fall 2008 version professor dan c. jones fina 4355 homework

TRANSCRIPT

Fall 2008 VersionFall 2008 Version

Professor Dan C. Jones

FINA 4355

Homework

Risk Management and Insurance: Perspectives in a Global EconomyRisk Management and Insurance: Perspectives in a Global Economy

16. Personnel Risk Management16. Personnel Risk Management

Professor Dan C. Jones

FINA 4355

Homework

3

Study PointsStudy Points

Employee benefits

Risk management for international employees

Employee Benefits

5

Some ObservationsSome Observations

Employee benefits consist of all forms of employer-provided compensation, exclusive of direct wages and salaries.

Expansion of a firm’s operations internationally adds to the complexity of designing and administering employee benefit plans.

Economic expansion and the substantial growth in salaries, particularly for executives and managers, have contributed to the increasing popularity of voluntary employee benefit plans in many countries.

Firms should strive to ensure consistency of treatment among employees.

6

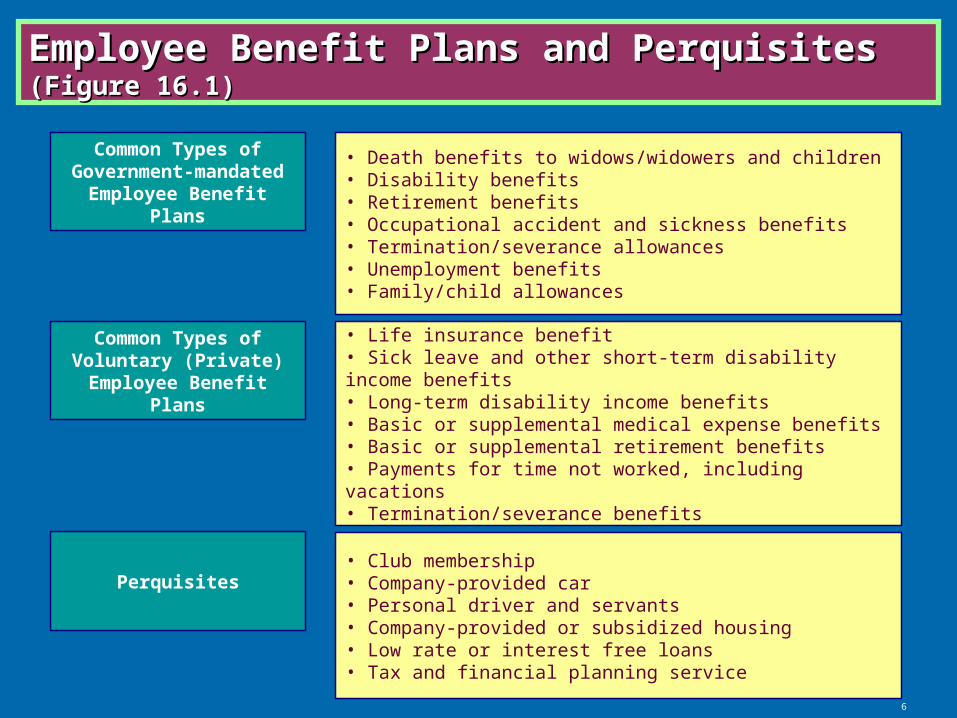

Employee Benefit Plans and Perquisites Employee Benefit Plans and Perquisites (Figure 16.1)(Figure 16.1)

Perquisites• Club membership• Company-provided car• Personal driver and servants• Company-provided or subsidized housing• Low rate or interest free loans• Tax and financial planning service

Common Types of Government-mandated Employee Benefit Plans

• Death benefits to widows/widowers and children• Disability benefits• Retirement benefits• Occupational accident and sickness benefits• Termination/severance allowances• Unemployment benefits• Family/child allowances

Common Types of Voluntary (Private)

Employee Benefit Plans

• Life insurance benefit• Sick leave and other short-term disability income benefits• Long-term disability income benefits• Basic or supplemental medical expense benefits• Basic or supplemental retirement benefits• Payments for time not worked, including vacations• Termination/severance benefits

