family office sector – australia office review 2011.pdf · some/ 350/ single/ family/ offices,/...

TRANSCRIPT

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 1

Australian Family Office Sector – Review 2011 January 2012. Welcome to the Family Office Connect, (FOC), annual review. FOC is a specialist research group on the family office sector in Australia and now, in collaboration with The Table Club, www.thetableclub.com , provides insights on the global family office landscape. Introduction Our review looks at the entire Australian family office sector and estimates there are some 350 Single Family Offices, (SFOs), with a total wealth of $226 billion as at December 2011. The range in wealth is $10.3 billion to $100 million. Most of our analysis focuses on SFOs with total wealth exceeding $200 million which is a universe of 250. FOC has been researching the family office sector in Australia, since early 2009 and now covers some 109 SFOs and Multi Family Offices, (MFOs). This coverage includes 92% of the top 50 SFOs by number and 90% by value of $116 billion. Extending to the Top 100 SFOs, the coverage by number is 65% and by value it is 80% or $129 billion of the universe of $162 billion. Our plan for 2012 is to extend the research to cover more of the Top 100 SFOs as well as those SFOs in the Top 250 where we feel there is a desire to outsource parts of their wealth to investment management firms. Confidentiality FOC has excellent relationships with many of the top SFOs and at all times respects the confidentiality of information gained through these relationships. The sources of information are from public available information and any confidential information is excluded from our reports.

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 2

Data & Review Methodology FOC has composed this review of the Australian family office sector, using data from a variety of sources including proprietary research, BRW Rich 200, (May 2011), Courier Mail QLD Rich List, Western Australian Rich List, (October 2011), and various other Australian media sources. Additionally, we have compared the US market using the most recent Forbes Top 400 list, (October 2011). The composition of the sector assumes that each Ultra High Net Worth, (UHNW), has a Single Family Office, (SFO). To qualify in the FOC top 350 each SFO must have gross assets > $100 million. The primary focus of the FOC research, are the SFOs and Multi Family offices, (MFOs), with gross assets > $200 million. We feel that in most cases, $200 million is the minimum required to establish a family office with adequate resources. These resources are either dedicated just for the SFO or may be shared with operational businesses. In the SFO range of 251 to 350, FOC currently researches 8 of these across Australia, this may increase slightly in 2012, however, the prime focus shall be on larger SFOs. For the purposes of avoiding double counting, we have not included the MFOs in our sector analysis. We will however make some reference to the MFOs later in this report. Table 4 below, shows a list of SFOs in detail for the top 250, and then an additional 8 SFOs ranging in wealth from $200 million to $150 million. To estimate the balance of the SFOs/UHNW’s to the top 350, we have assumed an average wealth of $125 million based on the range of the balance of SFOs as $150 million to $100 million. Two of the SFO groups have been consolidated for this report. These are Smorgon, (shown as 8 separate SFOs in FOC), and Liberman, (shown as 4 in FOC). Our rationale for the data inclusion was to ensure all BRW Rich 200 individuals and families were included as well as FOC SFOs that are not included in BRW, (Table 4). The wealth numbers are principally those quoted in the various “Rich Lists”. In some cases, FOC has changed those wealth figures to an estimate that we feel is more representative of the actual wealth of that SFO. We find the “Rich List” numbers are quite often less than the actual as the families are very private and often hold assets via trust structures.

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 3

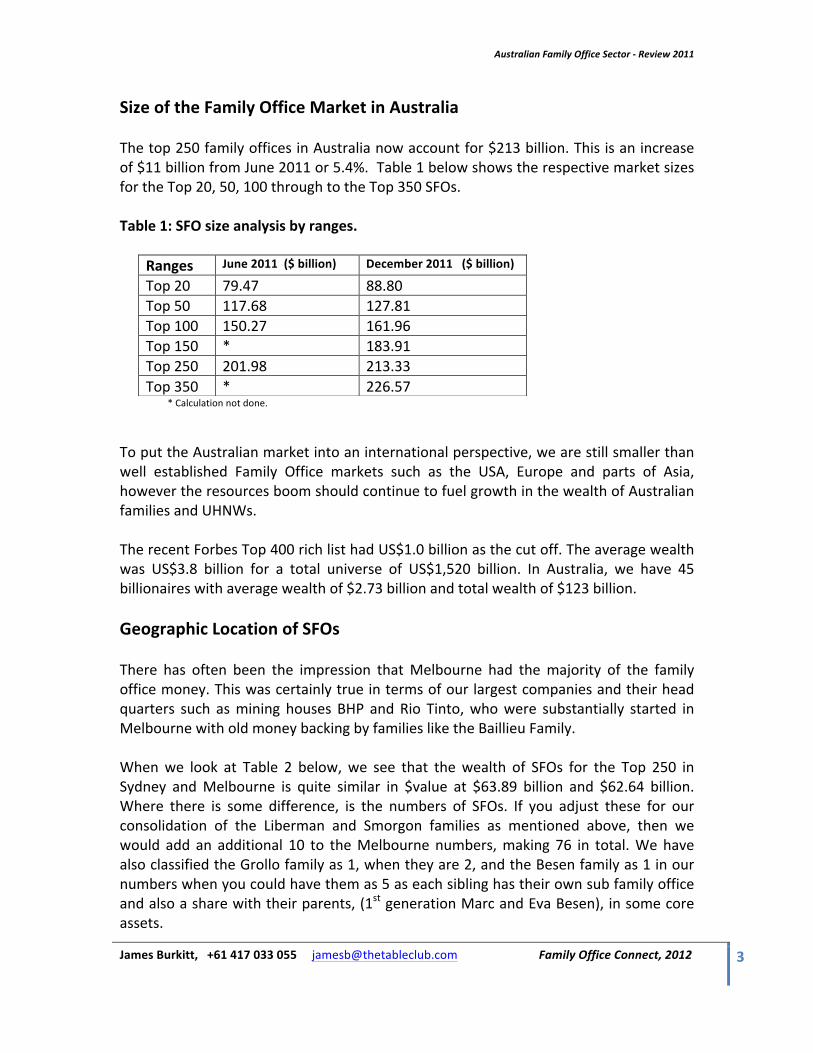

Size of the Family Office Market in Australia The top 250 family offices in Australia now account for $213 billion. This is an increase of $11 billion from June 2011 or 5.4%. Table 1 below shows the respective market sizes for the Top 20, 50, 100 through to the Top 350 SFOs. Table 1: SFO size analysis by ranges.

