exhibit 2 kitchenware in the uk: an overview - squarespace · exhibit 2 kitchenware in the uk: an...

TRANSCRIPT

ICAEW/CS/J17 Page 7 of 40

EXHIBIT 2

Kitchenware in the UK: an overview

Definitions

Kitchenware may be divided into three categories:

Tableware: dishes used for setting a table, serving food and dining. It includes cutlery or flatware (knives,

forks and spoons), crockery (plates, saucers, bowls and cups/mugs), glassware, serving dishes and other items

fulfilling practical and/or decorative purposes. Quality and design vary according to culture and cuisine.

Cookware: pots and pans (used on a hob), ovenware (used in conventional and/or microwave ovens) and

bakeware (also used in ovens).

Utensils: small handheld tools used in the preparation and serving of food. They include items for preparing

food (eg, knives, peelers); cooking tools (eg, wooden spoons, spatulas); serving implements (eg, ladles); and

measuring devices (eg, jugs, scales).

Kitchenware can be bought in many types of store, including kitchenware specialists, department stores and

supermarkets, as well as online and via mail order catalogues.

UK market trends

The total size of the UK kitchenware market is estimated at over £0.5 billion. It is influenced by a number of

factors.

Demographic issues

The number of UK households and average number of occupants have both steadily increased in recent years.

The latter has significant implications for buyer behaviour, fuelling the demand for both larger cookware items

that can cater for more people and bigger quantities of tableware.

Cooking trends

According to research by Mintel, every day around 10 million UK households (38% of the total) cook from basic

ingredients, and 21% of adults spend extra money on food and drink at home for a special occasion. These factors

are helping to stimulate demand for kitchenware. Home baking is popular, as both a necessity and a leisure

activity. The growing number of television programmes devoted to food and cookery has also had a major impact.

Prominent among these are The Great British Bake Off and MasterChef, both originating in the UK but now

replicated in many countries around the world. Celebrity tie-ups (where a well-known figure from the world of

cookery – often someone associated with a food and cookery programme – endorses a company’s products) are

common.

Consumers continue to live increasingly fast-paced lives, affecting demand for convenience in cooking (time-

saving benefits and ease of use). This has had a strong effect on the industry, leading to innovations such as new

utensils and improved non-stick surfaces. However, there has also been a negative impact: the availability of ready

meals from shops is limiting the frequency with which some households use cooking equipment, and this in turn

restricts potential demand and volume of sales. (Ready meals are packaged meals that simply need to be reheated

before being eaten.) Eating out at restaurants also remains popular.

Globalisation has driven the popularity of international foods over recent years, encouraging consumers to

experiment more in their home cookery. The popularity of spicy Thai and Indian food, in particular, has surged,

leading to a large rise in ownership of woks and in dishes used for preparing curry. Companies have attempted to

exploit demand by bringing more specialist cookware products to market. Such products represent an important

potential growth opportunity in an increasingly saturated market.

ICAEW/CS/J17 Page 8 of 40

Companies and brands

This is a diverse market, characterised by a wide range of companies and brands. Many leading brands in the UK

are owned by international companies. These include Amefa (Netherlands), Villeroy and Boch (Germany) and

Meyer (US). British companies include recent arrivals such as Joseph Joseph and Emma Bridgewater, among

more established companies such as Churchill China and Arthur Price.

A vast array of retailers sell kitchenware. Supermarkets and some other large chains such as IKEA account for

around 50% of the market, selling large volumes of relatively low-priced goods. Department stores, such as John

Lewis, are the main destinations for higher-quality goods (30% market share). The remaining 20% comes from

specialists, such as Lakeland, Kitchens Cookshop and Steamer Trading.

Brand awareness is strong, with the distinctive style of established names such as Tefal, Le Creuset and Pyrex.

Research shows these to be well known and likely to be recommended to friends, as well as being brands that

people feel are “worth paying more for”. Premium products are largely perceived to represent value for money

owing to their durability.

Sales drivers

Increased availability of products online is threatening specialist kitchenware retailers and reducing profit margins

for manufacturers. With the rise in ownership of smartphones and tablets – and the improved standard of websites

(so that consumers can form a good visual impression) – it is easier and more convenient than ever to browse and

shop on the internet. Further growth in online shopping is expected in the coming years.

Around 60% of UK consumers buy kitchenware each year, especially items in regular use (eg, cups, mugs and

glasses) and – to a lesser extent – baking tins and pans. The biggest driver of demand is replacement of damaged

items. Many say that upgrading is important to them when they buy a replacement. “Easy-care”, “long-lasting”,

“low-cost” and “versatile” are the main factors that they cite. Many consumers see cookware as a treat or as an

excellent gift for others.

ICAEW/CS/J17 Page 9 of 40

EXHIBIT 3

The UK kitchenware industry: key issues

Overview

Companies operating in the UK kitchenware sector typically sell their products to retailers, which then sell them

to consumers. Some also sell through their own retail stores, and many also sell direct to consumers, whether

online or through mail order catalogues.

Some companies additionally sell their products to corporates that provide catering services – notably offices

and other business premises, restaurants, hotels, cruise ships, sports and conference venues, as well as public

sector entities such as schools and hospitals.

In each of these different selling models, there are some companies that sell exclusively within the UK and

others that also sell to overseas customers.

There are also variations in manufacturing. Larger companies traditionally manufactured their own products in

their own factories, whether in the UK or overseas. In more recent years, there has been a tendency to outsource

production (and other key business processes, such as distribution) to other companies, again both in the UK

and overseas.

Kitchenware companies that outsource their production usually work closely with the manufacturers on the

design and quality of the products and on operational matters such as timescales and sizes of production runs.

Pricing

The price at which kitchenware companies sell products to retailers needs to cover their costs and earn a profit.

Retailers in turn need to be able to sell them to consumers at an acceptable profit.

Price is a major consideration for consumers. Many correlate price with performance but, if the price of a

product is too high, some consumers will not consider it to represent value for money and others may be unable

to afford it. However, there are many products that are viewed as essentials and therefore always in demand.

Diversification

As in other industries, many kitchenware companies look to diversify, for example by selling ancillary products

such as table linens, mats/coasters and small electrical goods (kettles, toasters). This creates the significant

advantage of cross-selling as the target market for all these products is essentially the same. The disadvantage is

that a company may have too many products and be unable to identify a true profit margin for each, to control

inventory or to optimise product mix.

Quality, performance and durability

A challenge for companies in this industry is to offer products of the ‘right’ quality and durability. They need

consumers to be replacing existing items and buying new ones. They need to have a large enough range of

products so that something new or different is always available to consumers.

Consumers expect metal coatings and non-stick surfaces to be durable, and they are willing to pay more for a

product that will last and that is perceived to improve the quality and/or appearance of their cooking or their

kitchen. This is reflected in the fact that some premium cookware products come with lifetime guarantees.

However, most items will not last indefinitely, and so the ability to replace them if damaged is also important.

People who have a set of tableware that they love are unlikely to buy a totally new set just because they have

broken a few plates. The ready availability of individual replacements – especially for items that are no longer

being manufactured – can therefore also influence consumers’ buying behaviour.

ICAEW/CS/J17 Page 10 of 40

Similarly, corporate users of kitchenware such as hotels and restaurants need products that are durable, easy to

clean – whether by hand or by machine – and (especially at the upper end of the market) attractive to look at. They

will always expect a certain level of breakages or damage (or even theft) and will either ensure that they buy

enough of each product to allow for these or expect their suppliers to be able to provide them with replacements at

short notice.

Product design

Design is important, for both aesthetic and practical reasons.

Consumers are particularly influenced by the appearance of products that are likely to be on display at home,

such as casserole dishes that might be taken to the table at a dinner party, saucepans that openly hang in the

kitchen when stored, or utensils such as blocks of knives on the kitchen worktop. ‘Retro’ products (ie, those

based on designs from the past) can also be popular.

Consumers are also attracted by innovative concepts that enhance ease of use. Big technological developments

are relatively rare as the market is mature, but companies continue to improve products by introducing new

features.

Brand management

A critical success factor for companies in this industry is their brand management. They spend time, money and

effort on research to find out how their brands are perceived by consumers, and this in turn impacts the level and

location of any advertising, as well as the pricing of their products.

