executive board 177 ex/54 - unescounesdoc.unesco.org/images/0015/001523/152305e.pdf · executive...

TRANSCRIPT

Executive Board 177 EX/54

Item 54 of the provisional agenda

REPORT BY THE EXTERNAL AUDITOR ON THE MANAGEMENT OF THE UNESCO OFFICE IN BRASILIA

SUMMARY

This document is submitted by the External Auditor in application of Article 12.4 of the Financial Regulations of UNESCO.

PARIS, 17 August 2007 Original: French

Hundred and seventy-seventh session

177 EX/54

REPORT ON THE MANAGEMENT OF THE UNESCO OFFICE IN BRASILIA

177 EX/54 - page 3

CONTENTS

1. PRESENTATION OF THE UNESCO OFFICE IN BRASILIA ..................................................5 1.1 The Office’s projects .......................................................................................................5 1.2 The Office’s financial resources .....................................................................................5 1.3 Cash position ..................................................................................................................6 1.4 The Office’s human resources ........................................................................................6 1.4.1 Staff employed at the Brasilia Office ................................................................6 1.4.2 Staff employed under projects ..........................................................................8 1.5 Profile of the Office’s suppliers and contractors .............................................................9

2. THE OFFICE’S EXPENDITURE ..............................................................................................9 2.1 The various expenditures ...............................................................................................9 2.2 Risks linked to the Office’s expenditure ........................................................................10 2.3 Legal risks and litigation ...............................................................................................12

3. RECENT DEVELOPMENTS IN THE OFFICE ......................................................................13 3.1 The beginning of reform ...............................................................................................13 3.2 Measures to be implemented as a priority ....................................................................13 3.3 Towards a normalized functioning of the Office? .........................................................14

4. RELATIONS WITH BRAZILIAN PUBLIC PARTNERS ..........................................................14 4.1 Evolution of projects funded by the Brazilian Government ...........................................14 4.2 Obligations exceeding the amount of funds received ...................................................15

5. COMPUTER SYSTEMS ........................................................................................................17 5.1 Harmonization of computerized accounting systems ...................................................17 5.2 Difficulties encountered by the information technology IT service ................................17 5.2.1 Human resources ...........................................................................................17 5.2.2 Predominance of ad hoc IT solutions .............................................................18 5.2.3 A costly incompatibility ...................................................................................19

6. STAFFING SITUATION AT THE OFFICE..............................................................................19 6.1 Widely varying contracts with no systematic connection to the duties performed ........19 6.2 Precarious situations ....................................................................................................20 6.3 A human resources service that is short-staffed ..........................................................20

CONCLUSION ................................................................................................................................21

177 EX/54 – page 5

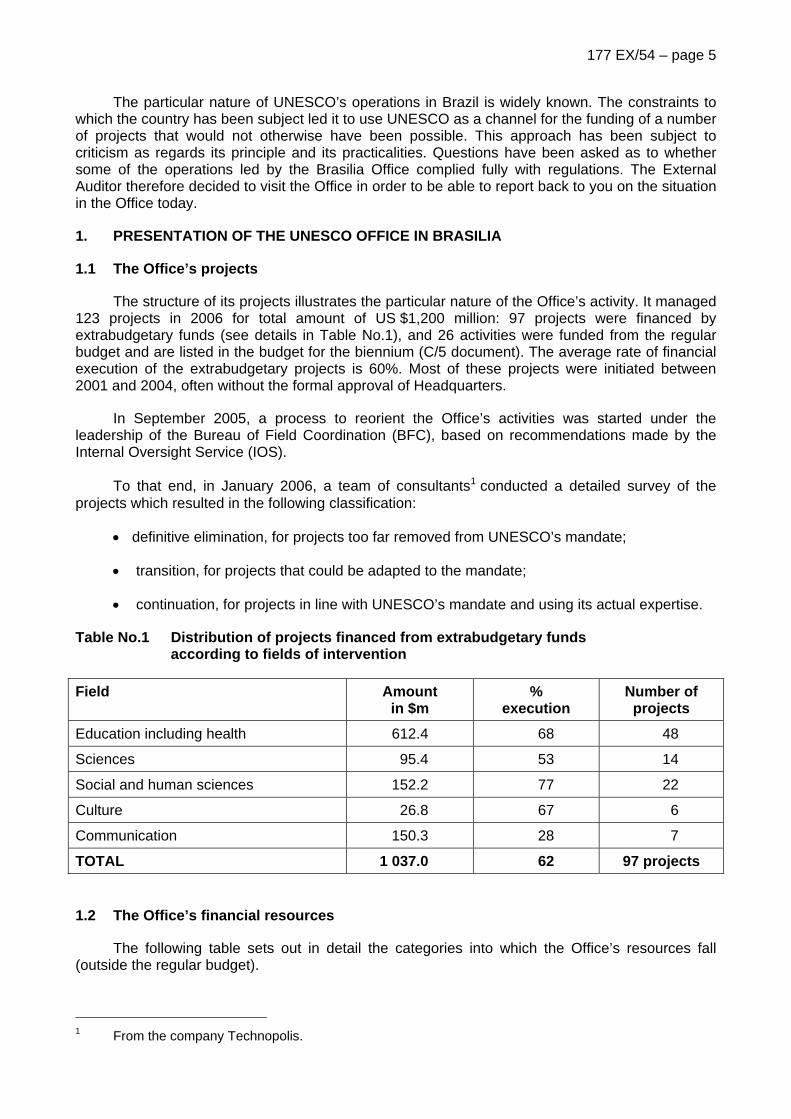

The particular nature of UNESCO’s operations in Brazil is widely known. The constraints to which the country has been subject led it to use UNESCO as a channel for the funding of a number of projects that would not otherwise have been possible. This approach has been subject to criticism as regards its principle and its practicalities. Questions have been asked as to whether some of the operations led by the Brasilia Office complied fully with regulations. The External Auditor therefore decided to visit the Office in order to be able to report back to you on the situation in the Office today.

1. PRESENTATION OF THE UNESCO OFFICE IN BRASILIA

1.1 The Office’s projects

The structure of its projects illustrates the particular nature of the Office’s activity. It managed 123 projects in 2006 for total amount of US $1,200 million: 97 projects were financed by extrabudgetary funds (see details in Table No.1), and 26 activities were funded from the regular budget and are listed in the budget for the biennium (C/5 document). The average rate of financial execution of the extrabudgetary projects is 60%. Most of these projects were initiated between 2001 and 2004, often without the formal approval of Headquarters.

In September 2005, a process to reorient the Office’s activities was started under the leadership of the Bureau of Field Coordination (BFC), based on recommendations made by the Internal Oversight Service (IOS).

To that end, in January 2006, a team of consultants1 conducted a detailed survey of the projects which resulted in the following classification:

• definitive elimination, for projects too far removed from UNESCO’s mandate;

• transition, for projects that could be adapted to the mandate;

• continuation, for projects in line with UNESCO’s mandate and using its actual expertise.

Table No.1 Distribution of projects financed from extrabudgetary funds according to fields of intervention

Field Amount in $m

% execution

Number of projects

Education including health 612.4 68 48

Sciences 95.4 53 14

Social and human sciences 152.2 77 22

Culture 26.8 67 6

Communication 150.3 28 7

TOTAL 1 037.0 62 97 projects

1.2 The Office’s financial resources

The following table sets out in detail the categories into which the Office’s resources fall (outside the regular budget).

