eyes on the ground viva industrial trust - cimb · eyes on the ground ... viva industrial trust...

TRANSCRIPT

REIT│Singapore│January 9, 2017

Eyes on the Ground

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Viva Industrial Trust Rose among the thorns

VIT is a Singapore-focused business park and industrial trust. Based on Bloomberg ■estimates, VIT is trading at 9.5% FY17 dividend yield, highest in the sub-sector.

Unlike its small-cap counterparts that reported an average 13.4% yoy decline in ■3Q16 DPU, VIT registered a 9.7% yoy increase in 3Q16 DPU.

Its DPU growth has been driven by acquisitions and AEI at VBP. Management ■expects DPU growth qoq in next few quarters due to rising contribution from VBP.

Risks are: i) non-renewal by McDermott, ii) expiry of rental support for UEBH-■business park component in FY18, and iii) short land lease tenure.

Highest-yielding industrial S-REIT currently VIT is a Singapore-focused business park and industrial trust. Including the proposed acquisition of 6 Chin Bee Avenue, the group has a total of nine assets with AUM of S$1.3bn and aggregate NLA of 3.3m sq ft. As business parks make up 54.2% of the group’s AUM, the group has the highest concentration of business parks among the S-REITs. Based on Bloomberg estimates, VIT is trading at 9.5% FY17 dividend yield, making it the highest-yielding industrial S-REIT currently.

Rose among the thorns In contrast to its small-cap counterparts that reported an average 13.4% yoy decline in 3Q16 DPU (market-cap weighted average), VIT bucked the trend and registered a 9.7% yoy increase in 3Q16 DPU. Its DPU growth has been driven by acquisitions and asset enhancement inititative (AEI) at Viva Business Park (VBP).

AEI at Viva Business Park Recall that in May 15, VIT announced its plan to maximise the “white” space at VBP (15% of total space) and to transform the business park into a “work-play-eat-shop” destination in the Chai Chee neighborhood. Average passing rent for the “white” space is about 2x that of the industrial space. For the next few quarters, management believes there could be DPU growth qoq as 93.4% of the “white” space has been committed. Only 43% of the “white” space contributed to 3Q16 DPU, indicating room for upside.

Inorganic growth with built-in stability Including the proposed acquisition of 6 Chin Bee Avenue, VIT has expanded its initial portfolio of three properties worth S$0.7bn to a total of nine assets worth S$1.3bn. The latest acquisition is expected to be slightly DPU accretive. Additionally, 76.1% of 3Q16 rental income was derived from master lease and full rental support arrangements. Nonetheless, VIT has been working to decrease its reliance on rental support.

Risks I: non-renewal risk Given its high yield, we focus on downside risks. We understand from management that McDermott (top 10 client; accounted for 3.8% of the group’s rental income in Sep 16) would not be renewing its lease in Jackson Square (expires in Apr 17). Downside is mitigated by rental guarantee for Jackson Square (until 2019). Additionally, VIT has partially backfilled the space and does not foresee issues in finding tenants due to Jackson Square’s central location (Toa Payoh).

Risks II: rental support for UEBH, short land lease tenure The rental support for UE BizHub’s (UEBH) business park component expires in Nov 2018. A material gap exists between the passing rent of UEBH and implied rent under the rental support arrangement. In the worst-case scenario, management deems that rising contribution from VBP could offset the absence of income support. Also, VIT has a weighted average land lease of 35.1 years. The manager remains confident of renewing the remaining 15.3-year land lease for VBP (at end-15).

▎Singapore

NON RATED Current price: S$0.76 Consensus Tgt Price: S$0.83 Up/downside: N/A Reuters: VIVA.SI Bloomberg: VIT SP Market cap: US$490.7m S$703.2m Average daily turnover: US$0.29m S$0.41m Current shares o/s: 931.4m Free float: 33.9%

Source: Bloomberg Price performance 1M 3M 12M Absolute (%) -0.7 -3.2 7.1 Relative (%) -1.6 -6.9 -1.3

Major shareholders % held Tong Jinquan 54.2 Ho Lee Group Trust 7.7 China Enterprises Limited 4.4

Analyst(s)

YEO Zhi Bin T (65) 6210 8669 E [email protected] LOCK Mun Yee T (65) 6210 8606 E [email protected]

SOURCE: COMPANY DATA, CIMB , BLOOMBERG

Financial summaryFYE Dec, S$m FY14 FY15 9MFY16 9MFY15Gross property revenue 61.7 74.0 69.6 54.3 Net property income 40.8 50.8 50.4 37.1 NPI margin 66.0% 68.7% 72.5% 68.4%Distributable income 47.5 41.0 45.0 35.0 Asset leverage 44.3% 38.6% 39.8% 38.8%DPS (S cts) 6.83 7.00 5.20 5.37 Dividend yield 9.0% 9.3% 9.2%* 9.5%*BVPS (S cts) 75.8 81.3 80.3 82.7 P/BV (x) 1.00 0.93 0.94 0.91 *Annualised

91.096.0101.0106.0111.0116.0

0.6000.6500.7000.7500.8000.850

Price Close Relative to FSSTI (RHS)

5

10

15

Jan-16 Apr-16 Jul-16 Oct-16

Vol m

REIT│Singapore│Viva Industrial Trust│January 9, 2017

2

Rose among the thorns Company snapshot VIT is a Singapore-focused business park and industrial trust, comprising Viva Industrial Real Estate Investment Trust (VI-REIT) and Viva Industrial Business Trust (VI-BT). Including the proposed acquisition of 6 Chin Bee Avenue, the group currently has a total of nine assets with AUM of S$1.3bn and aggregate NLA of 3.3m sq ft. Management views Viva Business Park (valued at S$330m) and UE BizHub East’s business park component (valued at S$335m) as the jewels in the group’s crown. As business parks make up 54.2% of the group’s current AUM, the group has the highest concentration of business parks among the industrial S-REITs. Post-acquisition, management expects VIT’s gearing to be 39.3%. The key shareholder and sponsors of VIT are Tong Jinquan (54.2% stake), Ho Lee Group (7.7%) and Kim Seng Holdings (4.2%). The group is externally managed, with the REIT manager owned by Maxi Capital Pte Ltd (55.5% stake), Kim Seng (16.7%) and Ho Lee (27.8%).

Rose among the thorns Bucking the trend Supply pressures in the form of lower portfolio occupancy and passing rents, multi-tenanted building (MTB) conversions, as well as the absence of capital distribution and manager’s fees paid in units have resulted in the small-cap industrial SREITs reporting an average 13.4% yoy decline in headline 3Q16 DPU (market-cap weighted average). VIT, however, has bucked this trend and registered a 9.7% yoy increase in its 3Q16 DPU.

To illustrate, VIT’s 3Q16 revenue increased by 31.9% yoy or S$5.9m. 3Q16 revenue growth was driven by the acquisition of 30 Pioneer Road in 2Q16 (which accounted for 19% of the revenue growth), acquisitions of 11 Ubi Road 1 and the Home-Fix Building in 4Q15 (44% of revenue growth) and AEI at Viva Business Park (34% of revenue growth).

Figure 1: Among the small-cap industrial REITs, VIT has bucked the 3Q16 trend by reporting a 9.7% yoy increase in DPU

Figure 2: 3Q16 revenue growth, by key driver (% yoy)

SOURCES: CIMB, COMPANY REPORTS SOURCES: CIMB, COMPANY REPORTS

Organic driver: AEI at Viva Business Park Recall that in May 15, VIT announced its plan to maximise the “white” space (space allowable for mixed uses, 15% of total space) of Viva Business Park (VBP). The asset enhancement initiative (AEI) involved the conversion of unutilised areas (around 230,000 sq ft) into retail and commercial space at three

1.99

1.91 1.89

1.79

1.72

1.65 1.63

1.64

1.75

1.81

1.40

1.50

1.60

1.70

1.80

1.90

2.00

2.10

3Q15 4Q15 1Q16 2Q16 3Q16

VIT Weighted average (by mkt cap) of small-cap industrial REITs

(S cts)

19%

44%

34%

3%

Newly-acquired 30 Pioneer Road

Newly-acquired 11 Ubi Road 1 & Home-Fix Building

AEI at Viva Buisness Park

Others

S$0.2m,

S$2.0m,

S$2.6m,

S$1.1m,

REIT│Singapore│Viva Industrial Trust│January 9, 2017

3

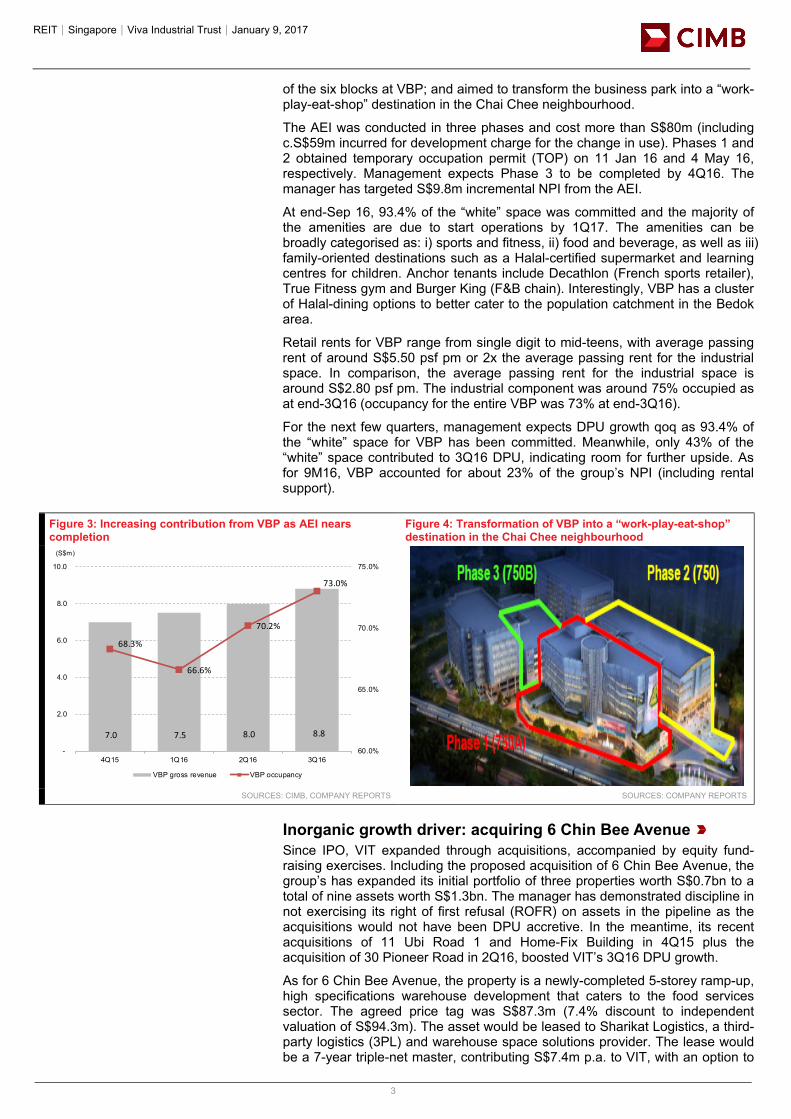

of the six blocks at VBP; and aimed to transform the business park into a “work-play-eat-shop” destination in the Chai Chee neighbourhood.

