapter 13.

Perks and Leiwy (2010) Chapter 13.

Approaching the question

A key learning outcome is to understand the role of budgetary control in organisations. This is a straightforward test of this knowledge. Candidates should not spend time in detailed explanation of the techniques of budgeting but concentrate on the requirement to outline the purposes and benefits of budgeting.

The main purposes and benefits of budgeting are:

• Planning and anticipation. Management are forced to think ahead and plan for future eventualities. Regular budget-setting and review procedures also lead to regular examination of the organisation’s goals and decisions.

• Communication and coordination. Preparation of budgets encourages communication between different parts of the organisation and different levels of management. A cohesive budget allows activities to be coordinated. For example, the production department needs to know how much the sales department is planning to sell in order to set its target for production.

• Motivation. Budgets and standard costs provide targets and, as such, can motivate staff to achieve them, especially if staff are rewarded on the basis of meeting budget (e.g. in the form of a bonus). The simple presence of a target of any kind can often improve performance. However, care must be taken to ensure that the target is set at an appropriate level.

Examiners’ commentaries 2012

27

• Authorisation and responsibility. Managers know that budgeted expenditure has been authorised and can act accordingly. Setting individual budget for particular business activities or departments can be used to assign responsibility to individual managers for meeting those budgets.

• Evaluation and control. Budgets provide plans against which subsequent performance can be judged. Management monitor and evaluate whether budgets are fulfilled. Management performance can also be assessed and rewarded on this basis.

(d) Cordelia plc manufactures three spice mixes for catering firms: Mild, Spicy and Hot. The selling price and the variable costs per unit for each product are as follows:

Mild Spicy Hot £ £ £

Selling price 30 40 60Variable cost

Spice A

Spice B

10

10

23

5

25

15

Spice B is in short supply and this year Cordelia is only able to purchase 240,000 kilos at £5 per kilo. Spice A is plentiful.

The marketing manager predicts that the maximum demand for each product for the year will be:

[For the full question please refer to the examination paper.]

Reading for this question

Subject guide Chapter 10.

Perks and Leiwy (2010) Chapter 15.

Approaching the question

A key learning outcome of this course is to explain and apply decision-making techniques using accounting information. This question tests your understanding of contribution analysis and limiting factors. It is important that answers calculate the contribution per unit of limiting factor in reaching the optimum mix of products. Answers to part (ii) need to be specific in identifying an appropriate technique.

i. • Contribution per unit of Spice BMild Spicy Hot

Sales price 30 40 60Variable cost (20) (28) (40)

10 12 20Spice B – input (k) 2 1 3

Contribution per kilo of Spice B 5 12 6.67

• Optimum mix is: Product units Kilos of Spice ASpicy

Hot

Mild

16,000

30,000

67,000

16,000

90,000

134,000240,000

AC1025 Principles of accounting

28

• Operating profits Profit Spicy

Hot

Mild

16,000 12 =

30,000 20 =

67,000 10 =

192,000

600,000

670,0001,462,000

Fixed costs 300,000Profit for year 1,162,000

ii. This situation gives multiple limiting factors and can only be resolved using linear programming.

Section BAnswer Question 2 from this section, and one further question from either Section B or C.

Question 2

Macbeth plc prepares its financial statements for the year ended 31 March. The company has extracted the following trial balance at 31 March 2012:

£000 £0006% Loan notes (redeemable 2016) 10,250Trade payables 8,120Trade receivables 9,930Accumulated depreciation at 31 March 2011:

Plant and equipment

Vehicles

6,460

1,670Administrative expenses 16,141Bank 456Purchases returns 106Distribution costs 9,060Dividends paid 5,800Dividends received 850Equity shares, 20p each, fully paid 19,000Interest paid on 6% loan notes 615Inventories 4,852Investments, non-current 15,000Plant and equipment, at cost 27,315Proceeds from issue of share capital 1,500Provision for doubtful debts at 31 March 2011 600Purchases 94,160Retained earnings at 31 March 2011 14,677Sales 124,900Taxation 4Vehicles, at cost 5,720

________ _______£188,593 £188,593

The following further information is available:

(1) Non-current assets are to be depreciated as follows: Plant and equipment 20% per annum straight-lineVehicles 25% per annum reducing balance

Examiners’ commentaries 2012

29

(2) An invoice for telephone charges for the quarter ended 1 May 2012 for £15,000 was received by the company after the above trial balance was extracted. Telephone expenses are included in administrative expenses.

