exchange bulletin - cboe.org · letin, including the regulatory bulletin ... triad hospitals, inc....

TRANSCRIPT

CLASS BID OFFER LASTSALEAMOUNT LASTSALEDATE

CBOE $2,525,000.00 $2,700,000.00 $2,600,000.00 July26,2007

CBOTFULLMEMBERSHIP(WITHOUTSTOCK)

CLASS BID OFFER LASTSALEAMOUNT LASTSALEDATE

WithERP $925,000.00 $995,000.00 $1,000,000.00 July23,2007

WithoutERP $675,000.00 $770,000.00 $640,000.00 June8,2007

ERP $240,000.00 $276,000.00 $270,000.00 July25,2007

ExchangeBulletinJuly27,2007Volume35,Number30

The Constitution and Rules of the Chicago Board Options Exchange, Incorporated (“Exchange”), in certain specific instances, requiretheExchangetoprovidenoticetotheExchangemembership.Tosatisfythisrequirement,acopyoftheExchangeBul-letin,includingtheRegulatoryBulletin,isdeliveredbye-mailfreeofchargeorbyhardcopyforafeetoalleffectivemembersonaweeklybasis.

MembersareencouragedtoreceivetheExchangeandRegulatoryBulletinandInformationCircularsviae-mail.E-mailsubscrip-tions may be obtained by submitting your name, firm if applicable, e-mail address, and phone number, to [email protected]. Thereisnochargefore-maildeliveryoftheExchangeandRegulatoryBulletinorforInformationCirculars.Ifyoudosignupfore-maildelivery,pleaseremembertoinformtheMembershipDepartmentofe-mailaddresschanges.

Subscriptions for hard copy delivery may be obtained by submitting your name, firm if any, mailing address and telephone num-berto:ChicagoBoardOptionsExchange,AccountingDepartment,400SouthLaSalle,Chicago,Illinois60605,Attention:BulletinSubscriptions.Thecostofanannualsubscription(January1throughDecember31)is$200.00($100.00afterJuly1),payableinadvance.

Forup-to-dateSeatMarketQuotes,call1-877-THE-CBOEandselectchoice3fromthemainmenu,or,visitwww.CBOE.org,click“CBOEMemberSite”andthen“SeatMarketInformation”onthefollowingpage.ForaccesstotheCBOEMemberWebSite,pleasealso notify the Membership Department by sending an e-mail to [email protected] or by phone at 312-786-7449.

Copyright©2007ChicagoBoardOptionsExchange,Incorporated

SEATMARKETQUOTESASOFFriday,July27,2007

CBOEMEMBERSHIPSALESANDTRANSFERSFrom To Price/Transfer DateNorman T. Hovda Patman Transfer 7/19/07 BurtR.Bondy CoasttoCoast,LLC Transfer 7/23/07Susquehanna Investment Group Infinium Capital Management, LLC $2,650,000.00 7/24/07MontR.Wickham UrbanaCorporation $2,650,000.00 7/26/07DRCCorporation DRCTradingCorporation Transfer 7/26/07SusquehannaInvestmentGroup SusanSolwaySiegel $2,650,000.00 7/26/07SusquehannaInvestmentGroup UrbanaCorporation $2,650,000.00 7/26/07PeterG.Nolan CitadelDerivativesGroup,LLC $2,600,000.00 7/26/07

CBOEMEMBERSHIPSALESANDTRANSFERSFrom To Price/Transfer Date

Page � July �7, �007 Volume 35, Number 30 Chicago Board Options Exchange

MEMBERSHIPAPPLICATIONSRECEIVEDFORWHICHAPOSTINGPERIODISREQUIRED

IndividualMembershipApplicants DatePosted

Jonathan P. Dempsey, Nominee 7/19/07EquitecRS,LLC1200W.MonroeSt.Chicago,IL60607

JustinA.Weiss,Nominee 7/24/07ConsolidatedTrading,LLC1130NorthDearborn,Apt.3307Chicago,IL60610

ChristopherT.Bilotti,Nominee 7/25/07WolverineExecutionServices,LLC309ForestAvenueGlenEllyn,IL60137

JoshuaP.Winter,Nominee 7/25/07WolverineTrading,LLC1512N.Sedgwick,#1Chicago,IL60604

MemberOrganizationApplicants DatePosted

MacatawaTrading,LLC 7/25/07LanceS.O’Donnell,Nominee338KenilworthAvenueKenilworth,IL60043LanceS.O’Donnell-MemberMEMBERSHIPLEASES

NewLeases EffectiveDate

Lessor: Alanna R. Arenstein 7/19/07Lessee: LanceS.O’DonnellRate: 0.25%Term:Monthly

Lessor: Consolidated Trading, LLC 7/19/07Lessee: HurricaneCapital,LLCRate: 0.25%Term:1Day

Lessor: PatMan 7/19/07Lessee: RoninCapital,LLC MichaelG.Barwacz,NOMINEERate: 0.2494%Term:Monthly

Lessor: Vincent J. Viola 7/19/07Lessee: EWT,LLCRate: $6,300Term:Monthly

Lessor: Vincent J. Viola 7/19/07Lessee: EWT,LLCRate: $6,300Term:Monthly

Lessor: Vincent J. Viola 7/19/07Lessee: EWT,LLCRate: $6,300Term:Monthly

Lessor: Vincent J. Viola 7/19/07Lessee: EWT,LLCRate: $6,300Term:Monthly

Lessor: ConsolidatedTrading,LLC 7/20/07Lessee: BruceA.WilliamsRate: 0.25%Term:1Day

EffectiveDate

Lessor: SusquehannaInvestmentGroup 7/23/07Lessee: SusquehannaSecuritiesRate: 0.25%Term:Monthly

Lessor: INGFinancialMarkets,LLC 7/23/07Lessee: TJMProprietaryTrading,LLCRate: 0.25%Term:Monthly

Lessor: CoasttoCoast,LLC 7/23/07Lessee: WolverineTrading,LLC EoinT.Callery,NOMINEERate: 0.2494%Term:Monthly

TerminatedLeases TerminationDate

Lessor: Norman T. Hovda 7/19/07Lessee: RoninCapital,LLC MichaelG.Barwacz(SYZ),NOMINEE

Lessor: Scott H. Arenstein 7/19/07Lessee: LanceS.O’Donnell(LSO)

Lessor: ConsolidatedTrading,LLC 7/20/07Lessee: HurricaneCapital,LLC StephenK.Fox(FOX),NOMINEE

Lessor: BurtR.Bondy 7/23/07Lessee: WolverineTrading,LLC EoinT.Callery(DUB),NOMINEE

Lessor: INGFinancialMarkets,LLC 7/23/07Lessee: SusquehannaSecurities

Lessor: ConsolidatedTrading,LLC 7/23/07Lessee: BruceA.Williams(BAW)

MEMBERSHIPTERMINATIONS

IndividualMembers

TemporaryMember: TerminationDate

William C. Floersch (WCF) 7/19/07FortisClearingAmericas,LLC

Lessee(s): TerminationDate

BruceA.Williams(BAW) 7/23/07

Lessor(s): TerminationDate

Scott H. Arenstein 7/19/07

Norman T. Hovda 7/19/07

Nominee(s)/InactiveNominee(s): TerminationDate

Matthew P. O’Connell (MOC) 7/19/07TradeLink,LLC

StephenK.Fox(FOX) 7/20/07HurricaneCapital,LLC

StevenA.Williams(STE) 7/25/07MOGCapital,LLC

MEMBERSHIPINFORMATIONFOR7/19/07THROUGH7/25/07

Page 3 July �7, �007 Volume 35, Number 30 Chicago Board Options Exchange

EFFECTIVEMEMBERSHIPS

IndividualMembers

Lessee(s): EffectiveDate

BruceA.Williams(BAW) 7/20/07OptiverUS,LLCTypeofBusinesstobeConducted:MarketMaker

Lessor(s): EffectiveDate

Alanna R. Arenstein 7/19/07

Vincent J. Viola 7/19/07

David Salomon 7/19/07

Nominee(s)/InactiveNominee(s): EffectiveDate

Thomas Pologruto 7/19/07MerrillLynchProfessionalClearingCorp.TypeofBusinesstobeConducted:RemoteMarketMaker

Stephen K. Fox (FOX) 7/19/07HurricaneCapital,LLCTypeofBusinesstobeConducted:MarketMaker

MarkP.Corman 7/23/07TJMProprietaryTrading,LLCTypeofBusinesstobeConducted:RemoteMarketMaker

JeffreyW.Sieck(JWS) 7/23/07EquitecStructuredProducts,LLCTypeofBusinesstobeConducted:FloorBroker

JamesJ.Buckley(JJB) 7/24/07OptiverUS,LLCTypeofBusinesstobeConducted:RemoteMarketMaker

StephenG.Berman 7/25/07MOGCapital,LLCTypeofBusinesstobeConducted:RemoteMarketMaker

TrentS.Cutler 7/25/07CutlerGroup,LPTypeofBusinesstobeConducted:RemoteMarketMaker

MemberOrganizations

Lessor(s): EffectiveDate

PatMan 7/19/07

CoasttoCoast,LLC 7/23/07

JOINTACCOUNTSCHANGESINMEMBERSHIPSTATUS

IndividualMembers EffectiveDate

JohnM.TobiasIII 7/25/07From: TemporaryMemberforSpartaGroupOf Chicago,LP;MarketMakerTo: TemporaryMemberforCassandraTrading Group,LLC;MarketMaker

MemberOrganizations EffectiveDate

EWT, LLC 7/19/07From: Owner;AssociatedwithaMarketMaker/ RemoteMarketMakerTo: Lessee;AssociatedwithaMarketMaker/Remote MarketMaker

Fortis Clearing Americas, LLC 7/19/07From: Lessee/Non-MemberCustomerBusiness/Member Organization Affiliated with a Temporary Member / OrderServiceFirm;AssociatedwithaMarketMaker/ FloorBrokerTo: Lessee/Non-MemberCustomerBusiness/Order ServiceFirm;AssociatedwithaMarketMaker/ FloorBroker

MEMBERNAMECHANGES

MemberOrganizations EffectiveDate

From: ADPClearing&OutsourcingServices,Inc.7/20/07To: RidgeClearing&OutsourcingSolutions,Inc.

Page � July �7, �007 Volume 35, Number 30 Chicago Board Options Exchange

RESEARCHCIRCULARSThefollowingResearchCircularsweredistributedbetweenJuly20andJuly26,2007.Ifyouwishtoreadtheentiredocument,pleaserefertotheCBOEwebsiteatwww.cboe.comandclickonthe“TradingTools”Tab.NewlistingsandseriesinformationisalsoavailableintheTradingToolssectionofthewebsite.ForquestionsregardinginformationdiscussedinaResearchCircular,pleasecallTheOptionsClearingCorporationat1-888-OPTIONS.