The AEI was conducted in three phases and cost more than S$80m (including c.S$59m incurred for development charge for the change in use). Phases 1 and 2 obtained temporary occupation permit (TOP) on 11 Jan 16 and 4 May 16, respectively. Management expects Phase 3 to be completed by 4Q16. The manager has targeted S$9.8m incremental NPI from the AEI.

At end-Sep 16, 93.4% of the “white” space was committed and the majority of the amenities are due to start operations by 1Q17. The amenities can be broadly categorised as: i) sports and fitness, ii) food and beverage, as well as iii) family-oriented destinations such as a Halal-certified supermarket and learning centres for children. Anchor tenants include Decathlon (French sports retailer), True Fitness gym and Burger King (F&B chain). Interestingly, VBP has a cluster of Halal-dining options to better cater to the population catchment in the Bedok area.

Retail rents for VBP range from single digit to mid-teens, with average passing rent of around S$5.50 psf pm or 2x the average passing rent for the industrial space. In comparison, the average passing rent for the industrial space is around S$2.80 psf pm. The industrial component was around 75% occupied as at end-3Q16 (occupancy for the entire VBP was 73% at end-3Q16).

For the next few quarters, management expects DPU growth qoq as 93.4% of the “white” space for VBP has been committed. Meanwhile, only 43% of the “white” space contributed to 3Q16 DPU, indicating room for further upside. As for 9M16, VBP accounted for about 23% of the group’s NPI (including rental support).

Figure 3: Increasing contribution from VBP as AEI nears completion

Figure 4: Transformation of VBP into a “work-play-eat-shop” destination in the Chai Chee neighbourhood

SOURCES: CIMB, COMPANY REPORTS SOURCES: COMPANY REPORTS

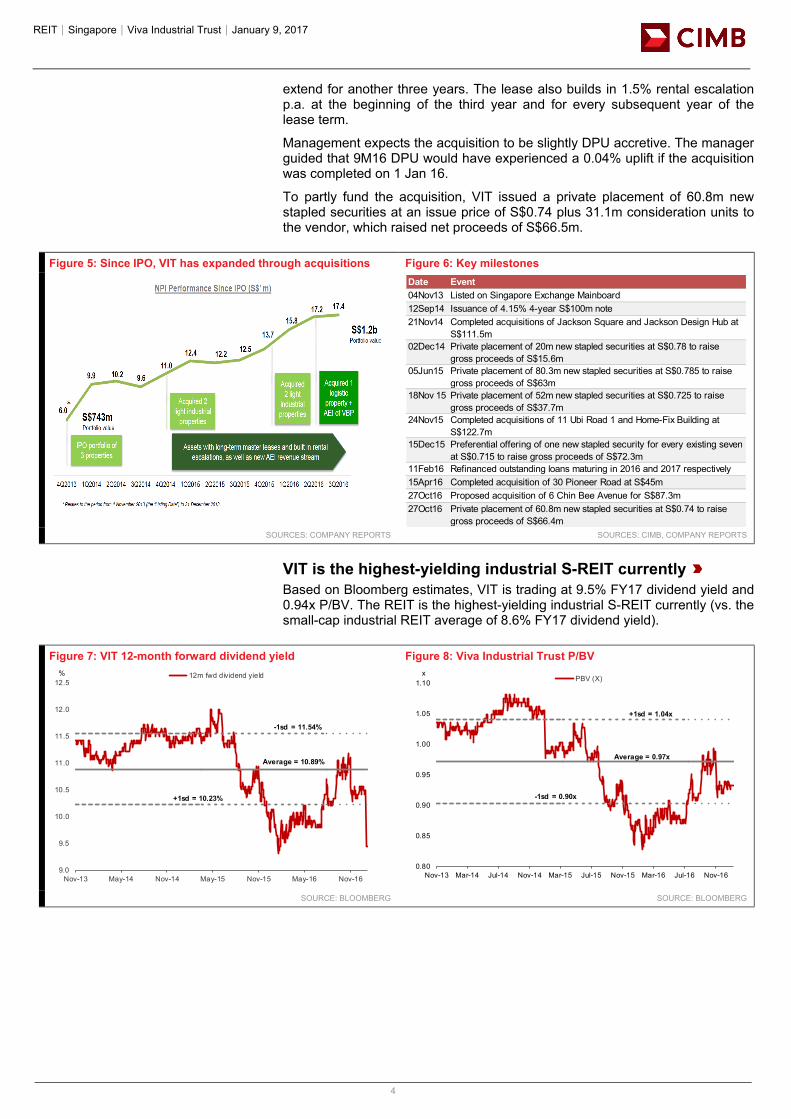

Inorganic growth driver: acquiring 6 Chin Bee Avenue Since IPO, VIT expanded through acquisitions, accompanied by equity fund-raising exercises. Including the proposed acquisition of 6 Chin Bee Avenue, the group’s has expanded its initial portfolio of three properties worth S$0.7bn to a total of nine assets worth S$1.3bn. The manager has demonstrated discipline in not exercising its right of first refusal (ROFR) on assets in the pipeline as the acquisitions would not have been DPU accretive. In the meantime, its recent acquisitions of 11 Ubi Road 1 and Home-Fix Building in 4Q15 plus the acquisition of 30 Pioneer Road in 2Q16, boosted VIT’s 3Q16 DPU growth.

As for 6 Chin Bee Avenue, the property is a newly-completed 5-storey ramp-up, high specifications warehouse development that caters to the food services sector. The agreed price tag was S$87.3m (7.4% discount to independent valuation of S$94.3m). The asset would be leased to Sharikat Logistics, a third-party logistics (3PL) and warehouse space solutions provider. The lease would be a 7-year triple-net master, contributing S$7.4m p.a. to VIT, with an option to

68.3%

66.6%

70.2%

73.0%

7.0 7.5 8.0 8.8

60.0%

65.0%

70.0%

75.0%

-

2.0

4.0

6.0

8.0

10.0

4Q15 1Q16 2Q16 3Q16

VBP gross revenue VBP occupancy

(S$m)

68.3%

66.6%

70.2%

73.0%

7.0 7.5 8.0 8.8

60.0%

65.0%

70.0%

75.0%

-

2.0

4.0

6.0

8.0

10.0

4Q15 1Q16 2Q16 3Q16

VBP gross revenue VBP occupancy

(S$m)

REIT│Singapore│Viva Industrial Trust│January 9, 2017

4

extend for another three years. The lease also builds in 1.5% rental escalation p.a. at the beginning of the third year and for every subsequent year of the lease term.

Management expects the acquisition to be slightly DPU accretive. The manager guided that 9M16 DPU would have experienced a 0.04% uplift if the acquisition was completed on 1 Jan 16.

To partly fund the acquisition, VIT issued a private placement of 60.8m new stapled securities at an issue price of S$0.74 plus 31.1m consideration units to the vendor, which raised net proceeds of S$66.5m.

Figure 5: Since IPO, VIT has expanded through acquisitions Figure 6: Key milestones

