examiner’s report on the chartered … examiners report oct 2014 old... · nigeria . october 2014...

TRANSCRIPT

EXAMINER’S REPORT

ON

THE CHARTERED INSTITUTE OF BANKERS OF NIGERIA

OCTOBER 2014 DIET EXAMINATION

(OLD SYLLABUS)

1

Table of Contents CERTIFICATE IN BANKING Business Communication Skills 3 Elements of Banking 15 Information Communication Technology 25 Introduction to Biz Finance 34 Introduction to Business Law & Ethics 48 Introduction to Financial Accounting 59 Principles of Economics 79 Principles of Management 86 Quantitative Techniques 95

FOUNDATION Basic Accounting 106 Economics 130 General Principles of Law 138 INTERMEDIATE

Elements of Banking 146 Financial Economics 156

Quantitative Techniques 169 PROFESSIONAL EXAMINATION I Financial & Management Accounting 180 Information Communication Technology 195 Management Theory & Practice 205 PROFESSIONAL EXAMINATION II International Trade 217

Law, Ethics and Corporate Governance 232 Marketing of Financial Services 245 Research Methodology 252

PROFESSIONAL EXAMINATION III

Bank Lending and Credit Administration 263 Corporate Finance 277 Practice of Banking 292 Strategic Management in Financial Services364 306

2

CERTIFICATE IN BANKING

BUSINESS COMMUNICATION SKILLS

3

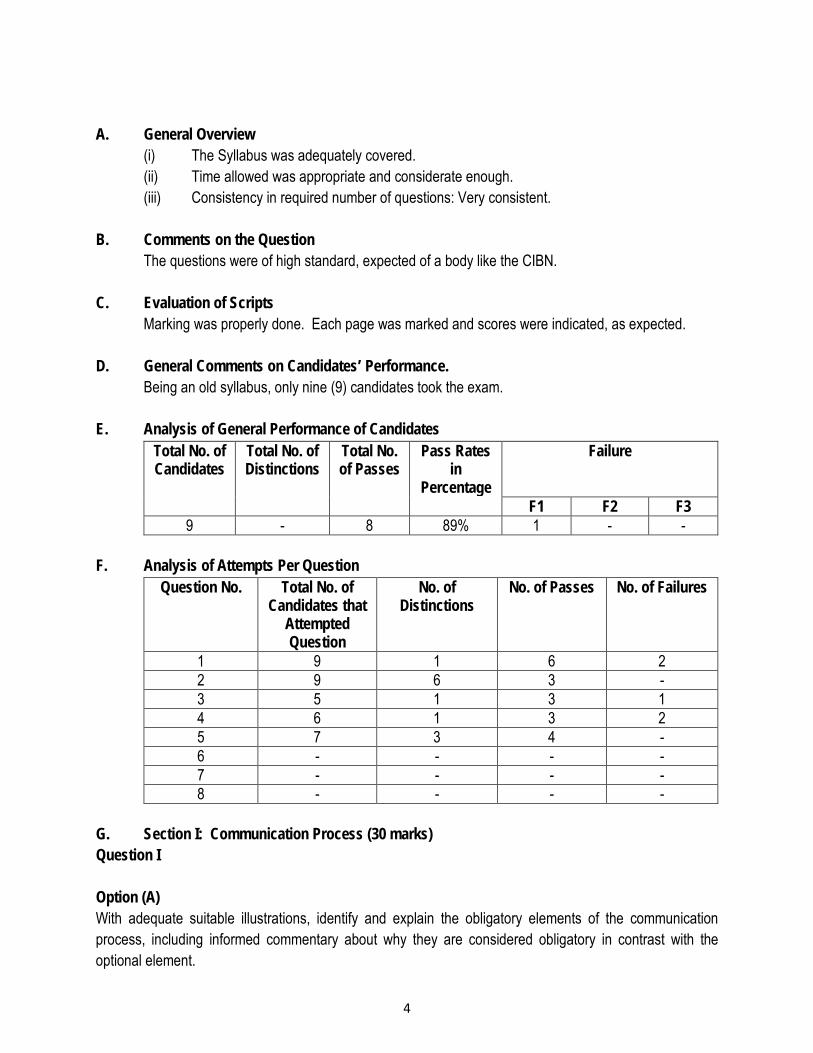

A. General Overview (i) The Syllabus was adequately covered. (ii) Time allowed was appropriate and considerate enough. (iii) Consistency in required number of questions: Very consistent. B. Comments on the Question

The questions were of high standard, expected of a body like the CIBN. C. Evaluation of Scripts

Marking was properly done. Each page was marked and scores were indicated, as expected. D. General Comments on Candidates’ Performance. Being an old syllabus, only nine (9) candidates took the exam. E. Analysis of General Performance of Candidates

Total No. of Candidates

Total No. of Distinctions

Total No. of Passes

Pass Rates in

Percentage

Failure

F1 F2 F3 9 - 8 89% 1 - -

F. Analysis of Attempts Per Question

Question No. Total No. of Candidates that

Attempted Question

No. of Distinctions

No. of Passes No. of Failures

1 9 1 6 2 2 9 6 3 - 3 5 1 3 1 4 6 1 3 2 5 7 3 4 - 6 - - - - 7 - - - - 8 - - - -

G. Section I: Communication Process (30 marks) Question I Option (A) With adequate suitable illustrations, identify and explain the obligatory elements of the communication process, including informed commentary about why they are considered obligatory in contrast with the optional element.

4

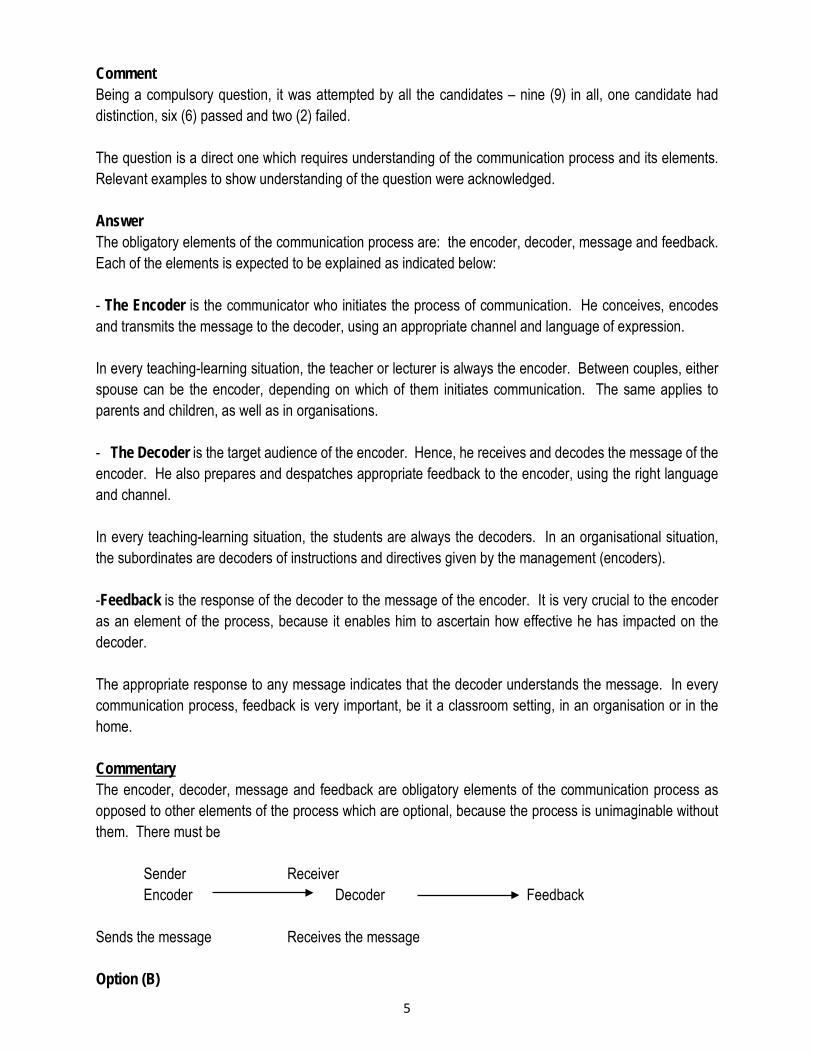

Comment Being a compulsory question, it was attempted by all the candidates – nine (9) in all, one candidate had distinction, six (6) passed and two (2) failed. The question is a direct one which requires understanding of the communication process and its elements. Relevant examples to show understanding of the question were acknowledged. Answer The obligatory elements of the communication process are: the encoder, decoder, message and feedback. Each of the elements is expected to be explained as indicated below: - The Encoder is the communicator who initiates the process of communication. He conceives, encodes and transmits the message to the decoder, using an appropriate channel and language of expression. In every teaching-learning situation, the teacher or lecturer is always the encoder. Between couples, either spouse can be the encoder, depending on which of them initiates communication. The same applies to parents and children, as well as in organisations. - The Decoder is the target audience of the encoder. Hence, he receives and decodes the message of the encoder. He also prepares and despatches appropriate feedback to the encoder, using the right language and channel. In every teaching-learning situation, the students are always the decoders. In an organisational situation, the subordinates are decoders of instructions and directives given by the management (encoders). -Feedback is the response of the decoder to the message of the encoder. It is very crucial to the encoder as an element of the process, because it enables him to ascertain how effective he has impacted on the decoder. The appropriate response to any message indicates that the decoder understands the message. In every communication process, feedback is very important, be it a classroom setting, in an organisation or in the home. Commentary The encoder, decoder, message and feedback are obligatory elements of the communication process as opposed to other elements of the process which are optional, because the process is unimaginable without them. There must be

Sender Receiver Encoder Decoder Feedback

Sends the message Receives the message Option (B)

5

“Feedback entails the reversal of roles in the communication process” with pertinent examples, justify this statement. Comment It is a straightforward question, that requires the application of what the candidate had learnt about communication as a process. Answer Candidates are expected to identify and explain what feedback is in the communication process. Mention that feedback can be positive or negative and identify what can be responsible for either a negative or positive feedback. Explain the importance of feedback as a crucial part of the communication process. Give examples to show feedback as an important element in effective communication.

(20 marks) Option (C) As the Head of your Unit, how can you use the English Language, being the official language, to promote organisational objectives through communication? Comment This is also a direct question, calling for a sound knowledge and understanding of operations of organisations with regard to objectives and effective communication in the workplace. Answer Organizational objectives can only be achieved through effective use of language, which should be courteous, relaxed and straight forward.

- Good communicators go the extra mile to become competent in English Language.