ResearchCircular#RS07-618July25,2007AngloAmericanplc(“AAUK/QEB”)Demerger/ShareConsolidationandReverseSplit**RevisedCashAmount**

ResearchCircular#RS07-620July24,2007AdvancedMagnetics,Inc.(“AMAG/AVM”)NameChangeto:AMAGPharmaceuticals,Inc.EffectiveDate:July25,2007

ResearchCircular#RS07-621July25,2007AngloAmericanplc(“AAUK/QEB”)Demerger/ShareConsolidationandReverseSplit**RevisedCashAmount–Approximate**

ResearchCircular#RS07-622July25,2007TriadHospitals,Inc.(“TRI/OUV/WXG”)MergerCOMPLETEDwithCommunityHealthSystems,Inc.(“CYH”)-CashSettlement

ResearchCircular#RS07-624July25,2007*****UPDATE-Ex”ContingentDividendDateCONFIRMED*****FloridaEastCoastIndustries,Inc.(“FLA”)CONTRACTADJUSTMENTFORSPECIALCASHDIVIDEND“Ex”ContingentDividendDate:July26,2007ResearchCircular#RS07-625July25,2006SiliconwarePrecisionIndustriesCo.,Ltd.(“SPIL/QSP/ZLN”)1.972871367%ADSDividendEx-DistributionDate:July27,2007

ResearchCircular#RS07-627July20,2007***UPDATE–RevisedEx-DistributionDate***NovaStarFinancial,Inc.(“NFI/OZA”)1-for-4ReverseStockSplitEx-DistributionDate:July30,2007

ResearchCircular#RS07-629July26,2007FloridaEastCoastIndustries,Inc.(“FLA”)MergerCOMPLETEDwithFortressInvestmentGroupLLC

ResearchCircular#RS07-605July20,2007TheBISYSGroup,Inc.(“BSG/OSY”)ProposedMergerwithCitibankN.A.

ResearchCircular#RS07-606July20,2007NovaStarFinancial,Inc.(“NFI/OZA”)1-for-4ReverseStockSplitEx-DistributionDate:July27,2007

ResearchCircular#RS07-607July20,2007Aeroflex Incorporated (“ARXX/ARX”) Proposed MergerwithAXHoldingCorp.

ResearchCircular#RS07-608July20,2007FloridaEastCoastIndustries,Inc.(“FLA”)ProposedMergerwithFortressInvestmentGroupLLC

ResearchCircular#RS07-609July20,2007StationCasinos,Inc.(“STN/OXD/WCE”)ProposedMergerwithFertittaColonyPartnersLLC

ResearchCircular#RS07-611July20,2007WildOatsMarkets,Inc.(“OATS/QOQ/ZAC/LMJ”)TenderOfferFURTHEREXTENDEDbyWFMIMergerCo.

ResearchCircular#RS07-612July20,2007AllianceDataSystemsCorporation(“ADS”)ProposedMergerwithAladdinHoldco,Inc.

ResearchCircular#RS07-613July20,2007***UPDATE-ANTICIPATEDMERGEREFFECTIVEDATE-AU-GUST1,2007***TheBISYSGroup,Inc.(“BSG/OSY”)ProposedMergerwithCitibankN.A.

ResearchCircular#RS07-614July20,2007FloridaEastCoastIndustries,Inc.(“FLA”)CONTRACTADJUSTMENTFORSPECIALCASHDIVIDENDAnticipated“Ex”ContingentDividendDate:July26,2007ResearchCircular#RS07-615July23,2007***UPDATE-ANTICIPATEDMERGEREFFECTIVEDATE-JULY26,2007***FloridaEastCoastIndustries,Inc.(“FLA”)ProposedMergerwithFortressInvestmentGroupLLC

POSITIONLIMITCIRCULARSPursuanttoExchangeRule4.11,theExchangeissuedthebelowlistedPositionLimitCircularsonJuly27,2007.ThecompletecircularsareavailablefromtheDepartmentofMarketRegulation,inthedatainformationbinsonthe2ndFlooroftheExchange,andontheCBOEwebsiteatcboe.comunderthe“MarketData”tab.

Toreceiveregularupdatesofthepositionlimitlistviafax,contactCandiceNickrandat(312)786-7730.QuestionsconcerningpositionandexerciselimitsmaybedirectedtotheDepartmentofMarketRegulationtoJoeAcevedoat(312)786-7602orTimMacDonaldat(312)786-7706.

PositionLimitCircularPL07-32July27,2007PositionandExerciseLimitswillbedecreasedtoaLowerTierLimitEffectiveAugust20,2007

PositionLimitCircularPL07-33July27,2007AdjustedPositionandExerciseLimitsforacertainEquityOptionClasswillreverttoitsApplicableStandardPositionandExerciseLimiteffectiveAugust20,2007

August 1, 2007 Volume RB18, Number 31 ____________________________________________________________________________________

The Constitution and Rules of the Chicago Board Options Exchange, Incorporated (“Exchange”), in certain specific instances, require the Exchange to provide notice to the membership. The weekly Regulatory Bulletin is delivered to all effective members to satisfy this requirement. Copyright © 2007 Chicago Board Options Exchange, Incorporated. ____________________________________________________________________________________

REGULATORY CIRCULARS ____________________________________________________________________________________________ RG07-78 – INTER-EXCHANGE PROCEDURES IN VOLATILE MARKETS FOR THIRD QUARTER 2007

August 1, 2007 Volume RB18, Number 31 1

When the NYA advances (or declines) 190 points from the previous day's close: Index arbitrage orders for S&P 500® component stocks must be entered with buy-minus (or sell-plus) instruction until the advance or decline returns to within 90 points from previous day's close.

1350 DJIA POINTS (10%) BELOW PREVIOUS DAY'S

CLOSING VALUE

Trading halts: Trading in all stocks halts for the following time periods when the DJIA reaches this value at the following times:

Before 1:00 p.m.: for one hour;From 1:00 p.m. but before 1:30 p.m.: for 30 minutes;From and after 1:30 p.m.: no mandated trading halt

Limit comes into effect: On CBOT open-ing (7:20 a.m.).

Trading halt: If the futures contract is limit offered during an NYSE trading halt, futures trading will halt until NYSE ends its trading halt and 50% of the underly-ing stocks (capitalization weighted) have resumed trading.

Limit no longer in effect: After futures trading has resumed following an NYSE trading halt or at 1:30 p.m.

1350 POINTS (10%) BELOW PREVIOUS DAY'S

SETTLEMENTBecause CME or CBOT limit is reached: None required; discretionary actions include trading halts and suspensions (with the exercise restrictions described above).

Because NYSE declares floor-wide circuit breaker halt: Trading in all CBOE securities halted during NYSE circuit breaker halt (with the exercise restrictions described above).

None required because of CME or CBOT limit or NYSE actions; discretionary actions include trading halts and suspensions.

Except on the last business day before their expiration, CBOE normally will restrict exercise of American style, cash settled index options during any trading halt that occurs prior to 3:00 p.m. CBOE may restrict exercise in equity options (other than during the 10 business days before their expiration), but it normally will not do so because of trading halts.

None required.

Regulatory Circular RG07-78(supersedes Regulatory Circular RG07-44)

INTER-EXCHANGE PROCEDURES IN VOLATILE MARKETS FOR THIRD QUARTER 2007

As of July 1, 2007

(OVER)

75 POINTS (5%) BELOW PREVIOUS DAY’S SETTLEMENT

Limit comes into effect: On CME opening (8:30 a.m.)

Trading halt: For 2 minutes if the offer is at limit 10 minutes after limit is reached or at 2:30 p.m. Limit no longer in effect: After the 2 minute halt or, if no halt, 10 minutes after the limit is reached or otherwise at 2:30 p.m.

150 POINTS (10%) BELOWPREVIOUS DAY'S SETTLEMENT

Under Normal Limits

Limit comes into effect: After the 75 point (5%) limit or at 2:30 p.m.

Trading halts: Trading will halt for the follow-ing time periods if the futures contract is limit offered under the following circumstances:

During an NYSE trading halt: Until NYSE ends its trading halt and 50% of the underlying stocks (capitalization weighted) have resumed trading.

After 1:30 p.m., if no NYSE trading halt is declared: For 2 minutes if the contract is limit offered 10 minutes after the limit is reached.

Limit no longer in effect: After a mandated futures trading halt.

******

Under Second Day Limits (those appli-cable on a day after the futures contract was limit offered at the 300 point (20%) level at the close of trading).

Limit comes into effect: After the 75 point (5%) limit, unless there is an NYSE trading halt, in which case only the 20% limit applies upon reopening.

Trading halts:

During an NYSE trading halt (regardless whether the futures con-tract is limit offered): Until NYSE ends its trading halt and 50% of the underlying stocks (capitalization weighted) have resumed trading.

If no NYSE trading halt is declared: For 2 minutes if the contract is limit offered 10 minutes after the limit is reached or at 2:30 p.m.

Limit no longer in effect: After a mandated futures trading halt or, if no halt, 10 minutes after the limit is reached or otherwise at 2:30 p.m.

CME (S&P 500® FUTURES) NYSE ACTION CBOT (DJIASM FUTURES) CBOE ACTION

Discretionary actions include trading halts in individual stocks.

This information has been compiled by CBOE for general information purposes only, and therefore should not be considered complete or precise. Most matters discussed are subject to detailed exchange rules and to the discretion of exchange officials. The rules of the various exchanges are subject to change and may not be reflected in this information. CBOE assumes no responsibility for any errors or omissions in the information presented. In addition, this circular does not address specialized circumstances, such as the times that would be applicable on days when one or more underlying equity markets is scheduled to close trading earlier than normal or the rules applicable to Chapter 30 securities. These specialized matters are covered in detail by exchange rules. All times listed are Central times. “S&P” and “S&P 500” are trademarks of Mc-Graw Hill, Inc., and "DJIA" is a service mark of Dow Jones & Company, Inc., and neither company assumes any liability in connection with the trading of any contract based on its indexes.

(Date of issuance: July 23, 2007)

CME (S&P 500 FUTURES) NYSE ACTION CBOT (DJIA FUTURES) CBOE ACTION

Regulatory Circular RG07-78As of 07/01/07

Under Normal Limits

Limit comes into effect: After the 150 point (10%) limit.

Trading halts: For 2 minutes if the contract is at limit 10 minutes after limit is reached.

Limit no longer in effect: After any such 2 minute halt.

