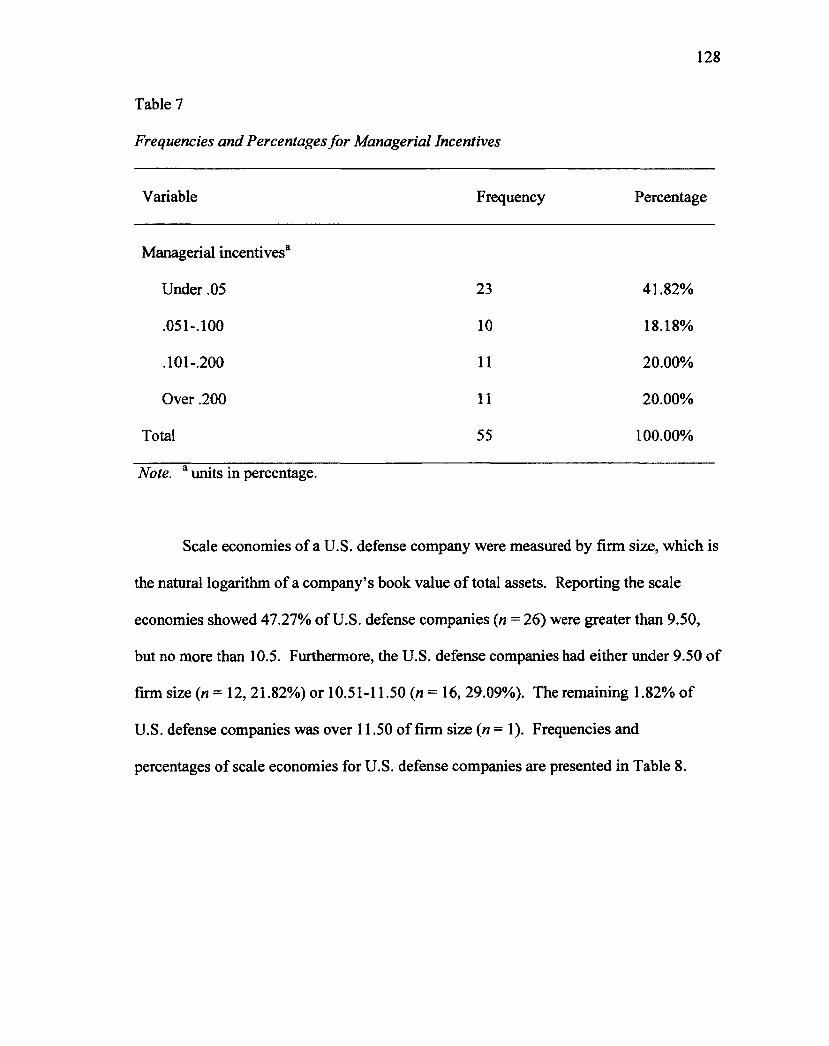

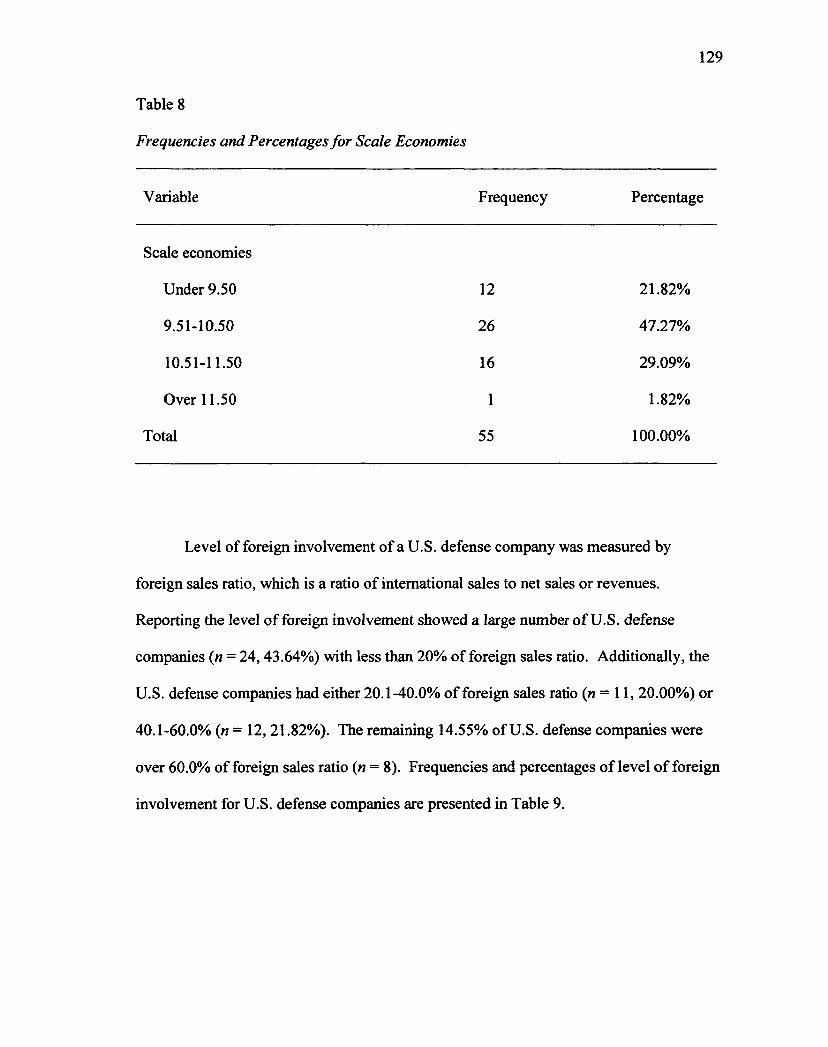

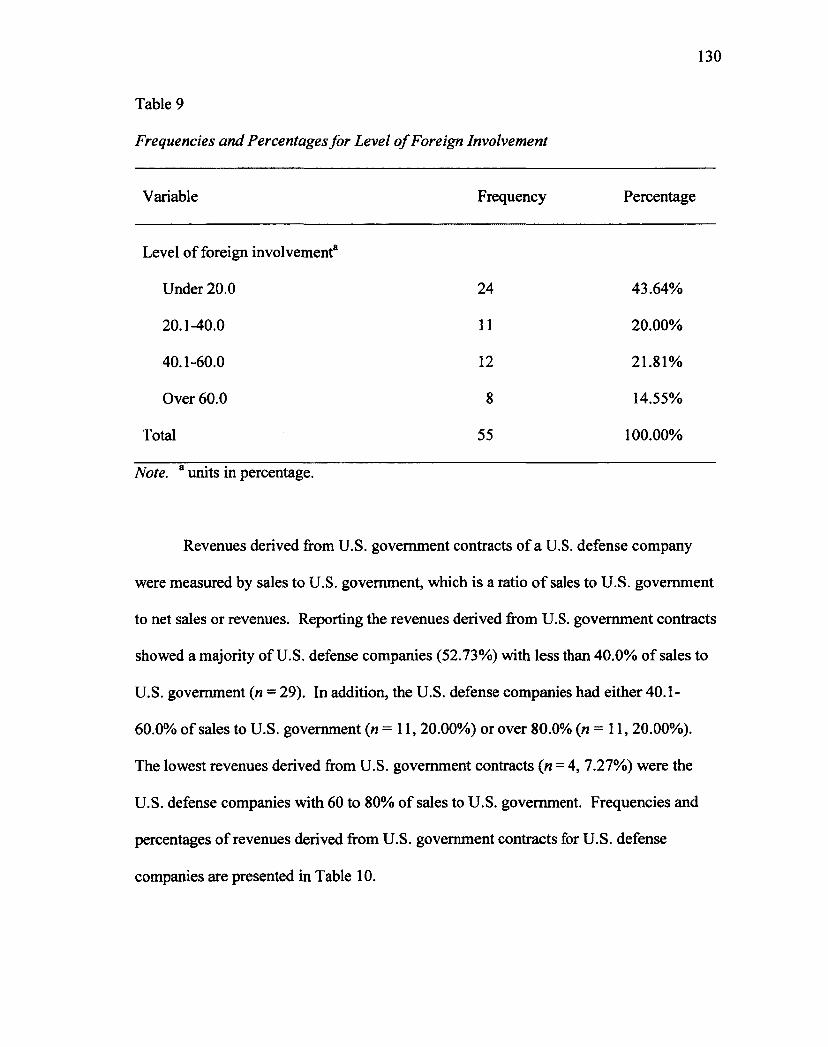

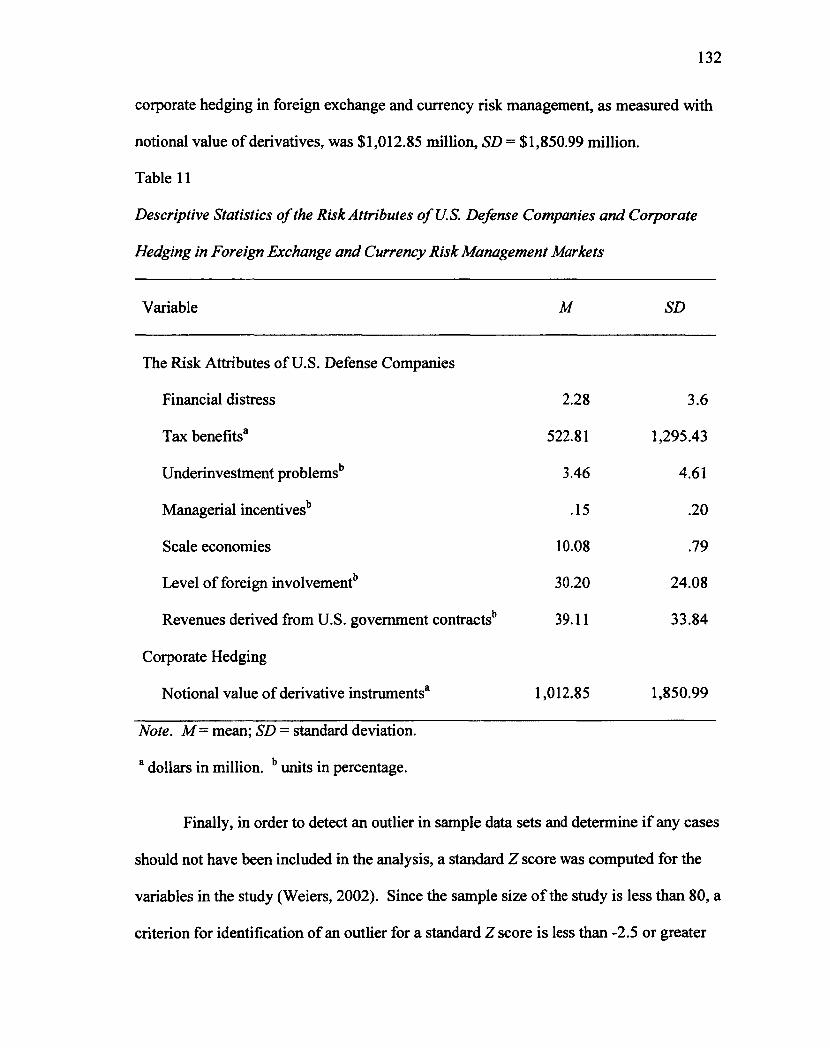

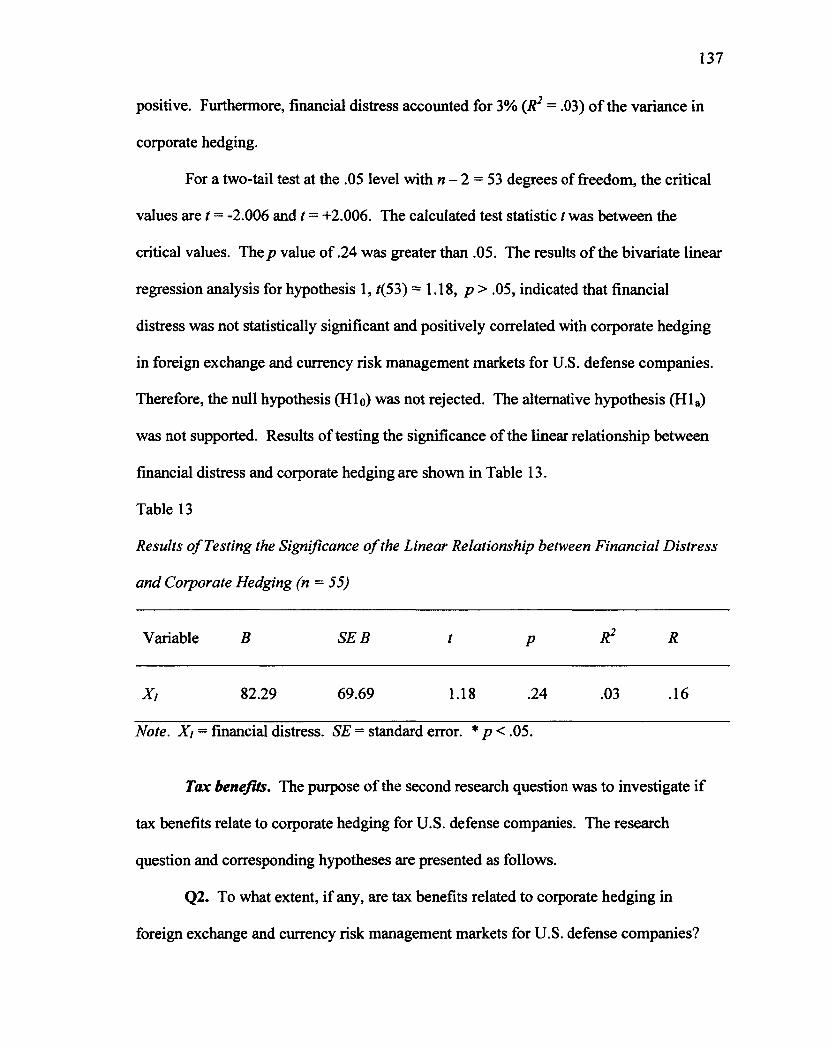

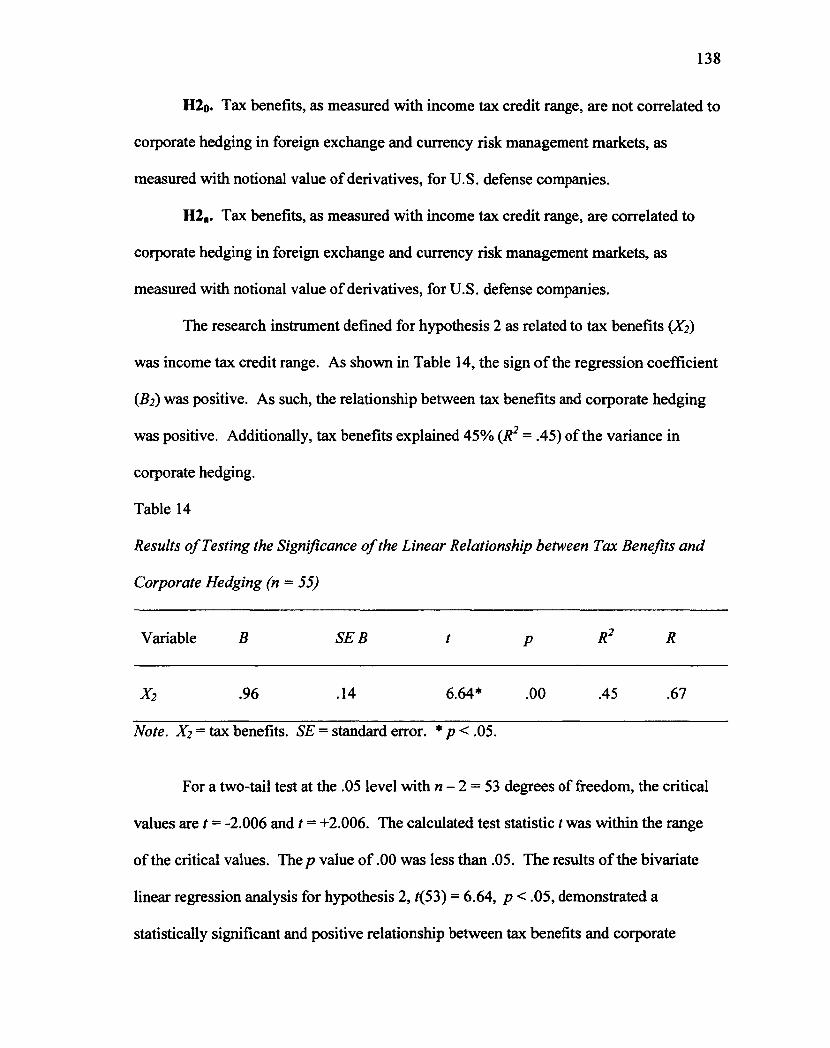

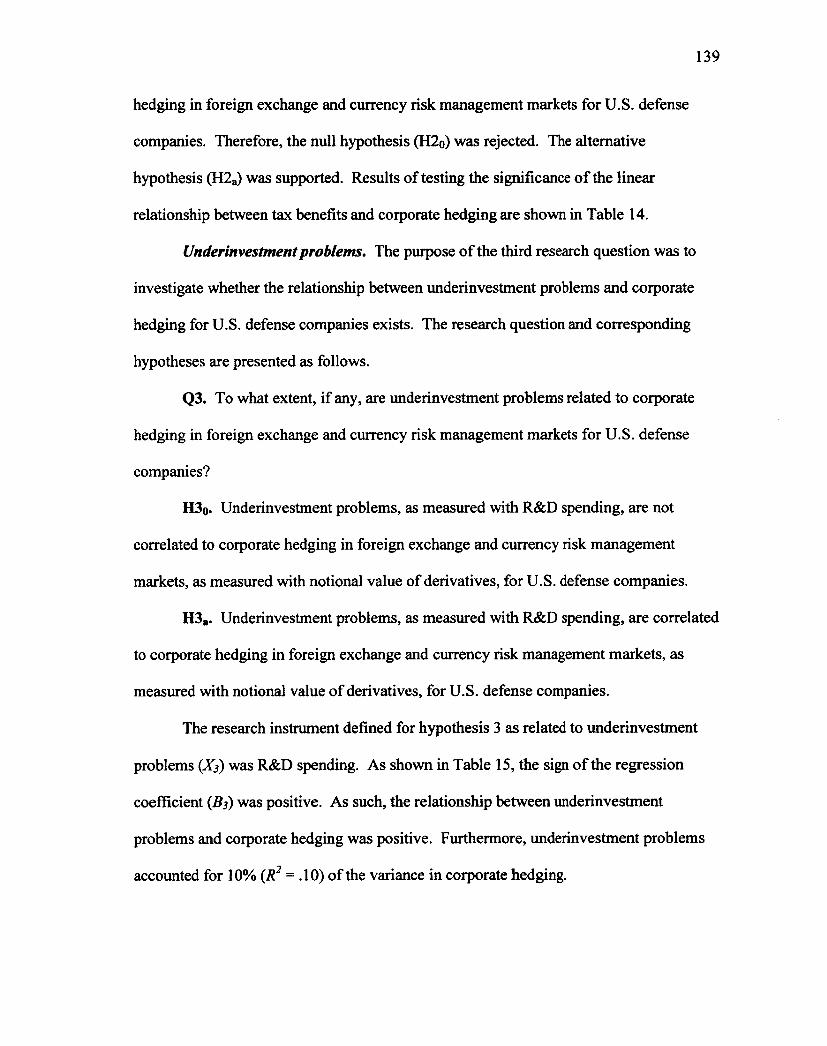

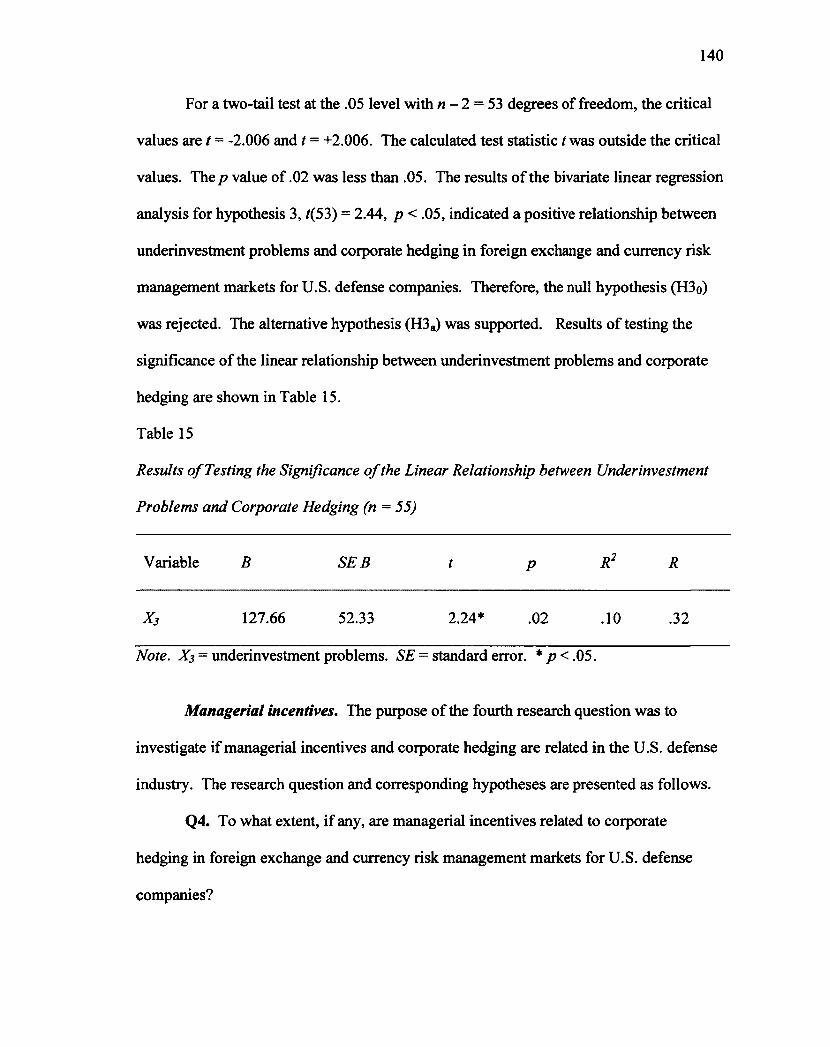

examining the relationship between organizational risk attributes hedging

DESCRIPTION

examining relationTRANSCRIPT

Examining the Relationship between Organizational Risk Attributes of U.S. Defense

Companies and Corporate Hedging

Dissertation

Submitted to Northcentral University

Graduate Faculty of the School of Business and Technology Management in Partial Fulfillment of the

Requirements for the Degree of

DOCTOR OF BUSINESS ADMINISTRATION

by

CHARLIE SHAO

Prescott Valley, Arizona September 2012

UMI Number: 3534186

All rights reserved

INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted.

In the unlikely event that the author did not send a complete manuscript and there are missing pages, these will be noted. Also, if material had to be removed,

a note will indicate the deletion.

UMI 3534186

Published by ProQuest LLC 2012. Copyright in the Dissertation held by the Author. Microform Edition © ProQuest LLC.

All rights reserved. This work is protected against unauthorized copying under Title 17, United States Code.

ProQuest LLC 789 East Eisenhower Parkway

P.O. Box 1346 Ann Arbor, Ml 48106-1346

2012

Charlie Shao

APPROVAL PAGE

Examining the Relationship between Organizational Risk Attributes of U.S. Defense

Companies and Corporate Hedging

by

Charlie Shao

Approved by:

Chair: Steven Munkeby, D.M U/-T/ao\a.

Date

Member: Roy Nafarrete, D.M.

Member: Becky Takeda-Tinker, Ph.D.

Certified by:

School Dean: A. Lee Smith, Ph.D. vi /W/?-

Date

Abstract

Corporate hedging had become a vital activity for success of United States (U.S.) defense

firms. As a result of corporate hedging in foreign exchange and currency risk

management, U.S. defense companies were exposed recently to financial risks resulting

in millions of dollars of lost profits. While research has shown organizational risk

attributes may be indicators of corporate hedging activities, the relationship between

organizational risk attributes and corporate hedging practices in U.S. defense industry has

not been studied. To ensure the success of corporate hedging, managers in the U.S.

defense companies need to be attentive to the organizational determinants that might

influence corporate hedging decisions. The purpose of this study was to examine the

relationship between the risk attributes of U.S. defense companies and corporate hedging

in foreign exchange and currency risk management. A linear regression model was

utilized to estimate the relationship between seven risk attributes and corporate hedging

for a random sample of 55 U.S. defense companies that were faced with foreign exchange

and currency risk exposures. Evidence indicated financial distress was not statistically

significant correlated with corporate hedging, t(53) = 1.18,/? > .05; tax benefits were

statistically significant and positively correlated with corporate hedging, t(53) = 6.64, p

< .05; underinvestment problems were positively correlated with corporate hedging, /(53)

= 2.44, p < .05; managerial incentives were not statistically significant correlated with

corporate hedging, /(53) = -1.92, p > .05; scale economies were statistically significant

