exploring new business impacts - gsma · 2013-04-29 · exploring new business impacts ... computin...

TRANSCRIPT

© GSM Association 2012

Exploring New Business Impacts

Ana Tavares Latiibeaudiere,Head of the Connected Living Programme

© GSM Association 2012

Speakers

Matt Hatton, Director, Machina Research

Mel Coker, Vice President of Product Development, AT&T EmergingDevices

Marc Overton, Vice President of Wholesale & Machine to Machine(M2M) Everything Everywhere

Nakul Duggal, Vice President of Product Management, QualcommCDMA Technologies, Qualcomm

Peter Linder, Networked Society Evangelist, Ericsson

© GSM Association 2012

© GSM Association 2012

Connected House 2012

Hospitality Suite CY13, The Courtyard

The Global Impact of theConnected LifeMatt Hatton, Director

Machina Research

29 February 2012

The ‘Connected Life’ in 2020: a world of24 billion connected devices

• Global connected devices1 willincrease from 9 billion in 2011 to24 billion in 2020 across alltechnologies

• Growth will be dominated byM2M, which will account for halfof all devices in 2020, up from14% in 2011

• 2.3 billion cellular M2M devicesin 2020

• A USD1.2 trillion opportunity forMNOs

MachinaResearch 6

0

5

10

15

20

25

30

2011 2015 2020

Conn

ecte

d de

vice

s (b

illio

n)

Network infrastructure Mobile handsets

PC/laptops Tablets

M2M

Connected devices 2011-2020Source: Machina Research, 2011

1 “Connected devices” comprises all devices used for transmitting and receivingpacket data telecommunications via any wide-area or local area network. Itincludes PCs/laptops, mobile handsets, tablets and numerous M2M applications

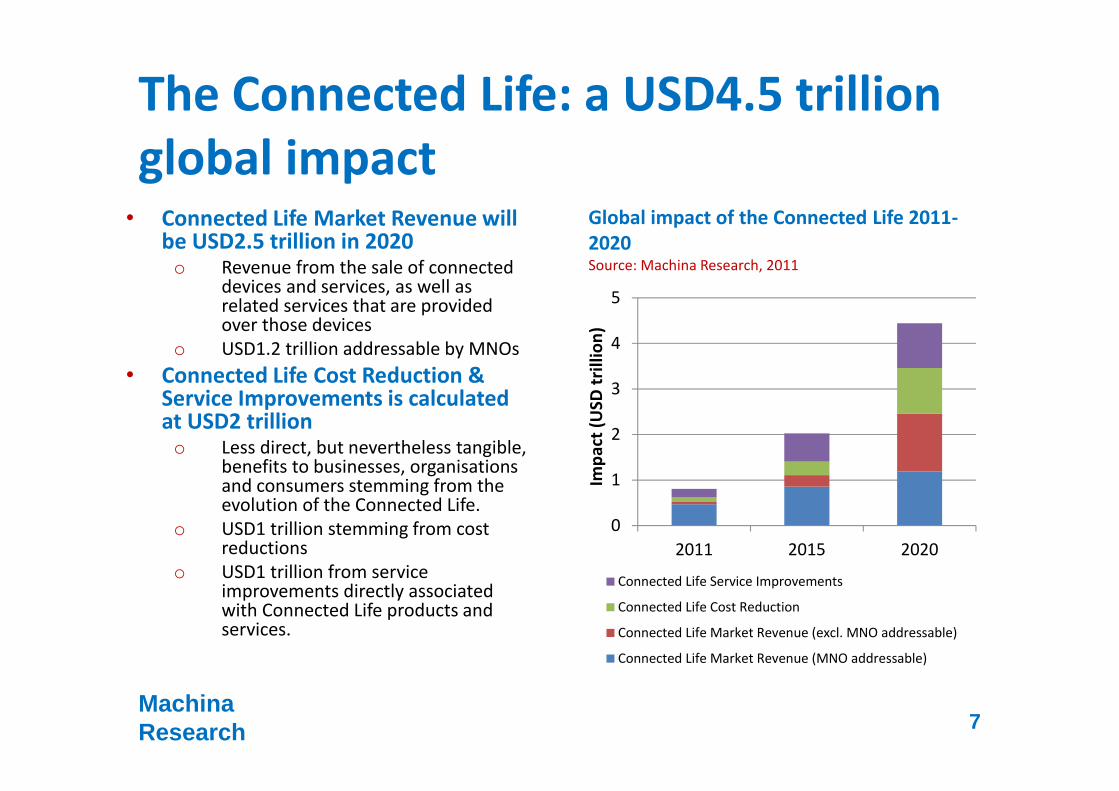

The Connected Life: a USD4.5 trillionglobal impact

0

1

2

3

4

5

2011 2015 2020

Impa

ct (U

SD tr

illio

n)Connected Life Service Improvements

Connected Life Cost Reduction

Connected Life Market Revenue (excl. MNO addressable)