******

Under Second Day Limits

Limit comes into effect: After the 150 point (10%) limit, unless there is an NYSE trading halt, in which case only the 20% limit applies upon reopening.

Trading halts:

During an NYSE trading halt (regardless whether the futures contract is limit offered): Until NYSE ends its trading halt and 50% of the underlying stocks (capitalization weighted) have resumed trading.

If no NYSE trading halt is declared: For 2 minutes if the contract is limit offered 10 minutes after the limit is reached or at 2:30 p.m.

Limit no longer in effect: After a man-dated futures trading halt or, if no halt, 10 minutes after the limit is reached or otherwise at 2:30 p.m.

For more information, call 1-888-OPTIONS or visit our Web site at www.cboe.com

4050 DJIA POINTS (30%) BELOW PREVIOUS DAY'S

CLOSING VALUE

Trading halts and does not reopen for the day.

The 300 point (20%) limit remains in effect.

Settlement value will not be less than the limit value, regardless of the value of the cash index.

Limit comes into effect: After the 2700 point (20%) limit.

Limit remains in effect for the remainder of the trading day.

Trading halt: Trading shall halt for the rest of the day if the futures contract is limit offered at any time during the trading day and the NYSE declares a trading halt for the rest of the trading day.

4050 POINTS (30%) BELOW PREVIOUS DAY'S

SETTLEMENT

If NYSE declares floor wide trading halt for the remainder of the day: CBOE halts trading for the remainder of the day (with the exercise restrictions described above).

Because CBOT limit is reached: None required; discretionary actions include trading halts and suspensions (with the exercise restrictions described above).

2700 DJIA POINTS (20%) BELOW PREVIOUS DAY'S

CLOSING VALUE

Trading halts: Trading in all stocks halts for the following time periods when the DJIA reaches this value at the following times:

Before 12:00 p.m.: for two hoursFrom 12:00 p.m. but before 1:00 p.m.: for one hourFrom and after 1:00 p.m.: for the remainder of the day

Limit comes into effect: After the 1350 point (10%) limit or at 1:30 p.m.

Trading halt: If the futures contract is limit offered during an NYSE trading halt, futures trading will halt until NYSE ends its trading halt and 50% of the underly-ing stocks (capitalization weighted) have resumed trading.

Limit no longer in effect: After futures trading has resumed following an NYSE trading halt.

Because CME or CBOT limit is reached: None required; discretionary actions include trading halts and suspen-sions (with the exercise restrictions described above).

Because NYSE declares a floor wide circuit breaker halt: Trading in all CBOE securities halted during NYSE circuit breaker halt (with the exercise restrictions described above).

2700 POINTS (20%) BELOW PREVIOUS DAY'S

SETTLEMENT

INTER-EXCHANGE PROCEDURES IN VOLATILE MARKETS(continued)

225 POINTS (15%) BELOW PREVIOUS DAY'S

CLOSING VALUE

Limit comes into effect: After the 225point (15%) limit or, when Second Day Limits are in effect, at 2:30 p.m. or after trading resumes following an NYSE trading halt.

Limit remains in effect for the remainder of the trading day.

Trading halt:

(Normal Limits): If the futures contract is limit offered during an NYSE trading halt.

(Second Day Limits): If there is an NYSE trading halt, regardless whether the futures contract is limit offered.

Trading will resume when NYSE ends its trading halt and 50% of the underly-ing stocks (capitalization weighted) have resumed trading.

Settlement value will not be less than the limit value, regardless of the value of the cash index.

300 POINTS (20%) BELOWPREVIOUS DAY'S

SETTLEMENT

None required; discretionary actions in-clude trading halts in individual stocks.

None required; discretionary actions include trading halts and suspensions (with the exercise restrictions described above).

August 1, 2007 Volume RB18, Number 31 3

CBOE Regulatory Circular RG07-79 Date: July 25, 2007 To: Members and Member Firms From: CBOE Research and Product Development Subject: New Product Launch on July 31, 2007:

Basket Credit Event Binary Options OVERVIEW On July 31, 2007, CBOE plans to commence trading Basket Credit Event Binary Options ("Basket CEBOs"). Below are some features of the proposed Basket CEBOs:

• Basket CEBOs pay out a cash settlement amount upon the confirmation of a Credit Event in one, some or all of the Basket Components. Each Basket Component pays a predetermined settlement value, based on the recovery rate specified for that component, to the option holder upon the confirmation of a Credit Event (e.g., bankruptcy or failure-to-pay) in a Basket Component (i.e., debt issuer or guarantor) and $0 if there is no Credit Event prior to the Last Trading Day.

• Basket CEBOs will continue to trade after a Credit Event has been confirmed, unless

there are no remaining Basket Components. Holders, as of the close of the confirmation date of the Credit Event, will receive the payout based on that Credit Event.

• Bankruptcy and Failure-to-Pay Default, as described in the CREDIT EVENTS section of

this circular, will be the applicable Credit Events for Basket CEBOs.

• The Last Trading Day for Basket CEBOs, if there is no Credit Event, will be the 3rd Friday of the month. If a Credit Event has been confirmed prior to that date in every Basket Component or if a Redemption Event has been confirmed in the last Basket Component prior to that day, the series will cease trading at the time of the confirmation and the Last Trading Day will be changed to the confirmation date.

• The Expiration Date for Basket CEBOs if there is no Credit Event will be the 4th

business day after the Last Trading Day. If a Credit Event has been confirmed before that day in every Basket Component or if a Redemption Event has been confirmed in the last Basket Component prior to that day, the Expiration Date will be accelerated to the 2nd business day immediately following the last confirmation date.

• Up to 41 quarterly expiration months (10.25 years) may be listed at any time.

• Basket CEBOs will have unique class symbols for each calendar year. Standard Call Month codes will be used for Basket CEBOs and "Z" will be used for the "dummy" $1 strike code.

• Basket CEBOs will be P.M.-settled.

• Basket CEBOs will trade from 8:30 a.m. – 3:00 p.m. (CT).

CURRENT CLASS LISTINGS Following are the classes and contract months for series of Basket CEBOs currently listed for trading:

Expiration Month and Option Symbols Product Name Sep 2008 Sep 2012 Auto Sector Basket CEBO AFY AFZ Home Builder Basket CEBO BBR BBS High Yield Composite Basket CEBO HAU HEU

• At the end of this circular, CBOE sets forth a listing of the specific components contained

within each basket identified above, and other relevant information. CREDIT EVENTS To the extent they are provided in the terms of the Relevant Obligations (described below) of the Basket Components within a Basket CEBO, the following are the applicable Credit Events for the above-listed classes:

• A Failure-to-Pay Default on its Reference Obligation (e.g., Company ABC 8.5% July 2013 bond) or on any other debt security obligations of the Reference Entity other than non-recourse indebtedness (the set of these obligations and the Reference Obligation are referred as the “Relevant Obligations”); provided that the minimum failure-to-pay amount, individually or in the aggregate, shall be the greater of $750,000 or the amount specified in accordance with the terms of the Relevant Obligation(s).

• Bankruptcy as defined in the terms of the Relevant Obligation(s).

August 1, 2007 Volume RB18, Number 31 4

INFORMATION SOURCES CBOE will confirm Credit Events and Special Contingencies based on at least two of the following sources of publicly available information: (1) Wall Street Journal, Bloomberg Service, Reuters, Dow Jones News Wire, Financial Times, New York Times; and/or (2) information submitted to or filed with the courts, the SEC, an exchange or association, the OCC, or another regulatory agency or similar authority. SUCCESSION ADJUSTMENTS Each Basket Component for which the Exchange has confirmed a Succession Event may be replaced by one or more Basket Components (“Successor Basket Components”) consisting of the Successor Basket Component(s) that have succeeded the original Basket Component as a result of a Succession Event based on the applicable share of each Successor Basket Component.

• A “Successor Basket Component” and a “Succession Event” will be defined in accordance with the terms of the Relevant Obligations of the Basket Component that is subject to adjustment for succession. In determining the applicable share, an equal share will be allocated to each Successor Basket Component that has succeeded the original Basket Component as issuer or guarantor of at least one Relevant Obligation and at least 25% of the principal amount of the original Basket Component’s outstanding debt obligations other than non-recourse indebtedness. If no Successor Basket Component satisfies the “at least 25%” requirement and the original Basket Component does not survive following the Succession Event, an equal share will be allocated to the Successor Basket Component(s) that succeeded to the largest percentage of the original Basket Component’s outstanding debt obligations other than non-recourse indebtedness.

• In the event of an adjustment for succession, the Exchange will specify the Reference

Obligation, recovery rate and the basket weight of each Successor Basket Component. The newly specified weight(s) will equal the weight of the predecessor Basket Component replaced by the Successor Basket Component(s). The recovery rates of Successor Basket Components may differ from the specified recovery rate of the predecessor Basket Component and the recovery rates of two or more Successor Basket Components could differ from one another.

• In respect of each Basket CEBO contract that was subject to adjustment for succession,

all other terms and conditions of each Basket CEBO containing a Successor Basket Component will be the same as the original Basket CEBO unless the Exchange determines, in its sole discretion, that a modification is necessary and appropriate for the protection of investors and the public interest, including but not limited to the maintenance of fair and orderly markets, consistency of interpretation and practice, and the efficiency of settlement procedures.

