ey - financial reporting briefs...accounting update 4 | financial reporting briefs retail and...

TRANSCRIPT

Financial reporting briefs Retail and consumer products What you need to know about this quarter’s accounting, financial reporting and other developments

September 2014

In this issue:

Top story ..................................... 2 Accounting update ........................ 3 Regulatory developments .............. 7 Other considerations ..................... 9 Effective date highlights .............. 10 Reference library ........................ 12

2 | Financial reporting briefs Retail and consumer products September 2014

Top story FASB moves quickly on simplification projects The Financial Accounting Standards Board (FASB or Board) issued three proposals in its new simplification initiative to improve US GAAP by moving quickly to address narrow issues identified by stakeholders.

One proposal could significantly affect retail and consumer products entities. It would simplify the subsequent measurement of inventory by requiring entities to use the lower of cost or net realizable value (i.e., estimated selling price in the ordinary course of business, less reasonably predictable costs of completion, disposal and transportation). Today, entities use the lower of cost or market (LOCOM), which requires them to also consider the replacement cost and net realizable value of inventory, less a normal profit margin (i.e., floor). Entities that use last-in first-out (LIFO) to value inventory should carefully consider how the proposal would affect their accounting. The FASB does not intend for the proposal to change other aspects of inventory accounting, such as the methods entities use to estimate inventory cost (e.g., average cost, first- in first-out or FIFO, LIFO, retail inventory method).

Another proposal would eliminate extraordinary items from US GAAP. The last would require customers in cloud computing arrangements to apply a framework to determine whether they are acquiring licenses of intellectual property or just paying for a service.

The FASB launched the initiative earlier this year to reduce the cost and complexity of financial reporting by making targeted changes to US GAAP while maintaining or improving the usefulness of information for investors. In a recent column in the FASB Outlook publication, FASB Chairman Russell Golden discussed the initiative and summed up the sentiments of both investors and preparers of financial statements by saying: “When accounting is complex, no one wins.”

We support the FASB’s simplification objective. While the projects individually might not have a significant impact, we expect the Board to make meaningful progress over time. So far, the FASB has received more than 70 suggestions from constituents and is soliciting other ideas on topics it can tackle as part of the initiative. Many of the simplification projects will be of interest to retail and consumer products companies.

The FASB is moving more quickly than usual on these projects, sometimes by adding topics to its agenda, deliberating them and deciding to issue proposals at the same meeting. That was the case in August, when the Board added projects and decided to move ahead with proposals on simplifying the presentation of debt issuance costs on the balance sheet and allowing employers to measure defined benefit plan assets and the related projected benefit obligation as of the closest calendar month end to their fiscal year end. At the meeting, the FASB also added projects to its agenda to (1) simplify the balance sheet classification of debt and (2) simplify income tax accounting by requiring all deferred tax assets and liabilities to be classified as noncurrent and eliminating the exception for recognition of income taxes on intercompany transactions.

Mr. Golden noted in his column that the FASB is taking other steps to address complexity, including simplifying the accounting for private companies and voting to go its own way in joint projects with the International Accounting Standards Board (IASB), such as on certain elements of the leases project and in the financial instruments project.

The initiative comes as the Securities and Exchange Commission (SEC) staff is reviewing its own rules to determine whether changing them could make disclosures more effective and potentially less voluminous. The FASB also is working on a disclosure framework project aimed at making disclosures more effective.

Welcome to the September 2014 Financial reporting briefs — retail and consumer products. This edition highlights the latest developments in financial reporting for the retail and consumer products industries and alerts you to some important considerations for 2014.

Interested in the latest developments at the FASB? We’ve got it covered in our Top story and the Accounting update section, where you also can find the status of the FASB’s joint projects with the IASB.

In our Regulatory developments section, we offer other insights about the SEC and the PCAOB.

Our Other considerations section provides you with other news from the quarter and a summary of open comment periods.

Need more information? Check out our Reference library, where we list our recent publications on the topics discussed here and provide links to them.

Financial reporting briefs Retail and consumer products September 2014 | 3

Accounting update It’s off to the races on revenue recognition As they assess how to implement the new revenue recognition standard, many companies are monitoring the discussions of the Joint Transition Resource Group on Revenue Recognition (TRG), which met for the first time in July. The big question now is whether the FASB and the IASB (collectively, the Boards) will decide that, based on the TRG’s discussions, more implementation guidance is needed. As expected, the TRG didn’t make any recommendations when it discussed questions about gross versus net presentation, royalties on licensed intellectual property and impairment of capitalized contract costs. The Boards have promised to provide a status update on these issues by the next TRG meeting on 31 October 2014. That could include a decision on whether to reconsider an issue. Many of the 16 industry task forces formed by the American Institute of Certified Public Accountants (AICPA) also began meeting to discuss industry-specific issues and how to update the AICPA’s non-authoritative guidance on revenue recognition. The AICPA has not established a task force for the retail or consumer products industries.