Connected Life Market Revenue (MNO addressable)

MachinaResearch 7

Global impact of the Connected Life 2011-2020Source: Machina Research, 2011

• Connected Life Market Revenue willbe USD2.5 trillion in 2020o Revenue from the sale of connected

devices and services, as well asrelated services that are providedover those devices

o USD1.2 trillion addressable by MNOs• Connected Life Cost Reduction &

Service Improvements is calculatedat USD2 trilliono Less direct, but nevertheless tangible,

benefits to businesses, organisationsand consumers stemming from theevolution of the Connected Life.

o USD1 trillion stemming from costreductions

o USD1 trillion from serviceimprovements directly associatedwith Connected Life products andservices.

About the research• Undertaken by Machina Research

during December 2011 and January2012 in conjunction with the GSMAssociation

• Building on our ConnectedIntelligence forecast databaseo 54 countrieso 60 application groupso Connections, traffic and revenueo 2010-2020 forecasts

• For each application group weidentified the impact that connecteddevices would have in three keyareas:o Connectivity, devices and service

revenue (from CI database), andrevenue from related services

o Cost reductiono Service improvement

Category ofimpact

Type of benefit

Connected Lifemarket revenue

The connected PAYD insurance device,device/service management, theprovision of connectivity and the saleof PAYD insurance.

Connected Lifecost reduction

Cost reductions for drivers throughonly paying for the cover that theyneed, cost reductions for insurersthrough better information and theability to better manage risk and betterenforce policy terms and conditions.

Connected Lifeserviceimprovements

The ability to better tailor insurancepolicies to individual driver needs.

MachinaResearch 8

Global impact of the Connected Life,example application: connected carinsuranceSource: Machina Research, 2011

