fao investment centre - food and agriculture · pdf fileinvestment centre division food and...

TRANSCRIPT

Please address questions and comments to:Investment Centre DivisionFood and Agriculture Organization of the United Nations (FAO)Viale delle Terme di Caracalla – 00153 Rome, Italy [email protected]://www.fao.org/investment/en

Russian Federation: Meat sector reviewReport No. 15 - July 2014 I3

533E

/1/1

1.13

FAO Investment CentreCOUNTRy HIGHLIGHTS

Russian FederationMeat sector review

Ru

ssian Fed

eration

– Meat secto

r reviewR

epo

rt No

. 15

FAO Investment Centre

Rome, 2014

Russian Federation

Meat sector review

Dmitry PrikhodkoEconomist, Investment Centre Division, FAO

Albert DavleyevNational Meat Consultant, Investment Centre Division, FAO

country highlightsprepared under the FAO/EBRD Cooperation

The designations employed and the presentation of material in this information product do not imply the expression of any opinion whatsoever on the part of the Food and Agriculture Organization of the United Nations (FAO) or the European Bank for Reconstruction and Development (EBRD) concerning the legal or development status of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers or boundaries. The mention of specific companies or products of manufacturers, whether or not these have been patented, does not imply that these have been endorsed or recommended by FAO or EBRD in preference to others of a similar nature that are not mentioned.

The views expressed in this information product are those of the author(s) anddo not necessarily reflect the views or policies of FAO or EBRD.

© FAO 2014

FAO encourages the use, reproduction and dissemination of material in this information product. Except where otherwise indicated, material may be copied, downloaded and printed for private study, research and teaching purposes, or for use in non-commercial products or services, provided that appropriate acknowledgement of FAO as the source and copyright holder is given and that FAO’s endorsement of users’ views, products or services is not implied in any way.

All requests for translation and adaptation rights, and for resale and other commercial use rights should be made via www.fao.org/contact-us/licencerequest or addressed to [email protected].

FAO information products are available on the FAO website (www.fao.org/ publications) and can be purchased through [email protected].

For further information on this publication, please contact:DirectorInvestment Centre DivisionFood and Agriculture Organization of the United Nations (FAO)Viale delle Terme di Caracalla, 00153 Rome, Italy

Cover photo: ©Dreamstime

iii

TABLE OF CONTENTS

Foreword v

Acknowledgements vi

Acronyms and abbreviations viii

Executive summary xi

1 Global medium-term meat market outlook with focus on the Russian Federation 1

2 The Russian Federation meat sector in brief 11

3 Detailed review of the meat sector 25

4 Meat processing 60

5 Meat market concentration 68

6 Meat trade 87

7 Meat prices 96

8 Policy 99

Annex 1 Distribution of poultry, swine and cattle inventories by region and type of farm in 2010 120

Annex 2 Main breeds and crosses 133

Annex 3 Meat production technologies 140

Annex 4 Applicable state standards in the Russian Federation 149

Annex 5 Profitability of poultry, pork, and beef production in various administrative subjects of the Russian Federation 153

Annex 6 Leading meat brands 156

Annex 7 Major agroholdings and meat producers in the Russian Federation 158

Annex 8 Recent investments in the poultry sector 168

iv

Annex 9 Broiler meat production (Far East Russian Federation): investment model assumptions, results and sensitivity 171