1 From the company Technopolis.

177 EX/54 – page 6

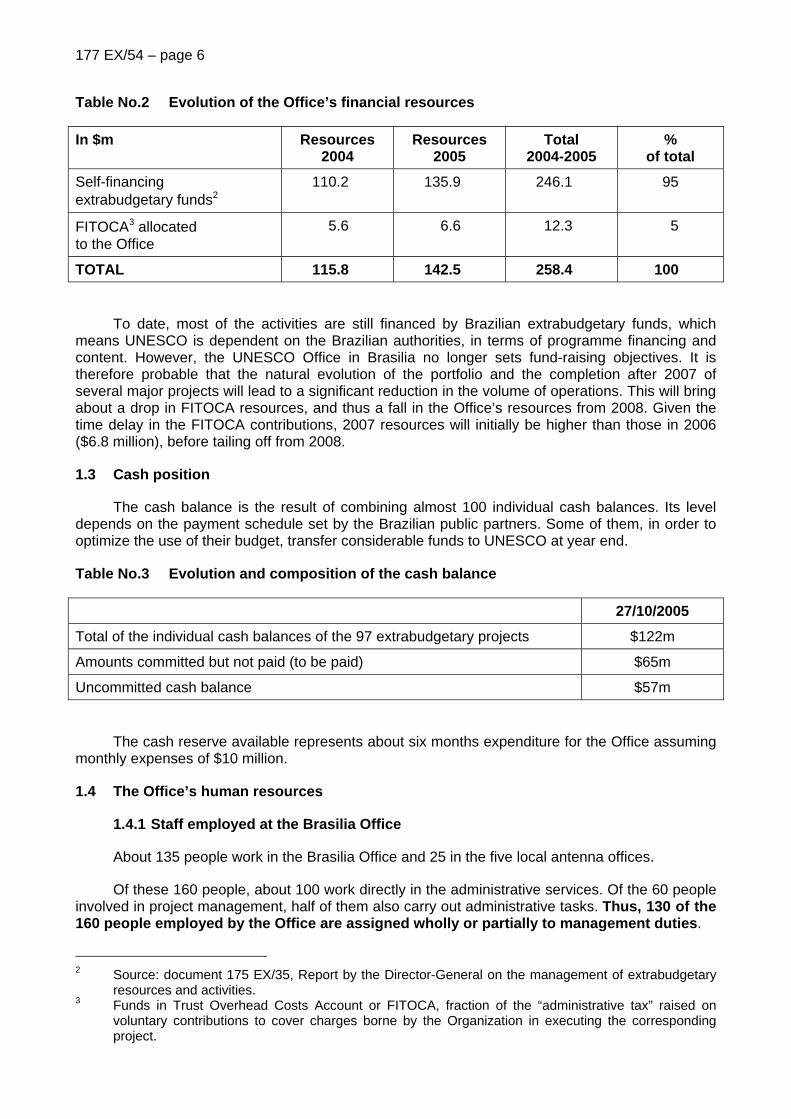

Table No.2 Evolution of the Office’s financial resources

In $m Resources 2004

Resources 2005

Total 2004-2005

% of total

Self-financing extrabudgetary funds2

110.2 135.9 246.1 95

FITOCA3 allocated to the Office

5.6 6.6 12.3 5

TOTAL 115.8 142.5 258.4 100

To date, most of the activities are still financed by Brazilian extrabudgetary funds, which means UNESCO is dependent on the Brazilian authorities, in terms of programme financing and content. However, the UNESCO Office in Brasilia no longer sets fund-raising objectives. It is therefore probable that the natural evolution of the portfolio and the completion after 2007 of several major projects will lead to a significant reduction in the volume of operations. This will bring about a drop in FITOCA resources, and thus a fall in the Office’s resources from 2008. Given the time delay in the FITOCA contributions, 2007 resources will initially be higher than those in 2006 ($6.8 million), before tailing off from 2008.

1.3 Cash position

The cash balance is the result of combining almost 100 individual cash balances. Its level depends on the payment schedule set by the Brazilian public partners. Some of them, in order to optimize the use of their budget, transfer considerable funds to UNESCO at year end.

Table No.3 Evolution and composition of the cash balance

27/10/2005

Total of the individual cash balances of the 97 extrabudgetary projects $122m

Amounts committed but not paid (to be paid) $65m

Uncommitted cash balance $57m

The cash reserve available represents about six months expenditure for the Office assuming monthly expenses of $10 million.

1.4 The Office’s human resources

1.4.1 Staff employed at the Brasilia Office

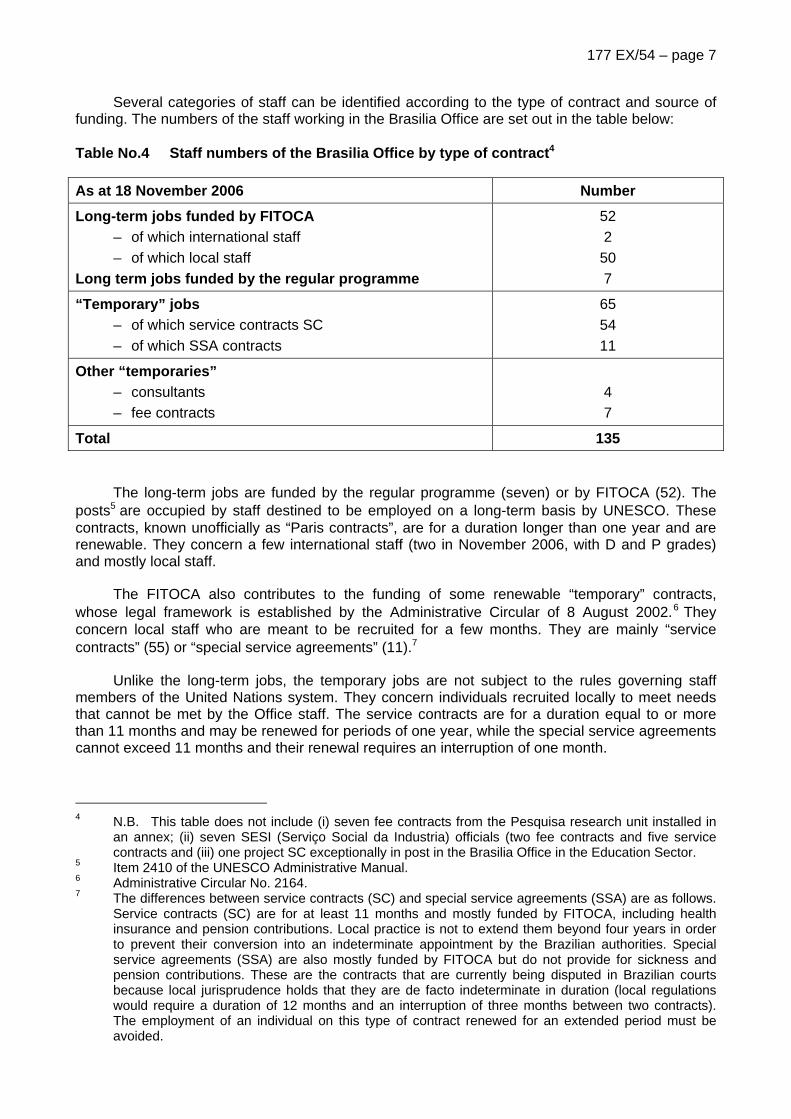

About 135 people work in the Brasilia Office and 25 in the five local antenna offices.

Of these 160 people, about 100 work directly in the administrative services. Of the 60 people involved in project management, half of them also carry out administrative tasks. Thus, 130 of the 160 people employed by the Office are assigned wholly or partially to management duties.

2 Source: document 175 EX/35, Report by the Director-General on the management of extrabudgetary

resources and activities. 3 Funds in Trust Overhead Costs Account or FITOCA, fraction of the “administrative tax” raised on

voluntary contributions to cover charges borne by the Organization in executing the corresponding project.

177 EX/54 – page 7

Several categories of staff can be identified according to the type of contract and source of funding. The numbers of the staff working in the Brasilia Office are set out in the table below:

Table No.4 Staff numbers of the Brasilia Office by type of contract4

As at 18 November 2006 Number

Long-term jobs funded by FITOCA – of which international staff – of which local staff Long term jobs funded by the regular programme

52 2

50 7

“Temporary” jobs – of which service contracts SC – of which SSA contracts

65 54 11

Other “temporaries” – consultants – fee contracts

4 7

Total 135

The long-term jobs are funded by the regular programme (seven) or by FITOCA (52). The posts5 are occupied by staff destined to be employed on a long-term basis by UNESCO. These contracts, known unofficially as “Paris contracts”, are for a duration longer than one year and are renewable. They concern a few international staff (two in November 2006, with D and P grades) and mostly local staff.

The FITOCA also contributes to the funding of some renewable “temporary” contracts, whose legal framework is established by the Administrative Circular of 8 August 2002.6 They concern local staff who are meant to be recruited for a few months. They are mainly “service contracts” (55) or “special service agreements” (11).7

Unlike the long-term jobs, the temporary jobs are not subject to the rules governing staff members of the United Nations system. They concern individuals recruited locally to meet needs that cannot be met by the Office staff. The service contracts are for a duration equal to or more than 11 months and may be renewed for periods of one year, while the special service agreements cannot exceed 11 months and their renewal requires an interruption of one month.