* Calculation not done.

To put the Australian market into an international perspective, we are still smaller than well established Family Office markets such as the USA, Europe and parts of Asia, however the resources boom should continue to fuel growth in the wealth of Australian families and UHNWs. The recent Forbes Top 400 rich list had US$1.0 billion as the cut off. The average wealth was US$3.8 billion for a total universe of US$1,520 billion. In Australia, we have 45 billionaires with average wealth of $2.73 billion and total wealth of $123 billion. Geographic Location of SFOs There has often been the impression that Melbourne had the majority of the family office money. This was certainly true in terms of our largest companies and their head quarters such as mining houses BHP and Rio Tinto, who were substantially started in Melbourne with old money backing by families like the Baillieu Family. When we look at Table 2 below, we see that the wealth of SFOs for the Top 250 in Sydney and Melbourne is quite similar in $value at $63.89 billion and $62.64 billion. Where there is some difference, is the numbers of SFOs. If you adjust these for our consolidation of the Liberman and Smorgon families as mentioned above, then we would add an additional 10 to the Melbourne numbers, making 76 in total. We have also classified the Grollo family as 1, when they are 2, and the Besen family as 1 in our numbers when you could have them as 5 as each sibling has their own sub family office and also a share with their parents, (1st generation Marc and Eva Besen), in some core assets.

Ranges June 2011 ($ billion) December 2011 ($ billion)

Top 20 79.47 88.80 Top 50 117.68 127.81 Top 100 150.27 161.96 Top 150 * 183.91 Top 250 201.98 213.33 Top 350 * 226.57

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 4

The resources boom in Australia has seen considerable increases in the wealth of many of our SFOs, in particular those in Queensland, 13% of the $ value of the Top 250 SFOs and 41 in number or 16%. For WA, the $value is even higher at 17% and 12% by number. Table 2: Top 250 SFOs – by State State # SFOs $ bil FOC # FOC $ % FOC $bil WA 30 36.42 14 85.0% 31.08 VIC 66 62.64 24 71.8% 44.96 TAS 3 1.08 0 0 0 SA 9 3.50 3 47.4% 1.66 QLD 41 27.78 10 52.5% 14.59 O/seas 15 17.48 3 19.19% 3.35 NSW 85 63.89 31 62.06 39.65 ACT 1 .93 1 100% .93 FOC Coverage As at December 2011, the latest update of client research had 109 SFOs and MFOs covered. Of this, 106 were SFOs and 5 were MFOs. The double counting was due to both the Myer and Baillieu families also having MFOs. In our numbers on the size of the market we have only shown the Myer family at $2.01 billion when the combined MFO has approximately $4 billion in funds under administration. The Baillieu family, are listed at $495 million when total funds under administration of Mutual Trust are approximately $1.5 billion. Table 2 above, is an analysis of the Top 250 SFOs. The last three columns show FOC coverage with 86/250 by number. The next column shows the percentage coverage by state, and the last column the $ value by state. The 86 SFOs that FOC have researched as at December 2011, represent 64% by $ value of the Top 250 and $136.22 billion of the $213.68 billion universe. By numbers, the coverage is certainly concentrated with the larger SFOs. Of the Top 250 the FOC by number coverage is 34%, (86 of 250). The growth of the SFOs in the WA and Qld markets has been a focus of FOC in the second half of 2011, and now includes 24 SFOs for a wealth value of $55.67 billion. We anticipate expanding the coverage of these two markets.

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 5

Generational Dynamics The Australian Family Office sector is largely still controlled by the 1st and 2nd generations. When we look at the top 50 SFOs by wealth, the concentration is quite dramatic, see Table 3. For the purposes of this analysis, on generational control, we have looked to the Head of the Family Office in terms of which generation they are in the wealth creation phase. Where the 1st generation is still alive but have stepped back from day to day running, we have classified the next generation as the head. As an example, Sam Alter is the head of the Alter Family Office, (Albany), whilst his father, Maurice is still listed by BRW as the head. We have Sam as a 2nd generation for this analysis. Where the 3rd generation or older is running the family office, examples such as Myer, Fairfax, Smorgon and Albert families, we have classified as > 2nd, so that we have three categories in our table below. We also looked at the Top 50 SFO heads currently over 70 years of age and feel that there will be a further change to “the next gen” over the next few years, which will ultimately lead to further diversification of investments away from the core wealth as greater focus is on preservation than creation. There are 14 of the Top 50 SFO heads who are 1st generation and over 70 years of age, (average age 77.8 years). The split of the Top 20 has 60% of the SFO heads as 1st generation and of these, 6 are over 70 with an average age of 80.2 years. In the next group of 21 to 50 SFOs, we have 25 who are 1st generation or 83.3% with 7, (23%), over 70 years of age and an average of 76.3 years. FOC does note that some of these 1st generation SFO heads have clear succession plans in place, with either sons or daughters in CEO type roles within the SFO. The current head has typically moved to a Chairman position, allowing the son or daughter to assume a lot more day to day responsibility. Examples here in the top 50 SFOs include:

• Lowy • Fox • Oatley • Sarich

We have also seen some early allocations of capital to beneficiaries, to allow each sibling to develop their own sub family offices, such as the Besen, Lew, Pratt, Myer, Fairfax, Roberts and Kahlbetzer families.

