export study - sidf.gov.sa subject export study has been conducted by ecu which relates to the...

TRANSCRIPT

Marketing Consultancy Division (MCD)

Export Consultancy Unit (ECU)

______________________________________________________________

Export Study

Global Study on Cement

Safar, 1429H (March, 2008)

��

EXECUTIVE SUMMARY The subject Export Study has been conducted by ECU which relates to the global cement market. The study aims at investigating the current position and the developments of the Cement industry in the global market. In addition, it will explore and identify the potential export markets. The findings of the study are also hoped to be helpful and supportive in formulating the Fund�s future loan policy in this sector.

In general, most of the world Cement producers, characterize the Cement industry, as a capital and energy intensive industry, low labor intensity, homogenous product and heavy & mature product.

As for the KSA Cement industry, there are 10 local Cement companies in operation, which are strategically located in 10 different cities with an annual capacity of 33.2 million tons of Cement production. Local sales of Cement rose from 15.6 million tons in 2000 to over 27.1 million tons in 2007. In 2007, the quantity directed to the local market constitutes 88.4% of the total sales while the remaining i.e. 11.6% were exported. The installed capacity had increased massively during 2005-2007 period by around 52% due to the new capacity expansions for the existing projects and the entrance of new plants which started production in 2007.

The total cement capacity expansions amount to about 21.813 million tons, thus, KSA total Cement capacity will reach 49.4 million tons by 2009. With projected 7.5% annual growth in Cement demand, Cement industry will experience an overcapacity situation by 17.3 million tons in 2009. The actual local demand of Cement reached a level of 27.8 million tons in 2007 and expected to reach 32.1 million tons in 2009.

KSA total Cement exports in 2007 reached 3.56 million tons i.e. an increase of about 104% in volume from previous level. The exported quantities were basically targeted to some neighboring countries i.e. Bahrain (42%), Iraq (34%), Qatar (11%), Yemen (11%), Kuwait (1.2%), Jordan (0.21%) and UAE (0.01%).

The exports capabilities of Saudi Cement companies are very modest and needs to be developed to enhance the export performance of these companies. So far only one Saudi company has developed its exporting capability by developing a cement exporting terminal.

III

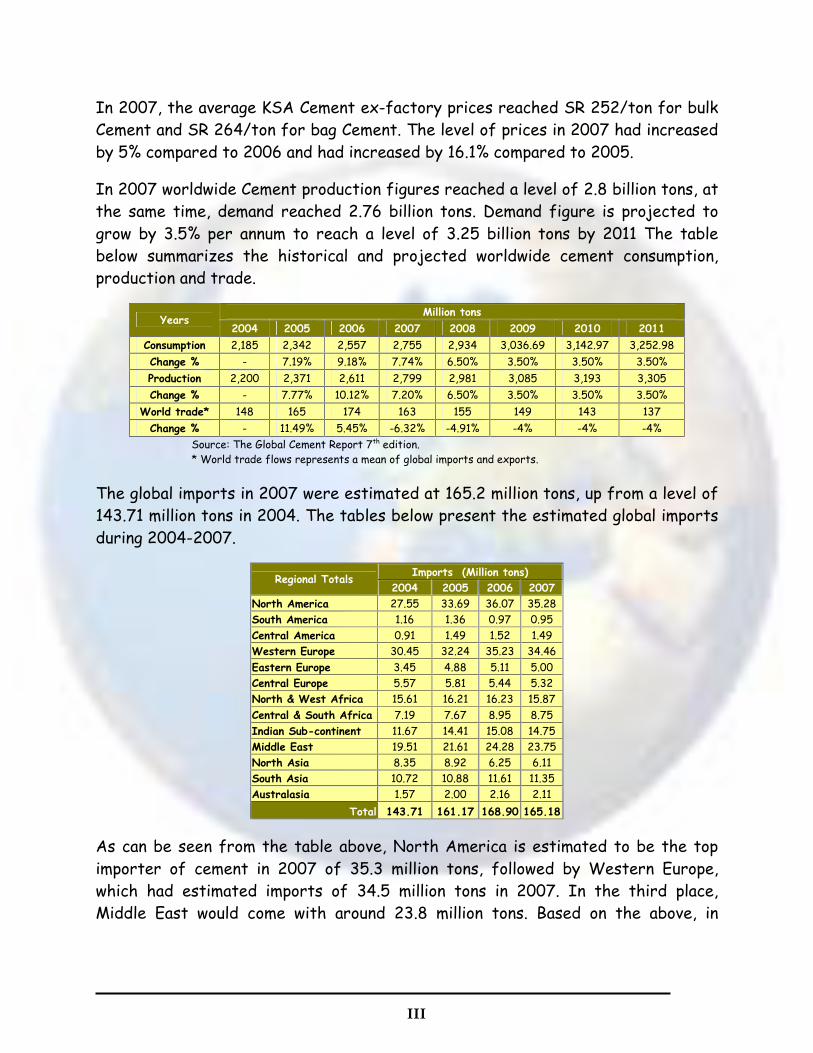

In 2007, the average KSA Cement ex-factory prices reached SR 252/ton for bulk Cement and SR 264/ton for bag Cement. The level of prices in 2007 had increased by 5% compared to 2006 and had increased by 16.1% compared to 2005.

In 2007 worldwide Cement production figures reached a level of 2.8 billion tons, at the same time, demand reached 2.76 billion tons. Demand figure is projected to grow by 3.5% per annum to reach a level of 3.25 billion tons by 2011 The table below summarizes the historical and projected worldwide cement consumption, production and trade.

Million tons Years

2004 2005 2006 2007 2008 2009 2010 2011

Consumption 2,185 2,342 2,557 2,755 2,934 3,036.69 3,142.97 3,252.98

Change % - 7.19% 9.18% 7.74% 6.50% 3.50% 3.50% 3.50%

Production 2,200 2,371 2,611 2,799 2,981 3,085 3,193 3,305

Change % - 7.77% 10.12% 7.20% 6.50% 3.50% 3.50% 3.50%

World trade* 148 165 174 163 155 149 143 137

Change % - 11.49% 5.45% -6.32% -4.91% -4% -4% -4%

Source: The Global Cement Report 7th edition. * World trade flows represents a mean of global imports and exports.

The global imports in 2007 were estimated at 165.2 million tons, up from a level of 143.71 million tons in 2004. The tables below present the estimated global imports during 2004-2007.

Imports (Million tons) Regional Totals

2004 2005 2006 2007 North America 27.55 33.69 36.07 35.28 South America 1.16 1.36 0.97 0.95 Central America 0.91 1.49 1.52 1.49 Western Europe 30.45 32.24 35.23 34.46

Eastern Europe 3.45 4.88 5.11 5.00 Central Europe 5.57 5.81 5.44 5.32 North & West Africa 15.61 16.21 16.23 15.87

Central & South Africa 7.19 7.67 8.95 8.75 Indian Sub-continent 11.67 14.41 15.08 14.75 Middle East 19.51 21.61 24.28 23.75 North Asia 8.35 8.92 6.25 6.11 South Asia 10.72 10.88 11.61 11.35 Australasia 1.57 2.00 2.16 2.11

Total 143.71 161.17 168.90 165.18

As can be seen from the table above, North America is estimated to be the top importer of cement in 2007 of 35.3 million tons, followed by Western Europe, which had estimated imports of 34.5 million tons in 2007. In the third place, Middle East would come with around 23.8 million tons. Based on the above, in

IV

addition of distance advantages, both Middle East and North & West Africa and regions could be seen as promising markets for Saudi cement companies.

Screening for potential export markets have been conducted to find out the top 10 potential markets, namely Spain, UAE, Sir Lanka, Singapore, Malaysia, Kuwait, Iraq, Ghana, Syria and Turkey. A full analysis of above markets has been included in this study. The table below presents the imports of those markets.

The imports of targeted markets (Million tons) Countries

2004 2005 2006 2007* 2008* 2009* 2010* Spain 8.84 10.72 11.5 10 9 8.1 7.29 UAE 4.4 3.5 5.5 5.3 5.3 0.5 0.5

Sri Lanka 2.6 3.1 3.5 3.7 4.1 5 5.5

Singapore 3.2 3.1 3.1 3.4 3.8 4.2 4.5

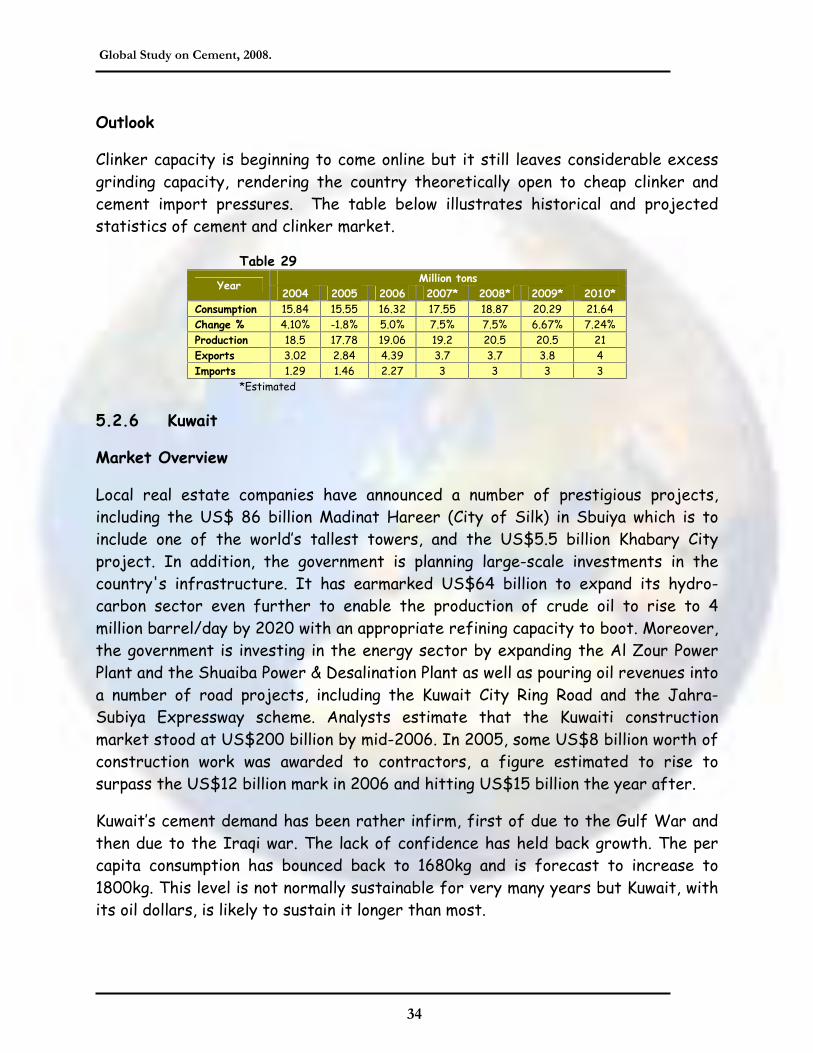

Malaysia 1.29 1.46 2.27 3 3 3 3 Kuwait 1.4 1.8 2.1 2.4 2.8 1.3 1.7

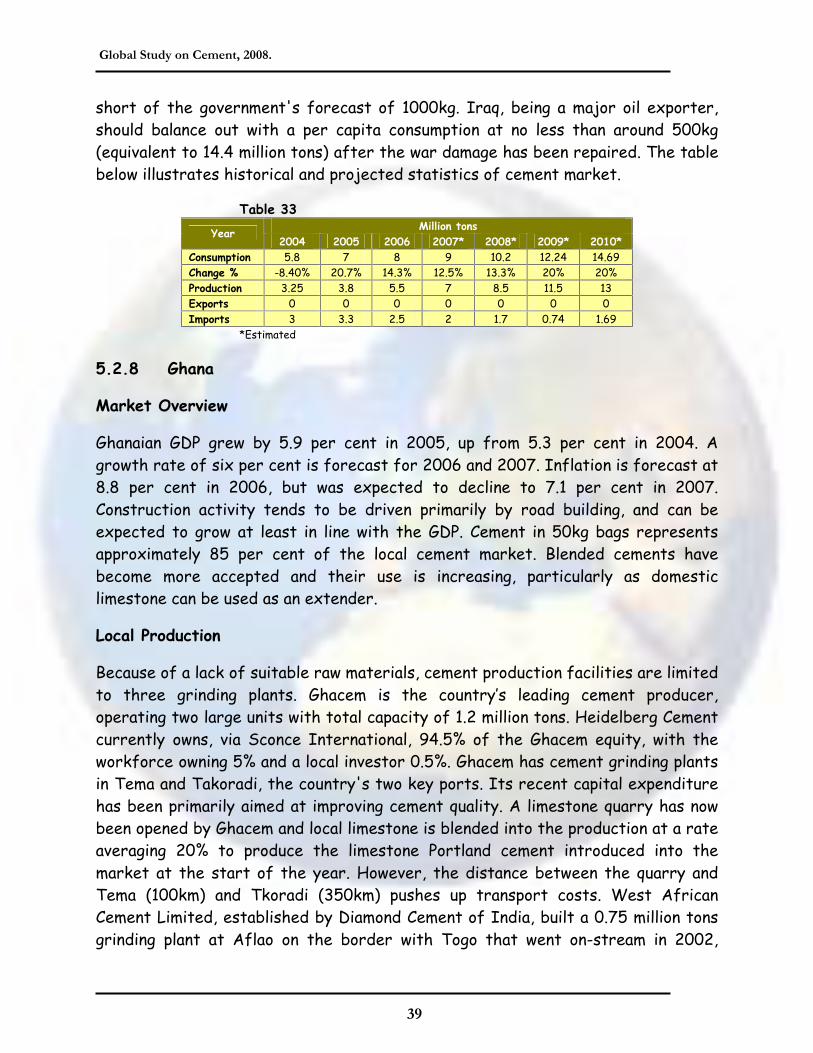

Iraq 3 3.3 2.5 2 1.7 0.74 1.69

Ghana 2.1 2.2 2.25 2.4 2.4 2.68 2.84

Syria 1.24 1.66 2.26 2.31 2.23 2.68 3.2 Turkey 0 0.25 2 2 2 2 2

* Estimated

Cement is a costly product to transport relative to its price. The cost of transporting cement from one country to another can exceed the value of its production. For years, cement was considered a local product, unfeasible to export due to the high cost of land transportation. However, with the development of marine shipping and the savings it introduced to the global transportation industry, regional markets for cement started to evolve, with cement being transported between neighboring countries at an economically feasible cost. The following tables present the land and ocean transportation costs, per ton, in SR.