For additional information regarding Basket CEBO adjustments, please refer to Rule 29.4. BASKET CEBO PRODUCT DESCRIPTION August 1, 2007 Volume RB18, Number 31 5

Description: Basket CEBOs are cash-settled call options based on a Basket of Reference Entities (“Basket Components”). The options automatically pay out a cash settlement amount upon the confirmation of a Credit Event in one, some or all of the Basket Components, as specified by the Exchange at listing. The cash settlement amount could be different for different Basket Components. From time to time, CBOE may create new baskets that contain several of the same Basket Components contained in existing Basket CEBOs, which would be listed as a new options class. Existing Basket CEBOs will continue to trade until expiration. For each Basket CEBO class, the Exchange will specify:

(a) the Notional Face Value of the Basket (e.g., $100,000),

(b) the Basket Components,

(c) the weight of each Basket Component, which represents the fraction of the Notional Face Value of the Basket allocated to each Basket Component. (For example, if the Notional Face Value of the Basket is $100,000, and there are 10 equally weighted Basket Components, each Basket Component has a Notional Face Value of $10,000),

(d) the recovery rate of each Basket Component,

(e) the specified debt security that defines the Reference Obligation of each Basket

Component (e.g., Corporation XYZ 8.375% July 2033 bond), and

(f) the applicable Credit Event(s). Basket Components will remain fixed from the time of listing to the expiration date of the option, except that Basket Components could be replaced by Successor Basket Components following a Succession Event and would be removed from the Basket CEBO after a Credit Event or Redemption Event is confirmed by the Exchange. Relevant Securities: The specified debt security that defines the Reference Obligation of each Basket Component and all its other debt security obligations. Strike Price: Not applicable. A dummy strike price of $1.00 will be in the OPRA strike price field. The strike code for Basket CEBOs will be "Z". Only Call Options will trade: You may receive data (Month/Strike) information for puts. In that event, please disregard the information. Exercise Settlement Value:

The automatic payout for a Basket CEBO will be equal to the cash settlement amount divided by the contract multiplier specified by the Exchange. For example, if a Credit Event is confirmed in August 1, 2007 Volume RB18, Number 31 6

a Basket Component with a cash settlement amount of $6,000, the Exercise Settlement Value will be $6.00 (equivalent to $7.00 minus the dummy strike value of $1.00). Unit/Multiplier: 1,000 per contract. Cash Settlement Amount: If the Exchange confirms a Credit Event in an Basket Component occurred prior to 10:59 p.m. (CT) on the Last Trading Day, the cash settlement amount will be equal to the Notional Face Value of the Basket Component times one minus its Recovery Rate (its "loss rate"). For example, if the Notional Face Value of the Basket Component is $10,000, and the Exchange specifies a recovery rate of 40% (or 0.40) for the particular Basket Component in which a Credit Event is confirmed, the cash settlement amount is $6,000 = $10,000 * (1 – 0.40). Minimum Price Increment: $0.05 per unit ($50 per contract). Contract Months: Unless a Credit Event in all Basket Components has been confirmed, the Last Trading Day in the series will be the 3rd Friday of the expiration month in the March, June, September or December expiration month (however, if that day is not a business day, the Last Trading Day in the series will be on the preceding business day). Special Contingencies: Special procedures will apply if one or more of the following events occur on or before the Last Trading Day: (1) A Succession Event, which will be defined in accordance with the terms of the Relevant Obligation(s).

Adjustment for Succession: Once the Exchange has confirmed a Succession Event in an Basket Component, that component may be replaced by one or more Basket Components (“Successor Basket Components”) that have succeeded the original Basket Component as a result of a Succession Event based on the applicable share of each Successor Basket Component, as determined in accordance with Rule 29.4. For each Successor Basket Component, the Exchange will specify the Reference Obligation (e.g., XYW 8.375% December 2033 bond), recovery rate and the Basket weight of each Successor Basket Component. The sum of the weights of the Successor Basket Components will equal the weight of the Basket Component replaced by the Successor Basket Components. The recovery rates of Successor Basket Components may differ from the specified recovery rate of the predecessor Basket Component and the recovery rates of two or more Successor Basket Components could differ from one another.

August 1, 2007 Volume RB18, Number 31 7

(2) A Redemption Event, which will be defined in accordance with the terms of the Relevant Obligation(s) and will include the redemption or maturity of the Reference Obligation and of all other Relevant Obligations. If the Reference Obligation is redee

(3) med or matures but other Relevant Obligation(s) remain, a new Reference Obligation will be specified from among the remaining Relevant Obligation(s) and the substitution will not be deemed a Redemption Event.

Adjustment for Redemption: Once the Exchange has confirmed a Redemption Event in a Basket Component, that Basket Component will be removed from the Basket CEBO.

Confirmation of Credit Event and Special Contingencies: The Exchange will confirm Credit Events and Special Contingencies based on at least two of the following sources of publicly available information: (1) announcements published by newswire services or information services companies, the names of which will be announced to the membership via Regulatory Circular; and/or (2) information submitted to or filed with the courts, the SEC, an exchange or association, the OCC, or another regulatory agency or similar authority. Every determination made by the Exchange shall be within its sole discretion and shall be conclusive and binding on all investors and not subject to review. CBOE identifies the specific information sources on page 3 of this circular. The confirmation period will begin when the Basket CEBO contract is listed and will extend to 3:00 p.m. (CT) on the Expiration Date. Settlement: Basket CEBOs settle in cash. If the Exchange confirms a Credit Event in an Basket Component prior to 10:59 p.m. (CT) on the Last Trading Day, the cash settlement amount will be equal to the Notional Face Value of the Basket Component times one minus its Recovery Rate (its "loss rate"). If no Credit Event is confirmed in a Basket Component, the cash settlement value will be $0.

Last Trading Day: The 3rd Friday of the expiration month (or, if that day is not a business day, the preceding business day); provided, however, if a Credit Event is confirmed prior to that day, the series will cease trading at the time of confirmation of the Credit Event and the Last Trading Day would be accelerated to the confirmation date. Expiration Date: The 4th business day after the 3rd Friday of the expiration month (or, if that day is not a business day, the 4th business day after the preceding business day); provided, however, if a Credit Event is confirmed by the Exchange to members and the OCC, the Expiration Date will be accelerated to the 2nd business day immediately following the confirmation date. Final Settlement Date: The day following the Expiration Date. Trading Hours:

August 1, 2007 Volume RB18, Number 31 8

8:30 a.m. – 3:00 p.m. (CT). Trading Platform: CBOEdirect. Position Limit: 50,000 contracts. Margin: As described in Rule 12.3(l). ADDITIONAL INFORMATION Please refer to Chapter XXIX of CBOE’s rules Basket CEBOs:

• RG07-80: Basket Credit Event Binary Options - System Settings You can also find additional information on our website located at: http://www.cboe.com/credit. Any questions about this memorandum may be directed to the Help Desk at (312) 786-7086 or 786-8749.

August 1, 2007 Volume RB18, Number 31 9

August 1, 2007 Volume RB18, Number 31 10

Auto Sector Basket CEBOS (AFY, AFZ)

Company Name Equity Ticker Reference Obligation REF OB CUSIP Equity Cusip

Notional Value

Assumed Recovery

Rate

Cash Settlement

Amount

1 ArvinMeritor Inc ARM ARM 8 1/8 09/15/15 043353AC5 043353101 $14,285.71 0.40 $8,571.432 Amern Axle & Mfg Inc AXL AXL 5 1/4 02/11/14 02406PAE0 024061103 $14,285.71 0.40 $8,571.433 Ford Mtr Co F F 6 1/2 08/01/18 345370BX7 319963104 $14,285.71 0.40 $8,571.434 Gen Mtrs Corp GM GM 7 1/8 07/15/13 370442BS3 382550101 $14,285.71 0.40 $8,571.435 Goodyear Tire & Rubr Co GT GT 9 07/01/15 382550AU5 413619107 $14,285.71 0.40 $8,571.436 TRW Automotive Inc TRW TRW 9 3/8 02/15/13 87264QAM2 873168108 $14,285.71 0.40 $8,571.437 Visteon Corp VC VC 7 03/10/14 92839UAC1 969457100 $14,285.71 0.40 $8,571.43

$100,000.00 $60,000.00

Home Builder Sector Basket CEBOS (BBR, BBS)

Company Name Equity Ticker Reference Obligation REF OB CUSIP Equity Cusip

Notional Value

Assumed Recovery

Rate

Cash Settlement

Amount 1 KB Home KBH KBH 7.75 02/01/10 48666KAF6 526057104 $12,500.00 0.40 $7,500.002 K Hovnanian Entpers Inc HOV HOV 6.5 01/15/14 442488AQ8 451663108 $12,500.00 0.40 $7,500.003 Beazer Homes USA Inc BZH BZH 6.5 11/15/13 07556QAJ4 07556Q105 $12,500.00 0.40 $7,500.004 Std Pac Corp SPF SPF 7 08/15/15 85375CAT8 00206R102 $12,500.00 0.40 $7,500.005 Centex Corp CTX CTX 5.25 06/15/15 152312AQ7 126650100 $12,500.00 0.40 $7,500.006 Lennar Corp LEN LEN 5.95 03/01/13 526057AG9 532716107 $12,500.00 0.40 $7,500.007 Pulte Homes Inc PHM PHM 5.25 01/15/14 745867AQ4 V7780T103 $12,500.00 0.40 $7,500.008 Toll Bros Inc TOL TOL 6.875 11/15/12 88947EAA8 88732J108 $12,500.00 0.40 $7,500.00

$100,000.00 $60,000.00

August 1, 2007 Volume RB18, Number 31 11

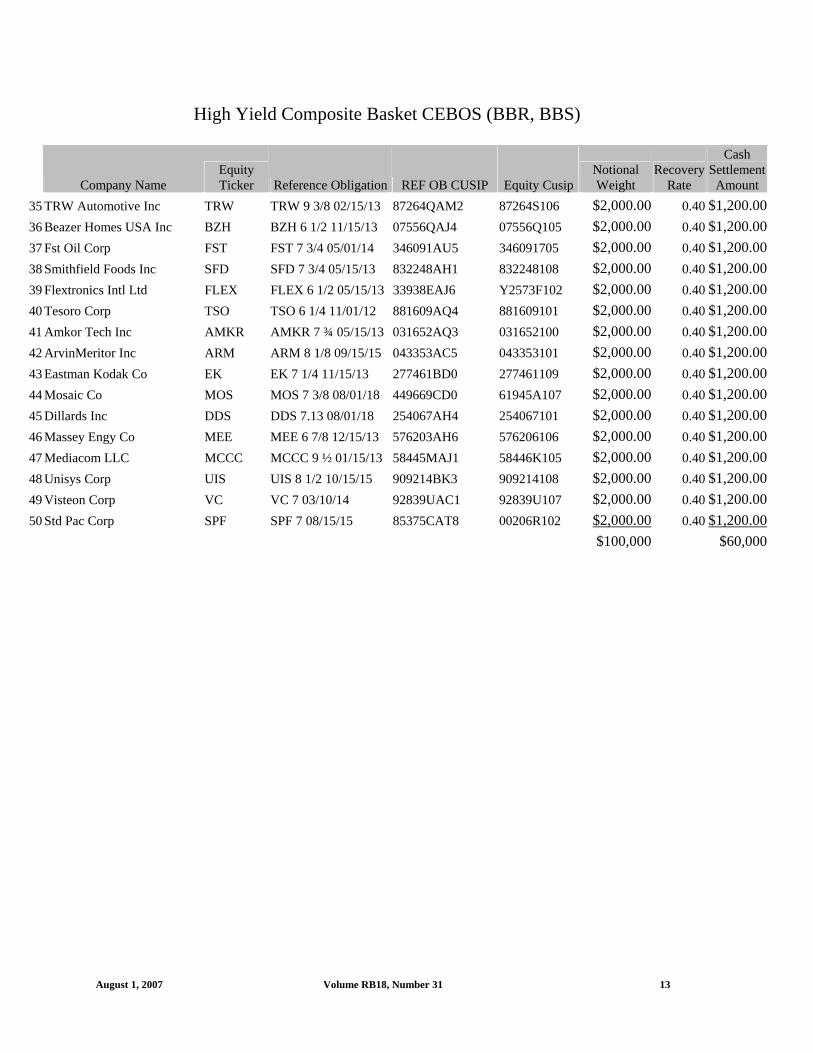

High Yield Composite Basket CEBOS (BBR, BBS)