4 N.B. This table does not include (i) seven fee contracts from the Pesquisa research unit installed in

an annex; (ii) seven SESI (Serviço Social da Industria) officials (two fee contracts and five service contracts and (iii) one project SC exceptionally in post in the Brasilia Office in the Education Sector.

5 Item 2410 of the UNESCO Administrative Manual. 6 Administrative Circular No. 2164. 7 The differences between service contracts (SC) and special service agreements (SSA) are as follows.

Service contracts (SC) are for at least 11 months and mostly funded by FITOCA, including health insurance and pension contributions. Local practice is not to extend them beyond four years in order to prevent their conversion into an indeterminate appointment by the Brazilian authorities. Special service agreements (SSA) are also mostly funded by FITOCA but do not provide for sickness and pension contributions. These are the contracts that are currently being disputed in Brazilian courts because local jurisprudence holds that they are de facto indeterminate in duration (local regulations would require a duration of 12 months and an interruption of three months between two contracts). The employment of an individual on this type of contract renewed for an extended period must be avoided.

177 EX/54 – page 8

1.4.2 Staff employed under projects

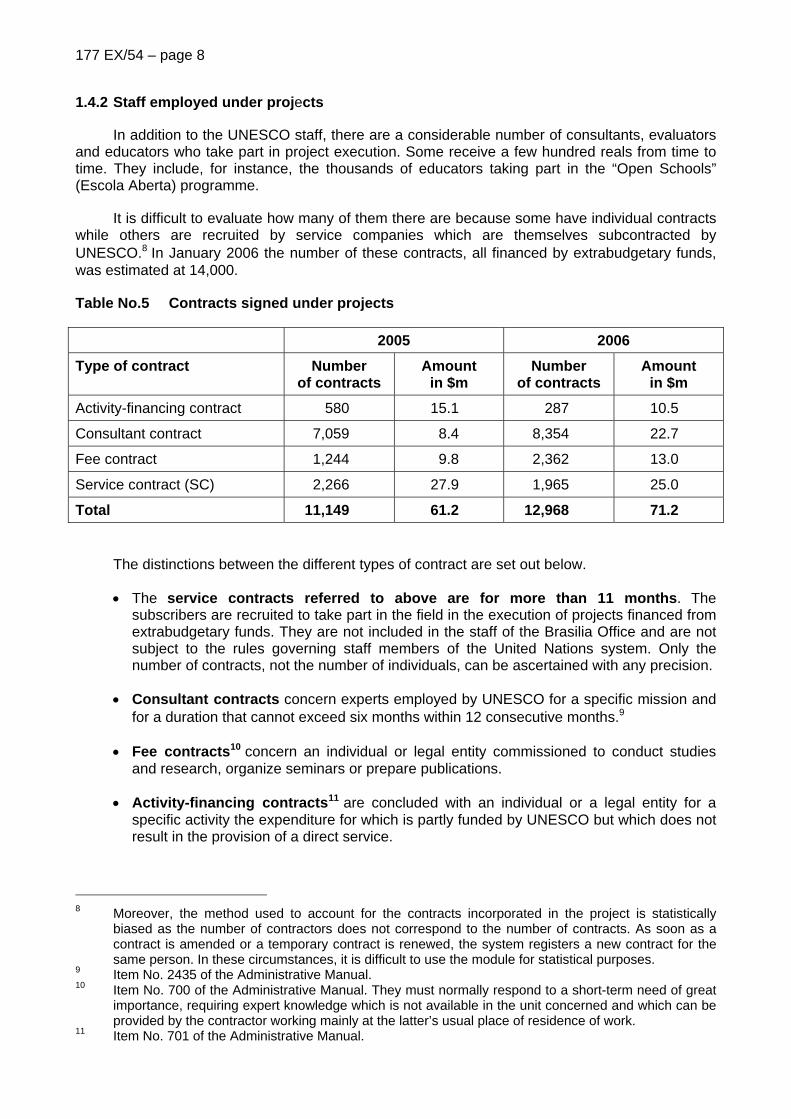

In addition to the UNESCO staff, there are a considerable number of consultants, evaluators and educators who take part in project execution. Some receive a few hundred reals from time to time. They include, for instance, the thousands of educators taking part in the “Open Schools” (Escola Aberta) programme.

It is difficult to evaluate how many of them there are because some have individual contracts while others are recruited by service companies which are themselves subcontracted by UNESCO.8 In January 2006 the number of these contracts, all financed by extrabudgetary funds, was estimated at 14,000.

Table No.5 Contracts signed under projects

2005 2006

Type of contract Number of contracts

Amount in $m

Number of contracts

Amount in $m

Activity-financing contract 580 15.1 287 10.5

Consultant contract 7,059 8.4 8,354 22.7

Fee contract 1,244 9.8 2,362 13.0

Service contract (SC) 2,266 27.9 1,965 25.0

Total 11,149 61.2 12,968 71.2

The distinctions between the different types of contract are set out below.

• The service contracts referred to above are for more than 11 months. The subscribers are recruited to take part in the field in the execution of projects financed from extrabudgetary funds. They are not included in the staff of the Brasilia Office and are not subject to the rules governing staff members of the United Nations system. Only the number of contracts, not the number of individuals, can be ascertained with any precision.

• Consultant contracts concern experts employed by UNESCO for a specific mission and for a duration that cannot exceed six months within 12 consecutive months.9

• Fee contracts10 concern an individual or legal entity commissioned to conduct studies and research, organize seminars or prepare publications.

• Activity-financing contracts11 are concluded with an individual or a legal entity for a specific activity the expenditure for which is partly funded by UNESCO but which does not result in the provision of a direct service.

8 Moreover, the method used to account for the contracts incorporated in the project is statistically

biased as the number of contractors does not correspond to the number of contracts. As soon as a contract is amended or a temporary contract is renewed, the system registers a new contract for the same person. In these circumstances, it is difficult to use the module for statistical purposes.

9 Item No. 2435 of the Administrative Manual. 10 Item No. 700 of the Administrative Manual. They must normally respond to a short-term need of great

importance, requiring expert knowledge which is not available in the unit concerned and which can be provided by the contractor working mainly at the latter’s usual place of residence of work.

11 Item No. 701 of the Administrative Manual.

177 EX/54 – page 9

The Brasilia Office does not have a computer system adapted to its needs regarding the monitoring of its contracts (about 12,000 contracts are concluded every year). In particular, it does not have readily available information about temporary contracts and has to request them from the information technology division.

Monitoring the performance of the contractors employed to lead projects is entirely delegated to the Brazilian public partners. The project managers in the Office do not have the resources to check the work carried out and in particular the tasks entrusted to contractors (hours worked, overtime, performance, relevance of tasks to the project). Accordingly, in the current configuration of the Office, it is up to the Brazilian partners to implement the project and inform the UNESCO Office of anything that might call into question the amount of remuneration.

Assessing the quality of the work provided (reports, studies, and so on) is mostly the responsibility of UNESCO’s partners, because even though some project managers in the Office are able to evaluate the work carried out, they manage too many projects to be able to carry out checks systematically.