Supply chain management

The ability to manage the whole supply chain is crucial. Whether a company manufactures its own products

(and therefore needs to source raw materials, equipment and energy) or outsources its manufacturing, it must be

able to rely on its relationships with a range of other companies.

ICAEW/CS/J17 Page 11 of 40

EXHIBIT 4

Piccolo: Company overview

Introduction Piccolo earns its revenue from the sale of tableware, cookware and utensils to business customers in the Retail and Hospitality sectors across the UK. All sales are in £ sterling. Piccolo outsources production to specialist manufacturers, both within the UK and overseas. It works closely with these manufacturers in designing its products and ensuring that they are of the requisite standard. Piccolo does not undertake any manufacturing of its own. Piccolo’s base is in Birmingham, around 160 kilometres from London. This comprises the head office and storage areas plus product innovation and design facilities.

History

Piccolo was founded in 1993 by Eliza Fitzwilliam, a successful piccolo player who – when she was not rehearsing or playing in concerts – enjoyed spending time in her kitchen. Eliza often could not find in the shops suitable items to prepare and cook her food, or elegant tableware on which to serve it. She was particularly annoyed by the apparent lack of labour-saving devices. On mentioning her frustrations to friends and fellow members of her orchestra, she found that many people felt the same way. So, with the help of a cousin, a successful banker in the City of London, she created Piccolo.

Piccolo initially manufactured and sold kitchenware to department stores in London’s West End. With a fixed-term loan, it acquired a disused site near Birmingham and turned this into a head office building and factory, viewed as one of the most modern of its time, with state-of-the-art equipment and efficient production scheduling. It employed staff on shifts around the clock to meet demand, notably at the peak Christmas period. The customer portfolio was extended to include upmarket restaurants and hotels. The business prospered and the loan was repaid on schedule.

By 2007, although the name was well known and respected, Piccolo had lost its way in terms of strategic direction. It had started to experience cashflow problems, and was taken over. Eliza left the company and the new management team, all with experience in the industry, vacated the factory part of the site (retaining use of the head office building), outsourced all manufacturing and rationalised the portfolio of products. This enabled Piccolo to reposition itself as a premium supplier of top-quality kitchenware in time for its 15th anniversary year, under the slogan ‘Pick a Piccolo’.

Piccolo is now a design, sales and marketing operation. Its success can be attributed to a clear market position, a reputation for the quality and resilience of its products, and a consistent marketing message.

Key personnel

Directors

Although there have been several changes in personnel since 2007, the company is still mainly led by those responsible for turning it around at that time. They comprise:

Clive Oaks (Managing Director, with responsibility for HR)

Sabrina Kroos (Finance and IT Director)

Gautam Singh (Marketing Director)

Daniel Lejeune (Product Innovation and Design Director)

Tamsin Wright (Sales and Operations Director)

ICAEW/CS/J17 Page 12 of 40

Sabrina, who is an ICAEW Chartered Accountant, is responsible for all aspects of the company’s finances, including the management accounts, performance measurement and budgeting.

The directors hold quarterly board meetings to discuss strategic, financial and operational issues. At their July 2016 meeting, the directors developed a strategy for the two years to 31 May 2018, which was accompanied by ‘high’ and ‘low’ budgets for the first of the two years (see Exhibit 12).

Lucy Tyler

Piccolo is heavily dependent on celebrity chef Lucy Tyler. Her endorsement is central to the success of many of its products. A protégée of Aaron Swepson, another celebrity chef, Lucy is one of several new figures to have emerged on the UK food scene in recent years.

Lucy’s Italian aunt instilled in her an appreciation and love of good food at a young age. Some years later, while at university, Lucy took a holiday job working in the kitchen on a cruise ship. Her culinary skills were noticed when she covered at very short notice for the sous-chef after he had to leave a transatlantic voyage because of a family bereavement.

On graduating, Lucy joined the team at a London restaurant, The Coronet, under Aaron Swepson. She soon made a strong impression and saw the restaurant achieve its first Michelin star – a hallmark of fine dining quality. She first came to public attention when she was asked to present a children’s cookery programme on UK television. She went on to appear in a documentary series advising obese adults and children on the benefits of healthy eating. She is now one of the most recognised people on UK television – both from these roles and, since 2013, as the face and voice of Piccolo on its advertising.

Under the terms of its contract with Lucy (renewable on 31 May 2018), Piccolo pays her an annual fee on 31 May, covering her work for the year then ending, plus a success fee if revenue reaches an agreed target. Amounts paid to Lucy have been as follows:

Year ended 31 May 2014: £600,000

Year ended 31 May 2015: £700,000 (plus £100,000 success fee as Piccolo achieved its revenue target of £39.2 million)

Year ended 31 May 2016: £750,000 (plus £150,000 success fee as Piccolo achieved its revenue target of £41.5 million)

The agreed fee for the year ending 31 May 2017 is £800,000, plus a success fee of £200,000 if revenue reaches £44.0 million.

Products

Piccolo’s products are in the following three categories (see also Exhibit 7):

Piccolo Tableware: serving dishes, plates, cups/mugs and bowls. Piccolo does not sell glassware

or cutlery.

Piccolo Cookware: pots, pans and baking vessels. These include items that are usable on electric and/or gas hobs and in conventional and/or microwave ovens.

Piccolo Utensils: a wide range of products such as peelers, metal and wooden spoons, mixing bowls, measuring jugs and ladles.

Customers

Piccolo serves two markets, both of them exclusively within the UK: Hospitality and Retail.

Hospitality customers comprise restaurants, hotels and conference centres. Retail customers are mostly the leading department stores, supermarkets and specialist kitchenware shops.

ICAEW/CS/J17 Page 13 of 40

These form two separate business lines. Retail is by far the larger, typically accounting for almost 80% of annual revenue. Customers in each case include both large and medium-sized chains and some smaller independent businesses (see Exhibits 8 and 9). Piccolo sells all three categories of products in its Retail business line but only tableware and cookware to its Hospitality customers. Shares of total revenue have remained relatively constant in the two years ended 31 May 2016, as follows: Hospitality Retail

Piccolo Tableware 70% 60% Piccolo Cookware 30% 30% Piccolo Utensils - 10%

Suppliers

Piccolo relies extensively on its supply chain to be able to service its customers. Its key suppliers are the manufacturers of the products that it sells (Exhibit 10) and the distribution company RDN (Exhibit 11). Piccolo has an ethical trading policy and takes steps, including factory visits, to ensure that its standards are implemented throughout the supply chain and that its trading partners comply with regulations.

Financial results

The results for the three years ended 31 May 2016 are set out in Exhibit 5. They show that Retail revenue grew by almost 9% in 2016, more than offsetting a fall in Hospitality. In general, Hospitality revenue fluctuates more than Retail revenue, as it depends on where hotels and restaurants are in their replacement cycle and on the number of new customers in a year. Also, gross margins in Hospitality are higher than Retail gross margins. This is for a number of reasons:

products sold to Hospitality customers are tailored to their requirements, incorporating logos and other corporate design features;

large retailers obtain lower prices from Piccolo because their annual order quantities are much bigger than those of Hospitality customers; and

sales to Retail customers include utensils, on which the profit margins are lower than for the other product categories.