Company Name Equity Ticker Reference Obligation REF OB CUSIP Equity Cusip

Notional Weight

Recovery Rate

Cash Settlement

Amount 1 Ford Mtr Co F F 6 1/2 08/01/18 345370BX7 345370860 $2,000.00 0.40 $1,200.002 Gen Mtrs Corp GM GM 7 1/8 07/15/13 370442BS3 370442105 $2,000.00 0.40 $1,200.003 Charter Comms Hldgs LLC CHTR CHTR 10 04/01/09 16117PAK6 16117M107 $2,000.00 0.40 $1,200.004 El Paso Corp EP EP 7 7/8 06/15/12 28336LAE9 28336L109 $2,000.00 0.40 $1,200.005 Williams Cos Inc WMB WMB 7 1/2 01/15/31 969457BB5 969457100 $2,000.00 0.40 $1,200.006 The AES Corp AES AES 7 3/4 03/01/14 00130HBC8 00130H105 $2,000.00 0.40 $1,200.007 Chesapeake Engy Corp CHK CHK 6 7/8 01/15/16 165167BE6 165167107 $2,000.00 0.40 $1,200.008 Lyondell Chem Co LYO LYO 10 1/2 06/01/13 552078AV9 552078107 $2,000.00 0.40 $1,200.009 CMS Engy Corp CMS CMS 6 7/8 12/15/15 125896AZ3 125896100 $2,000.00 0.40 $1,200.00

10 RH DONNELLEY Corp RHD RHD 8 7/8 01/15/16 74955WAG4 74955W307 $2,000.00 0.40 $1,200.0011 NRG Energy Inc XEL NRG 7 1/4 02/01/14 629377AT9 98389B100 $2,000.00 0.40 $1,200.0012 Level 3 Comms Inc LVLT LVLT 3 1/2 06/15/12 52729NBK5 52729N100 $2,000.00 0.40 $1,200.0013 Dynegy Hldgs Inc DYN DYN 8 3/8 05/01/16 26816LAT9 26817G102 $2,000.00 0.40 $1,200.0014 AMR Corp AMR AMR 9.1 05/01/16 001765AB2 001765106 $2,000.00 0.40 $1,200.0015 Allied Waste North Amer Inc AW AM 7 3/8 06/01/16 026375AL9 019589308 $2,000.00 0.40 $1,200.0016 EchoStar DBS Corp DISH DISH 6 5/8 10/01/14 27876GAX4 278762109 $2,000.00 0.40 $1,200.0017 Tenet Healthcare Corp THC THC 7 3/8 02/01/13 88033GAY6 88033G100 $2,000.00 0.40 $1,200.0018 Ctzns Comms Co CZN CZN 6 1/4 01/15/13 17453BAP6 17453B101 $2,000.00 0.40 $1,200.0019 Royal Caribbean Cruises Ltd RCL RCL 6 7/8 12/01/13 780153AP7 V7780T103 $2,000.00 0.40 $1,200.0020 L 3 Comms Corp LLL LLL 7 5/8 06/15/12 502413AJ6 502424104 $2,000.00 0.40 $1,200.0021 Mirant North America LLC MIR MIR 7 3/8 12/31/13 60467XAC1 60467R100 $2,000.00 0.40 $1,200.0022 Goodyear Tire & Rubr Co GT GT 9 07/01/15 382550AU5 382550101 $2,000.00 0.40 $1,200.0023 Rite Aid Corp RAD RAD 7.7 02/15/27 767754AJ3 767754104 $2,000.00 0.40 $1,200.0024 Abitibi Consol Inc ABY ABY 8 3/8 04/01/15 003669AJ7 003924107 $2,000.00 0.40 $1,200.0025 Nortel Networks Corp NTL NT 4 1/4 09/01/08 656568AB8 656567401 $2,000.00 0.40 $1,200.0026 Reynolds Amern Inc RAI RAI 7 5/8 06/01/16 761713AE6 761713106 $2,000.00 0.40 $1,200.0027 Idearc Inc IAR IAR 8 11/15/16 451663AC2 451663108 $2,000.00 0.40 $1,200.0028 KB Home KBH KBH 7 3/4 02/01/10 48666KAF6 48666K109 $2,000.00 0.40 $1,200.0029 Advanced Micro Devices Inc AMD AMD 7 3/4 11/01/12 007903AJ6 007903107 $2,000.00 0.40 $1,200.00

30 Smurfit Stone Container Enterprises Inc SSCC SSCC 7 1/2 06/01/13 47508XAD7 832727101 $2,000.00 0.40 $1,200.00

31 Allegheny Engy Supp Co LLC AYE AYE 8 1/4 04/15/12 017363AE2 017361106 $2,000.00 0.40 $1,200.00

32 K Hovnanian Entpers Inc HOV HOV 6 1/2 01/15/14 442488AQ8 442487203 $2,000.00 0.40 $1,200.0033 NOVA Chems Corp NCX NCX 0 11/15/13 66977WAH2 66977W109 $2,000.00 0.40 $1,200.0034 Sanmina SCI Corp SANM SANM 8 1/8 03/01/16 800907AK3 800907107 $2,000.00 0.40 $1,200.00

August 1, 2007 Volume RB18, Number 31 12

High Yield Composite Basket CEBOS (BBR, BBS)

Company Name Equity Ticker Reference Obligation REF OB CUSIP Equity Cusip

Notional Weight

Recovery Rate

Cash Settlement

Amount 35 TRW Automotive Inc TRW TRW 9 3/8 02/15/13 87264QAM2 87264S106 $2,000.00 0.40 $1,200.0036 Beazer Homes USA Inc BZH BZH 6 1/2 11/15/13 07556QAJ4 07556Q105 $2,000.00 0.40 $1,200.0037 Fst Oil Corp FST FST 7 3/4 05/01/14 346091AU5 346091705 $2,000.00 0.40 $1,200.0038 Smithfield Foods Inc SFD SFD 7 3/4 05/15/13 832248AH1 832248108 $2,000.00 0.40 $1,200.0039 Flextronics Intl Ltd FLEX FLEX 6 1/2 05/15/13 33938EAJ6 Y2573F102 $2,000.00 0.40 $1,200.0040 Tesoro Corp TSO TSO 6 1/4 11/01/12 881609AQ4 881609101 $2,000.00 0.40 $1,200.0041 Amkor Tech Inc AMKR AMKR 7 ¾ 05/15/13 031652AQ3 031652100 $2,000.00 0.40 $1,200.0042 ArvinMeritor Inc ARM ARM 8 1/8 09/15/15 043353AC5 043353101 $2,000.00 0.40 $1,200.0043 Eastman Kodak Co EK EK 7 1/4 11/15/13 277461BD0 277461109 $2,000.00 0.40 $1,200.0044 Mosaic Co MOS MOS 7 3/8 08/01/18 449669CD0 61945A107 $2,000.00 0.40 $1,200.0045 Dillards Inc DDS DDS 7.13 08/01/18 254067AH4 254067101 $2,000.00 0.40 $1,200.0046 Massey Engy Co MEE MEE 6 7/8 12/15/13 576203AH6 576206106 $2,000.00 0.40 $1,200.0047 Mediacom LLC MCCC MCCC 9 ½ 01/15/13 58445MAJ1 58446K105 $2,000.00 0.40 $1,200.0048 Unisys Corp UIS UIS 8 1/2 10/15/15 909214BK3 909214108 $2,000.00 0.40 $1,200.0049 Visteon Corp VC VC 7 03/10/14 92839UAC1 92839U107 $2,000.00 0.40 $1,200.0050 Std Pac Corp SPF SPF 7 08/15/15 85375CAT8 00206R102 $2,000.00 0.40 $1,200.00

$100,000 $60,000

August 1, 2007 Volume RB18, Number 31 13

August 1, 2007 Volume RB18, Number 31 14

Regulatory Circular RG07-80

To: Members, Member Firms and Member Organizations

From: Trading Operations

Date: July 25, 2007

Re: Basket Credit Event Binary Options - System Settings

On July 31, 2007, CBOE plans to begin trading Basket Credit Event Binary Options ("Basket CEBOs") on the following products:

• Auto Sector Basket • Home Builder Sector Basket • High Yield Composite Basket

The Jane Street DPM, located at Post 6 Station 4, has been allocated the Auto Sector and Home Builder Sector Basket CEBOs, and Susquehanna DPM, also located at Post 6 Station 4, has been allocated the High Yield Composite Basket CEBO. System settings for Multiple and Single Payout Basket CEBOs1 will be as follows:

- Trading will take place on the Hybrid 2.0 trading platform. - RMMs will be permitted. - Please refer to Rule 29.17 for details on quoting obligations. - Seat cost will be .001. - Trades executed electronically will be allocated in Pro-Rata fashion with Public

Customer and DPM Participation Entitlements (trades executed in open outcry will be allocated pursuant to Rule 6.45B(b)).

- C, F, B, M and N orders will be eligible for auto-ex. The interval for the entry of M and N orders will be 0 seconds.

- C, F, B, M and N orders will be eligible for booking. - Book trigger timer (N-second joining period) will be inactive. - Quote-to-Quote Lock timer will be set to 1 second. - AIM will be available with a penny auction increment. - COB and COA will not be available. - HAL will not be available. - Preferred Market-Maker will not be available.

1 At this time, CBOE does not intend to list Single Payout Basket CEBOs; however, the system settings described in this circular are applicable to Single Basket CEBOs, except where otherwise noted.

Other details will be as follows:

- Multiple and Single Payout Basket CEBOs are single-strike binary options. - A single call (no puts) with a strike price of 1 will be listed for each product. - Quotes and last sales will be disseminated to OPRA. - The open outcry crossing entitlement will be 40% (after satisfying public customer

orders) for facilitation and solicitation of eligible orders of 50 contracts or more. Please refer to Rule 6.74(d) for further details.

- Openings will be conducted via the Hybrid Opening System, which will initiate the opening procedure and send a Rotation Notice at a random time after 8:30 a.m. Series will then begin opening in the manner described in Information Circular IC06-104.

- Trading will continue in Multiple Payout Basket CEBOs when a Credit Event has been confirmed by the Exchange, unless there are no remaining basket components. Holders as of the close of the confirmation date of the Credit Event will receive the payout based on that Credit Event.