SOURCES: COMPANY REPORTS SOURCES: CIMB, COMPANY REPORTS

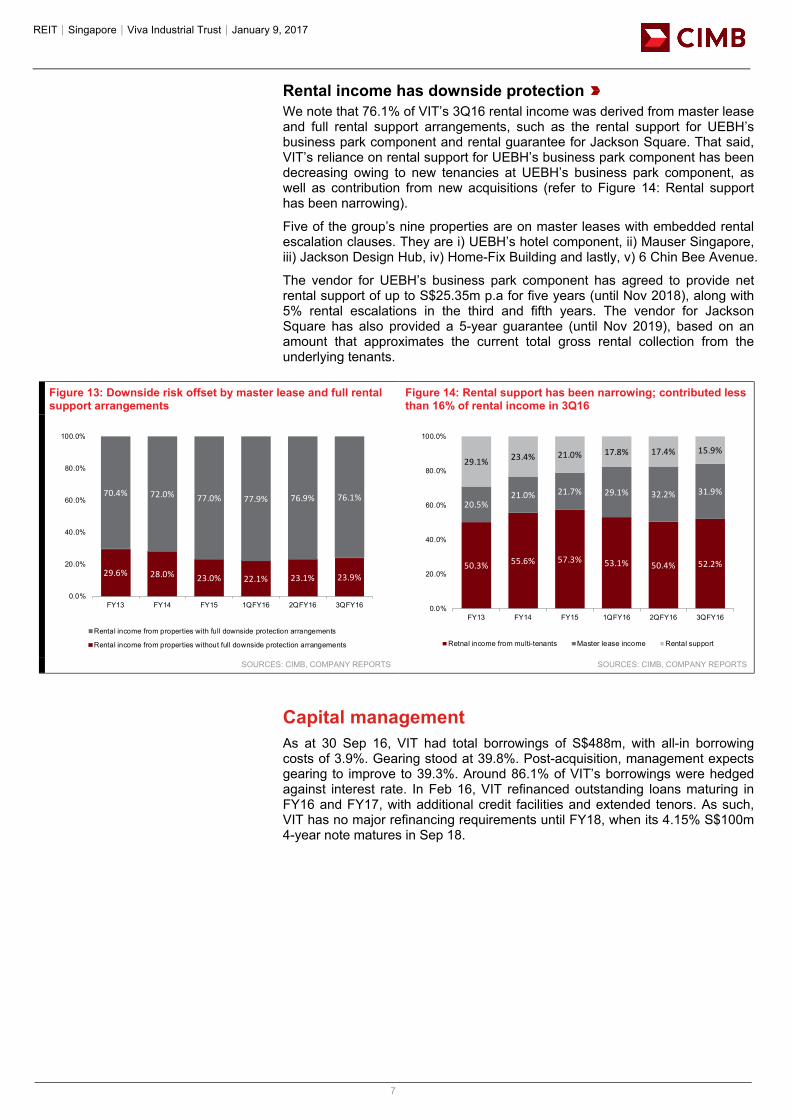

VIT is the highest-yielding industrial S-REIT currently Based on Bloomberg estimates, VIT is trading at 9.5% FY17 dividend yield and 0.94x P/BV. The REIT is the highest-yielding industrial S-REIT currently (vs. the small-cap industrial REIT average of 8.6% FY17 dividend yield).

Figure 7: VIT 12-month forward dividend yield Figure 8: Viva Industrial Trust P/BV

SOURCE: BLOOMBERG SOURCE: BLOOMBERG

7.0 7.5 8.0 8.8

68.3%

66.6%

70.2%

73.0%

60.0%

65.0%

70.0%

75.0%

-

2.0

4.0

6.0

8.0

10.0

4Q15 1Q16 2Q16 3Q16

VBP gross revenue VBP occupancy

(S$m) Date Event04Nov13 Listed on Singapore Exchange Mainboard12Sep14 Issuance of 4.15% 4-year S$100m note21Nov14 Completed acquisitions of Jackson Square and Jackson Design Hub at

S$111.5m 02Dec14 Private placement of 20m new stapled securities at S$0.78 to raise

gross proceeds of S$15.6m05Jun15 Private placement of 80.3m new stapled securities at S$0.785 to raise

gross proceeds of S$63m18Nov 15 Private placement of 52m new stapled securities at S$0.725 to raise

gross proceeds of S$37.7m24Nov15 Completed acquisitions of 11 Ubi Road 1 and Home-Fix Building at

S$122.7m15Dec15 Preferential offering of one new stapled security for every existing seven

at S$0.715 to raise gross proceeds of S$72.3m11Feb16 Refinanced outstanding loans maturing in 2016 and 2017 respectively15Apr16 Completed acquisition of 30 Pioneer Road at S$45m27Oct16 Proposed acquisition of 6 Chin Bee Avenue for S$87.3m27Oct16 Private placement of 60.8m new stapled securities at S$0.74 to raise

gross proceeds of S$66.4m

9.0

9.5

10.0

10.5

11.0

11.5

12.0

12.5

Nov-13 May-14 Nov-14 May-15 Nov-15 May-16 Nov-16

12m fwd dividend yield

Average = 10.89%

-1sd = 11.54%

+1sd = 10.23%

%

0.80

0.85

0.90

0.95

1.00

1.05

1.10

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16

PBV (X)

Average = 0.97x

+1sd = 1.04x

-1sd = 0.90x

x

REIT│Singapore│Viva Industrial Trust│January 9, 2017

5

Figure 9: CIMB REIT/BT Overview

SOURCES: CIMB, COMPANY REPORTS, BLOOMBERG

Property portfolio Property portfolio details VIT currently has a total of nine assets with AUM of S$1.3bn and aggregate NLA of 3.3m sq ft (including the proposed acquisition of 6 Chin Bee Avenue). Management views Viva Business Park (valued at S$330m) and UE BizHub East’s business park component (valued at S$335m) as the jewels in the group’s crown. Business parks make up 54.2% of the group’s current AUM, and the REIT has the highest concentration of business parks among the industrial S-REITs.

In Figure 10, we provide details on VIT’s properties. UE BizHub East’s (UEBH) business park component and VBP are the largest contributors to VIT’s distributable cash flow, accounting for estimated 34% and 23%, respectively, of the group’s 9M16 NPI (including rental support).

SREIT Price as at08 Jan 17

HospitalityAscott Residence Trust ART SP $1.16 $1,333 41.0% 1.30 0.89 $1.11 H 6.8% 7.1% 7.2%Ascendas Hospitality Trust ASCHT SP $0.72 $550 33.2% 0.73 0.98 NA NR 7.6% 7.7% 7.6%CDL Hospitality Trust CDREIT SP $1.39 $962 36.3% 1.57 0.88 $1.30 H 6.6% 6.8% 7.0%Far East Hospitality Trust FEHT SP $0.60 $754 32.8% 0.93 0.65 $0.56 H 7.2% 7.0% 7.2%Frasers Hospitality Trust FHT SP $0.66 $849 38.3% 0.80 0.82 NA NR 8.2% 7.9% 8.1%OUE Hospitality Trust OUEHT SP $0.69 $856 31.2% 0.79 0.87 $0.70 A 6.5% 7.1% 7.3%

Simple Average 35.5% 0.85 7.1% 7.3% 7.4%IndustrialAIMS AMP AAREIT SP $1.34 $593 33.1% 1.53 0.87 NA NR 8.5% 8.5% 8.8%Ascendas REIT AREIT SP $2.38 $4,736 37.0% 2.03 1.17 $2.25 H 6.5% 6.4% 6.4%Cache Logistics Trust CACHE SP $0.82 $514 41.2% 0.83 0.99 $0.74 RD 9.2% 8.7% 8.3%Cambridge Industrial Trust CREIT SP $0.55 $496 36.9% 0.68 0.80 $0.55 H 8.0% 7.9% 8.1%Keppel DC REIT KDCREIT SP $1.21 $950 29.1% 0.92 1.32 $1.18 H 5.1% 5.7% 5.8%Mapletree Industrial Trust MINT SP $1.65 $2,075 29.0% 1.37 1.20 $1.68 A 6.8% 6.9% 6.9%Mapletree Logistics Trust MLT SP $1.04 $1,806 37.6% 0.98 1.06 $1.02 H 7.1% 7.2% 7.4%Sabana Shariah SSREIT SP $0.34 $177 41.5% 0.81 0.42 NA NR 0.0% 0.0% 0.0%Soilbuild Business Space REIT SBREIT SP $0.66 $482 36.0% 0.77 0.86 NA NR 9.2% 9.5% 8.9%Viva Industrial Trust VIT SP $0.76 $489 39.8% 0.80 0.94 NA NR 9.3% 9.5% 10.6%

Simple Average 36.1% 0.92 7.0% 7.0% 7.1%OfficeCapitaLand Commercial Trust CCT SP $1.54 $3,174 37.8% 1.72 0.89 $1.52 H 5.8% 6.1% 6.3%Frasers Commercial Trust FCOT SP $1.27 $705 36.3% 1.55 0.82 $1.26 H 7.8% 7.5% 7.3%Keppel REIT KREIT SP $1.05 $2,412 39.0% 1.41 0.74 $1.02 H 6.4% 6.4% 6.3%OUE Commercial REIT OUECT SP $0.70 $629 40.2% 0.91 0.76 $0.65 H 7.6% 7.6% 7.7%

Simple Average 38.3% 0.80 6.9% 6.9% 6.9%RetailCapitaLand Mall Trust CT SP $1.97 $4,858 35.4% 1.89 1.04 $1.96 H 5.6% 5.5% 5.6%Frasers Centrepoint Trust FCT SP $1.96 $1,255 28.3% 1.93 1.01 $2.01 A 6.0% 6.0% 6.2%Mapletree Commercial Trust MCT SP $1.46 $2,472 37.3% 1.32 1.10 $1.45 H 5.6% 5.7% 5.9%SPH REIT SPHREIT SP $0.97 $1,718 25.7% 0.94 1.03 $0.95 H 5.7% 5.9% 6.0%Starhill Global REIT SGREIT SP $0.77 $1,164 35.0% 0.92 0.83 $0.76 H 6.8% 6.9% 7.1%Suntec REIT SUN SP $1.68 $2,970 37.8% 2.13 0.79 $1.54 RD 6.1% 6.2% 6.2%

Simple Average 33.3% 0.97 6.0% 6.0% 6.2%Retail Ex-SinCapitaLand Retail China Trust CRCT SP $1.41 $852 36.7% 1.58 0.89 NA NR 7.2% 7.9% 7.8%Croesus Retail Trust CRT SP $0.85 $469 44.6% 1.00 0.84 $0.98 A 8.1% 9.4% 9.4%Lippo Malls Indonesia Retail Trust LMRT SP $0.37 $724 27.9% 0.39 0.95 $0.38 H 8.6% 9.1% 9.2%Mapletree Greater China Commercial Trust MAGIC SP $0.96 $1,867 39.9% 1.19 0.81 $1.13 A 7.6% 7.8% 7.9%

Simple Average 37.3% 0.87 7.9% 8.5% 8.6%HealthcareFirst REIT FIRT SP $1.29 $692 30.0% 1.03 1.25 $1.26 H 6.5% 6.5% 6.7%Parkway Life REIT PREIT SP $2.38 $1,005 38.2% 1.67 1.43 $2.53 A 5.1% 5.3% 5.4%RHT Health Trust RHT SP $0.92 $515 19.1% 0.88 1.04 $0.89 H 8.5% 33.3% 6.9%

Simple Average 29.1% 1.24 6.7% 15.0% 6.3%Simple average for SIN 35.0% 0.93 6.8% 7.7% 6.9%

Price / Stated

NAVBloomberg

TickerMkt Cap (US $m)

Last reported

asset leverage

Last stated

NAV

Target Price (DDM-

based) Rec.FY16F

YieldFY18F

YieldFY17F

Yield

REIT│Singapore│Viva Industrial Trust│January 9, 2017

6

Figure 10: Property details

SOURCES: CIMB, COMPANY REPORTS

THE ACQUISITION OF 30 PIONEER ROAD WAS COMPLETED ON 15 APR 2016 WHILE THE ACQUISITION OF 6 CHIN BEE AVENUE HAS NOT BEEN COMPLETED AT THE TIME OF WRITING

Among the industrial sub-asset types such as warehouses and factories, we are most positive on business parks. Given the minimal supply post-2016 and the high pre-commitment levels, we believe that business park rents and capital values are supported by Singapore’s structural shift towards higher-value activities. That said, we foresee some near-term supply pressure after completions peaked in 2016 (refer to Appendix: Business park outlook).

