expansion of the panama canal and its impact … · expansion of the panama canal and its impact on...

TRANSCRIPT

EXPANSION OF THE PANAMA CANAL AND ITS IMPACT ON TANKERS

José Ramón Arango S.Liquid Bulk Segment

October 4th 2017

Agenda

Panama Canal Expansion

Panama Canal ExpansionPerformance

Impact of the Expansion on Tankers

The Next Frontier

4,400 TEU’s33.5 m (110’)

32.3 m (106’)

12.8 m (42’)

12.04 m(39.5’)

Maximum existing Locks:

55 m (180’)

13,000 – 14,000 TEU’s

18.3 m (60’)

15.2 m(50’)

New Locks Max Vessel Size:

Dimensions of Locks and Ships

Agenda

Panama Canal Expansion

Panama Canal ExpansionPerformance

Impact of the Expansion on Tankers

The Next Frontier

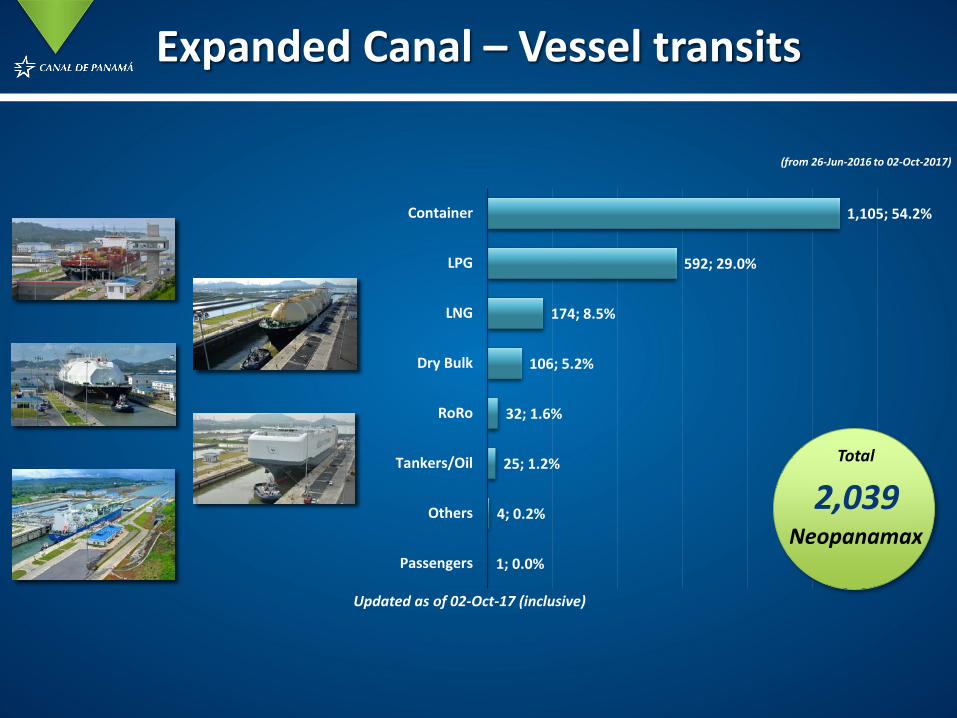

Expanded Canal – Vessel transits

1; 0.0%

4; 0.2%

25; 1.2%

32; 1.6%

106; 5.2%

174; 8.5%

592; 29.0%

1,105; 54.2%

Passengers

Others

Tankers/Oil

RoRo

Dry Bulk

LNG

LPG

Container

Updated as of 02-Oct-17 (inclusive)

(from 26-Jun-2016 to 02-Oct-2017)

Neopanamax2,039

Total

236; 11.6%

1; 0.0%

4; 0.2%

25; 1.2%

32; 1.6%

106; 5.2%

174; 8.5%

592; 29.0%

1,105; 54.2%

Panamax

Passengers

Others

Tankers/Oil

RoRo

Dry Bulk

LNG

LPG

Container

Updated as of 02-Oct-17 (inclusive)

NPxPx 236

2,039

2,275Total

(from 26-Jun-2016 to 02-Oct-2017)

Expanded Canal – Vessel transits

7.8

7.1

8.4

7.9

9.0

6.6

3.3

2.9

7.9

9.6

43.0

41.5

50.3

53.9

59.3

64.3

101.1

49.8

1.4

20.0

16.0

0.0

1.6

0.9

8.1

8.3

79.7

2.6%1.9%2.7%2.1%

3.5%7.1%

4.2%1.1%

0.8%2.5%

2.5%14.2%11.6%

16.7%14.8%

19.9%19.6%

36.3%35.2%

0 20 40 60 80 100 120 140

FY 2016FY 2017FY 2016FY 2017FY 2016FY 2017FY 2016FY 2017FY 2016FY 2017FY 2016FY 2017FY 2016FY 2017FY 2016FY 2017FY 2016FY 2017FY 2016FY 2017