and positively correlated with corporate hedging, r(53) = 4.54, p < .05; level of foreign

involvement was not statistically significant correlated with corporate hedging, f(53) =

1.45, p > .05; and revenues derived from U.S. government contracts were negatively

iv

correlated with corporate hedging, /(53) = -2.39, p < .05. Findings of this research

suggest tax benefits, underinvestment problems, scale economies, and revenues derived

from U.S. government contracts are important determinants of corporate hedging for U.S.

defense companies. Further research in assessment of the relationship between

organizational risk attributes of U.S. defense companies and corporate hedging is

recommended.

v

Acknowledgements

There is no way I could have written this dissertation manuscript without my

support team. I would like to take this opportunity to express my profound gratitude to

all who helped me complete this research study. Their comments and suggestions were

inestimably contributed to the success of the study. I am particularly grateful to my

committee chair, Dr. Steven Munkeby, who made specific comments and suggestions

that led to significant improvements of the study. The consistent counsel and guidance

provided by Dr. Munkeby have been invaluable. I would like to thank my committee

members, Dr. Roy Nafarrete and Dr. Becky Takeda-Tinker, for their wisdom and advices

as well. I also owe a word of appreciation to Dr. Bob Goldwasser, Dr. Catherine

Crocker, Dr. Emil Berendt, Dr. Carrie Williams, and Dr. John Caruso for their

encouragement and knowledge in my pursuit of this academic journey.

I would like to give a special thanks to the establishment of an employee scholar

program at United Technologies Corporation (UTC) and Computer Sciences Corporation

(CSC). I have been encouraged to develop additional skills and engage in lifelong

learning from the program. In particular, my thanks go out to my former and current

managers, Aksel Sidem, Barbara Nickels, and Daniel Hamernick, for their support of my

academic study along the way.

Most naturally, I want to say thanks to my wife Jenny and sons Jason and Tyler,

who gave me the time and quiet I needed to work and do research for the study. Without

their constant support and patience, the completion of this study would not have been

possible. I also appreciate my brother, Dr. Ruijin Shao, to let me learn from his

vi

knowledge and experience. As always, I would like to thank my parents and parents-in-

law for their love and prayers for me on the journey.

vii

Table of Contents

List of Tables x

List of Figures xi

Chapter 1: Introduction 1 Background 2 Problem Statement 4 Purpose of the Study 4 Theoretical Framework 6 Research Questions 11 Hypotheses 12 Nature of the Study 14 Significance of the Study 17 Definitions 18 Summary 24

Chapter 2: Literature Review 26 Overview 28 Financial Distress 33 Tax Benefits 37 Underinvestment Problems 43 Managerial Incentives 46 Scale Economies 53 Level of Foreign Involvement 56 Other Factors 59 Corporate Hedging in Foreign Exchange and Currency Risk Management 78 Summary 85

Chapter 3: Research Method 87 Research Design and Methods 88 Participants 91 Research Instruments 93 Operational Definition of Variables 101 Data Collection, Processing, and Analysis 104 Methodological Assumptions, Delimitations, and Limitations 117 Ethical Assurances 118 Summary 120