The new standard will supersede virtually all of the revenue guidance in US GAAP and IFRS and will require entities to use more judgment than they do today. Our recent Technical Line, The new revenue recognition standard — retail and consumer products, summarizes the key implications for retail and consumer products entities.

Public entities should consider how they will communicate the effects of the new standard with investors and other stakeholders, including their plans for disclosures about the effects of new accounting standards discussed in SEC Staff Accounting Bulletin (SAB) Topic 11.M. An SEC staff member recently said the staff won’t object if companies that use the full retrospective approach to adopt the standard do not recast the earliest two years in their five-year selected financial data disclosures. That is, a company will be required to reflect the accounting change in the summary only for the three years for which it presents full financial statements elsewhere in the filing. The staff member said clear disclosure about the lack of comparability will be required. Under US GAAP, the standard is effective for public entities for fiscal years beginning after 15 December 2016 and interim periods therein. The effective date for nonpublic entities is fiscal years beginning after 15 December 2017 and interim periods within fiscal years beginning after 15 December 2018. Nonpublic entities may adopt the standard early, but not before the effective date for public entities.

Management will have to assess going concern uncertainties The FASB issued final guidance that requires management of public and private companies to evaluate whether there is substantial doubt about the entity’s ability to continue as a going concern and, if so, disclose that fact. Management will also be required to evaluate and disclose whether its plans alleviate that doubt. The assessment will be similar to the one auditors historically have done, but management will have to make the assessment and related disclosures for both annual and interim reporting periods (if the entity reports on an interim basis).

Unlike the auditing standards, the new standard defines substantial doubt as when it is probable (i.e., likely) that the entity will be unable to meet its obligations as they become due within one year of the date the financial statements are issued (or available to be issued, when applicable). The guidance states that, when making this assessment, management should consider relevant conditions or events that are known or reasonably knowable on the date the financial statements are issued or available to be issued. The standard is effective for annual periods ending after 15 December 2016 and interim periods thereafter, and early adoption is permitted. We expect the Public Company Accounting Oversight Board (PCAOB) and the AICPA’s Auditing Standards Board to align their standards with the guidance in the Accounting Standards Update (ASU) by, for example, adding the definition of substantial doubt to their auditing standards and changing the timing of the auditor’s review, which currently is as of the balance sheet date.

Accounting update

4 | Financial reporting briefs Retail and consumer products September 2014

FASB still debating financial instruments guidance The FASB continued to discuss making targeted improvements to current US GAAP guidance for classifying and measuring financial instruments rather than overhauling it, as it had proposed in 2013. The FASB reaffirmed its proposal to apply a one-step impairment test (which is a qualitative test) to equity securities without readily determinable fair values but hasn’t decided whether to apply this test to equity method investments or retain today’s other-than-temporary impairment model. The FASB also decided to add and eliminate various disclosure requirements.

On impairment, the Board has decided that available-for-sale debt securities would continue to follow today’s other-than-temporary impairment model with some modifications. The Board also reaffirmed its decision that held-to-maturity debt securities will follow the proposed lifetime expected credit losses model. The Board said the final standard would not provide examples of financial assets for which a zero allowance would be acceptable. Constituents had asked the Board to provide more guidance on how to treat highly rated debt securities such as US Treasury securities. We expect the Board to wrap up deliberations on both parts of the financial instruments project in the coming months and issue new guidance in 2015. The Board plans to begin discussing the hedging part of the project soon.

Boards push ahead on leases The FASB and the IASB continued to look for ways to clarify and simplify their 2013 proposal to put most leases on lessees’ balance sheets. During the quarter, the Boards decided that seller-lessees in sale and leaseback transactions would use the definition of a sale in the new revenue recognition standard to determine whether a sale has occurred. They also confirmed their earlier decision that the presence of a leaseback, in and of itself, would not preclude a sale. However, they reached different conclusions on how to determine whether a sale occurs in certain circumstances. The differences resulted, in part, from the Boards’ earlier disagreement on the lessee accounting model. As we’ve said before, the FASB is pursuing a dual model for lessee accounting while the IASB is pursuing a single model with an exception for small-ticket assets. It is unclear whether or when the Boards will revisit their differences. The FASB also affirmed its 2013 proposal to eliminate leveraged lease accounting under the final standard but decided that leveraged leases that exist at transition would be grandfathered. The Boards aren’t likely to issue new standards before the second half of 2015.