(3) The company paid £156,000 insurance premiums for the year 1 November 2011 to 30 October 2012. This amount is included in administrative expenses.

[For the full question please refer to the examination paper.]

Reading for this question

Subject guide Chapters 5 and 6.

Perks and Leiwy (2010) Chapter 17.

Approaching the question

The preparation of final accounts from structured information is a key learning outcome. A trial balance with several adjusting items has been the format for the compulsory question over recent years. In answering this type of question a methodical and organised approach is needed. It is very important that detailed, legible workings are given in order that marks are awarded for all work which is correct. If figures in the final accounts comprise a number of items marks will be awarded accordingly but without workings one error may result in several marks being lost. The workings may be shown on the face of the accounts or separately but candidates should try and help markers to award all appropriate marks by clear presentations. The 8-column accounting paper provided is particularly useful for presenting the financial statements. You should pay attention to the presentation of your answer taking care to use the appropriate descriptions of line items in the income statement and statement of financial position. The format of the Statement of Changes in Equity should follow best practice.

Part (b) of this question tests the ability to calculate and explain the dividends a shareholder will receive and how this relates to the information in the financial statements.

(a) Macbeth plc

i. Income statement for the year ended 31 March 2012

£000 £000Sales 124,900Cost of sales

Opening inventory

Purchases (94,160 – 106)

(4,852)

(94,054)(98,906)

Closing inventory 5,180(93,726)

Gross profit 31,174Dividends received 850

32,024ExpensesAdministrative expenses 16,141 + (2/3 15) – (7/12 156) (16,060)Distribution costs (9,060)Bad debts 75% 348 (261)Decrease in provision for doubtful debts [5% (9,930 – 348)] – 600 120.9Depreciation: Plant and equipment 20% 27,315

Motor vehicles 25% (5,720 – 1,670)

(5,463)

(1,012.5)(31,735.6)

AC1025 Principles of accounting

30

Profit before interest and tax 288.4Interest payable (615)Loss for the year before tax (326.6)Taxation (26.0)

352.6

ii. Macbeth plc

Statement of changes in equity for the year ended 31 March 2012

Equity share capital

Share premium

Retained earnings

Total

£000 £000 £000 £000Balance at 1 April 2011 19,000 14,677 33,677Issue of shares 1,000 500 1,500Loss for the year (352.6) (352.6)Dividends paid (5,800) (5,800)Balance at 31 March 2012 20,000 500 8,524.4 29,024.4

iii. Macbeth plc

Statement of financial position at 31 March 2012

ASSETS £000 £000 £000Non-current assets Cost Accum Deprn NBV Plant and equipment

Motor vehicles

27,315

5,720

11,923

2,682.5

15,392

3,037.533,035 14,605.5 18,429.5

Investments 15,00033,429.5

Current assets Inventory

Trade receivable (9,930 – 261)

Less: provision for doubtful debts

Prepayments

9,669

(479.1)

5,180

9,189.9

9114,460.9

Total assets 47,890.4

EQUITY & LIABILITIESEquity

Equity share capital

Share premium

Retained earnings

20,000

500

8,524.429,024.4

Non-current liabilities

67% loan notes 10,250

Current liabilities

Bank overdraft

Trade payables

Accruals

Corporation tax

456

8,120

10

308,616

Total equity and liabilities 47,890.4

Examiners’ commentaries 2012

31

(b) Information for Mrs Macduff

£• Dividends received in 31/3/12

2011 Final dividend (1000 4p)

2012 Interim dividend (1000 2p)

40

2060

• Dividend yield for 31/3/12

Interim (as above)

