externalities and market failure

TRANSCRIPT

Russell Kueh

Market Failure

When the two FTWE hold, role of public sector relegated to that of providing the institutional and legal framework for market operations and possibly to redistributing income.

Otherwise, a prima facie case for non-market mechanisms that permit Pareto improvements might be given.

Fundamental market failures: (1) non-competitive behaviour (2) externalities resulting from a lack of property rights (3) externalities resulting from jointness in consumption and production including public goods [and (4) informational externalities, discussed later in the course].

(1) violates perfect competition assumption; (2), (3) and (4) violate market completeness assumption.

(1) non-competitive behaviour

Important assumption underlying fundamental theorems: agents are price-takers.

In many case, there are sufficiently few agents on one side of the market that they recognise their influence over market price.

Suppose there is a single seller of good x1 (Alice) facing many price-taking buyers of x1 (Bobs) who sell x2. In an exchange economy, each agent is a buyer and seller so Alice has monopoly power in selling x1 and monopsony power in purchasing x2. She realises she can alter the relative price of the two goods in her favour i.e. realising a higher level of utility than she received at (Pareto) competitive equilibrium. The new equilibrium would not be Pareto optimal in general.

In diagram below, it is shown that Alice recognises her ability to set price and thus to attain any point on Bobs’ offer curve of OCb. Thus she maximises w.r.t. OCb, as shown by the tangency between it and her highest possible IC, u2

a.

While Alice is better off, the Bobs are worse off and the resulting allocation non-Pareto efficient. All results apply to the production economy and more sophisticated instances of market power.

Russell Kueh

(2) Externalities arising from a lack of property rights

B&B

For market mechanism to work ⇒ firms and HHs must be able to exchange claims on the right to (not) use a (unwanted) factor or (not) consume a (unwanted) commodity ⇒ a well-defined system of property rights that restrict agents’ behaviour accordingly.

For many goods and factors, it’s prohibitively costly or even infeasible to assign or enforce property rights – such items are ‘common property’, where some agents can free ride and enjoy the fruit of others’ labour and/or expense, or impose negative effects (e.g. pollution) on them.

Classic case of a common property externality in fishery. When a fisherman increase his catch, reduces equilibrium fish stock and raises others’ cost of finding a fish. Such cost is ignored since it’s external to the fisherman. In other words, private agents optimise consumption where MPC = MPB, while efficiency requires MSB (=MPB) = MSC. Result: overfishing, leaving too small a stock of fish than is socially desirable.

Russell Kueh

Lecture: The Bilateral Externality Model between a consumer and firm

Policy responses

• Facilitate Bargaining (Coase Theorem) • Quotas (Centralised) • Pigouvian Taxes (Centralised)

Russell Kueh

Analysis of Bargaining using the above case

Coase Theorem: If externality can be traded, then bargaining lead to an efficient outcome regardless of property right distribution.

The outcome above is identical due to the analytical form of the firm and consumer utility functions (i.e. quasi-linear). But the method of evaluating outcomes in case of other utility functions stays the same.

However, while the allocation of right does not affect efficiency of outcomes, it does affect wealth distribution (as shown by the different constant term in the consumer utility for each of the setups above)

Quotas

Assume the government knows the parameters of the cost and benefit functions and thus the efficient level of pollution, ho.

It can then limit the level of h to be at most ho.