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 6

FOC believes that this diversification shall be achieved through building of internal investment experience as well as out sourcing to investment managers in areas that the SFOs feel they lack the skill set or resources. A good example of this trend is the increased outsourcing to hedge funds and in particular international hedge funds. Table 3: Generational Control – Top 50 SFOs

Generation – Head of SFO # % 1st 37 74 2nd 10 20 > 2nd 3 6

Multi Family Offices & Wealth Management Groups Multi Family Offices, (MFOs), are a common grouping in the USA, but not many as yet in Australia. FOC have a total of 5 MFOs that we research:

• Myer Family Company • Mutual Trust • GGB Wealth Care • EWM • Caerus Capital

The first two are large SFOs, Myer and Baillieu families of Melbourne, that manage the wealth of a number of smaller families. In the case of Myer Family Company, they administer some 60 -‐ 70 additional families to the 10 or so Myer family members. These additional assets, to the Myer Family wealth, are approximately $2 billion or $28 -‐ $33 million on average. This seems to be consistent with our earlier assumptions on the size of family wealth required to establish an SFO which we feel is closer to $200 million than $100 million. The other MFOs that FOC currently research, are state based offering services to families that either outsource parts of their wealth management, i.e. Caerus Capital, a Perth based group headed by Chris Michael, which manages part of the wealth of the Paspaley and Harmanis families, and most recently another family. Both the Paspaley and Harmanis families are researched separately by FOC with respective wealth of $540 million and $544 million.

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 7

GGB Wealth Care, are a Sydney based MFO managing wealth for approximately 5 -‐ 10 families with wealth typically from $30 million to $300 million, although there is not a size constraint as a family may allocate just a component of their wealth. GGB have a full discretionary model of managing approximately 50% of the investments internally and outsourcing to sector specialists for the balance. Lastly, EWM is a Brisbane based MFO managing approximately 10 families with wealth exceeding $20 million per family. EWM is headed by Brad Scott and use largely an outsourced model of investment specialists. We note that various wealth management platforms, such as UBS, MSSB, Citigroup and the Australian Private Banks such as NAB, Westpac, ANZ, Commonwealth and Macquarie, tend to service families with wealth < $100 million. Quite often they have strong banking relationships as well as securities services that the larger family offices may use, that have internal investment teams. The wealth platforms usually have a definition of UHNW as those with wealth, (excluding the family home), > $10 million. FOC feels that most of the clients of these wealth platforms fall out side the Top 250 SFOs as per our Table 4 below, however, there well may be a number in the Top 250 to Top 350, ($200 million to $100 million group).

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 8

Strategic asset allocation & position of family offices in Australia The earlier analysis in this review on the early generational concentration of SFOs in Australia to 1st and 2nd generation, Table 3, showed that the Top 50 SFOs were 74% controlled by 1st generation or the wealth accumulators. In fact, we discussed that the concentration was even higher in the next range of SFOs with wealth from $2.1 billion to $933 million. Extending the analysis to the next 50 SFOs or $910 million to $550 million, the concentration of new wealth gets even bigger at 88% as 1st generation SFO heads, a further 10% as 2nd generation. This tends to suggest that a large number of our SFOs will continue to be wealth accumulators as they strive to build a bigger legacy to hand to the next generation. 2011 was not a good investment year for markets and fund managers. The Australian All Ordinaries Index ended the year -‐ 14%, this compared with the Dow Jones -‐ 6.2% and the MSCI -‐8%. We also note that most hedge funds had single figure negative returns for 2011. It was not surprising that our Australian family offices have sat on the sidelines through much of 2011 and have even cashed up in some areas through liquidity events, (Fairfax, Gandel and Maloney as examples). The FOC estimate of Top 100 SFO cash positions is 20% as at December 2011. This is approximately $16 billion of fire power. In discussions with many of the SFOs, their cash position is high for two reasons;

• Firstly, the uncertainty of Europe is not rewarding in listed markets compared to the Australian risk free rate. Most large SFOs are getting 5.5% on their cash.

• Secondly, liquidity is very powerful to take up opportunities. There are a

number of SFOs who are waiting for the buying opportunities that are likely to flow from the eventual restructuring in Europe, particularly debt. They are also seeing opportunities in the US. If you couple these events with the strength in the AUD then medium to longer term 2012 should present some very good opportunities to cash up families.

Table 4 below shows the SFO sector by descending wealth size down to the Top 258 SFOs and an estimate of the balance of the Top 350 to arrive at a universe size of $226 billion. We have also added a column for the Top 50 SFOs on which generation is the SFO head. Lastly, the column titled, “FOC covered Dec – 11”, shows whether FOC has researched the respective SFO and included in the December 2011 client update.

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 9

Table 4: Analysis of Family Offices in Australia

Family Office Sector in Australia

December 2011 Rank Family Office Generation SFO Head $ mil FOC # (1st, 2nd, Age 2011 BRW/other Covered Location > 2nd) (> 70 years) or FOC est. Dec-‐11