2012 Final (1000 5p)

20p

50p

70p

Yield 7 100 = 200

3.5%

Question 3

Falstaff plc’s statements of financial position for the years ended 31 December 2011 and 2010 are shown below:

Statements of financial position at 31 December

2011 2010£000 £000 £000 £000

Non-current assets Property Cost Accumulated depreciation

2,100 700

1,725 555

1,400 1,170 Fixtures and fittings Cost Accumulated depreciation

1,9001,060

1,493 840

840 6532,240 1,823

Current assets Inventory Accounts receivable

620 290

435 255

910 690Total assets £ 3,150 £ 2,513

Equity Ordinary share capital Share premium Accumulated profits

1,800250 282

1,500–

1872,332 1,687

Non-current liabilities 8% debentures 450

360

Current liabilities Bank Accounts payable Taxation

70248 50

222176 68

368 466Total equity and liabilities £ 3,150 £ 2,513

[For the full question, please refer to the examination paper.]

Reading for this question

Subject guide Chapter 6.

Perks and Leiwy (2010) Chapter 6.

AC1025 Principles of accounting

32

Approaching the question

This question requires an understanding of how specific items are shown in a cash flow statement (CFS) which is part of the learning outcome which refers to the preparation of financial statements from structured data. You should adopt a systematic approach which will enable you to extract the cash flows from the accruals-based income statement and statement of financial position. Good answers will be well presented, correctly describing the component cash flows with laid out workings.

Answers which prepare a full cash flow statement would be appropriately awarded but candidates are advised to produce only the answers required by the rubric of the question as the marks are allocated to the amount of time and effort required for such answers.

Part (a) tests candidates’ understanding of the difference between cash flows and accruals based accounting. Candidates should note that three examples are required.

(a) Income statement prepared according to accounting convention of accruals: The accruals concept means profit is the difference between income earned and expenses incurred – cash doesn’t have to be received or paid for time to be recorded.

The statement of cash flows shows actual movements of cash (monies passing through current or near-current bank accounts) as well as cash receipts and payments and shows whether more cash has come in than has gone out over the accounting period. Net cash flow reconciles opening and closing bank and cash balances.

Examples could include depreciation, receivables/prepayments and payables/accruals effect on profit, acquisition of non-current assets, share and loan movements.

(b) i. Interest paid = 8% [(360 9/12) + (450 3/12)] = £30,600. This is shown in the statement of cash flows as a separate line in operating activities.

ii. Loss on sale of non-current assets = 30 – (250 – 204) = £16,000. This is added back to profit before tax in reconciliation of this to cash flow from operating activities.

iii. Taxation paid = 68 + (90 – 50) = £108,000. This is shown in statement of cash flows as a separate line in operating activities.

iv Payments to acquire non-current assets = £1,032,000

Property = 2,100 – 1,725 = 375

F + F = 1,900 – (1,493 – 250) = 657

This is shown in statement of cash flows as a separate line in investing activities.

v. Increase in accounts receivable = 290 – 255 = £35,000. This is deducted from profit before tax in reconciliation of this to cash flow from operating activities.

vi. Dividends paid = Profit for year – difference between SoFP retained earnings

= 175 – (282 – 187)

= £80,000

This is shown in a statement of cash flows as a separate line in financing activities but could also be shown as part of operating cash flows.

Examiners’ commentaries 2012

33

Question 4

Duncan plc operates a mobile phone network for personal and business customers. The latest annual report has just been released on the company’s website. The annual report includes the following:

Duncan plc – Extract from the financial review for the year ended 31 December 2011.

Highlights for the year:

• A review of operating and administrative systems resulted in investment in non-current assets with a significant reduction in staffing levels.

• Growth has been offset by competitive pricing due to strong competition.