7

Rationales for Employee Benefit PlansRationales for Employee Benefit Plans

Lifetime utility maximizationDeferred wage theory

Meeting the competition

Improved employee productivity

8

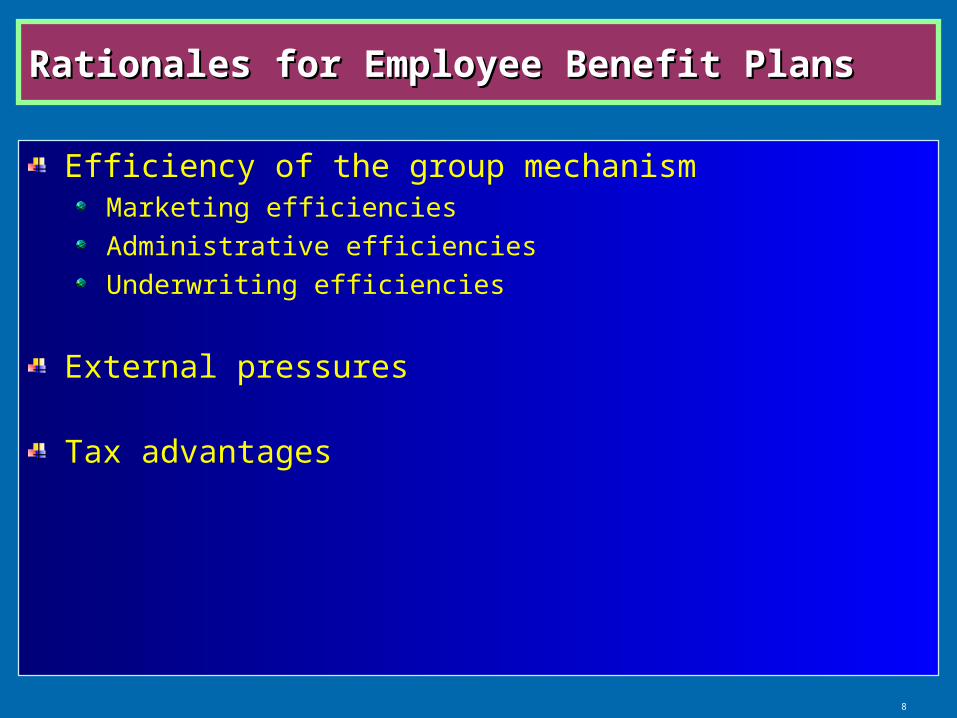

Rationales for Employee Benefit PlansRationales for Employee Benefit Plans

Efficiency of the group mechanismMarketing efficiencies

Administrative efficiencies

Underwriting efficiencies

External pressures

Tax advantages

9

Designing Employee Benefit PlansDesigning Employee Benefit Plans

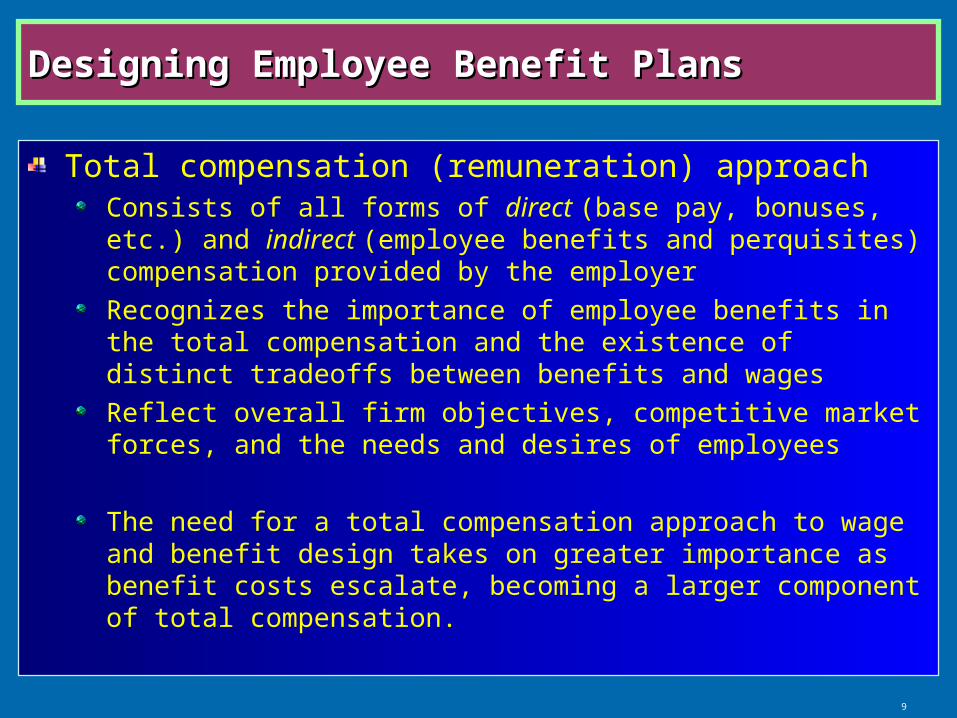

Total compensation (remuneration) approachConsists of all forms of direct (base pay, bonuses, etc.) and indirect (employee benefits and perquisites) compensation provided by the employer

Recognizes the importance of employee benefits in the total compensation and the existence of distinct tradeoffs between benefits and wages

Reflect overall firm objectives, competitive market forces, and the needs and desires of employees

The need for a total compensation approach to wage and benefit design takes on greater importance as benefit costs escalate, becoming a larger component of total compensation.

10

Defined Benefit (DB) vs. Defined Contribution (DC)Defined Benefit (DB) vs. Defined Contribution (DC)