Regarding fright rates, it is usually determined based on several parameters such as loading and discharging rate. However, the following table presents the average fright rates from KSA to different destinations at 4,500 ton/day loading and discharging rate.

Destination USD/Ton GCC states 22-18 India 50-40 China 60-70

(SR/Ton) From / To

UAE Qatar Kuwait Oman Bahrain Yemen Lebanon Iraq Jordan Syria RUH 140 80 80 180 72 180 244 140 208 232

JED 260 192 184 300 172 140 224 236 184 212

DAM 120 52 52 160 48 224 290 112 235 280

V

South Asia 60-70

Eastern Europe 50-60

Western Europe 80-90 North America 100-130 South America 120-140 West Africa 90-100 East Africa 50-60 South Africa 70-80 North Africa 40-50 Australia & New Zealand 100-120

With regards to the landed prices, the table below illustrates the average landed prices in targeted markets.

Countries USD/ton Spain 107.03 UAE 80 Sir Lanka 112 Singapore 59.14 Malaysia 67.90 Kuwait 75 Iraq 107 Ghana 107.62 Syria 130 Turkey 75.6

CONCLUSION

The Kingdom�s Cement industry is operating at near full capacity, with the domestic demand comprising 88.4% of the total supplies and exports representing around 11.6% (3.6 million tons). Bahrain and Iraq are considered the biggest export markets as they imports around 42% and 34% of total Saudi export respectively. The total local installed capacity is expected to reach more than 49 million tons in 2009, an increase of 49% in comparison with 2007.

Overall, although there are potential export markets for Saudi cement, exporting cement seems to be difficult due to number of export barriers. Firstly, the Saudi ports do not have cement export terminals, which are very crucial to increase the loading rate of cement and, consequently, reducing the shipping costs. Secondly, Saudi cement companies lack of experiences and relationships with international cement trading companies, which are aware of cement imports orders and manage/arrange shipping and delivering throughout the world. Unfortunately, such companies are fully dominated by international cement company�s cartel such as Lafarge and Italicement. Furthermore, increasing the fright rates of shipping costs, which is attributed to the increasing of oil prices, war risk insurance and depreciation of USD value. Finally, most of Saudi cement companies do not develop

VI

their vision of international expansion strategies such as installing grinding plants in neighborhood markets.

RECOMMENDATION

Based on the current market situation of the local market and challenges existing in export markets, exporting cement seems to be difficult due to the lacking of enough export capability within the existing Saudi cement companies. Local cement companies should jointly consider establishing a cement trading company, which could act as the export arm for the Saudi cement companies in overseas markets. The best legal form for such company is to be owned by all Saudi cement companies. The main objectives of this company could be summarized as follows:-

To develop export port terminals in the major coasts of KSA. To explore export opportunities and identify promising export markets. To establish worldwide networks of contacts with the cement trading

companies as so to receive export orders. To manage the surpluses of cement in KSA and to prevent future

strangulations in the local market. To establish contacts with shipping companies and arrange shipping process

with the lowest cost.

Furthermore, exporters should be encouraged to contact local export insurance and credit institutions in order to utilize the available facilities for export credit & insurance programs towards risky countries. �The Saudi Export Program� from the Saudi Fund for Development will help local manufactures in increasing their market share and expanding their export activities to more countries with the lowest possible risk. This is a good omen as Saudi Arabia has joined WTO.

GLOBAL STUDY ON CEMENT TABLE OF CONTENTS

Sections Page

1 INTRODUCTION ................................................................................. 1 1.1 Research Objectives ......................................................................................................................................1 1.2 Data Collection Methods and Sources .....................................................................................................2 1.3 Cement Conferences ......................................................................................................................................2

2 PRODUCT DESCRIPTION ........................................................................ 3 2.1 General Background........................................................................................................................................3 2.2 Cement................................................................................................................................................................3 2.3 Cement Manufacturing Process..................................................................................................................4 2.4 Major Characteristics of the Cement Industry ...................................................................................5

3 WORLD CEMENT MARKET....................................................................... 6 3.1 Highlight on Regional Consumption/Production Situation ..................................................................7 3.2 International Trade Flows ...........................................................................................................................8 3.3 Major Cement consuming countries ..........................................................................................................9 3.4 Leading cement and clinker exporters................................................................................................... 10 3.5 Leading cement and clinker importers ....................................................................................................11 3.6 Leading International cement companies .............................................................................................. 13

4 HIGHLIGHTS ON KSA CEMENT INDUSTRY.................................................. 15 4.1 Demand............................................................................................................................................................. 15 4.2 Supply ............................................................................................................................................................... 16 4.3 Imports ............................................................................................................................................................ 17 4.4 Export sales.................................................................................................................................................... 17 4.5 Views of local cement producers on cement exporting .................................................................... 18 4.6 Advantage/Disadvantage of exporting .................................................................................................. 19 4.7 Exporting Capability & Requirements of exporters........................................................................... 19

5 POTENTIAL CEMENT EXPORT MARKETS..................................................... 20 5.1 Potential markets for Saudi Cement companies..................................................................................20 5.1.1 Spain .................................................................................................................................................................20 5.1.2 UAE ...................................................................................................................................................................23 5.1.3 Sir Lanka..........................................................................................................................................................26 5.1.4 Singapore.........................................................................................................................................................29 5.1.5 Malaysia ........................................................................................................................................................... 31 5.1.6 Kuwait ...............................................................................................................................................................34 5.1.7 Iraq ...................................................................................................................................................................36 5.1.8 Ghana ................................................................................................................................................................39 5.1.9 Syria..................................................................................................................................................................40 5.1.10 Turkey ..............................................................................................................................................................42

6 TRANSPORTATION ............................................................................. 45 6.1 Land Transportation Cost...........................................................................................................................45 6.2 Ocean Transportation Cost........................................................................................................................45

7 INSURANCE ..................................................................................... 48 8 CONCLUSION ................................................................................... 49 9 RECOMMENDATION ............................................................................ 50

Global Study on Cement, 2008.

1

1 INTRODUCTION

The subject report has been conducted by ECU which relates to the Global Cement Industry. The study aims at investigating the current position and the developments of the Cement industry in the global markets. In addition, it will explore the potential export markets for Saudi Cement companies. The findings of the study are also hoped to be helpful and supportive in formulating the Fund�s future loan policy in this sector. Therefore, the following sections will provide an insight on the historical & the expected market situation. In addition, it will include ECU overall assessment of those markets at present.

1.1 Research Objectives

The aim and the principle of this present study are to provide a perspective on the current position and the level of developments of the Cement industry in the global market. Accordingly, the subject study intends to achieve the following research objectives:-

To determine the Cement product classifications and characteristics. In addition, identifying what changes are taking place in the product in terms of technology, features and quality that could affect the complete competitive situation for the Saudi Cement exporters.

To provide a glance on the global cement market in terms of market size, capacity, major players and market trends/developments.

To provide a glance on the Saudi cement market in terms of market size, capacity and market trends/developments.

To identify current situation of cement market worldwide and assess the supply/demand situation in light of any recent developments.

To screen international markets as so to identify potential markets for Saudi cement manufacturers based on certain selected criteria.

To measure the historical market of the potential export markets by identifying their production capacity, imports and exports. Also, investigating the imports� contribution to their overall markets.

To determine the latest available average CIF prices, in addition to explore the competitiveness of the Saudi Cement prices compared to other competitors prices in potential export markets.

To identify the requirements of Saudi cement exporters in order to increase their export performance.

To describe the competition environment in potential export markets and to determine the key success factors of those markets.

Global Study on Cement, 2008.

2

To provide the current fright rates of ocean transportation and the current quotations of land transportation to different destinations.

1.2 Data Collection Methods and Sources

Having identified the study objectives, the next step is to seek the data required for the fulfillment of those objectives. For the purpose of this industry both primary and secondary sources were required. All relevant secondary data on the global Cement market, from SIDF existing reports, imports statistics from United Nations Statistics Division � Commodity Trade Statistics Database (CO MILLION TONS RADE), the Global Cement Report (seventh edition), INTERCEM Dubai 2007 Conference, Middle East Cement conference Doha 2007, Cement industry in the GCC done by HSBC, internet sources and field survey with Saudi exporting companies, have been used to fulfill the study objectives. Compiling secondary data has built up an initial understanding of the global Cement industry characteristics before conducting the analysis.

1.3 Cement Conferences

2nd Cement Trade Middle East/Africa, 4-5 December 2007, Doha, Qatar

The conference was attended as a step to prepare and collect information for this study. CMT�s 2nd CemenTrade Mideast/Africa Conference aims to provide an update of the market dynamics in the Middle East and Africa. Besides cement and construction markets updates including Saudi Arabia, UAE, Qatar, Iraq, Iran, Bahrain, South Africa, East Africa, Egypt and South Asia, the conference also examined climate change & environmental issues and cementitious materials utilization. The conference was a good opportunity to get acquainted with new changes in cement industry and discuss the current situation of international cement industry and market with experts in cement industry.

The most interesting presentation was about Iraq market, which gave a detailed analysis about the outlook of cement consumption in Iraq market. However, unfortunately, some papers that had presented in the INTERCEM Dubai 2007 Conference were presented again in this conference with the same information.

Cemtech Dubai 16-19 February 2008

The conference held at the Grand Hyatt Hotel, the meeting attracted an impressive 300 delegates from 49 countries, all keen to gain insights into recent Middle East cement market developments. Conference proceedings featured a

Global Study on Cement, 2008.

3

variety of market-based reports including a look at what lies ahead for the Middle East cement sector in a changing world, the outlook for UAE cement and construction markets, plus overviews of expansion projects in the buoyant markets of Saudi Arabia and Iran.

2 PRODUCT DESCRIPTION

2.1 General Background

Having illustrated the objectives and research methodology of this study, it is therefore appropriate firstly to discuss the product types and its specifications.

Concrete is the most widely used man-made product in the world and is second only to water as the world�s most utilized substance. In its simplest form, concrete is a mixture of Cement paste and aggregates. As Cement being a basic ingredient of concrete, it has been around for at least 12 million years.

When the earth itself was undergoing intense geologic changes natural, Cement was being created. It was this natural Cement that humans first put to use. Eventually, they discovered how to make Cement from other materials. The Assyrians and Babylonians used clay. Later, the Egyptians advanced to the discovery of lime and gypsum mortar as a binding agent for building such structures as the Pyramids. The Greeks made further improvements and finally the Romans developed Cement that produced structures of remarkable durability.

2.2 Cement

Cement and concrete might be synonymous as household terms, but are by nature different. Concrete is a material used in building construction, as signature material in driveways, patios, basements and a host of other household items. It consist of a hard, chemically inert particulate substance, known as an aggregate (usually made from different types of sand and gravel), that is bonded together by Cement and water.

Cement is the basic ingredients of concrete and mortars. It is an artificial hydraulic binder which binds the particles of sand and aggregates together. Others, define it as, an ultra-fine gray powder, binds sand and rocks into a mass or matrix of concrete.

There are 27 types of common Cement which can be grouped into 5 general categories (Portland, Portland composite, blast furnace/slag, pozzolanic and

Global Study on Cement, 2008.

4

composite Cement & others) and 3 strength classes (ordinary, high and very high). Portland Cement, the most widely used Cementitious ingredient in today�s concrete, which currently accounts for more than three-quarters of all Cement sales worldwide, is comprised of phases that consist of atoms of calcium, silicon, aluminum, iron and oxygen. In addition, some special Cement exists like sulphate resisting Cement, low heat Cement and calcium aluminate Cement.

2.3 Cement Manufacturing Process

Cement plants are usually located closely either to hot spots in the market or to areas with sufficient quantities of raw materials. The aim is to keep transportation costs at low levels. Basic constituents for Cement (limestone and clay) are taken from quarries in these areas.

