export credit conditions - ebf export credit working group

TRANSCRIPT

EXPORT CREDIT CONDITIONSA PRACTITIONER’S REPORT FROM THE COMMERCIAL BANKING SPHEREInternational Working Group meeting, 4th February, 2015 – BRUSSELS

2

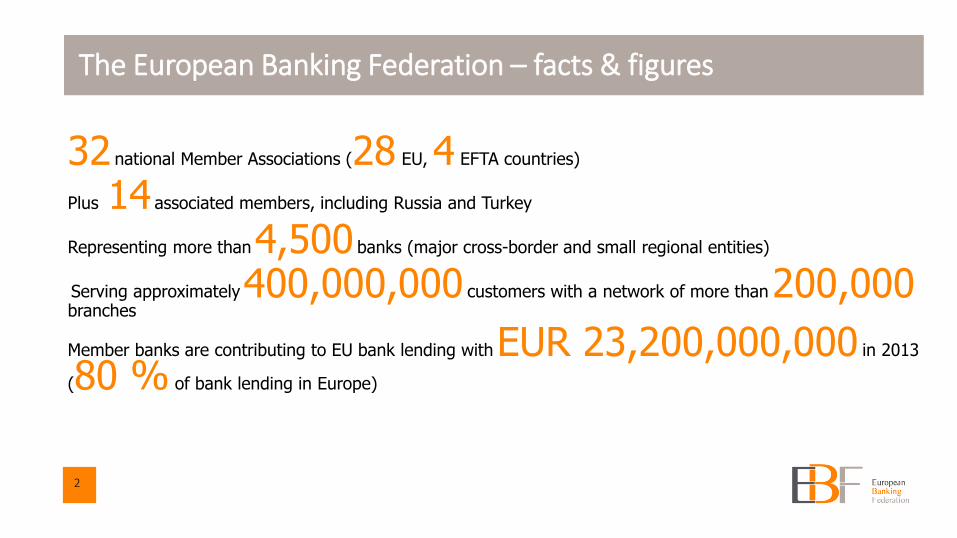

The European Banking Federation – facts & figures

32 national Member Associations (28 EU, 4 EFTA countries)

Plus 14 associated members, including Russia and Turkey

Representing more than4,500 banks (major cross-border and small regional entities)

Serving approximately400,000,000 customers with a network of more than200,000branches

Member banks are contributing to EU bank lending withEUR 23,200,000,000 in 2013

(80 % of bank lending in Europe)

3

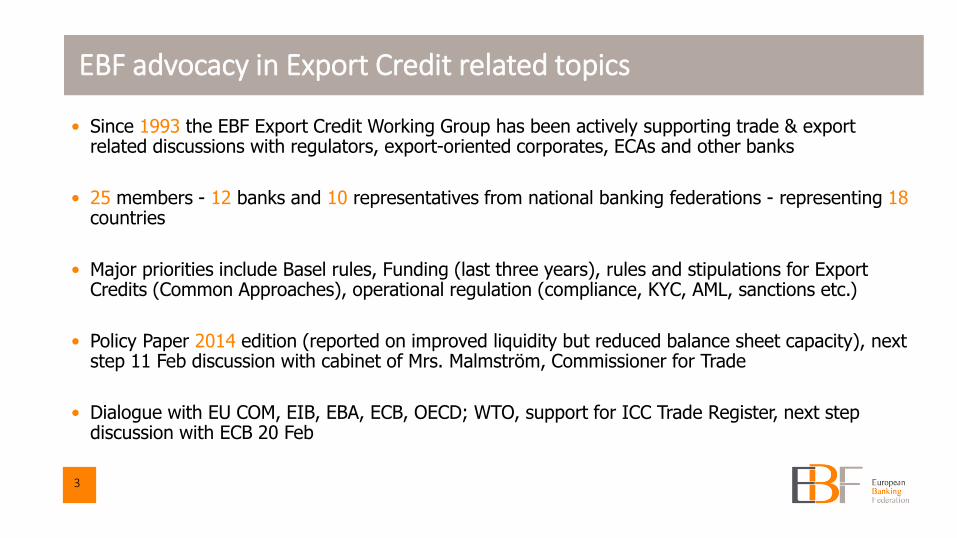

EBF advocacy in Export Credit related topics

• Since 1993 the EBF Export Credit Working Group has been actively supporting trade & export related discussions with regulators, export-oriented corporates, ECAs and other banks