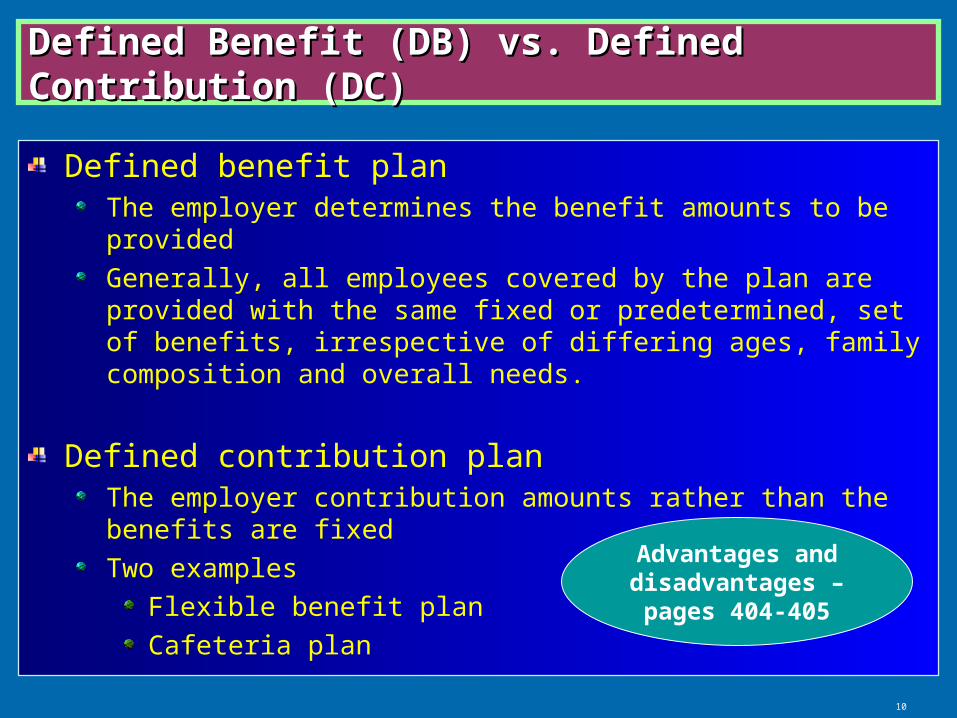

Defined benefit planThe employer determines the benefit amounts to be provided

Generally, all employees covered by the plan are provided with the same fixed or predetermined, set of benefits, irrespective of differing ages, family composition and overall needs.

Defined contribution planThe employer contribution amounts rather than the benefits are fixed

Two examples

Flexible benefit plan

Cafeteria plan Advantages and disadvantages – pages 404-405

11

International Variations – PensionInternational Variations – Pension

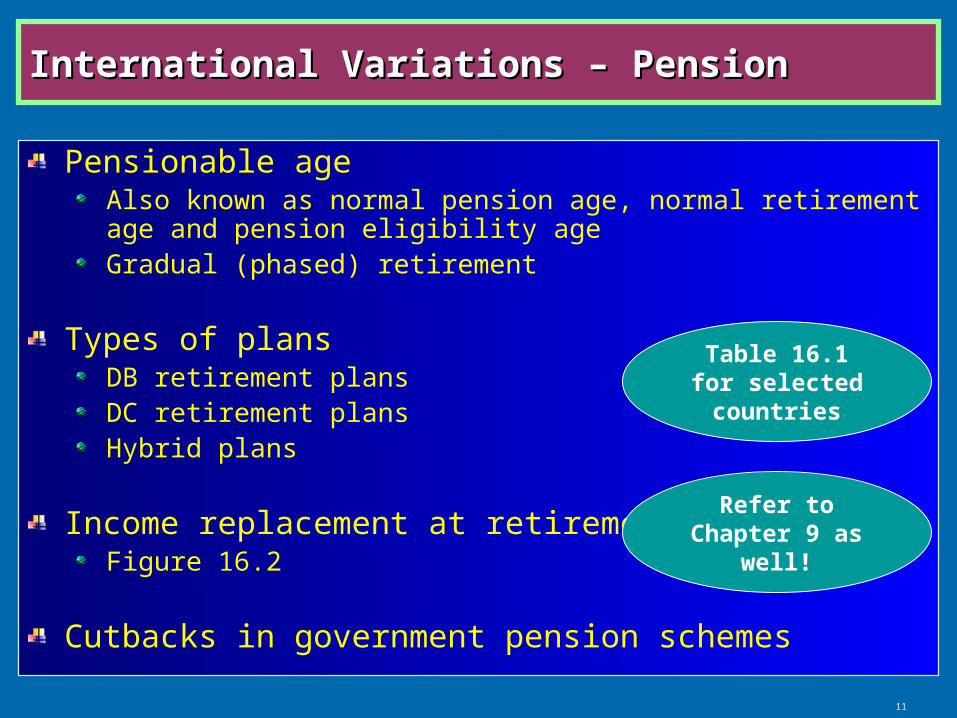

Pensionable ageAlso known as normal pension age, normal retirement age and pension eligibility ageGradual (phased) retirement