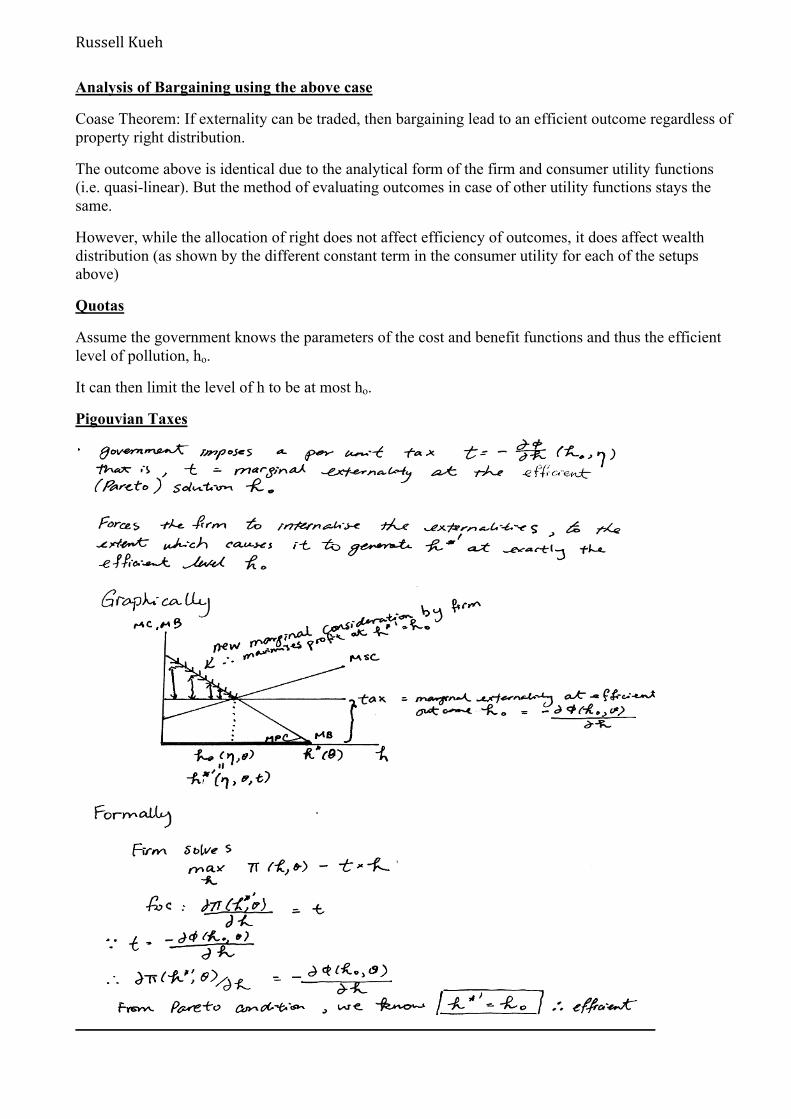

Pigouvian Taxes

Russell Kueh

Thus, with perfect information, price and quantity instruments are equally effective.

(3) Externalities arising from jointness in production and consumption; Public goods

Jointness of consumption means that a consumption activity undertaken by one household affects the utility of one or more other households, or that one firm’s activity affects the production possibilities of one or more other firms.

May occur among HHs, among producers, or between producers and HHs.

This is the general case, of which the above pollution problem is a specific example.

The 1st FTWE will generally fail in the presence of jointness of consumption or production externalities, because decantralised HHs and firms in competitive economy will not take into account of the external benefits or costs of their actions when making decisions.

Put differently, the conditions for Pareto optimality will differ when external effects are present from the conditions achieved in competitive equilibrium, which therefore fails to achieve Pareto optimality.

Public Good

Private good is a commodity for which use of a unit by one agent precludes entirely the use of that unit by other agents. It is thus rival.

Pure public good is a commodity for which use of a unit by one agent has no effect on the use of that unit by other agents. It is non-rival (non-depletable)

Mixed is where the use of one reduces the amount of that unit available for others. E.g. park, road.

All private goods are excludable. Pure public goods may or may not be excludable (scrambling TV signals).

This is why market fails in such case: even if pure public goods are excludable, it would be Pareto inefficient to do so as allowing one other agent to consume the public makes him/her better off while leaving others at least as well off. That is, since marginal costs of an extra user is zero, it is not optimal to set prices that will exclude anyone who derives marginal utility from the public good. But if exclusion is not possible, the free rider problem is present, with HHs concealing their preferences. Consequently, too little, if any, of the public good is provided.