We note that for an area zoned for business park, a maximum of 15% of GFA is allowed for “white” uses, which may include retail shops, offices and restaurants. As for a business park zoned as “business park white”, more than 15% and up to 40% of the development’s overall GFA is allowed for “white” uses.

The land at UEBH is zoned for “business park white” development, while the land at VBP is zoned for “business park”.

As at 30 Sep 16, VIT’s portfolio has a weighted average lease expiry (WALE) of 3.3 years (by rental income), with portfolio occupancy of 88.6% (up from 80.8% at 30 Sep 15). VIT has a diverse set of tenants and sub-tenants from trade sectors, including Cisco System (global IT company), Meiban Group (local precision engineering company), Decathalon (French sporting goods) and NTUC Fair Price (local grocery retailer). Please refer to Figure 20: top 10 customers. About 44% of the group’s tenants are from the IT sector and 18.4% from the engineering sector. Interestingly, VIT has leased out data centre space at VBP (on a shell and core basis) to 1-Net, a government linked data centre operator. 1-Net accounted for around 5% of rental income in Sep 16.

Figure 11: Asset type, by valuation (post-acquisition of 6 Chin Bee Avenue)

Figure 12: Tenant type, by gross rental income (30 Sep 16)

SOURCES: CIMB, COMPANY REPORTS SOURCES: CIMB, COMPANY REPORTS

# Property Property type Valuation (S$m) FY15 gross revenue (S$m)

GFA (sq ft) Building age (yr)

Remaining land lease (yr)

FY15 occupancy (%)

1 UE BizHub EAST - business park component

Business park 355.0 23.5 626,018 3.7 52.1 88.4%

2 UE BizHub EAST - hotel component

Hotel 160.0 9.4 157,397 3.7 52.1 99.5%

3 Viva Business Park Business park 330.0 27.0 1,524,685 19.2 15.3 68.3%4 Mauser Singapore Logsitics 28.0 1.9 107,566 3.5 50.6 100.0%5 Jackson Square Light industrial 82.0 9.0 418,586 6.1 13.4 98.9%6 Jackson Design Hub Light industrial 33.4 2.1 85,070 6.9 51.4 100.0%7 11 Ubi Road 1 Light industrial 87.0 0.7 253,058 18.1 39.7 100.0%8 Home-Fix Building Light industrial 47.8 0.3 120,556 4.6 51.7 100.0%9 30 Pioneer Road Logistics 45.0 na 281,090 6.3 20.1 na10 6 Chin Bee Avenue Logistics 87.3 na 324,166 0.7 26.8 na

Business Park,

54.2%

Hotel, 12.5%

Light Industrial, 19.5%

Logistics, 13.8%

MNC, 58.4%

SME, 36.9%

GLC, 4.7%

REIT│Singapore│Viva Industrial Trust│January 9, 2017

7

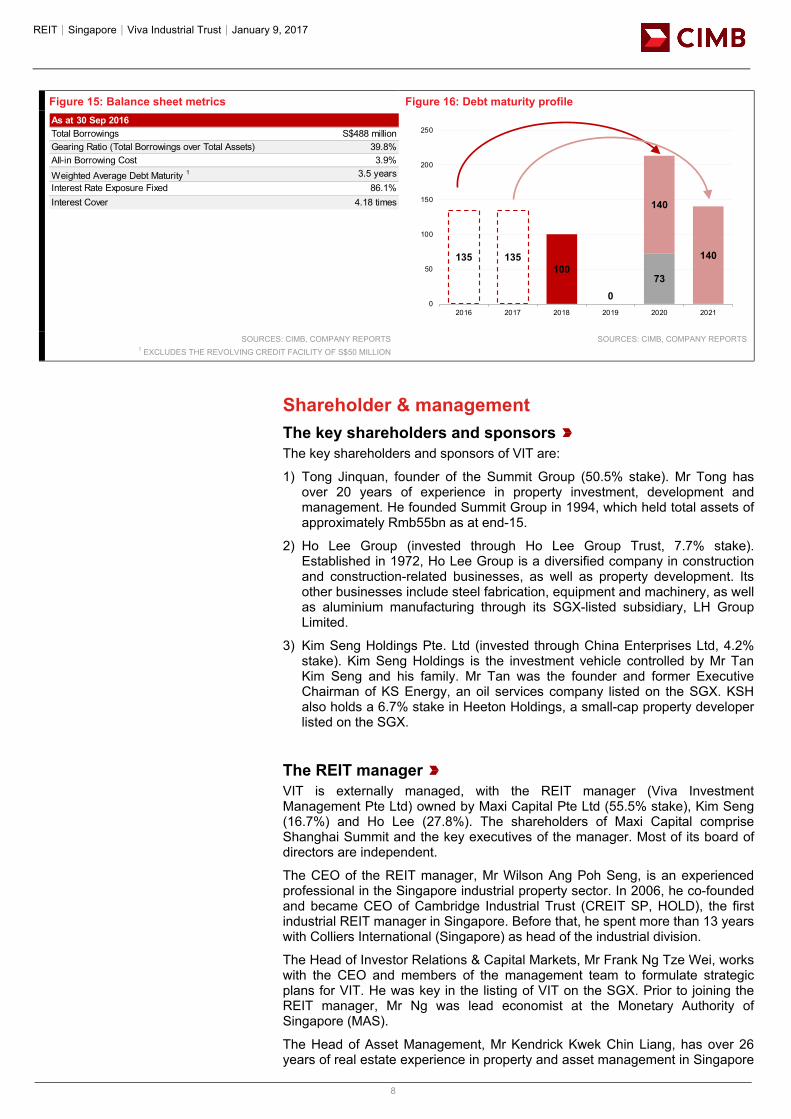

Rental income has downside protection We note that 76.1% of VIT’s 3Q16 rental income was derived from master lease and full rental support arrangements, such as the rental support for UEBH’s business park component and rental guarantee for Jackson Square. That said, VIT’s reliance on rental support for UEBH’s business park component has been decreasing owing to new tenancies at UEBH’s business park component, as well as contribution from new acquisitions (refer to Figure 14: Rental support has been narrowing).

Five of the group’s nine properties are on master leases with embedded rental escalation clauses. They are i) UEBH’s hotel component, ii) Mauser Singapore, iii) Jackson Design Hub, iv) Home-Fix Building and lastly, v) 6 Chin Bee Avenue.

The vendor for UEBH’s business park component has agreed to provide net rental support of up to S$25.35m p.a for five years (until Nov 2018), along with 5% rental escalations in the third and fifth years. The vendor for Jackson Square has also provided a 5-year guarantee (until Nov 2019), based on an amount that approximates the current total gross rental collection from the underlying tenants.

Figure 13: Downside risk offset by master lease and full rental support arrangements

Figure 14: Rental support has been narrowing; contributed less than 16% of rental income in 3Q16

SOURCES: CIMB, COMPANY REPORTS SOURCES: CIMB, COMPANY REPORTS

Capital management As at 30 Sep 16, VIT had total borrowings of S$488m, with all-in borrowing costs of 3.9%. Gearing stood at 39.8%. Post-acquisition, management expects gearing to improve to 39.3%. Around 86.1% of VIT’s borrowings were hedged against interest rate. In Feb 16, VIT refinanced outstanding loans maturing in FY16 and FY17, with additional credit facilities and extended tenors. As such, VIT has no major refinancing requirements until FY18, when its 4.15% S$100m 4-year note matures in Sep 18.

70.4% 72.0% 77.0% 77.9% 76.9% 76.1%

29.6% 28.0% 23.0% 22.1% 23.1% 23.9%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

FY13 FY14 FY15 1QFY16 2QFY16 3QFY16

Rental income from properties with full downside protection arrangements

Rental income from properties without full downside protection arrangements

29.1% 23.4% 21.0% 17.8% 17.4% 15.9%

20.5%21.0% 21.7% 29.1% 32.2% 31.9%

50.3% 55.6% 57.3% 53.1% 50.4% 52.2%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

FY13 FY14 FY15 1QFY16 2QFY16 3QFY16

Retnal income from multi-tenants Master lease income Rental support

REIT│Singapore│Viva Industrial Trust│January 9, 2017

8

Figure 15: Balance sheet metrics Figure 16: Debt maturity profile

SOURCES: CIMB, COMPANY REPORTS

1 EXCLUDES THE REVOLVING CREDIT FACILITY OF S$50 MILLION SOURCES: CIMB, COMPANY REPORTS

Shareholder & management The key shareholders and sponsors The key shareholders and sponsors of VIT are:

1) Tong Jinquan, founder of the Summit Group (50.5% stake). Mr Tong has over 20 years of experience in property investment, development and management. He founded Summit Group in 1994, which held total assets of approximately Rmb55bn as at end-15.