- This can be made possible by a gradual life-long learning process, though it takes time, patience, and hard work to master skills which result in enormous rewards and satisfaction. Thus, as the head of your unit, ensure that your language in all business communication is accurate for the following reasons: • To establish a relationship with the people you communicate with regularly. Unsuitable and

inaccurate language could destroy relationships.

- To communicate your ideas precisely, which may be affected by using unsuitable and inappropriate language, thereby making your meaning unclear to your recipients.

6

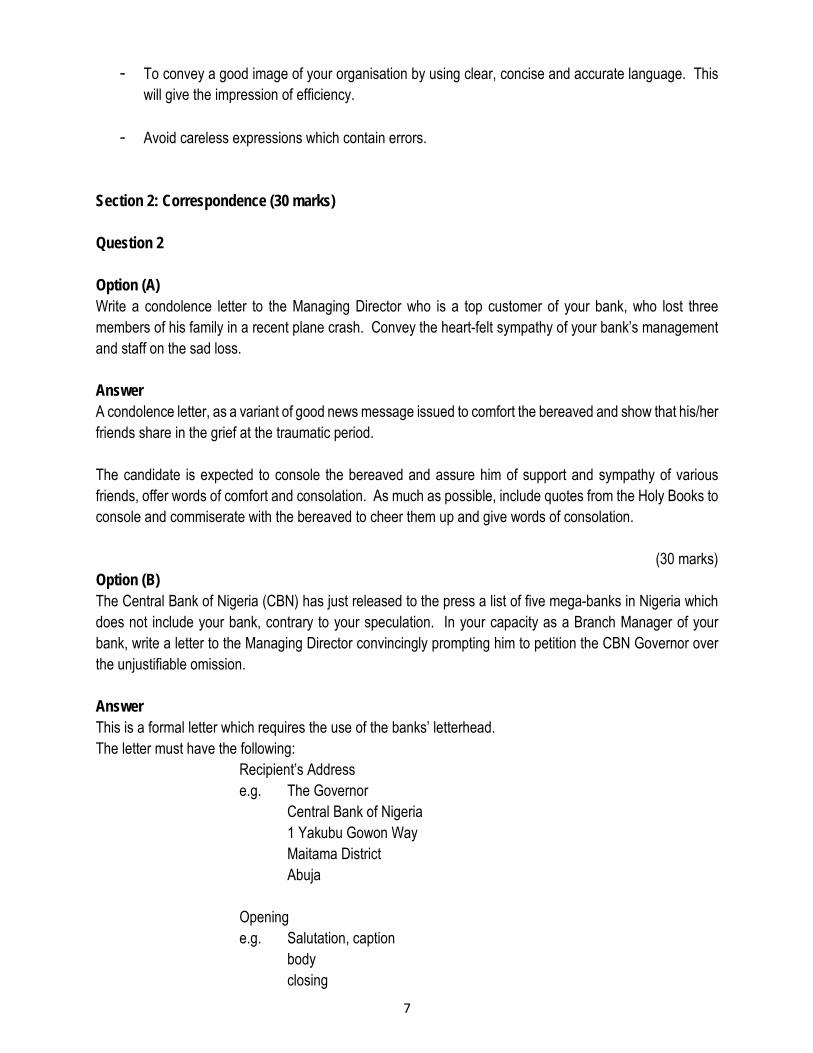

- To convey a good image of your organisation by using clear, concise and accurate language. This will give the impression of efficiency.

- Avoid careless expressions which contain errors.

Section 2: Correspondence (30 marks) Question 2 Option (A) Write a condolence letter to the Managing Director who is a top customer of your bank, who lost three members of his family in a recent plane crash. Convey the heart-felt sympathy of your bank’s management and staff on the sad loss. Answer A condolence letter, as a variant of good news message issued to comfort the bereaved and show that his/her friends share in the grief at the traumatic period. The candidate is expected to console the bereaved and assure him of support and sympathy of various friends, offer words of comfort and consolation. As much as possible, include quotes from the Holy Books to console and commiserate with the bereaved to cheer them up and give words of consolation.

(30 marks) Option (B) The Central Bank of Nigeria (CBN) has just released to the press a list of five mega-banks in Nigeria which does not include your bank, contrary to your speculation. In your capacity as a Branch Manager of your bank, write a letter to the Managing Director convincingly prompting him to petition the CBN Governor over the unjustifiable omission. Answer This is a formal letter which requires the use of the banks’ letterhead. The letter must have the following:

Recipient’s Address e.g. The Governor

Central Bank of Nigeria 1 Yakubu Gowon Way Maitama District Abuja Opening e.g. Salutation, caption

body closing

7

Content should include: 1. A suitable introductory paragraph on the purpose of the letter.

2. At least three convincing reasons why the managing director has to petition the CBN Governor. The

reasons must reflect clear-cut criteria for determining or categorising some banks as mega-banks which the writer’s bank has capacity to have met.

3. A summary of the business/image prospects of the writer’s bank should the proposed petition sail

through.

4. An appropriate concluding paragraph, Option (C) Question Several customers to your bank have recently approached you in your capacity as a branch manager raising issues about exorbitant bank charges in connection with interest on savings accounts, interest on short-term loan, withholding tax savings account, interest and commission on turnover. Taking a defensive posture on all the issues, write a letter to one of these your valuable customers, Godwin Alaba of Bona Ventures, 114 Herbert Macaulay Way, Yaba, Lagos classifying the issues in question to convince him to the effect that the charges should not be reviewed downwards contrary to his demand. Answer This is a formal letter, hence it should be written on the Bank’s letterhead. It must have the following features:

- Recipient’s Address just as we have in option (b).

- The body must comprise a suitable introductory paragraph which will spell out the purpose of the letter.

- At least two acceptable reasons to justify the identified bank charges on running cost analysis.

- A concise summary of customers’ benefits from corresponding bank services.

The candidate is expected to use appropriate words and grammatical errors (linguistic noise). The letter must be appropriately punctuated. Section 3: Interpersonal Communication (20 marks)

8

Question 3 Option (A) Non-verbal communication can complement verbal communication in any organisation. Enumerate the ways the following non-verbal forms can aid or distract effective communication in any organisation.

(i) Use of body language (ii) Dressing style (iii) Use of space (iv) Use of time (v) Vocal cues

Comment Five (5) of the nine(9) candidates, attempted this question. Answer The candidate is expected to: Explain what is meant by non-verbal communication and discuss ways it can complement or contradict verbal communication. List the use of the various non-verbal communication modes to complement or contradict verbal communication. Explain how body language can reinforce the spoken word (show sincerity, conviction) or contradict (show insincerity). Give relevant examples here. Dressing style can reinforce image conveyed of a personality spoken form or speak volumes of vain pursuits, can also cause distraction away from the speaker’s message to the personal characteristics by the speaker. - Space can communicate meaning in speaking and listening. Space can convey intimacy, etc.

- Time can convey how we manage our affairs, how we arrive early or late for appointments, prioritise our

telephone calls or manage our daily schedules.

(4 marks each x 5 = 20 marks) Option (B) Interpersonal communication can be oral or written. Relying on your knowledge of the oral form, explain how the following skills serve to enhance effective interpersonal communication, fluency, eloquence, stress and intonation, restatement. Answer

9

Fluency and eloquence enhance effective communication by attracting and helping to sustain the decoder’s interest. It is an indication of self-confidence anchored on the speaker’s mastery of the subject matter. Stress and intonation serve necessary emphatic purposes, and so help to send the message on the mind of the decoder for lasting affect and therefore prevent forgetfulness. Restatement helps to pragmatically draw the decoder’s attention to notable or salient messages for deserved prompt and effective feedback.

(Content - 12 marks) (Style - 8 marks)

(Total = 20 marks) Option (C) Explain how the listening skills help to promote understanding in interpersonal communication. Answer For understanding to take place in interpersonal communication, the receiver has to pay attention to get and understand what the sender says. Listening skill is not passive because the listener is a partner in the communication process. Good listening skill is borne out of training. In order to actively listen to another person, concentration, will power and great mental effort are required. Without discipline and full concentration, the listener’s attention will not be total. The right type of words and proper presentation will not allow the listener’s attention to wander to other issues. Again, understanding will be promoted when a conscious effort is made to check the points raised in the communication encounter to ensure that each has been understood. In most interpersonal encounters, there is the tendency that you as the listener are busy thinking of what reply to give as soon as the speaker stops, that you do not listen to understand the message/information. This will definitely affect understanding and the appropriate response to be given. To guard against passive listening, a conscious effort should be made to train oneself to concentrate and not be passive in a listening communication process. Listen only to the speaker with full attention. To enhance understanding, the listener is encouraged to take notes which would be brief, logical and easy to read thereafter.

(Content -12 marks) (Style – 8 marks)

(Total = 20 marks) Section 4: Public Speaking/Presentation (20 marks)

10

Question 4 Option (A) As the officer nominated to address the employees of your organisation on the urgent needs to guard against rumour mongering, present your speech with particular emphasis on the damaging consequences of rumour on the business prospects of the organisation. Answer Title: The Urgent Need To Guard Against Rumour Mongering – A speech presented at ABC Organisation/Company to all employees of the organisation/company to stem the spate of rumour mongering in the organisation/company. Highlight of the Content Introduction 1. What prompted the speech? Two or three instances of rumour mongering in the company along

with their consequences. 2. (a) What is rumour? (b) what is rumour mongering? (c) relevant – illustration 3. At least three causes of rumour mongering linked to the organisational culture along with their

solution. 4. Proposed disciplinary measures as a last resort against rumour mongers. 5. What the company stands to benefit if rumour mongering is drastically curtailed, if not eliminated. 6. Conclusion: Appeal for the employees’ co-operation.

(Layout = 3 marks) (Content = 8 marks)

(Total = 11 marks) Option (B) You have been invited to give a career talk to graduating students of Bells University on “Banking as a fulfilling career”. Prepare a speech of not more than 500 words for this purpose. Answer The essence of a good speech should be demonstrated as to what it takes to make a persuasive, convincing speech to arouse the audience -should show understanding of the peculiarities of the audience and tailor the message accordingly. The structure of a good speech. -good introduction -explain the subject matter extensively in the body of the speech. -summarise the speech effectively in the conclusion. Appropriate use of language and relevant examples and illustrations, facts, figures to support the evidence in the speech.

11

The conclusion should summarise concisely the theme of the speech. The length of the speech should be observed. Excess writing will attract sanctions.