Private Company Council update At its September meeting, the Private Company Council (PCC) was scheduled to discuss its project on how to allow private companies to simplify their accounting for intangible assets acquired in a business combination. The discussion was expected to include research the FASB staff performed on the accounting for noncompetition arrangements in asset acquisitions and the possible narrowing of the definition of contractual customer-related intangibles. The PCC also was scheduled to discuss FASB staff research on how to simplify private company accounting for share-based payments. The PCC has an ongoing project to consider whether the various definitions of public and nonpublic entities in US GAAP that predate the FASB’s use of the term public business entity should be changed or consolidated. It is also considering whether to address partnership accounting.

New consolidation guidance is coming soon The FASB has finished redeliberations on its consolidation project and plans to issue a final standard after certain constituents review a draft to make sure there are no unintended consequences. In redeliberations, the FASB abandoned its 2011 proposal to require a separate principal-agent analysis and decided instead to make targeted revisions to current guidance to achieve the same objective (i.e., to rescind the current FAS 167 deferral for certain investment companies). While the proposal is aimed at asset managers, it could affect entities in all industries, particularly those that have involvement with limited partnerships or similar entities.

The standard is expected to relax the criteria in US GAAP for determining when fees paid to a decision maker or service provider do not represent a variable interest by focusing on whether those fees are “at market.” The FASB has said it will clarify what this means in drafting the new standard, but significant judgment will likely be required to make this determination. The standard also is expected to amend the criteria for determining whether a limited partnership (or similar entity) is a variable interest entity by allowing a general partner to consider kick-out rights held by a simple majority of partners in its analysis.

Accounting update

Financial reporting briefs Retail and consumer products September 2014 | 5

In addition, the standard is expected to eliminate the current presumption that a general partner controls a limited partnership in the voting model. The FASB decided to make the standard effective for annual periods and interim periods within those annual periods beginning after 15 December 2015. For nonpublic business entities, it will be effective for annual periods beginning after 15 December 2016 and interim periods beginning after 15 December 2017. The FASB plans to permit early adoption.

FASB issues final guidance on EITF share-based payment issue The FASB issued an ASU with guidance saying that a performance target that affects vesting of a share-based payment and that could be achieved after the requisite service period is a performance condition under Accounting Standards Codification (ASC) 718, Compensation — Stock Compensation. The guidance is based on a consensus of the Emerging Issues Task Force (EITF).

EITF to discuss comments on pushdown accounting, other topics At its September meeting, the EITF is scheduled to discuss comments on a FASB proposal to give all entities the option to apply pushdown accounting when an acquirer obtains control of them. Under pushdown accounting, an acquired entity’s separate financial statements reflect the acquirer’s new basis of accounting for the acquired entity’s assets and liabilities. The comment letters express broad support for the proposal, which is based on an EITF consensus.

The EITF is also expected to discuss potential application guidance for its consensus that all stated and implied substantive terms and features of a hybrid financial instrument issued in the form of a share should be considered when determining whether the host contract is more akin to debt or to equity.

In addition, the EITF is expected to discuss two new issues. One of them would address diversity in practice in how entities categorize certain investments measured at net asset value in Level 2 or Level 3 of the fair value hierarchy.

FASB continues work on disclosure framework project Comments are in on the FASB’s proposal to add a chapter to the Conceptual Framework describing how it would evaluate new and existing disclosure requirements. In our comment letter on the proposed Conceptual Framework chapter, we supported the FASB’s goal of improving disclosure effectiveness by developing a framework for the Board to consider when evaluating disclosure requirements. But we said the framework, as proposed, would likely add to the volume of disclosures. We also recommended ways the FASB could improve the proposal, including providing guidance on materiality and clearly distinguishing between annual and interim disclosure requirements.

During the quarter, the FASB began discussing the comments it received on the proposed Conceptual Framework chapter. The FASB also began discussing how to promote the appropriate use of discretion by reporting entities. To do this, the FASB is looking at disclosure requirements for defined benefit plans by employers, fair value measurement, income taxes and inventory. The FASB also is looking at how to promote discretion in preparing disclosure for interim financial reporting. The Board plans to propose an ASU on the entity’s decision process.

New actuarial tables may raise benefit plan sponsors’ obligations The Society of Actuaries is expected to soon issue new mortality tables for benefit plan sponsors to use when measuring their benefit plan costs and obligations. The proposed tables, which reflect improved life expectancies, are likely to be finalized in time to affect 2014 year-end benefit plan calculations. If that happens, plan sponsors should consider the changes in life expectancies when determining their best estimate of the mortality rate for measuring defined benefit plan costs and obligations. The effect will vary by plan, but using the new data could cause a significant increase in a sponsor’s defined benefit plan obligation.