2) Ho Lee Group (invested through Ho Lee Group Trust, 7.7% stake). Established in 1972, Ho Lee Group is a diversified company in construction and construction-related businesses, as well as property development. Its other businesses include steel fabrication, equipment and machinery, as well as aluminium manufacturing through its SGX-listed subsidiary, LH Group Limited.

3) Kim Seng Holdings Pte. Ltd (invested through China Enterprises Ltd, 4.2% stake). Kim Seng Holdings is the investment vehicle controlled by Mr Tan Kim Seng and his family. Mr Tan was the founder and former Executive Chairman of KS Energy, an oil services company listed on the SGX. KSH also holds a 6.7% stake in Heeton Holdings, a small-cap property developer listed on the SGX.

The REIT manager VIT is externally managed, with the REIT manager (Viva Investment Management Pte Ltd) owned by Maxi Capital Pte Ltd (55.5% stake), Kim Seng (16.7%) and Ho Lee (27.8%). The shareholders of Maxi Capital comprise Shanghai Summit and the key executives of the manager. Most of its board of directors are independent.

The CEO of the REIT manager, Mr Wilson Ang Poh Seng, is an experienced professional in the Singapore industrial property sector. In 2006, he co-founded and became CEO of Cambridge Industrial Trust (CREIT SP, HOLD), the first industrial REIT manager in Singapore. Before that, he spent more than 13 years with Colliers International (Singapore) as head of the industrial division.

The Head of Investor Relations & Capital Markets, Mr Frank Ng Tze Wei, works with the CEO and members of the management team to formulate strategic plans for VIT. He was key in the listing of VIT on the SGX. Prior to joining the REIT manager, Mr Ng was lead economist at the Monetary Authority of Singapore (MAS).

The Head of Asset Management, Mr Kendrick Kwek Chin Liang, has over 26 years of real estate experience in property and asset management in Singapore

As at 30 Sep 2016Total Borrowings S$488 millionGearing Ratio (Total Borrowings over Total Assets) 39.8%All-in Borrowing Cost 3.9%Weighted Average Debt Maturity 1 3.5 yearsInterest Rate Exposure Fixed 86.1%Interest Cover 4.18 times

135 135100

073

140

140

0

50

100

150

200

250

2016 2017 2018 2019 2020 2021

REIT│Singapore│Viva Industrial Trust│January 9, 2017

9

and China. He has extensive experience in managing a wide range of real estate portfolios. Prior to joining the REIT manager in May 16, Mr Kwek was Senior Director of Tishman Speyer, where he was the Head of Property Management in China.

Figure 17: VIT sponsors & strategic partners Figure 18: REIT manager structure

SOURCES: CIMB, COMPANY REPORTS SOURCES: CIMB, COMPANY REPORTS

Risks Non-renewal risk As at 30 Sep 16, about 16.1% of VIT’s gross rental income is due for renewal in 2017. We understand that US oil services company, McDermott Asia Pacific will not be renewing its lease on Jackson Square (expires in Apr 17). The non-renewal follows the move by oil services MNCs such as Technip, Subsea 7 and Saipem to relocate their Southeast Asia headquarters from Singapore to Kuala Lumpur. The MNCs want to take advantage of the lower cost base and more importantly, to be closer to strategic clients such as Petronas (Malaysia’s state-owned oil & gas company).

McDermott accounted for around 3.8% of the group’s rental income in Sep 16; and occupies about 109,500 sq ft in Jackson Square (or 23% of its NLA). We understand that a multinational electronics contract manufacturing company has taken up a portion of the McDermott space; and that the signing rent was on par with McDermott’s.

In addition, Jackson Square is located in Toa Payoh, the central region of Singapore. Hence, the manager does not foresee any issues in backfilling the vacant space. Lastly, Jackson Square has a rental guarantee in place that would protect VIT from any drop in rental income until 2019.

On MTB conversions risks, we note that the Mauser Singapore master lease will expire in 2019, with an option to renew for another five years.

1. Investment holding company of sponsor Kim Seng Holdings2. Shareholdings as at 10 October 2016.3. 1 stapled security comprises 1 unit in VI-REIT and 1 unit in VI-BT.4. VI-BT will remain dormant and exist primarily as a "lessee of last resort".

Ho Lee Group Trust (“HLGT”)

China Enterprises

Limited (“CEL”)1

Other Stapled SecurityholdersTong Jinquan

54.2%2 7.7%2 4.2%2 33.9%2

Stapling Deed

VIT3

VI-REIT VI-BT 4

Maxi Capital Pte. Ltd

Sponsor: Kim Seng Holdings Pte. Ltd.

Sponsor: Ho Lee Group Pte. Ltd.

Viva Investment Management Pte. Ltd.

55.5% 27.8%

VITM (VI-REIT Manager)

VAM (VI-BT Trustee Manager)

16.7%

100%

REIT│Singapore│Viva Industrial Trust│January 9, 2017

10

Figure 19: Lease expiry, by gross rental income (30 Sep 16) Figure 20: Top 10 customers accounted for 43.2% of monthly committed rental income in Sep 16

SOURCES: CIMB, COMPANY REPORTS SOURCES: CIMB, COMPANY REPORTS

Rental support for UEBH expires in FY18 The rental support for UEBH’s business park component expires in Nov 2018.

In 9M16, UEBH’s business park component contributed around S$12m to NPI, while rental support for UEBH was around S$8m. We understand from management that the average passing rent of c.S$4.50 psf pm and occupancy of c.90% underpinned the S$12m NPI contribution. Including the rental support, this implies that the average passing rent for UEBH’s business park component is around S$5.90 psf pm (vs. spot rent of S$5.60 for comparable properties in Changi Business Park) and occupancy rate is 95%. This also means that VIT needs to increase UEBH’s passing rent by 30% in two years (or by FY18) and raise occupancy by 5% to achieve the desired stabilised state.

In mitigation, the completion of the new Downtown Line in 3Q17 would increase the accessibility of UEBH, and enable VIT to negotiate for higher rents, closer to the spot rate of S$5.60 when it renews leases in 2017-18. Additionally, some of the shortfall could be partially offset by an additional S$1m p.a. in NPI from UEBH’s hotel component (function of the 10-year master lease agreement that started in Nov 13).

In the worst-case scenario of VIT being unable to bridge the rental gap of S$4.50 and S$5.90, the manager deems that increasing contribution from VBP should offset the absence of income support for UEBH’s business park component. This could result in a plateau for DPU profile, rather than an increasing one (refer to Figure 1).

Short land lease tenure VIT has a weighted average land lease (by valuation) of 35.1 years. Of note, VBP has a remaining land lease of 15.3 years (as at end-15). The implication of shorter land tenure is that it could restrict industrial end-users’ longer-term business planning, making the space less attractive to them. In addition, we understand that the valuers are likely to treat properties with land lease tenure of less than 10 years as depreciating assets. This could spell NAV erosion.

The manager remains confident that the land lease for VBP will be renewed. The renewal of land lease depends on the Urban Redevelopment Authority’s (URA) master plan zoning, as well as the site owner’s investment commitment.

In the Master Plan 2008, VBP was rezoned from High-Tech Industrial to Business Park. The rezoning took into account the site’s location within mature residential estates and the shifting profile of businesses that are likely to locate there. In addition, VIT has invested more than S$80m in VBP’s AEI to utilise the “white” component of the development, converting industrial space into retail and office space.

0.3%

16.1%

18.7%

35.0%

29.9%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

FY16 FY17 FY18 FY19 FY20 & beyond

6.9%

5.7%5.2% 5.0%

4.1% 3.8% 3.6% 3.6%

2.9%2.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

REIT│Singapore│Viva Industrial Trust│January 9, 2017

11

Hence, the manager remains confident that the land lease for VBP will be renewed. It believes that there is potential upside to VBP’s value from the land lease being extended.

Appendix: Business park outlook We deem business parks as the pinnacle of industrial space sophistication and a real estate proxy for Singapore’s shift towards higher value-added activities. Business park buildings are located in government-identified zones called “Business Parks”, which accommodate various amenities such as food and beverage outlets, convenience stores and childcare centres. The business park buildings are high-rise, multi-tenanted buildings located in a landscaped environment. The concentration of companies from the same sector allow for greater economies of scale from shared infrastructure.

As at end-3Q16, Singapore had a total of 23m sq ft of business park space. After a sizeable 2.37m sq ft of completions in 9M16 (prominent completions included Ascent at the Singapore Science Park and MBC II), supply in the pipeline is expected to stay low in 2017. According to the JTC, around 0.28m sq ft of supply (assuming 80% efficiency) or 1.2% of the existing stock is expected to be completed between now to 2018. There is notable incoming supply in the form of purpose-built business park being developed by BP-Vista, a JV between Boustead Singapore and a Middle-Eastern sovereign wealth fund, in 4Q16.

As a result of the supply peak in 2016, we expect island-wide occupancy to fall to 80.2% in 2016 (2015: 84.1%). However, assuming a moving 5-year average net absorption, occupancy is expected to recover to 90.2% in 2018. Furthermore, we understand that the developments under construction are 100% pre-committed.

Amid limited supply and expected recovery of the office market, we expect business park rents to strengthen in 2H17/2018. As at end-3Q16, business park median monthly rent stood at S$4.25 psf pm, an improvement of c.5% from end-2015.