• 25 members - 12 banks and 10 representatives from national banking federations - representing 18countries

• Major priorities include Basel rules, Funding (last three years), rules and stipulations for Export Credits (Common Approaches), operational regulation (compliance, KYC, AML, sanctions etc.)

• Policy Paper 2014 edition (reported on improved liquidity but reduced balance sheet capacity), next step 11 Feb discussion with cabinet of Mrs. Malmström, Commissioner for Trade

• Dialogue with EU COM, EIB, EBA, ECB, OECD; WTO, support for ICC Trade Register, next step discussion with ECB 20 Feb

4

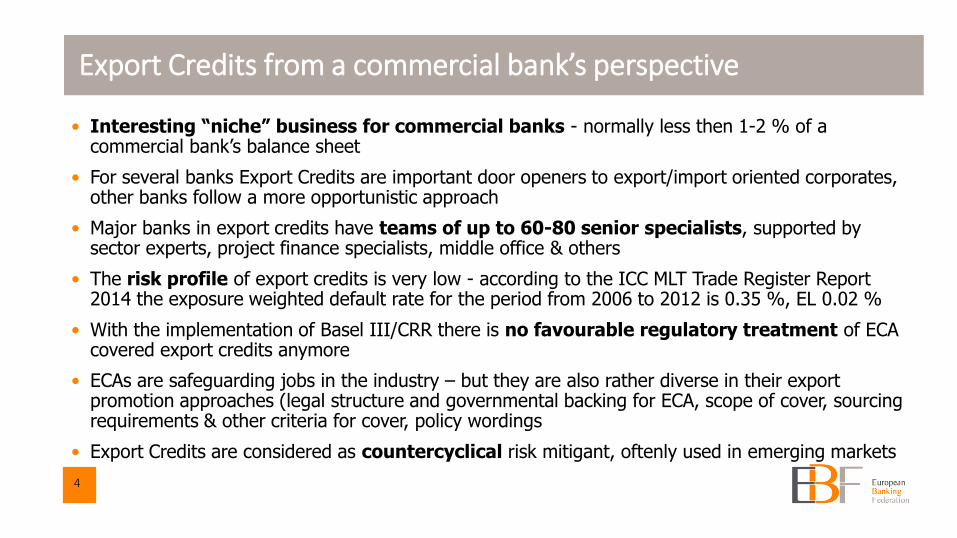

Export Credits from a commercial bank’s perspective

• Interesting “niche” business for commercial banks - normally less then 1-2 % of a commercial bank’s balance sheet

• For several banks Export Credits are important door openers to export/import oriented corporates, other banks follow a more opportunistic approach

• Major banks in export credits have teams of up to 60-80 senior specialists, supported by sector experts, project finance specialists, middle office & others

• The risk profile of export credits is very low - according to the ICC MLT Trade Register Report 2014 the exposure weighted default rate for the period from 2006 to 2012 is 0.35 %, EL 0.02 %

• With the implementation of Basel III/CRR there is no favourable regulatory treatment of ECA covered export credits anymore

• ECAs are safeguarding jobs in the industry – but they are also rather diverse in their export promotion approaches (legal structure and governmental backing for ECA, scope of cover, sourcing requirements & other criteria for cover, policy wordings

• Export Credits are considered as countercyclical risk mitigant, oftenly used in emerging markets

5

The countercyclical nature of Export Credits: Hermes

„first“ oil crisis 1973

„second“ oil crisis 1980 / LatAm debt crisis 1982

transformation of Eastern European economies,

from 1990

Current Financial and economic crisis, from 2007

Data provided

by HERMES

6

Major ECA’s and lenders in 2014

* Export Credit data submitted by 18 banks and some ECAs to tagmydeals – covering approx. 60-80 % of the market as a whole

Total Export Credit volume registered in TXF data (FY 2014): 116,659.79 USDm*

7

Major borrowers and destination countries in 2014*

Top 12 borrowing countries in export finance, considering the overall amount of every deal with at least one ECA or export finance tranche.