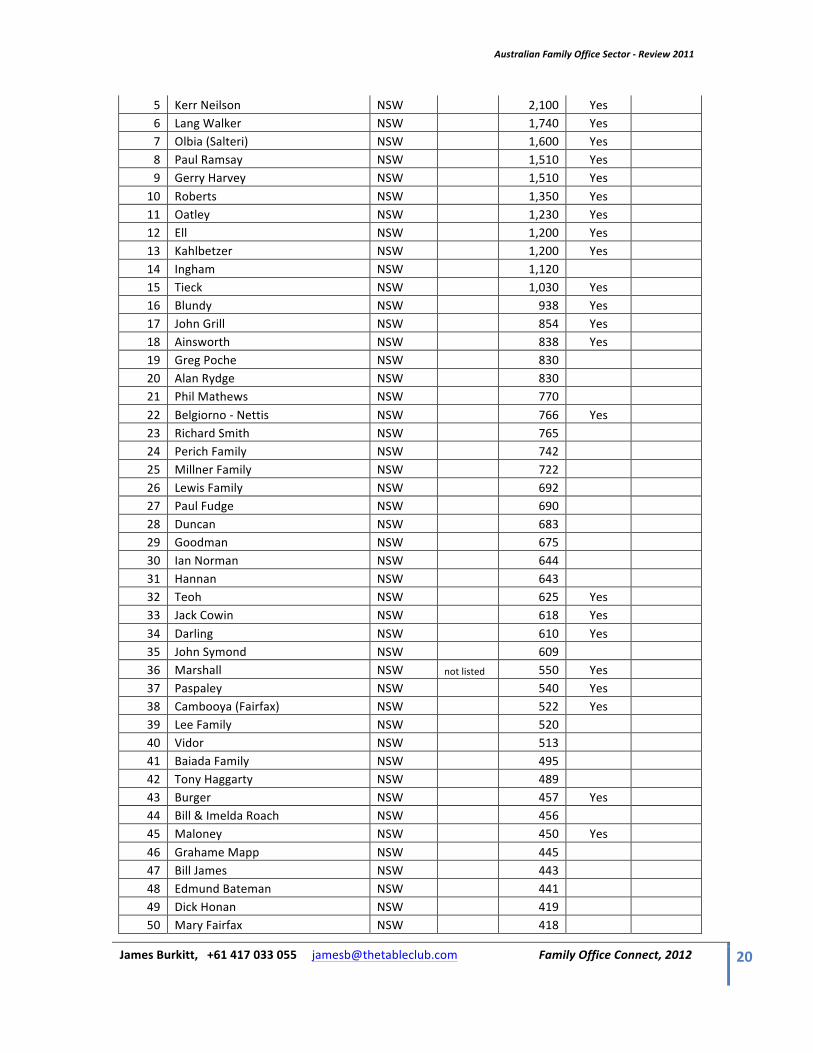

1 Rinehart WA 2nd 10,310 Yes 2 Ivan Glasenberg OS 1st 8,800 3 Smorgon Group VIC >2nd 8,765 Yes 4 Andrew Forrest WA 1st 6,180 Yes 5 Clive Palmer QLD 1st 6,080 Yes 6 Thorney (Pratt) VIC 2nd 5,180 Yes 7 Lowy NSW 1st 80 4,980 Yes 8 Triguboff NSW 1st 78 4,300 Yes 9 Packer NSW >2nd 4,160 Yes

10 Liberman Family VIC >2nd 3,900 Yes 11 Gandel VIC 1st 75 3,450 Yes 12 Chris Wallin QLD 1st 3,100 Yes 13 Stan Perron WA 1st 88 2,700 Yes 14 Len Buckeridge WA 1st 74 2,600 Yes 15 Australian Capital Equity (Stokes) WA 1st 2,550 Yes 16 Besen VIC 1st 86 2,500 Yes 17 Alter VIC 2nd 2,400 Yes 18 Terrace Tower Group (Saunders) NSW 2nd 2,400 Yes 19 Portland House (Hains) VIC 1st 2,300 Yes Top 20 20 Bennett/Wright WA 2nd 74 2,140 Yes $88,795 21 Kerr Neilson NSW 1st 2,100 Yes 22 Fox VIC 1st 74 2,050 Yes 23 Myer VIC >2nd 2,010 Yes 24 Lang Walker NSW 1st 1,740 Yes 25 Olbia (Salteri) NSW 2nd 1,600 Yes 26 Bruce Gordon OS 1st 82 1,570 27 Paul Ramsay NSW 1st 74 1,510 Yes 28 Gerry Harvey NSW 1st 72 1,510 Yes 29 Grollo Family VIC 2nd 1,430 Yes 30 Talbot QLD 1st Dead/wife 1,420 Yes 31 John van Lieshout QLD 1st 1,390 Yes 32 Roberts NSW 2nd 1,350 Yes 33 Century Plaza (Lew) VIC 1st 1,330 Yes 34 Oatley NSW 1st 81 1,230 Yes

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 10

35 Ell NSW 1st 1,200 Yes 36 Kahlbetzer NSW 2nd 1,200 Yes 37 Fraid & Fried VIC 1st 1,130 Yes 38 Ingham NSW 1st 79 1,120 39 Sarich WA 1st 72 1,120 Yes 40 Makris SA 1st 1,070 Yes 41 Bruce Mathieson VIC 1st 1,050 Yes 42 Tarascio VIC 1st 1,050 Yes 43 Tieck NSW 1st 1,030 Yes 44 Frank Timis OS 1st 1,020 45 Nathan Tinkler QLD 1st 1,010 Yes 46 Tony Poli WA 1st 984 Yes 47 Chau Chak Wing OS 1st 970 Yes 48 Sammy Chong QLD 1st 950 49 Blundy NSW 1st 938 Yes Top 50 50 Terry Snow ACT 1st 933 Yes $127,810 51 Little VIC 910 52 John Grill NSW 854 Yes 53 Lloyd Williams VIC 839 Yes 54 Ainsworth NSW 838 Yes 55 Greg Poche NSW 830 56 Alan Rydge NSW 830 57 RG Capital (Grundy) OS 814 Yes 58 Ron Walker VIC 810 Yes 59 Maha Sinnathamby QLD 809 60 Baron VIC 805 Yes 61 PGA (Gunn) VIC 800 Yes 62 Phil Mathews NSW 770 63 Belgiorno -‐ Nettis NSW 766 Yes 64 Richard Smith NSW 765 65 Greg Coffey OS 743 66 Perich Family NSW 742 67 Allan Myers VIC 739 68 Millner Family NSW 722 69 Gordon Fu QLD 716 70 Barro Family VIC 704 71 Lewis Family NSW 692 72 Paul Fudge NSW 690 73 Duncan NSW 683 74 Goodman NSW 675 75 Flannery QLD 674 76 Ian Norman NSW 644 77 Hannan NSW 643 78 Juilliard Group (Werdiger) VIC 637 Yes 79 Teoh NSW 625 Yes 80 Chris Morris VIC 621