ICAEW/CS/J17 Page 15 of 40

EXHIBIT 5

Piccolo: Management accounts for the three years ended 31 May 2016

Statement of profit or loss

for the years ended 31 May Note 2016 2015 2014 £000 £000 £000

Revenue 1 41,713 39,506 37,327 Changes in inventories 821 573 371 Purchases of goods for resale (26,215) (23,928) (22,812)

Gross profit 1 16,319 16,151 14,886 Other costs 2 (13,156) (12,920) (12,613)

Operating profit 3,163 3,231 2,273 Net finance income/(expense) 34 26 (35)

Profit before taxation 3,197 3,257 2,238 Taxation (639) (651) (448)

Profit for the year 2,558 2,606 1,790

Statement of financial position as at 31 May Note 2016 2015 2014

£000 £000 £000

Non-current assets: Property, plant and equipment 3 223 276 418

Current assets Inventories (finished goods) 7,936 7,115 6,542 Trade and other receivables 4 7,795 6,738 6,102 Cash at bank and in hand 2,826 1,814 81

Total current assets 18,557 15,667 12,725

Total assets 18,780 15,943 13,143

Shareholders’ equity Called up share capital 500 500 500 Retained earnings 11,982 9,424 6,818

12,482 9,924 7,318

Current liabilities Trade and other payables 5 6,298 6,019 5,825

Total equity and liabilities 18,780 15,943 13,143

ICAEW/CS/J17 Page 16 of 40

Statement of cash flows for the years ended 31 May 2016 2015 2014

£000 £000 £000

Profit before taxation 3,197 3,257 2,238 Adjust for: Depreciation 115 132 199 Loss/(profit) on sale of property, plant and equipment 23 (1) - Net finance (income)/expense (34) (26) 35

Operating cash flow before changes in working capital 3,301 3,362 2,472 Change in inventories (821) (573) (371) Change in trade and other receivables (1,057) (636) (320) Change in trade and other payables 291 (9) (200)

Cash generated from underlying operations 1,714 2,144 1,581 Income tax paid (651) (448) (500)

Net cash from operating activities 1,063 1,696 1,081

Investing activities Net interest received/(paid) 34 26 (35) Purchase of property, plant and equipment (85) (15) (147) Proceeds on disposal of property, plant and equipment - 26 -

Net cash (used in)/from investing activities (51) 37 (182)

Change in cash and cash equivalents 1,012 1,733 899 Cash and cash equivalents at beginning of the year 1,814 81 (818)

Cash and cash equivalents at the end of the year 2,826 1,814 81

Notes to the management accounts

Note 1: Segmental analysis

2016 2015 2014

£000 £000 £000 Revenue Hospitality 8,837 9,316 8,272 Retail 32,876 30,190 29,055

41,713 39,506 37,327

Gross profit Hospitality 4,345 4,911 4,148 Retail 11,974 11,240 10,738

16,319 16,151 14,886

Note 2: Other costs 2016 2015 2014 £000 £000 £000 Sales and distribution 4,034 3,956 3,802 Product innovation and design 2,153 2,060 2,150 Advertising and marketing 4,038 3,906 3,675 Administration and support 2,931 2,998 2,986

13,156 12,920 12,613

ICAEW/CS/J17 Page 17 of 40

Note 3: Property, plant and equipment Leasehold Furniture, Motor TOTAL improvements fittings and vehicles equipment

£000 £000 £000 £000 Cost At 1 June 2013 139 1,116 196 1,451 Additions - 92 55 147 Disposals - - (14) (14)

At 1 June 2014 139 1,208 237 1,584 Additions - 15 - 15 Disposals - (140) (59) (199)

At 1 June 2015 139 1,083 178 1,400 Additions 29 45 11 85 Disposals - - (54) (54)

At 31 May 2016 168 1,128 135 1,431

Depreciation At 1 June 2013 73 780 128 981 Disposals - - (14) (14) Charge for the year 41 127 31 199

At 1 June 2014 114 907 145 1,166 Disposals - (128) (46) (174) Charge for the year 24 90 18 132

At 1 June 2015 138 869 117 1,124 Disposals - - (31) (31) Charge for the year 4 92 19 115

At 31 May 2016 142 961 105 1,208 Carrying amount At 31 May 2013 66 336 68 470

At 31 May 2014 25 301 92 418

At 31 May 2015 1 214 61 276

At 31 May 2016 26 167 30 223

Note 4: Trade and other receivables 2016 2015 2014 £000 £000 £000

Trade receivables 6,706 5,673 5,283 Prepayments and other receivables 1,089 1,065 819

7,795 6,738 6,102

Note 5: Trade and other payables

2016 2015 2014 £000 £000 £000

Trade payables 4,354 4,006 3,885 Accruals and other payables 1,305 1,362 1,492 Income tax payable 639 651 448

6,298 6,019 5,825

ICAEW/CS/J17 Page 19 of 40

EXHIBIT 6

Piccolo: Review of the business to 31 May 2016 (prepared by Sabrina Kroos for the Piccolo board, July 2016) Revenue

Revenue growth in the year ended 31 May 2016 (2016) was similar to growth in 2015. However, there were contrasting performances by the two business lines:

Hospitality: Our valued, established relationships with Hospitality customers remained strong in 2016 despite several pressures during the year. After showing good growth in 2015, revenue dropped by 5%, partly because of problems being experienced by our key customer Dougal Hotels, which caused it to delay indefinitely a kitchenware replacement programme that had been scheduled for January 2016 at 50 of its hotels. This was coupled with a decline in the number of new customers acquired.

Retail: After a modest increase in 2015, Retail recorded excellent revenue growth of almost 9% in 2016, in line with our strategic objectives for the year. We were delighted with the further growth in business from our customer Gullen with its ongoing programme of new store openings. We expect this to continue in the future as we get more of our products into Gullen stores. We were also pleased with the response to the latest advertising campaign featuring Lucy Tyler.

Gross profit

Gross margins suffered slightly in 2016 as two of our key manufacturers passed on to us their higher energy, raw material and commodity costs. We knew that this was going to happen but its impact was less than it might have been as it occurred later than we had expected. We also managed to reduce the impact by passing on some of the cost increases to our Retail customers, for many of whom we had kept our prices constant for two years. However, we were not able to do this for our smaller Hospitality customers, some of whom are in financial difficulties and have delayed payment. It is likely that we will choose to stop dealing with them – or that they will make the choice for us by seeking a new supplier or by cutting back on their kitchenware purchases.

Other costs

We have continued to control our other costs carefully, resulting in little overall change over the past two years. Sales and distribution costs have fallen slightly as a percentage of revenue: working closely with RDN, we continue to look at ways to streamline this important activity. Product innovation and design expenditure has shown a small rise in 2016 as we continue to refresh our product portfolio to meet the preferences of the modern consumer. We also paid a contractual success fee of £0.15m to Lucy Tyler in recognition of her efforts. Administration and support costs have remained constant.

Product innovation

Product innovation remains critical to our success. The PE7 non-stick pan, introduced in 2015 and using world-class technology developed by and licensed from a major international company, has proved highly popular. Further variations were added to the basic version during 2016. All new products have been subject to the same rigorous quality control that has been Piccolo’s hallmark over a long period now. Customers continue to value the blend between traditional and modern for which we are known. At the same time, we are conscious of the need to avoid confusing consumers, so we should not be expecting retailers to stock our new products alongside those that are no longer in fashion.

We continue to invest time and money in working with manufacturers and customers, not only on new products but also on new technologies that can differentiate us from our competitors. We are currently carrying out some potentially significant market testing of our new tableware (Classic).

ICAEW/CS/J17 Page 20 of 40

Property, plant and equipment

Additions during both 2015 and 2016 have been low as our existing assets continue to work well, even though many of them are now fully depreciated. However, we are aware that we will need to increase capital expenditure, notably IT equipment and facilities (a large part of our asset base), in the next two years. This will enable us to expand our design capability and to reconfigure part of our Birmingham premises. As a result, we will be able to hold more inventory ourselves and therefore meet demand for replacement items.

Inventories

We seek to ensure that we always have sufficient levels of our products (including replacements) to meet demand. This applies especially to the new products that we have recently launched or are due to launch shortly. As well as reflecting the general growth in our trade, the 2016 increase is also caused by higher underlying production costs, together with delays in getting products to customers towards the end of year. We are currently investigating these delays, which arose from supply inefficiencies at overseas manufacturers.

Trade and other receivables

As well as showing the impact of higher sales, the increase in trade receivables in 2016 is due to the struggling Hospitality customers, who are continuing to pay but taking more credit. Trade receivables also include an amount due from Kaster (one of our Retail customers) that was settled in June 2016 after a protracted dispute.

Trade and other payables

Trade payables have remained fairly constant when expressed as a percentage of purchases, reflecting our adherence to key suppliers’ credit terms.

Cash and cashflow

We believe that we now hold sufficient cash to deal with any seasonal variations and any unexpected events in the business. Despite a similar profit performance, the increase in cash balances in 2016 was less than in 2015, as a result of changes in working capital, especially the increases in inventories and trade receivables described above.

ICAEW/CS/J17 Page 21 of 40

EXHIBIT 7

Piccolo: Business operations Products

Selling arrangements vary between Retail and Hospitality customers.