• Average revenue per personal customer per month (2011 = £10.56, 2010 = £11.20) has been affected by increased regulatory pressures on the pricing of mobile phone tariffs.

• Customers registered during 2011 have increased by 7% (2010: 3%).

• £10 million has been spent in 2011 on new advertising and sports sponsorship to boost brand awareness.

[For the full question please refer to the examination paper.]

Reading for this question

Subject guide Chapter 7

Perks and Leiwy (2010) Chapters 4, 5 and 7.

Approaching the question

The learning outcomes for Chapter 7 of the subject guide include the ability to analyse, interpret and communicate the information contained in financial statements. The most common analytical technique is often testing by a mini-case study of the type used in this question. It is important that answers go beyond simply stating that a particular ratio has gone up or down; the interpretation should use the contextual information given in the question and make links between different ratios. Good answers will draw conclusions from the ratios and the background information, which provide insight into the financial position and performance of the companies.

Excellent answers will use the analysis to draw appropriate conclusions which will be discussed from the perspectives of potential users.

You should carefully read the requirements of the question, which in this case, specify the number and nature of the ratios to be calculated. If you do not follow these instructions your work may not be marked.

There are no absolute answers to this type of question and you will be rewarded for a logical and informed analytical approach to the case study described in the question. The answer below illustrates such an approach, but for completeness provides more ratios than the question requires.

(a) 2010 2011Return on capital employed

(755 ÷ (4945 + 2050)) 100

(985 ÷ (5220 + 2080)) 100

10.8%

14.5%

Net profit margin

(755 ÷ 2610) 100

(1060 ÷ 2695) 100

28.9%

39.3%

Asset turnover

2610 ÷ 6995

2695 ÷ 7300

0.37 x

0.37 x

AC1025 Principles of accounting

34

Gross profit margin

(1115 ÷ 2610) 100

(1400 ÷ 2695) 100

42.7%

51.9%

Current ratio

(735 : 660)

(1095 : 910)

1.1 : 1

1.2 : 1

Quick ratio

((735 – 95) : 660)

((1095 – 15) : 910)

1.0 : 1

1.2 : 1

Gearing

(2050 ÷ 6995) 100

(2080 ÷ 7300) 100

29.3%28.5%

EPS

(445 ÷ 2660) 100

(590 ÷ 2670) 100

16.7p

22.1p

PE No.

200 ÷ 16.7

309 ÷ 22.1

12

14

(b) Commentary (summary of key points):

• ROCE – Improved return on capital employed

Increase due to improved margins with stable asset turnover

• Net profit margin

• Significant increase

• Staffing cost savings

• Even better if take out increased marketing costs

• Selling and distribution costs reduced

• Administrative costs are similar

• Asset turnover

• Remained constant

• Increase in volume of customers but fall in revenue per customer due to competitive pricing and regulatory pressures.

• Net asset increases but note PPE investment and fall in intangibles.

• Gross margin

• Significant increase

• See net margin for analysis

• Current ratio

• Constant at reasonable level

• Quick ratio

• Improvement in solvency/liquidity

• Large cash balance

• But higher payables

Examiners’ commentaries 2012

35

• EPS

• Significant improvement for reasons explained above.

• PE No.

• Market price indicates that investors are happy with the strategies adopted by the company (If the PE had remained at 12 price would now be £2.65 rather than £3.09).

Section CAnswer ONE question from this section, and ONE further question from either Section B or C

Question 5

Ophelia plc operates a chain of furniture stores and is considering its strategy on distribution and transport. The present position is that distribution is out-sourced to a transport company. The expected cost for the year ended 30 June 2013 is £250,000. This cost, it is projected, will rise by 10% per annum over the next five years.

The Directors of Ophelia plc are considering an alternative strategy of acquiring a company owned and managed transport fleet. The initial cost of the transport fleet on 1 July 2012 would be £750,000 and it is estimated that the fleet would be sold at the end of year 2017 for £150,000.