Accounting update

6 | Financial reporting briefs Retail and consumer products September 2014

Goodwill impairment reminders As a reminder, you may need to allocate the assets and liabilities in your existing businesses and subsidiaries among your reporting units to perform Step 1 of the impairment test. Generally, assets and liabilities are included in a reporting unit’s carrying amount if the asset will be used in the reporting unit or the liability relates to the operations of the reporting unit. The same principle applies to assigning corporate assets and liabilities (e.g., trade or brand names, pension obligations, debt, environmental liabilities) to a company’s reporting units. Assets or liabilities that relate to multiple reporting units are assigned to the various units using a reasonable and supportable method that is applied consistently each year.

The SEC staff often asks questions about companies’ disclosures about goodwill impairment and the determination of reporting units. Recently, the staff has focused on whether companies that aggregate multiple components into a reporting unit provide enough information in their disclosures. Retail and consumer products companies also should make sure that their review controls over impairment testing are precise enough to detect a possible misstatement that could be material.

Financial reporting briefs Retail and consumer products September 2014 | 7

Regulatory developments SEC staff continues work on disclosure effectiveness project The SEC staff is continuing to review SEC disclosure requirements and discussing how to streamline disclosures and make them more meaningful. One or more concept releases are expected later this year. In the meantime, the staff is continuing to highlight actions registrants can take on their own to make their disclosures more effective. The staff has said that registrants should consider ways to cross-reference disclosures rather than repeat them within the filing. For example, disclosures about legal proceedings are often repeated elsewhere in the filing, such as in risk factors, management’s discussion and analysis (MD&A) and the notes to the financial statements. Registrants also can streamline MD&A by focusing on material matters rather than mechanically discussing the change in each financial statement line item.

Mark Kronforst, the chief accountant in the Division of Corporation Finance, has said publicly that companies should remove disclosures made in response to earlier SEC staff comment letters if those matters are no longer material. Other SEC staff members said the staff would not challenge registrants on why certain disclosures, if no longer material, were removed from filings.

SEC issues final rule on money market funds The SEC issued final rules aimed at minimizing money market funds’ exposure to rapid redemptions. Institutional prime money market funds will be required to operate with floating net asset values after a two-year transition period. Boards of directors of nongovernment money market funds will be required to impose 1% fees on redemptions if a fund’s weekly liquid assets fall below 10% of total assets unless the board determines that imposing such a fee would not be in the best interest of the fund. Boards of these funds will have the option of imposing fees of up to 2% or suspending redemptions (i.e., imposing gates) for up to 10 business days in a 90-day period, if the fund’s weekly liquid assets fall below 30% of its total assets.

The SEC also said that, in normal circumstances, an investment in a money market fund with a floating net asset value or one that could impose fees or gates still could be considered a “cash equivalent” under US GAAP. However, the SEC said shareholders would have to assess whether that classification remains appropriate if a fund experiences credit or liquidity issues or imposes a fee or gate.

SEC takes aim at ICFR violations In a recent enforcement action, the SEC charged the chief executive officer (CEO) and the former chief financial officer (CFO) of a small company with misleading its auditors and the public about the state of the company’s internal control over financial reporting (ICFR). According to the SEC, the men falsely represented, among other things, that the CEO participated in management’s assessment of the effectiveness of ICFR and that they had disclosed all significant internal control deficiencies to the auditors. The former CFO settled the charges. The SEC enforcement case is unusual because it relates to deficiencies in ICFR and management’s responsibilities when there was not also a material misstatement of the financial statements. However, it is indicative of the staff’s current focus on ICFR. The staff continues to ask companies that correct immaterial errors how the underlying control deficiencies were considered in management’s current and previous assessments of the effectiveness of both ICFR and disclosure controls and procedures.

SEC staff weighs in on XBRL practices

The SEC Division of Corporation Finance recently sent letters to certain registrants saying their XBRL exhibits omitted the required calculation relationships for certain line item elements and requesting that they be included in future XBRL exhibits. These relationships show the mathematical connection between elements (e.g., current assets plus noncurrent assets equal total assets on the balance sheet).

Separately, the staff of the Division of Economic and Risk Analysis issued observations about custom tagging in XBRL exhibits and noted that some registrants, often those in the last XBRL phase-in group, used custom tags for more than half the tagged items in their filings. SEC rules permit custom tags to be used only when a standard tag from the XBRL taxonomy doesn’t exist for a financial element. The SEC staff plans to continue monitoring trends in custom tagging and may consider further guidance or other actions. Registrants should consider these actions and, if they use an XBRL service provider, discuss them with that provider.

Regulatory developments

8 | Financial reporting briefs Retail and consumer products September 2014

James Schnurr named Chief Accountant of the SEC The SEC said James Schnurr will join the agency as Chief Accountant in its Office of the Chief Accountant in October, succeeding Paul Beswick who is leaving the SEC. Mr. Schnurr recently retired from Deloitte LLP, where he served as vice chairman and senior professional practice director in the firm’s national accounting office. He was a partner at Deloitte for 29 years and previously served in the firm’s mergers and acquisitions group.