Figure 21: Annual supply, net absorption and occupancy of business parks island-wide

Figure 22: Average rents for business parks have been stable

SOURCES: CIMB, URA SOURCES: CIMB, CBRE

60

65

70

75

80

85

90

95

100

-50

0

50

100

150

200

250

Annual supply ('000 sq m) Annual demand ('000 sq m)

Occupancy (%, RHS)

5-yr ave. supply: 104k sq m

3-yr fwd ave. supply: 82k sq m

2.50

3.00

3.50

4.00

4.50

5.00

5.50

6.00

Business Park (city fringe) Business Park (Rest of the Island)

(S$ psf pm)

REIT│Singapore│Viva Industrial Trust│January 9, 2017

12

DISCLAIMER #02 The content of this report (including the views and opinions expressed therein, and the information comprised therein) has been prepared by and belongs to CIMB and is distributed by CIMB. This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. By accepting this report, the recipient hereof represents and warrants that he is entitled to receive such report in accordance with the restrictions set forth below and agrees to be bound by the limitations contained herein (including the “Restrictions on Distributions” set out below). Any failure to comply with these limitations may constitute a violation of law. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this report may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMB. The information contained in this research report is prepared from data believed to be correct and reliable at the time of issue of this report. CIMB may or may not issue regular reports on the subject matter of this report at any frequency and may cease to do so or change the periodicity of reports at any time. CIMB is under no obligation to update this report in the event of a material change to the information contained in this report. CIMB has no, and will not accept any, obligation to (i) check or ensure that the contents of this report remain current, reliable or relevant, (ii) ensure that the content of this report constitutes all the information a prospective investor may require, (iii) ensure the adequacy, accuracy, completeness, reliability or fairness of any views, opinions and information, and accordingly, CIMB, or any of their respective affiliates, or its related persons (and their respective directors, associates, connected persons and/or employees) shall not be liable in any manner whatsoever for any consequences (including but not limited to any direct, indirect or consequential losses, loss of profits and damages) of any reliance thereon or usage thereof. In particular, CIMB disclaims all responsibility and liability for the views and opinions set out in this report. Unless otherwise specified, this report is based upon sources which CIMB considers to be reasonable. Such sources will, unless otherwise specified, for market data, be market data and prices available from the main stock exchange or market where the relevant security is listed, or, where appropriate, any other market. Information on the accounts and business of company(ies) will generally be based on published statements of the company(ies), information disseminated by regulatory information services, other publicly available information and information resulting from our research. Whilst every effort is made to ensure that statements of facts made in this report are accurate, all estimates, projections, forecasts, expressions of opinion and other subjective judgments contained in this report are based on assumptions considered to be reasonable as of the date of the document in which they are contained and must not be construed as a representation that the matters referred to therein will occur. Past performance is not a reliable indicator of future performance. The value of investments may go down as well as up and those investing may, depending on the investments in question, lose more than the initial investment. No report shall constitute an offer or an invitation by or on behalf of CIMB or its affiliates to any person to buy or sell any investments. CIMB, its affiliates and related companies, their directors, associates, connected parties and/or employees may own or have positions in securities of the company(ies) covered in this research report or any securities related thereto and may from time to time add to or dispose of, or may be materially interested in, any such securities. Further, CIMB, its affiliates and its related companies do and seek to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities of such company(ies), may sell them to or buy them from customers on a principal basis and may also perform or seek to perform significant investment banking, advisory, underwriting or placement services for or relating to such company(ies) as well as solicit such investment, advisory or other services from any entity mentioned in this report. CIMB or its affiliates may enter into an agreement with the company(ies) covered in this report relating to the production of research reports. CIMB may disclose the contents of this report to the company(ies) covered by it and may have amended the contents of this report following such disclosure. The analyst responsible for the production of this report hereby certifies that the views expressed herein accurately and exclusively reflect his or her personal views and opinions about any and all of the issuers or securities analysed in this report and were prepared independently and autonomously. No part of the compensation of the analyst(s) was, is, or will be directly or indirectly related to the inclusion of specific recommendations(s) or view(s) in this report. CIMB prohibits the analyst(s) who prepared this research report from receiving any compensation, incentive or bonus based on specific investment banking transactions or for providing a specific recommendation for, or view of, a particular company. Information barriers and other arrangements may be established where necessary to prevent conflicts of interests arising. However, the analyst(s) may receive compensation that is based on his/their coverage of company(ies) in the performance of his/their duties or the performance of his/their recommendations and the research personnel involved in the preparation of this report may also participate in the solicitation of the businesses as described above. In reviewing this research report, an investor should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest. Additional information is, subject to the duties of confidentiality, available on request. Reports relating to a specific geographical area are produced by the corresponding CIMB entity as listed in the table below. The term “CIMB” shall denote, where appropriate, the relevant entity distributing or disseminating the report in the particular jurisdiction referenced below, or, in every other case, CIMB Group Holdings Berhad ("CIMBGH") and its affiliates, subsidiaries and related companies.

Country CIMB Entity Regulated by Hong Kong CIMB Securities Limited Securities and Futures Commission Hong Kong India CIMB Securities (India) Private Limited Securities and Exchange Board of India (SEBI) Indonesia PT CIMB Securities Indonesia Financial Services Authority of Indonesia Malaysia CIMB Investment Bank Berhad Securities Commission Malaysia Singapore CIMB Research Pte. Ltd. Monetary Authority of Singapore South Korea CIMB Securities Limited, Korea Branch Financial Services Commission and Financial Supervisory Service Taiwan CIMB Securities Limited, Taiwan Branch Financial Supervisory Commission Thailand CIMB Securities (Thailand) Co. Ltd. Securities and Exchange Commission Thailand

REIT│Singapore│Viva Industrial Trust│January 9, 2017

13

(i) As of January 8, 2017, CIMB has a proprietary position in the securities (which may include but not limited to shares, warrants, call warrants and/or any other derivatives) in the following company or companies covered or recommended in this report: (a) Ascendas REIT, Ascott Residence Trust, Cache Logistics Trust, Cambridge Industrial Trust, CapitaLand Commercial Trust, CapitaLand Mall Trust, Croesus Retail Trust, Frasers Centrepoint Trust, Frasers Commercial Trust, Keppel DC REIT, Keppel REIT, Lippo Malls Indonesia Retail Trust, Mapletree Commercial Trust, Mapletree Greater China Commercial Trust, Mapletree Industrial Trust, Mapletree Logistics Trust, OUE Commercial REIT, OUE Hospitality Trust, Parkway Life REIT, SPH REIT, Starhill Global REIT, Suntec REIT, Viva Industrial Trust (ii) As of January 9, 2017, the analyst(s) who prepared this report, and the associate(s), has / have an interest in the securities (which may include but not limited to shares, warrants, call warrants and/or any other derivatives) in the following company or companies covered or recommended in this report: (a) -

This report does not purport to contain all the information that a prospective investor may require. CIMB or any of its affiliates does not make any guarantee, representation or warranty, express or implied, as to the adequacy, accuracy, completeness, reliability or fairness of any such information and opinion contained in this report. Neither CIMB nor any of its affiliates nor its related persons shall be liable in any manner whatsoever for any consequences (including but not limited to any direct, indirect or consequential losses, loss of profits and damages) of any reliance thereon or usage thereof. This report is general in nature and has been prepared for information purposes only. It is intended for circulation amongst CIMB and its affiliates’ clients generally and does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. The information and opinions in this report are not and should not be construed or considered as an offer, recommendation or solicitation to buy or sell the subject securities, related investments or other financial instruments or any derivative instrument, or any rights pertaining thereto. Investors are advised to make their own independent evaluation of the information contained in this research report, consider their own individual investment objectives, financial situation and particular needs and consult their own professional and financial advisers as to the legal, business, financial, tax and other aspects before participating in any transaction in respect of the securities of company(ies) covered in this research report. The securities of such company(ies) may not be eligible for sale in all jurisdictions or to all categories of investors.

Australia: Despite anything in this report to the contrary, this research is provided in Australia by CIMB Securities (Singapore) Pte. Ltd. and CIMB Securities Limited. This research is only available in Australia to persons who are “wholesale clients” (within the meaning of the Corporations Act 2001 (Cth) and is supplied solely for the use of such wholesale clients and shall not be distributed or passed on to any other person. You represent and warrant that if you are in Australia, you are a “wholesale client”. This research is of a general nature only and has been prepared without taking into account the objectives, financial situation or needs of the individual recipient. CIMB Securities (Singapore) Pte. Ltd. and CIMB Securities Limited do not hold, and are not required to hold an Australian financial services licence. CIMB Securities (Singapore) Pte. Ltd. and CIMB Securities Limited rely on “passporting” exemptions for entities appropriately licensed by the Monetary Authority of Singapore (under ASIC Class Order 03/1102) and the Securities and Futures Commission in Hong Kong (under ASIC Class Order 03/1103). Canada: This research report has not been prepared in accordance with the disclosure requirements of Dealer Member Rule 3400 – Research Restrictions and Disclosure Requirements of the Investment Industry Regulatory Organization of Canada. For any research report distributed by CIBC, further disclosures related to CIBC conflicts of interest can be found at https://researchcentral.cibcwm.com . China: For the purpose of this report, the People’s Republic of China (“PRC”) does not include the Hong Kong Special Administrative Region, the Macau Special Administrative Region or Taiwan. The distributor of this report has not been approved or licensed by the China Securities Regulatory Commission or any other relevant regulatory authority or governmental agency in the PRC. This report contains only marketing information. The distribution of this report is not an offer to buy or sell to any person within or outside PRC or a solicitation to any person within or outside of PRC to buy or sell any instruments described herein. This report is being issued outside the PRC to a limited number of institutional investors and may not be provided to any person other than the original recipient and may not be reproduced or used for any other purpose. France: Only qualified investors within the meaning of French law shall have access to this report. This report shall not be considered as an offer to subscribe to, or used in connection with, any offer for subscription or sale or marketing or direct or indirect distribution of financial instruments and it is not intended as a solicitation for the purchase of any financial instrument. Germany: This report is only directed at persons who are professional investors as defined in sec 31a(2) of the German Securities Trading Act (WpHG). This publication constitutes research of a non-binding nature on the market situation and the investment instruments cited here at the time of the publication of the information. The current prices/yields in this issue are based upon closing prices from Bloomberg as of the day preceding publication. Please note that neither the German Federal Financial Supervisory Agency (BaFin), nor any other supervisory authority exercises any control over the content of this report. Hong Kong: This report is issued and distributed in Hong Kong by CIMB Securities Limited (“CHK”) which is licensed in Hong Kong by the Securities and Futures Commission for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 6 (advising on corporate finance) activities. Any investors wishing to purchase or otherwise deal in the securities covered in this report should contact the Head of Sales at CIMB Securities Limited. The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Conduct Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CHK has no obligation to update its opinion or the information in this research report. This publication is strictly confidential and is for private circulation only to clients of CHK. CIMB Securities Limited does not make a market on the securities mentioned in the report.