(Layout - 3 marks) (Content - 8 marks)

(Style - 7 marks) (Accuracy - 2 marks)

(Total = 20 marks) Option (C) As a public speaker, what are the principles you will consider when presenting a speech to a group of undergraduates of Paramount University in taking up a career in Banking. Answer Title: Choosing Banking as a Career. The following principles should be followed in presenting this speech: 1. Introduction 2. Body of the Speech -Elucidate the functions of banking in the economy. -Highlight the prospects of the banking industry. 3. Conclusion

-Highlight the need to acquire a professional training by enrolling with the Chartered Institute of Bankers so thatyou will be recognised as a professional banker after writing their examination.

(Layout - 3 marks)

(Content - 8 marks) (Style - 7 marks)

(Accuracy - 2 marks) (Total = 20 marks)

Section 5 OrganisationalCommunication (20 marks) Question 5 Option (A) Explain the following impediments to effective organisational communication.Highlight their specific practical inhibitions. (i) Size of the organisation (ii) Network breakdown (iii) Status differences (iv) Conflict of interests (v) Poor listening and premature evaluation. Answer

12

i. Size of the Organisation:The bigger the organisational structure, the more transmission layers it has for messages and feedback and, therefore, the more likely they are to be distorted and/or delayed from arriving at their destination.

ii. Network Breakdown: This occurs to hinder effective organisational communication when, for instance, workers are too busy to remember to despatch necessary information or a message, or feedback is delayed.

iii. Status Differences: These occur to interrupt or disrupt upward or downward communication flow, and

so, render it ineffective.For instance, subordinates do not wish to express opinions which are at variance with those of their bosses. Again, the climate may be so poor as to hinder information flow totally. Climate, refers to respective attitudes of subordinates and superiors to one another, which may be positive or negative.

iv. Conflict of Interests: If the interests of various officers clash with one another on a given subject

matter.

(7 marks)

Option (B) Your organisation is set for an Annual General Meeting (AGM) scheduled to take place in the second week of September. Write a notice to this effect and include the Agenda to all the stakeholders. Answer The candidate is expected to write a notice of meeting, indicating the date, time and venue of the meeting. He is also expected to prepare the Agenda for the meeting. Agenda

- Opening Prayer - Welcome address by the chairman - Reading and adoption of the minutes of the previous meeting. - Matters arising from the minutes - Reading of correspondence, by the secretary - Business adjourned from last meeting - Financial matters (treasurer’s report, circulation of account, etc). - Reportsfrom Committees, Sub-committees and officers. - Election of new officers. - First motion moved and seconded. - Any other business (AOB) - Date of next meeting - Adjournment - Meeting declared closed by Chairman

13

(13 marks)

Option (C) What are the challenges of exchange of information flow among the units in the organisation at the same level? Answer The following are the challenges of exchange of information flow among the units in the organisation at the same level. Attitudes of heads of department

i. Failure of any unit to co-operate with the others will have a negative effect on the organisation’s functional procedures and effective communication in the department.

Not making information available to other units can also pose a challenge. Ineffective communication flow, hoarding of information. ii Demarcation line which exists between departments. For instance, the sales Dept and Accounts Dept operate at the same level with two heads of Departments. Not being open and coming with information that can help two units to function effectively can pose a serious challenge.

iii Distortion of information: This is because much information between departments is verbal with oral communication in particular.

iv Language problem is experienced because modern communication gadgets are completely in use in most organisations.

14

ELEMENTS OF BANKING

15

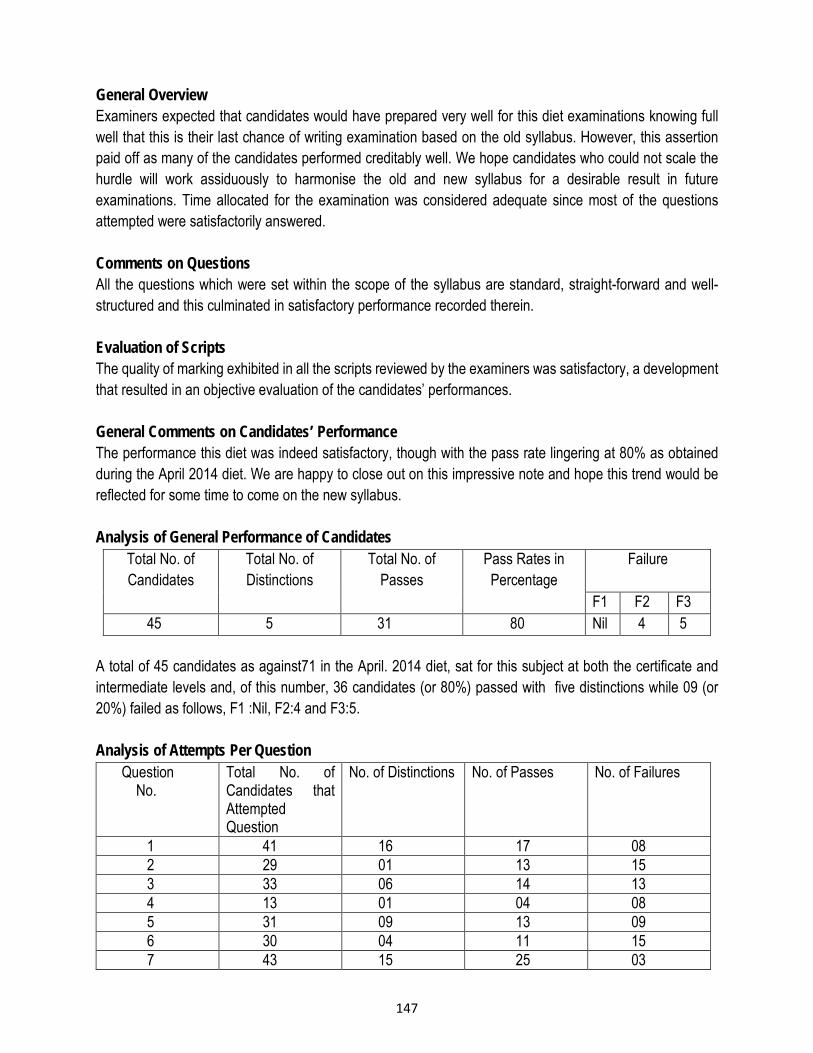

General Overview Examiners expected that candidates would have prepared very well for this diet examinations knowing full well that this is their last chance of writing examination based on the old syllabus. However, this assertion paid off as many of the candidates performed creditably well. We hope candidates who could not scale the hurdle will work assiduously to harmonise the old and new syllabus for a desirable result in future examinations. Time allocated for the examination was considered adequate since most of the questions attempted were satisfactorily answered. Comments on Questions All the questions which were set within the scope of the syllabus are standard, straight-forward and well-structured and this culminated in satisfactory performance recorded therein. Evaluation of Scripts The quality of marking exhibited in all the scripts reviewed by the examiners was satisfactory, a development that resulted in an objective evaluation of the candidates’ performances. General Comments on Candidates’ Performance The performance this diet was indeed satisfactory, though with the pass rate lingering at 80% as obtained during the April 2014 diet. We are happy to close out on this impressive note and hope this trend would be reflected for some time to come on the new syllabus. Analysis of General Performance of Candidates

Total No. of Candidates

Total No. of Distinctions

Total No. of Passes

Pass Rates in Percentage

Failure

F1 F2 F3 45 5 31 80 Nil 4 5

A total of 45 candidates as against71 in the April. 2014 diet, sat for this subject at both the certificate and intermediate levels and, of this number, 36 candidates (or 80%) passed with five distinctions while 09 (or 20%) failed as follows, F1 :Nil, F2:4 and F3:5. Analysis of Attempts Per Question

Question No.

Total No. of Candidates that Attempted Question

No. of Distinctions No. of Passes No. of Failures

1 41 16 17 08 2 29 01 13 15 3 33 06 14 13 4 13 01 04 08 5 31 09 13 09 6 30 04 11 15 7 43 15 25 03

QUESTION- BY- QUESTION ANALYSIS

16

Question 1 (a) List and discuss five types of money. (b) Is there any difference between near-money and pure money?

(20 marks) Comment This is a popular question and the end justified the means as most of those that attempted it appeared to have a full grasp of the question, more so when the topic has become a familiar terrain for candidates. This question was attempted by 41 (or 91%) of the candidates, out of which 33 (or 80%) passed. It ranked 2nd in popularity and in pass rate. Answer (a)(i) Commodity Money: This is money which has commodity value/content in relation to its value as money, i.e. it carries intrinsic value (e.g. gold and silver), but if the commodity content is higher than its value as money, it ceases to serve as money. (ii) Legal Tender: This type of money has the backing of the law of the country. Any commodity which a country’s law legislate as money is regarded as a legal tender. (iii) Token Money: This type of money has no commodity content. It is a money without intrinsic value. For example, Naira in Nigeria is worthless as a commodity but has value as money. The face value is greater than the value of the content used in printing it, i.e. the intrinsic value is less than the face value. (iv) Quasi/Near-Money: Near money is an asset that performs the function of store of value but does not adequately perform the function of medium of exchange. These are those financial instruments that needed to be converted before they can be generally accepted for the settlement of trade debts (v) Paper Money/Fiat Money: This is a pure token issued by each country’s central bank as fiduciary issue. It is a legal tender because it is enforced by law. (vi) Bank Deposits: These are deposits in current accounts/demand deposits. They are acceptable as a means of payment because people can draw cheques on their accounts to make payments. In other words, bank deposits are forms of money deposited with the bank which are equally withdrawn by cheques. They are an example of pure money. (The above list is not exhaustive through 3 marks each for any 5 points = 15 marks) | (Total = 20 marks) (b) Near Money and Pure Money The difference between pure money and near money is that pure money is in its spendable form and therefore enhances the exchange process unlike near money which is not generally acceptable for payment for goods and services. Pure money is easily transferable from one party to another and generally acceptable, unlike near money, e.g. Cheque. (5 marks) Question 2 (a). Explain what is meant by Development Bank. (b). What are the objectives of Bank of Agricultural Co-operative and Rural Development Bank. (BOA)?