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 11

81 Peter Scanlon VIC 620 Yes 82 Jack Cowin NSW 618 Yes 83 Michael Hintze OS 614 84 Withers Family VIC 612 85 Darling NSW 610 Yes 86 John Symond NSW 609 87 Reg Rowe QLD 602 88 Peter Bond QLD 597 Yes 89 Peabody QLD 594 90 Rowsthorn VIC 594 91 Kevin Seymour QLD 585 Yes 92 Juniper QLD 582 Yes 93 Jack Bendat WA 578 94 Jeff Chapman VIC 575 95 Gordon Merchant QLD 573 Yes 96 Spooner VIC 571 97 Silviu Itescu VIC 562 98 Steven Kalmin OS 560 99 Kerry Harmanis WA 554 Yes Top 100

100 Marshall NSW 550 Yes $161,960 101 Paspaley NSW 540 Yes 102 Geoff Harris VIC 536 103 Krongold VIC 530 Yes 104 Inge Family VIC 526 105 Cambooya (Fairfax) NSW 522 Yes 106 Lee Family NSW 520 107 Mick Power QLD 516 108 Vidor NSW 513 109 Dale Elphinstone TAS 497 110 John Wilson VIC 497 111 Baiada Family NSW 495 112 Baillieu VIC 495 Yes 113 Alan Wilson VIC 491 114 Tony Haggarty NSW 489 115 Bruce Wilson VIC 487 116 Shi Zhengrong OS 484 117 Menegazzo VIC 470 Yes 118 Stamoulis Family VIC 459 119 Burger NSW 457 Yes 120 Bill & Imelda Roach NSW 456 121 Maloney NSW 450 Yes 122 Graham Turner QLD 446 123 Grahame Mapp NSW 445 124 Bill James NSW 443 125 Edmund Bateman NSW 441 126 Simpson WA 440 Yes

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 12

127 Martin Family WA 435 128 Dick Honan NSW 419 129 Mary Fairfax NSW 418 130 John Kinghorn NSW 414 131 George Kepper VIC 412 132 Rae Family WA 412 133 Kornhauser Family VIC 411 134 John Longhurst QLD 410 135 Anderson Family QLD 409 136 Wagner Family QLD 409 137 Mandie VIC 409 Yes 138 John Higgins VIC 405 139 Andrew Abercrombie VIC 403 140 Goldberger & Wieland VIC 400 141 Wyllie WA 400 Yes 142 Holmes a Court WA 400 Yes 143 Packer & Co WA 400 Yes 144 Hilton Nathanson OS 400 145 Michael Boyd VIC 396 146 Shaun Bonett NSW 390 147 Kidman Family SA 384 148 Handbury NSW 383 149 Casella NSW 382 Top 150 150 Charles Bass WA 377 $184,283 151 Ray White (White Family) NSW 375 152 Peter Bartlett WA 369 153 Max Beck VIC 369 154 Peter Brooks NSW 369 155 Knowles Family VIC 365 156 Scott Family SA 360 157 Bill Patterson NSW 358 158 Robert Whyte NSW 355 Yes 159 Cyril Maloney NSW 355 160 Danny Hill OS 352 161 Robert Magid NSW 352 162 McDonald Family QLD 352 163 Neville Pask QLD 350 164 Albert NSW 350 Yes 165 Pellicano Family VIC 346 166 Fleming NSW 338 Yes 167 Lewis Saragossi QLD 338 168 Graeme Wood QLD 337 169 Doug Shears NSW 335 170 Cooper Family SA 335 171 Laidlaw Family VIC 335 172 Scheinberg Family NSW 334

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 13

173 Roth Family NSW 334 174 Nigel Slatterley WA 329 175 Valmorbida Family VIC 327 176 George Koukis OS 326 177 Clive Berghofer QLD 325 178 Mark Creasy WA 323 179 Tony Wales NSW 323 180 John & Robert Kirby VIC 322 181 Neil Statham QLD 320 182 Gerry Ryan VIC 317 183 Peter Hughes & Family QLD 316 184 Andrew Muir VIC 316 185 Joe Catalfamo VIC 314 186 Iris Lustig-‐Moar & Max Moar VIC 312 187 Michael Gordon QLD 309 188 Joseph Gutnick VIC 307 189 Nicole Kidman OS 304 190 Bridgestar (James Fairfax) NSW 300 Yes 191 Michell SA 300 Yes 192 Kailis WA 300 Yes 193 John Singleton NSW 299 194 Costa Family VIC 297 195 Patricia Iihan VIC 297 196 Evan & Graeme Acton QLD 295 197 Jan Cameron TAS 295 198 Nik Zuks WA 294 199 Gary Brown-‐Neaves WA 293 Top 200 200 Tony Lennon WA 292 $200,698 201 Tom Misner NSW 292 202 Harold Mitchell VIC 292 203 Bruce Neill TAS 292 204 Dale Alcock WA 291 205 Andy Plummer NSW 291 206 Allan Moss NSW 288 207 Maclachlan SA 286 Yes 208 Sterling Buntine WA 285 209 Farrell Family NSW 284 210 Rabinowicz Family VIC 284 211 Richards Family QLD 283 212 Young Family NSW 283 213 Rod Jones WA 282 214 Peter Meurs WA 280 215 Chan Family NSW 279 216 Russell Staley NSW 278 217 Doug Rathbone VIC 273 218 Angus & Richard Grinham NSW 271