Basically, Cement is produced in two steps: first, clinker is produced from raw materials. In the second step, Cement is produced from Cement clinker. The first step can be a dry, wet, semi-dry or semi-wet process according to the state of the raw material.

The raw materials are delivered in bulk, crushed and homogenized into a mixture which is fed into a rotary kiln. This is an enormous rotating pipe of 60 to 90 m long and up to 6 m in diameter. This huge kiln is heated by a 2000°C flame inside of it. The kiln is slightly inclined to allow for the materials to slowly reach the other end, where it is quickly cooled to 100-200°C.

Four basic oxides in the correct proportions make Cement clinker: calcium oxide (65%), silicon oxide (20%), alumina oxide (10%) and iron oxide (5%). These elements mixed homogeneously (called �raw meal� or slurry) will combine when heated by the flame at a temperature of approximately 1450°C. New compounds are formed: silicates, aluminates and ferrites of calcium. Hydraulic hardening of Cement is due to the hydration of these compounds. The final product of this phase is called �clinker�. These solid grains are then stored in huge silos which is the end of phase one.

The second phase is handled in a Cement grinding mill, which may be located in a different place to the clinker plant. Gypsum (calcium sulphates) and possibly additional Cementitious (such as blast furnace slag, coal fly ash, natural pozzolanas, etc.) or inert materials (limestone) are added to the clinker. All constituents are ground leading to a fine and homogenous powder which is the end of phase two. The

Global Study on Cement, 2008.

5

Cement is then stored in silos before being dispatched either in bulk or bagged forms.

2.4 Major Characteristics of the Cement Industry

The following highlights the main characteristics of the Cement industry in general, as viewed by world Cement producers.

A process, capital intensive industry: The cost of a new Cement plant is usually above US$ 300 million. The cost of a new Cement plant is equivalent to around 3 years of turnover, which ranks the Cement industry among the most capital intensive industries. Long time periods are therefore needed before investments can be recovered and plant modifications have to be carefully planned and must take account of the long-term nature of the industry.

An energy intensive industry: Each tone of Cement produced requires 60 to 130 kilogram�s of fuel oil or its equivalent, depending on the Cement variety and the process used, and an average of 110 KWh of electricity. The energy bill represents over 25% of total production costs in the Cement industry.

An industry with low labor intensity: The growing use of computer technology and automated manufacturing techniques has allowed Cement companies minimize the number of workers needed. A modern plant is usually manned by less than 150 people.

An industry with a homogeneous product: Although produced from natural raw materials, which vary from plant to plant, Cement can be considered a standard product. There are only a few classes of Cement and in each class products from different producers can generally be interchanged. Therefore, price is the most important sales parameter next to customer service; quality premiums exist but are rather limited.

A heavy product: Land transportation costs are significant and it used to be said that Cement could not be economically hauled beyond 200 or at most 300km. The price of long road transportation may even be higher than the cost of the product. Bulk shipping has changed that, however, it is now cheaper to cross the Atlantic Ocean with 35,000 tones of cargo than to truck it 300km. In large countries, transportation costs normally cluster the markets into regional areas, with the exception of a few long-distance transfers (where, for example, sea terminal facilities exist).

A mature product: Demand for Cement (which was first produced in the early 1800s) increased considerably in the 20th century, reflecting the development of industry and growing urbanization. Consumption in the industrialized

Global Study on Cement, 2008.

6

countries multiplied 6 to 8 times following World War II. Other than a few ups and downs in both the United States and Europe in the intervening years, growth continued until the 1975 oil crisis - with a subsequent decline of 20 to 40 percent in mature markets. However, over the last 25 years, some European countries have doubled or even tripled their consumption (Greece, Portugal, Spain and Turkey), since these countries have experienced significant growth over the last 10 years.

Market parameters: Consumption of Cement is closely linked to both the state of economic development in any given country or region and to the economic cycle. In mature markets, such as Europe, where Cement consumption per capita still varies considerably from one country to another, Cement sales are dependent on evolution and habits in the construction sector, a sector that itself following very closely (usually after a brief delay) the evolution of the economy in general.

3 WORLD CEMENT MARKET

Global cement consumption has surpassed all forecasts, with worldwide demand rising from 2.185 billion tons in 2004 to stand at 2.755 billion tons in 2007 and, on present indicators, likely to rise to 2.934 billion tons in 2008. Demand figure is projected to grow by 3.5% per annum to reach a level of 3.25 billion tons by 2011 The table below summarizes the historical and projected worldwide cement consumption, production and trade.

Table 1 Million tons

Years 2004 2005 2006 2007* 2008* 2009* 2010* 2011*

Consumption 2,185 2,342 2,557 2,755 2,934 3,036.69 3,142.97 3,252.98

Change % - 7.19% 9.18% 7.74% 6.50% 3.50% 3.50% 3.50% Production 2,200 2,371 2,611 2,799 2,981 3,085 3,193 3,305

Change % - 7.77% 10.12% 7.20% 6.50% 3.50% 3.50% 3.50%

World trade 148 165 174 163 155 149 143 137

Change % - 11.49% 5.45% -6.32% -4.91% -4% -4% -4%

Source: The Global Cement Report 7th edition. * Estimated

As can be seen, the consumption of cement has increased and will increase�further during the current year. The average growth rate of consumption is around 7.7%. Nonetheless, this increase of consumption is expected to be supplied by local production as its growth rate increase in parallel with the consumption growth rate. Contrarily, world trade (imports and exports) is expected to decline due to

Global Study on Cement, 2008.

7

increasing of the local demand in most of top exporting country such as India, which starts to direct its exports to satisfy the local demand.

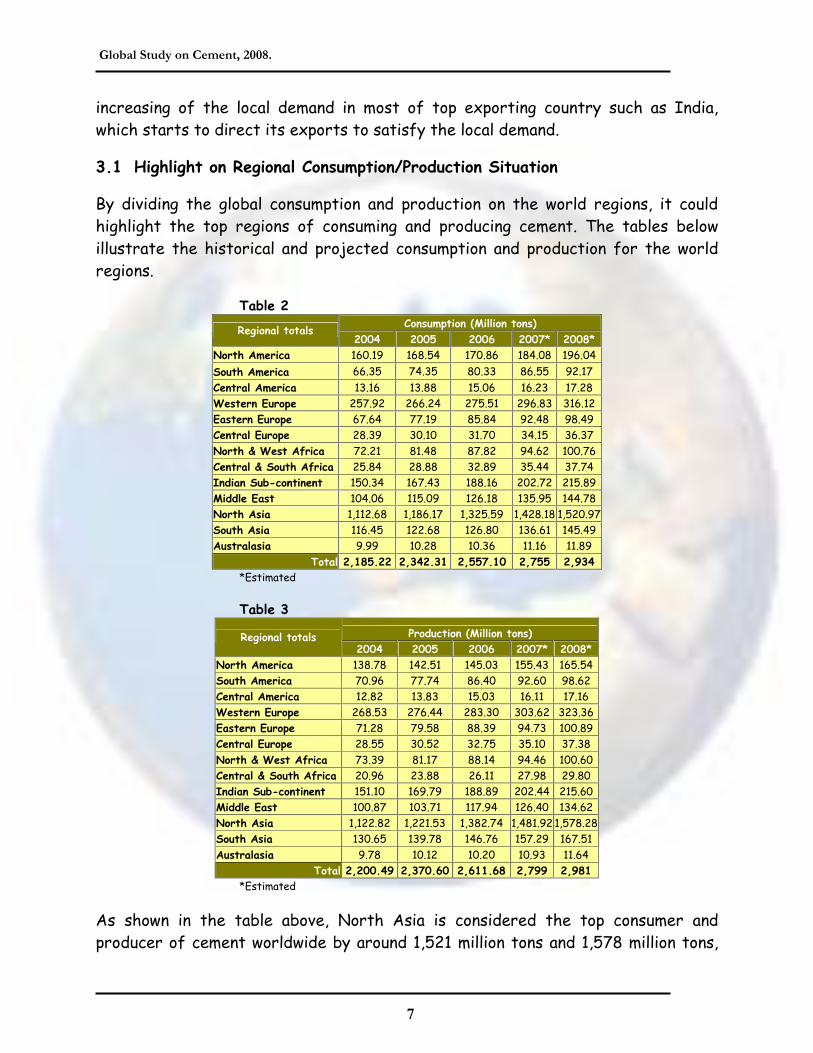

3.1 Highlight on Regional Consumption/Production Situation

By dividing the global consumption and production on the world regions, it could highlight the top regions of consuming and producing cement. The tables below illustrate the historical and projected consumption and production for the world regions.

Table 2 Consumption (Million tons)

Regional totals 2004 2005 2006 2007* 2008*

North America 160.19 168.54 170.86 184.08 196.04

South America 66.35 74.35 80.33 86.55 92.17

Central America 13.16 13.88 15.06 16.23 17.28 Western Europe 257.92 266.24 275.51 296.83 316.12 Eastern Europe 67.64 77.19 85.84 92.48 98.49 Central Europe 28.39 30.10 31.70 34.15 36.37 North & West Africa 72.21 81.48 87.82 94.62 100.76 Central & South Africa 25.84 28.88 32.89 35.44 37.74 Indian Sub-continent 150.34 167.43 188.16 202.72 215.89 Middle East 104.06 115.09 126.18 135.95 144.78 North Asia 1,112.68 1,186.17 1,325.59 1,428.18 1,520.97 South Asia 116.45 122.68 126.80 136.61 145.49 Australasia 9.99 10.28 10.36 11.16 11.89

Total 2,185.22 2,342.31 2,557.10 2,755 2,934 *Estimated

Table 3

Production (Million tons) Regional totals 2004 2005 2006 2007* 2008*

North America 138.78 142.51 145.03 155.43 165.54 South America 70.96 77.74 86.40 92.60 98.62 Central America 12.82 13.83 15.03 16.11 17.16 Western Europe 268.53 276.44 283.30 303.62 323.36 Eastern Europe 71.28 79.58 88.39 94.73 100.89 Central Europe 28.55 30.52 32.75 35.10 37.38 North & West Africa 73.39 81.17 88.14 94.46 100.60 Central & South Africa 20.96 23.88 26.11 27.98 29.80 Indian Sub-continent 151.10 169.79 188.89 202.44 215.60 Middle East 100.87 103.71 117.94 126.40 134.62 North Asia 1,122.82 1,221.53 1,382.74 1,481.92 1,578.28 South Asia 130.65 139.78 146.76 157.29 167.51 Australasia 9.78 10.12 10.20 10.93 11.64

Total 2,200.49 2,370.60 2,611.68 2,799 2,981 *Estimated

As shown in the table above, North Asia is considered the top consumer and producer of cement worldwide by around 1,521 million tons and 1,578 million tons,

Global Study on Cement, 2008.

8

respectively. In the second place, Western Europe comes with around 316 million tons as estimated consumption in 2008 and approximately 323 million tons as estimated cement production in 2008. Regarding Middle East, it is anticipated to consume roughly 145 million tons and produce 135 million tons in 2008. Such gap between consumption and production (10 million tons) in the Middle East region would be considered as export opportunities for Saudi cement companies.

3.2 International Trade Flows

The international trade flows show the imports and exports of cement among world regions. The tables below present the historical and projected imports and exports for the world regions.

Table 4 Imports (Million tons)

Regional totals 2004 2005 2006 2007* 2008*

North America 27.55 33.69 36.07 35.28 31.22 South America 1.16 1.36 0.97 0.95 0.84 Central America 0.91 1.49 1.52 1.49 1.32 Western Europe 30.45 32.24 35.23 34.46 30.49 Eastern Europe 3.45 4.88 5.11 5.00 4.42 Central Europe 5.57 5.81 5.44 5.32 4.71 North & West Africa 15.61 16.21 16.23 15.87 14.05 Central & South Africa 7.19 7.67 8.95 8.75 7.75 Indian Sub-continent 11.67 14.41 15.08 14.75 13.05 Middle East 19.51 21.61 24.28 23.75 21.01 North Asia 8.35 8.92 6.25 6.11 5.41 South Asia 10.72 10.88 11.61 11.35 10.05 Australasia 1.57 2.00 2.16 2.11 1.87

Total 143.71 161.17 168.90 165.18 146.18 *Estimated

As can be seen from the table above, North America is estimated to be the top importer of cement in 2008 of around 31.22 million tons, followed by Western Europe, which is expected to import about 30.5 million tons. In the third place, Middle East would come with around 21 million tons. Regarding North & West Africa, it is estimated to be the top fourth imported region with around 14 million tons. Based on the above, in addition of distance advantages, both North & West Africa and Middle East regions could be seen as promising markets for Saudi cement companies.

Table 5 Exports (Million tons)

Regional totals 2004 2005 2006 2007* 2008*

North America 7.20 7.71 8.94 8.58 8.18 South America 6.17 6.41 6.86 6.58 6.28 Central America 1.11 1.28 1.57 1.51 1.44

Global Study on Cement, 2008.