As part of a typical order for a Retail customer (eg, Longfield – see Exhibit 9), Piccolo might sell 10 boxed sets of matching tableware, each consisting of 4 large plates, 4 side plates, 4 bowls and 4 cups or mugs. If these 10 boxed sets are sold at (say) £100 each (ie, £1,000 in total) and the purchase cost to Piccolo was (say) £60 per set, Piccolo earns a gross margin of 40%. Longfield will then sell them to the consumer for (say) £150 each so as to generate its own profit.

Alternatively, Piccolo might send the same number of 40 large plates, 40 side plates etc to Longfield, but not packaged as boxed sets. These would then be sold individually to consumers. Both the prices charged by Piccolo to Longfield and the prices charged by Longfield to the consumer will be different from those applicable to the boxed sets.

For cookware, the model is similar: items may be sold as large orders of boxed sets (eg, three or five matching saucepans) or as large orders of individual pans. Utensils are normally sold as large orders of individual items but some products are sold in a package (eg, a set of wooden spoons). The average price of a utensil sold by Piccolo is much lower than that for an item of tableware or cookware.

For a typical Hospitality customer (eg, Dougal Hotels – Exhibit 8), Piccolo’s sales are mostly made in large quantities, but not as boxed sets. Piccolo also offers the opportunity for small-scale replacements.

Piccolo does not sell utensils to Hospitality customers as it does not consider this to be commercially worthwhile. The products are mostly of low value and would be needed in relatively small quantities, which in turn would be costly and inefficient to distribute. Also, many of the utensils used by restaurants and hotels differ in size and capability from those used domestically. In addition, as they are kept in hotel and restaurant kitchens, they are not seen by diners and so do not help to raise Piccolo’s profile.

Production and distribution

Products are manufactured by a variety of companies, both within the UK and overseas (see Exhibit 10).

For Retail customers, size and frequency of orders are based on recent retail sales patterns. These are extrapolated into short-term future sales projections that take account of any known special promotions. Piccolo carries out this task in close collaboration with each retailer and notifies the requirements to the manufacturers. Hospitality customers’ requirements and hence orders tend to be less predictable. After production and packaging by the manufacturer, the finished goods are collected by Piccolo’s sole distribution company, RDN, stored and transported to their destinations (see Exhibit 11). Finished goods are treated as Piccolo’s inventory and recorded in Piccolo’s accounts until they are physically transferred to customers (retailers, hotels etc), at which point they are treated as revenue. A small amount of inventory (around 5% of the total in the accounts) is held by Piccolo at its own premises in Birmingham. This comprises replacements of popular items – or of items that may have ceased to be manufactured – available to be supplied at short notice. There are no ‘sale or return’ arrangements: retailers are responsible for disposing of products that they no longer wish to sell, for example by discounting to consumers. However, under their agreements with Piccolo, certain retailers are required to consult with Piccolo before introducing major reductions so as not to give consumers the impression of poor-quality products. Piccolo makes large payments to its key suppliers and also receives large payments from customers. At any one time, there may be significant trade payable and receivable balances in Piccolo’s accounts.

ICAEW/CS/J17 Page 22 of 40

Hospitality customers

Growing success with its Hospitality customers in recent years clearly demonstrates that Piccolo can cope reliably with substantial regular orders and still offer high-quality products.

The portfolio of customers making regular purchases now comprises two medium-sized hotel chains (Dougal Hotels and Ringford) and the UK sites of a major US-headquartered restaurant chain (Quincy Restaurants). There are also a number of smaller hotel and restaurant chains, plus individual hotels, conference centres and restaurants. In any one year, there are also a large number of one-off orders.

Revenue can fluctuate between years, depending on the replacement cycles of customers and the success in acquiring new customers. (See Exhibit 8.) Revenue by customer has been as follows:

Year ended 31 May 2016 2015 2014

£000 £000 £000

Dougal Hotels 1,056 1,335 1,163

Ringford 1,299 1,108 434

Quincy Restaurants 766 807 661

3,121 3,250 2,258

Other 5,716 6,066 6,014

8,837 9,316 8,272

Retail customers

Retail achieved higher growth in 2016 than in 2015, with no major changes in sales patterns or customer relationships. Piccolo’s three main customers are Longfield (a specialist kitchenware retailer), Kaster (a major supermarket chain) and Gullen (one of the UK's biggest department stores), but it also sells to smaller chains and smaller individual stores around the country. (See Exhibit 9.) Revenue by customer has been as follows:

Year ended 31 May 2016 2015 2014 £000 £000 £000

Longfield 4,889 4,303 4,111

Kaster 4,720 4,629 4,583

Gullen 2,872 2,347 1,990

12,481 11,279 10,684

Other 20,395 18,911 18,371

32,876 30,190 29,055

Competitors

Piccolo operates in a market and competitive environment with a range of business models. It has historically seen its main competitors as being Amefa, Churchill China, Joseph Joseph, Lakeland and Kitchencraft. Between them, these companies sell a wide variety of kitchenware in the UK (and further afield), both to businesses (retailers, hotels, restaurants and others) and direct to individual consumers. Some have their own retail presence, whether in physical stores, online or both. Some sell products within the same three categories as Piccolo; others, within one or two categories; and others also sell items of kitchenware that Piccolo does not sell (eg, cutlery and glassware within tableware). Some of these companies manufacture their own products; others outsource some or all of their production.

More recently, a number of other companies have emerged, primarily working with Retail customers. These include several that specialise in utensils, as well as PanOply, a cookware specialist. It is too early to say what impact, if any, these organisations will have on Piccolo or on the wider kitchenware market.

ICAEW/CS/J17 Page 23 of 40

Seasonality Revenue for the Retail business is typically skewed towards the Christmas period. Around 40% of Piccolo’s annual sales to Retail customers occur in October, November and December. This reflects the fact that retailers stock up in anticipation of the busy Christmas period (when people buy gifts for friends and family or entertain large numbers of guests). There is no regular seasonal pattern for Hospitality.

Product innovation and design

Piccolo works with its manufacturers to design products based on the latest technology and materials, coupled with design and production expertise. It also works with Hospitality customers, using their house styles as a base, to ensure that products are bespoke as required. As in the case of the PE7, Piccolo often licenses technology from third parties. Piccolo strives to identify future market trends and demand. During the year to 31 May 2016, Piccolo increased its investment in product innovation to take advantage of market opportunities. It has high expectations for its new tableware (Classic), due to be launched on 1 September 2016. The period for design of a new product for the Retail market – and the associated costs – can vary considerably. For an upgrade of an existing product, the process can be quick (one or two months) and the expense to Piccolo minimal (say, £10,000), while a totally new product can take up to two years from concept to sale and involve significant personnel, design and market testing costs. At any one time, there are likely to be a number of ongoing projects. Because of inherent uncertainties, there is no guarantee of success and a high risk of failure of products. Proof that the final design will be successful is often only known after launch. Product innovation and design are controlled through regular meetings chaired by Daniel Lejeune. The success of new launches is reviewed in the short term against individual targets (for example, by comparing actual sales against forecast sales) and over the longer term as a part of strategy.

Advertising and marketing Piccolo’s advertising and marketing plans are focused around Lucy Tyler. Advertising is primarily aimed at individual consumers, with regular slots on television and in magazines. The target audience is those aged 25-40, who are considered to be the main buyers of Piccolo products: the majority of advertising is in magazines aimed at this age-group and during food-related television programmes.

Piccolo spends around 10% of its revenue on advertising and marketing. This comprises both external expenditure (fees to Lucy Tyler and to advertising agencies), internal expenditure (eg, staff, materials) and other marketing costs. Other marketing costs include joint promotions with retailers to ensure that products are widely available and suitably positioned on shelves (or on the retailers’ websites). They also include sponsorship of hospitality trade conferences and other events that are likely to raise the profile of the company and its products among hotel and restaurant owners. Piccolo currently uses a single agency (Thor) for its external advertising and market research work.

Piccolo’s spending on advertising and marketing (especially with Thor) depends on a variety of factors. For example, the absolute amount may rise at times when a major baking or cooking competition is running on television. As its rivals will be in the same situation, Piccolo may need to spend more in order to remain ahead of these rivals. It may also have to increase its budget to support a new product launch or if a rival launches a new product which it promotes heavily, or if there is any form of scare in the industry about the suitability or safety of a particular product.