* Export Credit data submitted by 18 banks and some ECAs to tagmydeals – covering approx. 60-80 % of the market as a whole

8

Sector & rating breakdown in Export Credits - 2014 results*

* Export Credit data submitted by 18 banks and some ECAs to tagmydeals – covering approx. 60-80 % of the market as a whole

The arrows indicate a volume increase

or decrease in the rating band

9

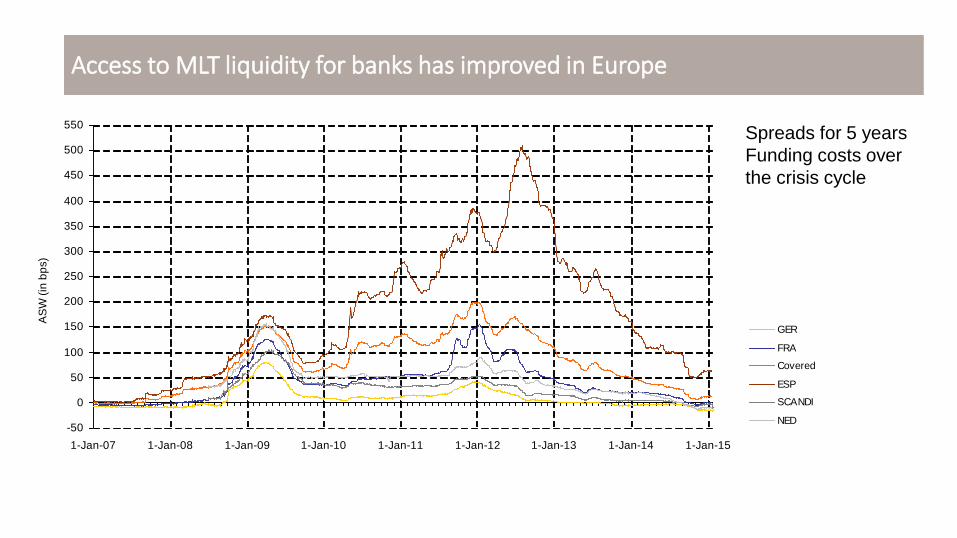

EBF survey confirms that MLT liquidity has improved

ECAs and public authorities have done a lot to support MLT liquidity in Europe

Funded refinancing solutions:13 of 20 markets surveyed have funded systems

Unfunded refinancing solutions: more common since the crisis, currently Belgium, France, Germany, Netherlands, Spain; securitisation guarantee model

Covered bonds: various - most active markets Austria, Belgium, France, Germany, UK

Public capital market transactions: active markets in France, Germany, UK

Direct lending: since crisis, available in 7 countries; in some cases SMEs only

CIRR: In EU – and more widely – there are marked differences in availability and terms. Arrangement provisions now under discussion