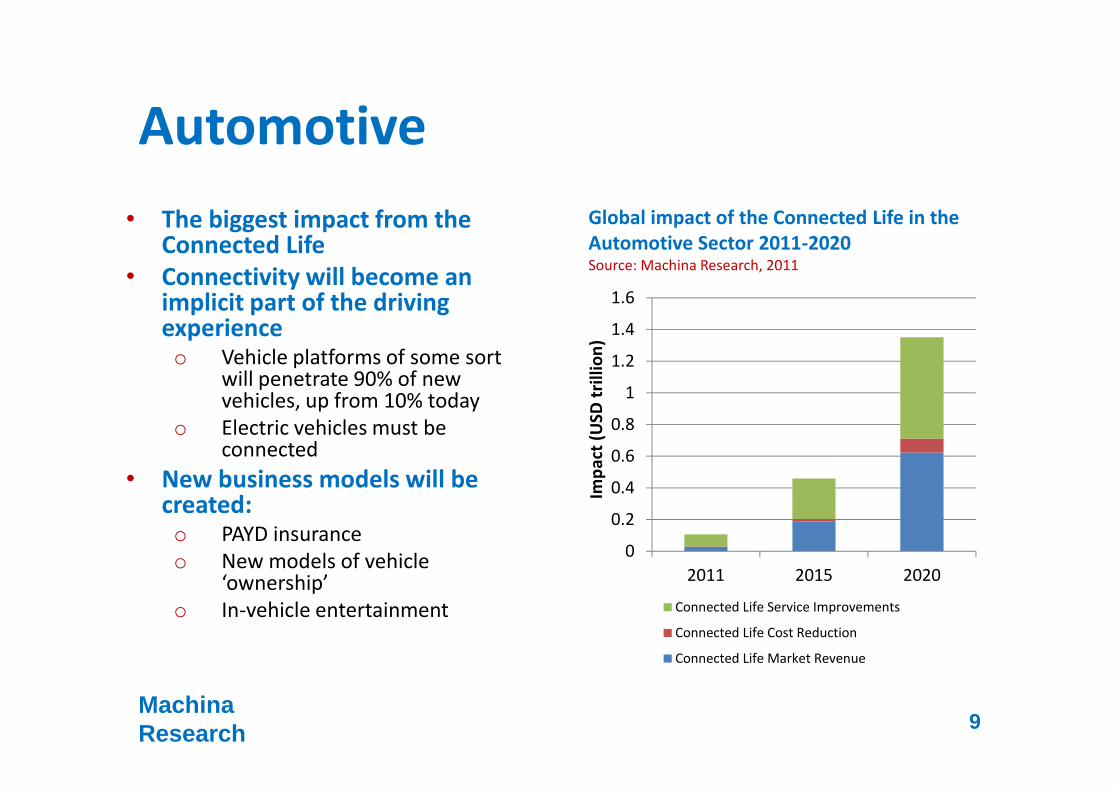

Automotive

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

2011 2015 2020Im

pact

(USD

trill

ion)

Connected Life Service Improvements

Connected Life Cost Reduction

Connected Life Market Revenue

MachinaResearch 9

Global impact of the Connected Life in theAutomotive Sector 2011-2020Source: Machina Research, 2011

• The biggest impact from theConnected Life

• Connectivity will become animplicit part of the drivingexperienceo Vehicle platforms of some sort

will penetrate 90% of newvehicles, up from 10% today

o Electric vehicles must beconnected

• New business models will becreated:o PAYD insuranceo New models of vehicle

‘ownership’o In-vehicle entertainment

Healthcare

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

2011 2015 2020Im

pact

(USD

trill

ion)

#REF!

Connected Life Service Improvements

Connected Life Cost Reduction

MachinaResearch 10

Global impact of the Connected Life in theHealthcare Sector 2011-2020Source: Machina Research, 2011

• Huge cost savings can berecognised in healthcareo Clinical remote monitoring

will generate USD350 billionin cost savings and benefitsfrom pre-emptive action

o ‘Assisted Living’ applications(from Vitality Glow-Capsthrough to comprehensiveliving solutions) will allowpeople to stay in their homeslonger, saving USD270 billion

o Numerous other applicationsincluding telemedicine andfirst responder connectivitywill also generate cost savingsand quality-of-serviceimprovements

Utilities

0

0.05

0.1

0.15

0.2

0.25

2011 2015 2020Im

pact

(USD

trill

ion)

Connected Life Service Improvements

Connected Life Cost Reduction

Connected Life Market Revenue

MachinaResearch 11

Global impact of the Connected Life in theUtilities Sector 2011-2020Source: Machina Research, 2011

• Smart meters will facilitate bigcost reduction gainso Utilities – automated meter

reading and fraud reductionsworth USD20 billion in 2020

o Home-owners – changing userbehaviour in reducing energyusage (and thus spend) to thetune of USD85 billion

• Other utilities benefits include:o Revenue generated from

electric vehicle chargingo More secure and reliable

distribution network

Conclusions

• The impact of the Connected Life goes waybeyond the USD1.2 trillion addressableopportunity for mobile network operators

• It facilitates new business models and allowsmassive efficiency savings and serviceimprovements to give a total impact valuedat USD4.5 trillion

• Immeasurable impact on, and benefit to,society

MachinaResearch 12

EmergingDevicesToday

© 2012 AT&T Intellectual Property. All rights reserved. AT&T and the AT&T logo are trademarks of AT&T Intellectual Property.

AT&T’s Emerging Devices Organization

Created to bring wireless connectivity to ahost of new devices and applications in theconsumer marketplace

Created to deliver success by building strongpartnerships to launch innovative productsin new connected consumer segments

The Emerging Devices Organizationwas formed in October 2008 toharness the tremendous growth inthe demandfor wireless data and build the “nextbig thing” in the communicationsindustry.

15

AT&T’s Embedded Devices Growth

Added more than 11M devicesin 2+ years

M2M growth sustained throughhome security, tracking, insurance, …

eReaders and Tablets paceConsumer growth

3Q094Q091Q102Q103Q104Q101Q112Q113Q114Q11

3.4 M

15.8 MAT&T EDO Subscribers

by Quarter

16 © 2012 AT&T Intellectual Property. All rights reserved. AT&T and the AT&T logo are trademarks of AT&T Intellectual Property.