India: This report is issued and distributed in India by CIMB Securities (India) Private Limited (”CIMB India") which is registered with SEBI as a stock-broker under the Securities and Exchange Board of India (Stock Brokers and Sub-Brokers) Regulations, 1992, the Securities and Exchange Board of India (Research Analyst) Regulations, 2014 (SEBI Registration Number INH000000669) and in accordance with the provisions of Regulation 4 (g) of the Securities and Exchange Board of India (Investment Advisers) Regulations, 2013, CIMB India is not required

REIT│Singapore│Viva Industrial Trust│January 9, 2017

14

to seek registration with SEBI as an Investment Adviser. The research analysts, strategists or economists principally responsible for the preparation of this research report are segregated from equity stock broking and merchant banking of CIMB India and they have received compensation based upon various factors, including quality, accuracy and value of research, firm profitability or revenues, client feedback and competitive factors. Research analysts', strategists' or economists' compensation is not linked to investment banking or capital markets transactions performed or proposed to be performed by CIMB India or its affiliates.” Indonesia: This report is issued and distributed by PT CIMB Securities Indonesia (“CIMBI”). The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Conduct Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMBI has no obligation to update its opinion or the information in this research report. Neither this report nor any copy hereof may be distributed in Indonesia or to any Indonesian citizens wherever they are domiciled or to Indonesian residents except in compliance with applicable Indonesian capital market laws and regulations. This research report is not an offer of securities in Indonesia. The securities referred to in this research report have not been registered with the Financial Services Authority (Otoritas Jasa Keuangan) pursuant to relevant capital market laws and regulations, and may not be offered or sold within the territory of the Republic of Indonesia or to Indonesian citizens through a public offering or in circumstances which constitute an offer within the meaning of the Indonesian capital market law and regulations. Ireland: CIMB is not an investment firm authorised in the Republic of Ireland and no part of this document should be construed as CIMB acting as, or otherwise claiming or representing to be, an investment firm authorised in the Republic of Ireland. Malaysia: This report is issued and distributed by CIMB Investment Bank Berhad (“CIMB”) solely for the benefit of and for the exclusive use of our clients. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Conduct Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMB has no obligation to update, revise or reaffirm its opinion or the information in this research reports after the date of this report. New Zealand: In New Zealand, this report is for distribution only to persons who are wholesale clients pursuant to section 5C of the Financial Advisers Act 2008. Singapore: This report is issued and distributed by CIMB Research Pte Ltd (“CIMBR”). CIMBR is a financial adviser licensed under the Financial Advisers Act, Cap 110 (“FAA”) for advising on investment products, by issuing or promulgating research analyses or research reports, whether in electronic, print or other form. Accordingly CIMBR is a subject to the applicable rules under the FAA unless it is able to avail itself to any prescribed exemptions. Recipients of this report are to contact CIMB Research Pte Ltd, 50 Raffles Place, #19-00 Singapore Land Tower, Singapore in respect of any matters arising from, or in connection with this report. CIMBR has no obligation to update its opinion or the information in this research report. This publication is strictly confidential and is for private circulation only. If you have not been sent this report by CIMBR directly, you may not rely, use or disclose to anyone else this report or its contents. If the recipient of this research report is not an accredited investor, expert investor or institutional investor, CIMBR accepts legal responsibility for the contents of the report without any disclaimer limiting or otherwise curtailing such legal responsibility. If the recipient is an accredited investor, expert investor or institutional investor, the recipient is deemed to acknowledge that CIMBR is exempt from certain requirements under the FAA and its attendant regulations, and as such, is exempt from complying with the following : (a) Section 25 of the FAA (obligation to disclose product information); (b) Section 27 (duty not to make recommendation with respect to any investment product without having a reasonable basis where you may be reasonably expected to rely on the recommendation) of the FAA; (c) MAS Notice on Information to Clients and Product Information Disclosure [Notice No. FAA-N03]; (d) MAS Notice on Recommendation on Investment Products [Notice No. FAA-N16]; (e) Section 36 (obligation on disclosure of interest in securities), and (f) any other laws, regulations, notices, directive, guidelines, circulars and practice notes which are relates to the above, to the extent permitted by applicable laws, as may be amended from time to time, and any other laws, regulations, notices, directive, guidelines, circulars, and practice notes as we may notify you from time to time. In addition, the recipient who is an accredited investor, expert investor or institutional investor acknowledges that a CIMBR is exempt from Section 27 of the FAA, the recipient will also not be able to file a civil claim against CIMBR for any loss or damage arising from the recipient’s reliance on any recommendation made by CIMBR which would otherwise be a right that is available to the recipient under Section 27 of the FAA, the recipient will also not be able to file a civil claim against CIMBR for any loss or damage arising from the recipient’s reliance on any recommendation made by CIMBR which would otherwise be a right that is available to the recipient under Section 27 of the FAA. CIMB Research Pte Ltd ("CIMBR"), its affiliates and related companies, their directors, associates, connected parties and/or employees may own or have positions in securities of the company(ies) covered in this research report or any securities related thereto and may from time to time add to or dispose of, or may be materially interested in, any such securities. Further, CIMBR, its affiliates and its related companies do and seek to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities of such company(ies), may sell them to or buy them from customers on a principal basis and may also perform or seek to perform significant investment banking, advisory, underwriting or placement services for or relating to such company(ies) as well as solicit such investment, advisory or other services from any entity mentioned in this report. As of January 8, 2017, CIMBR does not have a proprietary position in the recommended securities in this report. CIMB Securities Singapore Pte Ltd and/or CIMB Bank Berhad have/has had an investment banking relationship with Ascott Residence Trust within the preceding 12 months. CIMB Securities Singapore Pte Ltd and/or CIMB Bank does not make a market on the securities mentioned in the report.

South Korea: This report is issued and distributed in South Korea by CIMB Securities Limited, Korea Branch (“CIMB Korea”) which is licensed

REIT│Singapore│Viva Industrial Trust│January 9, 2017

15

as a cash equity broker, and regulated by the Financial Services Commission and Financial Supervisory Service of Korea. In South Korea, this report is for distribution only to professional investors under Article 9(5) of the Financial Investment Services and Capital Market Act of Korea (“FSCMA”). Spain: This document is a research report and it is addressed to institutional investors only. The research report is of a general nature and not personalised and does not constitute investment advice so, as the case may be, the recipient must seek proper advice before adopting any investment decision. This document does not constitute a public offering of securities. CIMB is not registered with the Spanish Comision Nacional del Mercado de Valores to provide investment services. Sweden: This report contains only marketing information and has not been approved by the Swedish Financial Supervisory Authority. The distribution of this report is not an offer to sell to any person in Sweden or a solicitation to any person in Sweden to buy any instruments described herein and may not be forwarded to the public in Sweden. Switzerland: This report has not been prepared in accordance with the recognized self-regulatory minimal standards for research reports of banks issued by the Swiss Bankers’ Association (Directives on the Independence of Financial Research). Taiwan: This research report is not an offer or marketing of foreign securities in Taiwan. The securities as referred to in this research report have not been and will not be registered with the Financial Supervisory Commission of the Republic of China pursuant to relevant securities laws and regulations and may not be offered or sold within the Republic of China through a public offering or in circumstances which constitutes an offer or a placement within the meaning of the Securities and Exchange Law of the Republic of China that requires a registration or approval of the Financial Supervisory Commission of the Republic of China. Thailand: This report is issued and distributed by CIMB Securities (Thailand) Company Limited (“CIMBS”) based upon sources believed to be reliable (but their accuracy, completeness or correctness is not guaranteed). The statements or expressions of opinion herein were arrived at after due and careful consideration for use as information for investment. Such opinions are subject to change without notice and CIMBS has no obligation to update its opinion or the information in this research report. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Conduct Authority apply to a recipient, our obligations owed to such recipient are unaffected. CIMB Securities (Thailand) Co., Ltd. may act or acts as Market Maker, and issuer and offerer of Derivative Warrants and Structured Note which may have the following securities as its underlying securities. Investors should carefully read and study the details of the derivative warrants in the prospectus before making investment decisions. AAV, ADVANC, AMATA, ANAN, AOT, AP, BA, BANPU, BBL, BCH, BCP, BDMS, BEAUTY, BEC, BEM, BH, BJCHI, BLA, BLAND, BTS, CBG, CENTEL, CHG, CK, CKP, COM7, CPALL, CPF, CPN, DELTA, DTAC, EGCO, EPG, ERW, GL, GLOBAL, GLOW, GPSC, GUNKUL, HANA, HMPRO, ICHI, IFEC, INTUCH, IRPC, ITD, IVL, JWD, KBANK, KCE, KKP, KTB, KTC, LH, LHBANK, LPN, MAJOR, MINT, MTLS, PLANB, PS, PTG, PTT, PTTEP, PTTGC, QH, ROBINS, RS, S, SAMART, SAWAD, SCB, SCC, SGP, SIRI, SPALI, SPCG, STEC, STPI, SVI, TASCO, TCAP, THAI, THCOM, TISCO, TMB, TOP, TPIPL, TRC, TRUE, TTA, TTCL, TTW, TU, TVO, UNIQ, VGI, VNG, WHA, WORK. Corporate Governance Report: The disclosure of the survey result of the Thai Institute of Directors Association (“IOD”) regarding corporate governance is made pursuant to the policy of the Office of the Securities and Exchange Commission. The survey of the IOD is based on the information of a company listed on the Stock Exchange of Thailand and the Market for Alternative Investment disclosed to the public and able to be accessed by a general public investor. The result, therefore, is from the perspective of a third party. It is not an evaluation of operation and is not based on inside information. The survey result is as of the date appearing in the Corporate Governance Report of Thai Listed Companies. As a result, the survey result may be changed after that date. CIMBS does not confirm nor certify the accuracy of such survey result.