9

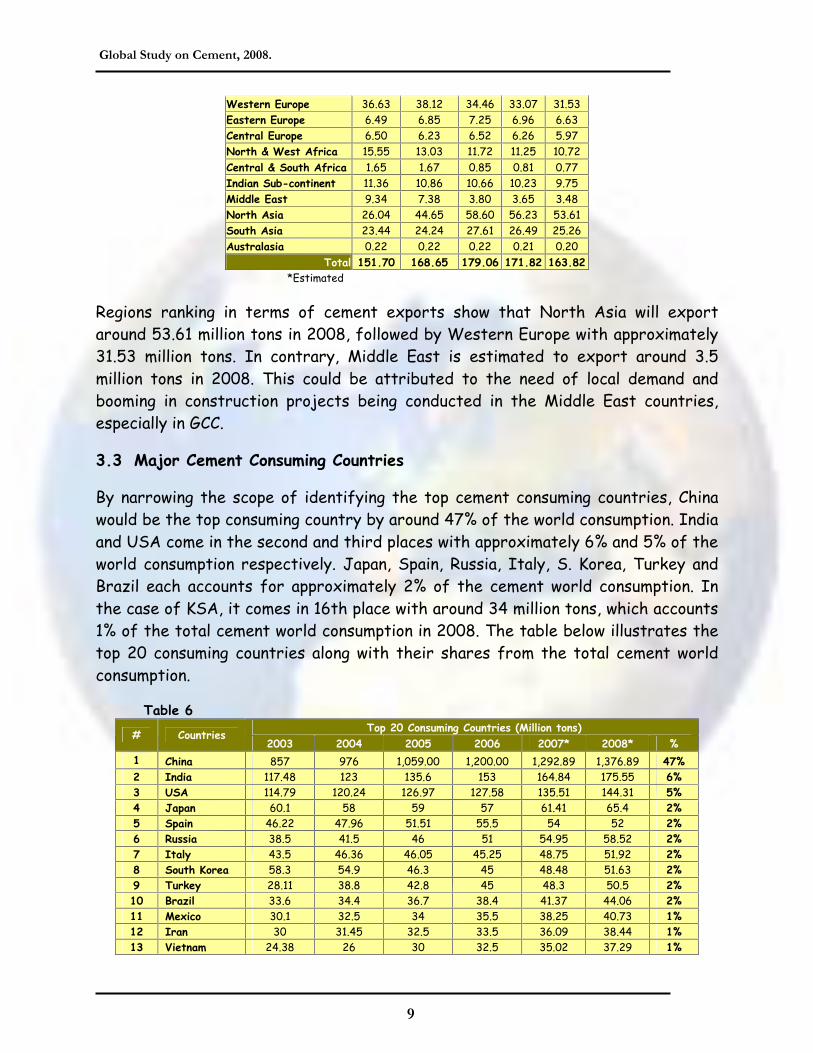

Western Europe 36.63 38.12 34.46 33.07 31.53 Eastern Europe 6.49 6.85 7.25 6.96 6.63 Central Europe 6.50 6.23 6.52 6.26 5.97 North & West Africa 15.55 13.03 11.72 11.25 10.72 Central & South Africa 1.65 1.67 0.85 0.81 0.77 Indian Sub-continent 11.36 10.86 10.66 10.23 9.75 Middle East 9.34 7.38 3.80 3.65 3.48 North Asia 26.04 44.65 58.60 56.23 53.61 South Asia 23.44 24.24 27.61 26.49 25.26 Australasia 0.22 0.22 0.22 0.21 0.20

Total 151.70 168.65 179.06 171.82 163.82 *Estimated

Regions ranking in terms of cement exports show that North Asia will export around 53.61 million tons in 2008, followed by Western Europe with approximately 31.53 million tons. In contrary, Middle East is estimated to export around 3.5 million tons in 2008. This could be attributed to the need of local demand and booming in construction projects being conducted in the Middle East countries, especially in GCC.

3.3 Major Cement Consuming Countries

By narrowing the scope of identifying the top cement consuming countries, China would be the top consuming country by around 47% of the world consumption. India and USA come in the second and third places with approximately 6% and 5% of the world consumption respectively. Japan, Spain, Russia, Italy, S. Korea, Turkey and Brazil each accounts for approximately 2% of the cement world consumption. In the case of KSA, it comes in 16th place with around 34 million tons, which accounts 1% of the total cement world consumption in 2008. The table below illustrates the top 20 consuming countries along with their shares from the total cement world consumption.

Table 6 Top 20 Consuming Countries (Million tons)

# Countries 2003 2004 2005 2006 2007* 2008* %

1 China 857 976 1,059.00 1,200.00 1,292.89 1,376.89 47% 2 India 117.48 123 135.6 153 164.84 175.55 6% 3 USA 114.79 120.24 126.97 127.58 135.51 144.31 5% 4 Japan 60.1 58 59 57 61.41 65.4 2% 5 Spain 46.22 47.96 51.51 55.5 54 52 2% 6 Russia 38.5 41.5 46 51 54.95 58.52 2% 7 Italy 43.5 46.36 46.05 45.25 48.75 51.92 2% 8 South Korea 58.3 54.9 46.3 45 48.48 51.63 2% 9 Turkey 28.11 38.8 42.8 45 48.3 50.5 2% 10 Brazil 33.6 34.4 36.7 38.4 41.37 44.06 2% 11 Mexico 30.1 32.5 34 35.5 38.25 40.73 1% 12 Iran 30 31.45 32.5 33.5 36.09 38.44 1% 13 Vietnam 24.38 26 30 32.5 35.02 37.29 1%

Global Study on Cement, 2008.

10

14 Indonesia 27.54 30.2 31.45 32.1 34.58 36.83 1% 15 Egypt 26.6 23.6 28.5 30.1 32.43 34.54 1% 16 Saudi Arabia 22.26 24.1 26.51 29.7 32 34.08 1% 17 Thailand 23.45 26.3 28.1 27.6 29.74 31.67 1% 18 Germany 29.03 29.02 26.93 27.4 29.52 31.44 1% 19 France 20.68 21.94 22.52 23.5 25.32 26.96 1% 20 Pakistan 12.3 12.52 14.79 16.87 18.18 19.36 1%

Others 367.75 387.78 418.36 451.80 493.37 531.88 18% Total 2,011.69 2,186.57 2,343.59 2,558.30 2,755 2,934 100%

*Estimated

3.4 Leading Cement and Clinker Exporters

By narrowing the scope of identifying the top cement exporters, China would be the top exporting country by around 20% of the world exports. Thailand and Japan come in the second and third places with approximately 8% and 6% of the world exports, respectively. In the fourth and fifth places, Turkey and India comes with around 8.9 and 8 million tons respectively. Egypt, Turkey, Taiwan and Indonesia each accounts for approximately 4% of the cement world exports. The table below illustrates the top 20 exporting countries along with their share from the total cement world exports.

Table 7 Top 20 Cement Exporters (Million tons)

# Countries 2003 2004 2005 2006 2007* 2008* %

1 China 5.22 6 22.15 35 33.59 32.02 20% 2 Thailand 12.2 11.24 13.8 14 13.43 12.81 8% 3 Japan 9.6 10.2 9.5 10.7 10.27 9.79 6% 4 Turkey 10.25 10.67 10.52 7.5 8.5 8.9 5% 5 India 8.89 10.06 9.19 8.8 8.44 8.05 5% 6 Egypt 7.4 12.4 9.5 7.5 7.2 6.86 4% 7 Taiwan 5 5.74 7 7 6.72 6.4 4% 8 Indonesia 7.3 7.62 5.01 6.7 6.43 6.13 4% 9 South Korea 3.14 4 5.9 5.8 5.57 5.31 3% 10 Germany 5.7 6.19 6.24 5.7 5.47 5.22 3% 11 Greece 4.35 4.89 5.7 5.5 5.28 5.03 3% 12 Canada 6.37 5.76 5.49 5.04 4.84 4.61 3% 13 Malaysia 2.54 3.02 2.84 4.39 3.7 3.7 2% 14 Belgium 2.2 3.06 3.15 3.3 3.17 3.02 2% 15 Italy 2.26 2.01 2.43 2.75 2.64 2.52 2% 16 Mexico 2.4 1.44 2.22 2.5 2.4 2.29 1% 17 Philippines 1.66 1.52 2.54 2.48 2.38 2.27 1% 18 Colombia 2.37 2.09 2.16 2.13 2.04 1.95 1% 19 Russia 2.3 2.1 2.1 2 1.92 1.83 1% 20 Ukraine 1.5 1.68 1.63 2 1.92 1.83 1%

Others 48.3 40.0 39.6 38.3 35.9 33 20% Total 150.95 151.69 168.64 179.05 171.82 163.81 100%

*Estimated

Global Study on Cement, 2008.

11

However, according to Comtrade Database, the statistics of top cement exporters reveals different ranking for top exporting countries. China is the top exporting country by around 19% of the world exports. Thailand and Japan came in the second and third places with approximately 7% of the world exports, for each. In the fourth place, Germany came with around 4.56 million tons (5%). India, Canada and South Korea each accounts for approximately 4% of the cement world exports. The table below illustrates the top 20 exporting countries, according to Comtrade Database, during years 2004 -2006 along with their share from the total cement world imports.

Table 8 Top 20 Cement Exporters (Million tons)

# Countries 2004 2005 2006 %

1 China 5.84 11.19 19.03 19%

2 Thailand 4.70 6.20 7.04 7%

3 Japan 5.34 6.09 6.82 7%

4 Germany 3.45 3.82 4.56 5%

5 India 2.83 3.95 4.04 4%

6 Canada 4.75 4.38 4.03 4%

7 South Korea 2.75 4.07 3.95 4%

8 Turkey 7.10 6.26 3.18 3%

9 Greece 2.63 3.34 2.77 3%

10 Russia 1.66 2.26 2.77 3%

11 Malaysia 1.76 2.65 3%

12 Egypt 1.50 1.66 2.46 2%

13 Saudi Arabia 1.32 1.62 2.28 2%

14 Mexico 1.44 2.22 2.11 2%

15 Italy 1.84 2.37 2.05 2%

16 Colombia 2.00 2.15 1.84 2%

17 Belgium 1.60 1.72 1.81 2%

18 Pakistan 0.72 1.90 1.81 2%

19 Indonesia 1.88 2.02 1.77 2%

20 Ukraine 1.35 1.39 1.36 1%

Others 24.48 26.35 20.86 21%

Total 80.94 94.98 99.19 100%

As can be seen from the two tables above, there is a clear discrepancy between the statistics of Global Cement Report and Comtrade Database. Such discrepancy could be attributed to the non-availability of trade statistics of some countries in the Comtrade Database. Hence, it is advised to stick to the Global Cement Report� statistics, as it cover most countries and contain credible information.

3.5 Leading Cement and Clinker Importers

By narrowing the scope of identifying the top cement importers, USA would be the top importing country by around 21% of the world imports. Spain and Bangladesh

Global Study on Cement, 2008.

12

come in the second and third places with approximately 6% and 5% of the world imports, respectively. In the fourth place, UAE comes with around 5.3 million tons (4%). Italy, Sir Lanka and Singapore each accounts for approximately 3% of the cement world imports. The table below illustrates the top 20 importing countries along with their share from the total cement world imports.

Table 9 Top 20 Cement Importers (Million tons)

# Countries 2003 2004 2005 2006 2007* 2008* %

1 USA 23.63 26.67 32.81 35.18 34.73 30.73 21% 2 Spain 8.15 8.84 10.72 11.5 10 9 6% 3 Bangladesh 6.4 5.54 7.5 8 7.82 6.92 5% 4 UAE 1 4.4 3.5 5.5 5.3 5.3 4% 5 Italy 4.5 5 5 4.9 4.79 4.24 3% 6 Sri Lanka 1.5 2.63 3.09 3.48 3.7 4.13 3% 7 Singapore 3.75 3.17 3.11 3.12 3.4 3.8 3% 8 Netherlands 3.1 3.77 3.74 3.85 3.77 3.33 2% 9 Vietnam 3.5 4.1 4.2 3.5 3.42 3.03 2% 10 Malaysia 1.2 1.29 1.46 2.27 3 3 2% 11 France 2.45 2.56 2.92 3.45 3.37 2.99 2% 12 Kuwait 0.3 1.4 1.84 2.13 2.43 2.8 2% 13 South Korea 1.87 3.6 3.4 3.2 3.13 2.77 2% 14 Iraq 2.3 3 3.3 2.5 2.8 2.5 2% 15 Ghana 2.18 2.1 2.2 2.25 2.4 2.4 2% 16 Syria - 1.24 1.66 2.26 2.31 2.23 2% 17 Turkey 0.01 - 0.25 2 2 2 1% 18 Afghanistan 1.4 1.6 2.05 2.3 2.25 1.99 1% 19 Kazakhstan 0.45 0.85 1.7 2.2 2.15 1.9 1% 20 Nigeria 0.2 7.4 7.72 8.33 2.67 0.5 0.3%

Others 58.6 54.55 59 56.98 59.75 50.62 35% Total 126.49 143.71 161.17 168.9 165.19 146.18 100%

*Estimated

However, according to Comtrade Database, the statistics of top cement importers reveals different ranking for top importing countries. USA is the top importing country by around 40% of the world imports. South Korea and Spain came in the second and third places with approximately 4% of the world imports, for each. In the fourth place, Singapore came with around 2.82 million tons (4%). Syria and Kazakhstan each accounts for approximately 3% of the cement world imports. The table below illustrates the top 20 importing countries, according to Comtrade Database, during years 2004 -2006 along with their share from the total cement world imports.