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 14

219 Peter & Stephen Hill VIC 271 220 Greg Norman OS 271 221 Bob Sharpless QLD 271 222 Shesh Ghale VIC 269 223 Marylyn New WA 266 224 Gerard Family SA 262 225 Mitchell Family QLD 259 226 Jiwan Mohan QLD 259 227 Robert Maple-‐Brown NSW 258 228 Charles Curran NSW 256 229 David Knappick QLD 252 230 Roger Fletcher NSW 251 231 Kantor VIC 250 232 Roche Family SA 250 233 Nick DiMauro SA 250 234 Bob Rose NSW 249 235 Chris Corrigan OS 248 236 Susan Marchant QLD 248 237 St Baker QLD 248 Yes 238 Chris Ellis NSW 246 239 Calvert-‐Jones VIC 243 240 Max Begley WA 240 241 Andrew Brice QLD 237 242 Bob Bryan QLD 235 243 McMullin Family VIC 234 244 Ivany NSW 230 Yes 245 Doug Moran NSW 228 246 Terry Morris QLD 224 247 Christina & Tony Quinn QLD 219 248 Lachlan Murdoch NSW 217 249 John Hunt NSW 215 Top 250 250 Graham McCamley QLD 215 $213,683 251 Beville NSW 200 Yes 252 Zupp QLD 193 Yes 253 Scifleet QLD 181 Yes 254 Higgins Brothers NSW 180 Yes 255 Ellison WA 168 Yes 256 Cotter QLD 168 Yes 257 Friday Group (Goldburg) QLD 151 Yes 258 Clement Lee VIC 150 Yes 350 Other family offices to $100 mil, (est) 11,500

Total Top 350 $226,574

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 15

Our last table of this review, Table 5, looks at the location of the Top 250 SFOs in Australia. We have discussed much of the issues pertaining to this data earlier in this review and also summarized earlier in this review in Table 2. One aspect that was not touched on was some of the international based SFOs of Australian origin, (shown as OS in our table). The largest, Ivan Glasenberg at $8.8 billion, is only a new entry to the Rich Lists after the listing of Glencore. Ivan has lived in Switzerland for 20 years is the CEO of Glencore. Others on the list as “OS” are either domiciled where their respective jobs/businesses are, such as hedge fund managers Michael Hintze and Greg Coffey, or have chosen to live off shore for tax reasons or lifestyle, such as Bruce Gordon, Chris Corrigan and Reg Grundy. One of the trends of the European and some Asian family offices has been to set up offices in other parts of the world to better manage their affairs. Most recently, a number have chosen Singapore as a safe hub to cover the Asian markets, (Parly Group as a good example out of Switzerland). On the Australian family office side, we have families with investment resources on the ground in other parts of the world, (Portland House – London, Lowy – NYC, Saunders – NYC and Roberts – NYC). As more capital is deployed offshore to take up the currency strength and distressed opportunities, we see the trend to have resources offshore to continue.

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 16

Table 5: Family Offices by State location

Family Office Sector in Australia -‐ State location

December 2011 Rank Family Office $ mil FOC # BRW/other Covered Location or FOC est. Dec-‐11

1 Rinehart WA 10,310 Yes 2 Andrew Forrest WA 6,180 Yes 3 Stan Perron WA 2,700 Yes 4 Len Buckeridge WA 2,600 Yes 5 Australian Capital Equity (Stokes) WA 2,550 Yes 6 Bennett/Wright WA 2,140 Yes 7 Sarich WA 1,120 Yes 8 Tony Poli WA 984 Yes 9 Jack Bendat WA 578

10 Kerry Harmanis WA 554 Yes 11 Simpson WA 440 Yes 12 Martin Family WA 435 13 Rae Family WA 412 14 Wyllie WA 400 Yes 15 Holmes a Court WA 400 Yes 16 Packer & Co WA 400 Yes 17 Charles Bass WA 377 18 Peter Bartlett WA 369 19 Nigel Slatterley WA 329 20 Mark Creasy WA 323 21 Kailis WA 300 Yes 22 Nik Zuks WA 294 23 Gary Brown-‐Neaves WA 293 24 Tony Lennon WA 292 25 Dale Alcock WA 291 26 Sterling Buntine WA 285 27 Rod Jones WA 282 28 Peter Meurs WA 280 29 Marylyn New WA 266 30 Max Begley WA 240 WA #30

Ellison WA 168 Yes $36,424 1 Smorgon Group VIC 8,765 Yes 2 Thorney (Pratt) VIC 5,180 Yes 3 Liberman Family VIC 3,900 Yes 4 Gandel VIC 3,450 Yes 5 Besen VIC 2,500 Yes

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 17

6 Alter VIC 2,400 Yes 7 Portland House (Hains) VIC 2,300 Yes 8 Fox VIC 2,050 Yes 9 Myer VIC 2,010 Yes

10 Grollo Family VIC 1,430 Yes 11 Century Plaza (Lew) VIC 1,330 Yes 12 Fraid & Fried VIC 1,130 Yes 13 Bruce Mathieson VIC 1,050 Yes 14 Tarascio VIC 1,050 Yes 15 Little VIC 910 16 Lloyd Williams VIC 839 Yes 17 Ron Walker VIC 810 Yes 18 Baron VIC not listed 805 Yes 19 PGA (Gunn) VIC 800 Yes 20 Allan Myers VIC 739 21 Barro Family VIC 704 22 Juilliard Group (Werdiger) VIC 637 Yes 23 Chris Morris VIC 621 24 Peter Scanlon VIC 620 Yes 25 Withers Family VIC 612 26 Rowsthorn VIC 594 27 Jeff Chapman VIC 575 28 Spooner VIC 571 29 Silviu Itescu VIC 562 30 Geoff Harris VIC 536 31 Krongold VIC not listed 530 Yes 32 Inge Family VIC 526 33 John Wilson VIC 497 34 Baillieu VIC 495 Yes 35 Alan Wilson VIC 491 36 Bruce Wilson VIC 487 37 Menegazzo VIC 470 Yes 38 Stamoulis Family VIC 459 39 George Kepper VIC 412 40 Kornhauser Family VIC 411 41 Mandie VIC 409 Yes 42 John Higgins VIC 405 43 Andrew Abercrombie VIC 403 44 Goldberger & Wieland VIC 400 45 Michael Boyd VIC 396 46 Max Beck VIC 369 47 Knowles Family VIC 365 48 Pellicano Family VIC 346 49 Laidlaw Family VIC 335 50 Valmorbida Family VIC 327 51 John & Robert Kirby VIC 322