Types of plansDB retirement plansDC retirement plansHybrid plans

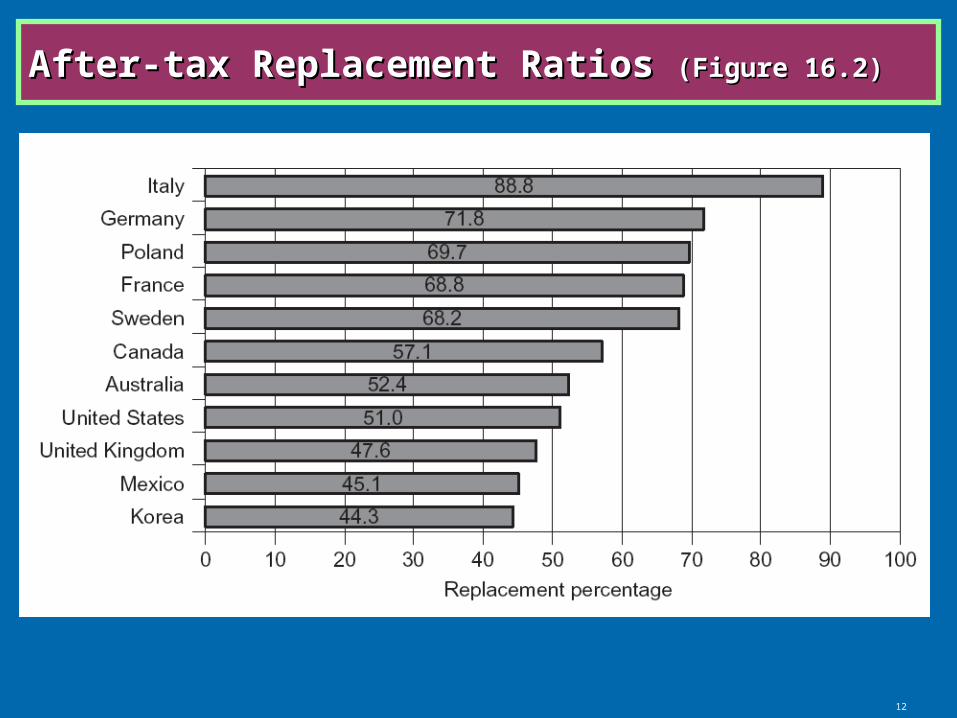

Income replacement at retirementFigure 16.2

Cutbacks in government pension schemes

Refer to Chapter 9 as well!

Table 16.1 for selected countries

12

After-tax Replacement Ratios After-tax Replacement Ratios (Figure 16.2)(Figure 16.2)

13

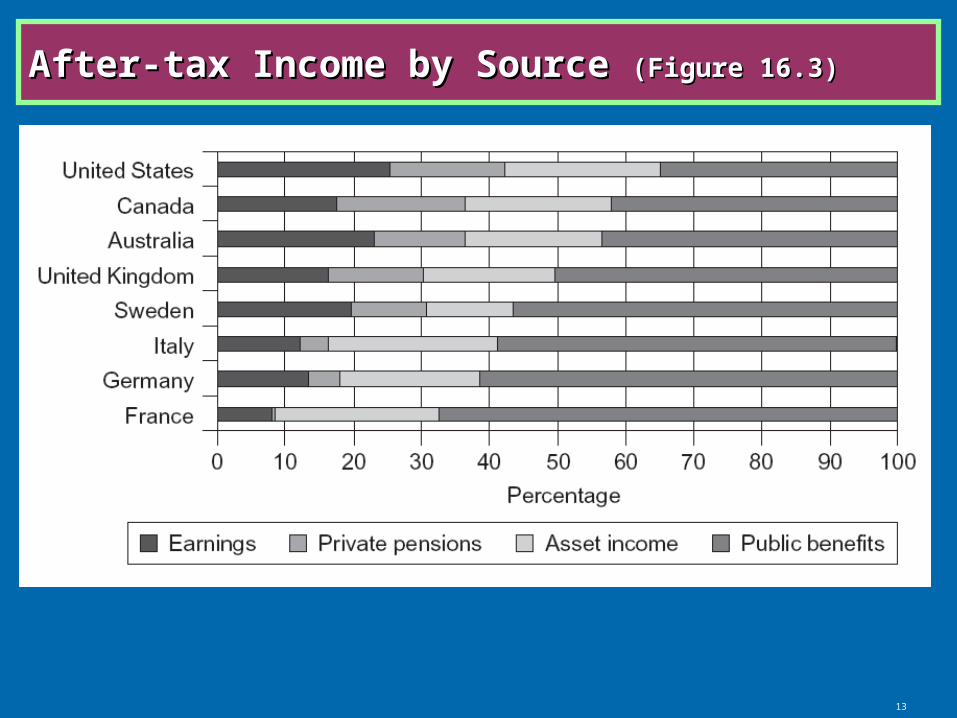

After-tax Income by Source After-tax Income by Source (Figure 16.3)(Figure 16.3)

14

International Variations – HealthcareInternational Variations – Healthcare

BenefitsBasic healthcare benefitsSupplemental healthcare benefits

Containing escalating healthcare plan costs

Managed care programsPreferred provider organization (PPO)Health maintenance organization (HMO)