Global Study on Cement, 2008.

13

Table 10 Top 20 Cement Importers (Million tons)

# Countries 2004 2005 2006 %

1 USA 24.18 28.83 30.95 40%

2 South Korea 3.42 3.40 3.18 4%

3 Spain 2.33 2.68 2.90 4%

4 Singapore 2.94 2.83 2.82 4%

5 Syria 0.55 1.28 2.58 3%

6 Kazakhstan 0.98 1.66 2.46 3%

7 Netherlands 1.23 1.41 1.74 2%

8 Yemen 1.40 1.48 1.68 2%

9 Sudan 1.73 1.92 1.63 2%

10 Italy 2.09 1.99 1.45 2%

11 France 1.01 1.15 1.36 2%

12 Hong Kong 2.05 1.77 1.35 2%

13 Indonesia 0.06 1.01 1.20 2%

14 Qatar 0.55 1.43 1.18 2%

15 Albania 1.02 1.43 1.12 1%

16 Japan 0.82 0.91 1.05 1%

17 Germany 0.95 0.98 0.97 1%

18 Czech Rep. 0.89 0.85 0.90 1%

19 Belgium 0.87 0.70 0.81 1%

20 China 0.05 0.81 0.76 1%

Others 19.83 18.59 15.82 20%

Total 68.97 77.10 77.88 100%

As can be compared between the two tables above, there is a clear discrepancy between the statistics of Global Cement Report and Comtrade Database. Such discrepancy could be attributed to the non-availability of trade statistics of some countries in the Comtrade Database such as UAE, Iraq and Kuwait. Hence, it is advised to stick to the Global Cement Report� statistics, as it cover most countries and contain credible information.

3.6 Leading International Cement Companies

There are six leading cement companies in the world i.e. Buzzi Unicem, Holcim, Lafarge, Cemex, Heidelberg Cement. These companies have adopted strong expansion strategies such as acquiring or establish green field project to produce and distribute in several oversea countries. Furthermore, all of them have developed their exporting capabilities to ship and distribute cement in overall world. In general, the expansion strategies of theses companies can be summarized in the following points:-

Acquisition and establishment of cement factories in potential markets. Establishing trade cement companies to market and distribute the surplus

of cement production.

Global Study on Cement, 2008.

14

Investing in building and developing export terminals in sea ports� of targeted countries.

Froward integration toward establishing ready-mix and pre-cast factories.

The following lines will present a glance about each company and its installed capacities.

Buzzi Unicem is the market leader in Luxembourg and the second largest cement producer in Italy, Germany and the Ukraine as well as fifth largest in the United States. In 2005, Buzzi Unicem cement sales increased by one per cent to 32.2 million tons and group turnover rose by 6.5% to �2,941.4 million. Ready-mixed concrete deliveries were 2.7 per cent higher at 15.6 millions m3.

Holcim is market leader in cement in Latin America, North America, Switzerland, Slovakia and, through a joint venture, in Australia. It also enjoys strong market positions in Europe and in Asia. Holcim increased cement and clinker volume by 8.3% to 11 0.6 million tons in 2005, with ready-mixed concrete deliveries rising by 30.4% to 38.2 million m3. Group turnover advanced by 39.8 per cent to CHF 18,468 million (�11,914 million), cement and clinker representing 55.8 per cent, or CHF11, 361 million (�7,459 million).

Lafarge is market leader in cement in France, Great Britain, Greece, Austria, North America plus several developing markets. Group turnover rose by 10.6 % to �15,969 million tons in 2005, with the strongest growth being achieved in the Mediterranean area and in Latin America. Cement deliveries rose by 3.2 % to 123.2 million tons, with turnover from cement, including sales to other parts of the group, increasing by 12.3% to �8,314 millions. Moreover, in January, 2008, Lafarge acquired Orascom Construction Industries (�OCI�), which has cement plants in divergent countries such as Egypt, Algeria, Syria, Sudan and Pakistan.

Cemex is by far the leading cement producer in Mexico and is also market leader in Spain, Venezuela and in a number of Central American and Caribbean countries, plus Croatia and Latvia. The group is number two in Colombia and number three in the US and Great Britain.

Heidelberg Cement is market leader in Germany, The Netherlands, Belgium, Sweden, Norway, Estonia, Poland, the Czech Republic, Hungary, the Ukraine, and Bosnia as well as in a number of African markets.

Italcementi is group market leader in cement in Italy, Bulgaria and, since 2005, Egypt, number two in France and Morocco as well as number three in Belgium, Greece and Kazakhstan. Italcementi increased cement sales by 17 per cent to

Global Study on Cement, 2008.

15

56.3 million tons 2005, while group turnover advanced by 10.4 % to �4,999.6 million.

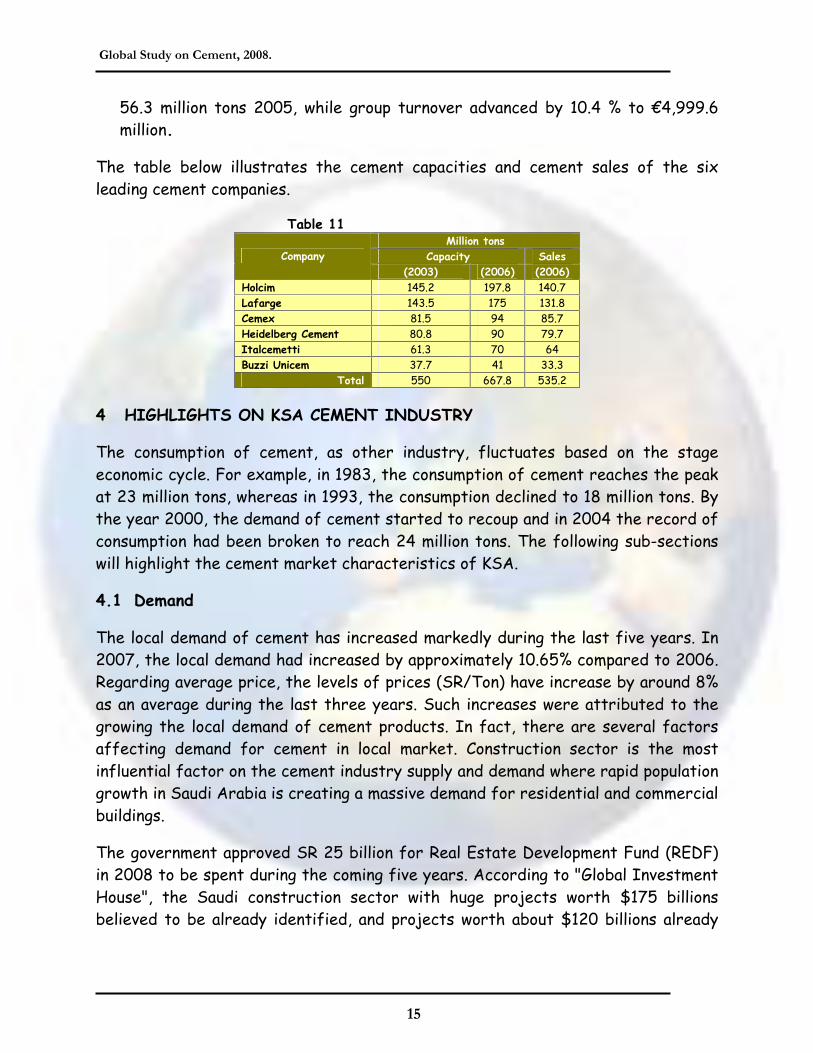

The table below illustrates the cement capacities and cement sales of the six leading cement companies.

Table 11 Million tons

Sales Capacity (2006) (2006) (2003)

Company

140.7 197.8 145.2 Holcim 131.8 175 143.5 Lafarge 85.7 94 81.5 Cemex 79.7 90 80.8 Heidelberg Cement 64 70 61.3 Italcemetti

33.3 41 37.7 Buzzi Unicem 535.2 667.8 550 Total

4 HIGHLIGHTS ON KSA CEMENT INDUSTRY

The consumption of cement, as other industry, fluctuates based on the stage economic cycle. For example, in 1983, the consumption of cement reaches the peak at 23 million tons, whereas in 1993, the consumption declined to 18 million tons. By the year 2000, the demand of cement started to recoup and in 2004 the record of consumption had been broken to reach 24 million tons. The following sub-sections will highlight the cement market characteristics of KSA.

4.1 Demand

The local demand of cement has increased markedly during the last five years. In 2007, the local demand had increased by approximately 10.65% compared to 2006. Regarding average price, the levels of prices (SR/Ton) have increase by around 8% as an average during the last three years. Such increases were attributed to the growing the local demand of cement products. In fact, there are several factors affecting demand for cement in local market. Construction sector is the most influential factor on the cement industry supply and demand where rapid population growth in Saudi Arabia is creating a massive demand for residential and commercial buildings.

The government approved SR 25 billion for Real Estate Development Fund (REDF) in 2008 to be spent during the coming five years. According to "Global Investment House", the Saudi construction sector with huge projects worth $175 billions believed to be already identified, and projects worth about $120 billions already

Global Study on Cement, 2008.

16

announced, in additional to about $27 billions for King Abdullah Economic City has, obviously, positive implications for the country's cement sector.

Moreover, the Ministry of Education is planning to build a total of 8,927 (5,035 and 3,892 for girls and boys respectively) of school and administrative buildings in the Kingdom during the current decade 1420 to 1430. The objective is to replace currently rented school buildings throughout the Kingdom. Moreover, current expansion projects of the two holy mosques in Makkah and Al Medina with an expected finishing period of 10-15 years. Another factor is related to Saudi Arabian General Investment Authority (SAGIA) where it is responsible for all the foreign and joint venture investment projects. The investment act covers four areas of investment; industry, agriculture, mining and service. It gives the foreign investors an attractive package of concession and facilities including free land, soft government loans, tax exemption, etc.

In addition, ARAMCO will introduce 4 huge projects for investment in Kharsaniah, Shaibah, Khrais and Al-Hawiah. The expected period to contract these projects is during 2006-2008. As for housing units, it is estimated that in the short run, there is demand for an additional 2 million housing units around the country, with over 600,000 in Riyadh alone (according to a study prepared by NCB); however, assuming Saudi population to reach 33.44 million by 2020 with a family size of 5.3 person, it is estimated that 2.32 million new housing units to be built in the Kingdom. Therefore, demand of cement is expected to increase in the next following years.

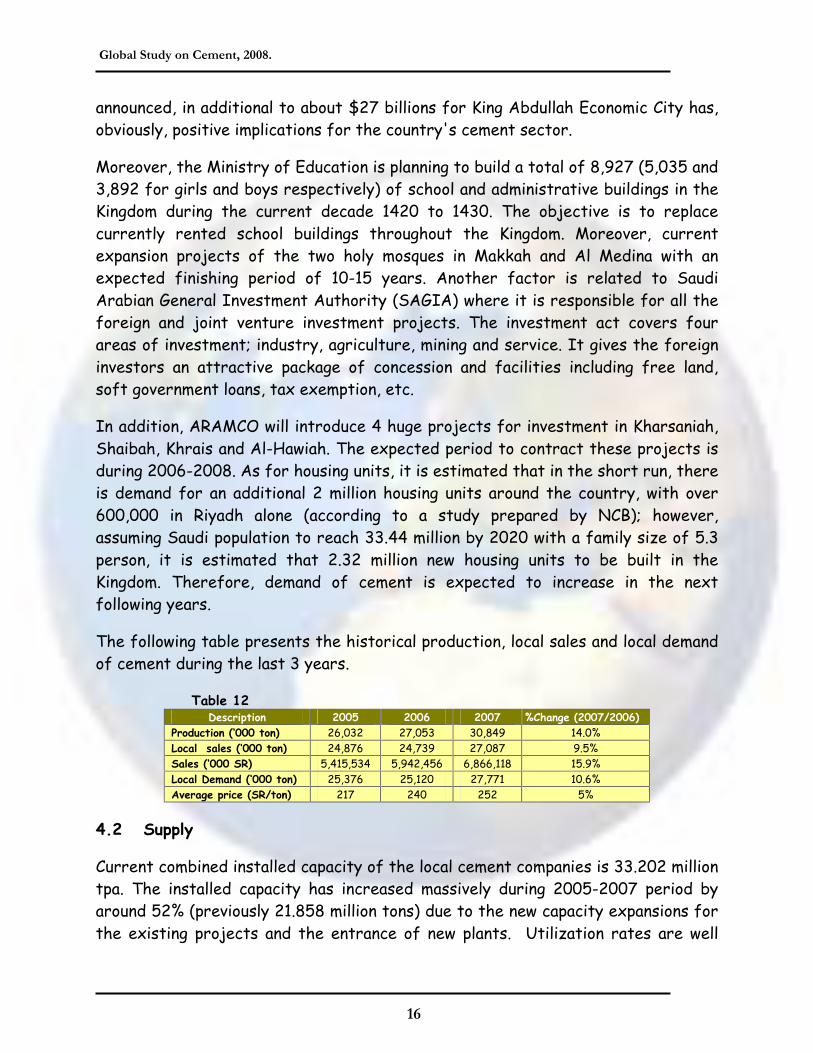

The following table presents the historical production, local sales and local demand of cement during the last 3 years.