SEC considering PCAOB guidance on related parties The SEC is considering a new PCAOB standard and related amendments intended to increase the auditor’s focus on a company’s transactions with related parties, significant unusual transactions and a company’s financial relationships and transactions with its executive officers. The standard and amendments, which are subject to SEC approval, would require auditors to perform specific procedures, including reading executives’ compensation agreements and obtaining evidence to substantiate management assertions regarding the nature of related party transactions.

The standard and amendments would be effective for audits of financial statements for fiscal years beginning on or after 15 December 2014, including reviews of interim financial information within those fiscal years.

PCAOB mulls changes to auditing estimates, fair value measurements The PCAOB issued a staff consultation paper seeking input on whether it should update its rules on auditing accounting estimates and fair value measurements in light of significant deficiencies it has found in these areas. The paper seeks comment on whether the PCAOB should develop a new standard that would consolidate existing audit guidance and include new material to address inspection findings, practice issues and changes in accounting guidance. The paper also seeks comment on whether alternative approaches, such as issuing staff guidance, might be more appropriate. The Board said it will host a Standing Advisory Group meeting on 2 October 2014 to discuss matters addressed in the paper.

PCAOB issues Staff Audit Practice Alert on auditing revenue The PCAOB issued a Staff Audit Practice Alert on auditing revenue due to significant audit deficiencies it frequently observes during inspections. The Alert discusses (1) testing recognition of revenue from contractual arrangements, (2) evaluating presentation of revenue (i.e., gross versus net revenue), (3) testing whether revenue was recognized in the correct period, (4) evaluating whether the financial statements include the required disclosures on revenue, (5) responding to risks of material misstatement due to fraud associated with revenue, (6) testing and evaluating controls over revenue, (7) applying audit sampling procedures to test revenue, (8) performing substantive analytical procedures to test revenue, and (9) testing revenue in companies with multiple locations.

Given that professional standards presume there is a risk of material misstatement due to fraud associated with revenue, the Alert emphasizes the importance of exercising professional skepticism when auditing revenue and the need for audit team executives to ensure that their teams are implementing and executing appropriate procedures. It also notes that it is critical for engagement quality reviewers to focus on our audit strategy and execution related to revenue.

Financial reporting briefs Retail and consumer products September 2014 | 9

Other considerations Highly inflationary economies The SEC staff has indicated that companies should treat the following countries as highly inflationary economies, as defined under US GAAP:

Venezuela

Belarus

Sudan

Iran

Because the cumulative three-year inflation rate in Belarus is projected to drop below 100% by the end of 2014, the SEC staff has said companies should monitor the data to determine whether it is appropriate to continue treating that economy as highly inflationary.

Summary of open comment periods Proposal Comment period ends

Customer’s accounting for fees paid in a cloud computing arrangement

18 November 2014

Simplifying income statement presentation by eliminating the concept of extraordinary items