- Single Payout Basket CEBOs will cease trading and expire when a Credit Event has been confirmed by the Exchange and holders will receive the payout based on that Credit Event.

Please see Chapter XXIX of CBOE’s rules or go to: http://www.cboe.com/micro/credit/introduction.aspx for further details. Please contact Greg Burkhardt at 312-786-7531 or the Help Desk at 1-312-786-7086 or 8749 with any questions.

RULE CHANGES EFFECTIVE-ON-FILING RULE CHANGE(S) The following rule filing(s) were submitted to the SEC “effective-on-filing,” and may have taken effect pursuant to Section 19(b)(3) of the Securities Exchange Act. They will remain in effect barring further action by the SEC within 60 days after their publication in the Federal Register. Below, any additions to rule text are underlined, and any deletions are [bracketed]. Copies are available on the CBOE public website at www.cboe.com/legal/effectivefiling.aspx. ______________________________________________________________________________ SR-CBOE-2007-86 Penny Pilot On July 24, 2007, the Exchange filed Rule Change File No. SR-CBOE-2007-86 which filing proposes to extend until September 27, 2007, the Penny Pilot Program while the SEC analyzes whether to expand the Pilot, and if so, by how much. Any questions regarding the rule change may be directed to Patrick Sexton, Legal Division, at 312-786-7464. The rule filing is available at http://www.cboe.org/publish/RuleFilingsSEC/SR-CBOE-2007-086.pdf. ______________________________________________________________________________

August 1, 2007 Volume RB18, Number 31 15

August 1, 2007 Volume RB18, Number 31 16

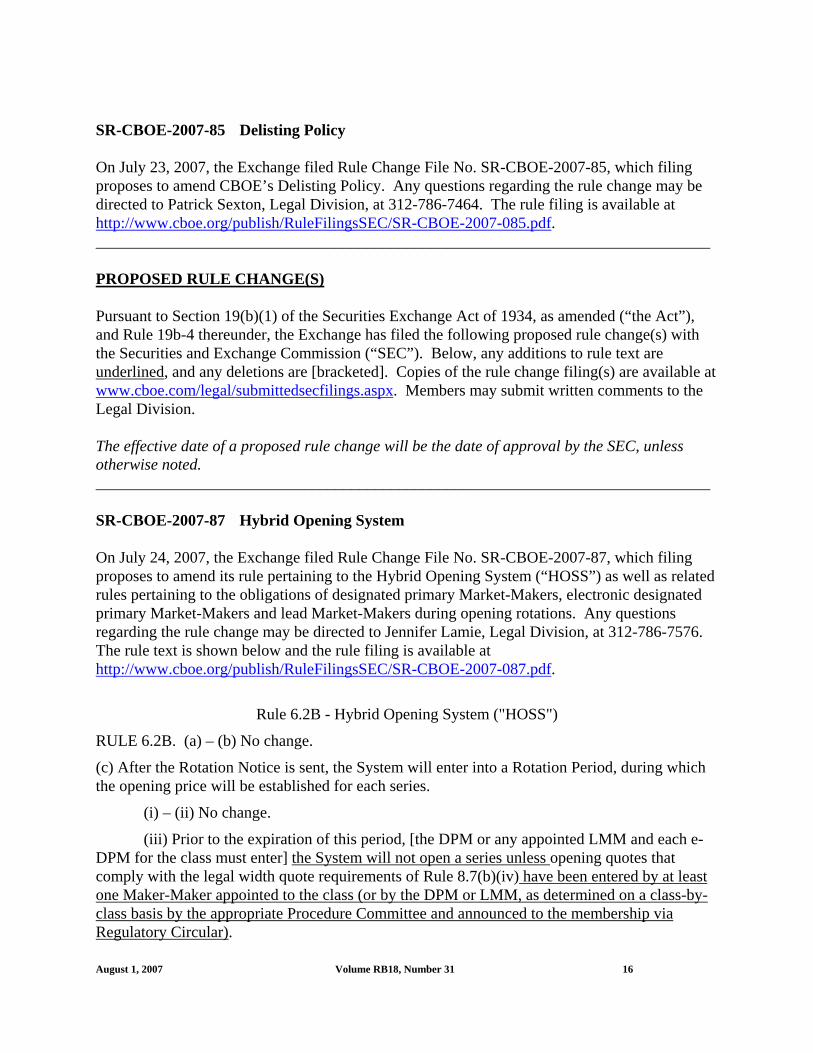

SR-CBOE-2007-85 Delisting Policy On July 23, 2007, the Exchange filed Rule Change File No. SR-CBOE-2007-85, which filing proposes to amend CBOE’s Delisting Policy. Any questions regarding the rule change may be directed to Patrick Sexton, Legal Division, at 312-786-7464. The rule filing is available at http://www.cboe.org/publish/RuleFilingsSEC/SR-CBOE-2007-085.pdf. _____________________________________________________________________________ PROPOSED RULE CHANGE(S) Pursuant to Section 19(b)(1) of the Securities Exchange Act of 1934, as amended (“the Act”), and Rule 19b-4 thereunder, the Exchange has filed the following proposed rule change(s) with the Securities and Exchange Commission (“SEC”). Below, any additions to rule text are underlined, and any deletions are [bracketed]. Copies of the rule change filing(s) are available at www.cboe.com/legal/submittedsecfilings.aspx. Members may submit written comments to the Legal Division. The effective date of a proposed rule change will be the date of approval by the SEC, unless otherwise noted. _____________________________________________________________________________ SR-CBOE-2007-87 Hybrid Opening System On July 24, 2007, the Exchange filed Rule Change File No. SR-CBOE-2007-87, which filing proposes to amend its rule pertaining to the Hybrid Opening System (“HOSS”) as well as related rules pertaining to the obligations of designated primary Market-Makers, electronic designated primary Market-Makers and lead Market-Makers during opening rotations. Any questions regarding the rule change may be directed to Jennifer Lamie, Legal Division, at 312-786-7576. The rule text is shown below and the rule filing is available at http://www.cboe.org/publish/RuleFilingsSEC/SR-CBOE-2007-087.pdf.

Rule 6.2B - Hybrid Opening System ("HOSS")

RULE 6.2B. (a) – (b) No change.

(c) After the Rotation Notice is sent, the System will enter into a Rotation Period, during which the opening price will be established for each series.

(i) – (ii) No change.

(iii) Prior to the expiration of this period, [the DPM or any appointed LMM and each e-DPM for the class must enter] the System will not open a series unless opening quotes that comply with the legal width quote requirements of Rule 8.7(b)(iv) have been entered by at least one Maker-Maker appointed to the class (or by the DPM or LMM, as determined on a class-by-class basis by the appropriate Procedure Committee and announced to the membership via Regulatory Circular).

(iv) No change.

(d) No change.

(e) The System will not open a series if one of the following conditions is met:

(i) There is no quote present in the series as provided in paragraph (c)(iii)[that complies with the legal width quote requirements of Rule 8.7(b)(iv)].

(ii) – (iii) No change.

(f) – (i) No change.

. . . Interpretations and Policies:

.01 No change.

* * * * *

Rule 8.15A – Lead Market-Makers in Hybrid Classes RULE 8.15A. (a) No change.

(b) LMM Obligations. LMMs are required to:

(i) – (iii) No change.

(iv) [participate in the Hybrid Opening System]ensure that a trading rotation is initiated promptly following the opening of the underlying security (or promptly after 8:30 a.m. (CT) in an index class) in accordance with Rule 6.2B in 100% of the series of each allocated class by entering opening quotes as necessary; and

(v) – (vi) No change.

* * * * *

Rule 8.85 – DPM Obligations

RULE 8.85. (a) Dealer Transactions. Each DPM shall fulfill all of the obligations of a Market-Maker under the Rules, and shall satisfy each of the following requirements in respect of each of the securities allocated to the DPM. To the extent that there is any inconsistency between the specific obligations of a DPM set forth in subparagraphs (a)(i) through (a)(xii) of this Rule and the general obligations of a Market-Maker under the Rules, subparagraphs (a)(i) through (a)(xii) of this Rule shall govern. Each DPM shall:

(i) – (x) No change.

(xi) [enter opening quotes]ensure that a trading rotation is initiated promptly following the opening of the underlying security (or promptly after 8:30 a.m. (CT) in an index class) in accordance with Rule 6.2B in 100% of the series of each allocated class by entering opening quotes as necessary.

(xii) No change.

(b) – (e) No change.

August 1, 2007 Volume RB18, Number 31 17

August 1, 2007 Volume RB18, Number 31 18

. . . Interpretations and Policies:

.01 - .03 No change.

* * * * *

Rule 8.93 – e-DPM Obligations RULE 8.93. Each e-DPM shall fulfill all of the obligations of a Market-Maker and of a DPM under the Rules (except those contained in Rules 8.85(a)(i),(iv),(v), (vii)-(x), and (xii), 8.85(c)(i) and (v), and 8.85(e)), and shall satisfy each of the following requirements:

(i) – (x) No change. (xi) [enter opening quotes] ensure that a trading rotation is initiated promptly following the

opening of the underlying security (or promptly after 8:30 a.m. (CT) in an index class) in accordance with Rule 6.2B in 100% of the series of each allocated class by entering opening quotes as necessary.

Information Circular IC07-96 Date: July 2, 2007 To: Membership From: Nominating Committee Re: Selection of Nominees for Board of Directors and Nominating Committee The Nominating Committee is accepting applications for nominees for the 2007 annual election to fill positions on the Board of Directors and Nominating Committee. Available Positions Available positions include: Board of Directors 1 At-Large Director 3-year term 2 Floor Directors 3-year terms 3 Off-Floor Directors Two 3-year terms and a 2-year term 4 Public Directors 3-year terms Nominating Committee 1 Firm Member 3-year term 3 Floor Members Two 3-year terms and a 1-year term 1 Lessor Member 3-year term 1 Public Member 3-year term The qualification criteria for the available positions on the Board of Directors and Nominating Committee are described in the attached materials. Application Submission Time Frame The Nominating Committee requests that candidates who wish to be considered for nomination by the Nominating Committee complete and submit the attached Candidate Application Form ("Application") by Monday, August 6, 2007. The Nominating Committee strongly encourages candidates to submit a current resume or curriculum vitae along with their Applications. The Nominating Committee will seek to interview all candidates that submit an Application by August 6, 2007. Although the Nominating Committee will continue to accept and consider any Applications submitted prior to 5:00 p.m. (Chicago time) on September 14, 2007, candidates that submit an Application after August 6, 2007 are not guaranteed to have a Committee interview. Application Submission Process The Application form is attached to this circular and may be obtained on the CBOE Member Website at www.cboe.org and at the 4th and 7th floor reception desks at the Exchange. You may print or type the requested information into either the hard copy version or electronic version of the Application form. The electronic version of the Application form is posted on www.cboe.org in an interactive pdf format which allows you to type the applicable information into the form and to print the completed form.