Annex 10 Recent investments in the pork sector 174

Annex 11 Recent investments in the beef sector 178

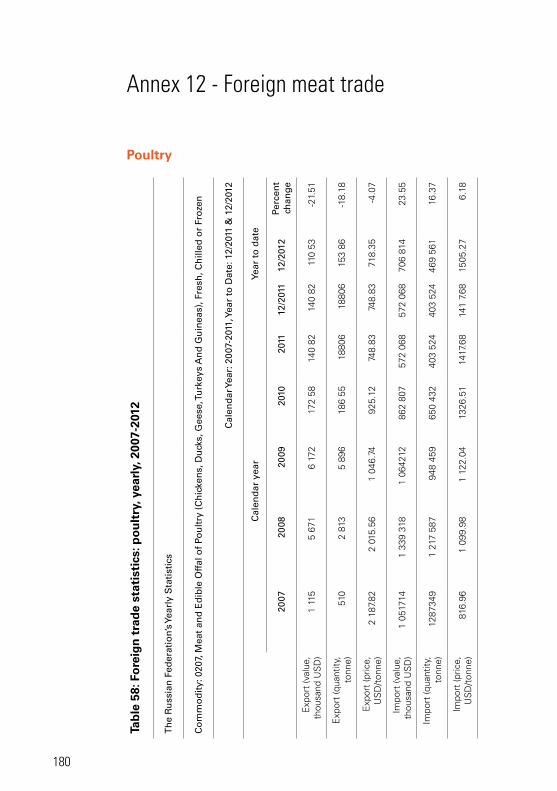

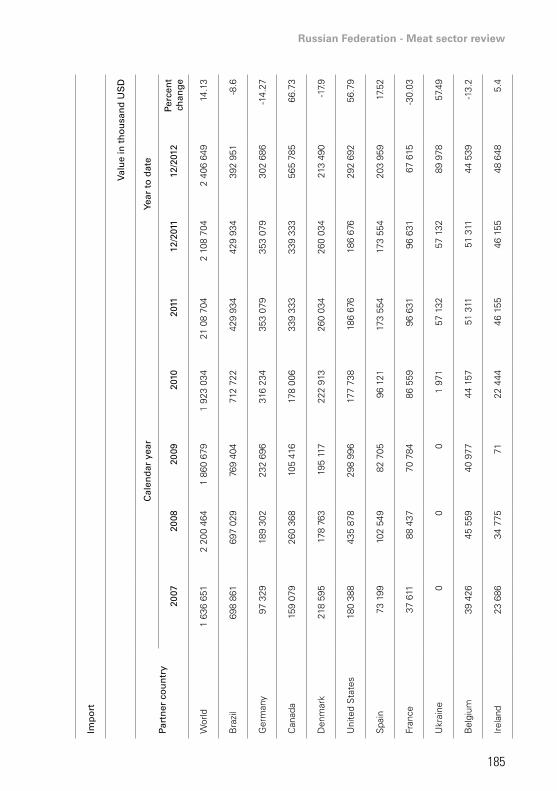

Annex 12 Foreign meat trade 180

v

FOrEwOrd

In recent years, the rise of agroholding farms, combined with strong consumer demand, higher incomes and substantial state support, have prompted an increase of meat production in the Russian Federation. Despite its improved self-sufficiency in the sector, the country will remain one of the principle global meat importers in the foreseeable future. The reduced import tariffs following Russia’s accession to the World Trade Organization (WTO) will put pressure on local meat producers to become more competitive. To do so, they will need to invest in the efficiency of primary production and higher food quality and safety standards.

This review of the Russian meat sector, conducted by the Food and Agriculture Organization of the United Nations (FAO) and the European Bank for Reconstruction and Development (EBRD), aims to inform policy makers and investors and promote a more efficient and inclusive meat sector. It provides information on the role of the Russian Federation in global meat markets, on production and consumption of meat in the country, as well as relevant trade and policy measures. The review presents international comparisons on meat production efficiency, sector concentration and support measures. It also provides information on major players in the Russian meat market and identifies key sector constraints and opportunities.

Readers interested in learning about mid-term prospects in the meat market are encouraged to read the latest version of the Agricultural Outlook jointly produced by the Organization for Economic Co-operation and Development (OECD) and FAO1.

1 http://www.oecd.org/site/oecd-faoagriculturaloutlook/.

vi

ACkNOwLEdgEmENTS

This sector review was prepared by the Investment Centre Division of FAO in the context of the cooperation between FAO and the EBRD. It was financed by FAO and EBRD’s Special Shareholder Fund.