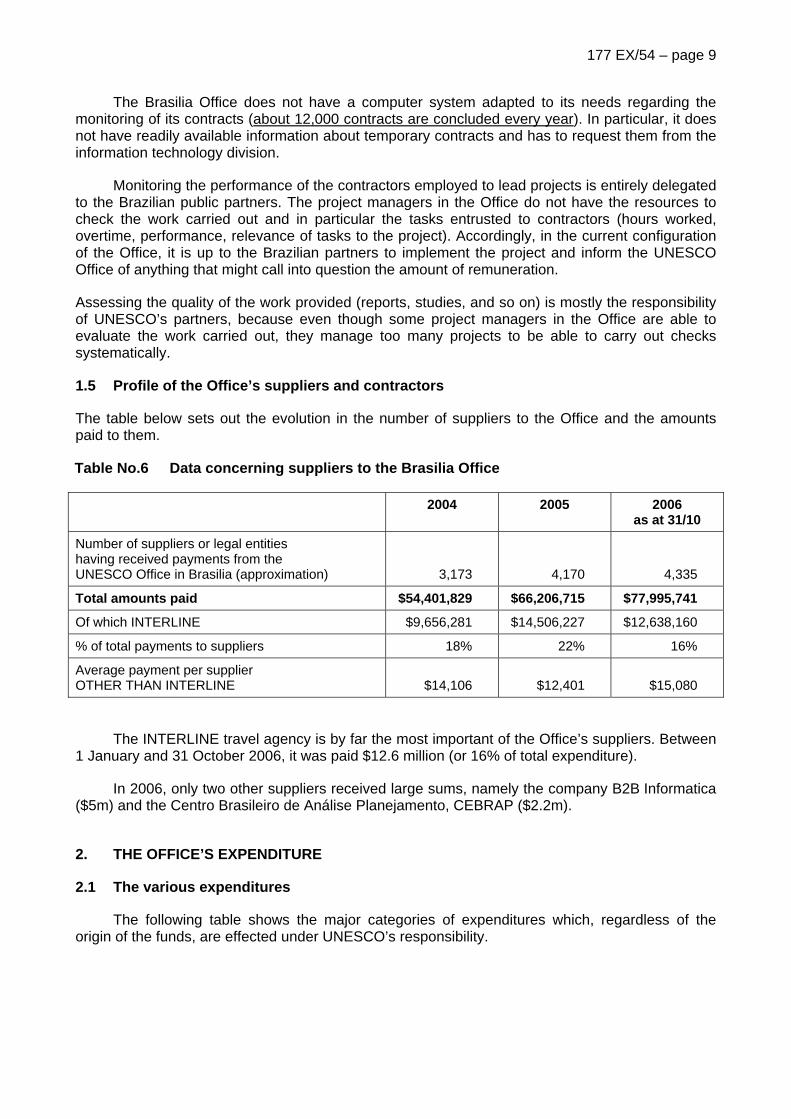

1.5 Profile of the Office’s suppliers and contractors

The table below sets out the evolution in the number of suppliers to the Office and the amounts paid to them.

Table No.6 Data concerning suppliers to the Brasilia Office

2004 2005 2006 as at 31/10

Number of suppliers or legal entities having received payments from the UNESCO Office in Brasilia (approximation)

3,173

4,170

4,335

Total amounts paid $54,401,829 $66,206,715 $77,995,741

Of which INTERLINE $9,656,281 $14,506,227 $12,638,160

% of total payments to suppliers 18% 22% 16%

Average payment per supplier OTHER THAN INTERLINE

$14,106

$12,401

$15,080

The INTERLINE travel agency is by far the most important of the Office’s suppliers. Between 1 January and 31 October 2006, it was paid $12.6 million (or 16% of total expenditure).

In 2006, only two other suppliers received large sums, namely the company B2B Informatica ($5m) and the Centro Brasileiro de Análise Planejamento, CEBRAP ($2.2m).

2. THE OFFICE’S EXPENDITURE

2.1 The various expenditures

The following table shows the major categories of expenditures which, regardless of the origin of the funds, are effected under UNESCO’s responsibility.

177 EX/54 – page 10

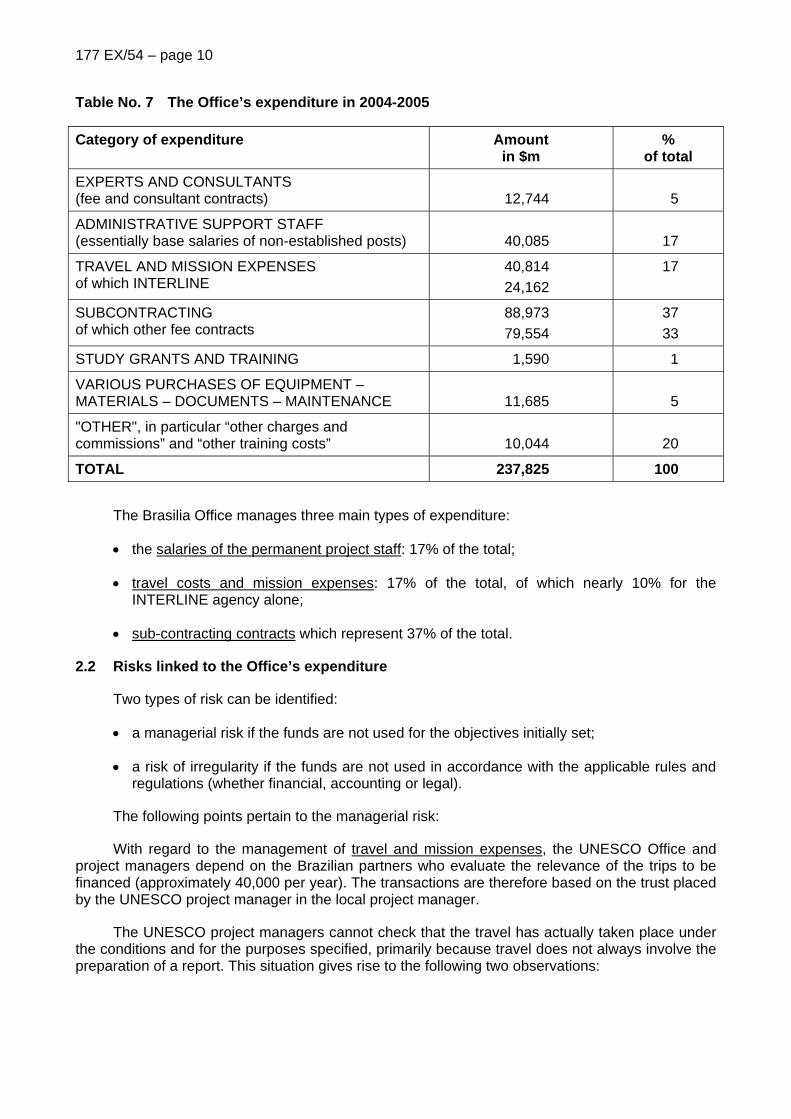

Table No. 7 The Office’s expenditure in 2004-2005

Category of expenditure Amount in $m

% of total

EXPERTS AND CONSULTANTS (fee and consultant contracts)

12,744

5

ADMINISTRATIVE SUPPORT STAFF (essentially base salaries of non-established posts)

40,085

17

TRAVEL AND MISSION EXPENSES of which INTERLINE

40,814 24,162

17

SUBCONTRACTING of which other fee contracts

88,973 79,554

37 33

STUDY GRANTS AND TRAINING 1,590 1

VARIOUS PURCHASES OF EQUIPMENT – MATERIALS – DOCUMENTS – MAINTENANCE

11,685

5

"OTHER", in particular “other charges and commissions” and “other training costs”

10,044

20

TOTAL 237,825 100

The Brasilia Office manages three main types of expenditure:

• the salaries of the permanent project staff: 17% of the total;

• travel costs and mission expenses: 17% of the total, of which nearly 10% for the INTERLINE agency alone;

• sub-contracting contracts which represent 37% of the total.

2.2 Risks linked to the Office’s expenditure

Two types of risk can be identified:

• a managerial risk if the funds are not used for the objectives initially set;

• a risk of irregularity if the funds are not used in accordance with the applicable rules and regulations (whether financial, accounting or legal).

The following points pertain to the managerial risk:

With regard to the management of travel and mission expenses, the UNESCO Office and project managers depend on the Brazilian partners who evaluate the relevance of the trips to be financed (approximately 40,000 per year). The transactions are therefore based on the trust placed by the UNESCO project manager in the local project manager.

The UNESCO project managers cannot check that the travel has actually taken place under the conditions and for the purposes specified, primarily because travel does not always involve the preparation of a report. This situation gives rise to the following two observations:

177 EX/54 – page 11

• it would appear necessary to set up a service dedicated to travel which would carry out checks on the purpose of and the arrangements for travel. This is one of the reforms envisaged by UNESCO under the TO-BE procedure12 which also makes provision for the presence of a UNESCO Office official within the partner ministries, responsible for the validation of the travel documents;

• the validation by UNESCO of the sums paid to the INTERLINE agency remains problematic. INTERLINE enters directly in the Office’s computer system the final price of the tickets invoiced. The payments are not subject to any preliminary control. An invitation to tender has been issued jointly with the United Nations Development Programme (UNDP) with a view to changing the service provider, which might be the occasion to review that procedure and eliminate direct access to the computer system.