Piccolo pays Thor a contractual fixed annual fee, with additional amounts for any extra work carried out. The fixed element increased from £800,000 to £900,000 on 1 June 2016 and will be held at this level until at least 31 May 2018. Additional amounts range from £100,000 to £250,000 per year. Both

ICAEW/CS/J17 Page 24 of 40

parties find that this arrangement works well. Piccolo’s previous agency charged purely a fixed fee with no increments but this led to disputes when there was a need for a major new one-off campaign.

To assess the effectiveness of its advertising, Piccolo measures its return on external advertising expenditure. It calculates this by dividing the increase in total revenue for the year by its total external advertising expenditure, which for this purpose comprises only the fee payable to Lucy Tyler plus the total fee to Thor. The target return is 120%. Piccolo recognises that the impact of advertising is only one of several reasons why revenue goes up (or down) in a given year.

Personnel

Piccolo’s employees work in the following departments:

Sales and distribution (director responsible – Tamsin Wright): ensure, in conjunction with RDN, that products of the right quality reach customers in the right quantities, at the right time and right price; identify potential new customers; oversee relationships with existing customers.

Product innovation and design (director responsible – Daniel Lejeune): devise ideas for new products, working closely with manufacturers, Hospitality customers and with the advertising and marketing team. Costs include licence and royalty payments to third parties for use of designs, non-stick technology and other intellectual property.

Advertising and marketing (director responsible – Gautam Singh): work with the product innovation and design team, as well as with Thor and Lucy Tyler; review media coverage and market research to ensure that products are promoted in the right media aimed at key target audiences.

Administration and support (director responsible – Sabrina Kroos): provide finance, legal, administration, property and IT services. Administration and support costs in the accounts comprise both personnel and premises costs, including heat, light and power plus all depreciation.

Sales and distribution includes the costs of account managers and their assistants, appointed for each key Retail and Hospitality customer. Advertising and marketing includes what Piccolo calls the ‘product teams’. There is one team for each of the three product categories; their job is to maintain the market position and to monitor sales trends. The tracking project being piloted with Longfield (see Exhibit 9) should assist with this task. Piccolo holds regular employee briefings to ensure that information is shared and concerns are aired. Its commitment to staff development (overseen by a dedicated training manager appointed in June 2015) has ensured that morale, motivation and retention all remain high. Training covers not just technical areas suited to an employee’s role: it also includes skills areas (eg, written communication, time management, financial fluency, ethical awareness) that pervade the whole business. The skills training programme enables employees from different functions to meet each other and to network.

Piccolo also expects its employees to become involved in community work. Each member of staff is encouraged to spend a minimum of five days per year in volunteering activities, either individually or as part of a team (eg, by running a cookery competition for a school or serving meals at a care home). Piccolo strives to provide a healthy and safe working environment for all employees and visitors, with all areas physically accessible to disabled people.

ICAEW/CS/J17 Page 25 of 40

EXHIBIT 8

Piccolo: The Hospitality market and customers (August 2016)

Overview

The Hospitality customers that Piccolo serves fall broadly into two market segments: (i) restaurants and (ii) hotels and conference centres. Piccolo sells items from two of its three product categories (tableware and cookware) to Hospitality customers.

The success of the sector – and therefore the size of Piccolo’s related revenue – depends on the wider economy. Where people have higher levels of disposable income, they are more likely to dine out and to take overnight trips. In the current period of economic uncertainty, UK-based consumers are cutting back on such leisure expenditure, but there are more tourists to the UK as a result of the depreciation in sterling. The level of investment by restaurant and hotel owners in new sites, or in the refurbishment of existing ones, is another big driver of demand for Piccolo’s products.

Piccolo derives a high proportion of revenue each year from repeat or replacement sales to existing customers. For a typical medium-sized hotel chain, the normal pattern is to replace kitchenware on a cyclical basis, thus giving a steady revenue stream for Piccolo. Customers typically undertake a full replacement every five years: thus, a customer with 100 hotels might replace the cookware and tableware for 20 hotels in year 1, 20 in year 2, and so on. However, this is only a guide: for example, a replacement could be brought forward or delayed so as to fit in with a customer’s rebranding.

Piccolo also gains a sizeable number of new customers every year. Revenue additionally depends on corporate activity within the sector. For example, when one large hotel chain acquires another chain that is an established customer of Piccolo, there is a danger that Piccolo will lose the business. Conversely, if an existing customer acquires another chain, Piccolo is well placed to become a supplier to the acquired company – which can be particularly lucrative if this involves a rebranding exercise.

Piccolo has long-standing relationships with many customers. These are mostly not contractual, as it is not always possible to predict demand. However, Piccolo continues to supply many of the same customers every year: they value Piccolo’s service, as well as the reliability and blend of tradition and innovation within its products.

Acquiring and retaining customers

Piccolo obtains new customers in a variety of ways. Some approach (or are approached by) Piccolo at hotel and restaurant industry trade shows; others invite Piccolo to tender for their business. For each customer, Piccolo appoints an account manager, who (together with a team of assistants) is responsible for ensuring that products are supplied according to agreed specifications (for example, bearing the logo of the customer). This applies both at the start of the arrangement and for any subsequent product supply.

The account manager also has to ensure that requests for replacements or additional items are fulfilled and to deal with any queries about product quality. For a typical hotel or restaurant, as well as making replacements as part of the regular replacement cycle, Piccolo expects to replace each year a proportion of products as a result of breakages. The extent of this varies between Piccolo Tableware and Piccolo Cookware and between products. It also varies between customers: Piccolo’s experience has shown that breakages occur less often in upmarket hotels than in other types of hotels.

For most customers, the account manager liaises mainly with a counterpart at the customer’s head office, but in some cases this authority is delegated to the customer’s individual venues or regional centres. Piccolo prefers the first type of arrangement, as the second can lead to variations and create tensions in the relationship.

ICAEW/CS/J17 Page 26 of 40

Contact between Piccolo and its customers takes place through face-to-face meetings and visits, conference calls, email and a dedicated online client portal (used primarily for placing and tracking orders). Each year, Piccolo’s directors review the relationships with Hospitality customers. A policy of openness is encouraged, so that any complaints are aired and resolved promptly.

Pricing

Piccolo has a tariff of prices for each product but these are generally used only as a starting-point for negotiation with each customer, along with payment terms. The negotiation is normally led by Tamsin Wright. Prices are set according to the size of the initial supply and expected future sales, and they take account of the branding and other corporate design features required. Where a customer indicates that it wants to buy only tableware, Piccolo staff are encouraged to promote cookware as well (or vice-versa), for example by offering discounts.

Summary of arrangements with Hospitality customers

As indicated in Exhibit 7, Piccolo's three largest Hospitality customers are Dougal Hotels, Ringford and Quincy Restaurants. The terms of trade with each of these customers are broadly similar.

Customer profile (1): Dougal Hotels

Dougal Hotels became a customer of Piccolo in 2008, when, under new management, it undertook a major refurbishment programme and rebranding that saw it become a major player in the UK hotel industry. As part of this relaunch, the eating facilities at all 159 hotels (there are now 225) were upgraded. All hotels began offering a full cooked breakfast, with a wider range of menu options than before, in their dining areas. These dining areas were then also available for use as restaurants or party venues in the evenings or during the day. A further development was the conversion of 20 hotels into conference venues, which meant that their restaurants were often full for lunch and dinner.

The Dougal relaunch provided an excellent opportunity for Piccolo and, following a tender process, it became the exclusive supplier of cookware and tableware to Dougal for the central kitchen and dining areas. All tableware items included the new Dougal logo. The initial deal was worth £2.6 million in revenue to Piccolo.

As more hotels joined the Dougal chain, and as existing hotels sought to expand their kitchenware or to replace damaged items, Piccolo continued to make sales, but revenue was inevitably more modest following the initial supply. One outcome of the relaunch was a significant increase in room occupancy – and hence also an increase in use of the dining areas. This was mostly because of the conference facilities and because more business travellers were choosing Dougal, attracted by – among other things – a loyalty scheme rewarding those staying for at least 10 nights in a year. Piccolo currently earns a gross margin of 60% on its sales to Dougal – a figure that has been constant in the two years to 31 May 2016.