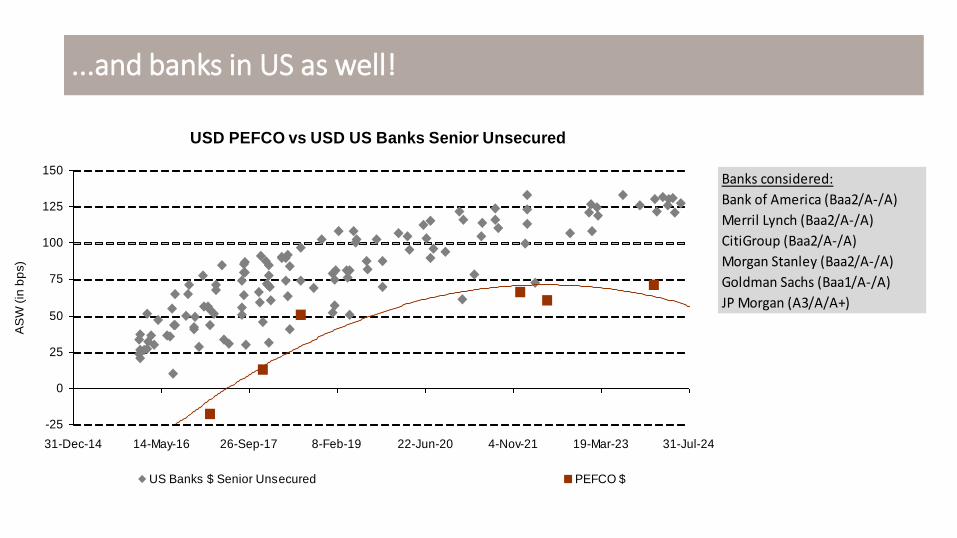

In Asia and US access to MLT liquidity was in general more stable during the recent crisis – but

ECAs also offered/supported funding solutions (e.g. direct lending by US Eximbank, KEXIM, JBIC

or project bonds)

10

-50

0

50

100

150

200

250

300

350

400

450

500

550

1-Jan-07 1-Jan-08 1-Jan-09 1-Jan-10 1-Jan-11 1-Jan-12 1-Jan-13 1-Jan-14 1-Jan-15

AS

W (

in b

ps)

GER

FRA

Covered

ESP

SCANDI

NED

Access to MLT liquidity for banks has improved in Europe

Spreads for 5 years

Funding costs over

the crisis cycle

11

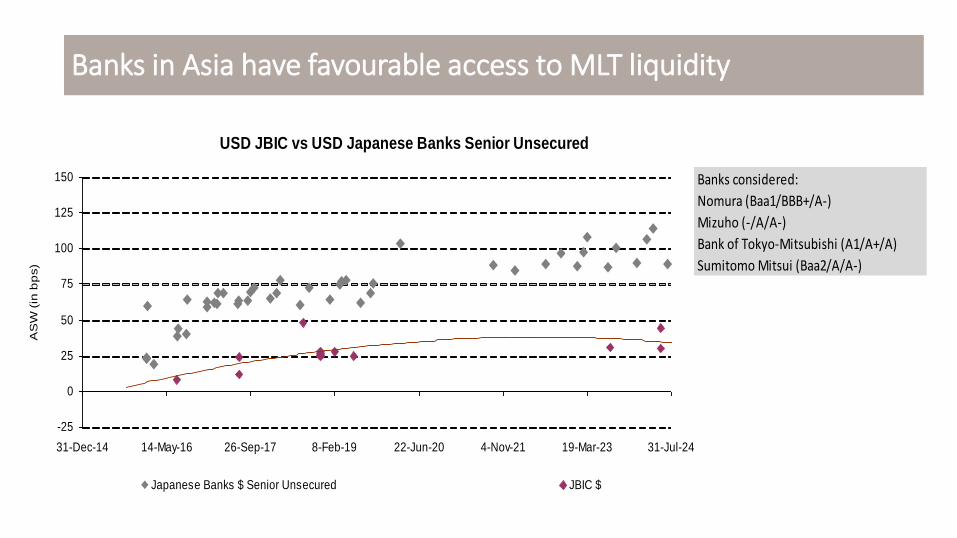

Banks in Asia have favourable access to MLT liquidity

USD JBIC vs USD Japanese Banks Senior Unsecured

-25

0

25

50

75

100

125

150

31-Dec-14 14-May-16 26-Sep-17 8-Feb-19 22-Jun-20 4-Nov-21 19-Mar-23 31-Jul-24

AS

W (

in b

ps)

Japanese Banks $ Senior Unsecured JBIC $

Banks considered:

Nomura (Baa1/BBB+/A-)

Mizuho (-/A/A-)

Bank of Tokyo-Mitsubishi (A1/A+/A)

Sumitomo Mitsui (Baa2/A/A-)

12

...and banks in US as well!