Score Range: 90 - 100 80 - 89 70 - 79 Below 70 or No Survey Result Description: Excellent Very Good Good N/A

United Arab Emirates: The distributor of this report has not been approved or licensed by the UAE Central Bank or any other relevant licensing authorities or governmental agencies in the United Arab Emirates. This report is strictly private and confidential and has not been reviewed by, deposited or registered with UAE Central Bank or any other licensing authority or governmental agencies in the United Arab Emirates. This report is being issued outside the United Arab Emirates to a limited number of institutional investors and must not be provided to any person other than the original recipient and may not be reproduced or used for any other purpose. Further, the information contained in this report is not intended to lead to the sale of investments under any subscription agreement or the conclusion of any other contract of whatsoever nature within the territory of the United Arab Emirates. United Kingdom: In the United Kingdom and European Economic Area, this report is being disseminated by CIMB Securities (UK) Limited (“CIMB UK”). CIMB UK is authorized and regulated by the Financial Conduct Authority and its registered office is at 27 Knightsbridge, London, SW1X7YB. Unless specified to the contrary, this report has been issued and approved for distribution in the U.K. and the EEA by CIMB UK. Investment research issued by CIMB UK has been prepared in accordance with CIMB Group’s policies for managing conflicts of interest arising as a result of publication and distribution of investment research. This report is for distribution only to, and is solely directed at, selected persons on the basis that those persons: (a) are eligible counterparties and professional clients of CIMB UK; (b) have professional experience in matters relating to investments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended, the “Order”), (c) fall within Article 49(2)(a) to (d) (“high net worth companies, unincorporated associations etc”) of the Order; (d) are outside the United Kingdom subject to relevant regulation in each jurisdiction, or (e) are persons to whom an invitation or inducement to engage in investment activity (within the meaning of section 21 of the Financial Services and Markets Act 2000) in connection with any investments to which this report relates may otherwise lawfully be communicated or caused to be communicated (all such persons together being referred to as “relevant persons”). This report is directed only at relevant persons and must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this report relates is available only to relevant persons and will be engaged in only with relevant persons. Where this report is labelled as non-independent, it does not provide an impartial or objective assessment of the subject matter and does not

REIT│Singapore│Viva Industrial Trust│January 9, 2017

16

constitute independent “investment research” under the applicable rules of the Financial Conduct Authority in the UK. Consequently, any such non-independent report will not have been prepared in accordance with legal requirements designed to promote the independence of investment research and will not subject to any prohibition on dealing ahead of the dissemination of investment research. Any such non-independent report must be considered as a marketing communication. United States: This research report is distributed in the United States of America by CIMB Securities (USA) Inc, a U.S. registered broker-dealer and a related company of CIMB Research Pte Ltd, CIMB Investment Bank Berhad, PT CIMB Securities Indonesia, CIMB Securities (Thailand) Co. Ltd, CIMB Securities Limited, CIMB Securities (India) Private Limited, and is distributed solely to persons who qualify as “U.S. Institutional Investors” as defined in Rule 15a-6 under the Securities and Exchange Act of 1934. This communication is only for Institutional Investors whose ordinary business activities involve investing in shares, bonds, and associated securities and/or derivative securities and who have professional experience in such investments. Any person who is not a U.S. Institutional Investor or Major Institutional Investor must not rely on this communication. The delivery of this research report to any person in the United States of America is not a recommendation to effect any transactions in the securities discussed herein, or an endorsement of any opinion expressed herein. CIMB Securities (USA) Inc, is a FINRA/SIPC member and takes responsibility for the content of this report. For further information or to place an order in any of the above-mentioned securities please contact a registered representative of CIMB Securities (USA) Inc. CIMB Securities (USA) Inc does not make a market on the securities mentioned in the report. Other jurisdictions: In any other jurisdictions, except if otherwise restricted by laws or regulations, this report is only for distribution to professional, institutional or sophisticated investors as defined in the laws and regulations of such jurisdictions.

Corporate Governance Report of Thai Listed Companies (CGR). CG Rating by the Thai Institute of Directors Association (Thai IOD) in 2016, Anti-Corruption 2016. AAV – Very Good, n/a, ADVANC – Very Good, Certified, AEONTS – Good, n/a, AMATA – Excellent, Declared, ANAN – Very Good, Declared, AOT – Excellent, Declared, AP – Very Good, Declared, ASK – Very Good, Declared, ASP – Very Good, Certified, BANPU – Very Good, Certified, BAY – Excellent, Certified, BBL – Very Good, Certified, BCH – not available, Declared, BCP - Excellent, Certified, BEM – Very Good, n/a, BDMS – Very Good, n/a, BEAUTY – Good, Declared, BEC - Good, n/a, BH - Good, Declared, BIGC - Excellent, Declared, BJC – Good, n/a, BLA – Very Good, Certified, BPP – not available, n/a, BTS - Excellent, Certified, CBG – Good, n/a, CCET – not available, n/a, CENTEL – Very Good, Certified, CHG – Very Good, n/a, CK – Excellent, n/a, COL – Very Good, Declared, CPALL – not available, Declared, CPF – Excellent, Declared, CPN - Excellent, Certified, DELTA - Excellent, Declared, DEMCO – Excellent, Certified, DTAC – Excellent, Certified, EA – Very Good, Declared, ECL – Good, Certified, EGCO - Excellent, Certified, EPG – Good, n/a, GFPT - Excellent, Declared, GLOBAL – Very Good, Declared, GLOW – Very Good, Certified, GPSC – Excellent, Declared, GRAMMY - Excellent, n/a, GUNKUL – Very Good, Declared, HANA - Excellent, Certified, HMPRO - Excellent, Declared, ICHI – Very Good, Declared, INTUCH - Excellent, Certified, ITD – Good, n/a, IVL - Excellent, Certified, JAS – not available, Declared, JASIF – not available, n/a, JUBILE – Good, Declared, KAMART – not available, n/a, KBANK - Excellent, Certified, KCE - Excellent, Certified, KGI – Good, Certified, KKP – Excellent, Certified, KSL – Very Good, Declared, KTB - Excellent, Certified, KTC – Excellent, Certified, LH - Very Good, n/a, LPN – Excellent, Declared, M – Very Good, Declared, MAJOR - Good, n/a, MAKRO – Good, Declared, MALEE – Very Good, Declared, MBKET – Very Good, Certified, MC – Very Good, Declared, MCOT – Excellent, Declared, MEGA – Very Good, Declared, MINT - Excellent, Certified, MTLS – Very Good, Declared, NYT – Excellent, n/a, OISHI – Very Good, n/a, PLANB – Very Good, Declared, PSH – not available, n/a, PSL - Excellent, Certified, PTT - Excellent, Certified, PTTEP - Excellent, Certified, PTTGC - Excellent, Certified, QH – Excellent, Declared, RATCH – Excellent, Certified, ROBINS – Very Good, Declared, RS – Very Good, n/a, SAMART - Excellent, n/a, SAPPE - Good, n/a, SAT – Excellent, Certified, SAWAD – Good, n/a, SC – Excellent, Declared, SCB - Excellent, Certified, SCBLIF – not available, n/a, SCC – Excellent, Certified, SCN – Good, Declared, SCCC - Excellent, Declared, SIM - Excellent, n/a, SIRI - Good, n/a, SPALI - Excellent, Declared, SPRC – Very Good, Declared, STA – Very Good, Declared, STEC – Excellent, n/a, SVI – Excellent, Certified, TASCO – Very Good, Declared, TCAP – Excellent, Certified, THAI – Very Good, Declared, THANI – Very Good, Certified, THCOM – Excellent, Certified, THRE – Very Good, Certified, THREL – Very Good, Certified, TICON – Very Good, Declared, TISCO - Excellent, Certified, TK – Very Good, n/a, TKN – Good, n/a, TMB - Excellent, Certified, TOP - Excellent, Certified, TPCH – Good, n/a, TPIPP – not available, n/a, TRUE – Very Good, Declared, TTW – Very Good, Declared, TU – Excellent, Declared, UNIQ – not available, Declared, VGI – Excellent, Declared, WHA – not available, Declared, WHART – not available, n/a, WORK – not available, n/a.

Companies participating in Thailand’s Private Sector Collective Action Coalition Against Corruption programme (Thai CAC) under Thai Institute of Directors (as of October 28, 2016) are categorized into: - Companies that have declared their intention to join CAC, and - Companies certified by CAC

Rating Distribution (%) Investment Banking clients (%)Add 58.4% 5.4%Hold 29.6% 1.4%Reduce 11.6% 0.4%

Distribution of stock ratings and investment banking clients for quarter ended on 31 December 20161626 companies under coverage for quarter ended on 31 December 2016

REIT│Singapore│Viva Industrial Trust│January 9, 2017

17

CIMB Recommendation Framework Stock Ratings Definition: Add The stock’s total return is expected to exceed 10% over the next 12 months. Hold The stock’s total return is expected to be between 0% and positive 10% over the next 12 months. Reduce The stock’s total return is expected to fall below 0% or more over the next 12 months. The total expected return of a stock is defined as the sum of the: (i) percentage difference between the target price and the current price and (ii) the forward net dividend yields of the stock. Stock price targets have an investment horizon of 12 months.

Sector Ratings Definition: Overweight An Overweight rating means stocks in the sector have, on a market cap-weighted basis, a positive absolute recommendation. Neutral A Neutral rating means stocks in the sector have, on a market cap-weighted basis, a neutral absolute recommendation. Underweight An Underweight rating means stocks in the sector have, on a market cap-weighted basis, a negative absolute recommendation.

Country Ratings Definition: Overweight An Overweight rating means investors should be positioned with an above-market weight in this country relative to benchmark. Neutral A Neutral rating means investors should be positioned with a neutral weight in this country relative to benchmark. Underweight An Underweight rating means investors should be positioned with a below-market weight in this country relative to benchmark.