Customer profile (2): Ringford

Ringford was formed in 2013 and made an immediate impact in the sector, thanks to its ‘value’ policy – rooms at an affordable price that included a full cooked breakfast. All hotels also offer an evening meal, both for those staying overnight and for casual diners. Several Ringford hotels have already established a reputation as providing some of the best meals in the area, reinforced by favourable reviews on TripAdvisor and similar websites. After a steady programme of openings in 2014 and 2015, Ringford now has 270 hotels across the UK. Piccolo was chosen to be the exclusive supplier of cookware and tableware to Ringford. Although it was not consistent with its usual profile of Hospitality customers, Piccolo saw this as an opportunity to extend its reach. It therefore undertook the arrangement knowing that it was not likely to achieve the

ICAEW/CS/J17 Page 27 of 40

same profit margins as other customers. Piccolo currently earns a gross margin of 40% on its sales to Ringford – a figure that has been constant in the two years to 31 May 2016. Ringford recently announced its intention to enter the conference market. This will see it buy 40 properties from the struggling Reeve chain in 2017 and modernise both public areas and bedrooms.

Customer profile (3): Quincy Restaurants

Quincy is a mid-range American restaurant chain that opened its first outlet in the UK in 2012. At that time, the head office in Dallas required all units around the world to serve the same ‘fusion’ menus (blends of international food dishes), to have the same décor and to use the same tableware and cookware. However, it soon became apparent – from the initial rollout – that this formula was not going to be successful in the UK. The UK management team were therefore allowed to alter the menus so that they appealed more to their local clientele. They were also allowed to select cookware and tableware designs and sizes that were consistent with this image. Following a short tender process, Quincy chose Piccolo, citing “quality”, “service commitment”, “dependability” and “speed in dealing with problems” as the principal reasons for the choice. The Piccolo products are not required to carry Quincy’s logo but they must be of the highest standard. All items of tableware are checked individually by a Quincy employee, and put through a dishwasher cycle for quality checking purposes, before they can be used. It is rare for an item to need replacing at this stage but Piccolo is always responsive in such a situation, where necessary investigating the problem back to its source (design and production). Since the initial tender, the arrangement has developed. Quincy now has over 300 restaurants across the UK, and is planning to open another 30 each year until 2020. Piccolo’s margin on sales to Quincy has been constant at around 50% since 2012.

ICAEW/CS/J17 Page 29 of 40

EXHIBIT 9

Piccolo: The Retail market and customers (August 2016) Overview

Piccolo supplies its products to a wide range of retailers across the UK, from small specialist kitchen shops to large department stores. Piccolo sells products from all three categories to the Retail market, though the precise products sold vary between customers. Some products are specific to one customer but the majority are designed to be sold in any shop. In general, the Retail market is subject to intense competition, and product lifecycles can be short.

The benefits that retailers receive from Piccolo include: rapid deliveries, online ordering, regular new product ideas and launches, marketing support, reliable inventory levels and rigorous quality control. Piccolo has won industry awards for service almost every year since 2008.

Acquiring and retaining customers

As with Hospitality customers, Piccolo obtains Retail customers by a variety of methods, such as trade shows, product demonstrations and tenders. However, unlike with Hospitality customers, the arrangements involve a steady supply of products, and so Retail customers sign formal contracts with Piccolo. Among other matters, these set out quality requirements, minimum orders and pricing.

For similar reasons, the role of account managers for Retail customers is also much more of an ongoing nature. It involves day-to-day contact both with individual stores and, in the case of larger chains, with head office or regional centres. Here, the use of technology – conference calls, email, internet and online client portal – is vital.

Issues for a retailer can arise if a batch of products is found to be of poor quality. If they have not yet been sold to consumers, the retailer can usually return them to Piccolo in accordance with the terms of its contract. If any products have been sold to consumers, the consumers are asked to return them to the retailer. (Larger retailers have quality checking processes: these usually ensure that the problem is identified before the products are sold to customers. Smaller shops do not generally have the time or the staff to carry out such checks and are prepared to take the risk of a later complaint.) Piccolo then investigates the problem, in conjunction with the manufacturer if necessary, to identify whether it is isolated or more extensive. It may have arisen in one manufacturing or packaging run or there may be a more endemic defect. In a worst case – especially if there is a health hazard – Piccolo may have to undertake a product recall, which could be from one branch of a single retailer, from all stores of a single retailer or from all stores to which it has sold the product. Piccolo has not had to make a recall since 2009 but it has a process in place to deal promptly with one if it occurs.

Pricing

Piccolo’s tariff of prices for each product is different from that used for Hospitality, but as for Hospitality this is only a starting-point for negotiation with each customer. Prices are set according to the expected pattern of sales and variety of products included in the customer’s order. A customer buying products across all three categories usually obtains more favourable terms than one buying (say) just utensils.

Certain larger retailers must consult with Piccolo before they can introduce product promotions (eg, ‘buy two, get one free’ or ‘25% off’).

Summary of arrangements with Retail customers

As indicated in Exhibit 7, Piccolo's main Retail customers are Longfield, Kaster and Gullen. The terms of trade with each of these customers are broadly similar.

ICAEW/CS/J17 Page 30 of 40

Customer profile 1: Longfield

One of the UK’s largest kitchenware specialists, Longfield is a key customer, and Piccolo’s sales to Longfield tend to be a reasonably good barometer of the UK market for kitchenware. Longfield stores around the country (and its website) sell a wide range of products within each of Piccolo’s three product categories.

Longfield earns a significant amount of its revenue from wedding lists. Under this system, also found at other large retailers, couples (‘clients’) who are about to marry or enter into civil partnerships create a list of products from those sold by Longfield. They then ask their guests, when buying a wedding gift, to choose one or more of the items listed. Piccolo products often feature prominently on such lists.

In December 2016, Longfield will become the ‘pilot’ for a new product tracking tool being developed by Piccolo. This will enable Piccolo to use historical sales information and customer feedback to identify gaps in the market (eg, tableware of a specific shape, colour, pattern or size) and determine which Longfield stores are likely to achieve the highest sales of new products. The system should enable Piccolo to forecast accurately the volumes of each product that it needs to commission and buy and, as a result, to keep (both existing and new) products in the market and in stock for longer.

Customer profile 2: Kaster

Kaster is a chain of European supermarkets that opened its first UK shop in 2010 and has expanded rapidly since then. Initially selling mainly food products, it has now extended its range to cover small electrical goods, toiletries and kitchenware, enabling it to compete with established UK supermarkets. However, Kaster’s UK expansion appears to have been poorly controlled. Two issues have arisen:

Over-ordering and disagreements with Piccolo about volume discounts

Confusion over the application of price increases on sales from Piccolo to Kaster, resulting in repeated disputes about amounts owed by Kaster to Piccolo.

A new cookware specialist, PanOply, is due to begin selling products to Kaster stores with effect from 1 September 2016, in good time for the busy Christmas period. It has offered Kaster big financial incentives to sell as many of its cookware products as possible, by whatever means it can. Piccolo will watch this development with interest but does not see PanOply as a competitor because its products are perceived to be of lower quality and not such good value for money. Customer profile 3: Gullen

As one of the UK’s leading department stores, Gullen is a valued and important customer for Piccolo. It became a customer in 2012 and Piccolo’s revenue from Gullen since then has steadily risen, reflecting both the expansion in the number of Piccolo products that Gullen stocks and its new store opening programme. This has seen the number of Gullen shops increase by 50% between 1 December 2014 and 31 May 2016, and it is due to increase further in the year to 31 May 2017. Piccolo renewed its contract with Gullen on 1 June 2016: the contract is next due for review on 1 June 2018.

Gullen’s managers at each store are responsible for the positioning of products on shelves. Gullen is contractually required to place Piccolo products in prominent positions, above other named brands. A trade discount has been agreed with Gullen to reflect this requirement and, to ensure that it is being met, Piccolo is entitled to undertake spot-checks on an occasional basis. The trade discount (which means that Piccolo’s margins from Gullen are lower than for the other two large Retail customers) is on a sliding scale, which will continue to increase during the period of Gullen’s expansion. The agreement also specifies that products should be displayed for a minimum of three months or until Piccolo agrees otherwise. In addition, so as not to taint Piccolo’s image, Gullen cannot sell Piccolo products at a discount without Piccolo’s express permission.