Table 12 Description 2005 2006 2007 %Change (2007/2006)

Production (�000 ton) 26,032 27,053 30,849 14.0% Local sales (�000 ton) 24,876 24,739 27,087 9.5% Sales (�000 SR) 5,415,534 5,942,456 6,866,118 15.9% Local Demand (�000 ton) 25,376 25,120 27,771 10.6% Average price (SR/ton) 217 240 252 5%

4.2 Supply

Current combined installed capacity of the local cement companies is 33.202 million tpa. The installed capacity has increased massively during 2005-2007 period by around 52% (previously 21.858 million tons) due to the new capacity expansions for the existing projects and the entrance of new plants. Utilization rates are well

Global Study on Cement, 2008.

17

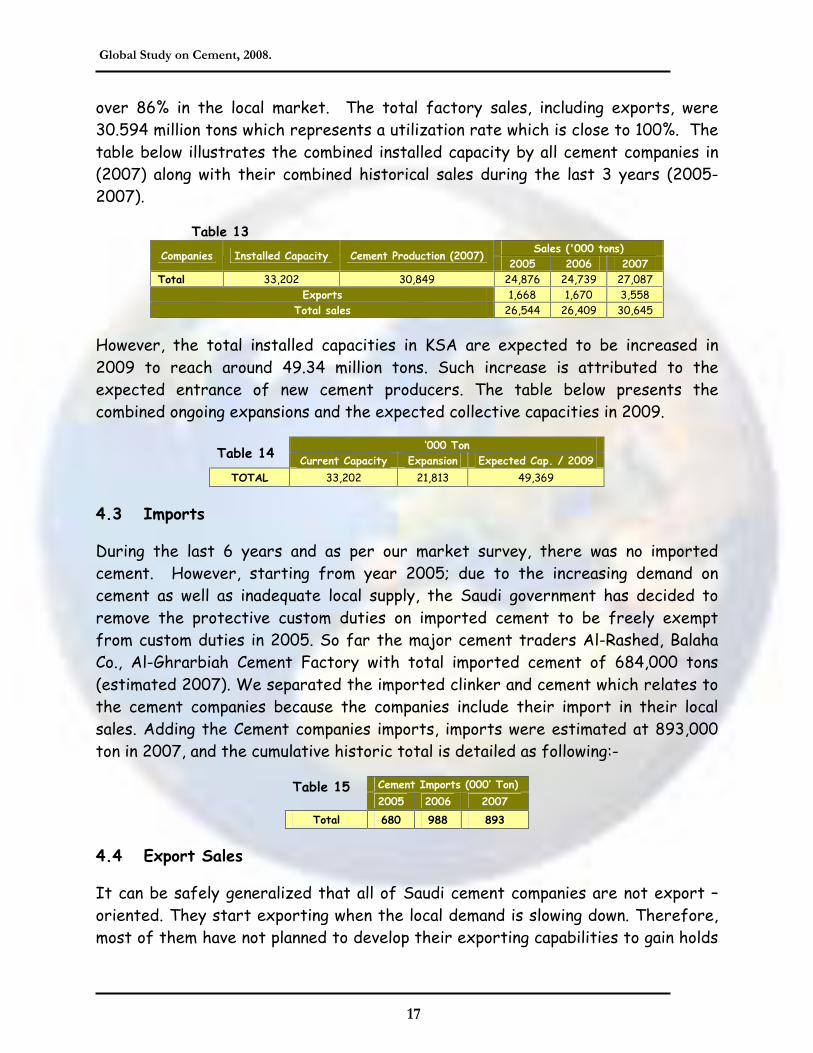

over 86% in the local market. The total factory sales, including exports, were 30.594 million tons which represents a utilization rate which is close to 100%. The table below illustrates the combined installed capacity by all cement companies in (2007) along with their combined historical sales during the last 3 years (2005-2007).

Table 13 Sales ('000 tons)

Companies Installed Capacity Cement Production (2007) 2005 2006 2007

Total 33,202 30,849 24,876 24,739 27,087 Exports 1,668 1,670 3,558

Total sales 26,544 26,409 30,645

However, the total installed capacities in KSA are expected to be increased in 2009 to reach around 49.34 million tons. Such increase is attributed to the expected entrance of new cement producers. The table below presents the combined ongoing expansions and the expected collective capacities in 2009.

�000 Ton Table 14

Current Capacity Expansion Expected Cap. / 2009

TOTAL 33,202 21,813 49,369

4.3 Imports

During the last 6 years and as per our market survey, there was no imported cement. However, starting from year 2005; due to the increasing demand on cement as well as inadequate local supply, the Saudi government has decided to remove the protective custom duties on imported cement to be freely exempt from custom duties in 2005. So far the major cement traders Al-Rashed, Balaha Co., Al-Ghrarbiah Cement Factory with total imported cement of 684,000 tons (estimated 2007). We separated the imported clinker and cement which relates to the cement companies because the companies include their import in their local sales. Adding the Cement companies imports, imports were estimated at 893,000 ton in 2007, and the cumulative historic total is detailed as following:-

Cement Imports (000� Ton) Table 15 2005 2006 2007

Total 680 988 893

4.4 Export Sales

It can be safely generalized that all of Saudi cement companies are not export �oriented. They start exporting when the local demand is slowing down. Therefore, most of them have not planned to develop their exporting capabilities to gain holds

Global Study on Cement, 2008.

18

in oversea markets. At that time, the experience of exporting was very modest and all transactions were priced at ex-factory. Gradually, some other cement companies have started exporting to some neighborhood markets i.e. some GCC states. The table below illustrates the combined exports sales of Saudi companies in 2007, broken down by export markets.

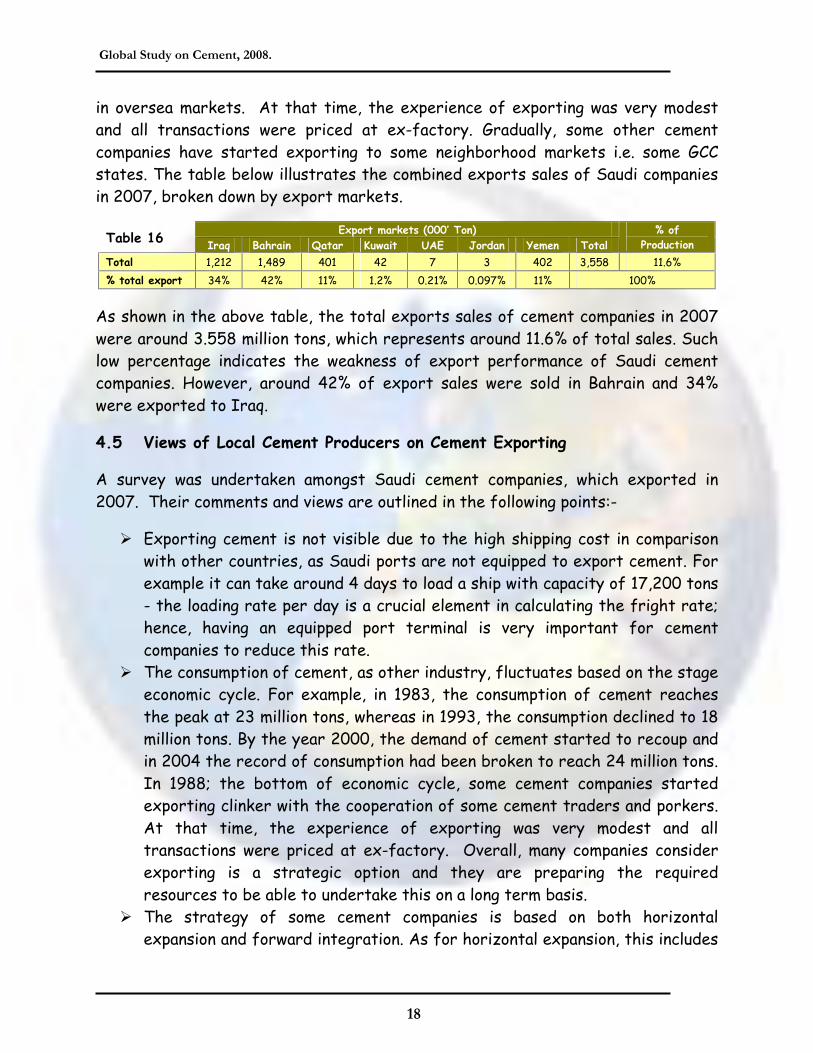

Export markets (000� Ton) Table 16

Iraq Bahrain Qatar Kuwait UAE Jordan Yemen Total % of

Production

Total 1,212 1,489 401 42 7 3 402 3,558 11.6%

% total export 34% 42% 11% 1.2% 0.21% 0.097% 11% 100%

As shown in the above table, the total exports sales of cement companies in 2007 were around 3.558 million tons, which represents around 11.6% of total sales. Such low percentage indicates the weakness of export performance of Saudi cement companies. However, around 42% of export sales were sold in Bahrain and 34% were exported to Iraq.

4.5 Views of Local Cement Producers on Cement Exporting

A survey was undertaken amongst Saudi cement companies, which exported in 2007. Their comments and views are outlined in the following points:-

Exporting cement is not visible due to the high shipping cost in comparison with other countries, as Saudi ports are not equipped to export cement. For example it can take around 4 days to load a ship with capacity of 17,200 tons - the loading rate per day is a crucial element in calculating the fright rate; hence, having an equipped port terminal is very important for cement companies to reduce this rate.

The consumption of cement, as other industry, fluctuates based on the stage economic cycle. For example, in 1983, the consumption of cement reaches the peak at 23 million tons, whereas in 1993, the consumption declined to 18 million tons. By the year 2000, the demand of cement started to recoup and in 2004 the record of consumption had been broken to reach 24 million tons. In 1988; the bottom of economic cycle, some cement companies started exporting clinker with the cooperation of some cement traders and porkers. At that time, the experience of exporting was very modest and all transactions were priced at ex-factory. Overall, many companies consider exporting is a strategic option and they are preparing the required resources to be able to undertake this on a long term basis.

The strategy of some cement companies is based on both horizontal expansion and forward integration. As for horizontal expansion, this includes

Global Study on Cement, 2008.

19

developing plans to develop new cement types, such as plastering cement in order to meet customer requirements. In terms of forward integration, some companies are considering entering the ready-mix sector, etc.

Some companies have no real plans to export but are concentration more on developing their local market.

4.6 Advantage/Disadvantage of Exporting

Advantages

Improvement of the overall utilization rates. Hence, more volume are sold. When prices of cement in the export market are higher than the home market, profitability will improve.

Maintaining presence in the export market should help reducing total dependence on home market.

Gaining reputation of quality products among other competing brands in those exported markets. This can only be obtained if quality standards are achieved.

Disadvantages

Being a home industry, cement shipping costs reduces profitability, particularly when there is a gap between local market prices and prices in targeted market higher than the shipping costs.

The longer the distance that cement shipped to can cause shortages of the product shelf life. Hence, this may negatively affect the quality of cement being exported to a distance area.

A clear disadvantage, where transportation is required, particularly for those cement companies located in distance from coastal areas. Coastal areas are those equipped with suitable terminals for exporting cement.

Cement is considered a heavy product, which would require large fleet/ships for transporting to export market. In this case, time of delivery could be a major disadvantage of exporting cement.

4.7 Exporting Capability & Requirements of Exporters

As implied earlier, the exports capabilities of Saudi Cement companies are very modest and needs to be developed to enhance the export performance of these companies. Hence, there is a solid concurrence among existing cement exporters about attributing the low of exporting cement to several points as follows:

Global Study on Cement, 2008.

20

The non- readiness of exports infrastructure in terms of railways and sea ports (exporting terminals).

The increase of ports fees for cement products. The fees of packed cement are SR22/Ton, whereas the fees of bulk cement is SR4/Ton.

Regarding the fees of exported cement, Saudi Cement companies suggest to eliminate any export fees in order to provide incentives for cement companies to start exporting.

5 POTENTIAL CEMENT EXPORT MARKETS

In this section, screening has been conducted on the top worldwide cement importers to identify export markets for Saudi cement companies. This screening had been conducted based on three criteria i.e. market demand, transportation distances from KSA and previous experiences of Saudi cement companies in those markets. The results of this screening come up with 10 potential export markets. In the following section, glances of local market for each targeted country will be provided.

5.2 Potential Markets for Saudi Cement Companies

The most potential export markets identified for Saudi cement companies are Iraq, Spain, Malaysia, Ghana, Kuwait, Syria, UAE, Sir Lanka, Singapore, and Turkey. For each country, information about market overview, existing players and landed prices are discussed in the following sub-sections.