USD PEFCO vs USD US Banks Senior Unsecured

-25

0

25

50

75

100

125

150

31-Dec-14 14-May-16 26-Sep-17 8-Feb-19 22-Jun-20 4-Nov-21 19-Mar-23 31-Jul-24

AS

W (

in b

ps)

US Banks $ Senior Unsecured PEFCO $

Banks considered:

Bank of America (Baa2/A-/A)

Merril Lynch (Baa2/A-/A)

CitiGroup (Baa2/A-/A)

Morgan Stanley (Baa2/A-/A)

Goldman Sachs (Baa1/A-/A)

JP Morgan (A3/A/A+)

Wells Fargo (A2/A+/AA-

13

Maximum tenors according to OECD Arrangement

Maximum term -years

Repayment of principal Repayment flexibility in case of timing imbalance[1]

Cat I country5 / 8.5 with prior notification

Equal repayments. First repayment no later than 6 months from starting point, repayments no less frequently than every 6 months.

First repayment of principal no later than 12 months from starting point of credit, repayments no less frequently than every 12 months. MWA: 4.5 – Sov; 5 – non-Sov

Cat II country 10 As above Repayment: as above; MWA: 5.25 – Sov; 6 – non-Sov

Rail [2] 12 - Cat I ; 14 - Cat II As above Repayment: as above; MWA: 6.25 - Cat I; 7.25 - Cat II

Nuclear 18 - main plant As aboveRepayment instalments: as above.Max. repayment term: 15 years; MWA: 9

Climate change, renewable energy

15/18 [3] Below SDR10m: 5/8.5 - Cat I; 10 - Cat II

As aboveFirst repayment of principal no later than 18 months from start, repayments no less frequently than every 12 months. MWA: 60% max. available tenor

Non-nuclear power12 (more with prior notification)

As above MWA: 6.25

Ships 12Equal repayments. First repayment no later than 6 months of start, others at regular intervals of normally 6 and max.12 months.

Civil aircraft12 – new; 15 -exceptionally Used aircraft: max 10

Equal repayments. First repayment no later than 3 months from start, repayments no less frequently than 3 months (or 6 for both after prior notification). With prior notification, final payment can be on a specified date.

Project finance 14Among conditions for project finance terms: first repayment no later than 24 months after starting point; MWA: 7.25.Principal may be repaid in unequal instalments; principal& interest in less-frequent than semi-ann. instalments subject to conditions.

[1]“An imbalance in the timing of the funds available to the obligor and the debt service profile available under an equal, semi-annual repayment schedule” – subject to various conditions including to Maximum Weighted Average term, and principal repayment schedule.[2] Maximum repayment term cannot exceed the useful life of the asset.[3] Carbon capture and storage – 18 years; Fossil fuel substitution and Energy efficiency – 15 years.

14

All individual tenors of Export Credits in 2014*

average

amount in mln.

tenor in years

In various ECA Export Credits 2014 maximum tenors according to OECD arrangement have been used

* Export Credit data submitted by 18 banks and some ECAs to tagmydeals – covering approx. 60-80 % of the market as a whole