(20 marks)

Comment

17

Although this question was fairly attempted by candidates, the overall result revealed that this part of the syllabus appears not to have received their reading attention. Therefore, candidates should note that it will do them a lot of good to dwell more on this section in order to acquire useful knowledge that could assist them in advising customers and clients alike. A total of 29 (or 64%) of the candidates answered the question, out of which 14 (or 48%) passed. Answer (a) A development bank is a specialised financial institution set up by the government to provide

medium- and long-term funds to accelerate the pace of development in the country. (4 marks)

(b) The objectives of Nigerian Agricultural Co-operative and Rural Development Bank are: (i) Acceptance of savings deposit from customers and the repayment of same with accrued interest

as and when due; (ii) Provision of opportunities for self-employment in the rural areas thereby reducing rural/urban

migration; (iii) Augmenting government efforts in the diversification of the productive base of the national

economy; (iv) Inculcating banking habits at the grass roots level of the Nigerian society;. (v) Provision of affordable credit facilities to less privileged Nigerians who cannot readily access the

services of conventional banks; (vi) Promotion of capacity building through the provision of relevant training and advisory service; (vii) Fostering an accelerated growth and development of the agricultural sector and rural economy; (viii) Encouraging the formation of co-operative societies at all levels.

(2 marks each 2 x 8 = 16 marks) (Total = 20 marks)

Question 3

(a) The Securities and Exchange Commission is the apex institution in the capital market. Briefly explain its related functions.

(b) List the membership of the Securities and Exchange Commission (SEC). (20 marks)

Comment Knowledge of the capital market structure and operations as well as its usefulness for economic development is very vital for students of banking. Candidates who attempted this question displayed reasonable understanding of the topic and were able to record good pass mark. A total of 33 |(or 73%) of the candidates attempted the question, out of which 20 (or 61%) passed. Answer (a) Functions of Securities and Exchange Commission (SEC)

(i) Determining the amount and time at which securities of companies are to be sold to the public either through offer for sale or subscription;

(ii) Registering all securities proposed to be offered privately;

18

(iii) Maintaining surveillance over the securities market (including the securities exchange) in order to ensure orderly, fair and equitable dealings in securities and to forestall illegal dealings by privileged insiders at the expense of innocent and often ignorant investors;

(iv) Protecting the integrity of the securities market against any abuses arising from the practice of insider trading;

(v) Acting as the apex regulatory organisation for the Nigerian Stock Exchange and its branches to which it is at liberty to delegate powers;

(vi) Creating the necessary atmosphere for the orderly growth and development of the capital market through enlightenment programmes such as seminars, workshops, symposia, publications and stimulation of ideas;

(vii) Determining the bases of allotment of securities in a public offering to ensure a wider spread of share ownership;

(viii) Determine when issuing houses or registrars should return surplus application monies and the penalty payable for non-compliance;

(ix) Auditing the books of companies and institutions involved directly or indirectly in the securities business;

(x) Determining the contents of the prospective and other issuing memoranda. (xi) Ensuring that banks raise money only by public offer. (xii) Registering the following:

- Stock exchanges and their branches. - Persons/institutions involved in securities dealing (e.g. stockbrokers, - registrars, issuing houses and fund managers). - Securities to be traded or being traded (share debentures, government stock). (1.5 marks each for any 10 points =15 marks)

(b) Membership of SEC (i) A representative of Central Bank as chairperson. (ii) One representative of the Nigerian Stock Exchange (iii) One representative of the Nigerian Enterprises. (iv) One representative each from (v) Federal ministry of Finance.

• Federal Ministry of Trade and Tourism; • Federal Ministry of Industries; • The Executive Directors of Commission;

(vi) Five (5) private members appointed by the Federal Government who hold office for 5 years and are eligible for reappointment.

(1 mark each for any 5 points = 5 marks) (Total = 20 marks) Question 4 Explain the following in the context of international banking.

(a) London Club of Creditors; (b) Eurobond; (c) Special Drawing Rights (SDRs); (d) West African Bankers’ Association (WABA). (20 marks)

19

Comment The world is now a global financial village and this position buttresses the need to acquire knowledge on in international banking. Very few candidates attempted this question and, even at that, they did not do well enough. Only 13 candidates (representing 29%) attempted the question but just 5 of them (or 38%) pass. Answer (a) London Club of Creditors

This is a cartel of international commercial banks which handles private debts and other commercial debts and operates strictly on commercial terms. They are thus stricter in terms than Paris Club of Creditors. The London Club debts are largely private trade debts and have two components viz (i) Promissory Notes. (ii) Brady par bond collateralised with US Treasury Bonds.

(5 marks) (b) Eurobond

-Eurobond is a method of raising long-term fund in the international capital market outside the country in whose currency the bonds are denominated. -They are issued directly by the borrower in bearer form. -The interest payment is not subject to withholding taxs. -There is secondary market and the currency control is convertible. -Bonds are usually issued as US Dollar, Swiss Franc, Pound Sterling and Euro. -Cost of issue is low, easy to arrange and simple. -It attracts higher rates (yields). (5 marks)

(c) Special Drawing Rights (SDRs) Special drawing rights is an unconditional additional international reserve asset.

introduced by the International Monetary Fund (IMF) to ease the problem of international liquidity. It is mere bookkeeping entry. SDRs are allotted to member nations of the IMF in proportion to their quotas with the fund. Member countries can use gold or scarce currencies to settle their debts when faced with balance of payments difficulties. (5 marks)

(d) West African Bankers Association (WABA)

The West African Bankers’ Association is the association of commercial and merchantbanks in West Africa. The decision to establish this association was reached in Bamako, Mali in 1978 while its draft constitution was ratified at a meeting of bankers held in Freetown, Sierra-Leone. (5 marks) (Total = 20 marks)

Question 5 Not all securities offered by customers are acceptable to banks. Mention and discuss the main types of securities acceptable to a lending banker. (20 marks)

20

Comment The examiners could observe the willingness on the part of the candidates to answer this question on security but they lack the depth and ability to explain the points and highlight the issues required. A total of 31 (or 69%) of the candidates answered the question and 22 (or 71%) passed. Answer Acceptable securities to a lending banker are as follows :

(i) Land and landed property that are free from encumbrances as legal or equitable mortgages. (3 marks)

(ii) Stocks and shares of first-class companies usually known as blue chips. Simple deposit of share certificates may be accepted, but deposit coupled with undated but signed transfer forms are preferable. However, the charge should be registered or noted with the CSCS. (4 marks)

(iii) Life Policies – with adequate or substantial surrender values are also acceptable. Preferred life policies are those of insurance companies whose integrity is unimpeachable. (3 marks)

(iv) Guarantee of reliable and responsible individuals or third parties is usually accepted by banks. This is provided that the guaranteed is worth more than the amount being guarantee. It is normal to take status inquiry on an intending guarantor to establish his worth and perhaps level of responsibility. (3 marks)

(v) Debentures- Banks often use company debentures (floating or fixed) as security. The assets of the company are executed in favour of the bank, subject to certain conditions. (3 marks)

(vi) Domiciliation of contract proceeds; Proceeds from specified contracts may be domiciled with a lending banker as security for intended borrowing. When the contract is performed, the underlying proceeds are paid through the bank in which it was domiciled into of the contractor’s account. (4 marks) (Total = 20 marks)

Question 6 Mention and explain the various methods of effecting international payments. (20 marks) Comment This question was set to test candidates’ understanding of the operational and payment methods in international trade. However, many of the candidates resorted to guesswork and by implication did not accord the topic the attention it requires thus leading to an average performance in the question.A total of 30 (or 67% of the candidates attempted the question and only 15 (or 50%) passed.

21

Answer Methods of Payment in International Trade

(i) Open Account: This is where an exporter sells his goods on credit and obtains payment at later date depending on the agreement. The exporter may face the problem of non-payment. (2 marks)

(ii) Payment in Advance: In this case, the exporter receives advance payment before the actual shipment of the goods or delay shipment. It is a more secure method of obtaining payment. (2 marks)

(iii) Bills for Collection: The bank is involved in this. It is the process whereby an agreement is

reached between the exporter and the importer that uniform rules for collection (URC) is applicable. The exporter will give instruction to his bank on how it should handle his documents in obtaining payments either against documents, against payments’ acceptance or negotiation. The collection is accompanied by commercial documents either with or without payments. (2 marks)

(iv) Documentary Letter of Credit: This is the most acceptable mode of payment in international trade. Under this method, the importer approaches his banker to open a letter of credit in favour of the exporter together with the list of all the conditions fulfilled. The documents include bills of lading, commercial papers, certificate of origin and insurance certificate. Documentary letters of credit may be revocable or irrevocable. (2 marks)

(v) Foreign Currencies : Commercial banks provide foreign exchange to ease travelers undertaking international transactions, e.g. Euro’s, Pounds Sterling and Dollars (2 marks)

(vi) Travellers’ Cheque: This is a cheque issued to a customer going on a foreign mission such as business, education, religion or holiday. It is denominated in the currencies of countries of destination and subject to a maximum amount stipulated by the government and the CBN annual credit guidelines.

(2 marks)

(vii) Basic Travelling Allowance (BTA): This differs, depending on the type of trip or mission. The cheque enjoys automatic recognition and is honoured once it is presented for payment in the designated foreign currency (2 marks)

(viii) Foreign Draft.: A customer may request his bank to issue a foreign draft in his name or in the exporters’ name payable at a designated bank overseas.

(2 marks)

(ix) SWIFT: (Society for World- Wide Interbank Financial Telecommunication) has members world-wide with headquarters in Brussels. Members are requested to contribute to a pool of funds

22

maintained for the development and maintenance of their central communication to which they link their own local system for urgent transactions and receipt of messages for interbank financial settlements. (2 marks)

(x) Telegraphic Transfer or Cable Payment Order. This is a transfer of fund by cable. It is more expensive but faster than mail transfer. It is usually authenticated by tested code or test keys. But the invention of SWIFT has reduced the usage of this method of payment. (2 marks) (Total = 20 marks)

Question 7 Banking in the 21st Century has been made easy through e-banking.

(a) Enumerate numerous benefits of e-banking in Nigeria (10 marks) (b) State clearly problems associated with e-banking in Nigeria. (10 marks)

Comment The examiner is happy to observe that candidates are now abreast with current innovative developments in the banking and financial environment in Nigeria, especially as it affects the pool of investments by deposit money banks towards the acquisition and deployment of modern technologies in the industry. It is therefore heartwarming to note that most of the candidates that attempted the question passed with good grades. A total of 43 (or 96%) of the candidates attempted the question and 40 (or 93%) passed.