Carg

aG

ener

al

Carg

aRe

frig

erad

a

Gas

eros

(LPG

)LN

GO

tros

Pasa

jer

o

Port

ave

hic

ulo/

Ro

RoTa

nqu

eros

Gra

nele

roSe

co

Port

aco

nte

nedo

r

PCUMS Tonnage(Million Tons)

October to August

100%

Container

Dry Bulker

Tanker

RoRo

Passenger

Other

LNG

LPG

Refrigerated

General Cargo

61.5%

75.0%

PANAMAXNEOPANAMAXAF2016AF2017

Agenda

Panama Canal Expansion

Panama Canal ExpansionPerformance

Impact of the Expansion on Tankers

The Next Frontier

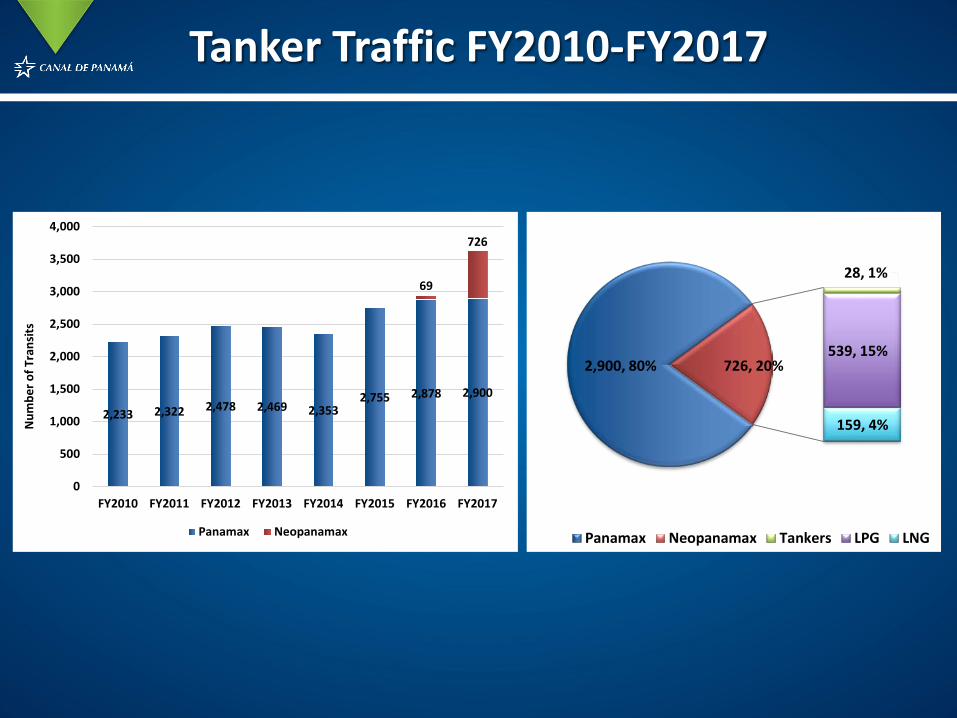

Panama Canal Tankers TrafficFY2010-FY2017

1,286 1,3111,477 1,418 1,378

1,5841,777 1,838

178 186

227 238 275

422

449

877

365454

433 459 393

436

456

431

314306

300 311273

289

221

301

17

163

8059

39 2630

24

25

14

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

FY2010 FY2011 FY2012 FY2013 FY2014 FY2015 FY2016 FY2017

Num

ber o

f tra

nsits

Chemical/Oil Tanker LPG Carrier Products Tanker Crude Oil Tanker LNG Carrier Chemical Tanker

2,900, 80%

28, 1%

539, 15%

159, 4%

726, 20%

Panamax Neopanamax Tankers LPG LNG

2,233 2,322 2,478 2,469 2,3532,755 2,878 2,900

69

726

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

FY2010 FY2011 FY2012 FY2013 FY2014 FY2015 FY2016 FY2017

Num

ber o

f Tra

nsits

Panamax Neopanamax

Tanker Traffic FY2010-FY2017

Main Commodities Carried by Tankers FY2010-FY2017

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

FY2010 FY2011 FY2012 FY2013 FY2014 FY2015 FY2016 FY2017

LON

G T

ON

S O

F CA

RGO

(IN

THO

USA

ND)