Flexible benefit plans

Wellness programs

Table 16.2 for selected countries

15

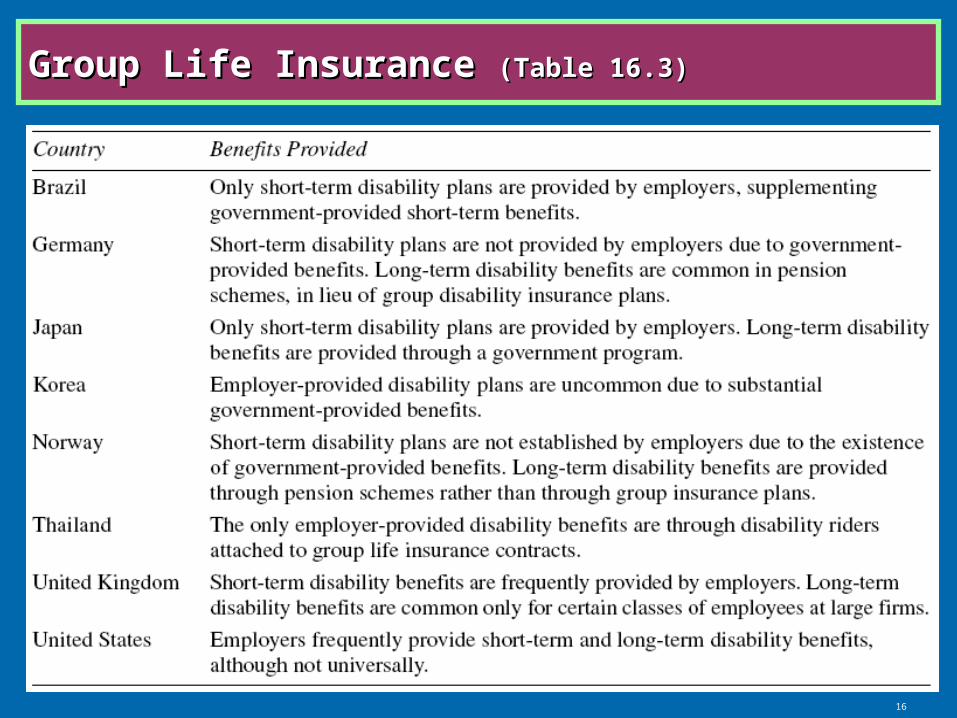

International Variations – Group Life InsuranceInternational Variations – Group Life Insurance

To fund employer-provided death benefits in many countries

Death benefits frequently are included in pension schemes

Employer contributions toward the cost of group life insurance often do not create any income tax liability to employees, within limits.

Insurance coverage limits generally are expressed either as a multiple of salary or a flat amount.

Table 16.3

16

Group Life Insurance Group Life Insurance (Table 16.3)(Table 16.3)

17

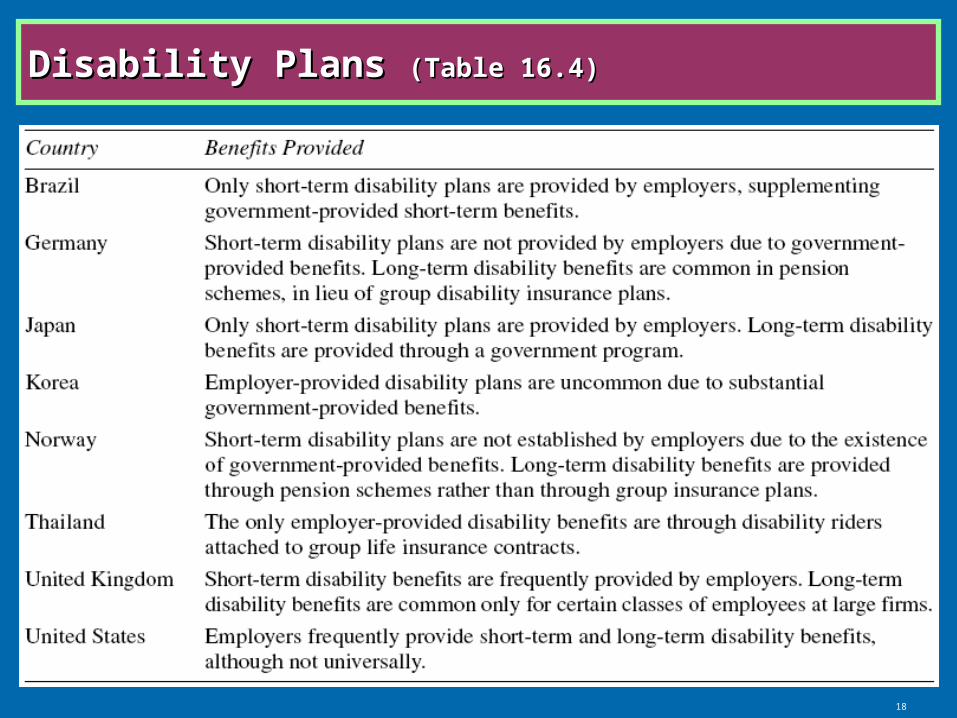

International Variations – DisabilityInternational Variations – Disability

Found less frequently than pension and life insurance benefits

Plans providing short-term benefits (e.g., 3~6 months) are more common than long-term benefit plans

Benefits often tied with severance benefits or to government-provided disability benefits

Table 16.4

18

Disability Plans Disability Plans (Table 16.4)(Table 16.4)