It is estimated that the following costs would be incurred over the next five years:

Drivers’ costsRepairs and

maintenanceOther costs

Year ended 30th June2013 33,000 8,000 230,0002014 35,000 13,000 235,0002015 36,000 15,000 240,0002016 38,000 16,000 236,0002017 40,000 18,000 242,000

The figure for ‘Other Costs’ includes depreciation on the fleet on the straight-line basis. The head office administration costs of Ophelia plc are expected to be £300,000 per annum and the running of the fleet would take up approximately 10% of the administrative time. However, the finance director believes that there is sufficient spare capacity in the head office to carry out the additional work.

[For the full question please refer to the examination paper.]

Reading for this question

Subject guide Chapter 12.

Perks and Leiwy (2010) Chapter 12.

Approaching the question

The application of capital investment techniques is an important element of the syllabus for this course and learning outcomes for Chapter 12 of the subject guide. The most effective approach is to construct a columnar table in which relevant cash flows can be inserted. It is important to give workings of all figures and to explain clearly treatment of all amounts, for example if a cost is to be treated as sunk and therefore not included as a relevant cost this should be stated. Having determined the net cash flow for each year, these are discounted using the discount factors taken from the tables provided. Thus a net present value can be arrived at and

AC1025 Principles of accounting

36

a decision recommended and justified. This type of question requires use of a significant amount of data and it is very important that your work is clearly presented and that all working are legible and understandable. The 8-column accounting paper can help in this respect. A suggested presentation of the answer is given below.

Part (c) gave good candidates an opportunity to show their understanding of the decision-making process and place this into a business context.

Part (d) required an understanding of Internal Rate of Return (IRR) and the problems in its application.

(a) Incremental cash flows – Transport Fleet Project2012 2013 2014 2015 2016 2017

£ £ £ £ £ £Out-source costs 250,000 275,000 302,500 332,750 366,025Drivers costs (33,000) (35,000) (36,000) (38,000) (40,000)Repairs and maintenance (8,000) (13,000 (15,000) (16,000) (18,000)Other costs (110,000) (115,000) (120,000) (116,000) (122,000)Fleet costs (750,000) 150,000Sub-contract income 50,000 50.000 50,000 50,000 50,000

_______ _______ ______ ______ _______ _______(750,000) 149,000 162,000 181,500 212,750 386,025

N.B. Ignore overheads

(b) i. Payback

Initial cost 750,000

Cumulative cash inflow

2013

2014 (+ 162,000)

2015 (+ 181,500)

2016 (+ 212,750)

2017 (+ 44,750)

149,000

311,000

492,500

705,250

75,000

Payback = 4 years 1.4 months.

ii. Net Present Value

CF. Discount Factor P.V.2012 (750,000) - (750,000)2013 149,000 0.893 133,0572014 162,000 0.797 129,1142015 181,500 0.721 129,2282016 212,750 0.636 135,3092017 386,025 0.567 218,876Net present value (4,416)

(c) Recommendation:

• Reject the transport fleet project

• Accept the alternative project.

Answers should explain the following:

• The project has a longer payback period than the alternative.

Examiners’ commentaries 2012

37

• The project has = negative NPV thus the project would reduce shareholder wealth. The alternative has a positive NPV at discount rate of 12%.

• Subject to reliability of assumptions.

• The project would give more control over future service and costs whereas outsourcing would not.

(d) IRR = the discount rate at which the NPV of the project is equal to zero. It is not appropriate for decisions involving mutually exclusive projects.

Workings

1. Other costs2013 2014 2015 2016 2017

Per Q 230,000 235,000 240,000 236,000 242,000

Depreciation

20% (750,000 – 150,000)

(120,000)

_______

(120,000)

_______

(120,000)

_______

(120,000)

_______

(120,000)

_______110,000 115,000 120,000 116,000 122,000

Question 6

Portia Ltd is a specialist manufacturer of components for luxury yachts. A contract has been offered to Portia by Nerrisa Supermarine plc for the supply over the next twelve months of 400 identical components, ZK44.