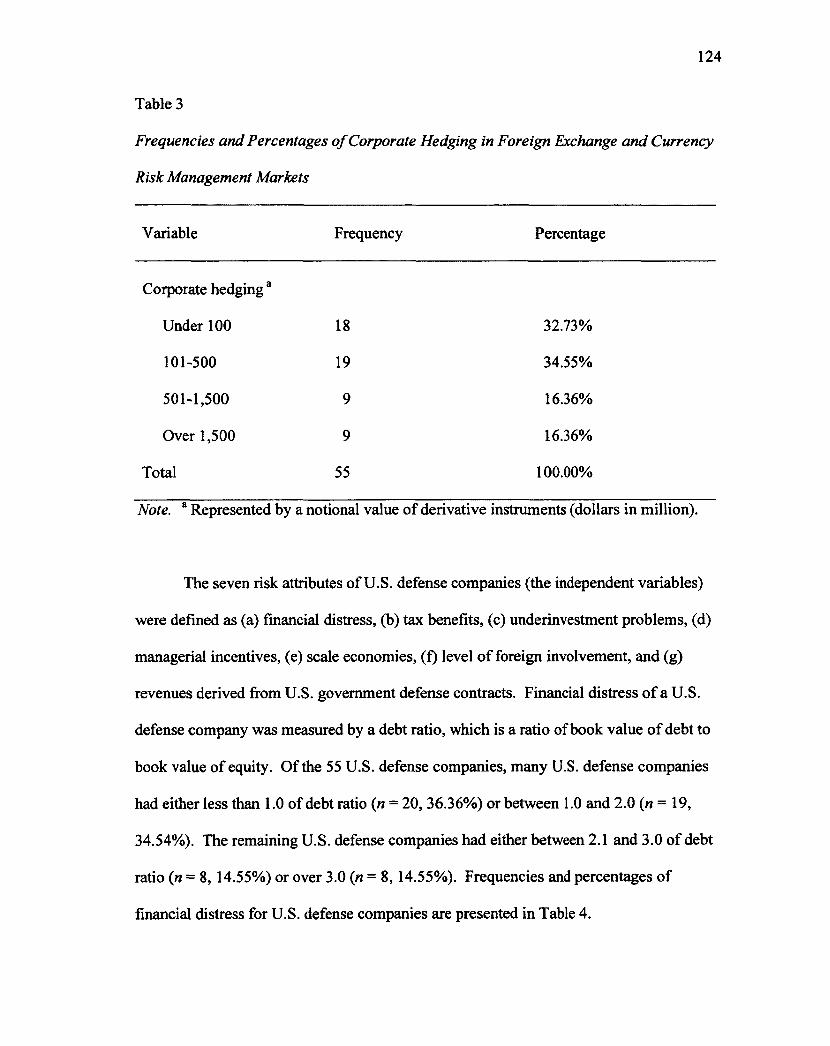

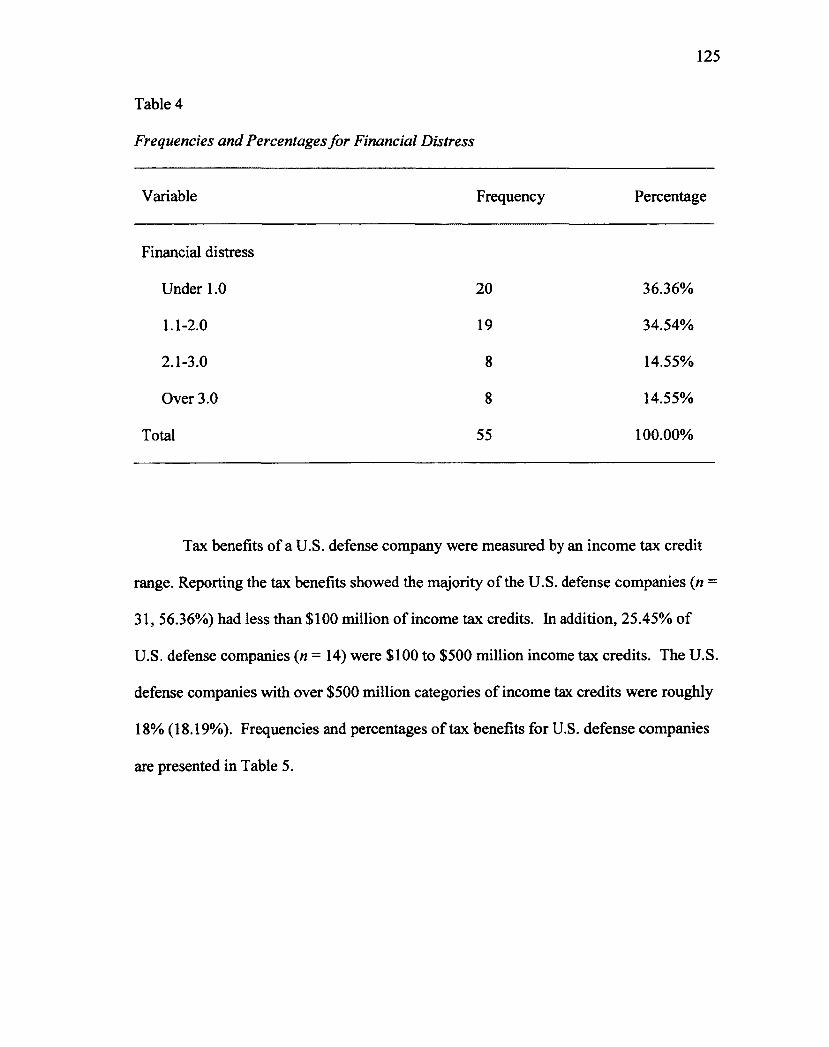

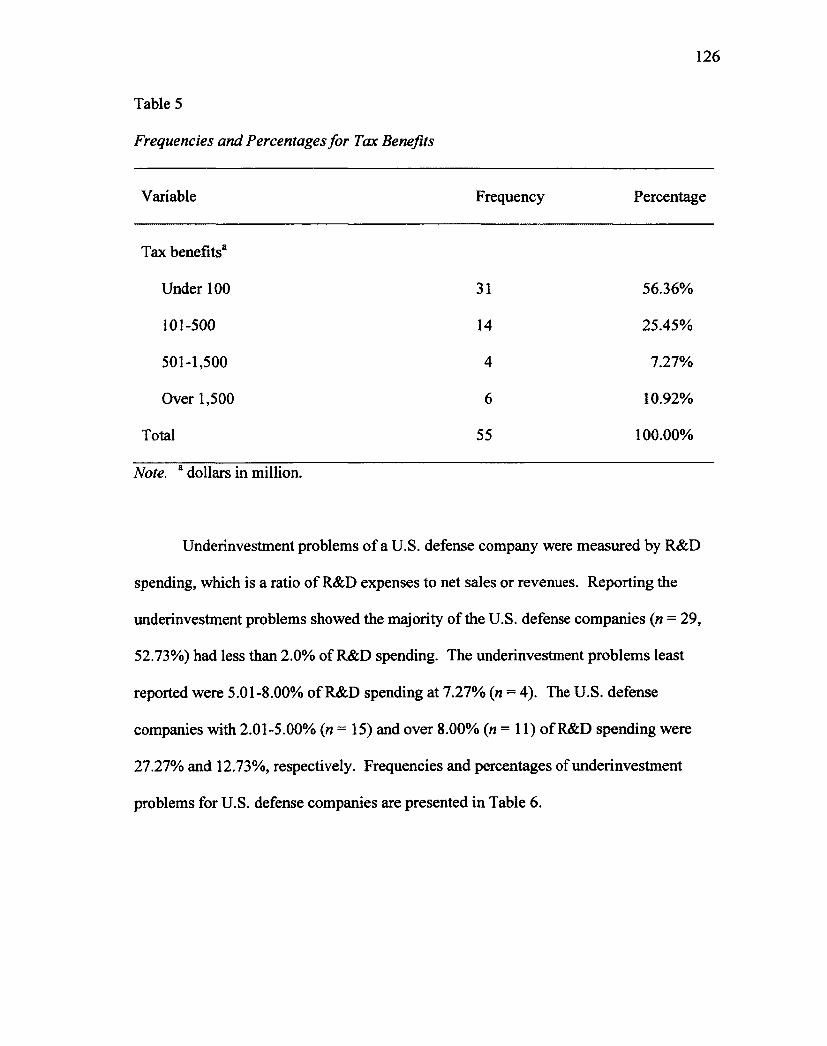

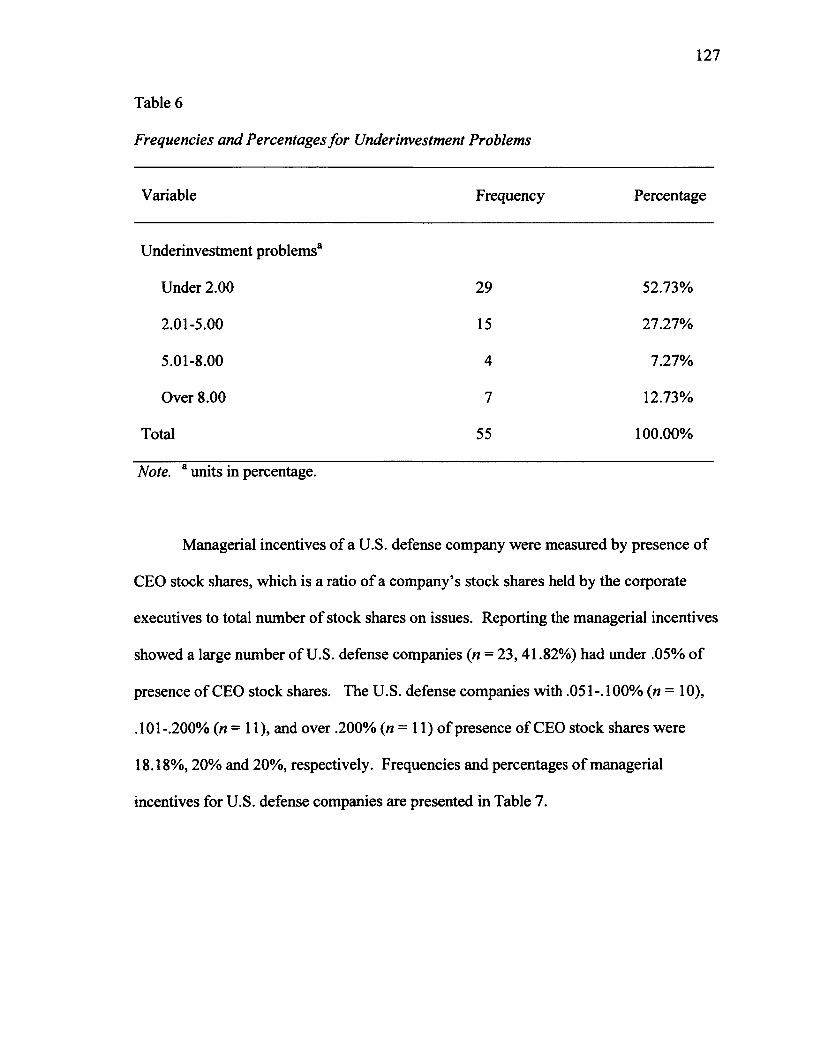

Chapter 4: Findings 122 Results 123 Evaluation of Findings 147 Summary 153

Chapter 5: Implications, Recommendations, and Conclusions 155

viii

Implications 156 Recommendations 167 Conclusions 169

References 174

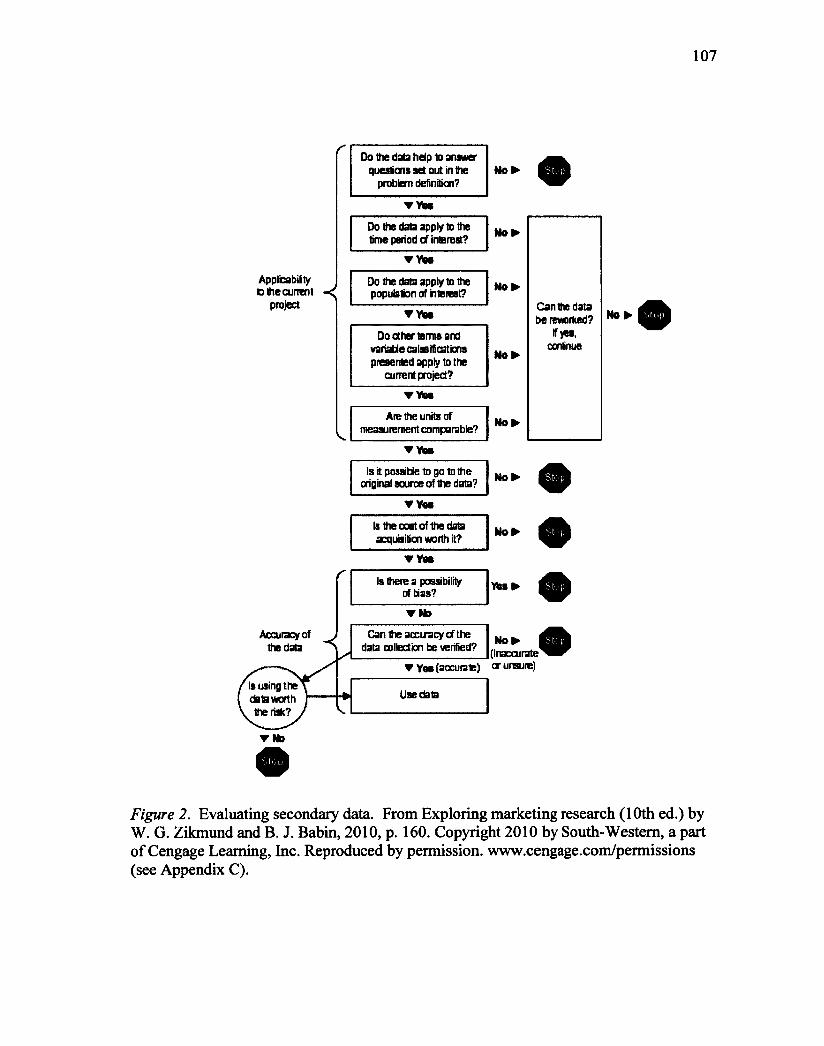

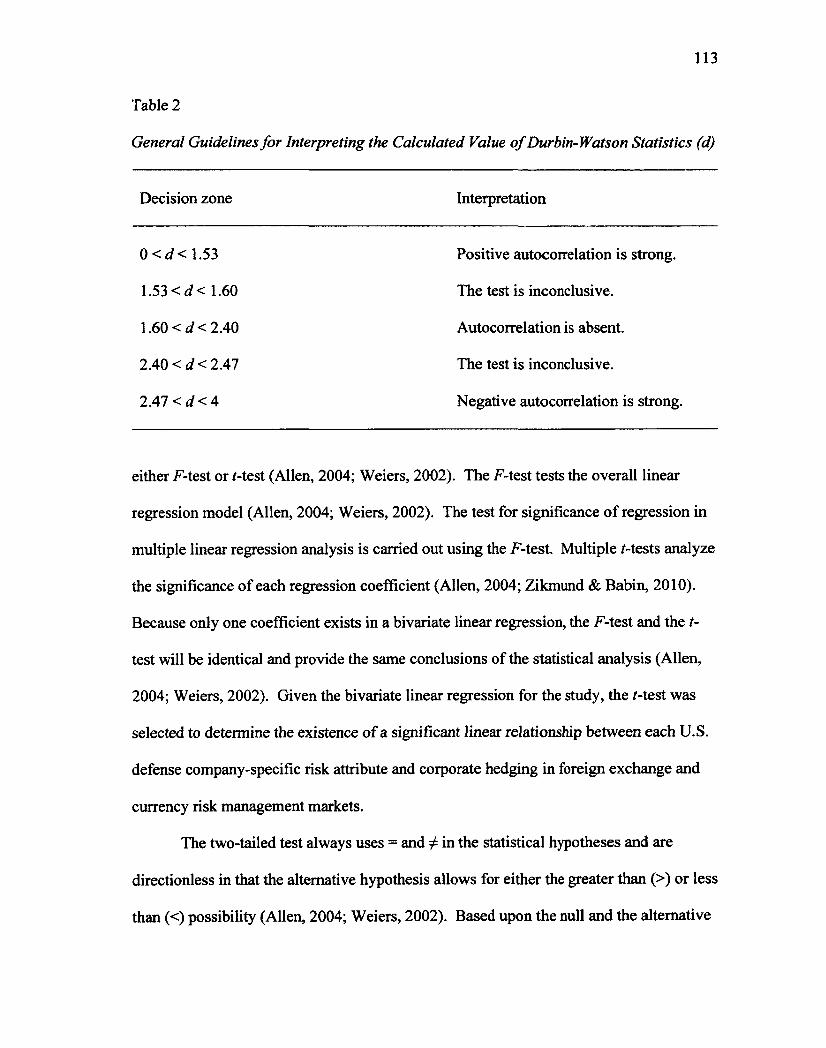

Appendixes 194 AppendixA: Random Sampling Procedure 195 Appendix B: Determination of Sample Size with a Priori Power Analysis 196 Appendix C: Permission to Use the Diagram of Evaluating Secondary Data 199 Appendix D: Residual Plots for the Independent Variables 200 Appendix E: Normal Probability Plots of Residuals for the Dependent Variable ....204 Appendix F: Approval Letter for the Research Study from the University's IRB ...208