19

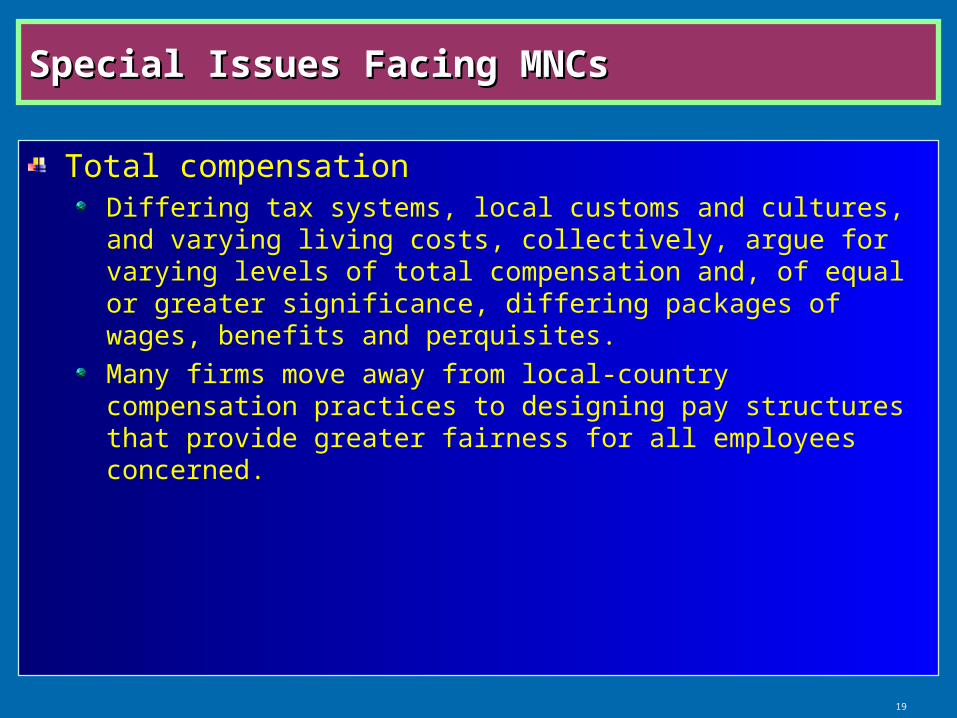

Special Issues Facing MNCsSpecial Issues Facing MNCs

Total compensationDiffering tax systems, local customs and cultures, and varying living costs, collectively, argue for varying levels of total compensation and, of equal or greater significance, differing packages of wages, benefits and perquisites.

Many firms move away from local-country compensation practices to designing pay structures that provide greater fairness for all employees concerned.

20

Special Issues Facing MNCsSpecial Issues Facing MNCs

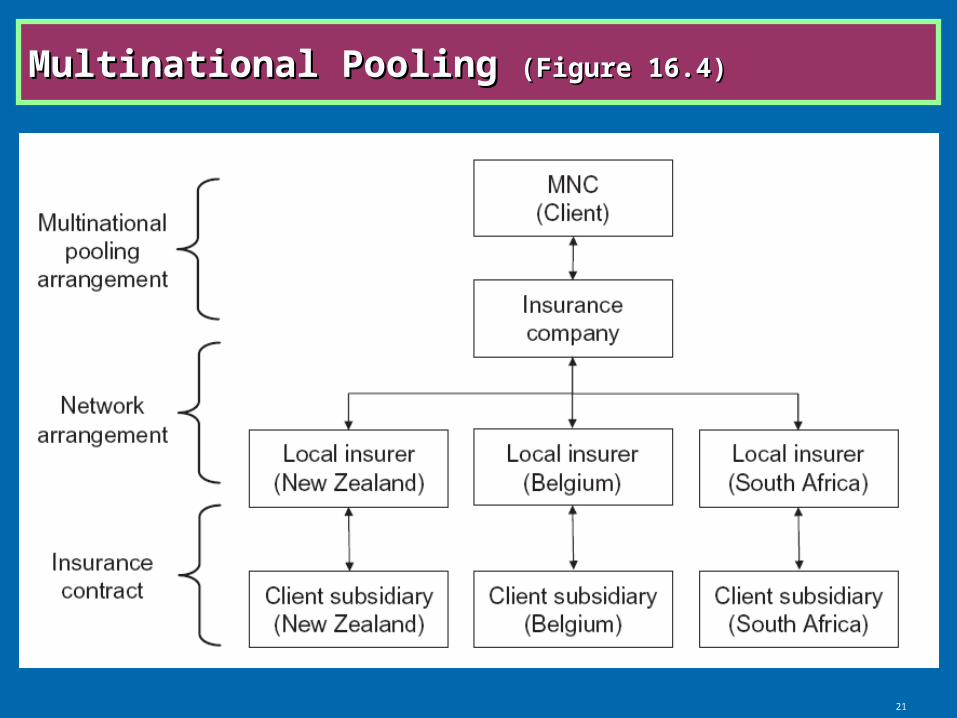

Multinational poolingParticipation in a global insurance arrangement to finance the costs of its worldwide benefit programs

AdvantagesTotal insurance costs are reduced through economies of scale and scope generated from the worldwide aggregation of all insured employees and all benefit plans.Favorable claims experience in some local markets can be used to offset unfavorable claims experience in other markets.The administration and management of employee benefit plans are made simpler.Excessive margins inherent in cartel and tariff-premium markets can be overcome through the international dividend calculation.An MNC may use a traditional or create its own captive.

21

Multinational Pooling Multinational Pooling (Figure 16.4)(Figure 16.4)