You may submit your Application in any of the following ways: (i) by hand, mail, or courier delivery to Arthur Reinstein, CBOE, 400 South LaSalle Street, 7th Floor, Chicago, Illinois 60605; (ii) by e-mail to [email protected]; or (iii) by facsimile to Arthur Reinstein at (312) 786-7919. Individuals generally submit their names to the Nominating Committee for consideration by submitting an Application instead of through the submission of written nominations by others. The names of those who have submitted an Application to the Nominating Committee to be considered for nomination will be posted on the Exchange’s bulletin board and on the Member Website.

Director Candidate Criminal History Searches and Background Investigations The Board of Directors recently approved a policy recommended by the Governance Committee relating to director candidate criminal history searches and background investigations. Pursuant to this policy, the Exchange will conduct a criminal history search for each director candidate by submitting that person's fingerprints to the FBI database. If a director candidate's fingerprints are already electronically on file with the Exchange, the candidate does not need to be re-fingerprinted and the Exchange will simply submit to the FBI database the electronic fingerprints that the Exchange already has on file for the candidate. If a director candidate's fingerprints are not already electronically on file with the Exchange, staff will contact the director candidate to make arrangements to obtain that person's fingerprints so that they can be submitted to the FBI database. In addition, director candidates who are not currently CBOE directors may be subject to a background investigation under the policy. At the present time, it is anticipated that Kroll Background America, Inc. (KBA) will be retained by the Exchange to conduct these background investigations. Because KBA requires that a consent form be completed with certain information required by KBA in order to conduct a background investigation, KBA's consent form is included as part of the Application for director candidates who are not current CBOE directors to complete and execute. Staff will advise those director candidates if a different company is retained by the Exchange to conduct these background investigations and if a different consent form needs to be executed in that event. Although a criminal history search will not be conducted for Nominating Committee candidates and they will not be subject to a background investigation, a Nominating Committee candidate's regulatory history and background information reflected on the candidate's Application will continue to be reviewed as has previously been the case.

Candidate Interviews The Nominating Committee will hold candidate interviews by appointment during August and September. The Nominating Committee will schedule interviews by contacting candidates to appear before the Nominating Committee for an individual interview at one of its meetings. During these interviews, the Nominating Committee questions candidates about a broad range of relevant issues and seeks to ascertain the experience and expertise the candidate would bring to the Board of Directors or Nominating Committee. After the interviews, the Nominating Committee selects the nominees that it believes will most effectively fill the available positions.

Deadline for Qualification to Be Considered for Nomination A candidate must satisfy the applicable qualification criteria for a position on the Board of Directors or Nominating Committee both at the time of nomination and at the time of election. It is anticipated that the nomination of candidates by the Nominating Committee will occur sometime during the time period between September 17, 2007 and October 10, 2007. Any candidate who does not satisfy the applicable qualification criteria at the time the candidate submits an Application should take steps to be qualified during the time period between September 17, 2007 and October 10, 2007 so that the candidate can be considered for nomination. The postings listing the candidates that have applied to be considered for nomination will indicate for each candidate as of the date of the posting whether (i) the candidate satisfies the applicable qualification criteria, (ii) the candidate does not satisfy the applicable qualification criteria, or (iii) the Nominating Committee has not yet reviewed, or is in the process of reviewing, whether or not the candidate satisfies the applicable qualification

2

criteria. Annual Election Process Dates The Nominating Committee will post its slate of candidates for available positions on the Board of Directors and Nominating Committee by no later than October 10, 2007. To run against the slated candidates, an individual must submit to the Office of the Secretary a petition signed by not less than 100 voting members of the Exchange. Any petitions must be received by no later than 5:00 p.m. (Chicago time) on October 29, 2007. The names of petition candidates, if any, will be posted on the Exchange bulletin board and on the Member Website. The annual election meeting will be held on November 15, 2007. The membership makes the final decisions with respect to ensuring that CBOE has the best leadership in the industry.

Demutualization Please note that the governance structure of the Exchange is proposed to be modified as part of CBOE's proposed demutualization and that the current CBOE governance structure (including the current nomination and annual election process) will continue in place until the approval and effectiveness of a demutualization, including its approval by a membership vote. Upon the effectiveness of a demutualization, the CBOE governance structure provided for under the demutualization will take the place of the current CBOE governance structure.

Contact Information The following persons currently serve on the Nominating Committee: Terrence Andrews (TAN) (Chairman), Daniel Carver (DPC), Terrence Cullen (CLN), J. Douglas Gray, Sean Haggerty (HAG), Jeffrey Kirsch, Benjamin Londergan (BNE), Richard Lund, David Miller (DFM), and Pamela Strobel. Please feel free to contact Terrence Andrews, Nominating Committee Chairman, at (312) 863-8044 if you have any questions regarding the nominating process or Arthur Reinstein, Legal Division, at (312) 786-7570 if you have any procedural questions regarding the nominating process or regarding how to complete the Application form. Attachment

3

2007 CANDIDATE APPLICATION FORM

Return this application form as soon as possible.

The Nominating Committee requests that completed application forms be submitted by August 6, 2007.

The Nominating Committee strongly encourages candidates to also attach and submit a current resume or curriculum vitae.

Name: ___________________________________________________________________________________ Acronym: ______________________ Title: ___________________________________________________ Firm:___________________________________________________________

Current CBOE Directors Should Skip to Item 1 Below. Preferred Mailing Address: _________________________________________________________________________________________________ City/State/Zip: ____________________________________________________________________________________________________________ Business Phone: ( ) ____________________________ Home Phone: ( ) ______________________________________ Trading Floor Phone: ( ) _________________________ Indicate: Trading Crowd Trading Booth Headset E-Mail:__________________________________________________ Pager:__________________________________________________________ Cell Phone:______________________________________________ Fax: ___________________________________________________________

POSITION(S) APPLIED FOR 1. Check the position(s) for which you are applying and indicate whether you currently satisfy the qualification criteria for the

position(s) you have checked. (See page 7 for qualification criteria.)

BOARD OF DIRECTORS CURRENTLY SATISFY QUALIFICATION CRITERIA

At-Large Director (One 3-year term) Yes No

Floor Director (Two 3-year terms) Yes No

Off-Floor Director (Two 3-year terms and a 2-year term) Yes No

Public Director (Four 3-year terms) Yes No

NOMINATING COMMITTEE

Firm Member (One 3-year term) Yes No

Floor Member (Two 3-year terms and a 1-year term) Yes No

Lessor Member (One 3-year term) Yes No

Public Member (One 3-year term) Yes No

Candidates must be qualified at the time of nomination and at the time of election. Candidates should ensure they are and remain qualified during the time period between September 17, 2007 and October 10, 2007 in order to be considered for nomination.

MEMBERSHIP STATUS

2. What are your current membership statuses, if any? (Check all that apply.)

Market-Maker Floor Broker DPM Designee Remote Market-Maker Sole Proprietor

Owner Lessor Lessee CBOT Exerciser ( CBOT Owner or CBOT Delegate)

Nominee. Firm: ________________________________________________________________________________________________________

Registered For. Firm: ___________________________________________________________________________________________________

Person Associated with a Member Firm. Explain: ___________________________________________________________________________ ________________________________________________________________________________________________________________________

None of the above

DISCIPLINARY HISTORY 3. Do you have any regulatory or disciplinary history and/or any pending regulatory or disciplinary matters? Yes No

If yes, attach any decision(s) issued to you in the matter(s), or if no decision has been issued because a matter is pending or otherwise, attach a description of the matter.

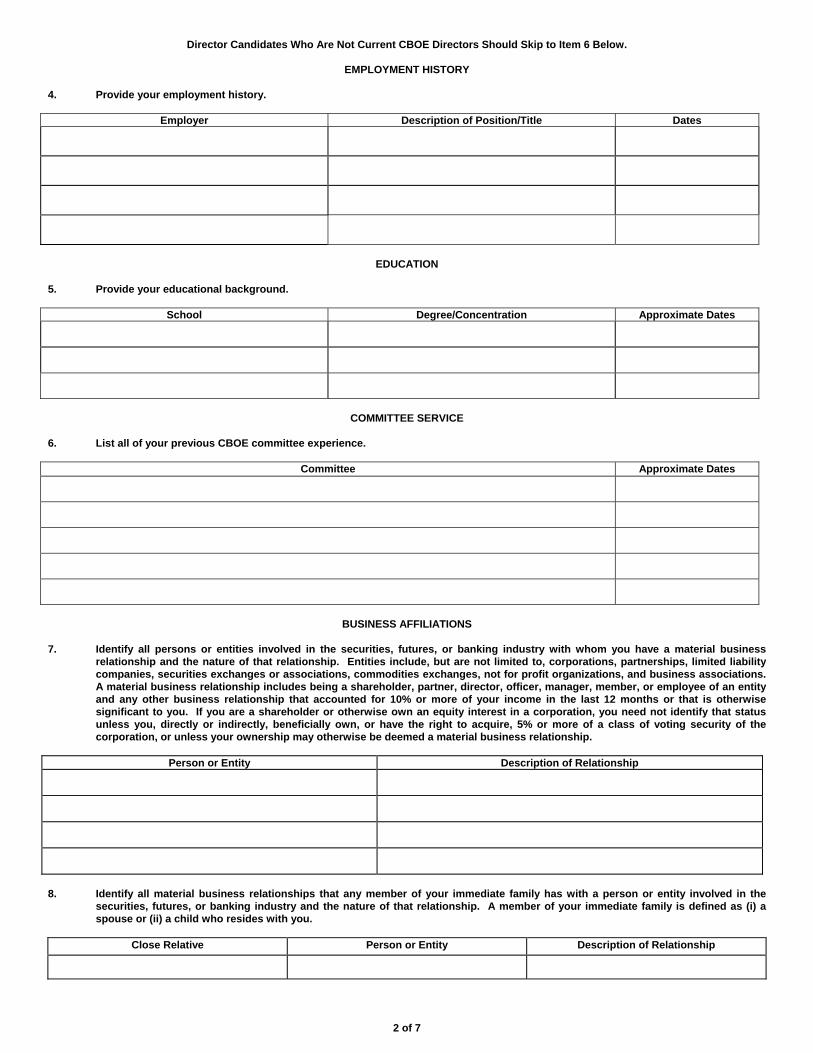

Director Candidates Who Are Not Current CBOE Directors Should Skip to Item 6 Below.

EMPLOYMENT HISTORY 4. Provide your employment history.