ix

List of Tables

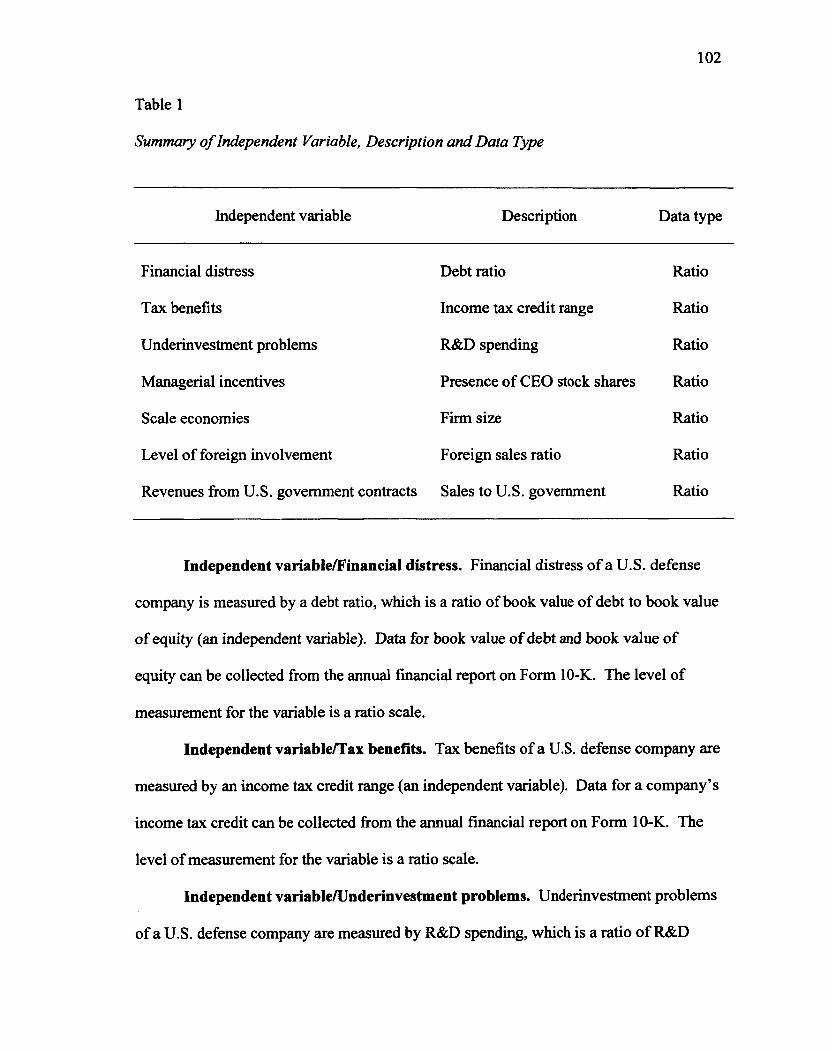

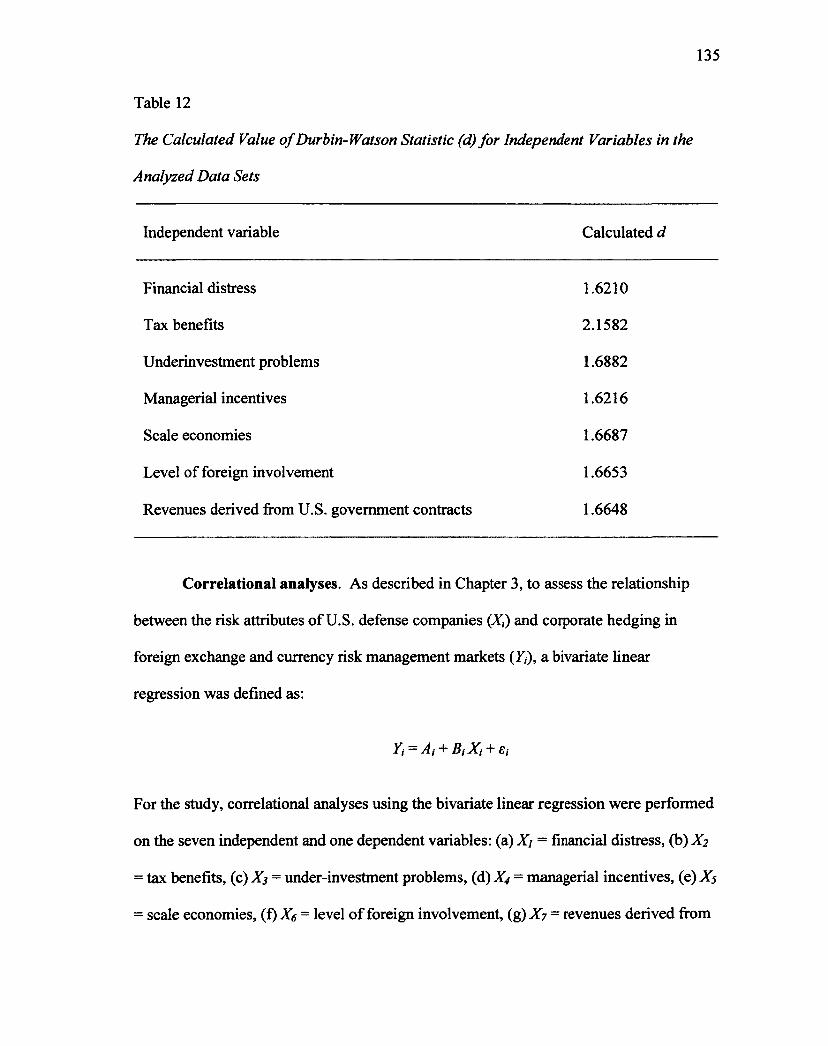

Table 1 Summary of Independent Variable, Description and Data Type 102 Table 2 General Guidelines for Interpreting the Calculated Value of Durbin-Watson Statistics (d) 113 Table 3 Frequencies and Percentages of Corporate Hedging in Foreign Exchange and Currency Risk Management Markets 124 Table 4 Frequencies and Percentages for Financial Distress 125 Table 5 Frequencies and Percentages for Tax Benefits 126 Table 6 Frequencies and Percentages for Underinvestment Problems 127 Table 7 Frequencies and Percentages for Managerial Incentives 128 Table 8 Frequencies and Percentages for Scale Economies 129 Table 9 Frequencies and Percentages for Level of Foreign Involvement 130 Table 10 Frequencies and Percentages for Revenues Derivedfrom U.S. Government Contracts 131 Table 11 Descriptive Statistics of the Risk Attributes of U.S. Defense Companies and Corporate Hedging in Foreign Exchange and Currency Risk Management Markets.... 132 Table 12 The Calculated Value of Durbin-Watson Statistic (d) for Independent Variables in the Analyzed Data Sets 135 Table 13 Results of Testing the Significance of the Linear Relationship between Financial Distress and Corporate Hedging (n = 55) 137 Table 14 Results of Testing the Significance of the Linear Relationship between Tax Benefits and Corporate Hedging (n = 55) 138 Table 15 Results of Testing the Significance of the Linear Relationship between Underinvestment Problems and Corporate Hedging (n = 55) 140 Table 16 Results of Testing the Significance of the Linear Relationship between Managerial Incentives and Corporate Hedging (n = 55) 141 Table 17 Results of Testing the Significance of the Linear Relationship between Scale Economics and Corporate Hedging (n = 55) 143 Table 18 Results of Testing the Significance of the Linear Relationship between Level of Foreign Involvement and Corporate Hedging (n = 55) 144 Table 19 Results of Testing the Significance of the Linear Relationship between Revenues Derived from U.S. Government Contracts and Corporate Hedging (n = 55) 146

x

List of Figures

Figure 1. Tax benefits in corporate hedging 38 Figure 2. Evaluating secondary data 107

xi

1

Chapter 1: Introduction

With growing globalization and the global economic and financial crisis

beginning in 2008, the increased volatility of the financial markets has given rise to

increased financial risks faced by United States (U.S.) defense companies such as

Lockheed Martin Corporation and the Boeing Company (The Boeing Company, 2009;

Chance & Brooks, 2007; Gregory, 2010; Lockheed Martin Corporation, 2009). The

management of financial risks has become paramount for the survival of U.S. defense

companies in volatile financial markets (The Boeing Company, 2009; Chance & Brooks,

2007; Lockheed Martin Corporation, 2009; Whaley, 2006). In 2009, a survey from the

International Swaps and Derivatives Association (ISDA) indicated increased corporate

usage of financial derivatives. Representatives of more than 94% of the top 500 global

companies use derivative instruments to manage and hedge financial risks more

effectively (ISDA, 2009). As a means of reducing financial risk, corporate hedging with

derivatives is an integral part of corporate risk management among leading companies

worldwide (Chance & Brooks, 2007).

An introduction to the problem resulting from corporate hedging in risk

management is provided in this chapter. Background information is presented regarding

the importance of the problem caused by corporate hedging. The problem and the

purpose of the study are presented, followed by a discussion of the theoretical framework

of the study. Research questions and hypotheses are defined, and the nature and

significance of the study are described. Finally, definitions of key terms for the study are

given, followed by a summary of the chapter.

2

Background

A derivative is a financial instrument whose value is derived iBrom the value of

another underlying asset (Chance & Brooks, 2007; Hull, 2006; Stulz, 2003). The

derivatives used by representatives of a company to hedge financial risk include forward

contracts, future contracts, option, and swap (Hancock-Weise, 2011; Hull, 2006; Whaley,

2006). In general, corporate hedging with derivatives is defined as "a component of a

more general process called risk management, the alignment of the actual level of risk

with the desired level of risk" (Chance & Brooks, 2007, p. 355). There is a demonstrated

need for corporate hedging in foreign exchange and currency risk management (Eiteman,

Stonehill, & Moffett, 2007; Homaifar, 2004; Nguyen & Faff, 2010). Such evidence

points to the fact that companies benefit from corporate hedging (Froot, Scharfstein, &

Stein, 1993; Graham & Smith, 1999; Jensen & Meckling, 1976; Morellec & Smith, 2007;

Smith & Stulz, 1985; Shapiro, 2005). Corporate hedging with derivatives can be

designed to create a wide range of cash flows because derivatives are cheap and flexible

(Hancock-Weise, 2011; Nguyen & Faff, 2010; Whaley, 2006).

As documented in the annual financial reports, company representatives in the

U.S. defense industry perform corporate hedging in risk management on a regular basis

(The Boeing Company, 2009; Lockheed Martin Corporation, 2009). Corporate hedging

is important to ensure that U.S. defense companies gain reliable, timely, and affordable

access to materials needed to produce defense products and to protect the value of the

assets of a company against appreciation or depreciation in foreign currencies (The

Boeing Company, 2009; Eiteman et al., 2007; Stulz, 2003; Lockheed Martin Corporation,

2009; Watts, 2008). However, company representatives are reluctant to hedge against a

3

foreign exchange and its currency risks because corporate hedging may introduce risks

such as a buildup of a derivative position, which is an uncertainty in terms of the hedge

performance, counterparty risks, and possible high hedging costs (Chance & Brooks,

2007; Gregory, 2010; Hancock-Weise, 2011; Stulz, 2003; Whaley, 2006). Uncertainties

regarding global currency may result in increased costs and reduced profits for U.S.

defense companies while limiting the desire of representatives of these companies to

conduct business with foreign markets (The Boeing Company, 2009; Eiteman et al.,

2007; Homaifar, 2004; Lockheed Martin Corporation, 2009).

Researchers (e.g., Artez & Bartram, 2010; Stulz, 2003) have suggested a range of

theoretical determinants that might influence corporate hedging decisions at the

organizational level. The main explanations of corporate hedging focus on risk

management as a means to lessen the possibility of financial distress (Smith & Stulz,

1985), reduce expected taxes (Graham & Smith, 1999; Smith & Stulz, 1985), avoid

underinvestment (Froot et al., 1993), and maximize managers' own self-interest (Jensen &

Meckling, 1976; Shapiro, 2005; Stulz, 2003). However, the determinants of corporate

hedging in foreign exchange and currency risk management can differ across different

industry sectors and companies with different characteristics (Adam, Dasgupta, &

Titman, 2007; Bartram, Brown, & Fehle, 2009; Lei, 2006; Papaioannou, 2006; Reynolds,

Bhabra, & Boyle, 2009; Rogers, 2002). To improve the efficiency of corporate hedging

in risk management, managers in the U.S. defense companies need to be attentive to the

organizational determinants that might affect corporate hedge policies (Artez & Bartram,

2010; Stulz, 2003).

4

Problem Statement

The problem addressed in this study was that, as a result of corporate hedging

practices in foreign exchange and currency risk management markets, U.S. defense

companies are exposed to financial risks leading to a potential loss of millions of dollars

of profit (The Boeing Company, 2009; Chance & Brooks, 2007; Eiteman et al., 2007;

Gregory, 2010; Lockheed Martin Corporation, 2009; Stulz, 2003). As a U.S. government

contractor, the Boeing Company reported net losses of $92 and $101 million, in 2007 and

2008 respectively, associated with corporate hedging transactions (The Boeing Company,

2009). Derivatives used for defense contracts, with notional foreign exchange and

currency values of $1.9 billion in 2008 and $1.4 billion in 2009, were designated as

hedging instruments (Lockheed Martin Corporation, 2009). Although corporate hedging

in risk management is receiving increasing attention in the U.S. defense industry, whether

organizational risk factors relate to corporate hedging for U.S. defense companies is

unknown (Artez & Bartram, 2010). To ensure that company managers succeed in

performing corporate hedging in risk management, a need exists for empirical assessment

regarding the relationship between the risk attributes of U.S. defense companies and

corporate hedging (Artez & Bartram, 2010; Petersen & Thiagarajan, 2000; Stulz, 2003).

The relationship between the risk attributes of U.S. defense companies and corporate

hedging practices in foreign exchange and currency risk management markets has not

been examined in previous literature.

Purpose of the Study

The purpose of this quantitative correlational study was to examine the

relationship between the risk attributes of U.S. defense companies and corporate hedging

5

in foreign exchange and currency risk management markets. A secondary data analysis

was used. The independent variables of the risk attributes of U.S. defense companies

were defined as financial distress, underinvestment problems, tax benefits, managerial

incentives, scale economies, level of foreign involvement, and revenues from U.S.

government contracts (Allayannis & Ofek, 2001; Bartram et al., 2009; Dolde & Mishra,

2007; Froot et al., 1993; Jensen & Meckling, 1976; Jorion, 1990; Smith & Stulz, 1985;

Stulz, 2003). The dependent variable was defined as corporate hedging in foreign

exchange and currency risk management markets. The population for the study consisted

of 194 U.S. defense companies in the National Automated Accounting Research System

(NAARS) database (American Institute of Certified Public Accountants, 2005). All 194

defense companies that conducted defense-related business from 2000 to 2010 in the U.S.

qualified for inclusion in the study. A random sample for the study was drawn from the

list of 194 U.S. defense companies. From this population, a sample size of 55 U.S.

defense companies was used to ensure statistical significance. All financial data were

collected from the annual financial report on Form 10-K and the annual proxy statement,

filed in the electronic data gathering and retrieval (EDGAR) database system of the U.S.