The data relating to the production of each component ZK44 is as follows:

Material requirements:3 kg material M1 – see note (i) below.2 kg material P2 – see note (ii) below1 part No. 678 – see note (iii) below.

Note (i) Material M1 is in continuous use by the company. 1,000 kg are currently held in stock at a book value of £4.70 per kg but it is known that future purchases will cost £5.50 per kg.

[For the full question please refer the examinatin question.]

Reading for this question

Subject guide Chapter 10.

Perks and Leiwy (2010) Chapters 14 and 15.

Approaching the question

Relevant and opportunity cost recognition are key techniques in short-term decision-making. This question tests candidates’ ability to apply these techniques. It is important in answering such questions that you keep in mind the basic contribution approach to the analysis and clearly distinguish between those costs and revenues that are relevant to the decision and those that are not. Good answers will set out the computations in a clear, logical and coherent manner.

Candidates should note that the question required a full explanation of the figures used in the analysis and marks were awarded as appropriate.

Part (b) requires candidates to place the calculations in the context of the wider business considerations by identifying three appropriate factors.

AC1025 Principles of accounting

38

(a) Contract for manufacture of ZK44.

Analysis of production and sale of 400 units to Nerissa Supermarine plc.

Notes £ £

Materials

M1 (1,200 kg at £5.50

P2 (800 kg at £2 per kg) (1)

Part no. 678 (400 at £50)

1

2

3

6,600

1,600

20,000 28,200

Labour:

Skilled (2,000 hours at £4 per hour)

Semi-skilled (2,000 hours at £3 per hour)

4

5

8,000

6,000 14,000

Overheads:

Variable (1,600 machine hours at £7 per hour)

Fixed: Incremental fixed costs

6 11,200

3,200

Total relevant cost 56,600

Contract price (400 components at £145 per component) 58,000

Contribution 1,400

The incremental revenues exceed the incremental costs. Therefore the contract should be accepted subject to the comments in (b) below.

Notes:

1. Material M1 – Opportunity cost is replacement cost.

2. Material P2:

If material P2 is not used on the contract it will be used as a substitute for material P4. Using P2 as a substitute for P4 results in a saving of £2 (£3.60 – £1.60) per kg. Therefore the relevant cost of P2 consists of the opportunity cost of £2 per kg.

3. Part No. 678 – actual impact cost

4. Skilled labour – opportunity cost is replacement labour cost.

5. Semi-skilled – cost of additional labour.

6. Overhead – variable overhead only is relevant. – additional fixed overhead is an incremental cost.

(b) Factors which should be considered are:

i. Can a price higher than £145 per component be negotiated? The contract only provides a contribution of £1,400 to general fixed costs. If the company generates insufficient contribution from its activities to cover general fixed costs then it will incur losses and will not be able to survive in the long tier. It is assumed that acceptance of the contract will not lead to the rejection of other profitable work.

ii. Will acceptance of the contract lead to repeat orders which are likely to provide a better contribution to general fixed costs?

iii. Acceptance of the contract will provide additional employment for 12 months and this might have a significant effect on the morale of the workforce.

iv. If there are few manufacturers, then acceptance of the contract may be necessary to build a client relationship.

Examiners’ commentaries 2012

39

v. Given market conditions, should Portia be looking at strategies for entering new markets?

Question 7

Cymbeline Ltd manufactures a single product. The company has two production departments, 1 and 2, and a service department. The following are the variable costs per product unit for April:

Direct materials £7.00

Direct labour £5.50

Manufacturing overhead £2.00

The selling price of the product is £36.00 per unit. Fixed manufacturing costs are budgeted to be £1,340,000 for April. Fixed selling costs are budgeted to be £875,000. Fixed manufacturing costs can be analysed between the departments as follows:

Production

1

£380,000

Production

2

£465,000

Service

Department

£265,000