30 September 2014

Simplifying the measurement of inventory 30 September 2014

10 | Financial reporting briefs Retail and consumer products September 2014

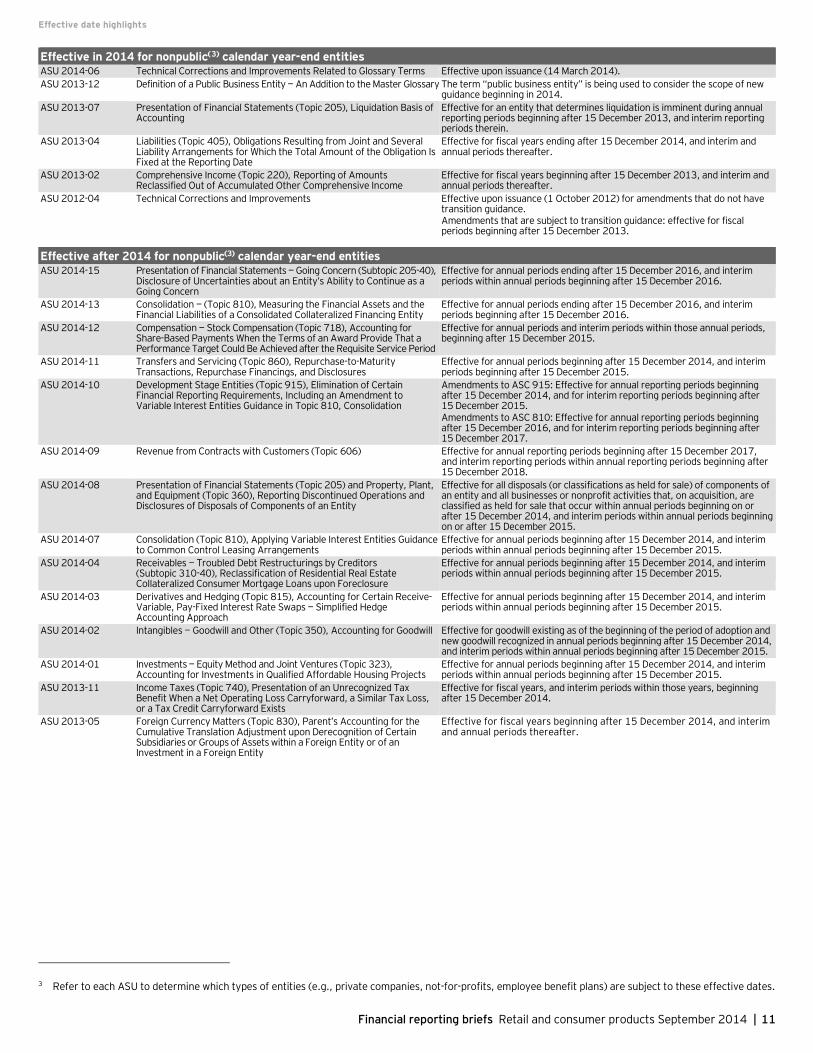

Effective date highlights Note: Early adoption generally is permitted unless otherwise noted.

Effective in 2014 for public(1) calendar year-end entities(2) ASU 2014-06 Technical Corrections and Improvements Related to Glossary Terms Effective upon issuance (14 March 2014). ASU 2013-12 Definition of a Public Business Entity — An Addition to the Master

Glossary The term “public business entity” is being used to consider the scope of new guidance beginning in 2014.

ASU 2013-11 Income Taxes (Topic 740), Presentation of an Unrecognized Tax Benefit When a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists

Effective for fiscal years, and interim periods within those years, beginning after 15 December 2013.

ASU 2013-07 Presentation of Financial Statements (Topic 205), Liquidation Basis of Accounting

Effective for an entity that determines liquidation is imminent during annual reporting periods beginning after 15 December 2013, and interim reporting periods therein.

ASU 2013-05 Foreign Currency Matters (Topic 830), Parent’s Accounting for the Cumulative Translation Adjustment upon Derecognition of Certain Subsidiaries or Groups of Assets within a Foreign Entity or of an Investment in a Foreign Entity

Effective for fiscal years, and interim periods within those years, beginning after 15 December 2013.

ASU 2013-04 Liabilities (Topic 405), Obligations Resulting from Joint and Several Liability Arrangements for Which the Total Amount of the Obligation Is Fixed at the Reporting Date

Effective for fiscal years, and interim periods within those years, beginning after 15 December 2013.

Effective after 2014 for public(1) calendar year-end entities(2) ASU 2014-15 Presentation of Financial Statements — Going Concern (Subtopic 205-40),

Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern

Effective for annual periods ending after 15 December 2016, and interim periods within annual periods beginning after 15 December 2016.

ASU 2014-13 Consolidation — (Topic 810), Measuring the Financial Assets and the Financial Liabilities of a Consolidated Collateralized Financing Entity

Effective for annual periods, and interim periods within those annual periods, beginning after 15 December 2015.

ASU 2014-12 Compensation — Stock Compensation (Topic 718), Accounting for Share-Based Payments When the Terms of an Award Provide That a Performance Target Could Be Achieved after the Requisite Service Period

Effective for annual periods and interim periods within those annual periods, beginning after 15 December 2015.

ASU 2014-11 Transfers and Servicing (Topic 860), Repurchase-to-Maturity Transactions, Repurchase Financings, and Disclosures

Effective for the first interim or annual period beginning after 15 December 2014. Disclosures for transactions accounted for as secured borrowings: Effective for annual periods beginning after 15 December 2014, and for interim periods beginning after 15 March 2015.

ASU 2014-10 Development Stage Entities (Topic 915), Elimination of Certain Financial Reporting Requirements, Including an Amendment to Variable Interest Entities Guidance in Topic 810, Consolidation

Amendments to ASC 915: Effective for annual reporting periods beginning after 15 December 2014, and interim periods therein. Amendments to ASC 810: Effective for annual reporting periods beginning after 15 December 2015, and interim periods therein.

ASU 2014-09 Revenue from Contracts with Customers (Topic 606) Effective for annual reporting periods beginning after 15 December 2016, including interim reporting periods within that reporting period.

ASU 2014-08 Presentation of Financial Statements (Topic 205) and Property, Plant, and Equipment (Topic 360), Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity

Effective for all disposals (or classifications as held for sale) of components of an entity, and all businesses or nonprofit activities that, on acquisition, are classified as held for sale, that occur within annual periods beginning on or after 15 December 2014, and interim periods within those years.

ASU 2014-04 Receivables — Troubled Debt Restructurings by Creditors (Subtopic 310-40), Reclassification of Residential Real Estate Collateralized Consumer Mortgage Loans upon Foreclosure

Effective for annual periods, and interim periods within those annual periods, beginning after 15 December 2014.