Russell Kueh

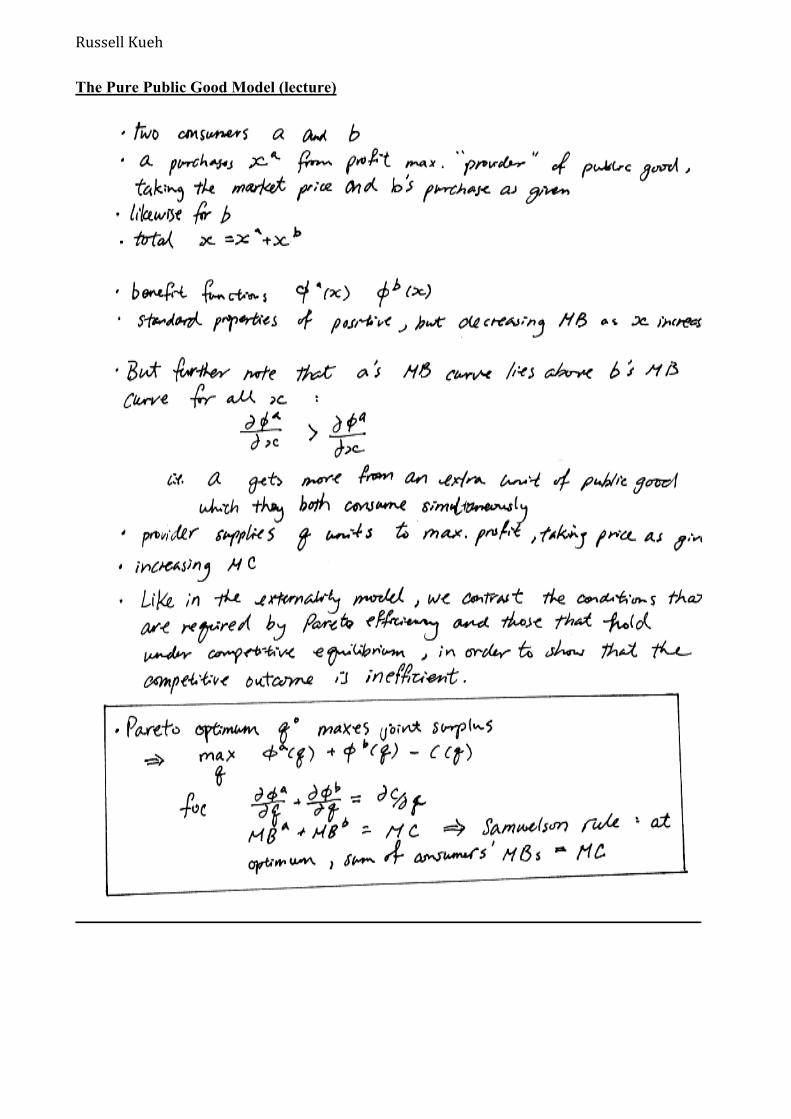

The Pure Public Good Model (lecture)

Russell Kueh

Russell Kueh

Policy responses

• Direct provision (quantity instrument) • Pigouvian Subsidies (price instrument) • Facilitating personalised markets

Direct provision and subsidies are the opposite case to that of quota and taxes: the quantity instrument is to provide q0 directly, while the price instrument is to provide a unit subsidy equivalent to the marginal externality at the Pareto efficient quantity, q0 i.e. MBb at q0.

Russell Kueh

Russell Kueh

Facilitating personalised markets

Russell Kueh

This thought experiment works because consumers: (1) expect to be excluded from the benefits of others’ provision (via heterogeneous experience) and (2) each pays a personalised price.

They all buy the same amount and are charged according to their MBs at that level.

No one is actually excluded, thus not violating the Pareto improvement argument above.