15

Examples for recent tenors of PRI deals in emerging markets

tenor in years1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Defense

Energy

Oil

Oil

Petrochemicals, Defense

Marine Infrastructure

Transport Infrastructure

Oil & Gaz

Data provided by

PRI should be seen as complimentary option for MLT Export Credits

16

Transportation sector – ECA tenors and alternatives

17

Energy & Renewables – ECA tenors & alternatives

* combined cycle is under renewables

18

Petrochemicals, LNG, mining – ECA tenors & alternatives

19

Telecoms – ECA tenors & alternatives

20

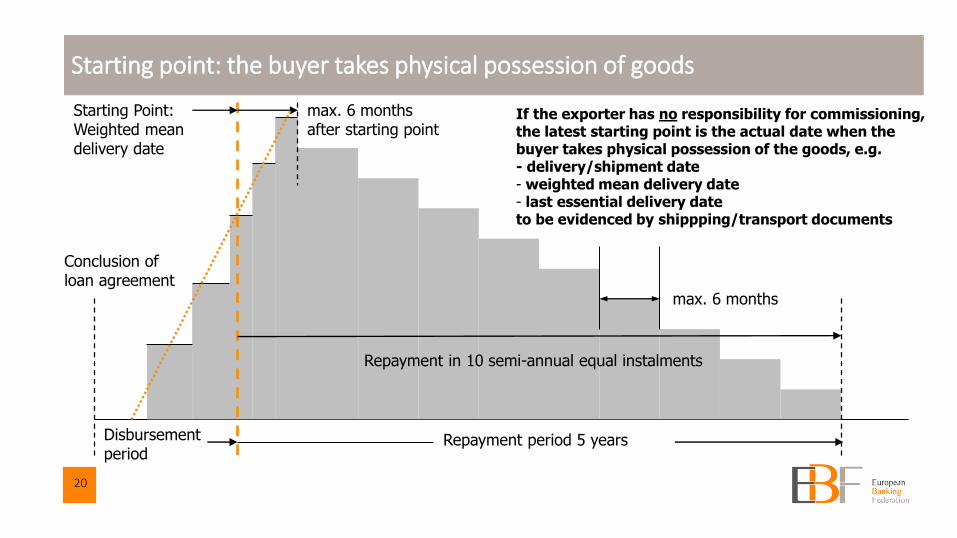

Starting point: the buyer takes physical possession of goods

Repayment period 5 years

Starting Point:Weighted mean delivery date

Disbursement period

Conclusion of loan agreement

max. 6 monthsafter starting point

Repayment in 10 semi-annual equal instalments

max. 6 months

If the exporter has no responsibility for commissioning, the latest starting point is the actual date when the buyer takes physical possession of the goods, e.g. - delivery/shipment date- weighted mean delivery date- last essential delivery dateto be evidenced by shippping/transport documents

21

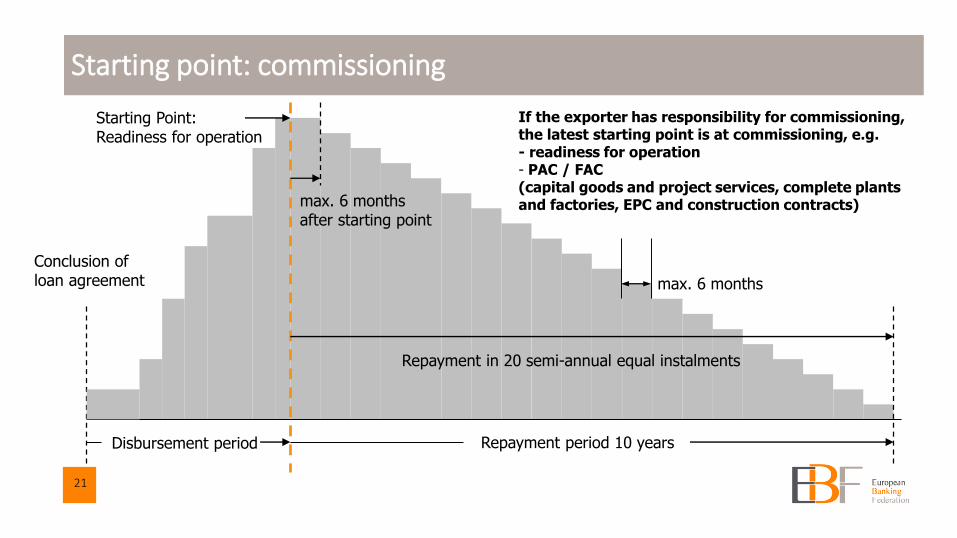

Starting point: commissioning

Repayment period 10 years

Starting Point:Readiness for operation

Disbursement period

Conclusion of loan agreement

max. 6 monthsafter starting point

If the exporter has responsibility for commissioning, the latest starting point is at commissioning, e.g. - readiness for operation- PAC / FAC(capital goods and project services, complete plants and factories, EPC and construction contracts)