Securities and Exchange Commission (Securities and Exchange Commission [SEC],

2012). With the passage of the Sarbanes-Oxley Act of2002, corporate executives must

certify the financial statements are faithful representations of the financial positions and

results of operations of the company (Whittington & Pany, 2004). Because of the

improved disclosure requirements for the business and financial information of a

company, more empirical studies have been based on the use of the data contained in the

annual financial reports (Apostolou & Apostolou, 2008; Bartram et al., 2009; Carter,

6

Rogers, & Simkins, 2006; Hsu, Ko, Wu, Cheng, & Chen, 2009; Judge, 2006; Nguyen,

Mensah, & Faff, 2007; Ramirez, 2007; Reynolds et al., 2009; Schiozer & Saito, 2009;

Spano, 2008; SprCic, 2007).

Theoretical Framework

The underlying theoretical framework supporting this study is composed of

corporate hedging theories and empirical studies. To discuss the rationale for engaging in

corporate hedging and what the effects of corporate hedging can be, the two most

prevalent theories used by representatives of nonfinancial companies are shareholder

value maximization theory and managerial utility maximization theory. Empirical

research on corporate hedging in foreign exchange and currency risk management for

nonfinancial companies is relatively recent, and the results of the empirical studies are

varied (Allayannis & Weston, 2001; Bartram et al., 2009; Berkman, Bradbury, Hancockc,

& Innes, 2002; Brown, 2001; Carter et al., 2006; Davies, Eckberg, & Marshall, 2006;

Dolde & Mishra, 2007; Fabling & Grimes, 2008; Graham & Rogers, 2002; Hagelin,

2003; Judge, 2006; Kapitsinas, 2008; Lei, 2006; Luiz & Junior, 2011; Marsden &

Prevost, 2005; Menon & Viswanathan, 2005; Nguyen & Faff, 2003; Reynolds & Boyle,

2005; Schiozer & Saito, 2009; Spano, 2008). The current study was designed to confirm

whether the corporate hedging theories and the findings from empirical studies are

applicable to corporate hedging practices in the U.S. defense industry.

According to the shareholder value maximization theory, the exploitation of

inefficiencies in the perfect capital market is based on the assumption that corporate

hedging can add value by reducing various costs involved with future cash flows and

alleviating problems associated with these costs. Furthermore, financially distressed

7

companies face costs of default on debt obligations and costs of filing for bankruptcy

(Smith & Stulz, 1985). One of the most important benefits in effective risk management

is to reduce the costs associated with financial distress (Stulz, 2003). Given these costs,

company representatives have incentives to reduce the probability of financial distress.

When companies are subject to a progressive tax system, corporate hedging can reduce

expected tax liabilities (Graham & Smith, 1999; Smith & Stulz, 1985). As such, a greater

convexity in the tax functiorj will lead to a greater likelihood of corporate hedging.

Furthermore, when external financing is more costly to companies than are internally

generated funds, company representatives may tend to use derivative instruments (Froot

et al., 1993). In particular, the company representatives can hedge cash flows to avoid a

shortfall in internal funds so that costly external financing from the capital markets may

be prevented (Froot et al., 1993).

The primary theoretical alternative to the shareholder value maximization as a

corporate hedging theory is managerial utility maximization. From the perspective of the

managerial utility maximization theory, corporate hedging can have different effects on

shareholder value. Corporate hedging decisions may be the result of the aversion of

company managers to financial risks because, unlike shareholders, the company

managers have disproportionately large investments in the company, which cannot easily

diversify their risks (Morellec & Smith, 2007). When the objectives of shareholders and

company managers diverge, the managers can behave in their own self-interest rather

than in the best interests of the shareholders (Jenson & Meckling, 1976). Therefore,

company managers may seek to maximize their own self-interest and have incentives to

hedge their own private wealth at the expense of the shareholders (Jensen & Meckling,

8

1976; Shapiro, 2005; Stulz, 2003). To ensure that company managers act to maximize

shareholder value and not just to advance their own private wealth, managerial

compensation policy can be designed to give the company managers incentives to select

corporate hedging that increase shareholder value (Jenson & Meckling, 1976; Shapiro,

2005; Stulz, 2003). Company managers may also be interested in protecting the

profitability of a company through corporate hedging in risk management because of a

possible change in corporate asset value (Shapiro, 2005).

In addition to the theoretical determinants of corporate hedging, some additional

factors are associated with the use of derivative instruments in company risk

management. These additional factors include scale economies (Allayannis & Ofek,

2001; Nance, Smith, & Smithson, 1993), firm value (Carter et al., 2006; Jin & Jorion,

2006), level of foreign involvement (Howton & Perfect, 1998; Menon & Viswanathan,

2005), foreign debt (Judge, 2009; Nguyen & Faff, 2006), asymmetric information

(Breeden & Viswanathan, 1996; DeMarzo & Duffie, 1991), board characteristics

(Borokhovich, Brunarski, Crutchley, & Simkins, 2004; Prevost, 2005), industry-specific

characteristics (Rogers, 2002; Schiozer & Saito, 2009), country-specific characteristics

(Lei, 2006; Marsden & Prevost, 2005), and accounting reporting methods (Sapra, 2002;

Supanvanij & Strauss, 2010).

Large companies are more likely to hedge than are small companies because the

large companies may have better access to external financing in capital markets

(Allayannis & Ofek, 2001). Smaller companies have been advised to hedge more than

larger ones because the smaller companies are likely to have a greater informational

asymmetric problem (Nance et al., 1993). Corporate hedging and firm value were

9

positively related in the U.S. airline industry (Carter et al., 2006). In contrast, corporate

hedging did not affect market values of companies in the U.S. oil and gas industry (Jin &

Jorion, 2006). Corporate hedging activities were significantly and positively related to

the extent of foreign involvement by U.S. multinational corporations (Menon &

Viswanathan, 2005). However, the relationship between the level of foreign involvement

and corporate hedging with currency derivatives was not strongly supported in another

study (Howton & Perfect, 1998). Corporate hedging was significantly related to the

existence of foreign debt in one study (Judge, 2009), but in a different study, the use of

foreign debt was found to be irrelevant to corporate hedging in foreign exchange and

currency risk management (Nguyen & Faff, 2006).

Corporate hedging decisions can be explained by the reputation of company

managers (Breeden & Viswanathan, 1996; Demarzo & Duffie, 1991). Board

composition was not related to the use of derivative instruments (Marsden & Prevost,

2005). Board size and the presence of corporate executives on the board were not found

to be determinants of corporate hedging (Borokhovich et al., 2004). Because regulated

industries operated in more stable environments (Smith & Watts, 1992), representatives

of companies in regulated industries used corporate hedging less than did representatives

of companies in unregulated industries (Rogers, 2002). Furthermore, company

representatives in regulated industries were less likely to use currency derivatives for

corporate hedging (Schiozer & Saito, 2009). Financial market developments, legal

environment, and macroeconomic characteristics of the country were considered to be

possible reasons for differences in corporate hedging practices (Lei, 2006; Marsden &

Prevost, 2005). Derivative reporting transparency is a significant determinant of

10

corporate hedging (Supanvanij & Strauss, 2010). Furthermore, increased reporting of

transparency resulting from the FAS 133 standard may induce company representatives

to take an excessive speculative position (Sapra, 2002).

From a theoretical perspective, companies benefit from corporate hedging in

foreign exchange and currency risk management because of shareholder value

maximization and managerial utility maximization (Froot et al., 1993; Graham & Smith,

1999; Jensen & Meckling, 1976; Morellec & Smith, 2007; Smith & Stulz, 1985; Shapiro,

2005). The theoretical framework presented in the study underscores the premise that

U.S. defense companies may benefit from corporate hedging in foreign exchange and

currency risk management. Recently, corporate hedging theories have been empirically

tested to examine if nonfinancial companies benefit from corporate hedging in foreign

exchange and currency risk management (Allayannis & Weston, 2001; Bartram et al.,

2009; Berkman et al., 2002; Brown, 2001; Carter et al., 2006; Davies, Eckberg, &

Marshall, 2006; Dolde & Mishra, 2007; Fabling & Grimes, 2008; Graham & Rogers,

2002; Hagelin, 2003; Judge, 2006; Kapitsinas, 2008; Lei, 2006; Luiz & Junior, 2011;

Marsden & Prevost, 2005; Menon & Viswanathan, 2005; Nguyen & Faff, 2003;

Reynolds & Boyle, 2005; Schiozer & Saito, 2009; Spano, 2008). However, the

conflicting findings from prior empirical studies remain because the conclusions from the

prior empirical studies are largely sample specific, and the measurement of the

determinants for corporate hedging is not consistent (Artez & Bartram, 2010; Nguyen &

Faff, 2010; Stulz, 2003).

Although the existing empirical studies on corporate hedging in foreign exchange

risk management by nonfinancial companies are diverse, in a recent review of the

11

literature, a gap in research studies on the relationship between the risk attributes of U.S.

defense companies and corporate hedging was identified. Therefore, additional research

to assess the relationship between the risk attributes of U.S. defense companies and

corporate hedging in foreign exchange and currency risk management markets is

warranted. Furthermore, an evaluation of the corporate hedging theories in light of the

findings from empirical studies was enabled by the current study. As such, the study can

be used to extend the body of knowledge on corporate hedging at an organizational level.

Research Questions

To broaden a view of corporate hedging in the U.S. defense industry with

discussions of risk management for a specific financial exposure to U.S. defense

companies, the following research questions directed the focus of the study:

Ql. To what extent, if any, is financial distress related to corporate hedging in

foreign exchange and currency risk management markets for U.S. defense companies?

Q2. To what extent, if any, are tax benefits related to corporate hedging in

foreign exchange and currency risk management markets for U.S. defense companies?

Q3. To what extent, if any, are underinvestment problems related to corporate

hedging in foreign exchange and currency risk management markets for U.S. defense

companies?

Q4. To what extent, if any, are managerial incentives related to corporate

hedging in foreign exchange and currency risk management markets for U.S. defense

companies?

Q5. To what extent, if any, are scale economies related to corporate hedging in

foreign exchange and currency risk management markets for U.S. defense companies?

12

Q6. To what extent, if any, is level of foreign involvement related to corporate

hedging in foreign exchange and currency risk management markets for U.S. defense

companies?

Q7. To what extent, if any, are revenues from U.S. government contracts related

to corporate hedging in foreign exchange and currency risk management markets for U.S.

defense companies?

Hypotheses

Based on the research questions and literature review presented in Chapter 2,

seven hypotheses about the relationship between the risk attributes of U.S. defense

companies and corporate hedging in foreign exchange and currency risk management

markets were developed for the study.

Hl0. Financial distress, as measured with debt ratio, is not correlated to corporate

hedging in foreign exchange and currency risk management markets, as measured with

notional value of derivatives, for U.S. defense companies.

Hla. Financial distress, as measured with debt ratio, is correlated to corporate

hedging in foreign exchange and currency risk management markets, as measured with

notional value of derivatives, for U.S. defense companies.

H2o. Tax benefits, as measured with income tax credit range, are not correlated to

corporate hedging in foreign exchange and currency risk management markets, as

measured with notional value of derivatives, for U.S. defense companies.

H2„. Tax benefits, as measured with income tax credit range, are correlated to

corporate hedging in foreign exchange and currency risk management markets, as

measured with notional value of derivatives, for U.S. defense companies.

13

H3o. Underinvestment problems, as measured with research and development

(R&D) spending, are not correlated to corporate hedging in foreign exchange and

currency risk management markets, as measured with notional value of derivatives, for

U.S. defense companies.

H3a. Underinvestment problems, as measured with R&D spending, are correlated

to corporate hedging in foreign exchange and currency risk management markets, as

measured with notional value of derivatives, for U.S. defense companies.

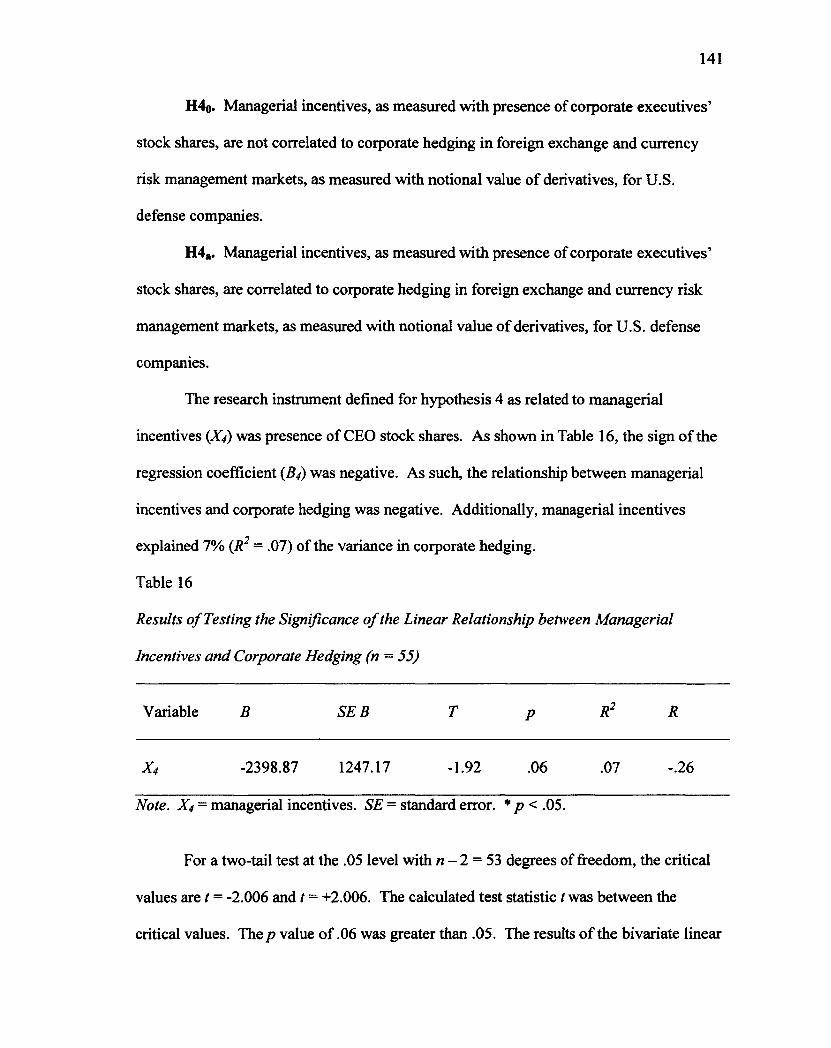

H4o. Managerial incentives, as measured with presence of corporate executives'

stock shares, are not correlated to corporate hedging in foreign exchange and currency

risk management markets, as measured with notional value of derivatives, for U.S.

defense companies.

H4„. Managerial incentives, as measured with presence of corporate executives'

stock shares, are correlated to corporate hedging in foreign exchange and currency risk

management markets, as measured with notional value of derivatives, for U.S. defense

companies.