Policy responses under private (imperfect) information

Russell Kueh

Preference Revelation

• Hope to design a mechanism that induces the consumers to reveal their preferences truthfully. • Lectures present a Discrete Public Good and N Agent model, in which government is deciding

whether to provide a public good at a cost of C to be shared equally among N agents. • If provided, agent i’s net benefit bi = φi – C/N; otherwise agent i’s net benefit is zero. • i’s valuation and thus her bi is private information. • Government wants to provide the public good if and only if social net benefit is non-negative i.e. ∑bi ≥ 0

Pivot Mechanism

• Each agent simultaneously report her net benefit • Provided iff net benefit non-negative

Russell Kueh

• An agent i pays a tax iff she is pivotal, the amount of which equals the absolute value of the sum of other agent’s announced net benefits

• It is a weakly dominant strategy for agent i to report her net benefit truthfully, satisfying government’s objective of truth-induction

• This and other similar mechanisms generally work since they effectively require each agent to take responsibility of the “net” externality that the agent’s decision imposes on others

• But the side payments involved in such mechanisms mean that the government runs a surplus that it has to “burn”

• Refer to Market Failure lecture notes P.50 for algebraic representations and proofs

Mixed Public Goods (Qualitative account, extracted from Ch. 4, B&B) Many goods are neither purely rival nor purely public. ‘Mixed public goods’ are those subject to congestion costs as the number of users increases e.g. parks, road, concerts, golf course etc. At some point the addition of another user reduces the enjoyment of others, usually in terms of ‘quality’, but it is analytically useful to think of congestion as the altering of the ’amount’ of the good per user. It (interestingly) turns out that it is possible to provide optimal allocation of missed public goods via a decentralised decision-making process. Tiebout (1956) analyses the case where mixed public goods such as police protection, fire proctection etc. are provided by local governments. He argues that if communities are geographically isolated so that some form of exclusion can be effected against those non-locals, and if HHs are mobile and can choose a community solely on the basis of the “local public good/ lump-sum tax” package offered by each of the communities, then (with a few more technical assumptions) there will be an optimal allocation of the local public goods achieved. Buchanan (1965) offered a private sector version of the above mechanism with ‘clubs’ instead of ‘local governments’ and a ‘membership fee/facility’ package instead of a ‘local public good/tax’ package. This result, that mixed public goods can be optimally provided by a decentralised mechanism, is very important. It implies jointness per se does not lead to market failure (non-excludability and non-rivalry required as well). And this result is quite general. The important assumptions are that excludability is present and that costs rise eventually due to congestion.

Market Failure and the Role of the Public Sector

B&B

Non-excludability (of HHs from certain desirable and undesirable commodities) is one of the important reasons why a Pareto optimal allocation of resources may not be achieved through a decentralised market system.

Exclusion may not be feasible for technological reasons, as in the case of national defence, or for institutional reasons, as in the case of ill-defined property rights system.

In other instances, exclusion would only yield a Pareto optimal outcome if the appropriate ‘personalised’ prices can be ascertained and enforced.

Russell Kueh

In all cases of market failure, the MSB will differ from MSB, since market participants are motivated by divergent MPC and MPB. Overconsumption or under-provision will occur where there are net external costs or net external benefits, respectively.

The government may have a role to play – to involve itself in the actual allocation of resources. It should be able (theoretically) to undertake mutually beneficial allocative actions (i.e. Pareto improvements) that private agents cannot because of it’s monopoly on the legal use of coercive power. It can extract involuntary payments and/or prohibit activities. This allows the public provision of non-excludable public goods that suffer from the free-rider problem and which, therefore, would not be provided privately.

Similarly, it can utilise corrective price instruments such as Pigouvian taxes/subsidies that eliminate the divergence between private and social MC/MB, and/or utilise quantity instruments like quotas.