Employer Description of Position/Title Dates

EDUCATION

5. Provide your educational background.

School Degree/Concentration Approximate Dates

COMMITTEE SERVICE

6. List all of your previous CBOE committee experience.

Committee Approximate Dates

BUSINESS AFFILIATIONS

7. Identify all persons or entities involved in the securities, futures, or banking industry with whom you have a material business

relationship and the nature of that relationship. Entities include, but are not limited to, corporations, partnerships, limited liability companies, securities exchanges or associations, commodities exchanges, not for profit organizations, and business associations. A material business relationship includes being a shareholder, partner, director, officer, manager, member, or employee of an entity and any other business relationship that accounted for 10% or more of your income in the last 12 months or that is otherwise significant to you. If you are a shareholder or otherwise own an equity interest in a corporation, you need not identify that status unless you, directly or indirectly, beneficially own, or have the right to acquire, 5% or more of a class of voting security of the corporation, or unless your ownership may otherwise be deemed a material business relationship.

Person or Entity Description of Relationship

8. Identify all material business relationships that any member of your immediate family has with a person or entity involved in the

securities, futures, or banking industry and the nature of that relationship. A member of your immediate family is defined as (i) a spouse or (ii) a child who resides with you.

Close Relative Person or Entity Description of Relationship

2 of 7

Close Relative Person or Entity Description of Relationship

9. Identify any other relationships that you or a member of your immediate family have, or any other activities in which you or a

member of your immediate family are engaged, which could be regarded as constituting a conflict of interest with respect to your service as a CBOE director or Nominating Committee member.

PREVIOUS APPLICATIONS TO NOMINATING COMMITTEE

10. Identify all positions on the Board of Directors and Nominating Committee for which you applied to the Nominating Committee to be

considered for nomination in the prior three years.

Year Position(s) 2006

2005

2004

FLOOR DIRECTOR AND FLOOR MEMBER CANDIDATES ONLY

11. For Floor Director and Nominating Committee Floor Member candidates: Are you primarily engaged in business on the floor of the

Exchange in the capacity of a member? Yes No

PUBLIC AND LESSOR CANDIDATES ONLY 12. For Public Director candidates and for Nominating Committee Public Member and Lessor Member candidates: Are you individually

registered as a broker-dealer? Yes No 13. For Public Director candidates and for Nominating Committee Public Member and Lessor Member candidates: Identify if you have

any direct or indirect affiliation with a broker-dealer or with an entity that is directly or indirectly affiliated with a broker-dealer as a parent, subsidiary, affiliate, or otherwise.

Person or Entity Description of Relationship

Director Candidates Who Are Not Current CBOE Directors Must Also Complete Pages 4-6.

The Nominating Committee will seek to interview all candidates that submit an application form by August 6, 2007. Although the Nominating Committee will continue to accept and consider application forms submitted by candidates prior to 5:00 p.m. (Chicago time) on September 14, 2007, candidates that submit an application form after August 6, 2007 are not guaranteed to have a Committee interview. The Nominating Committee will schedule interviews by contacting candidates to appear before the Nominating Committee for an individual interview at one of its meetings. Completed application forms and any accompanying resume or curriculum vitae should be submitted to:

Arthur Reinstein Phone: (312) 786-7570 Chicago Board Options Exchange, Incorporated Fax: (312) 786-7919 400 South LaSalle Street, 7th Floor Email: [email protected] Chicago, Illinois 60605

Please also feel free to contact Terrence Andrews, Nominating Committee Chairman, at (312) 863-8044 if you have any questions regarding the nominating process or Arthur Reinstein, Legal Division, at (312) 786-7570 if you have any procedural questions regarding the nominating process or regarding how to complete this form. Date of Issuance of Application Form: July 2, 2007

3 of 7

Only Director Candidates Who Are Not Current CBOE Directors Complete Pages 4-6.

AUTHORIZATION AND RELEASE FOR THE PROCUREMENT OF A CONSUMER, INVESTIGATIVE CONSUMER, OR BUSINESS REPORT

I, the undersigned candidate for director of Chicago Board Options Exchange, Incorporated (CBOE), do hereby authorize CBOE, by and through its independent contractor, KROLL BACKGROUND AMERICA, INC. (KBA), to procure a consumer report, investigative consumer report, or business report on me. Public records may include, but are not limited to employment verifications for the previous ten years; education verifications; a social security number trace; present and past addresses; and criminal and civil history/records. I understand that I am entitled to a complete and accurate disclosure of the nature and scope of any investigative consumer or business report prepared on me upon my written request to KBA that is made within a reasonable time after the date hereof. I also understand that I may receive a written summary of my rights under 15 U.S.C. § 1681 et. seq. I further authorize any person, business entity, or governmental agency who may have information relevant to the above to disclose the same to CBOE, by and through KBA, including, but not limited to, any courthouse, any public agency, any and all law enforcement agencies and any and all credit bureaus, regardless of whether such person, business entity or governmental agency compiled the information itself or received it from other sources. I hereby release CBOE, KBA, and any and all persons, business entities, and governmental agencies, whether public or private, from any and all liability, claims and/or demands of whatever kind, to me, my heirs, or others making such claim or demand on my behalf, for procuring, selling, providing, brokering, and/or assisting with the compilation or preparation of the consumer report, investigative consumer, or business report hereby authorized. SIGNATURE: DATE:

NAME: First Middle Last OTHER NAMES USED:

(e.g. maiden name/married name/nickname) SOCIAL SECURITY NUMBER: DAYTIME TELEPHONE NUMBER: DATE OF BIRTH*: GENDER*: COMPLETE RESIDENCE ADDRESS: Current Address:__________________________________________________________________________________________________________ Street Number/P.O. Box Street Name _________________________________________________________________________________________________________________________

City State Zip Code County or Parish

Prior Address (1):__________________________________________________________________________________________________________ Street Number/P.O. Box Street Name _________________________________________________________________________________________________________________________

City State Zip Code County or Parish Prior Address (2):__________________________________________________________________________________________________________ Street Number/P.O. Box Street Name _________________________________________________________________________________________________________________________

City State Zip Code County or Parish *Without this information, KBA will be unable to properly identify you in the event KBA finds adverse information during the course of the background search.

4 of 7

5 of 7

UNDERGRADUATE DEGREE: Institution Dates of Attendance Degree Received GRADUATE DEGREE: Institution Dates of Attendance Degree Received PROFESSIONAL LICENSES: Organization State of Issuance License Number Organization State of Issuance License Number Have you ever been convicted in a military court martial? Yes No

Have you ever been sanctioned or had your licenses suspended or revoked? Yes No

Are you currently under any investigation or pending charge? Yes No

The following is applicable only to residents of California, Minnesota, and Oklahoma if this report is to be used for Employment purposes. KBA will verify your state of residence in order to determine your eligibility.

Please provide me with a copy of my background investigation report. Yes No Provide a complete employment history for the prior ten years. Use additional pages if necessary.

Dates of Employment: Name of Employer: Position/Title: Address: City State Zip Code Telephone Dates of Employment: Name of Employer: Position/Title: Address: City State Zip Code Telephone Dates of Employment: Name of Employer: Position/Title: Address: City State Zip Code Telephone

6 of 7

Dates of Employment: Name of Employer: Position/Title: Address: City State Zip Code Telephone Dates of Employment: Name of Employer: Position/Title: Address: City State Zip Code Telephone Dates of Employment: Name of Employer: Position/Title: Address: City State Zip Code Telephone

Dates of Employment: Name of Employer: Position/Title: Address: City State Zip Code Telephone

7 of 7

BOARD OF DIRECTORS QUALIFICATION CRITERIA (CBOE Constitution Section 6.1) The Board of Directors consists of 23 directors – 22 directors who are elected by the membership of the Exchange (as described below) and the Chairman of the Board, who is a member of the Board by virtue of his office. 2 At-Large Directors At-Large Director in Class III: A member who functions as a member in any recognized capacity either individually or

on behalf of a member organization. At-Large Director in Class II: A member who functions as a member in any recognized capacity either individually or

on behalf of a member organization or a person who is a CBOE Stock Exchange Permit holder or an executive officer of a CBOE Stock Exchange Permit holder.

For 2007 annual election: The at-large director position available is the position in Class III. 4 Floor Directors A member who directly or indirectly owns and controls a membership and is primarily engaged in business on the

floor of the Exchange in the capacity of a member. 1 Lessor Director A person who directly or indirectly owns and controls a membership with respect to which s/he acts solely as lessor

and who is not actively engaged in business as a "broker-dealer" or as a "person associated with a broker-dealer" as those terms are defined in the Securities Exchange Act of 1934.

4 Off-Floor Directors An executive officer of a member organization that primarily conducts a non-member public customer business and

who is not individually engaged in business on the Exchange floor. The ordinary place of business of at least one of the two off-floor directors in each Class shall be a location more

than 80 miles from the Exchange's trading floor. 11 Public Directors A non-member who is not a broker-dealer or person affiliated with a broker-dealer. For purposes of Section 6.1: A person is considered to directly own and control a membership only if the person individually and directly owns of record and beneficially all right, title and interest in the membership. A person is considered to indirectly own and control a membership only if the person: (A) has the sole and exclusive right to vote the membership and control its sale, and (B) is in possession of and subject to all of the risks and rewards of a direct owner of at least a fifty percent (50%) interest in a membership, either through ownership of an equity interest in a member organization or of a beneficial interest in a trust, which in either case is the owner of one or more memberships as permitted under the Rules. NOMINATING COMMITTEE QUALIFICATION CRITERIA (CBOE Constitution Section 4.1) The Nominating Committee consists of 10 elected members, as described below: 2 Firm Members An officer of a member organization that primarily conducts a non-member public customer business. 4 Floor Members A member who is primarily engaged in business on the floor of the Exchange in the capacity of a member. 2 Lessor Members A person who directly or indirectly owns and controls (as defined in Section 6.1) one or more memberships in respect of

which s/he acts solely as lessor. At least one of the lessor members may not be actively engaged in business as a "broker-dealer" or as a "person

associated with a broker-dealer" as those terms are defined in the Securities Exchange Act of 1934. For the 2007 annual election: Since the lessor member position that is not up for election is currently held by a person

associated with a broker-dealer, the open lessor member position may only be filled by a person who is not actively engaged in business as a broker-dealer or as a person associated with a broker-dealer.

2 Public Members Representative of the public. A CBOE Stock Exchange Permit holder or an officer of a CBOE Stock Exchange Permit holder is eligible for one of the six floor member and firm member positions on the Nominating Committee, provided that the person otherwise satisfies the qualification criteria for the applicable position (notwithstanding that the person is not a regular member or an officer of a regular member).