Answer (a)The Benefits of E-Banking in Nigeria

(i) Increase in business patronage without corresponding increase in branches. (ii) Improvement in service delivery resulting from interactive facilities of e-banking system. (iii) E-banking phenomenon will not decrease the total workforce in the industry, however, more

computer-literate and educated staff will take preference over existing labour mix. (iv) It could be argued that with growth in banking culture, more people will be recruited by the various

financial institutions, without necessarily increasing branch network. (v) It will eliminate the endemic long queues at bank counters. (vi) Through online services, customers can withdraw funds or make deposits easily at any branch

office of the bank (vii) Accessing information on one’s account at the bank is made easier and quicker. (viii) The risk of carrying large sumsof money in cash on trips has drastically reduced because of

electronic transfer facilities. (ix) The temptation to store large sums of cash in the office or at home is also reduced since people

will not wait long to cash their cheques at the bank. (x) Bank statements of account come out quicker and readily these days.

(1 mark each for any point = 10 marks)

23

(b) Problems Associated with E-Banking in Nigeria (i) Poor telecommunication system. (ii) Unstable but expensive power supply. (iii) High cost of acquiring/ installation of information technology hardware. (iv) Dearth of skilled personnel. (v) High maintenance cost of technology equipment. (vi) Security implications of some of the equipment. (vii) Application limited to institutional clients as the private clients lack access to equipment for

interface with e-banking system. (viii) Lack of confidence among private clients. (ix) Increased computer fraud resulting from introduction of e-banking. (x) High cost of operations sometimes passed to the customers.

(1 mark each for any point = 10 marks) (Total =20 marks)

24

INFORMATION COMMUNICATION TECHNOLOGY

25

A. General Overview The questions covered the syllabus and were adequate for the level. A time of three hours was allowed to attempt five out of seven questions. The instructions were clear and in simple language.

B. Comments on the Questions The questions were in line with the structure as stated in the syllabus to attempt 5 out of 7 questions. The production of the question paper was clean and clear.

C. Evaluation of Scripts The standard of the marking was very good with consistency and accuracy. Marks were awarded based on points enumerated by candidates (i.e. no arbitrary award of marks).

D. General Comments on Candidates Performance The general performance was in the same range with that of the April diet examination. The overall pass rate of 65% was achieved.

E. Analysis of General Performance of Candidates Total No. of Candidates

Total No. of Distinctions

Total No. of Passes

Pass Rate Percentage

Failure F1 F2 F3

20 0 13 65 0 5 2

F. Analysis of Attempts for Question Question No.

Total No. of Candidates that Attempted Question

No. of Passes No. of failures

1 6 0 6 2 20 17 3 3 20 16 4 4 18 11 7 5 12 1 11 6 18 4 14 7 3 1 2

G. Examination Questions, Comments and Suggested Answers

Question 1 Give a brief explanation which would be suitable for a manager of the following telecommunication terms: a) PABX b) Protocol c) PSS d) Band Rate e) Modem (20 marks) Comment

26

This was the least attempted question. All the six (6) candidates that attempted it failed. It was clear that the candidates did not study the aspect of the syllabus that deals with telecommunication terms as stated in the question above. The question in 1(d) ought to read “baud” rate instead of band rate. Candidates who are familiar with the term got it right as one can only talk about band width but not rate. Answer (a). PABX—Private Automatic Branch Exchange (PABX systems) provide facilities for office switch-

boards and telephone systems. It can offer facilities such as automatic message switching automatic dialling, conference calls or when a line is engaged (call repeating). (4 marks)

(b). Protocols-- is the instruction used in a packet switching system. It divides a message into packet, gives each packet control data which identifies the sender and the destination address and transmits the packet along the network. (4 marks)

(c) PSS – Packet Switching System allows a number of computers to transmit data to one another in a more economical way than dedicated private lines. The data message in a PSS is divided up into packets which includes the identification of the sender and the address of its destination.

(d). Baud rate – means bit per second transmitted. Data is usually transmitted by means of bit serial transmission where the bits that make up a character are sent down the line in turn.

(e). Modem-- is a device which converts data digital form used (by a computer) into waveform ( as used by telephone lines) and vice-versa. For data transmission through the telephone line to be possible, the data has to be passed through a modem between a telephone line and the computer. There must a be modem at each end before the data set to computer and after before it gets to telephone lines.

Question 2 (a) State four (4) broad aims of an effective and efficient Payment System.

(8 marks) (b )Give four (4) factors that are responsible for the challenges in the Nigerian Payment System. (8 marks) (c) List four (4) examples of Electronic Money. (4 marks)

(Total = 20 marks) Comment This is the most attempted question, with all the 20 candidates taking a short at it. A pass rate of 85% was achieved. Majority of the candidates demonstrated a good understanding of the aims, and challenges of an effective and efficient payment system in Nigeria. Candidates also named examples of e-money. Answer (a). Aims of an effective and efficient payment system in Nigeria are:

i. To eliminate delays in settlement; ii. To reduce transaction costs;

27

iii. To minimise the volume of cash transaction in the economy; iv. To ensure convenience and facilitate greater volume of economic activities and hence productivity.

(2 marks per point = 2 x 4 = 8 marks) (b). Factors responsible for observed deficiencies are:

i. Inadequate infrastructure; ii. Human capacity limitation; iii. Distrust (lack of confidence) among the people; iv. Socio-cultural attitudes ; v. Financial illiteracy.

(2 marks for any 4 point = 2 x 4 = 8 marks) (c) Examples of e-money are i. Smart card / value card ii. Credit cards iii. Debit cards iv. SWIFT v. ATM

(1 mark per point = 1 x 4 = 4 marks) Question 3 (a) Explain four (4) main classes of computers with details of the environment of usage and their

components. (12 marks) (b) Mention four (4) modern secondary storage devices. (4 marks) (c) State four (4) computer input technologies. (4 marks)

(Total = 20 marks) Comment This question was attempted by all the 20 candidates with a pass rate of 80%. Candidates showed a good understanding of the concept of main classes of computers with the details of the environment of usage and their components. Also, majority of the candidates were able to mention the modern storage devices and computer input technologies. Answer (a). The 4 main classes of computers are:

i. Microcomputer: A microcomputer is any computer that is built around a microprocessor. A Microprocessor is the information control centre that processes and transfers information stored in the memory. (3 marks) ii. Mini computers are the least costly and most widely used computers. Minicomputers lie between microcomputers and mainframes in cost, speed and computing power. They can perform many tasks concurrently.

iii. Main frame computers are the large-scale computers found in the computer rooms of most large businesses, financial institutions and universities. (3 marks)

28

iv. Super computers are the most powerful and expensive computers of all. Super computers are useful for scientific and engineering calculations, weather forecast, cryptography and computer animation. (3 marks) (a) The 4 modern secondary storage devices are:

(a) Data card; (b) Flash drive; (c) Compact disc; (d) Optical disk drives; (e) Bluetooth.

(1 mark each for any 4 points = 4 marks) (b) Modern computer input technologies are:

i. Mouse; ii. Keyboard; iii. Touch screen; iv. Optical scanner; v. Voice recognition; vi. MICR- Magnetic Ink Character Recognition; vii. OCR- Optical Character Recognition.

(1 mark each for any 4 points = 4 marks) Question 4 (a) Differentiate between the terms - Application Package and General Purposes Package. Give an example of each. (14 marks) (b) Give three (3) advantages of each of the above packages (6 marks)

(Total = 20 marks) Comment Eighteen (18) candidates attempted the question with a pass rate of 61%. The candidates that did not perform well could not differentiate between an application package and a general purposes package, let alone give an example of each. They also failed to identify the advantages of each of the packages. Answer Application package is a ready-made program written to perform a particular job. The job will be common to many. A potential package could be adopted by all of them for their data processing operation. It is a complete system for a particular application supplied by some outside body for general use by individual firms. An application package is always fully documented with specifications of input, output formats and data layout ,user instruction manuals, hardware requirement and details of how the package can be used to suit the users’ needs. An example is word processors. A general purpose package is more general in application. The program can perform a specific function like spreadsheet or modeling, but it is up to the customer to use it for stock, payroll. An example is Corel draw

29

(b) Advantages of application package are: (i) The provisions of expertise are normally availableto the smaller user. (ii) Reduction in systems and programming efforts and cost. (iii) Reduction in time needed for implementation. (iv) Reduction in errors in design: the program should be well tested before usage.

(1 mark each for any 3 points = 3 marks) The advantages of general packages are:

i. They save time, in that programs do not have to be written specially or procedure carried out manually.

ii. They can be used for a variety of applications. iii. Parameters and data input can be changed or flexed to compare different results. iv. The packages are easy to use and require no great computer knowledge.

(1 mark each for any 3 points = 3 marks) Question 5 (a) Information Systems carry out three (3) general activities. State the activities. (1 mark) (b) Explain how the activities are carried out. (3 marks) (c) List four (4) types of Information System (4 marks) (d) Discuss three (3) of the information system types listed in (c) above showing clearly their differences. (12 marks)

(Total = 20 marks) Comment Twelve (12) out of the twenty (20) candidates attempted the question. The performance was very poor with a pass rate of 8%. The candidates did not understand the concept of information systems. Majority of them could not list the types of information system and the general activities involved in any information system. This is a basic requirement to understand the concept being tested here. Answer (a). The 3 activities are those of input, process and output. (b). It accepts input data from various sources within or without into the system.

i. Next, the inputted data is acted upon using a given procedure. This is called the processing stage to give the desired output.

ii. Finally, the result of processing is given out as information via output units as soft or hard output as desired.

(1 mark each = 1 x 3 = 3 marks) (c)(i) Transaction processing system, otherwise called Operation Information System. (OIS)

(ii) Management Information System (MIS); (iii) Decision Support System (DSS); (iv)Executive Information System (EIS); (v). Expert System; (vi)Office Automation System (work group, support system.).

(1 mark each for any 4 points. = 4 marks)

30

(d)(i) Basically, an Operational Information System (OIS) collects and stores data about business events (transactions) and something that controls the decision-making part of a transaction. A transaction which could be sales, purchase, supplies, etc .generates or modifies, data stored in the information system. The two main types OIS are batch processing and real-time processing. Examples are Point –Of- Sale system for sales, transactions, processing or credit card payments, etc OIS improves transaction processing. (4 marks)

(ii). Management Information System (MIS). This is a system that provides managers of organisations at all levels and all functions with appropriate information from relevant sources to enable them take timely and effective decisions for planning, directing, co-ordinating and controlling the activities for which they are responsible. MIS evolved from efforts made to provide answers to the shortcoming of OIS which improve transaction processing but no information for management.

(4 marks) (iii). Decision Support System (DSS):This is an information system that assists managers with unique

forms of non-recurring strategic decisions that are relatively instructed. It performs “what if“ and reports generated tasks as well as suggests alternatives that would prove most advantageous given a set of alternatives. It has the decision-making ability based on defined objectives. It serves as a supporting material for MIS.