ASU 2014-01 Investments — Equity Method and Joint Ventures (Topic 323), Accounting for Investments in Qualified Affordable Housing Projects

Effective for annual periods, and interim reporting periods within those annual periods, beginning after 15 December 2014.

1 Refer to each ASU to determine which types of entities (e.g., public business entities, not-for-profits, employee benefit plans) are subject to these effective dates. 2 The JOBS Act allows emerging growth companies to follow private company effective dates for new or revised accounting standards issued after 5 April 2012.

However, an emerging growth company must follow public company effective dates for all such standards if it has disclosed an election to do so.

Effective date highlights

Financial reporting briefs Retail and consumer products September 2014 | 11

Effective in 2014 for nonpublic(3) calendar year-end entities ASU 2014-06 Technical Corrections and Improvements Related to Glossary Terms Effective upon issuance (14 March 2014). ASU 2013-12 Definition of a Public Business Entity — An Addition to the Master Glossary The term “public business entity” is being used to consider the scope of new

guidance beginning in 2014. ASU 2013-07 Presentation of Financial Statements (Topic 205), Liquidation Basis of

Accounting Effective for an entity that determines liquidation is imminent during annual reporting periods beginning after 15 December 2013, and interim reporting periods therein.

ASU 2013-04 Liabilities (Topic 405), Obligations Resulting from Joint and Several Liability Arrangements for Which the Total Amount of the Obligation Is Fixed at the Reporting Date

Effective for fiscal years ending after 15 December 2014, and interim and annual periods thereafter.

ASU 2013-02 Comprehensive Income (Topic 220), Reporting of Amounts Reclassified Out of Accumulated Other Comprehensive Income

Effective for fiscal years beginning after 15 December 2013, and interim and annual periods thereafter.

ASU 2012-04 Technical Corrections and Improvements Effective upon issuance (1 October 2012) for amendments that do not have transition guidance. Amendments that are subject to transition guidance: effective for fiscal periods beginning after 15 December 2013.

Effective after 2014 for nonpublic(3) calendar year-end entities ASU 2014-15 Presentation of Financial Statements — Going Concern (Subtopic 205-40),

Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern

Effective for annual periods ending after 15 December 2016, and interim periods within annual periods beginning after 15 December 2016.

ASU 2014-13 Consolidation — (Topic 810), Measuring the Financial Assets and the Financial Liabilities of a Consolidated Collateralized Financing Entity

Effective for annual periods ending after 15 December 2016, and interim periods beginning after 15 December 2016.

ASU 2014-12 Compensation — Stock Compensation (Topic 718), Accounting for Share-Based Payments When the Terms of an Award Provide That a Performance Target Could Be Achieved after the Requisite Service Period

Effective for annual periods and interim periods within those annual periods, beginning after 15 December 2015.

ASU 2014-11 Transfers and Servicing (Topic 860), Repurchase-to-Maturity Transactions, Repurchase Financings, and Disclosures

Effective for annual periods beginning after 15 December 2014, and interim periods beginning after 15 December 2015.

ASU 2014-10 Development Stage Entities (Topic 915), Elimination of Certain Financial Reporting Requirements, Including an Amendment to Variable Interest Entities Guidance in Topic 810, Consolidation

Amendments to ASC 915: Effective for annual reporting periods beginning after 15 December 2014, and for interim reporting periods beginning after 15 December 2015. Amendments to ASC 810: Effective for annual reporting periods beginning after 15 December 2016, and for interim reporting periods beginning after 15 December 2017.

ASU 2014-09 Revenue from Contracts with Customers (Topic 606) Effective for annual reporting periods beginning after 15 December 2017, and interim reporting periods within annual reporting periods beginning after 15 December 2018.

ASU 2014-08 Presentation of Financial Statements (Topic 205) and Property, Plant, and Equipment (Topic 360), Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity

Effective for all disposals (or classifications as held for sale) of components of an entity and all businesses or nonprofit activities that, on acquisition, are classified as held for sale that occur within annual periods beginning on or after 15 December 2014, and interim periods within annual periods beginning on or after 15 December 2015.

ASU 2014-07 Consolidation (Topic 810), Applying Variable Interest Entities Guidance to Common Control Leasing Arrangements

Effective for annual periods beginning after 15 December 2014, and interim periods within annual periods beginning after 15 December 2015.

ASU 2014-04 Receivables — Troubled Debt Restructurings by Creditors (Subtopic 310-40), Reclassification of Residential Real Estate Collateralized Consumer Mortgage Loans upon Foreclosure

Effective for annual periods beginning after 15 December 2014, and interim periods within annual periods beginning after 15 December 2015.