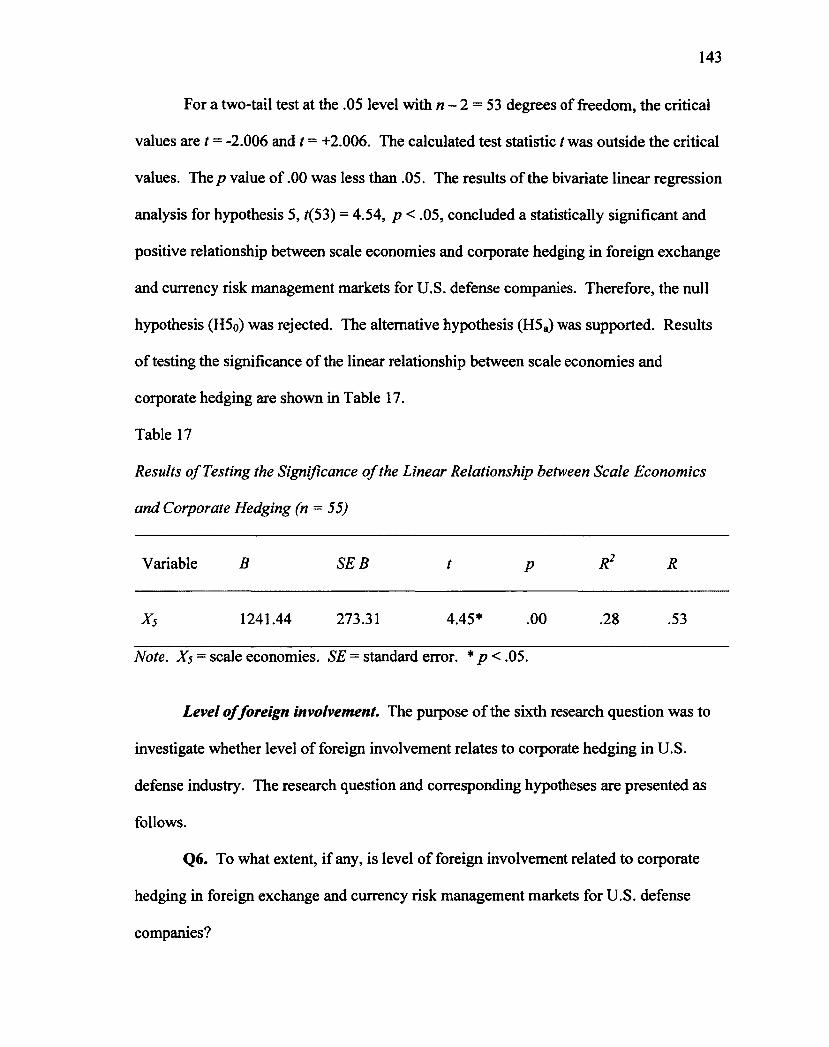

H5o- Scale economies, as measured with firm size, are not correlated to corporate

hedging in foreign exchange and currency risk management markets, as measured with

notional value of derivatives, for U.S. defense companies.

H5a. Scale economies, as measured with firm size, are correlated to corporate

hedging in foreign exchange and currency risk management markets, as measured with

notional value of derivatives, for U.S. defense companies.

14

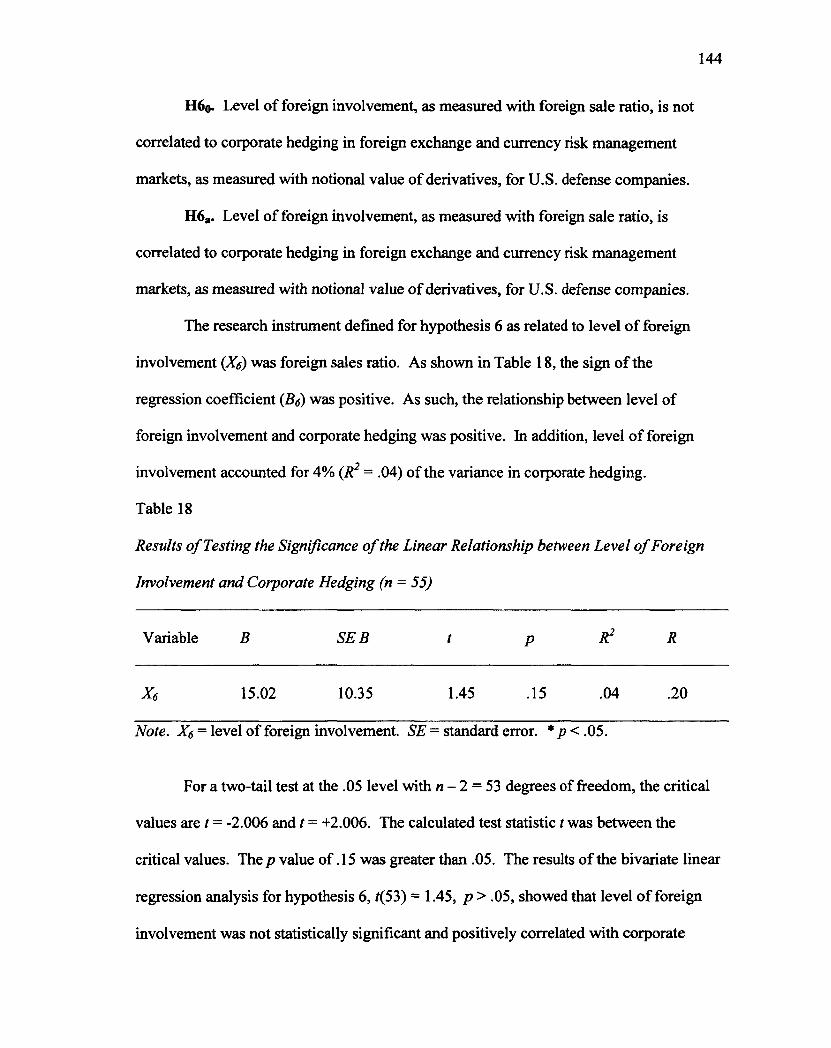

H6o. Level of foreign involvement, as measured with foreign sale ratio, is not

correlated to corporate hedging in foreign exchange and currency risk management

markets, as measured with notional value of derivatives, for U.S. defense companies.

H6a. Level of foreign involvement, as measured with foreign sale ratio, is

correlated to corporate hedging in foreign exchange and currency risk management

markets, as measured with notional value of derivatives, for U.S. defense companies.

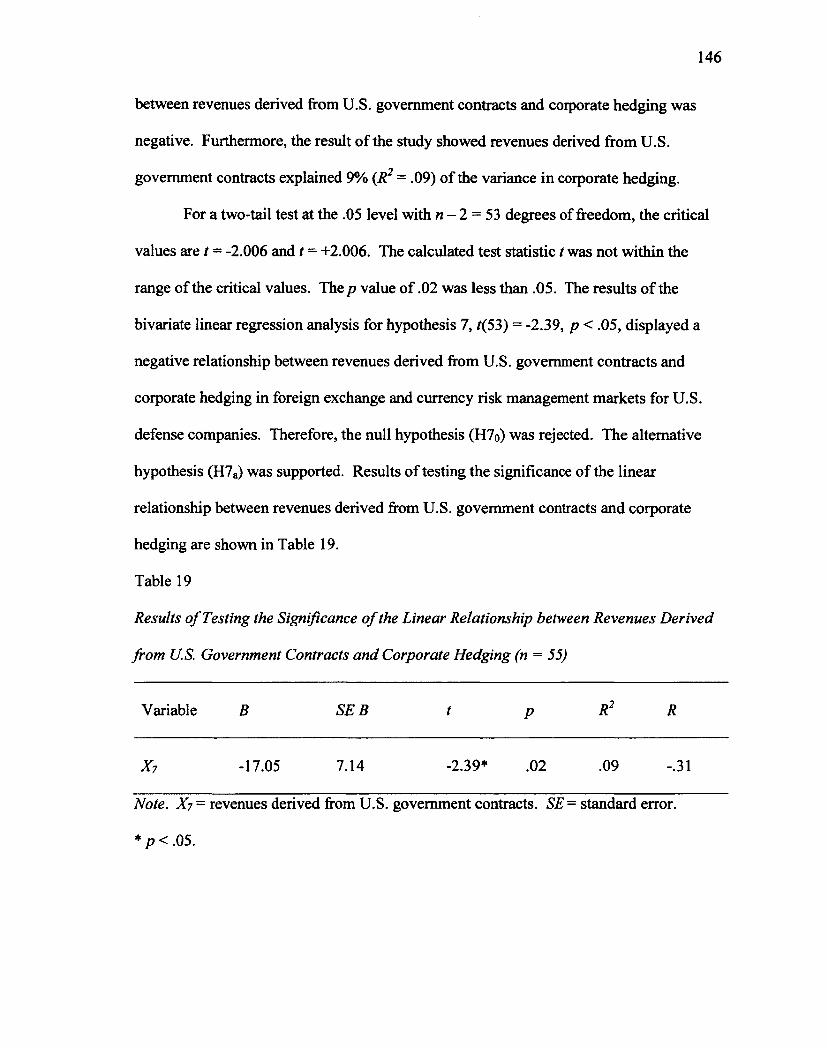

H70. Revenues derived from U.S. government contracts, as measured with sales

to U.S. government, are not correlated to corporate hedging in foreign exchange and

currency risk management markets, as measured with notional value of derivatives, for

U.S. defense companies.

H7a. Revenues derived from U.S. government contracts, as measured with sales

to U.S. government, are correlated to corporate hedging in foreign exchange and currency

risk management markets, as measured with notional value of derivatives, for U.S.

defense companies.

Nature of the Study

The purpose of this quantitative correlational study was to examine the

relationship between the risk attributes of U.S. defense companies and corporate hedging

in foreign exchange and currency risk management markets. The design of the study was

based on an analysis of secondary source. The quantitative correlational study was

theoretically informed by related literature on corporate hedging. A positivistic view was

used to develop a focus on theory testing, wherein corporate hedging theories were first

adopted as the framework for developing and testing hypotheses in the research context

(Trochim & Donnelly, 2008). Therefore, a deductive orientation of the study was

15

emphasized in the study (Trochim & Donnelly, 2008). Given the nature of the research

purpose, the research questions, and the adequate availability of previous empirical

studies to formulate hypothesized relationships for examination, the research design for

the study was a quantitative correlational design.

The population for the study consisted of 194 U.S. defense companies listed in the

NAARS database (American Institute of Certified Public Accountants, 2005). All 194

defense companies that conducted defense-related business from 2000 to 2010 in the U.S.

qualified for inclusion in the study. From this population, 55 U.S. defense companies

were randomly selected to ensure statistical significance. Seven constructed independent

variables were defined to represent the risk attributes of U.S. defense companies: (a)

financial distress, (b) underinvestment problems, (c) tax benefits, (d) managerial

incentives, (e) scale economies, (f) level of foreign involvement, and (g) revenues from

U.S. government contracts. The instruments to measure the independent variables were

debt ratio, income tax credit range, R&D spending, presence of corporate executives'

(CEO) stock shares, firm size, foreign sale ratio, and sales to U.S. government. The

constructed dependent variable for the study was defined as corporate hedging in foreign

exchange and currency risk management markets. Corporate hedging was measured as

the notional value of derivatives. All data were collected from the annual financial report

on Form 10-K and the annual proxy statement in the EDGAR database system of the

SEC.

In prior empirical studies, the outcome of corporate hedging decisions was

considered to be a linear function of the independent variables, which are proxies of the

determinants of corporate hedging (Allayannis & Weston, 2001; Berrospide,

16

Purnanandam, & Raj an, 2007; Carter et al., 2006; Hagelin, 2003; Jin & Jorion, 2006;

Judge, 2006; Khediri, 2010; Lei, 2006; Nguyen et al., 2007; Nguyen & Faff, 2010;

Spano, 2008; SprCic, 2007). In the current study, the relationship between each

independent variable and the dependent variable was measured as a bivariate linear

regression, with corporate hedging in foreign exchange and currency risk management

markets as the dependent variable and a U.S. defense company-specific risk attribute as

the independent variable. Bivariate linear regression analyses were performed to address

the research questions for the study. Parametric methods to test the hypotheses were used

because the normality, independence of errors, and equal variance assumptions for

performing a bivariate linear regression were met (Allen, 2004, Weiers, 2002).

Parametric linear regressions were used in prior empirical studies to determine similar

relationships (Carter et al., 2006; Hagelin, 2003; Hsu et al., 2009; Jin & Jorion, 2006;

Judge, 2006; Khediri, 2010; Lei, 2006; Nguyen et al., 2007; Nguyen & Faff, 2010;

Reynolds, Bhabra, & Boyle, 2009; Spano, 2008; SprCic, 2007). The following steps were

taken for conducting hypothesis testing to address the research questions in the study:

state the hypothesis to be tested, analyze the assumptions of underlying linear regression,

select test statistic used for measures of association, and define decision criterion to either

accept or reject the hypothesis (Allen, 2004; Lind, Marchal, & Mason, 2005; Zikmund,

2003). To support the interpretation associated with correlation in bivariate linear

regression analysis, the coefficient of determination and sign of regression coefficients

indicated the strength and direction of the association between the risk attributes of U.S.

defense companies and corporate hedging in foreign exchange and currency risk

management markets.

17

Significance of the Study

To compete in global markets as well as competitive and regulated environments,

U.S. defense companies are exposed to financial risks resulting in a potential loss of

millions of dollars of profits as a result of corporate hedging practices in foreign

exchange and currency risk management (The Boeing Company, 2009; Chance &

Brooks, 2007; Eiteman et al., 2007; Gregory, 2010; Lockheed Martin Corporation, 2009;

Stulz, 2003). Identifying and measuring the determinants for corporate hedging becomes

a critical battle for company managers in U.S. defense companies. If the relationship

between the risk attributes of U.S. defense companies and corporate hedging in foreign

exchange and currency risk management markets is conclusively demonstrated, the study

may provide useful insight for corporate hedging to company managers in the U.S.

defense industry, and may help to improve the effectiveness of strategic thinking and

decision-making for corporate hedging by U.S. defense companies in foreign exchange

and currency risk management markets.

The contribution of this study to the literature regarding corporate hedging is

significant given that U.S. defense companies potentially lose millions of dollars of

profits as a result of corporate hedging practices in foreign exchange and currency risk

management. In addition, no prior research studies have been conducted on corporate

hedging in risk management in terms of the risk attributes of U.S. defense companies.

Therefore, research designed to examine the relationship between the risk attributes of

U.S. defense companies and corporate hedging in foreign exchange and currency risk

management markets is merited. The current study was applied to add to the

understanding of the determinants of corporate hedging in foreign exchange and currency

18

risk management at the organizational level. Furthermore, the results of the study have

the potential to trigger further research into this relationship.

Definitions

Agency costs. Agency costs are "costs caused by management's ability to pursue

its own interests at the expense of the firm's shareholders" (Stulz, 2003, p. 645).

Bankruptcy costs. Bankruptcy costs are "the costs incurred as a result of a

bankruptcy filing" (Stulz, 2003, p. 645).

Counterparty risks. Counterparty risks are "the risk that a counterparty fails to

deliver the promised payoff, either because of being financially unable to do so or for

other reasons" (Stulz, 2003, p. 647).

Convex function. According to Jensen's inequality (Azar, 2008), iff(x) is a

convex function and x is a random variable with nonzero variance, the expectation of the

transform of a random variable x by a convex function is larger than the transform of the

expectation of x, that is, E(/(x)) >y(E(x)) (Azar, 2008). A tax function for a given

company is a convex function (Smith & Stulz, 1985).

Convexity. A convexity is "a curve above a straight line connecting two end

points" (Harvey, n.d., p. 376). This curve is used to describe characteristics of a tax

function for a given company.