(4 marks) (iv). Executive Support System (ESS): This is an information system that helps managers and executives

by providing them with flexible access to information for monitoring the operating results and general business conditions. It also helps in making unstructured decisions through advanced graphics and communication.

(4 marks) (v). Expert System (ES): This is a knowledge intensive program that solves problems by capturing the

expertise of a human in a limited domain of knowledge and experience. It helps in solving problems which require an expert knowledge of the process of performing specific tasks. Expert systems use computer programs that store facts and rules in what are called knowledge bases to mimic the decision process of the human expert. They are referred to as intelligent systems because of the infusion of knowledge and decision-making characteristics with computer processing power.

(4 marks) (vi). Office Automation System (OAS): This is an application that facilitates everyday communication and

information processing tasks in offices and business organisations just to improve the productivity of workers in the offices. It encompasses a wide range of tasks that include word processing, spreadsheet application and telephone systems.

(4 marks Question 6

a) List four (4) levels at which computer crimes are committed. (4 marks) b) How are the listed crimes committed and who are the criminals? (8 marks) c) Effects of virus attack can be disastrous to the system. List four of such effects.

(4 marks) d) State four (4) ways by which you can logically protect the system in your organisation.

(4 marks) (Total = 20 marks)

31

Comment The performance in this question was very poor as only 4 out of the 18 candidates that attempted the question managed to have a pass mark. The pass rate was 22%. The question was on levels at which computer crimes are committed. It also deals on how they are committed and on identifying the criminals. Very few candidates gave the effect of virus attack on the system while many listed how the system could be logically protected. Performance could have been improved if candidates paid particular attention to computer crimes, their effects and safeguards. Answer

a. At input, output, software development and data transmission levels. (1 mark each = 4 marks)

b. (i). At the input level, the computer operator commits the crime here. It involves feeding the computer with wrong data which would lead to wrong information in the output.

(2 marks) (ii). At output level, the result from the computer could be sold to competitors by any member of staff that has access to it.

(2 marks) (iii). At software level, the programmer can add a fictitious code to move a certain amount of money from one account to another. Most crimes occur at this level. (iv).At the data transmission level, the issue of networking and the Internet has exposed the firm to outsiders. Hackers can gain access into firms from any external location to perpetrate fraud.

(2 marks) c. (i). Wreckage of IT equipment;

(ii). Clogging up of e-mail computer server; (iii). Significant data loss from hard disk; (iv). Erasure of the content of the CMOS which will affect the date, time and other details that the

computer needs to boot; (v). Automatic mailing of a copy of the virus to all the e-mail addresses.

(1 mark for each point – 1 x 4 = 4 marks)

d. (i) By providing password for authorized users. (ii) By encrypting data

(iii) By regularly providing regular and full computing resources. (iv) By providing a system to monitor the ex-activities of all login users. (v). By introduction of a mechanism that will trigger when more than two attempts are made by

a user at login time. (1 mark each for any 4 points = 4 marks)

Question 7 When buying a printer for a small business computer, a layman sometimes takes a bewildering range of choices.

a) Explain the difference between Parallel and Serial Printers. (16 marks)

32

b) Briefly describe the following types of printer mechanisms and explain when they would be the preferred choice

i. Daisy Wheel. ii. Dot Matrix. (4 marks)

(Total = 20 marks) Comment This is the least attempted question with only three (3) candidates. One (1) out of whom showed a good understanding of the mechanism of printers but failed to differentiate between parallel and serial printers. Answer

a. i. A serial printer allows signals to pass serially from the computer to the printer. If the computer output is in a form different from that expected by the printer, an interface card can be provided to convert the data to the required form. The common serial interface is RS232 or RS423.

(3 marks) ii. A parallel printer can deal with signals in parallel as they are normally passed around inside the computer. The most common parallel interfaces are IEEE-488 and centronic (3 marks)

b(i) Daisy wheel printer: is quite widely used in microcomputer systems. A metal or plastic print wheel is

used which may be changed to alter character styles and can normally print 96 different characters. The characters arranged in the wheel circumference on spokes, strike the paper through a carbon ribbons and bold lettering is achieved by a slightly off set second strike. Printing speeds vary from 15 to 55 characters per second. Although the speed is slow, it is primarily used where print quality is more important than speed.

(7 marks) (ii) Dot matrix printer: This is the most commonly used printer in the microcomputer system. A set of

small pins is arranged in a vertical matrix. The matrix moves along the line of paper to print each character which is individually shaped by selected pins being pressed into the paper through an inked ribbon. The main advantages are: there is greater speed of printing up to 400 characters per second, and the character styles are wider with software control allowing a greater variety of character styles. The disadvantage of dot matrix printer is that print quality is not as high as with the impact printer. It is used where volume of report to be printed is high and speed is important.

(7 marks)

33

INTRODUCTION TO BUSINESS FINANCE

34

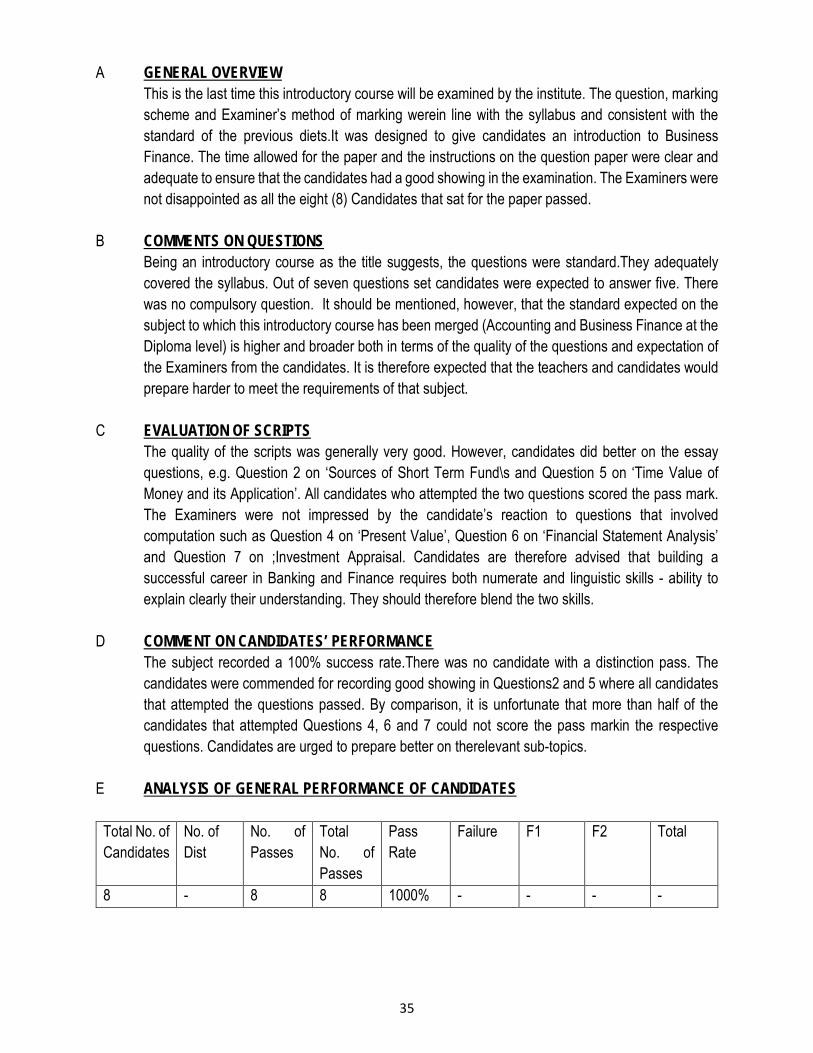

A GENERAL OVERVIEW This is the last time this introductory course will be examined by the institute. The question, marking scheme and Examiner’s method of marking werein line with the syllabus and consistent with the standard of the previous diets.It was designed to give candidates an introduction to Business Finance. The time allowed for the paper and the instructions on the question paper were clear and adequate to ensure that the candidates had a good showing in the examination. The Examiners were not disappointed as all the eight (8) Candidates that sat for the paper passed.

B COMMENTS ON QUESTIONS

Being an introductory course as the title suggests, the questions were standard.They adequately covered the syllabus. Out of seven questions set candidates were expected to answer five. There was no compulsory question. It should be mentioned, however, that the standard expected on the subject to which this introductory course has been merged (Accounting and Business Finance at the Diploma level) is higher and broader both in terms of the quality of the questions and expectation of the Examiners from the candidates. It is therefore expected that the teachers and candidates would prepare harder to meet the requirements of that subject.

C EVALUATION OF SCRIPTS

The quality of the scripts was generally very good. However, candidates did better on the essay questions, e.g. Question 2 on ‘Sources of Short Term Fund\s and Question 5 on ‘Time Value of Money and its Application’. All candidates who attempted the two questions scored the pass mark. The Examiners were not impressed by the candidate’s reaction to questions that involved computation such as Question 4 on ‘Present Value’, Question 6 on ‘Financial Statement Analysis’ and Question 7 on ;Investment Appraisal. Candidates are therefore advised that building a successful career in Banking and Finance requires both numerate and linguistic skills - ability to explain clearly their understanding. They should therefore blend the two skills.

D COMMENT ON CANDIDATES’ PERFORMANCE

The subject recorded a 100% success rate.There was no candidate with a distinction pass. The candidates were commended for recording good showing in Questions2 and 5 where all candidates that attempted the questions passed. By comparison, it is unfortunate that more than half of the candidates that attempted Questions 4, 6 and 7 could not score the pass markin the respective questions. Candidates are urged to prepare better on therelevant sub-topics.