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 18

52 Gerry Ryan VIC 317 53 Andrew Muir VIC 316 54 Joe Catalfamo VIC 314 55 Iris Lustig-‐Moar & Max Moar VIC 312 56 Joseph Gutnick VIC 307 57 Costa Family VIC 297 58 Patricia Iihan VIC 297 59 Harold Mitchell VIC 292 60 Rabinowicz Family VIC 284 61 Doug Rathbone VIC 273 62 Peter & Stephen Hill VIC 271 63 Shesh Ghale VIC 269 64 Kantor VIC 250 65 Calvert-‐Jones VIC 243 VIC # 65 66 McMullin Family VIC 234 $62,611

Clement Lee VIC not listed 150 Yes 1 Dale Elphinstone TAS 497 2 Jan Cameron TAS 295 TAS # 3 3 Bruce Neill TAS 292 $1,084 1 Makris SA 1,070 Yes 2 Kidman Family SA 384 3 Scott Family SA 360 4 Cooper Family SA 335 5 Michell SA not listed 300 Yes 6 Maclachlan SA 286 Yes 7 Gerard Family SA 262 8 Roche Family SA 250 SA # 9 9 Nick DiMauro SA 250 $3,497 1 Clive Palmer QLD 6,080 Yes 2 Chris Wallin QLD 3,100 Yes 3 Talbot QLD 1,420 Yes 4 John van Lieshout QLD 1,390 Yes 5 Nathan Tinkler QLD 1,010 Yes 6 Sammy Chong QLD 950 7 Maha Sinnathamby QLD 809 8 Gordon Fu QLD 716 9 Flannery QLD 674

10 Reg Rowe QLD 602 11 Peter Bond QLD 597 Yes 12 Peabody QLD 594 13 Kevin Seymour QLD 585 Yes 14 Juniper QLD 582 Yes 15 Gordon Merchant QLD 573 Yes 16 Mick Power QLD 516 17 Graham Turner QLD 446 18 John Longhurst QLD 410

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 19

19 Anderson Family QLD 409 20 Wagner Family QLD 409 21 McDonald Family QLD 352 22 Neville Pask QLD 350 23 Lewis Saragossi QLD 338 24 Graeme Wood QLD 337 25 Clive Berghofer QLD 325 26 Neil Statham QLD 320 27 Peter Hughes & Family QLD 316 28 Michael Gordon QLD 309 29 Evan & Graeme Acton QLD 295 30 Richards Family QLD 283 31 Bob Sharpless QLD 271 32 Mitchell Family QLD 259 33 Jiwan Mohan QLD 259 34 David Knappick QLD 252 35 Susan Marchant QLD 248 36 St Baker QLD 248 Yes 37 Andrew Brice QLD 237 38 Bob Bryan QLD 235 39 Terry Morris QLD 224 40 Christina & Tony Quinn QLD 219 QLD # 41 41 Graham McCamley QLD 215 $27,764

Zupp QLD 193 Yes Scifleet QLD 181 Yes Cotter QLD 168 Yes Friday Group (Goldburg) QLD 151 Yes

1 Ivan Glasenberg OS 8,800 2 Bruce Gordon OS 1,570 3 Frank Timis OS 1,020 4 Chau Chak Wing OS 970 Yes 5 RG Capital (Grundy) OS 814 Yes 6 Greg Coffey OS 743 7 Michael Hintze OS 614 8 Steven Kalmin OS 560 9 Shi Zhengrong OS 484

10 Hilton Nathanson OS 400 11 Danny Hill OS 352 12 George Koukis OS 326 13 Nicole Kidman OS 304 14 Greg Norman OS 271 O'seas #15 15 Chris Corrigan OS 248 $17,476 1 Lowy NSW 4,980 Yes 2 Triguboff NSW 4,300 Yes 3 Packer NSW 4,160 Yes 4 Terrace Tower Group (Saunders) NSW 2,400 Yes

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 20

5 Kerr Neilson NSW 2,100 Yes 6 Lang Walker NSW 1,740 Yes 7 Olbia (Salteri) NSW 1,600 Yes 8 Paul Ramsay NSW 1,510 Yes 9 Gerry Harvey NSW 1,510 Yes

10 Roberts NSW 1,350 Yes 11 Oatley NSW 1,230 Yes 12 Ell NSW 1,200 Yes 13 Kahlbetzer NSW 1,200 Yes 14 Ingham NSW 1,120 15 Tieck NSW 1,030 Yes 16 Blundy NSW 938 Yes 17 John Grill NSW 854 Yes 18 Ainsworth NSW 838 Yes 19 Greg Poche NSW 830 20 Alan Rydge NSW 830 21 Phil Mathews NSW 770 22 Belgiorno -‐ Nettis NSW 766 Yes 23 Richard Smith NSW 765 24 Perich Family NSW 742 25 Millner Family NSW 722 26 Lewis Family NSW 692 27 Paul Fudge NSW 690 28 Duncan NSW 683 29 Goodman NSW 675 30 Ian Norman NSW 644 31 Hannan NSW 643 32 Teoh NSW 625 Yes 33 Jack Cowin NSW 618 Yes 34 Darling NSW 610 Yes 35 John Symond NSW 609 36 Marshall NSW not listed 550 Yes 37 Paspaley NSW 540 Yes 38 Cambooya (Fairfax) NSW 522 Yes 39 Lee Family NSW 520 40 Vidor NSW 513 41 Baiada Family NSW 495 42 Tony Haggarty NSW 489 43 Burger NSW 457 Yes 44 Bill & Imelda Roach NSW 456 45 Maloney NSW 450 Yes 46 Grahame Mapp NSW 445 47 Bill James NSW 443 48 Edmund Bateman NSW 441 49 Dick Honan NSW 419 50 Mary Fairfax NSW 418