Corporate Hedging. Corporate hedging is "a component of a more general

process called risk management, the alignment of the actual level of risk with the desired

level of risk" in a company (Chance & Brooks, 2007, p. 355).

19

Currency risk. Currency risk is "the risk that currency exchange rates may

change adversely for a business that has exposure to foreign currency" (Stephens, 2001,

P- 8).

Default. Default is the failure to make interest and principal payments as agreed

to in a debt agreement based on the terms and at the designated time set (Penman, 2007).

Derivative. A derivative is "an instrument whose price depends on, or is derived

from, the price of another asset" (Hull, 2006, p. 747).

Economic risk. Economic risk is

The risk to the firm's present value of future operating cash flows from exchange

rate movements. In essence, economic risk concerns the effect of exchange rate

changes on revenues (domestic sales and exports) and operating expenses (cost of

domestic inputs and imports). Economic risk is usually applied to the present

value of future cash flow operations of a firm's parent company and foreign

subsidiaries. (Papaioannou, 2006, p. 131)

Empirical study. An empirical study is "a study using available market data and

observation to draw conclusion" (Hancock-Weise, 2011, p. 471).

Exchange rate. An exchange rate is "the rate at which a unit of one currency is

exchanged for another" (Whaley, 2006, p. 877).

Fair Value of Derivatives. Fair value of derivatives is recorded at market value

on the balance sheet, either an asset or liabilities (Penman, 2007).

Financial Accounting Standard No. 133 (FAS 133). FAS 133 is an accounting

standard that requires derivatives are reflected on the balance sheet at fair market value

20

for U.S. companies (Ramirez, 2007). FAS 133 was issued by the Financial Accounting

Standards Board (FASB).

Financial distress. Financial distress is "a low cash-flow state of the firm in

which it incurs deadweight losses without being insolvent" (Purnanandam, 2007, p. 706).

Financial leverage. Financial leverage is the degree to which a company funds

business operation and investment by debts (Chance & Brooks, 2007).

Financial risk. Financial risk is "the risk associated with changes in such factors

as interest rates, stock prices, commodity prices, and exchange rate" (Chance & Brooks,

2007, p. 627).

Foreign debt. Foreign debt is the debt denominated in foreign currency (Aabo,

2006).

Foreign exchange risk. Foreign exchange risk is

The likelihood that an unexpected change in exchange rates will alter the home

currency value of foreign currency cash payments expected from a foreign source.

Also, the likelihood that an unexpected change home currency needed to repay a

debt denominated in a foreign currency. (Eiteman et al., 2007, p. EM-37)

Foreign involvement. Foreign involvement ranges from simple import or export

activity to more complicated decisions including integrated global sourcing, production,

and competition (Eiteman et al., 2007).

Foreign tax credit. Foreign tax credit is "the amount by which a domestic firm

may reduce (credit) domestic income taxes for income tax payments to a foreign

government" (Eiteman et al., 2007, p. EM-37).

21

Form 10-K. Form 10-K is a report required by the U.S. SEC, in which a

comprehensive overview of a company's business and financial condition, including

audited financial statements, is provided (Penman, 2007).

Forward contract. Forward contract is "one party agrees to buy the underlying

from another party at maturity of the contract and pay for it then a price agreed upon

when the contract is originated with no cash changing hands before maturity" (Stulz,

2003, p. 648).

Future contract Future contract is "a contract traded on an exchange enabling

one party to buy for future delivery and another to sell for future delivery with gains and

losses settled daily" (Stulz, 2003, p. 649).

Hedge. Hedge is "a transaction in which an investor seeks to protect a position or

anticipated position in the spot market by using an opposite position in derivatives"

(Chance & Brooks, 2007, p. 628).

Hedge accounting. Hedge accounting is

A form of accounting for derivatives transactions in which certain transactions,

qualifying as hedges, are accounted for in such a manner that the gains or losses

from hedges are, to an extent, limited by specified rules, combined with gains and

losses from transactions they are designed to hedge, so as to minimize the impact

on reported earnings. (Chance & Brooks, 2007, p. 628-629)

Hedging costs. Hedging costs are "costs of putting on a hedge; examples include

transaction costs, monitoring costs, and design costs" (Stulz, 2003, p. 649).

22

Information asymmetry. When one party to a transaction has more or superior

knowledge and information, the other party does not. This informational disparity is

referred as information asymmetry (DaDalt, Gary, & Nam, 2002).

International Accounting Standard No. 39 (IAS 39). IAS 39 is an international

accounting standard that requires derivatives are reflected on the balance sheet at fair

market value for corporations (Ramirez, 2007). IAS 39 was issued by the International

Accounting Standard Board (IASB).

Managerial incentives. Managerial incentives are the variation in company

managers' total equity holdings as a result of increases in stock prices (Core, Guay, &

Larcker, 2003).

Marginal tax rate. Marginal tax rate is "the highest rate at which income is

taxed" (Penman, 2007, p. 313). In the U.S., "the marginal tax rate is usually the

maximum statutory tax rate for federal and state taxes combined" (Penman, 2007, p.

314).

Net operating loss (NOL) carryback. NOL carryback is an accounting

technique that applies the current year's net operating losses to past years' profits in order

to reduce tax liability (Penman, 2007)

NOL carryforward. NOL carryforward is an accounting technique that applies

the current year's net operating losses to future years' profits in order to reduce tax

liability (Penman, 2007).

Notional value of derivatives. Notional value of derivatives is "the quantity of

the underlying used to determine the payoff of the derivative" (Stulz, 2003, p. 650).

23

Option. Option is "a contract granting the right to buy or sell an asset, currency,

or futures at a fixed price for a specific time period" (Chance & Brooks, 2007, p. 633).

Progressive tax function. A progressive tax function is a convex function that

indicates marginal tax rates are increasing in taxable income, in which "the tax on the

average of two possible outcomes is less than the average of the tax reckoned on each

outcome individually" (Brennan, 2010, p. 2).

Risk aversion. Risk aversion is "the characteristic referring to an investor who

dislike risk and will not assume more risk without an additional return" (Chance &

Brooks, 2007, p. 636).

Risk management. Risk management is "the practice of identifying the risk

level a firm desires, identifying the risk level it currently has, and using derivative or

another financial instruments to adjust the actual risk level to the desired risk level"

(Chance & Brooks, 2007, p. 636).

Scale economies. Scale economies "constitute the relationship between the size

of a firm (or plant) and its costs of production in the broadest sense" (Stigler, 1983, p.

67).

Swap. Swap is "an agreement to exchange cash flows in the future according to a

prearranged formula" (Hull, 2006, p. 757).

Tax benefit. Tax benefit is an allowable deduction on a taxpayer's tax liability

(Penman, 2007).

Transaction risk. Transaction risk is

Cash flow risk and deals with the effect of exchange rate moves on transactional

account exposure related to receivables (export contracts), payables (import

24

contracts) or repatriation of dividends. An exchange rate change in the currency

of denomination of any such contract will result in a direct transaction exchange

rate risk to the firm. (Papaioannou, 2006, p. 131)

Translation risk. Translation risk is "balance sheet exchange rate risk and

relates exchange rate moves to the valuation of a foreign subsidiary and, in turn, to the

consolidation of a foreign subsidiary to the parent company's balance sheet"

(Papaioannou, 2006, p. 131).

Underinvestment problem. Underinvestment problem is characterized by "the

instances wherein companies are unable to fund profitable investments projects due to the

lack of adequate financing" (Salvary, 2005, p. 89).

Summary

The U.S. defense companies are exposed to financial risks resulting in millions of

dollars of lost profits as a result of corporate hedging practices in foreign exchange and

currency risk management markets. The purpose of this quantitative correlational study

was to examine the relationship between the risk attributes of U.S. defense companies

and corporate hedging in foreign exchange and currency risk management markets. The

seven constructed independent variables for the study were defined as (a) financial

distress, (b) underinvestment problems, (c) tax benefits, (d) managerial incentives, (e)

scale economies, (f) level of foreign involvement, and (g) revenues from U.S.

government contracts. The constructed dependent variable for the study was defined as

corporate hedging in foreign exchange and currency risk management markets. A

correlational design was used. The instruments to measure the independent variables

were debt ratio, income tax credit range, R&D spending, presence of corporate

25

executives' stock shares, firm size, foreign sale ratio, and sales to U.S. government. The

instrument for the dependent variable was the notional value of derivatives. The outcome

of the study was a contribution to the understanding of corporate hedging for the U.S.

defense companies and may be employed to help improve the effectiveness of strategic

thinking and decision-making for corporate hedging among U.S. defense companies in

foreign exchange and currency risk management markets. The need and purpose for the

study was established within this chapter; the theoretical framework, research questions,

hypotheses, research methods, nature of the study, and significance were summarized;

and definitions of key terms were provided.

26

Chapter 2: Literature Review

Company managers in the U.S. defense industry perform corporate hedging in

risk management on a regular basis, as documented in the annual financial reports (The

Boeing Company, 2009; Lockheed Martin Corporation, 2009). The problem addressed

within the study was that U.S. defense companies are exposed to financial risks resulting

in millions of dollars of lost profits as a result of corporate hedging practices in foreign

exchange and currency risk management markets (The Boeing Company, 2009; Chance

& Brooks, 2007; Eiteman et al., 2007; Gregory, 2010; Lockheed Martin Corporation,

2009; Stulz, 2003). Although the theoretical consideration and empirical evidence

indicated a range of factors that might influence corporate hedging, the relationship

between the risk attributes of U.S. defense companies and corporate hedging in foreign

exchange and currency risk management is not clear. The quantitative correlational study

was used to examine the relationship between the risk attributes of U.S. defense

companies and corporate hedging in foreign exchange and currency risk management

markets.

The literature search on corporate hedging in foreign exchange and currency risk

management was a significant step in the research process for the study. Since whether a

particular source would be cited in the literature review for the study was unknown, a

complete record of all of the bibliographic information from sources was developed for

the study. Search strategies for the study were to locate books that are currently accepted

reference texts in corporate hedging and find out who has cited the books in recent years

and to search original (seminal) journal papers and identify who has cited the papers in

recent years. Once information related to corporate hedging in foreign exchange and

27

currency risk management was located, the following step was to summarize the

information into a coherent literature review section for the study. To identify which

sources were applicable to the study and in what context sources were related to the

subject of the study, Booth, Colomb, and Williams (1995) suggested to become familiar

with the geography of the source, locate the point of the argument, identify key sub-

points, identify key themes, and skim paragraphs. Finally, literature material relevant to

corporate hedging in foreign exchange and currency risk management were focused

without spending time on the literature material that was at best only marginally related.

Most of references cited in the study are from books and peer-reviewed journals.

To assess the relationship between risk attributes and corporate hedging using

derivative instruments is a complex task (Artez & Bartram, 2010; Nguyen & Faff, 2010).

To measure the theoretical risk attributes as determinants of corporate hedging in foreign

exchange and currency risk management is difficult (Nguyen & Faff, 2010; Stulz, 2003).

The determinants of corporate hedging in foreign exchange and currency risk

management can differ across different industry sectors and companies with different

characteristics (Adam et al., 2007; Bartram et al., 2009; Lei, 2006; Papaioannou, 2006;

Rogers, 2002). Therefore, the theoretical discussions, the information from prior

empirical evidence, and the discussion of specific characteristics of the U.S. defense

industry were a theoretical framework upon which the study was built on.

In this chapter, the literature review begins with the importance of identifying

determinants of corporate hedging in risk management followed by the theoretical and

empirical research on corporate hedging in risk management pertaining to the constructs

for the study. In the literature review, theoretical discussions relevant to these constructs

28

are organized into sections to create a context for comprehension of the theoretical

rationale of corporate hedging and to help readers understand the study. In the final

review of literature, specific information and studies on corporate hedging in foreign

exchange and currency risk management are highlighted and followed by a summary of

the chapter.

Overview

Corporate hedging is the process that is used to reduce risk of loss against

negative outcomes within the capital market (Chance & Brooks, 2007). Corporate

hedging policy is a controversial subject in risk management (Stulz, 2003). By

facilitating the access of U.S. companies to international capital markets and enabling

U.S. companies to lower the cost of funds while diversifying the funding sources,

corporate hedging improves the position of U.S. companies in an expanding, competitive,

and global economy (Eiteman et al., 2007). However, the dramatic growth of corporate

hedging activities in risk management coupled with the derivatives-related losses has

resulted in millions of dollars of lost profits in U.S. companies (The Boeing Company,

2009; Chance & Brooks, 2007; Eiteman et al., 2007; Gregory, 2010; Lockheed Martin

Corporation, 2009; Stulz, 2003). The recent economic and financial crisis has further

accentuated the importance of understanding the incentives of corporate hedging

practices for U.S. companies. Identifying corporate hedging becomes an essential

component of corporate hedging strategy in risk management (Artez & Bartram, 2010;

Petersen & Thiagarajan, 2000; Stulz, 2003).

Theoretical and empirical researchers of corporate hedging in risk management

have focused on the question of what factors are used to justify corporate hedging

29

decisions when companies hedge a given risk (Artez & Bartram, 2010; Petersen &

Thiagarajan, 2000; Stulz, 2003). Viewed from a finance theory developed by Modigliani

and Miller (1958), corporate hedging policy is irrelevant in shareholder value creation.

However, characterized by corporate hedging theories, companies have incentives to

hedge (Artez & Bartram, 2010; Stulz, 2003). In the absence of capital market

perfections, the Modigliani and Miller (1958) framework does not hold (Eiteman et al.,

2007). Therefore, research studies, based on corporate hedging theories, were developed

to empirically test various factors to explain corporate hedging behavior in risk

management (Artez & Bartram, 2010; Stulz 2003). Despite extensive empirical research

studies in corporate hedging, the actual determinants of corporate hedging at the

organizational level remain uncertain (Artez & Bartram, 2010; Nguyen & Faff, 2010;

Stulz, 2003).

According to the Modigliani and Miller (1958) framework, perfect capital market

assumptions are no taxes, no transaction costs, no symmetric information between

company managers and shareholders, rational investors and markets, no costs of

bankruptcy, and aligned interests between company managers and shareholders. Under

these assumptions, corporate financing policy cannot be attributed to the shareholder

value creation because shareholders manage their own financial risks by holding well-

diversified portfolios (Modigliani & Miller, 1958). Corporate hedging policy is a

component of corporate financing policy because financial claims using derivative

instruments against a firm are involved (Stulz, 2003). Therefore, the Modigliani and

Miller (1958) framework can be extended to the application of corporate hedging

(Stiglitz, 1974). Under the perfect capital market assumptions defined by Modigliani and

Miller (1958), corporate hedging in foreign exchange and currency risk management is

irrelevant in value creation (Stiglitz, 1974). However, since the capital market is

imperfect, corporate hedging does matter in foreign exchange and currency risk

management (Artez & Bartram, 2010; Stulz 2003). Corporate hedging theories, based on

shareholder value maximization and managerial utility maximization, are utilized to

explain the reasons companies may require corporate hedging in a real financial world.