RM for International Employees

23

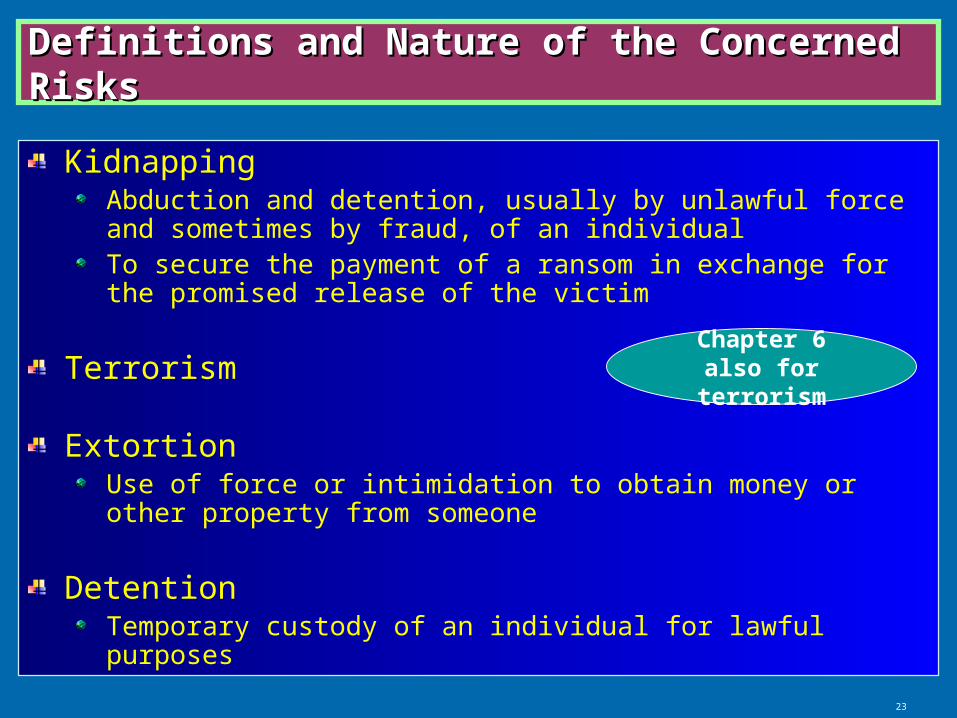

Definitions and Nature of the Concerned RisksDefinitions and Nature of the Concerned Risks

KidnappingAbduction and detention, usually by unlawful force and sometimes by fraud, of an individualTo secure the payment of a ransom in exchange for the promised release of the victim

Terrorism

ExtortionUse of force or intimidation to obtain money or other property from someone

DetentionTemporary custody of an individual for lawful purposes

Chapter 6 also for terrorism

24

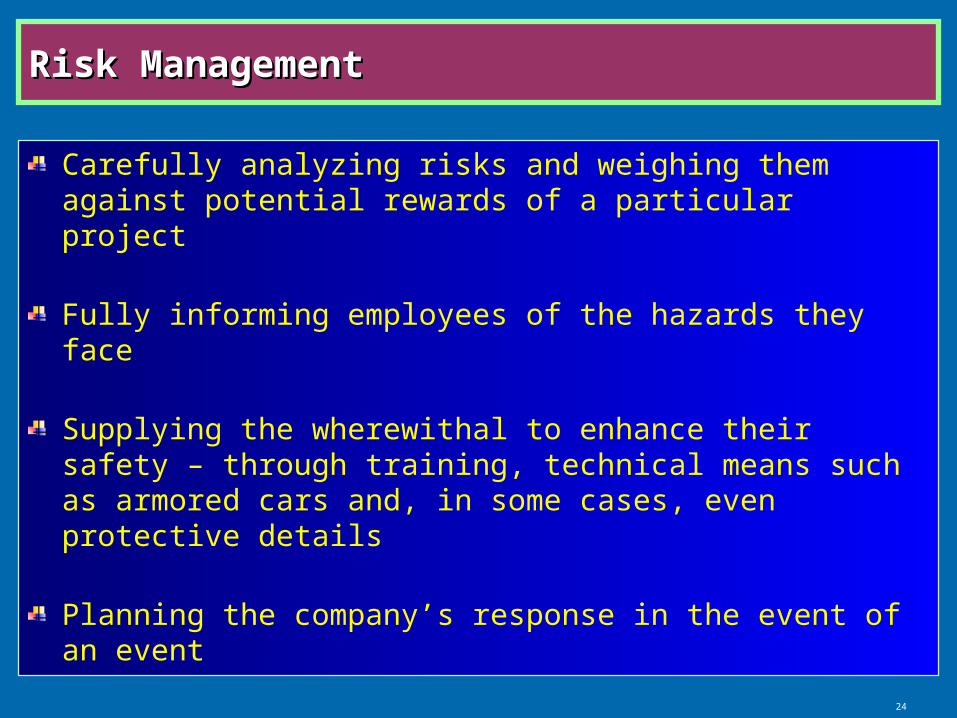

Risk ManagementRisk Management

Carefully analyzing risks and weighing them against potential rewards of a particular project

Fully informing employees of the hazards they face

Supplying the wherewithal to enhance their safety – through training, technical means such as armored cars and, in some cases, even protective details