R1 – The setting up of a service dedicated to travel, responsible for ensuring the proper functioning of travel ticket purchases, monitoring transactions and conducting specific checks, is a priority. This unit could be based on the many recommendations made in this field by the Internal Oversight Service (IOS).13

Reply by the Director-General

A travel management unit is being set up with two posts to be filled.

It should be noted that the Office is currently taking measures to implement the recommendations stemming from the IOS mission and its report 2006/16 and intensive work is being carried out to that end.

A recent invitation to tender for the services of a travel agency was issued by UNDP on behalf of several United Nations agencies in Brazil. Through the invitation to tender, a service provider other than the present one was identified, and contract negotiations are under way. The planned transfer to another provider will require substantial efforts with regard to systems integration and changes in operational practices.

With regard to the two other main categories of expenditure, namely subcontracting and temporary post salaries, the situation is comparable to that of travel: the UNESCO Office relies largely on teams of the Brazilian public partners, both for initiating the expenditure and for monitoring it.

The extent of the Office’s reliance on its Brazilian public partners varies according to the project. It reflects a problem already pinpointed by the Executive Board, namely the development of projects where UNESCO has only a role of administrative services provider. This fact has significant implications in terms of managerial risks. The problem is that for the projects in which the Office acts as service provider, and these are still the majority, it cannot ensure the relevance of the activities it is funding.

Reply by the Director-General

The Brazilian Cooperation Agency (ABC) is increasingly vigilant and strict when considering proposals for cooperation projects which are submitted to it by various federal bodies (ministries, states, municipalities), since the objective is to define as clearly as possible the contribution by UNESCO and to eliminate the service provision that was characteristic of the previous model. This requirement applies to the United Nations system as a whole.

12 The TO-BE process sets out the reforms that were considered desirable in spring 2006 in the

organization and functioning of the UNESCO Office in Brasilia. 13 IOS Audit report 2004/10 on the Brasilia Office.

177 EX/54 – page 12

On several occasions, the UNESCO Office in Brasilia has cooperated with the Federal Secretariat for Internal Control and provided all the information required in the framework of audits conducted by the Secretariat. ABC, the project entities and UNESCO have also jointly organized a number of project monitoring missions.

2.3 Legal risks and litigation

The UNESCO Office in Brazil is involved in many litigation cases, primarily linked to labour law (Brazilian law is more favourable than international law with regard to fixed-term contracts) and to certain cooperation contracts considered to be illegal.

In respect of litigation linked to labour law, the question of UNESCO’s immunity remains open. In the absence of a ruling by the Federal Supreme Court, the question has been resolved by different courts in various ways.

The most important case with regard to cooperation contracts involves the National Social Security Institute (INSS). That body had allegedly, during the implementation of a project carried out with UNESCO, remunerated possible fictitious jobs (criminal action). One of the cooperation contracts, which had not been cleared by the Brazilian Cooperation Agency as it should have been, might be deemed illegal (civil action). The same applies to the cooperation contract signed with the Ministry of the Environment in connection with the ProAgua project, mainly because it is considered to be unclear and because it was signed by the head of administrative services and not by the Director of the Office.

Moreover, the Organization remains involved in complex arrangements that put it at risk. Despite the reservations expressed in recent months, UNESCO is still associated with the Criança Esperança Programme14 under conditions that have remained unchanged since 2004. Its direct role in the collection of thousands of donations received through solidarity campaigns makes it particularly vulnerable.

Reply by the Director-General

In respect of criminal litigation, to the Secretariat’s knowledge, no criminal lawsuits have been filed against the Organization or its staff members.

The civil case concerning the INSS is still before the Supreme Court of Brazil. On that occasion, UNESCO affirmed its jurisdictional immunity, a position that was supported by the Federal State Prosecutor. Information on litigation relating to labour law can be found in 177 EX/30.

With regard to the Criança Esperança Programme, active renegotiations on the 2004 agreement are under way, which will take into account the recommendations of the Internal Oversight Service in order to address the risks run by the Organization. A meeting between the Brasilia Office, the central services, the programme sectors and two representatives of TV GLOBO was held from 6 to 8 June 2007 in that regard.

14 UNESCO’s action in Brazil is well know to the general public (press articles, annual prizes). The

Criança Esperança Programme, in particular, enjoys high visibility (partnership with TV GLOBO for a telethon, in which UNESCO took over from UNICEF in 2004).

177 EX/54 – page 13

3. RECENT DEVELOPMENTS IN THE OFFICE

3.1 The beginning of reform

The Brasilia Office has been the subject of numerous audits since 2001, seemingly justified by the exceptional nature of the situation.

The reform process was started in autumn 2005, specifically following the departure of the Director of the Office.

The process has led, among other things, to greater involvement by Headquarters in monitoring the Office’s activities which has resulted in a form of close supervision.

A review of the portfolio of projects (Doug Daniels review, January 2006) was carried out as was an analysis of procedures relating to accounting and financial functions (travel, investment policy, payments, income, contract awards, contracts, bank reconciliation, processing of interest for projects and of fluctuations in the exchange rate, budget).

In October 2006, the Office also communicated to its Brazilian partners a strategic framework to be used as a reference for new projects and revisions of existing projects. The document was the result of a major planning operation undertaken in consultation with local partners.

Reply by the Director-General

The strategic framework for UNESCO in Brazil was presented to the Brazilian authorities in Brasilia in October 2006, in Cuiaba (Mato Grosso) in March 2007 and in Porto Alegre (Rio Grande do Sul) in May 2007. In the same spirit, it is always used in meetings with current or potential partners. This programming tool has proved extremely useful in that it enables the establishment of constructive dialogue on how UNESCO can be associated appropriately with new projects, mainly with the new teams appointed after the November 2006 elections.

3.2 Measures to be implemented as a priority

The Office now has a mostly renewed management team15 and precise instructions as to desirable strategic developments.

Various reports produced recently (reviews of projects and human resources, internal audit reports, the strategic framework, reports by the Director-General) highlight a number of difficulties that penalize the Office. The points that we consider to be priorities are the following:

1. Financial relations with local public partners (especially the Ministry of Health) must be clarified: the practice of not blocking obligations when they exceed the funds received should stop, not only because it is irregular but also because it is a major impediment to ensuring the reliability of information about the Office that is available at Headquarters;

2. Mobilization of the resources needed to harmonize computerized accounting systems (SICOF-FABS) is essential;

3. Stabilization of the situation of the staff is vital.

These measures must be implemented as soon as possible.

15 A new head of administrative services took up duties in early October 2006.

177 EX/54 – page 14

3.3 Towards a normalized functioning of the Office?

By a Blue Note dated 21 April 2006, the Director-General appointed an Acting Director of the Office and entrusted him with the following mission: “In addition to the responsibilities linked to the management of the Office, Mr Defourny will continue to implement the action plan for the reorientation of the operations of the UNESCO Office in Brasilia (document 174 EX/21, Annex), in close cooperation and regular interaction with the programme sectors and central services, under the coordination of the Bureau of Field Coordination (BFC). Mr Defourny will continue to be assisted by a special team composed of external experts and staff members, including staff from the Brasilia Office”.16

The UNESCO Administrative Manual describes the competencies of established offices away from Headquarters17 as follows: “Under the overall authority of the Director-General and the supervision of the Director, Bureau of Field Coordination, and in close consultation with all Assistant Directors-General, the Director/Head of the Office will be responsible for the formulation, execution and evaluation of the programmes of the Office and for the overall management of the Office. This will include planning strategically, designing, implementing and evaluating projects and activities, taking account of multiple inputs from other Offices and Bureaux in the region and sectors at Headquarters; maintaining close consultation and cooperation with national authorities, with United Nations agencies as part of the United Nations country teams, with development banks, NGOs and bilateral organizations with a view to providing input for programming, generating projects and mobilizing corresponding funding from extrabudgetary sources. This will also include the management of the Office’s security requirements, human resources, administration and financial operations in line with the Organization’s policies and procedures, including effective internal controls”.18

R2 – At present the Office has only very limited autonomy. It would be desirable for the Director to be able henceforth to ensure the everyday management of the Office.