E ANALYSIS OF GENERAL PERFORMANCE OF CANDIDATES

Total No. of Candidates

No. of Dist

No. of Passes

Total No. of Passes

Pass Rate

Failure F1 F2 Total

8 - 8 8 1000% - - - -

35

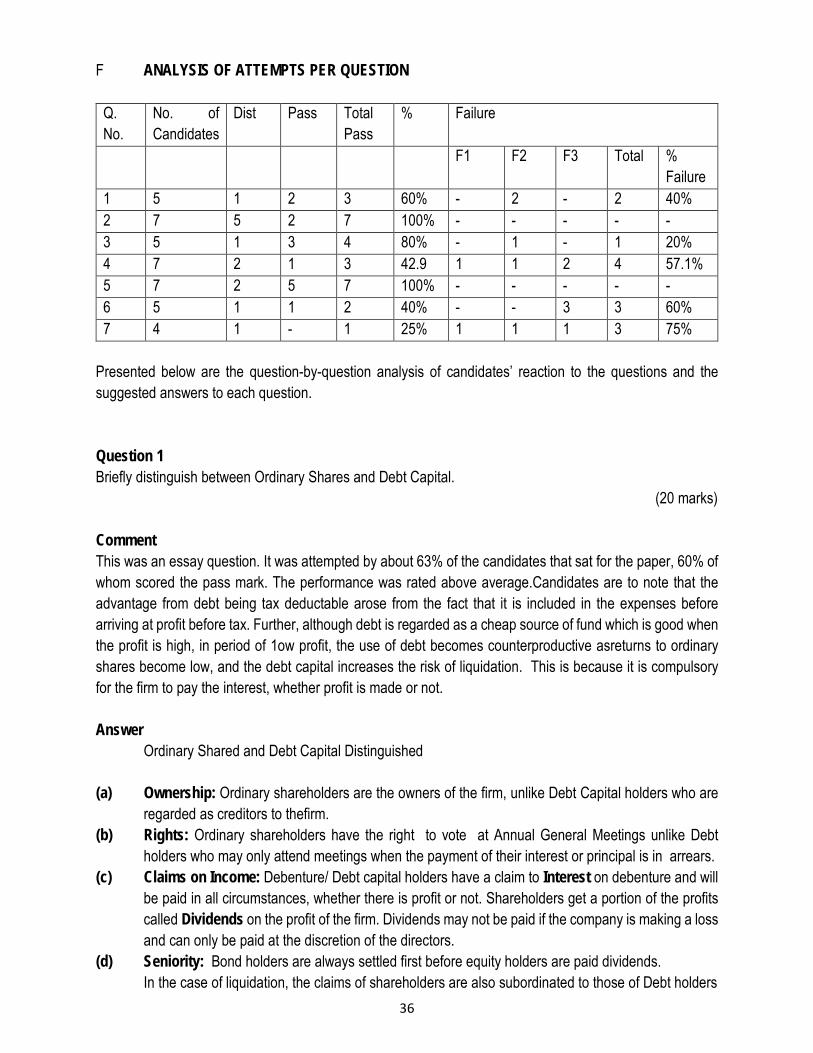

F ANALYSIS OF ATTEMPTS PER QUESTION

Q. No.

No. of Candidates

Dist Pass Total Pass

% Failure

F1 F2 F3 Total % Failure

1 5 1 2 3 60% - 2 - 2 40% 2 7 5 2 7 100% - - - - - 3 5 1 3 4 80% - 1 - 1 20% 4 7 2 1 3 42.9 1 1 2 4 57.1% 5 7 2 5 7 100% - - - - - 6 5 1 1 2 40% - - 3 3 60% 7 4 1 - 1 25% 1 1 1 3 75%

Presented below are the question-by-question analysis of candidates’ reaction to the questions and the suggested answers to each question. Question 1 Briefly distinguish between Ordinary Shares and Debt Capital.

(20 marks) Comment This was an essay question. It was attempted by about 63% of the candidates that sat for the paper, 60% of whom scored the pass mark. The performance was rated above average.Candidates are to note that the advantage from debt being tax deductable arose from the fact that it is included in the expenses before arriving at profit before tax. Further, although debt is regarded as a cheap source of fund which is good when the profit is high, in period of 1ow profit, the use of debt becomes counterproductive asreturns to ordinary shares become low, and the debt capital increases the risk of liquidation. This is because it is compulsory for the firm to pay the interest, whether profit is made or not. Answer

Ordinary Shared and Debt Capital Distinguished (a) Ownership: Ordinary shareholders are the owners of the firm, unlike Debt Capital holders who are

regarded as creditors to thefirm. (b) Rights: Ordinary shareholders have the right to vote at Annual General Meetings unlike Debt

holders who may only attend meetings when the payment of their interest or principal is in arrears. (c) Claims on Income: Debenture/ Debt capital holders have a claim to Interest on debenture and will

be paid in all circumstances, whether there is profit or not. Shareholders get a portion of the profits called Dividends on the profit of the firm. Dividends may not be paid if the company is making a loss and can only be paid at the discretion of the directors.

(d) Seniority: Bond holders are always settled first before equity holders are paid dividends. In the case of liquidation, the claims of shareholders are also subordinated to those of Debt holders

36

(e) Risk: From the investor’s perspective, shares represent a riskier bet in the company. Ordinary shareholders are risk-takers. In the case of liquidation, the claims of shareholders are subordinated to those of debt capital holders and they may not be paid anything.

(f) Cost of Funds: Debenture/ Debt Capital is regarded as a cheaper source of funds when compared with shares. The more debt the company employs the riskier the business is from the shareholders’ perspectives and so will require more compensation for taking the risk-(Risk –return trade-off).

(g) Maturity: There is maturity period for bonds or debt unlike equities. / shares. (h) Conversion: Shares cannot be converted into debentures, whereas debt capital (debentures) can

be converted to shares. Convertible debentures/debt capital can be issued which can be converted into shares at the option of the debt holders.

(i) Tax Treatment: Interest payments on debts are treated as tax-deductable expenses for the purpose of tax computation Dividend payment to equity holders is not tax-deductable.

(j) Issue at Discount: Debentures / Debt Capital can be issued at a discount. but there are legal restrictions on issue of shares at a discount. (20 marks)

Question 2 Write short notes on the following as sources of short-term funds: (i) Trade Credits (4 marks) (ii) Factoring (4 marks) (iii) Bank Overdraft (4 marks) (iv) Bankers Acceptance (4 marks) (v) Commercial Paper (Total = 4 marks) Comment The question was attempted by seven (7) (or 87.5%) of the eight (8) candidates that sat for the paper. All the candidates scored a pass mark in this question. Five (5) candidates (or 71.4%) distinction. The attempt was rated quite satisfactory. However, the performance ratings would have been better if some candidates’ understanding and presentation on Commercial Paper and Bankers Acceptance were adequate. Answer Notes in the following (i) Trade Credits: These facilitate the purchase of supplies without immediate payment .Goods or raw

material can be bought on credit for a period; conversion and eventual sales take place thereafter before payment of the trade credits. This provides a source of finance. From another perspective, trade credits are used by a supplier to encourage sales and at times a supplier will give a discount if the customer pays within a certain period of time. Trade credits are granted to those customers who have reasonable amount of financial standing and good will.

37

(ii) Factoring: This is a type of debtor finance in which a business sells its account receivables (i.e.

invoices) to a third party (called a factor) at a discount. The firm thus involves turning over the responsibility for collecting its debt to a specialist/Institution called the Factor.The firmreceives payment on the discounted invoices before the specialist collects the debt. Factoring is not the same as invoice discounting (which is called Assignment of Account Receivables). Factoring is the sale of receivables whereas invoice discounting is considered a borrowing that involves the use of the account receivable assets as collateral for the loan.

(iii) Bank Overdraft: This is an extension of credit from a lending institution (bank)when an account

reaches zero. It is a short term credit facility given by a bank for the duration of not more than one year. This facility is only available to the current account customer of a bank and is given at a stated rate of interest. It usually does not require collateral and is available to individuals and corporate entities. A customer that is granted an overdraft facility can withdraw from his account or issue cheques more than the amount in his favour up to a certain limit. Interest is paid on the outstanding balance of an overdraft.

(iv) Bankers’ Acceptance: This is a short-term debt instrument. It is a promised future payment, or time

draft which is accepted and guaranteed by a bank and drawn on a deposit at the bank. The Bankers’ Acceptance specifies the amount of money, the date, and the person to whom the payment is due. After acceptance, the draft becomes an unconditional liability of the bank.

It may further be explained as a bill of exchange drawn by a customer on a banker (financially stable bank). The bill is accepted by the bank, hence the title ‘Bankers Acceptance’. Once accepted by the first-class bank, the bill is ready for discounting with another bank or finance company to provide the funds needed. Bankers’ Acceptance is commonly used to finance import / export trade transaction, and has a tenor of 180 days. It makes a transaction safer between two parties who do not know each other because it allows the parties to substitute the bank’s creditworthiness for the one who owes the payment.

(v) Commercial Paper: This is an instrument issued by a large company (blue-chip) to raise short-term

finance from the money market. It is usually issued by a bank on behalf of its customers and sold at a discount so that the buyer obtains return on his investment upfront. The company can then pay the fixed amount on the maturity date specified on the notes. Commercial paper has a tenor of 90 days and can be rolled over twice after issue. This makes its maximum tenor to be 270 days. Typically, the longer the maturity date on a note, the higher the interest rate the issuing institution pays.

38

The following advantages may be claimed for using commercial paper: • High credit rating fetches lower cost of capital. • Wide range of maturity provides more flexibility. • It does not create any lien on the company’s asset. • Tradability of commercial paper provides investors with exit option.

Commercial paper has the following disadvantages:

• Its use is limited to blue chip company. • Issuance of commercial paper brings down bank credit limit. • Stand-by credit may become necessary. • A high degree of control is exercised on the issue of commercial paper.

Question 3 Senama is considering investing in two securities which have the following returns and risk relationships: Security A Possible Returns % -10 5 20 35 50 Probability of Occurrence 0.1 0.2 0.4 0.2 0.1 Security B Possible Returns % 5 -15 35 50 25 Probability of Occurrence 0.3 0.1 0.2 0.3 0.1 (I) You are required to calculate the expected risk of each security.

(15 marks) (II) Briefly distinguish between Risk and Uncertainty. (5 marks) (Total = 20 marks) Comment This question on risk was divided into two parts. Part (i) is a simple computation on the expected risk of two securities; which can be measured using Standard Deviation; while part (ii) tested the distinction between risk and uncertainty. The candidates made a very good attempt at the question. Five (5) (or 62.5%) of the candidates attempted the question, and 4 candidates for 80% scored pass marks. One (1) candidate (or 20%) presented excellent responses and passed at distinction level; One (1) candidate could not secure a pass mark in the question.