ICAEW/CS/J17 Page 31 of 40

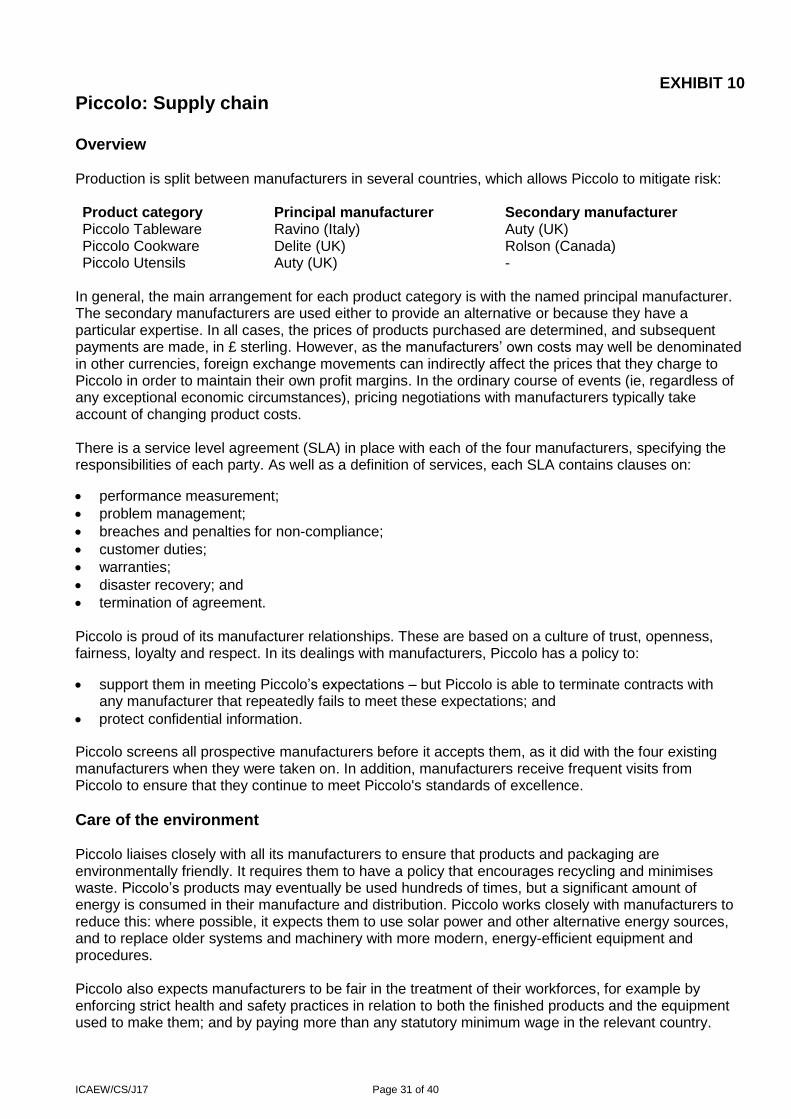

EXHIBIT 10

Piccolo: Supply chain Overview Production is split between manufacturers in several countries, which allows Piccolo to mitigate risk: Product category Principal manufacturer Secondary manufacturer Piccolo Tableware Ravino (Italy) Auty (UK) Piccolo Cookware Delite (UK) Rolson (Canada) Piccolo Utensils Auty (UK) -

In general, the main arrangement for each product category is with the named principal manufacturer. The secondary manufacturers are used either to provide an alternative or because they have a particular expertise. In all cases, the prices of products purchased are determined, and subsequent payments are made, in £ sterling. However, as the manufacturers’ own costs may well be denominated in other currencies, foreign exchange movements can indirectly affect the prices that they charge to Piccolo in order to maintain their own profit margins. In the ordinary course of events (ie, regardless of any exceptional economic circumstances), pricing negotiations with manufacturers typically take account of changing product costs. There is a service level agreement (SLA) in place with each of the four manufacturers, specifying the responsibilities of each party. As well as a definition of services, each SLA contains clauses on:

performance measurement;

problem management;

breaches and penalties for non-compliance;

customer duties;

warranties;

disaster recovery; and

termination of agreement.

Piccolo is proud of its manufacturer relationships. These are based on a culture of trust, openness, fairness, loyalty and respect. In its dealings with manufacturers, Piccolo has a policy to:

support them in meeting Piccolo’s expectations – but Piccolo is able to terminate contracts with any manufacturer that repeatedly fails to meet these expectations; and

protect confidential information.

Piccolo screens all prospective manufacturers before it accepts them, as it did with the four existing manufacturers when they were taken on. In addition, manufacturers receive frequent visits from Piccolo to ensure that they continue to meet Piccolo's standards of excellence.

Care of the environment Piccolo liaises closely with all its manufacturers to ensure that products and packaging are environmentally friendly. It requires them to have a policy that encourages recycling and minimises waste. Piccolo’s products may eventually be used hundreds of times, but a significant amount of energy is consumed in their manufacture and distribution. Piccolo works closely with manufacturers to reduce this: where possible, it expects them to use solar power and other alternative energy sources, and to replace older systems and machinery with more modern, energy-efficient equipment and procedures. Piccolo also expects manufacturers to be fair in the treatment of their workforces, for example by enforcing strict health and safety practices in relation to both the finished products and the equipment used to make them; and by paying more than any statutory minimum wage in the relevant country.

ICAEW/CS/J17 Page 32 of 40

Manufacturers

Piccolo Tableware – Ravino

Ravino was founded in 1972 and has been manufacturing tableware for Piccolo since 2011. It is known for its reliability. Piccolo especially values its collaboration with Ravino in creating attractive designs. Several new products that they have jointly developed have been successful, achieving significant sales and enhancing Piccolo’s public image.

The new tableware, Classic – which is scheduled for launch on 1 September 2016 and could initially generate revenue of up to £0.1 million per month – is the latest in a long line of innovative products designed in conjunction with Ravino. Classic includes a number of new features: this has extended the design and market testing process, and Piccolo hopes that further testing will confirm it as a potential bestseller and market leader. As well as taking market share from Piccolo’s rivals, Classic will gradually replace some of Piccolo’s other tableware products currently on sale.

Piccolo Tableware and Piccolo Utensils – Auty

Although it is the main manufacturer for Piccolo Utensils and secondary manufacturer for Piccolo Tableware, Auty takes its two roles equally seriously. Indeed, because it serves two product categories, it is Piccolo’s largest manufacturer overall. Auty is based in Stoke-on-Trent, one of the UK’s traditional homes for china products, and has been there since 1889. Although many long-standing manufacturers in the region no longer exist, Auty has maintained its presence as a result of several factors: a loyal workforce, a worldwide market for its products and services; and incentives from local government to prevent it from moving away.

In its tableware manufacture, Auty combines traditional methods with modern techniques. For example, in recent years it has invested in new kilns that accelerate production without compromising quality. Auty’s move into the manufacture of utensils occurred in 2010, when it acquired a utensils manufacturer that had lost market share through its inability to keep pace with fashion. Auty has been able to transfer its cookware expertise into utensils and it now supplies Piccolo and several other medium-sized kitchenware companies.

Piccolo Cookware – Delite

Around 70% of the manufacturing of Piccolo Cookware products is carried out by Delite, which has sufficient capacity to produce supplies as required, allowing Piccolo to meet high levels of demand. According to its website:

“Delite provides fast, flexible manufacturing for a wide range of customers, combining attractive pricing with unbeatable service. Our team – many with cookware experience – has helped shape our reputation for service, now a byword in the sector. We never compete against our customers with brands of our own: we manufacture only for their brands, to help them reach their objectives. With huge daily production capacity on our site, fully compliant with industry standards and with current environmental best practice, we can perform both long and short product runs. Expansion plans are being made to accommodate larger inventories and new products.

“Our services are all supported by extensive modern quality control procedures and equipment, ensuring strict adherence to standards and world-class products. By managing each step of the process, we ensure that finished goods leaving the premises fulfil customer expectations and statutory requirements: incoming components are inspected to ensure that all specifications are met; and factory visits provide final, independent quality assurance.”