Repayment in 20 semi-annual equal instalments

max. 6 months

22

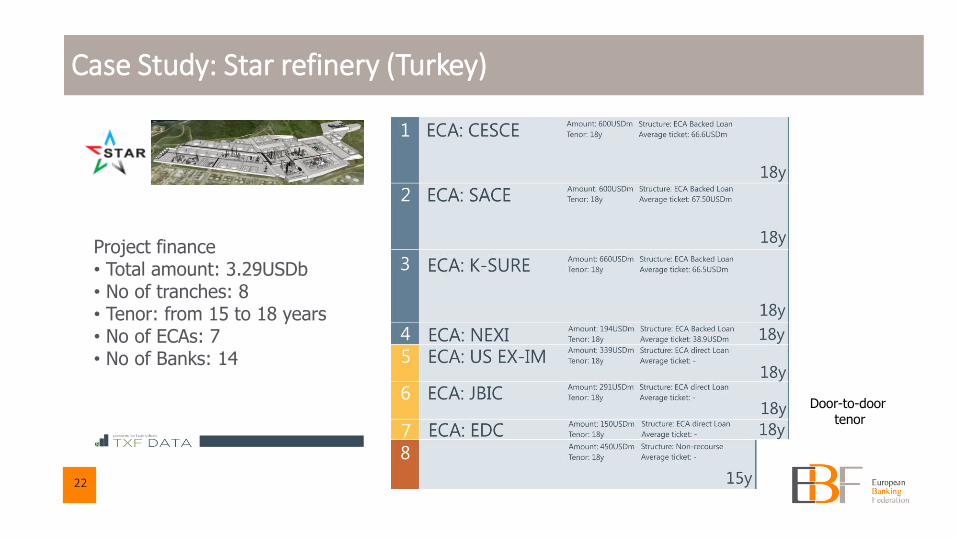

Case Study: Star refinery (Turkey)

Project finance• Total amount: 3.29USDb• No of tranches: 8• Tenor: from 15 to 18 years• No of ECAs: 7• No of Banks: 14

Door-to-door tenor

23

Case Study: Norwegian Cruise Line

Shipping finance of 2 vessels• Total amount: 1.77USDb• No of tranches: 2• Tenor: from 16 to 17 years• No of ECAs: 1• No of Banks: 5

Door-to-door tenor

24

Case Study: Freeport LNG

Project finance (LNG Terminal) • Total amount: 5.47USDb• No of tranches: 4+1• Tenor: from 6 to 24 years• No of ECAs: 2• No of Banks: 6

Door-to-door tenor

25

Conclusions & recommendations

• Preparation/negotiation of bigger capex investments is a time consuming exercise, therefore predictability of MLT financing solutions is very important - ECAs are considered as very predictable even in crisis scenarios or if the investment climate is going down

• Bigger capex investments require MLT financing solutions which are appropriate to the lifetime of goods or/and the amortisation period

• MLT Export Credits are not undermining commercial financing solutions for Emerging Markets (especially if tenors tend to be > 10 years)

• During the recent financial crisis Export Credits have also been used for MLT financing of capex investments in high income countries due to a lack of commercial alternatives

• Cooperation between ECAs, DFIs and PRIs could help to increase capacity for bigger transactions – especially if the sourcing is becoming more and more diverse

• Maximum tenors and repayment terms (e.g. starting points, first repayment due, frequency of repayment instalments) of MLT Export Credits should be consistently stipulated

26

Thank you for your attention!

For more information:

Ralph Lerch

Chairman, Export Credit Working Group

European Banking Federation

Avenue des Arts 56, B-1000 Brussels

European Transparency Register ID number: 4722660838-23.

+32 (0)2 508 37 11 | [email protected] | @EBF_FBE

www.ebf-fbe.eu

This presentation is based on substantial contributions from:

Alfonso Olivas, TXF Dominik Kloiber, TXF Folko Wohlang, HERMES Dr. Susanne Engelbach, VDMA Gina Fitzgerald, BPL Global Gerdpeter von Guretzky, SMS GmbH Florian Monschauer, Commerzbank Adrian Urbaczka, Commerzbank Benjamin Philippaerts, European CommissionElena Letemendia, EBF

Many thanks to all of you!!!