From the shareholder maximization theory, corporate hedging can be used to

reduce the various costs involved with future cash flows including costs of financial

distress, external financing, taxes, and underinvestment costs (Froot et al., 1993; Graham

& Smith, 1999; Smith & Stulz, 1985). First, corporate hedging can reduce the expected

transaction costs of financial distress by reducing the probability of incurring these costs

(Smith & Stulz, 1985). Second, since corporate tax expenses are a progressive tax

function to the taxable income of a company, corporate hedging can reduce the variability

of taxable income and the expected value of taxes (Graham & Smith, 1999; Smith &

Stulz, 1985). Third, corporate hedging ensures companies have sufficient internal funds

that enable the companies to mitigate unnecessary fluctuations in either investment

spending or costly external financing (Froot et al., 1993).

The primary theoretical alternative to the shareholder value maximization as a

corporate hedging theory is managerial utility maximization. From the managerial utility

maximization theory, company managers may seek to maximize their own self-interest at

the expense of shareholders because the company managers understand better than the

shareholders if the company's objectives the shareholders consider important can be met

(Jensen & Meckling, 1976). Furthermore, the company managers have the capability to

31

behave in their own self-interest rather than in the best interests of the shareholders

(Jensen & Meckling, 1976). Stulz (2003) indicated company managers have an incentive

to hedge their own wealth, which is aligned with the job performance at the expense of

the shareholders. Jensen and Meckling (1976) suggested the managerial compensation

policy can be "designed to give the manager incentives to select and implement actions

that increase shareholder wealth" (p. 226). Company managers may be interested in

protecting the company's profitability through corporate hedging in risk management

because of a possible change in corporate asset value (Shapiro, 2005). In addition,

company managers may have different risk preferences. The company managers are

essentially willing to consider risk-free prospects in financial decisions (Morellec &

Smith, 2007; Shapiro, 2005). Therefore, the company managers may be likely to be risk-

averse under uncertainty (Morellec & Smith, 2007; Shapiro, 2005).

Other possible justifications explore additional factors not well explained by the

corporate hedging theories. Jorion (1990) found the degree of foreign exchange and

currency risk exposure varies directly with the degree of foreign involvement and the

fluctuations of foreign exchange rate. Corporate hedging with financial derivatives was

found by Brown (2001) to depend on accounting reporting methods and foreign exchange

volatility. Judge (2006) indicated the level of foreign debt and foreign currency sales are

related to corporate hedging decisions.

According to Allayannis and Ofek (2001), large companies are more likely to

hedge than small companies. Market values of companies for derivative users are higher

than for non-users (Allayannis & Ofek, 2001). However, it was posited by Nance et al.

(1993) that smaller companies should hedge more than larger ones. Dolde and Mishra

(2007) argued the extent of information asymmetry about exposures of financial risks

between company managers and shareholders influences the likelihood of corporate

hedging. Firm value and corporate hedging have been reported to be significantly related

(Kapitsinas, 2008). Changes in reporting corporate hedging activities were documented

by Supanvanij and Strauss (2010) as having influenced the relationship between

executive compensation packages and use of financial derivatives. Furthermore, Adam,

Dasgupta, and Titman (2007) stated corporate hedging in financial risks depends on

industry-specific characteristics. Corporate governance mechanisms were demonstrated

by Lei (2006) and Marsden and Prevost (2005) as having an impact on the use of

financial derivatives in risk management. Finally, Bartram et al. (2009) and Marsden and

Prevost (2005) substantiated the legal support involvement in corporate hedging

decisions.

In summary, the theoretical area of interest for the study is determinants of

corporate hedging in risk management. Corporate hedging theories and empirical studies

of additional risk factors associated with corporate hedging are the foundation of the

study of the organizational determinants of hedging (Stulz 2003). The existing corporate

hedging literature indicated a range of factors that might influence corporate hedging

decisions in risk management (Artez & Bartram, 2010; Stulz 2003). If these factors do

matter in corporate hedging decisions, and if company managers could determine which

factors are critical to corporate hedging, the reduction of risks associated with corporate

hedging practices would be significant (Nguyen & Faff, 2010; Stulz, 2003).

Two main classes of theoretical explanations of why company managers engage

in corporate hedging practices are shareholder value maximization and managerial utility

33

maximization. Empirical studies have been applied in the exploration of additional

factors associated with corporate hedging in risk management, such as scale economies,

firm value, information asymmetry, level of foreign involvement, foreign debt, industry-

specific characteristics, country-specific characteristics, and account reporting methods

(Artez & Bartram, 2010; Stulz, 2003). Among the various company-specific factors

associated with corporate hedging in foreign exchange and currency risk management,

emphasis has been placed on financial distress, tax benefits, underinvestment problems,

managerial incentives, scale economies, and level of foreign involvement (Allayannis &

Ofek, 2001; Stulz, 2003). In spite of the fact that the theoretical and empirical evidence

on these company-specific determinants of corporate hedging are available, much

controversy remains about the effects of these company-specific determinants on

corporate hedging (Artez & Bartram, 2010; Nguyen & Faff, 2010; Stulz, 2003). In this

chapter, each of the company-specific determinants on corporate hedging in foreign

exchange and currency risk management will be presented with special reference to

corporate hedging in the U.S. defense industry, which applies to the study.

Financial Distress

Financial distress can impose significant costs on a company (Andrede & Kaplan,

1998; Korteweg, 2006). Companies that are significantly exposed to the exchange rate

fluctuations would derive benefits from corporate hedging because corporate hedging

reduces the costs of financial distress such as default and bankruptcy costs (Smith &

Stulz, 1985). Shareholders will be interested in corporate hedging to reduce the

probability of financial distress (Stulz, 2003). The costs of financial distress include not

only litigation expenses such as lawyer's and court fees and direct bankruptcy costs

(Andrede & Kaplan, 1998; Warner, 1977; Weiss, 1990), but less quantifiable effects of

financial trouble such as damage to the company's reputation, the loss of key employees

and customers, and the loss of value from foregone investment opportunities (Andrede &

Kaplan, 1998; Korteweg, 2006).

Warner (1977) and Weiss (1990) estimated the direct costs of litigation fees and

bankruptcy to be about 3 to 5% of total firm value at the time of financial distress.

However, a far greater consequence is the costs stemming from customers who are

reluctant to buy from a distressed company, high-quality employees who leave, company

managers who are distracted from running the business because of financing distress, and

potential investment opportunities that are missed because of insufficient capital funds

(Andrede & Kaplan, 1998; Korteweg, 2006). Andrede and Kaplan (1998) found the total

loss in firm value attributable to financial distress in the range of 10 to 23% of pre-

distress firm value. Korteweg (2006) stated the costs of financial distress are 31% of firm

value on average across industries if companies are at bankruptcy and the equity of a

company is zero. Since financial distress is costly to a company, a company has an

incentive to hedge the exposure of financial risks by reducing the costs of financial

distress. As such, "firms with a high probability of default and/or high financial distress

costs should be more likely to engage in corporate hedging" (Artez & Bartram, 2010, p.

348).

The magnitude of the costs of financial distress can be defined by the size and

exposure of a company's financial leverage (Geczy, Minton, & Schrand, 1997). A

company's financial leverage is the degree to which a company funds business operation

and investment by debts (Chance & Brooks, 2007). As payments of debts and interest

35

constitute obligations the debtholders are legally entitled to, debts put pressure on the

company. A distressed company more likely experiences difficulties of the payments of

debts and interest (Smith & Stulz, 1985). If the company does not meet the financial

obligations in time, financial distress occurs, followed by default and bankruptcy.

Therefore, the higher levered company with debts might have a strong incentive to hedge

(Geczy et al., 1997; Smith & Stulz, 1985).

Graham and Rogers (2002) illustrated companies with higher financial leverage in

long-term debt will typically hedge with foreign currency derivatives. Corporate hedging

may increase debt capacity and the present value of the tax benefits (Graham & Rogers,

2002). However, a large amount of debt may also increase the degree of financial

distress and probability of default and bankruptcy, which in turn may increase the

incentive for companies to hedge (Graham & Rogers, 2002). Nguyen and Faff (2003)

analyzed a sample of469 Australian nonfinancial companies and confirmed companies

with debts in the capital structure are more likely to hedge foreign currency risk

exposure. From a sample of 493 U.S. nonfinancial companies with sales exceeding $1

billion, Dolde and Mishra (2007) supported a strong positive relationship between

financial leverage and use of derivative instruments exists at the corporate level in

foreign exchange and currency risk management. Spano (2008) collected annual

financial data from 443 nonfinancial companies in United Kingdom and affirmed the

higher levered companies intend to hedge. The findings from these empirical studies are

consistent with Smith and Stulz's (1985) theory.

However, empirical results on costs of financial distress and corporate hedging

are varied. A large number of recent empirical studies confirmed financial leverage is

36

significantly positive related to corporate hedging (Bartram et al., 2009; Berkman, 2002;

Berrospide et al., 2007; Dolde & Mishra, 2007; Graham & Rogers, 2002; Haushalter,

2000; Lei, 2006; Nguyen & Faff, 2003; Reynolds et al., 2009; Schiozer & Saito, 2009;

Spand, 2008). In contrast, Allayannis and Ofek (2001) suggested the relationship

between financial leverage and corporate hedging is positively insignificant. Davies et al.

(2006) and SprCic (2007) indicated no evidence is found to support financial leverage is

an explanatory factor for corporate hedging. Hagelin (2003) and Hagelin, Holmen,

Knopf, and Pramborg (2007) stated financial leverage is negatively associated with

corporate hedging. Judge (2006) further acknowledged financial leverage with the level

of debt is not a good measure for costs of financial distress.

According to the Standard & Poor's industry survey for aerospace and defense

industries, a 30-year average debt ratio is about 60% in the defense industry, and the debt

ratio is widely varied among U.S. defense companies (Tortoriello, 2011). The U.S.

defense companies with foreign subsidiaries or U.S. defense companies that hold foreign

debts or foreign currencies are more susceptible to financial distress because of high

financial leverage. As a result, financial leverage may vary directly with corporate

hedging in U.S. defense industry.

Financial distress is one of the key elements in shareholder value maximization

theory used to explain corporate hedging (Smith & Stulz, 1985). Both theoretically and

empirically, financial distress can impose significant costs on a company (Andrede &

Kaplan, 1998; Korteweg, 2006; Warner, 1977; Weiss, 1990). Companies that face

greater risk of financial distress with the implicit and explicit costs contained may benefit

from corporate hedging (Artez & Bartram, 2010). Through corporate hedging, reduction

37

in the probability of financial distress will result in improvement of a company's ability

to increase financial leverage (Graham & Rogers, 2002). However, high financial

leverage increases the degree of financial distress and probability of default and

bankruptcy, which in turn increases the incentive for companies to hedge (Smith & Stulz,

1985).

Despite the theoretical analysis of financial distress, empirical results on the

relationship between costs of financial distress and corporate hedging are not without

ambiguity. Highly levered U.S. companies are more susceptible to financial distress.

Therefore, financial leverage in U.S. defense companies may be directly related to

corporate hedging decisions in foreign exchange and currency risk management (Geczy

et al. 1997; Graham & Rogers, 2002; Smith & Stulz, 1985).

While high debt capacity for a company increases, a degree of financial distress

and probability of default and bankruptcy increases (Graham & Rogers, 2002). Debts

also have tax advantages because the interest payments are made from pre-tax earnings

(Penman, 2007; Smith & Stulz, 1985). As such, the question exists whether tax benefits

are related to corporate hedging decisions in risk management situations.

Tax Benefits

A progressive tax is convex (Smith & Stulz, 1985). The principle of progressivity

is reflected in much of the U.S. tax system (Graham & Smith, 1999; Smith & Stulz,

1985). Corporate marginal tax rates vary as a convex function of the level of taxable

income in the U.S. (Graham & Smith, 1999; Smith & Stulz, 1985). Companies pay a

higher corporate marginal tax rate at higher levels of total taxable income. Therefore, the

U.S. tax system has significant convexity (Graham & Smith, 1999; Smith & Stulz, 1985).

38

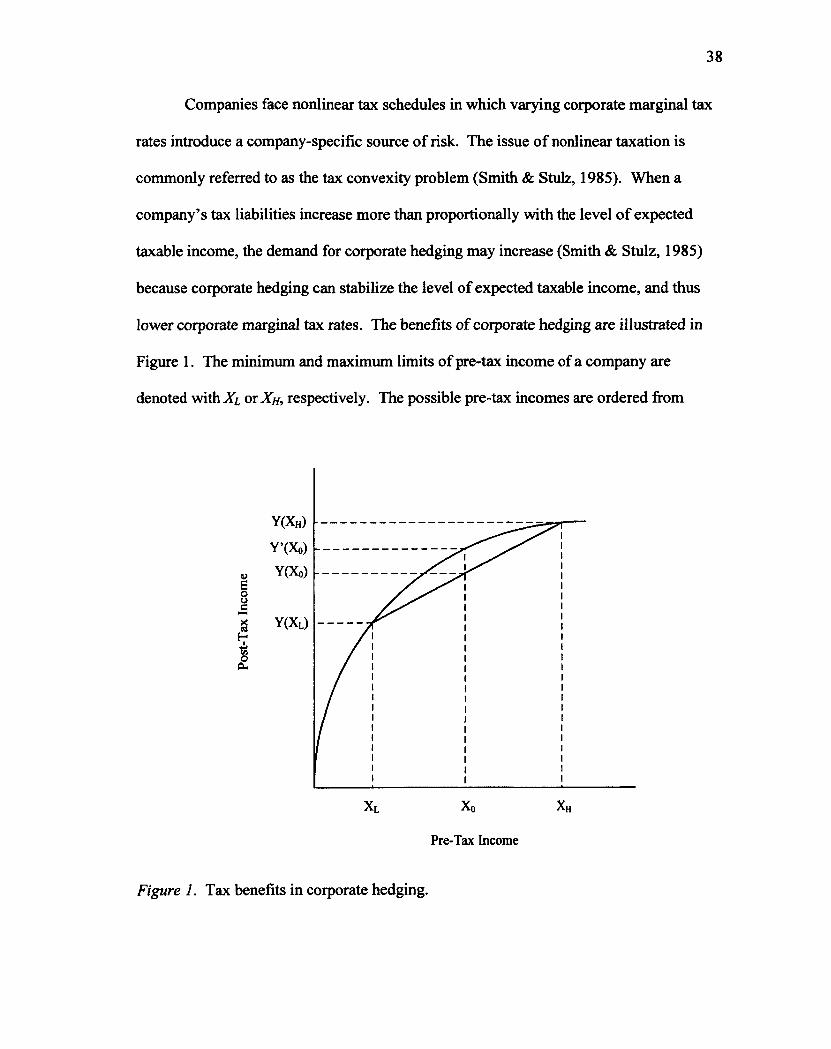

Companies face nonlinear tax schedules in which varying corporate marginal tax

rates introduce a company-specific source of risk. The issue of nonlinear taxation is

commonly referred to as the tax convexity problem (Smith & Stulz, 1985). When a

company's tax liabilities increase more than proportionally with the level of expected

taxable income, the demand for corporate hedging may increase (Smith & Stulz, 1985)

because corporate hedging can stabilize the level of expected taxable income, and thus

lower corporate marginal tax rates. The benefits of corporate hedging are illustrated in

Figure 1. The minimum and maximum limits of pre-tax income of a company are

denoted with Xi or XH, respectively. The possible pre-tax incomes are ordered from

Y(X„)

Y'(Xo)

u Y(Xo)

XL