It is worth emphasising that this view of the benefits of governmental allocative functions is quite distinct from the superficial view that the government ‘knows better’ and provides a coordinated and planned way to resource allocation as opposed to the ‘invisible hand’ approach of private market.

Although the government sector may pursue ‘corrective’ policies in an economy which is not Pareto optimal, it could also be a cause rather than a cure of market failure. Tax and transfer policies may lead to a non-optimal allocation of resources in an economy that would otherwise be Pareto optimal: non-lump-sum tax/subsidies alters the relative prices perceived by different agents, causing the Pareta optimal conditions not to be satisfied (e.g. the mechanism whereby MRSs are equated by the same relative price facing all—thereby achieving exchange efficiency—might break down).

Farrell (1987), Information and Coase Theorem

Critical Perspective on Coase Theorem

Coase challenged the view that complete competitive markets are necessary for efficiency, arguing that if market outcomes are inefficient, people get together and negotiate their way to efficiency. This seems far more ambiguous than FTWE, having dispensed with the strong assumptions of FTWE. The theorem can also be seen as a Decentralisation Result, allowing statements like ‘if this and this hold, then selfishly optimal individual decisions will lead to efficient aggregate outcome’ to be said.

But this theorem is important only if we believe efficient bargaining is likely. Note that while the theorem seems robust at first glance—claiming that ‘absent barriers to contracting, all must be well’—inherent in it are strong assumptions that no mutually beneficial agreement is missed (analogous to no market imperfection is present…).

Bargaining is typically inefficient when, as is likely, each bargainer knows something relevant that the other does not (presence of private information). The results are costly, delayed and incomplete bargaining.

Coase Theorem holds only if everyone’s preferences and opportunities are common knowledge, which is quite implausible unless people know others very well. But in any realistic economy, such informational requirement is at best idealistic.

As arguments against active government, FTWE and Coase Theorem are unconvincing: they simply claim that in ideal circumstances, laissez-faire outcome is no less Pareto-efficient that ideal government-dictated outcome, but don’t claim to be better, while having obvious disadvantages, as in problems of equity. Claims that markets will be efficient when government, under the same assumptions, is equally good are pretty unexciting.

Russell Kueh

Implications of Coase Theorem for the issue of institution

CT is viewed to recommend a particular institution: well-defined property rights and voluntary private bargaining over them. As shown above, this is not convincing, because CT requires such strict assumptions that if they were to hold, government-dictated outcome is just as efficient.

A more practical, and instructive, view of CT is to put it in the context of imperfect information, seeing negotiation not as a substitute for other institutions (e.g. market or government) but as a supplement or back-up to them; agents will reply on, say, markets where they can, and negotiate only when for some reason markets fail them. (This resembles Williamson’s (1985) Transaction-cost theory, where administrative system functions as patch to market system when contracting is costly.) This view implies that all economic institutions are better than they on their own seem. Any deficiencies can be repaired, to some extent, by private negotiations. A profound suggestion in this article is the two-stage evaluation of institutions. Extending the previous argument, it is noted that while we expect all institutions to be better than they seem, they need not be better to the same degree. There can be an institution (or student) that scores 75% without repairs by private negotiation (or revision), but scores only 2% more at 77% after all possible repairs (revisions) are done, while there can be one that scores only 60% without repairs (or revision) but 80% after all improvements are exhausted.

The two-stage evaluation of institution precisely focuses on this issue of ‘repairability’: before concluding overall efficiency, we must not only look at what outcomes the institution on its own would yield, but also ask how far it can be repaired by private negotiation.

In the case of bureaucrats, we need to ask whether or not the clumsy (inefficient) compromise that they are prepared to enforce is a good starting point for negotiation, compared, say, to one party’s most-preferred outcome (in which case he certainly won’t trade).

Farrell (1987) suggests therefore that this use of bureaucrats—to ensure an equitable status quo for bargaining—is more efficient than just letting the bureaucrat decide, or private property rights alone.