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 21

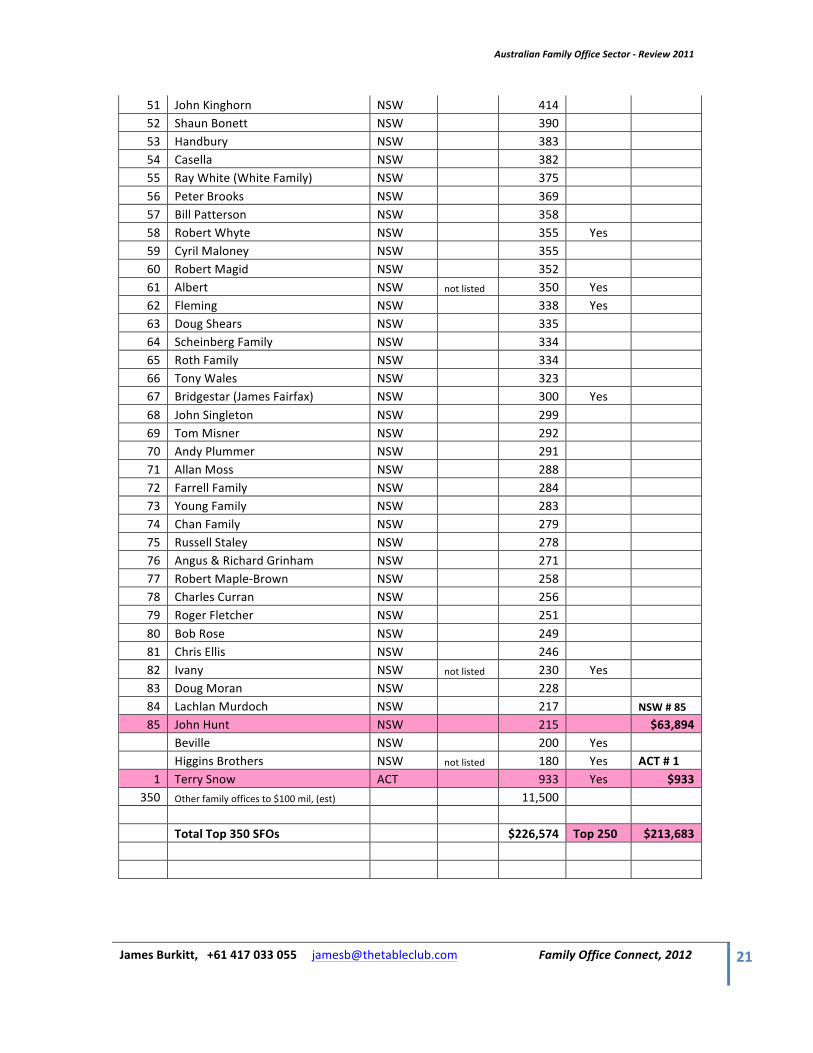

51 John Kinghorn NSW 414 52 Shaun Bonett NSW 390 53 Handbury NSW 383 54 Casella NSW 382 55 Ray White (White Family) NSW 375 56 Peter Brooks NSW 369 57 Bill Patterson NSW 358 58 Robert Whyte NSW 355 Yes 59 Cyril Maloney NSW 355 60 Robert Magid NSW 352 61 Albert NSW not listed 350 Yes 62 Fleming NSW 338 Yes 63 Doug Shears NSW 335 64 Scheinberg Family NSW 334 65 Roth Family NSW 334 66 Tony Wales NSW 323 67 Bridgestar (James Fairfax) NSW 300 Yes 68 John Singleton NSW 299 69 Tom Misner NSW 292 70 Andy Plummer NSW 291 71 Allan Moss NSW 288 72 Farrell Family NSW 284 73 Young Family NSW 283 74 Chan Family NSW 279 75 Russell Staley NSW 278 76 Angus & Richard Grinham NSW 271 77 Robert Maple-‐Brown NSW 258 78 Charles Curran NSW 256 79 Roger Fletcher NSW 251 80 Bob Rose NSW 249 81 Chris Ellis NSW 246 82 Ivany NSW not listed 230 Yes 83 Doug Moran NSW 228 84 Lachlan Murdoch NSW 217 NSW # 85 85 John Hunt NSW 215 $63,894

Beville NSW 200 Yes Higgins Brothers NSW not listed 180 Yes ACT # 1

1 Terry Snow ACT 933 Yes $933 350 Other family offices to $100 mil, (est) 11,500

Total Top 350 SFOs $226,574 Top 250 $213,683

Australian Family Office Sector -‐ Review 2011

James Burkitt, +61 417 033 055 [email protected] Family Office Connect, 2012 22

The Australian & New Zealand chapter of this unique family office networking group was formed in September 2010, with a founding members group of 20 principals of leading family offices in the region. The Table Club now has members across the spectrum of the Top 250 single and multi family offices which participate in networking lunches, dinners and workshops throughout each year. The Table Club was pleased to launch its “Ten Tables” plan in 2011 with the hosting of dinners in New York and LA for family office principals. The plan is to establish ten tables in major financial centres, where family office principals shall be the founding members of each table and shall hold dinners each year where the regional chapter hosts and invites other Table Club, (ten tables), members to attend. Each event shall be kept to 20 people. Ten Tables:

• London • Hong Kong • Singapore • Delhi • Shanghai • Sydney • Brazil • New York • LA • Tokyo