4. RELATIONS WITH BRAZILIAN PUBLIC PARTNERS

4.1 Evolution of projects funded by the Brazilian Government

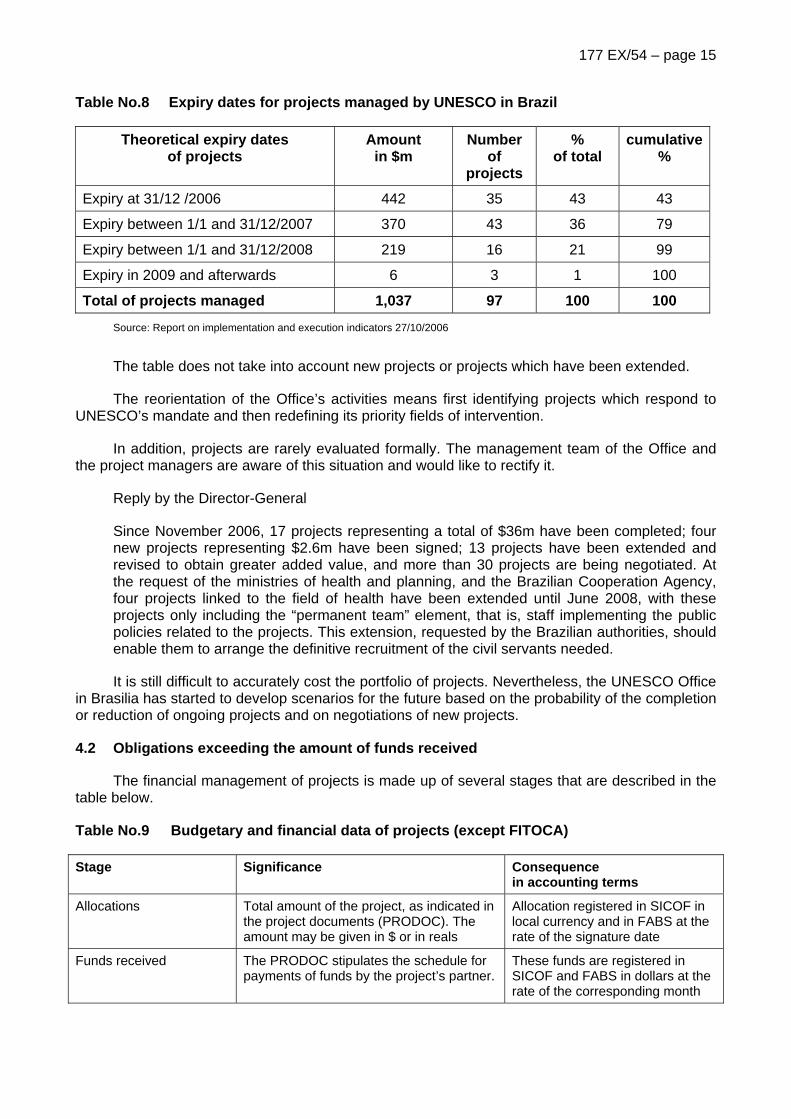

The financial relations between UNESCO and the Brazilian Government are atypical. In November 2006, of 97 projects financed from extrabudgetary funds, 77 were directly funded by the Brazilian Government. Most of these projects will have ended by the end of 2007 as the following table shows.

16 DG/Note/O6/18. 17 Item No. 140 of the UNESCO Administrative Manual, 17 July 2006. 18 Item No. 140 of the Administrative Manual also states that “BFC assists Field Offices in taking on

increased managerial autonomy by giving form to an integrated approach to management and coordination of field activities and their relationship with Headquarters through new reporting lines, ensuring that gaps and inequities … do not persist between decentralized units, sharing information and promoting lessons learned across regions”.

177 EX/54 – page 15

Table No.8 Expiry dates for projects managed by UNESCO in Brazil

Theoretical expiry dates of projects

Amount in $m

Number of

projects

% of total

cumulative %

Expiry at 31/12 /2006 442 35 43 43

Expiry between 1/1 and 31/12/2007 370 43 36 79

Expiry between 1/1 and 31/12/2008 219 16 21 99

Expiry in 2009 and afterwards 6 3 1 100

Total of projects managed 1,037 97 100 100

Source: Report on implementation and execution indicators 27/10/2006

The table does not take into account new projects or projects which have been extended.

The reorientation of the Office’s activities means first identifying projects which respond to UNESCO’s mandate and then redefining its priority fields of intervention.

In addition, projects are rarely evaluated formally. The management team of the Office and the project managers are aware of this situation and would like to rectify it.

Reply by the Director-General

Since November 2006, 17 projects representing a total of $36m have been completed; four new projects representing $2.6m have been signed; 13 projects have been extended and revised to obtain greater added value, and more than 30 projects are being negotiated. At the request of the ministries of health and planning, and the Brazilian Cooperation Agency, four projects linked to the field of health have been extended until June 2008, with these projects only including the “permanent team” element, that is, staff implementing the public policies related to the projects. This extension, requested by the Brazilian authorities, should enable them to arrange the definitive recruitment of the civil servants needed.

It is still difficult to accurately cost the portfolio of projects. Nevertheless, the UNESCO Office in Brasilia has started to develop scenarios for the future based on the probability of the completion or reduction of ongoing projects and on negotiations of new projects.

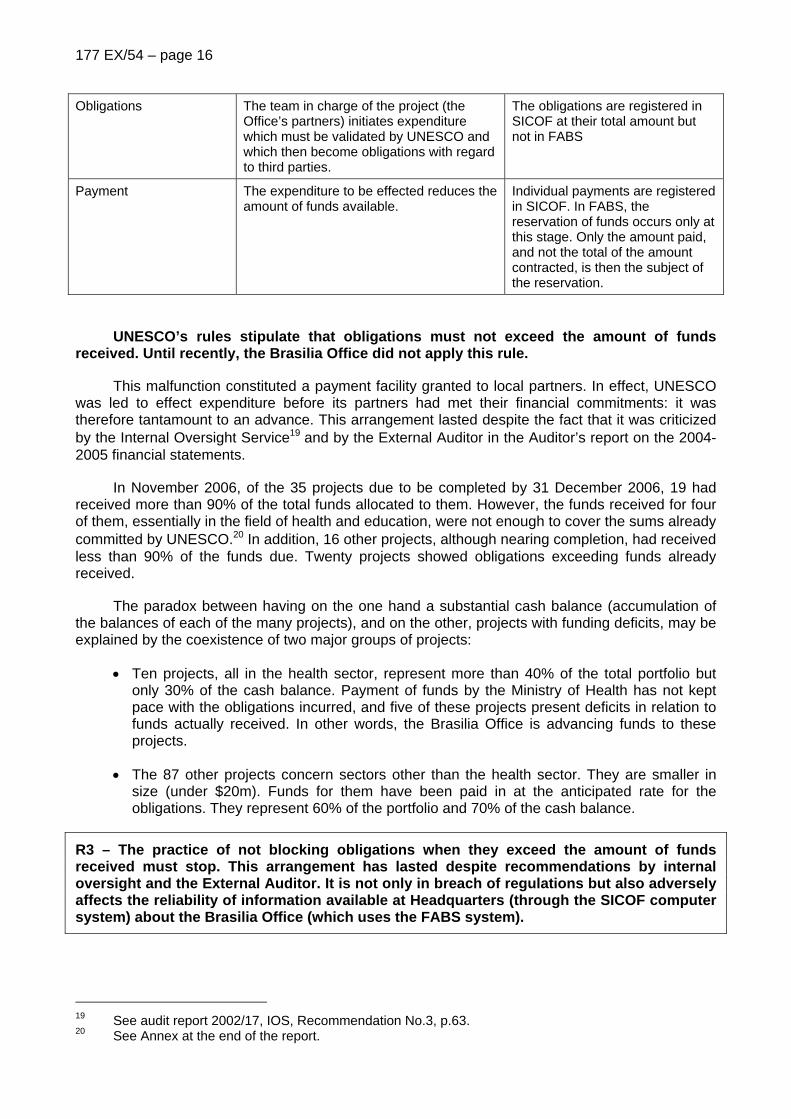

4.2 Obligations exceeding the amount of funds received

The financial management of projects is made up of several stages that are described in the table below.