5.2.1 Spain

Market Overview

Cement consumption in Spain rose, by 7.4 % from 47.97 million tons in 2000 to 51.51 million tons in 2005 and is estimated to end 2007 around 54 million tons , representing 7.6% expansion. The country remains the largest cement market in Europe and the per capita consumption has reached a new record of 1229kg.The strongest growth in cement consumption was seen in central Spain, which includes Madrid and Castilla-La Mancha, with an increase of 23.2%. Catalonia was in second place with an increase of 7.3%, followed by Castilla y Leon. Valencia and the Can-tabria area were the only regions of show declining cement consumption, in each case by around 0.2 %. In terms of overall consumption, Andalusia is the largest cement market in Spain and accounted for 20.3% of consumption in 2005, followed by Catalonia with 13.4%, the greater Madrid market with 11.7% and Valenciana with

Global Study on Cement, 2008.

21

11.3%. Between them, the four biggest markets represented 56.6% of the total Spanish cement consumption.

Bulk cement increased its share of market to 82% in 2005 compared with 81% two years earlier. The civil engineering industry accounted for 45% of cement consumption. Road projects and ports accounted for 24% and 22%, respectively. Building represented 55% of cement consumption, with house building accounting for 69% of this, commercial and industrial buildings for 20% and repair & maintains for 11%.

Local Production

There are now nine major cement producers left in Spain that have a production capacity of at least 1.5million tons, eight of which produce clinker, in addition to which there are a number of independent grinding stations. The nine leading producers control a combined cement capacity of 47.3 million tons at 43 plants.

There are now a number of independent grinding centers, following in the footsteps of the Valencia-based Cementos La Union, most of which have been established within the past six to eight years, and include cement producers such as Orascom and Nuh Cementos among their shareholders. The top three cement producers, Cementos Portland, Cemex and Holcim , between them account for roughly 50% of the Spanish cement consumption. The table below illustrates the 9 local cement manufacturers along with their capacities.

Table 17 Company (Million tons) Number of Plants

Cementos Portland 12.8 9 Cemex (Spanish) 11.2 10 Holcim (Spanish) 5.8 6 Lafarge Asland 5.2 4 Cimpor 3.8 6 Financieria Minera (Italcementi) 2.8 3 Tudela Veguin 2.6 3 Cementos Molins 1.6 1 Cementos Especiales de las 1.5 1

Trade

Exports were essentially and declined by 4.9 % in 2005 to 1.45 million tons. Cement produced in Spain is exported to the United States, France, Great Britain and Ireland and, in the case of white cement, to a wide range of countries, notably further to Africa.

Global Study on Cement, 2008.

22

Cemex Espana is the leading exporter of white cement, while the majority of the grey cement exports originate in the northeast of the country. Uniland has recently occupied the top slot in terms of exports, but with the change of ownership, some of the export business is likely to be shifted to the ports on the Bay of Biscay which is further removed from the main domestic markets. Imports of cement and clinker rose by 21.3 % in 2005 to a new record of 10.72 million tons.

The increase of 2.8 million tons, came from within the European Union, mainly from Portugal (1.14 million tons), Italy (O.7 million tons) and Greece (0.63 million tons), with both Italy and Greece more than doubling their shipments, while supplies from Portugal declined by 18.5%. China, which supplied less than 1000 tons in 2004, suddenly became the biggest source of imports in 2005, with deliveries of 2.45 million tons. Shipments from Egypt, which had reached 3.47 million tons in 2004, declined by 33.2 % in 2006 to 2.32 million tons. Turkey supplied 1.42 million tons, an increase of 11.7 % and Russia provided 13.2 % more at 0.82 million tons. Imports from India declined for the second year in a row and emerged 11.8 % lower at 0.28 million tons. These eight countries represented 90.4 % of the total imports in 2005, with France, Germany, Morocco and Tunisia each supplying between 0.1-0.2 million tons that year. Regarding Clinker, Spain imports are around 7.4 million tons by the end of 2005 and came from China, Egypt, India, Morocco and Croatia, while the main sources of cement were Russia, Italy, Turkey and Greece.

Prices

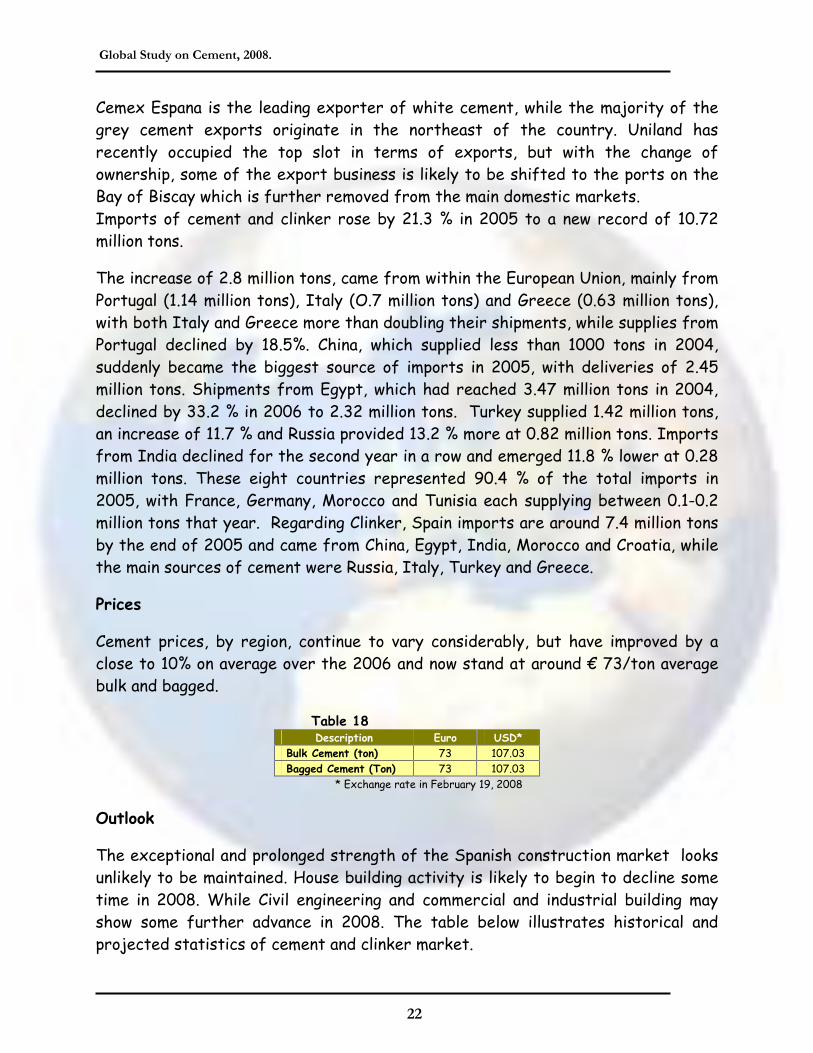

Cement prices, by region, continue to vary considerably, but have improved by a close to 10% on average over the 2006 and now stand at around � 73/ton average bulk and bagged.

Table 18 Description Euro USD*

Bulk Cement (ton) 73 107.03 Bagged Cement (Ton) 73 107.03

* Exchange rate in February 19, 2008

Outlook

The exceptional and prolonged strength of the Spanish construction market looks unlikely to be maintained. House building activity is likely to begin to decline some time in 2008. While Civil engineering and commercial and industrial building may show some further advance in 2008. The table below illustrates historical and projected statistics of cement and clinker market.

Global Study on Cement, 2008.

23

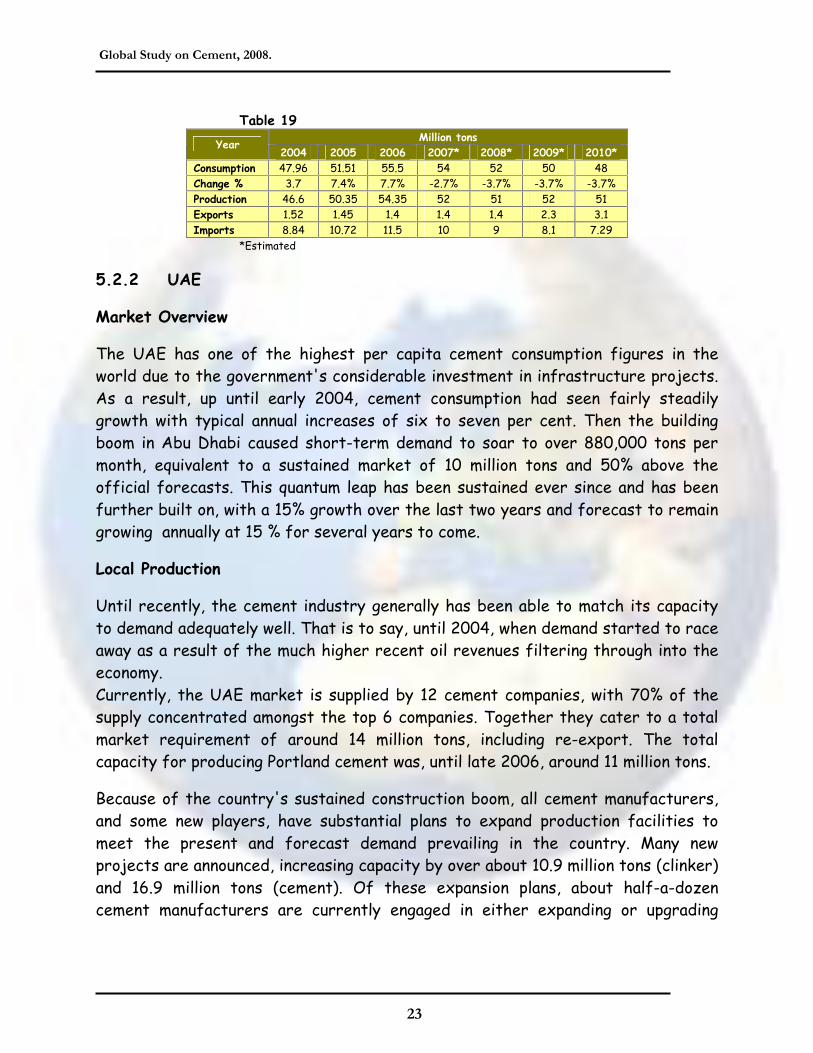

Table 19 Million tons

Year 2004 2005 2006 2007* 2008* 2009* 2010*

Consumption 47.96 51.51 55.5 54 52 50 48 Change % 3.7 7.4% 7.7% -2.7% -3.7% -3.7% -3.7% Production 46.6 50.35 54.35 52 51 52 51 Exports 1.52 1.45 1.4 1.4 1.4 2.3 3.1 Imports 8.84 10.72 11.5 10 9 8.1 7.29

*Estimated

5.2.2 UAE

Market Overview

The UAE has one of the highest per capita cement consumption figures in the world due to the government's considerable investment in infrastructure projects. As a result, up until early 2004, cement consumption had seen fairly steadily growth with typical annual increases of six to seven per cent. Then the building boom in Abu Dhabi caused short-term demand to soar to over 880,000 tons per month, equivalent to a sustained market of 10 million tons and 50% above the official forecasts. This quantum leap has been sustained ever since and has been further built on, with a 15% growth over the last two years and forecast to remain growing annually at 15 % for several years to come.

Local Production

Until recently, the cement industry generally has been able to match its capacity to demand adequately well. That is to say, until 2004, when demand started to race away as a result of the much higher recent oil revenues filtering through into the economy. Currently, the UAE market is supplied by 12 cement companies, with 70% of the supply concentrated amongst the top 6 companies. Together they cater to a total market requirement of around 14 million tons, including re-export. The total capacity for producing Portland cement was, until late 2006, around 11 million tons.

Because of the country's sustained construction boom, all cement manufacturers, and some new players, have substantial plans to expand production facilities to meet the present and forecast demand prevailing in the country. Many new projects are announced, increasing capacity by over about 10.9 million tons (clinker) and 16.9 million tons (cement). Of these expansion plans, about half-a-dozen cement manufacturers are currently engaged in either expanding or upgrading

Global Study on Cement, 2008.

24

their plants, adding approximately 6 million tons of clinker and 9 million tons of cement with an investment of over US$ 1 billion, all by the end of 2006.

Projects include Al Ruya Industry's 3.6 million tons new plant in the Hamriya Free Zone by 2008 and Gulf Cement, which has a 7500 ton/day clinker line (2.5 million tons cement) due on-line by the end of 2007, in line with the company�s announcement in December 2004. In addition, National Cement Factory (NCF) has 2 million tons came in the first quarter of 2007. Hakim took a 25% interest in the company in February 2006 and will manage the plant.