Planning the company’s response in the event of an event

25

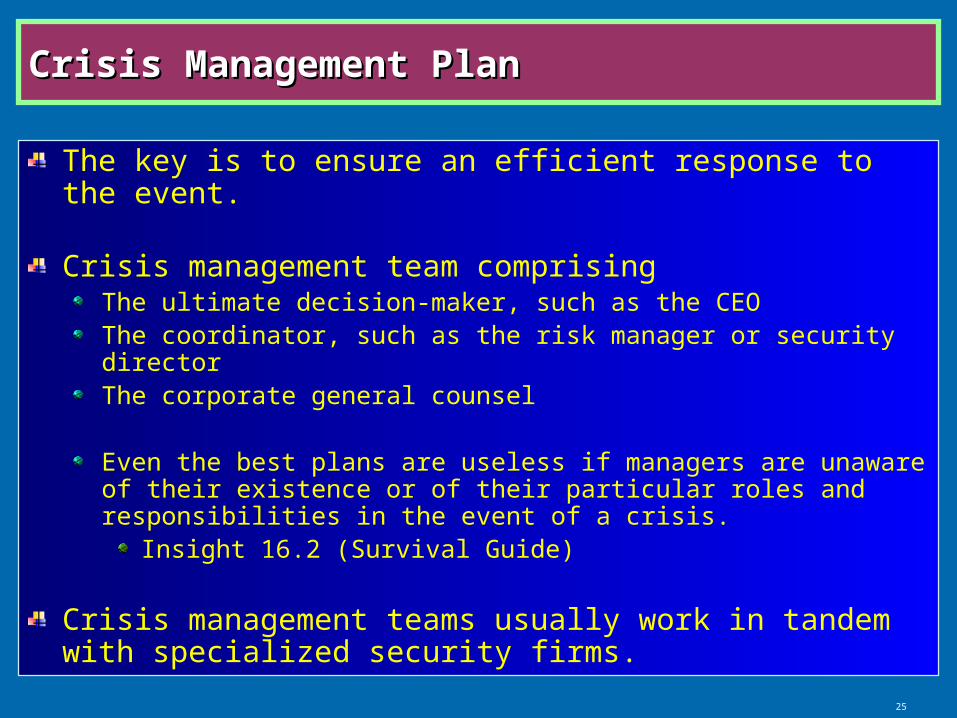

Crisis Management PlanCrisis Management Plan

The key is to ensure an efficient response to the event.

Crisis management team comprisingThe ultimate decision-maker, such as the CEOThe coordinator, such as the risk manager or security directorThe corporate general counsel

Even the best plans are useless if managers are unaware of their existence or of their particular roles and responsibilities in the event of a crisis.

Insight 16.2 (Survival Guide)

Crisis management teams usually work in tandem with specialized security firms.

26

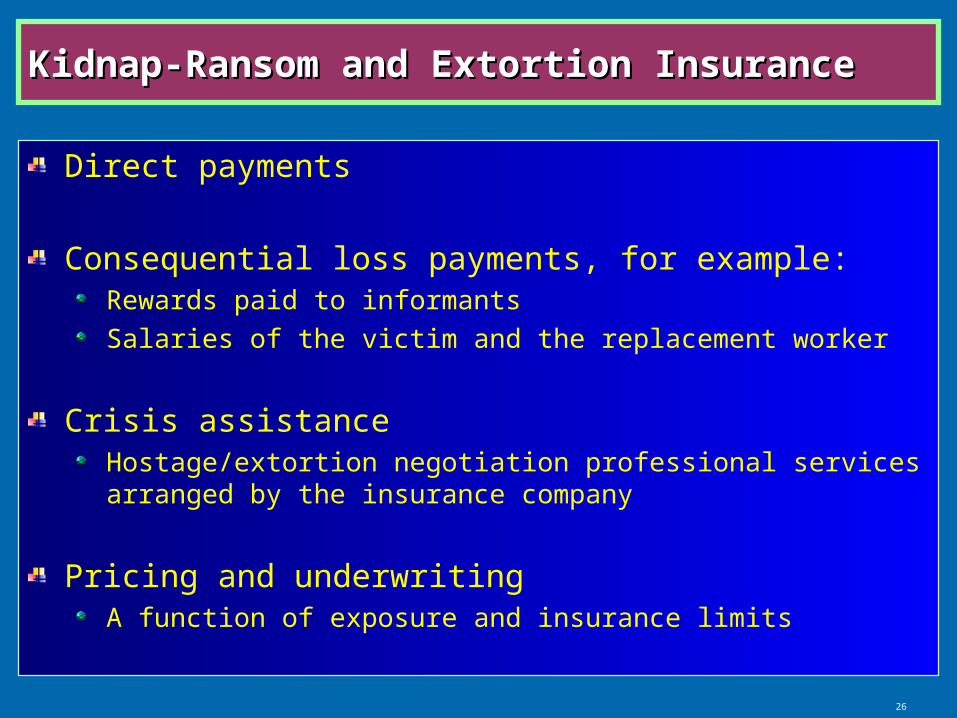

Kidnap-Ransom and Extortion InsuranceKidnap-Ransom and Extortion Insurance

Direct payments

Consequential loss payments, for example:Rewards paid to informants

Salaries of the victim and the replacement worker

Crisis assistanceHostage/extortion negotiation professional services arranged by the insurance company

Pricing and underwritingA function of exposure and insurance limits

Discussion Questions

28

Discussion Question 1Discussion Question 1

How will changing employment patterns, changing demographics and movement to a global marketplace affect employee benefit plan design in your country in the future? Has the government in your country introduced new laws related to this issue? If not, is it considering such a measure in the near future?

29

Discussion Question 2Discussion Question 2

What are the primary factors that account for the cross-country differences in voluntary employer-sponsored benefit programs?

30

Discussion Question 3Discussion Question 3

What unique or special issues/problems do MNCs face in the provision of employee benefits? How are MNCs addressing these issues today?

31

Discussion Question 4Discussion Question 4

Why is it envisioned that employer-provided economic security will assume an increasing role in virtually all countries?

32

Discussion Question 5Discussion Question 5

Should we expect greater uniformity worldwide in the types of employee benefit programs offered and the way in which they are provided? Why or why not?

33

Discussion Question 6Discussion Question 6

Identify a large MNC in your home country and examine (a) the scope of employee benefits and (b) the approach (DB, DC or hybrid) it uses to offer the benefits.

34

Discussion Question 7Discussion Question 7

Briefly describe the structure of (a) healthcare programs and (b) employee retirement programs in your (your friend’s) country.

35

Discussion Question 8Discussion Question 8

Why do kidnap/ransom and extortion insurance policies prohibit the insured from disclosing the existence of the insurance?

36

Discussion Question 9Discussion Question 9

How do MNCs’ personnel risks differ from those of purely national corporations?