OTHERS VEGETABLE OILS AND MOLASSES CHEMICALSPETROLEUM CHEMICALS CRUDE PETROLEUM DIESEL OILGASOLINE JET FUEL LPG

Diesel

Gasoline

Crude

LPG

LNG

Chemicals

United States

Peru

Chile

Ecuador

Mexico

Guatemala

Diesel – Main Routes

United States

Peru

Chile

Ecuador

Mexico

Guatemala

Gasoline – Main Routes

United States

Ecuador

Mexico

Nicaragua Colombia

Bahamas

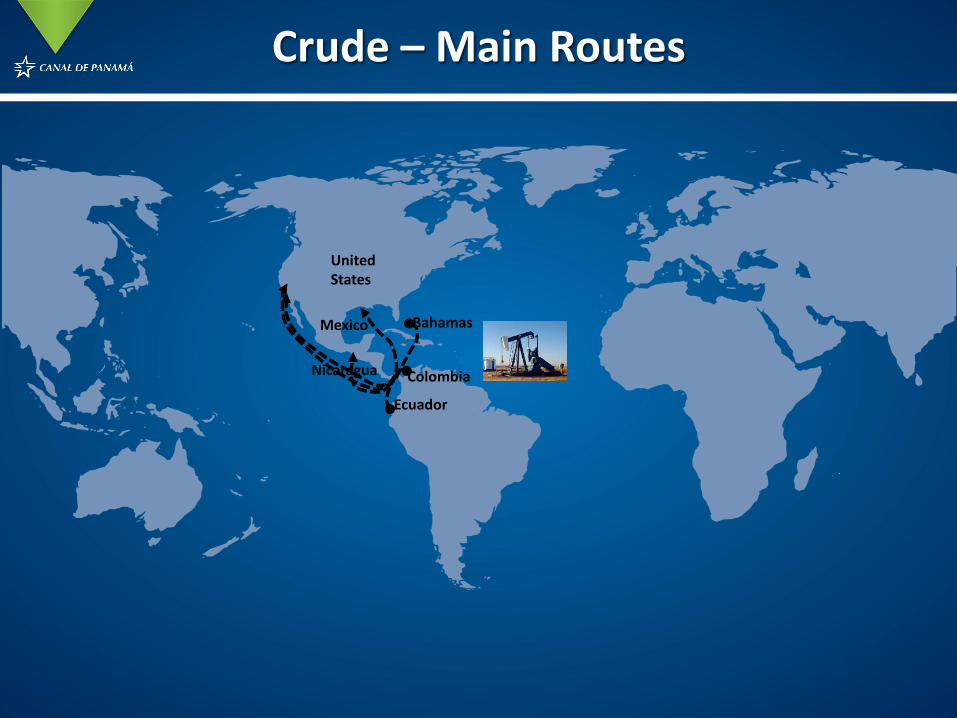

Crude – Main Routes

United StatesJapan

Benzene – Main Routes

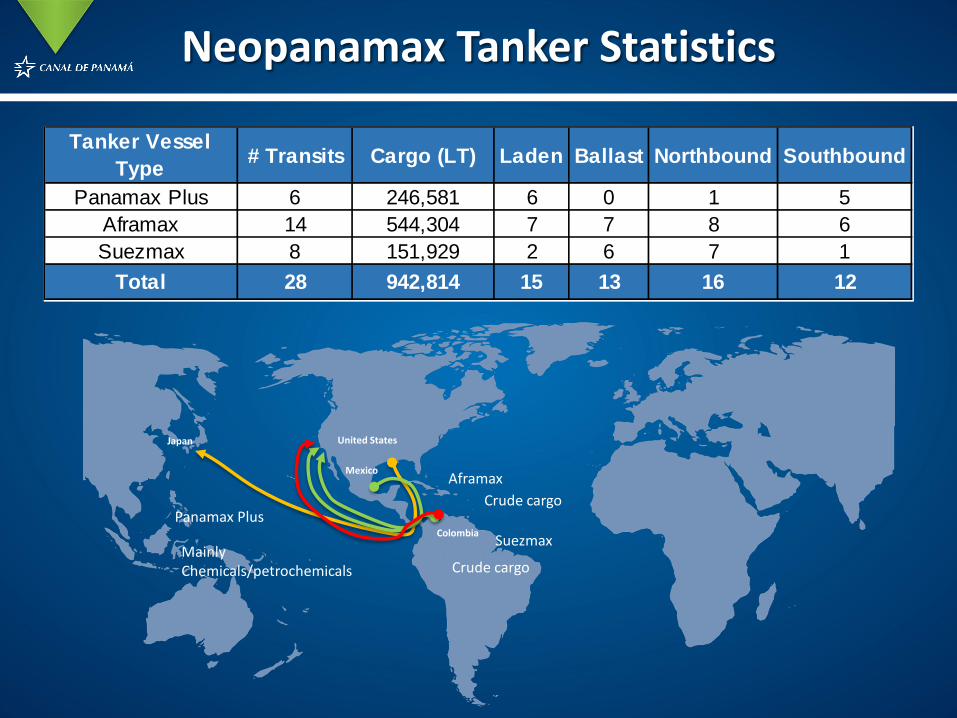

Neopanamax Tanker Statistics

Tanker Vessel Type # Transits Cargo (LT) Laden Ballast Northbound Southbound

Panamax Plus 6 246,581 6 0 1 5Aframax 14 544,304 7 7 8 6Suezmax 8 151,929 2 6 7 1