ICAEW/CS/J17 Page 33 of 40

Piccolo Cookware – Rolson

As the secondary producer of Piccolo Cookware, Rolson has an important role to play as both an alternative for some of Piccolo’s most popular cookware products and the exclusive provider for some of its high-end products that are mainly used by chefs in leading hotels and restaurants.

Based in Toronto, Rolson was chosen by Piccolo from a shortlist of six manufacturers because of its investment in the very latest manufacturing technology and its commitment to quality. Rolson has a reputation for making cookware that lasts. Its location also provides Piccolo with an important strategic base, should it ever consider selling its products in North America.

Piccolo works closely with Rolson in product innovation and design. Piccolo staff often travel to Toronto in order to discuss possible new designs with Rolson’s technical team. The PE7 non-stick pans, launched by Piccolo in the year to 31 May 2015, were the result of a collaboration with Rolson.

ICAEW/CS/J17 Page 35 of 40

EXHIBIT 11

Piccolo: Logistics, inventory storage and distribution After production and packaging by the relevant manufacturer in the UK or overseas, the finished products for both Retail and Hospitality customers are collected for transportation to their destinations. All of Piccolo’s logistics (storage and distribution of finished goods) are undertaken by RDN. RDN is a vital link in Piccolo's supply chain, with a proud record of fulfilling short-notice orders to both Retail and Hospitality customers. Piccolo and RDN collaborate closely to ensure that products physically arrive in accordance with agreed timescales and quantities – and undamaged. For Retail customers, they are taken to individual stores; for Hospitality customers, they are taken to each hotel or restaurant.

Piccolo appointed RDN its sole distribution company in 2013 following a tender and trial by three companies. RDN was chosen over the other two because of its efficiency and attention to detail. The five-year contract with RDN is due for renewal on 31 May 2018.

RDN’s logistics systems are designed to ensure the accurate measurement of inventory levels of Piccolo’s products, as well as accurate dispatch. Enough inventory is maintained at all times to fulfil customer orders as promptly as possible, even at times of high demand. Through RDN’s sophisticated technology, customers can track their deliveries in real time.

RDN distributes to small and large shops, hotels, restaurants and conference centres (as well as offices and hospitals) in the UK. A retail chain often orders a set of products for a large number of its stores at the same time (for example, at the start of the Christmas season). This requires a complex process of scheduling trucks and liaison, both with individual stores and with Piccolo’s head office team (led by Tamsin Wright). However, most orders for large retailers are for individual stores or for a small number of stores in one region. When a small replacement order is required and Piccolo holds the products at its own site, it sometimes arranges the distribution itself.

RDN also has operations in other countries. This enables it to work with Piccolo’s manufacturers in Italy and Canada in bringing products to its UK warehouses (which are strategically located near major transport routes) for onward distribution to customers. Products from overseas may be transported by air or sea, depending on the weight, size and urgency of the order as well as the quality, material and value of the products.

Performance target Piccolo monitors RDN’s performance under its contract by reference to the percentage of deliveries to customers achieved to deadline (the ‘Delivery Rate’). Deadlines vary from customer to customer and between orders, depending on such criteria as geography and time constraints (orders for Retail customers tend to be needed more urgently than those for Hospitality customers). As a result, some of them are set contractually while others are agreed on an ad hoc basis. The annual Delivery Rate target of 90% is based on the overall number of deliveries, without taking account of order size, value, location numbers or other variable factors. If RDN does not meet the target (as occurred in the year ended 31 May 2014, when the actual figure was 89.8%), it is required to pay Piccolo a £10,000 penalty for each 0.1 percentage point by which it falls short. The actual Delivery Rate is measured annually on 31 May. Any resulting penalty is deducted from the payments due from Piccolo to RDN for distribution and reflected in the draft management accounts for the year then ended. As the two companies have a long-standing relationship, they have always agreed the actual Delivery Rate without any issues. If RDN fails to meet the target, Piccolo investigates the reasons as there may be more serious underlying operational issues to be addressed. These could include product breakages in transit, incomplete documentation or incorrect number and/or type of product being delivered, potentially leading to a loss of customer goodwill. In an extreme case, there could even be defections by unhappy Piccolo customers if the matter cannot be satisfactorily resolved.

ICAEW/CS/J17 Page 37 of 40

EXHIBIT 12

Piccolo: Board briefing (prepared by Sabrina Kroos, July 2016)

Overview

At the time of writing, the main issue affecting not just Piccolo and its market but the UK as a whole is economic uncertainty arising from Brexit – the UK vote on 23 June 2016 to leave the European Union (EU). Although the result may take several years to come into effect, its impact is already being felt in a fall in the value of sterling (£). Piccolo’s Retail revenue may suffer if consumers become more cautious in their spending. Hospitality revenue could be reduced by delayed new hotel openings or delayed refurbishment programmes but equally it could benefit from a higher number of tourists to the UK.

Meanwhile, globalisation continues to have a big impact. Kitchenware importers and manufacturers based abroad are becoming more influential within the UK marketplace. Another factor is the changing face of the UK retail sector, and especially the continued strong growth of internet shopping, which gives consumers a breadth of choice that smaller bricks-and-mortar retailers cannot match.

Key risks

The main risks affecting Piccolo are categorised into market risks and operational risks, as follows. The board is ultimately responsible for taking actions to manage and mitigate these risks wherever possible.

Market risks: o Demand risk arising from changes in consumer preferences and the competitive environment in

which Piccolo operates: we mitigate this by regularly reviewing market conditions and our product portfolio, introducing new products where circumstances dictate.

o Currency / pricing risk relating to the value of sterling (in which all transactions are denominated), which can impact the prices charged to us by manufacturers: we review – and, where necessary, act on – currency rate movements as part of our pricing discussions with customers and manufacturers but we do not undertake any specific hedging activities.

o Regulation risk in relation to our products meeting accepted safety standards (both existing and potential new, stricter standards): we manage this by monitoring standards and testing products.

Operational risks: o Competition to retain and recruit the right calibre of people at all levels: we mitigate this through

succession planning and by identifying training, development and recruitment needs. o Reputational risk as a result of failure to meet quality standards in all our activities: we manage

this by adhering to quality control and by creating a culture of quality throughout the company. o Dependence on manufacturers, with potential interruption to supply and changes in costs

arising from economic or regulatory change: we control this through use of alternative suppliers.

Future strategy

The Piccolo directors have approved the following strategic goals for the two years to 31 May 2018:

1. To expand by selling into overseas markets, eg by exploring relationships with global hotel chains.

2. To review external sourcing arrangements to ensure that we are getting the best possible value from (UK or overseas) manufacturers; where necessary, we will terminate ineffective arrangements.

3. To develop a marketing strategy for our 25th anniversary (the year beginning 1 June 2018).

4. To continue to identify opportunities for improving our portfolio through adaptation of existing products and launches of new products in response to market demand (eg, international cookware).

5. To improve cross-selling across / within product categories, eg, by incentivising kitchenware shops to buy more utensils and to position them nearer to cookware shelves; this should help to counter the growing threat from new utensils specialists and increase Piccolo Utensils’ share of total Retail revenue to 15% by 31 May 2018.

ICAEW/CS/J17 Page 38 of 40

Budgets for the year ending 31 May 2017

In view of the economic uncertainty, we have prepared two 2017 budgets, together with notes and assumptions: high (optimistic) and low (pessimistic). We consider these to be at either extreme of the likely outcomes.

High Low £000 £000

Revenue (Note 1) 45,000 38,000

Gross profit (Note 2) 18,000 12,500 Other costs (14,000) (12,000)

Operating profit 4,000 500

Note 1: Revenue High Low

£000 £000

Hospitality 10,000 7,000 Retail 35,000 31,000

45,000 38,000

Assumptions

High: Strong revenue growth in both business lines (consumer optimism); good sales from new products and from new customers; effective cross-selling, both within and between product categories; impact of estimated general 7.5% upturn in UK kitchenware market

Low: Fall in both business lines (consumer caution); poor sales of new products and from new customers; loss of Hospitality customers; aggressive sales techniques by competitors; impact of estimated general 2.5% downturn in UK kitchenware market

Note 2: Gross profit High Low

£000 £000

Hospitality 5,000 3,000 Retail 13,000 9,500

18,000 12,500

Assumptions

High: Higher costs passed on to customers where possible; less profitable Hospitality customers replaced by new, more profitable customers