Emerging Devices:AT&TVerticals

Computing

Automotive

ConnectedHome

Tracking

Healthcare &Fitness

ConsumerElectronics

17 © 2012 AT&T Intellectual Property. All rights reserved. AT&T and the AT&T logo are trademarks of AT&T Intellectual Property.

The AT&TNetworks

Wireless + BroadbandWi-Fi + International

EmergingDeviceTrends

© 2012 AT&T Intellectual Property. All rights reserved. AT&T and the AT&T logo are trademarks of AT&T Intellectual Property.

Emerging Devices Trends

•Mobile gamedownloads

•Multi-playerconnectivity anywhere

•Augmented realityexperiences

GamingHealthcareTabletseReaders•Dosage reminders:text or voice

•Family alerts to ensureadherence

•Track adherence overtime

•New options to meetevolving needs (entrylevel, laptopreplacement)

•Use LTE networks foroptimal streamingexperience

•Purchase contentanywhere

•Share content acrossdevices

•Optimize readingexperience

19 © 2012 AT&T Intellectual Property. All rights reserved. AT&T and the AT&T logo are trademarks of AT&T Intellectual Property.

Emerging Devices Trends

Tethered Solutions• Use /share content & apps from smartphone• Streaming audio & video• Access to web, cloud for entertainment

Embedded Solutions• Engine, system diagnostics• Auto crash notification• Stolen vehicle assistance• Navigation, local search• Emergency voice calls• Remote Unlock, Remote Start• Real-time traffic, weather, parking• State of charge & Pre-Conditioning for EVs

Extending connectivity to the car…

20

Emerging Devices TrendsSynching it all up with the home…

Home Automation• Moisture Sensing, Water Shut Off• Temperature Control• Garage Open/Close• Lights On/Off/Dim• WiFi Touch Pad• IP Cameras

Synchronization• The home becomes the hub of personal

data• Access via any web-enabled device• Share content across all connected devices• Transition experiences between devices

Seizing theOpportunity

© 2012 AT&T Intellectual Property. All rights reserved. AT&T and the AT&T logo are trademarks of AT&T Intellectual Property.

AT&T’s Model

A winning team – one-stop shop,a “start-up” within AT&T

Business model flexibilityand openness

Fastest Mobile BroadbandNetwork…Getting Faster with 4G LTE*

AT&T Foundry – innovatingto accelerate technology

*Limited 4G LTE availability in select markets. 4G speeds delivered by LTE, or HSPA+ with enhancedbackhaul, where available. Deployment ongoing. Compatible device and data plan required. LTE is atrademark of ETSI.

23

Emerging Devices Ecosystem

Manufacturers Developers

OperatingSystems

Carriers

ContentProviders

Retailers

© 2012 AT&T Intellectual Property. All rights reserved. AT&T and the AT&T logo are trademarks of AT&T Intellectual Property.

Connected Living: BusinessImpacts Seminar

Marc OvertonVP Wholesale and M2M+44 7782 [email protected]

Hello there, allow us to introduce ourselves.We’re the UK’s biggest mobilecommunications company.

We run two of Britain’s most famoustelecoms brands, Orange and T-Mobile andare the largest wholesale mobile operator (24MVNOs including Virgin and China Telecom)

We do it with the backing of two globaltelecoms giants, France Telecom andDeutsche Telekom.

Everything Everywhere

Operators have a key role to play in enabling businesstransformation in other verticals

Operator Model Enabler Model

Defend

Capture

ConnectAccess

CollaborateIntelligence

CooperatePartnerships

ConnectedDevices

Transport &Logistics

AutomotiveUtilities

Wellbeing& health

HomeAutomation

everything. everywhere .

32%

29%

25%

7% 7%

FlatCAGR

PartnershipsPartnering is in our blood. As thelargest wholesale operator in UK, wehave considerable experience andwant to target new segments together.

Focus on M2MM2M is one of our strategic objectives. Ithas our board’s focus and as a stand-alone business unit, leverages ourInternational roaming and MVNObusinesses.

Investment and InnovationWe are investing significantly in M2M,and leveraging DT/FT’s R&D todevelop world class propositions withpartners such as the Dual IMSI.

Global footprintWe have a global service agreementwith FT/DT and TeliaSonera allowingus to closely service our connectionsand respond immediately to issues.

Global SupportOur global service agreement withFT/DT and TeliaSonera allows usto actively service our connectionsand respond immediately to anyissues.