39

Answer Senama (i) Calculation of Expected Risk Security A Return

X Prob. X X-X (X-X)2 P (X-X)2 -0.10 0.1 -0.01 -0.30 0.090 0.009 0.05 0.2 0.01 -0.15 0.0225 0.0045 0.20 0.4 0.08 0 0 0 0.35 0.2 0.07 0.15 0.0225 0.0045 0.50 0.1 0.05 0.30 0.090 0.009 X = 0.20 0.028 Standard Deviation = P(X-X)2

= 0.028 = 0.1673 = 16.73% (7 ½ marks) Security B X Prob. X X-X (X-X)2 P(X-X)2 0.05 0.3 0.015 0.195 0.038 0.0114 -0.15 0.1 -0.015 0.395 0.156 0, 0156 0.35 0.2 0.07 0.105 0.011 0.0022 0.50 0.3 0.15 0.255 0.065 0.0195 0.25 0.1 0.025 0.005 0.000 0.0000 X =0.245 0.0487 Standard Deviation = P(X-X)2 = 0.0487 = 0.2207 = 22.07% (7 ½ marks) (ii) Risk and Uncertainty Risk can be explained to mean a situation in which there are known probabilities (both subjective and objective) for potential outcomes. The decision maker is assumed to be aware of all possible future states of nature which may occur and affect relevant decision parameters.

40

Uncertainty, on the other hand, is defined as a situation in which such probabilities are either unknown or cannot be accurately estimated. (5 marks) Question 4 (i) Bandwidth is a beneficiary in the Trust established by Mabayoje Foundation. Under the trust, she is

to receive N25, 000.00 annually in perpetuity at the end of each year. You are required to compute the present value of this annuity if investment can be done at 25%. (8 marks)

(ii) Write short notes on the following: (a) Annuity (3 marks) (b) Perpetual Annuity (3 marks) (c) Annuity Due (3 marks) (d) Ordinary Annuity (3 marks) (Total = 20 marks) Comment The question was attempted by seven (7) (or 87.5%) of the candidates. It was divided into two parts. The part (i) involves computation to determine present value of annuity. The candidates who knew the formula and its application did well in this part of the question. However, the part (ii) which was an essay question did not produce good responses as many candidates described annuity only. The overall effect was that out of the seven (7) candidates that attempted the question, only three (3) secured a pass mark, with one (1) making the pass at distinction level. Four (4) candidates failed with half of them producing woeful scripts and obtaining F3 results. Answer (i) Calculation of present value of perpetual annuity PV = A r Where PV = Present Value of Perpetual Annuity A = Annual Payments r = Interest Rates PV = N25,000 0.25 PV = N100,000 (ii) (a) Annuity: This can be explained to mean equal receipts and payments over a period of time

41

(b) Perpetual Annuity: This is equal payment or receipt into perpetuity without an end. It is given by the formula PV = A R

(c) Annuity Due: This is equal payment or receipts at the beginning of a year. It is given by the formula FV = K (1+r) (1+r)n r

(d) Ordinary Annuity: This is equal payment or receipt received at the end of a year. It is given by the

formula. FV = K (1+r)n-1 r

Question 5 (i) Briefly explain what you understand by “Time value of money”. (10 marks) (ii) How does this concept apply to the process of Compounding and Discounting? (10 marks) (Total = 20 marks) Comments This was an essay question on Time value of money, and the process of determining its effect on the value of money -that is, compounding and discounting. It was attempted by 87.5% of the candidates and all of them secured pass marks; with two (2) |(or 26.8%) making the pass at distinction level. The overall assessment of the performance was adjudged ‘Very Good’. Answer (i) Time Value of Money

This is the notion that money in the present is worth more than some amount in the future. This is attributable to inflation, missed opportunities and the risk of default. One Naira today is worth more than one Naira in the future. This is so because the owner of one Naira can invest it in a profitable investment or put it in a deposit account that will give him a return. The key components of time value of money are future value and present value. (10 marks)

(ii) Compounding and Discounting The concept of future or compound value involves the application of compound interest rate to a present or initial sum of money that will materialise in some future amount.

42

It is the sum to which the initial amount of money or principal will group over a number of years, when interest is earned at a rate per annum. The higher the value of interest, the faster the rate of growth of the initial amount of money or principal. The concept of discounting or present value is the inverse of compounding. Discounting helps the decision maker to determine the present value of a future amount, assuming he has an opportunity cost to earn a certain return on the money. This return is also known as the discount rate, required return, cost of capital or opportunity cost. (10 marks)

Question 6 Cherish Plc. Statement of Financial position as at the year ended December 31, 2012. Fixed Assets N000 N000 Property, Plant and Equipment 2276 Other Financial Assets 98 2374 Current Assets Stock 289 Debtor 503 Marketable Securities 68 Cash 363 Total Assets 1223 3597 Equity and Liabilities Equity Ordinary Shares 191 Preference Shares 200 Reserves 428 Retained Earnings 1135 Shareholders’ Funds 1954 Non Current Liabilities Long-erm liabilities 1023 Current Liabilities Creditors 382 Bank Overdraft 79 Long-term loans 159

43

620 Total Equities & Liabilities 3597 Extract of Revenue Account ‘’000 Sales 3,074 Cost of Sales 2,088 You are required to calculate the following: (i) Net working capital (4 marks) (ii) Current Ratio (4 marks) (iii) Quick Ratio (4 marks) (iv) Stock Turnover (4 marks) (v) Debt Equity Ratio (4 marks) (Total = 20 marks) Comments This question tested Ratio Analysis -a very important sub-topic in Business Finance that has wide implication on career progression of bankers. A good knowledge of the sub-topic will also aid easy qualification in the institute’s examination because of the relevance to other core courses in the institute’s qualifying curriculum. It was attempted by 87.5% of the candidates that sat for the examination. Two (2) (or 20%) of the candidates passed at distinction level. Another 2 (or 20%) passed ordinarily. The three (3) candidates (or 60%) that failed presented woeful answers and scored F3 marks. This suggests that candidates have not mastered this important topic and that those who cared to were amply rewarded. Performance in the question was rated below average. Candidates are advised to note the classification, formula and explanation of the basis for computing the various ratios. Answer Cherish Plc (i) Net Working Capital

Current Assets - current liabilities N1,223, 000 – 620,000 = 603,000

(ii) Current Ratio Current Assets Current Liabilities = 1,223,000 620,000 = 1.97 times (iii) Quick Ratio

44

= Current Assets – Stock Current Liabilities = 1,223,000 – 289,000 620,000 = 1.51 times (iv) Stock Turnover = Cost of Goods Sold Average Stock of Inventory = 2,088,000 289,000 = 7.2 Times (v) Debt/Equity Ratio = Long-Term Debt X 100 Shareholders Funds 1

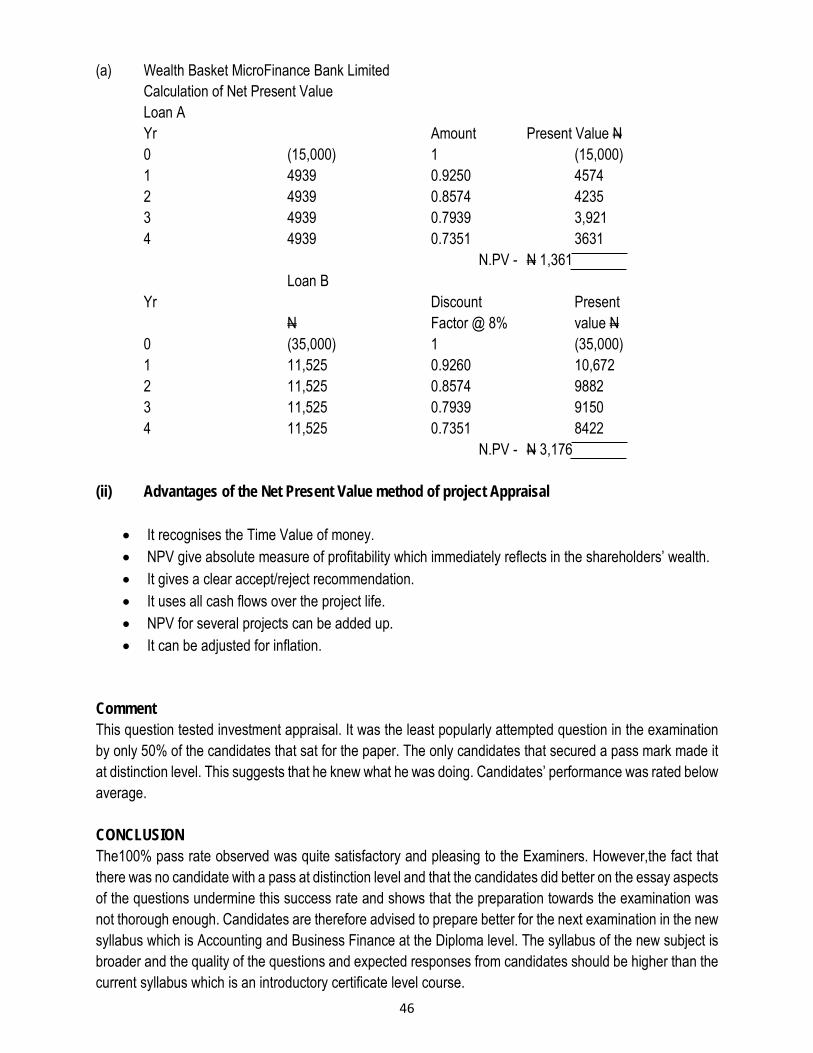

= 1,023,000 X 100 1,954,000 X 1 = 52.4% Question 7 (a) Wealth Basket Microfinance Bank Limited has two loan applications with the following cash flows: Year 0 1 2 3 4 Loan A - N15, 000 4,939 4,939 4,939 4,939 Loans B - N 35,000 11,525 11,525 11,525 11,525 Both loans attract a 12 per cent interest rate and are amortised annually over a four-year period. if the cost of funds is 8%, you are required to determine the value created with the use of the Net Present Value Method. (15 marks) (b) What are theadvantages of the Net Present Value project appraisal method? (5 marks) (Total = 20 marks) Answer

45

(a) Wealth Basket MicroFinance Bank Limited Calculation of Net Present Value

Loan A Yr Amount Present Value N 0 (15,000) 1 (15,000) 1 4939 0.9250 4574 2 4939 0.8574 4235 3 4939 0.7939 3,921 4 4939 0.7351 3631 N.PV - N 1,361

Loan B Yr Discount Present

N Factor @ 8% value N 0 (35,000) 1 (35,000)

1 11,525 0.9260 10,672 2 11,525 0.8574 9882 3 11,525 0.7939 9150 4 11,525 0.7351 8422 N.PV - N 3,176 (ii) Advantages of the Net Present Value method of project Appraisal

• It recognises the Time Value of money. • NPV give absolute measure of profitability which immediately reflects in the shareholders’ wealth. • It gives a clear accept/reject recommendation. • It uses all cash flows over the project life. • NPV for several projects can be added up. • It can be adjusted for inflation.