ASU 2014-03 Derivatives and Hedging (Topic 815), Accounting for Certain Receive-Variable, Pay-Fixed Interest Rate Swaps — Simplified Hedge Accounting Approach

Effective for annual periods beginning after 15 December 2014, and interim periods within annual periods beginning after 15 December 2015.

ASU 2014-02 Intangibles — Goodwill and Other (Topic 350), Accounting for Goodwill Effective for goodwill existing as of the beginning of the period of adoption and new goodwill recognized in annual periods beginning after 15 December 2014, and interim periods within annual periods beginning after 15 December 2015.

ASU 2014-01 Investments — Equity Method and Joint Ventures (Topic 323), Accounting for Investments in Qualified Affordable Housing Projects

Effective for annual periods beginning after 15 December 2014, and interim periods within annual periods beginning after 15 December 2015.

ASU 2013-11 Income Taxes (Topic 740), Presentation of an Unrecognized Tax Benefit When a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists

Effective for fiscal years, and interim periods within those years, beginning after 15 December 2014.

ASU 2013-05 Foreign Currency Matters (Topic 830), Parent’s Accounting for the Cumulative Translation Adjustment upon Derecognition of Certain Subsidiaries or Groups of Assets within a Foreign Entity or of an Investment in a Foreign Entity

Effective for fiscal years beginning after 15 December 2014, and interim and annual periods thereafter.

3 Refer to each ASU to determine which types of entities (e.g., private companies, not-for-profits, employee benefit plans) are subject to these effective dates.

12 | Financial reporting briefs Retail and consumer products September 2014

Reference library To the Point • FASB requires management to assess an entity’s ability to

continue as a going concern (4 September 2014)

• FASB addresses sale and leasebacks, US GAAP topics in leases project (3 September 2014)

• FASB decides to change accounting and disclosures for long-duration insurance contracts (28 August 2014)

• FASB to issue final guidance on short-duration insurance disclosures (14 August 2014)

• New projects added to FASB and EITF agendas (14 August 2014)

• SEC adopts rules to minimize money market funds’ exposure to rapid redemptions (25 July 2014)

• Boards address sale and leaseback transactions, lessor disclosures (24 July 2014)

• Joint Transition Resource Group for Revenue Recognition debates implementation issues (23 July 2014)

• PCC discusses how to simplify the accounting for intangible assets and other potential projects (17 July 2014)

• Proposals would eliminate extraordinary items and simplify accounting for inventory (17 July 2014)

• Audit committee considerations for the new revenue standard (10 July 2014)

• Awards with targets that affect vesting and that could be achieved after the requisite service period (19 June 2014)

• Boards continue their march toward new leases standard (19 June 2014)

Technical Line • The new revenue recognition standard — retail and consumer

products (26 August 2014) • Using the 2014 XBRL US GAAP Taxonomy (19 June 2014)

• FASB changes accounting for certain repurchase agreements and requires new disclosures (19 June 2014)

• A closer look at the new revenue recognition standard (16 June 2014)

• New revenue standard affects more than just revenue (16 June 2014)

Financial reporting developments • Lease accounting (14 August 2014)

• Consolidated and other financial statements — Noncontrolling interests, combined financial statements, parent company financial statements and consolidating financial statements (23 July 2014)

• Statement of cash flows (21 July 2014)

• Share-based payment (15 July 2014)

• Intangibles — Goodwill and other (9 July 2014)

• Exit or disposal cost obligations (1 July 2014)

• Segment reporting (19 June 2014 )

• Bankruptcies, liquidations and quasi-reorganizations (18 June 2014)

• Joint ventures (12 June 2014)

• Real estate project costs (10 June 2014)

• Real estate sales (10 June 2014)

Comment letters • FASB proposal on Conceptual Framework for Financial Reporting,

Chapter 8: Notes to financial statements (14 July 2014)

• AICPA proposed statement on standards for attestation engagements (23 June 2014)

Other • The JOBS Act: 2014 mid-year update — August 2014

• Second quarter 2014 Standard Setter Update — Financial reporting and accounting developments — July 2014

• SEC in Focus (3 July 2014)

• Quarterly tax developments — June 2014

• Board Matters Quarterly — Critical insights for today’s audit committee — June 2014

• EITF Update — June 2014 meeting highlights

On-demand webcasts • EY Q3 2014 financial reporting update

• The new revenue recognition standard — industry

Upcoming webcasts • SEC comments and trends: current reporting issues

• Accounting for income taxes: a quarterly perspective • Market trends: 2015 outlook IPO and M&A IPO session

Click on any of the EY publications below, all of which are available free of charge on AccountingLink at www.ey.com/us/accountinglink.

EY | Assurance | Tax | Transactions | Advisory

© 2014 Ernst & Young LLP. All Rights Reserved.

SCORE No. BB2834

ey.com/us/accountinglink

About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com. Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US. This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.