Total 28 942,814 15 13 16 12

Panamax Plus

Mainly Chemicals/petrochemicals

United StatesJapan

SuezmaxColombia

Mexico

Crude cargoAframax

Crude cargo

Liquid Bulk – Market Outlook

15,750

40,875

18,000

13,000

30,000

14,625

12,500

28,750

13,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2010

-Jan

2010

-Mar

2010

-May

2010

-Jul

2010

-Sep

2010

-Nov

2011

-Jan

2011

-Mar

2011

-May

2011

-Jul

2011

-Sep

2011

-Nov

2012

-Jan

2012

-Mar

2012

-May

2012

-Jul

2012

-Sep

2012

-Nov

2013

-Jan

2013

-Mar

2013

-May

2013

-Jul

2013

-Sep

2013

-Nov

2014

-Jan

2014

-Mar

2014

-May

2014

-Jul

2014

-Sep

2014

-Nov

2015

-Jan

2015

-Mar

2015

-May

2015

-Jul

2015

-Sep

2015

-Nov

2016

-Jan

2016

-Mar

2016

-May

2016

-Jul

2016

-Sep

2016

-Nov

2017

-Jan

2017

-Mar

2017

-May

2017

-Jul

Tanker Time Charter Evolution

1 Year Timecharter Rate 150,000 dwt D / H Modern Tanker 1 Year Timecharter Rate 110,000 dwt D / H Modern Tanker

1 Year Timecharter Rate 74,000 dwt Modern Products Tanker

Source: Clarksons Research, October 2017

Tankers Actual Capacity (in million DWT)

265%

7212% 61

10%

10919%87

15%

22439%

Handysize

Handymax

Panamax

Aframax

Suezmax

VLCC

3, 4% 5, 7%

7, 10%

15, 22%

10, 14%

30, 43%

Tankers Capacity by 2022 (in million DWT)

Tanker Fleet Actual Fleet Total Capacity FleetPanamax 4,277 158,680,738 Neopanamax 1,495 184,374,642 Postpanamax 802 236,318,999 Grand Total 6,574 579,374,379

Tanker Fleet Order Book by 2022 Capacity Added by 2022Panamax 417 13,926,914 Neopanamax 195 24,662,656Postpanamax 95 29,558,212 Grand Total 707 68,147,782

88% 59% 87% 56%

Tanker Fleet Capacity Current and Estimated by 2022

Neopanamax Tanker Economics160,000 dwt Suezmax

DWT @ 50 f ≈ 130,000 m. tons

US crude oil API barrelsWTI 39.6 1,000,003

Colombian crude oils API barrelsCaño-limon 30.0 933,173Vasconia 24.3 900,238

Venezuelan crude oilsBachaquero Heavy 17.0 858,057Bachaquero Extra Heavy 13.0 834,945Tia Juana Light 31.0 938,951

Brazilian crude oilFrade 20.5 878,223

Ecuadorian crude oilOriente 24.0 898,504

Agenda

Panama Canal Expansion

Panama Canal ExpansionPerformance

Impact of the Expansion on Tankers

The Next Frontier

Corozal Container Terminal

New container terminal to serve more than 5MM TEU.

LNG Terminal Capitalizes on global LNG flows by offering LNG bunkering to

vessels. Competitive LNG traffic toll system will support U.S. to Asia market.

Pipelines Opportunities related to the flow of

petrochemicals and refined products from one ocean to the other.

Vessel Repairs Services Facilities to provide major scheduled ship

repairs, routine maintenance or emergency repairs.

Top-Off Operations Potential for developing a ship-to-ship top-off

operation in Panama.

Power Generation Cost-competitive through the use of LNG as

alternate fuel source.

Logistics Park Offers a strategic location for distribution and

value-added activities.

Bunkering Opportunities to obtain a larger market share in

vessel bunkering.

Roll-on Roll-off Terminal Potential for a dedicated terminal for vehicle

transshipment in Panama

Areas with Development Potential

EXPANSION OF THE PANAMA CANAL AND ITS IMPACT ON TANKERS

José Ramón Arango S.Liquid Bulk Segment

October 4th 2017