FlexibilityUsing our MVNO experience, wehave developed a best-in-class,flexible M2M platform to managecomplex deployments.

Easy to do businesswithWe are easy to do business with:one dedicated account team,one contract, one SLA.

Embedded connectivity is different from smartphones

Everything Everywhere has :• The largest GPRS network in the world and the largest on-net footprint in Europe• Outstanding global roaming coverage• EE/ FT/DT/ TeliaSonera M2M service alliance• Dual IMSI – single SIM covering US and UK – simplify logistics/ reduce cost

Global connectivity is vital for M2Mcross border business

EE / TMUSDual IMSI

Operators are now moving into complex connectedsolutions

1. Business models vary by vertical - ARPU is not the best KPI

2. It takes a long time for some industries to grasp the M2M opportunity

3. Operators cannot do it alone - partnerships are key

1. Business models vary by vertical - ARPU is not the best KPI

2. It takes a long time for some industries to grasp the M2M opportunity

3. Operators cannot do it alone - partnerships are key

© 2011 QUALCOMM Incorporated. All rights reserved. 32

Internet ofEverything / M2MNakul DuggalVice President, Product ManagementFebruary 29, 2012

© 2011 QUALCOMM Incorporated. All rights reserved. 33

Key Trends driving M2M adoption

• Integrated System Solutions• AP + Modem + Connectivity driving down cost, size, power

• Technology and Coverage• HSPA is ubiquitous today; LTE evolving towards a global footprint

• M2M as a managed service• Devices “come with data connectivity”

© 2011 QUALCOMM Incorporated. All rights reserved. 34

Value of Integration in the M2M value chain

Qualcomm

moduleOEM

licensee

deviceOEM

systemintegrator

WLANPLC / HomePlug Green PHYBluetoothFMLocation / GPS / GNSSEthernetPON

© 2011 QUALCOMM Incorporated. All rights reserved. 35

Integration optimizes total system costExample: A Smart Meter – before and after integration

WWANmodem

Appsprocessingand HANcomms

Metrology

LCD, PCB,materials

© 2011 QUALCOMM Incorporated. All rights reserved. 36

HSPA and LTE optimize use of spectrumM2M can access globally ubiquitous high bandwidth, low latency networks

Spectral efficiency2x5Mhz TDD

Source: Mobile Broadband Comparison; CDG; 2008.(1) Assumptions 5 MHz FDD, WCDMA assumes no DSCH. HSDPA assumes 1x1 SISO, HSPAassumes 1x2 SIMO; HSPA+ includes 1x2 SIMO and equalizer: LTE includes 2x2 MIMO

(2) Assumptions, 5 MHz FDD, HSPA+ and LTE includes 1x2 SIMO. HSPA+ includes no IC, HSPA =Rel. 6. HSPA+ = Rel. 7

Deployed in 135 countries

On course to reach 1 billionconnections in 2012

Mobile operators to investUS$100 billion in HSPA,HSPA+ and LTE over next 5

years

Source: Connected Life – GSMA PositionPaper; GSMA; October 2011

© 2011 QUALCOMM Incorporated. All rights reserved. 37

Smart AutomotiveINFOTAINMENT & INTERNET ACCESS

TELEMATICS, SAFETY & CONVENIENCE

Hotspot

QUALCOMM CONFIDENTIAL & PROPRIETARY – INTERNAL ONLY 38

Smart Energy in the Intelligent HomeApplication Processing and Always Connected – From the Grid to the Home

smart meter /utility gateway

© 2011 QUALCOMM Incorporated. All rights reserved. 39

M2MSearch.com

Web resource withdatabase of over ~100M2M modules offered byour OEM partners Searchable by chipset model modem technology operator certification market availability form factor

© 2011 QUALCOMM Incorporated. All rights reserved. 40

©2012 Qualcomm Incorporated. All rights reserved. Qualcomm is registered trademark of QualcommIncorporated. All the trademarks or brands in this document are registered by their respective owner.

QUALCOMM Incorporated, 5775 Morehouse Drive, San Diego, CA 92121-1714

Slide subtitle

networked society

Peter Linder

Networked society Evangelist #7

Ericsson Region North America

Slide subtitle

TEX

T

TEX

T

Slide subtitle

Slide subtitle

Slide subtitle

Slide subtitle

PanelDiscussion

Thank you!