Table No.9 Budgetary and financial data of projects (except FITOCA)

Stage Significance Consequence in accounting terms

Allocations Total amount of the project, as indicated in the project documents (PRODOC). The amount may be given in $ or in reals

Allocation registered in SICOF in local currency and in FABS at the rate of the signature date

Funds received The PRODOC stipulates the schedule for payments of funds by the project’s partner.

These funds are registered in SICOF and FABS in dollars at the rate of the corresponding month

177 EX/54 – page 16

Obligations The team in charge of the project (the Office’s partners) initiates expenditure which must be validated by UNESCO and which then become obligations with regard to third parties.

The obligations are registered in SICOF at their total amount but not in FABS

Payment The expenditure to be effected reduces the amount of funds available.

Individual payments are registered in SICOF. In FABS, the reservation of funds occurs only at this stage. Only the amount paid, and not the total of the amount contracted, is then the subject of the reservation.

UNESCO’s rules stipulate that obligations must not exceed the amount of funds received. Until recently, the Brasilia Office did not apply this rule.

This malfunction constituted a payment facility granted to local partners. In effect, UNESCO was led to effect expenditure before its partners had met their financial commitments: it was therefore tantamount to an advance. This arrangement lasted despite the fact that it was criticized by the Internal Oversight Service19 and by the External Auditor in the Auditor’s report on the 2004-2005 financial statements.

In November 2006, of the 35 projects due to be completed by 31 December 2006, 19 had received more than 90% of the total funds allocated to them. However, the funds received for four of them, essentially in the field of health and education, were not enough to cover the sums already committed by UNESCO.20 In addition, 16 other projects, although nearing completion, had received less than 90% of the funds due. Twenty projects showed obligations exceeding funds already received.

The paradox between having on the one hand a substantial cash balance (accumulation of the balances of each of the many projects), and on the other, projects with funding deficits, may be explained by the coexistence of two major groups of projects:

• Ten projects, all in the health sector, represent more than 40% of the total portfolio but only 30% of the cash balance. Payment of funds by the Ministry of Health has not kept pace with the obligations incurred, and five of these projects present deficits in relation to funds actually received. In other words, the Brasilia Office is advancing funds to these projects.

• The 87 other projects concern sectors other than the health sector. They are smaller in size (under $20m). Funds for them have been paid in at the anticipated rate for the obligations. They represent 60% of the portfolio and 70% of the cash balance.

R3 – The practice of not blocking obligations when they exceed the amount of funds received must stop. This arrangement has lasted despite recommendations by internal oversight and the External Auditor. It is not only in breach of regulations but also adversely affects the reliability of information available at Headquarters (through the SICOF computer system) about the Brasilia Office (which uses the FABS system).

19 See audit report 2002/17, IOS, Recommendation No.3, p.63. 20 See Annex at the end of the report.

177 EX/54 – page 17

Reply by the Director-General

On 18 September 2006, UNESCO’s partners in Brazil were informed in writing that in the future no obligation concerning the provision of goods and services would be incurred before the funds covering the totality of the amount in question had been received and allocated to the project. This letter enabled the partners to plan for the change in practice by the UNESCO Office in Brasilia and on 14 February 2007 an automatic blocking mechanism was added to the SICOF system. This has enabled the regularization of the budgetary situation for all projects as regards expenditure on goods and services (other than travel costs for the moment). At present, the Office shows no over-utilization of allotments.

In order to improve the communication of data between SICOF and FABS, a mechanism for the daily transfer of obligations registered in SICOF will be introduced in July 2007. It is a transitional solution before the full roll-out of FABS.

5. COMPUTER SYSTEMS

5.1 Harmonization of computerized accounting systems

The Brasilia Office uses the financial management software SICOF, derived from the ORACLE system, while Headquarters works with a different tool, FABS, derived from the SAP system.

It is not possible to enter into FABS the actual level of obligations incurred by the Office because for a large number of projects this level of obligation exceeds the amount of the funds received. FABS rejects these transactions, which do not comply with UNESCO’s Financial Regulations. Headquarters’ ability to monitor the budgets of the Office’s projects is consequently limited.

Since 2001 UNESCO has been planning to harmonize the two software packages. In his report to the Executive Board in October 2006 (175 EX/24), the Director-General of UNESCO said, “In order to speed up the integration of budget and financial information of UBO in the central system of UNESCO, a technical proposal for the roll-out to UBO of the FABS budget and financial module was submitted to Headquarters at the end of March 2006. Following discussion of this proposal, a second more detailed proposal was formulated at the end of June. Once a technical solution is validated, development work will start for the FABS roll-out”.

Reply by the Director-General

A project charter organizing the transition to FABS was adopted in April 2007. The charter sets out five phases and a schedule for interventions which runs to spring 2008. It establishes a Project Committee, chaired by the Comptroller, and bringing together representatives of the central services, representatives of the Brasilia Office and operational and technical teams. The first phase of evaluation and planning is nearing completion.

5.2 Difficulties encountered by the information technology IT service

5.2.1 Human resources

A certain disparity may be noted between the current composition of the IT division and the minimum skills it should master, in particular in order to manage the projected migration of SICOF to FABS.

Of the 17 posts in the division’s organizational chart, five remained to be filled at the date of our audit, including that of head of the service. In addition to a possible staffing shortage, there is the question of the skills in place, which do not perfectly match needs.

177 EX/54 – page 18

In a context where the workload has been increased by the reorientation of the Office, the situation is thus characterized by the lack of an IT director who would have the experience and authority required to engage with the Division of Information Systems and Telecommunications (DIT) at Headquarters and the Division of the Comptroller (DCO).

5.2.2 Predominance of ad hoc IT solutions

In the absence of planning for the measures necessary to harmonize the computerized accounting systems, the Office’s IT specialists have had to develop case-by-case ad hoc solutions, which might involve meeting the Office’s needs or, in conjunction with DIT at Headquarters, improving communication between the two systems in a specific area.

One recent example was the creation of a SICOF module enabling the payment schedule of UNESCO’s partners, and not only the total amount of the donation, to be taken into account. This adjustment to the system was developed by two workers in the IT service without, for instance, planning rigorous and exhaustive validation tests.

Over the course of a year, the IT division makes several hundred modifications of this kind. They are developed according to the wishes of the users but the requests are not necessarily shared.

In addition, the Office’s server is highly unstable and has to be reconfigured every five to six weeks without the origin of the malfunctions having been identified.

Lastly, some of the recommendations from previous audits have still to be implemented. For example, the Office’s network is still connected to the network of a sub-contracting company (SBPI) even though formal separation was strongly advised by an audit dating from 2002 (Brisa report). Several individuals who have left the Office are still on the list of network users even though the Internal Oversight Service recommended that removal from the list should take place at the same time as separation (recommendations 3 and 4, pages 17 and 18, of IOS/2004/Memo 19 of 25 June 2004). It has also been noted that there is still room for improvement in the data safety policy, which was the subject of several recommendations in 2002 (Brisa report): the most recent simulations of full data recovery date back to February and March 2005.

The Office is considering contracting some of its IT services (and even, more broadly, a few administrative services) to Headquarters, to a private company, or to another international organization present in Brasilia. This outsourcing would enable specialist staff to be used, the number of which could more easily be adapted to the probable reduction in the Office’s portfolio.

R4 – We recommend the recruitment as soon as possible of a high-level IT manager. The IT division of the Brasilia Office is a function that must not be overlooked just because it is technical. For a body that manages projects worth several hundred million dollars, makes more than 1,000 payments every day and manages a balance of $130m, the existence of a robust and reliable IT service is absolutely essential. Unless the function can be professionalized and the necessary resources devoted to it, the Office will have to work with local solutions, which are at the root of poor communication with Headquarters. The implementation of the recommendations of the External Auditor (set out in the report on the financial statements for 2004-2005) involves the harmonization of SICOF and FABS.

Reply by the Director-General

Responsibility for the IT team has to date been in the hands of a member of that team who is still exercising that function ad interim. Nevertheless, a recruitment process was launched on 25 May 2007 and the IT manager should be appointed in early July 2007.