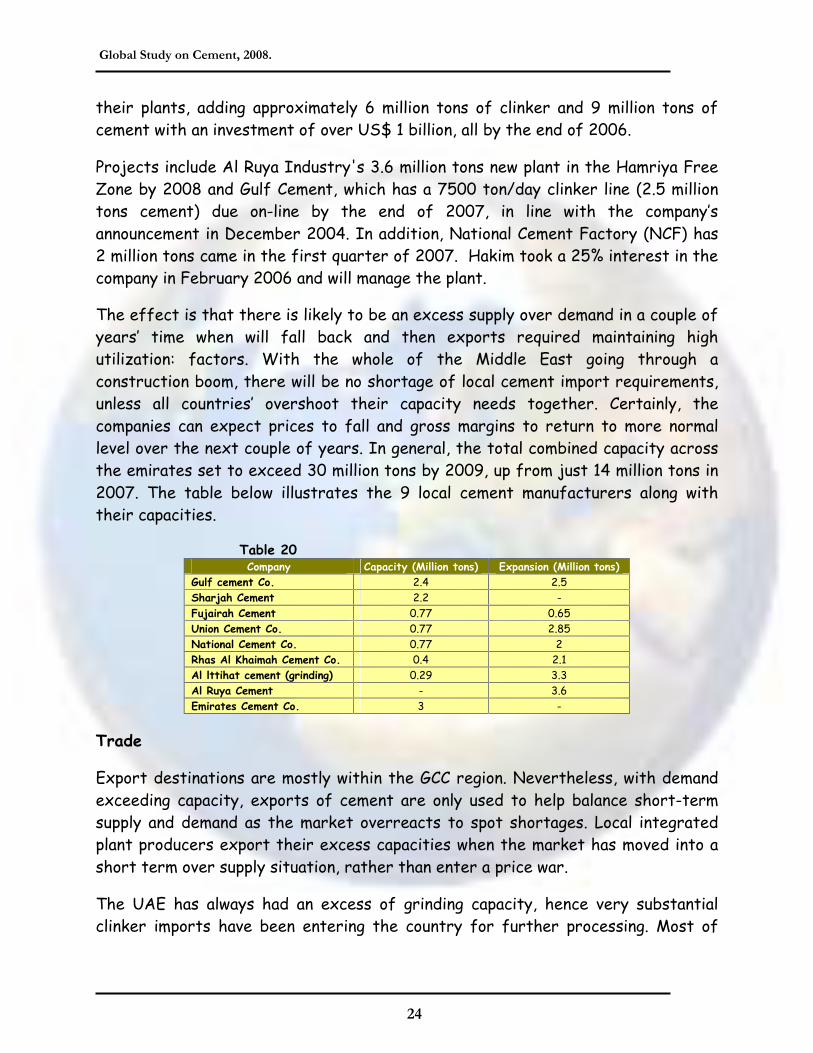

The effect is that there is likely to be an excess supply over demand in a couple of years� time when will fall back and then exports required maintaining high utilization: factors. With the whole of the Middle East going through a construction boom, there will be no shortage of local cement import requirements, unless all countries� overshoot their capacity needs together. Certainly, the companies can expect prices to fall and gross margins to return to more normal level over the next couple of years. In general, the total combined capacity across the emirates set to exceed 30 million tons by 2009, up from just 14 million tons in 2007. The table below illustrates the 9 local cement manufacturers along with their capacities.

Table 20 Company Capacity (Million tons) Expansion (Million tons)

Gulf cement Co. 2.4 2.5 Sharjah Cement 2.2 - Fujairah Cement 0.77 0.65 Union Cement Co. 0.77 2.85 National Cement Co. 0.77 2 Rhas Al Khaimah Cement Co. 0.4 2.1 Al lttihat cement (grinding) 0.29 3.3 Al Ruya Cement - 3.6 Emirates Cement Co. 3 -

Trade

Export destinations are mostly within the GCC region. Nevertheless, with demand exceeding capacity, exports of cement are only used to help balance short-term supply and demand as the market overreacts to spot shortages. Local integrated plant producers export their excess capacities when the market has moved into a short term over supply situation, rather than enter a price war.

The UAE has always had an excess of grinding capacity, hence very substantial clinker imports have been entering the country for further processing. Most of

Global Study on Cement, 2008.

25

this grinding capacity is in the Ras Al Khaimah port district. Up to1.8 million tons have been imported recently, mainly from Iran, Pakistan, India and the Philippines.

Prices

Prices were around US$87 in June 2006, but they have proved to be very volatile in the present situation of high market growth rates and as new capacity come on-line. Only a month before, in May 2006, spot prices leapt 200 per cent to U5$150/ton as supplies fell short. But, because of this shortage, panic or entrepreneurial importing has led to a low price in October 2006 that has led to a major share price fall as the industry tried to push through fuel based price rises that government resisted - all within five months of a high.

As new lines come on line, the typical median prices are likely to fall back to the mid U5$60s and if capacity gets seriously out of line, then a price war could break out. In a few years time, when the Middle Eastern countries scale back their investment plans, there is likely to be a large excess capacity that may hang around and mimic the scenarios of long standing excess capacities of over 50% in Thailand and Japan have had in the past, prompting the need to find large export markets in order to survive.

Outlook

After over two years of sustained growth, per capita cement consumption in the UAE has doubled to 3000kg, no doubt one of the highest in the world, reflecting the government's continuing investment in the country's infrastructure. This level would not normally be sustainable, but with huge increases in oil and gas revenues that are likely to remain historically very high for the foreseeable future, the economy is likely to continue to grow at over five per cent annually for many years to come.

With 13 player in the market and new ones joining in, there maybe some price wars once capacity exceeds demand, or at least when the clinker capacity exceeds demand. When this occurs, some consolidation is likely and the multinational could well move in to help rationalize capacity within the region through better marrying of group capacity utilization and local cross border trade.

The new planned additional capacity of 10.9 million tons of clinker and 16 million tons of cement, tabled in response to the recent shortage would seem to be a recipe for disaster since this would represent a per capita consumption 4600kg of

Global Study on Cement, 2008.

26

clinker or 8000 kg of cement. The table below illustrates historical and projected statistics of cement market.

Table 21 Million tons

Year 2004 2005 2006 2007* 2008* 2009* 2010*

Consumption 10.2 11.56 13.3 15.3 17.6 20.2 23.3 Change % 48.8% 13% 15% 15% 15% 15% 15% Production 9.8 10.3 12.9 14.8 17 30 30 Exports 0.4 0.8 0 0.8 0.8 10.3 7.2 Imports 4.4 3.5 5.5 5.3 5.3 0.5 0.5

*Estimated

5.2.3 Sir Lanka

Market Overview

Cement consumption in Sir Lanka has shown consistent growth each year over the last 5 years, growing at compound annual growth rate of 8.2% between 2001 and 2006. In 2006, demand remained strong with double �digit growth in excess of 10% for the second year in a row and overall consumption recorded at 4.05 million tons. Per capita consumption has been rising quickly and now stands at 204kg, though this level is still below the global average. Nevertheless the cement market is in good shape, and a positive growth trajectory supported by consistent demand from small homebuilders using cement for renovations and extensions. The rise in per capita income levels and strong growth in the property sector makes homebuilders the main driver for cement consumption. Over 100,000 housing units are being added annually and it is estimated that there is a shortage of around 400,000 housing units, a situation made worse by the tsunami disaster. Tax incentives and the increased availability of housing finance have raised demand for housing, but land scarcity (especially in urban areas) and the difficulty of obtaining clear title deeds remain constraints, limiting market growth.

Sri Lanka continues to see a high and increasing level of Gross Fixed Investment (GFI). As a percentage of GDP, GFI continues to rise and stood at an estimated 28.2 % in 2006, up from 26.4% in 2005. GFI is estimated to increase to 28.9 % in 2007, equivalent of US$9.0bn (at current market prices).

Local Production

There are six primary suppliers of cement in Sri Lanka, though only two - Hokim Lanka Ltd and Tokyo Cement - operate production facilities. Hokim (Lanka) Ltd operates the islands only integrated cement plant at Puttalam in the west of the

Global Study on Cement, 2008.

27

country, where capacity was upgraded to 1 million tons in 2005. The company also operates the 0.425 million tons Ruhunu grinding facility located in Galle, in the south of Sri Lanka, and also owns a bulk import terminal and packing plant at Galle port. The company has seen its market share declined from 34% in 2001 to 27% in 2006, when total sales reached 1.l million tons. Hokim (Lanka) Ltd generated annual revenues of approximately 102 millions USD in 2006.

However, the competitive landscape is changing in Sri Lanka following Holcim Group�s 2006 acquisition of Gujarat Ambuja Cements (GAC) in India. Holcim (Lanka) Ltd will see its combined market share boosted by around nine per cent to 35.5 per cent. Management of GAC�s Sri Lankan subsidiary, Ambuja Cement, will be merged with Holcim, and it is likely that Holcim will opt to merge brands in line with its historical corporate policy.

While Hokim is the dominant force in the Western Province where consumption is the highest, Holcim has been unable to penetrate the north of the island where Tokyo Cement is dominant. In the past the company has considered relocating its Galle packing facilities to Trincomalee in the north of Sri Lanka in order to extend coverage to the north east of the island from which it is effectively excluded at present, but this move seems to have been hampered by the difficult political environment and lack of government approval.

Tokyo Cement Co (Lanka) is a joint venture between Mitsui Mining Ltd, Japan and the privately held St. Anthony�s Consolidated Ltd, Sri Lanka, each of whom hold a 27.5% stake in the company. The company operates a dedicated grinding plant at Trincomalee in northeast Sri Lanka, with a cement capacity of 0.9 million tons, and import operations via its subsidiary, Tokyo Cement Colombo Terminal (Pvt) Ltd, located in Colombo port. Tokyo Cement is able to supply 1.5 million tons cement to the market annually. The company is currently upgrading its grinding operations with an investment of approximately US$12.9 million and including the installation of a new 1l0 tph Vertical Roller Mill. The new mill, which came online in March 2007, would increase annual capacity by 1 million tons, bringing total supply capabilities to 2.5 million tons. Tokyo Cement was the leading cement company in terms of sales volume in 2006 with annual sales reaching a record l.2 million tons, raising market share by half a per cent to 29.5%. Since 2001, the company has increased its market share from 19 %, partly at the expense of its competitors but also due to the doubling of demand in the North-Eastern province which the company successfully captured.

Global Study on Cement, 2008.

28

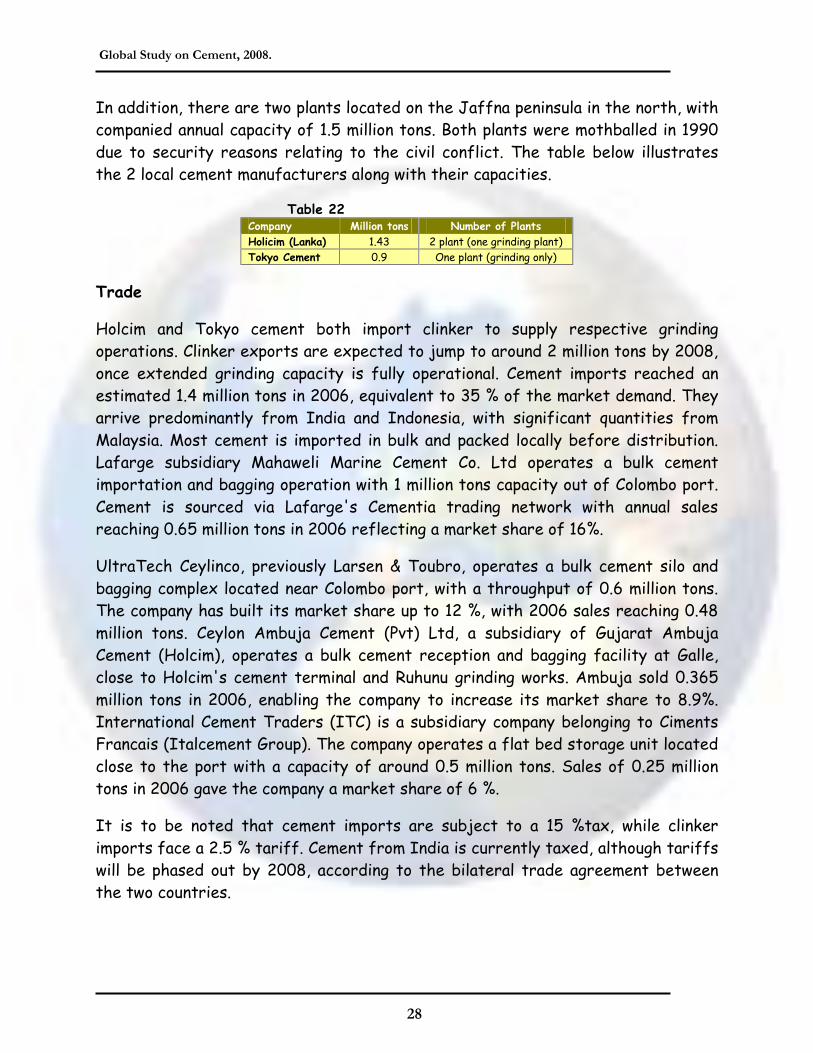

In addition, there are two plants located on the Jaffna peninsula in the north, with companied annual capacity of 1.5 million tons. Both plants were mothballed in 1990 due to security reasons relating to the civil conflict. The table below illustrates the 2 local cement manufacturers along with their capacities.

Table 22 Company Million tons Number of Plants Holicim (Lanka) 1.43 2 plant (one grinding plant) Tokyo Cement 0.9 One plant (grinding only)

Trade