177 EX/54 – page 19

5.2.3 A costly incompatibility

The administrative teams in the Office and at Headquarters devote a great many hours to reconciling the data generated by FABS and SICOF and correcting anomalies. On the basis of interviews conducted during our audit, we estimate the workload associated with these tasks to be the equivalent of five to six full-time posts for the administrative services in Brasilia alone.

• Reconciling the financial statements of FABS and SICOF requires the equivalent of one person working full-time for one year. It was estimated that in 2006, three to four people in the accounts service devoted 80% of their time over three months (March, April and May 2006) to validating, manually, the 162 provisional financial statements established by FABS using data from SICOF. Indeed, the initial financial statements are wrong by their very construction: they are established in FABS, using data supplied from SICOF by means of an Excel file which does not contain the amounts of the obligations.21

• Processing the funds reservations rejected by FABS also occupies one person full time. Requests for payment are charged per project to a different budget line according to their nature. However, as neither the project coordinator nor the UNESCO Office monitors the use of funds per line, the payments often exceed the funds available on the budget line concerned. The FABS system, unlike the SICOF system, systematically checks the availability of funds for each line, and rejects several dozen transactions every day. In order to process them, the Office staff, working with the Bureau of the Budget (BB) at Headquarters, have to charge them individually.

Processing the transactions rejected by FABS in a suspense account also takes up the equivalent of one person working full time for three months a year, and processing bank reconciliations and imprest accounts takes three people working full time.

6. STAFFING SITUATION AT THE OFFICE

6.1 Widely varying contracts with no systematic connection to the duties performed

The contractual situations of employees varies widely and does not necessarily match the nature of the duties performed. By way of example, one individual, remunerated by a fee contract concluded under a specific project, in fact works in the accounts service analysing the financial statements and carrying out financial audits.

In the non-statistical sample of contracts examined, there was also the case of an employee who, for carrying out similar tasks, was employed first as a consultant22 (for nearly one year), then under a special service agreement (for 13 months, which is in breach of the regulations) and finally under a service contract (for three months).

These observations apply in the same way to staff in the Antenna Offices who continue working indefinitely but are employed on temporary contracts that are usually renewed when they run out. The Office explains this discrepancy by the transition strategy which makes it reluctant to stabilize any situation. In the Antenna Offices, the contractual regimes are varied (even though they perform similar duties, the staff in Sao Paolo are employed as consultants and those in Rio de Janeiro have service contracts). The situation of the coordinators is particularly unsatisfactory as

21 It should be recalled that the Office does not communicate to Headquarters its obligated payments

because the Office does not comply with the financial rule that obligations must not exceed funds actually received. The daily registration of the transactions of the Brasilia Office in FABS, which in theory registers the full obligation to be noted before any payment is made, only occurs after the effective payment in the bank and only for the amount paid in.

22 These long-term consultant contracts have been until now authorized under the local administrative manual. This type of contract is due to be abolished.

177 EX/54 – page 20

they are usually financed from the funds of a particular project but perform cross-cutting administrative tasks. It would be desirable to harmonize contracts.

6.2 Precarious situations

Service contracts have been renewed on several occasions for two or three months, periods which are shorter than that which the Administrative Circular of 2002 stipulates as being applicable for such contracts. This situation is a probably inevitable consequence of the reorientation process implemented by the Office but it remains a source of uncertainty and demoralization for the staff concerned. All these contracts were recently extended for a period of six months.

R5 – We recommend that the atypical utilization of temporary contracts should be as limited as possible, not only because it is based on the use of contracts that do not correspond to the purpose for which they were concluded, but also because these precarious situations are a source of demoralization and heighten the risk of losing competent, experienced staff. The regularization of contractual regimes is necessary as is a forecast of staffing trends in the Office.

6.3 A human resources service that is short-staffed

The current head of the human resources service (grade NO A) is under the authority of the head of administrative services. She is assisted by one official (grade L4). Her job description includes 13 specific missions which cover essentially (i) monitoring procedures to recruit local staff, (ii) day-to-day management of the Office’s human resources (staff records, monitoring overtime, and so on) and also (iii) training activities and (iv) the proper application of safety regulations.

Previously, the two employees in the human resources service had been under the authority of a P-4 level official who also ran the contracts service. The abolition of this post was justified by the separation of the two services.

R6 – We recommend the strengthening of this unit which is short-staffed. This strengthening is especially desirable because during the reorganization period the head of administrative services does not have the time to be involved in human resources management.

Reply by the Director-General

During the first half of 2007 it was not possible to make significant headway on this matter, and temporary contracts (service contracts and special mission contracts) have been extended until the end of the year. It is planned to conduct an overall review of the structure in mid-2007 based in particular on the gradual introduction of the “to-be” process and the reconsideration of the main management and oversight processes. This work of structural redefinition will be combined with a post review so as to identify posts that are essential regardless of the size of the Office and posts that are directly linked to the volume of activity. Discussions are under way with the Bureau of Human Resources Management (HRM) with the aim of seconding a staff member to Brasilia to carry out the post review and consolidate the Office’s human resources management structure.

HRM and BFC will review the situation of contractual arrangements in the field with a view to responding more appropriately to the specific needs of the field offices while improving the employment conditions of contractors such as length of service and matters of remuneration and social security.

177 EX/54 – page 21

The Director-General is, in principle, in favour of strengthening the functions of the Administrative Officer (AO) and human resources in order to ensure rigorous management of administrative and financial transactions and more modern staff administration.

CONCLUSION

UNESCO’s financial statements show the considerable weight of the activities of the Brasilia Office, as the expenditure of the Office amounted to $238m in the 2004-2005 biennium, that is, more than 50% of all the Organization’s expenditure charged to extrabudgetary funds and 20% of UNESCO’s total expenditure ($610m under the regular programme and $523m extrabudgetary funds). The reasons for this situation are well known – as are the risks.

The Office has some 135 staff members. However, more than 10,000 individuals take part in projects and thus receive remuneration, occasionally or regularly, from UNESCO.

As the depositary and manager of funds, UNESCO’s responsibility is engaged and it must in particular ensure that the resources are used for the stated objectives, in the framework of its mandate and in accordance with applicable rules.

UNESCO’s operations in Brazil depend almost entirely on extrabudgetary funds received from Brazilian public partners. UNESCO is thus used as an administrative services provider in the implementation of important public policies. Under the terms of a decree of July 2004, the Brazilian authorities officially stated their intention of abandoning this model.

UNESCO’s withdrawal from projects which do not comply with its mandate is still far from complete. The decision to shut down some projects on 31 December 2006 was unrealistic as important national partners did not seem ready to take over. The transfer of thousands of consultants employed in Brazilian bodies but remunerated by UNESCO is complex, especially in the field of health: it is to be hoped that the working group that has been set up composed of representatives of the Office and the Brazilian authorities will rapidly reach agreement on the completion or resumption of the projects concerned.

* * *

The extent of the Office’s dependency on its Brazilian partners differs according to the project. In those, and they are still the majority, where the Office is acting as an administrative services provider, it does not have the resources to check the relevance of the operations it is funding and the activities it carries out. As a result, the Office processes many transactions without always knowing the details of them: this is the case in particular for travel costs and mission expenses (17% of the total, of which 10% is for the INTERLINE agency alone), sub-contracting contracts, which account for 37%, and the salaries of individuals employed to manage projects.

The quality of project management also depends far more on the project coordinators, who are often ministry officials, than on UNESCO’s project managers.

Given the way the Office has worked for several years now, and given the large number of transactions and sums that have transited through it, the possibility that breaches of the regulations have occurred cannot be excluded. However, our work has not revealed any new instances of a potentially fraudulent nature. The management of this risk of litigation is up to UNESCO and our role, in this instance, consists of drawing attention to the risks inherent in the system.

* * *

177 EX/54 – page 22

The UNESCO Office in Brasilia has been in a reorientation phase since September 2005. The management team has been mostly renewed. The Office should now complete its transition phase and return to a normal way of functioning.

There are deliberately few recommendations contained in this report, because there have been numerous audits, evaluations and analyses of the Office since 2001 and a great many recommendations (over 100) have already been made. That is why we decided to try and focus our observations on those elements we considered to be vital. We did not want to draw up a long list of recommendations that would only add to the others and would have maintained a certain confusion as to the way ahead.

Printed on recycled paper