Dimitry Prikhodko, Economist, Investment Centre Division, FAO, and Albert Davleyev, President, Agrifood Strategies, a Moscow-based agribusiness consultancy company, are the main authors of this report. Mr Prikhodko also led the team of other co-authors that contributed to the study. Inna Punda, Agribusiness Officer, Investment Centre Division, FAO, reviewed the initial version of the report and carried out desk research on Russia’s meat trade with Ukraine and within the Customs Union of Belarus, Kazakhstan and the Russian Federation. Vasyl Hovhera, Economist, Investment Centre Division, FAO, provided inputs on meat consumption and on the profitability of broiler meat production. Arianna Carità, Economist, Investment Centre Division, FAO, assisted in reviewing the study and prepared the executive summary. On the EBRD side, Marta Bruska, Operational Leader for this project, provided leadership and coordination.

The FAO/EBRD team would like to express its sincere gratitude to Natalya Zhukova, Senior Banker, Agribusiness, EBRD, Moscow, and Oona Schreiner, Banker, Agribusiness, EBRD, for their constructive comments on current issues and trends in the Russian meat sector. The authors would also like to thank Eugenia Serova, Director, Rural Infrastructure and Agro-industries Division, FAO, for her guidance and inputs at the initial stages of the review.

The report benefited from useful comments by Pedro Marcelo Arias, Economist, Trade and Markets Division, FAO. Specials thanks are extended to Hsin Huang, Secretary General of the International Meat Secretariat (IMS), for his careful review and valuable suggestions.

The authors would also like to thank Emmanuel Hidier, Senior Economist, Investment Centre Division, FAO, and Claudio Gregorio, Chief, Europe, Central Asia, Near East, North Africa, Latin American and Caribbean Service, FAO, for their support and guidance, and Genevieve Joy, Sarah Mercadante and Maria Ricci,

vii

Communications support, Investment Centre Division, FAO, for assisting with the finalization and publication of the report. Maaike Loogman, Joana Maison Aidoo, Eleonora De Feo and Monica Romanelli, Investment Centre Division, FAO, provided excellent administrative support throughout the course of this project.

viii

ACrONymS ANd ABBrEviATiONS

AI avian influenzaAMS aggregate measurement of supportASF African swine fever

EBITDA earnings before interest, taxes depreciation and amortization

EBRD European Bank for Reconstruction and Development

EU European Union

FAO Food and Agriculture Organization of the United Nations

FAPRI Food and Agricultural Policy Research Institute

FIRA First Independent Rating Agency

FMD foot-and-mouth disease

FOB free on board

FSSS Federal Service of State Statistics

GDP gross domestic product

GK group of companies

GNI gross national income

GOR Government of Russian Federation

HACCP hazard analysis and critical control points

HORECA retail, hotel, restaurant and catering services

HS harmonized system

IMS International Meat Secretariat

IRR internal rate of return

KMPP Kornshtadt meat processing plant

LSE London Stock Exchange

MPS market price support

NPC nominal protection coefficient

NPV net present value

OECD Organisation for Economic Co-operation and Development

OIE World Organisation for Animal Health

OJSC open joint-stock company

ix

OKVED Russian Classification of Economic Activities

PPP purchasing price parity

PSE producer support estimate

PSF private subsidiary farming

RAAS Russian Academy of Agricultural Sciences

RUR Russian rouble

SANPIN sanitary norms and rules

SCT single commodity transfers

SPS sanitary and phytosanitary (measures)

TCI Investment Centre Division of the Food and Agricultural Organization

TRQ tariff-rate quota

USDA United States Department of Agriculture

VAT value added tax

VNIIMP All-Russia Scientific Research Institute of Meat Processing Industry

VNIIMS All-Russia Scientific Research Institute Of Meat Cattle Breeding

VNIIZZH All-Russia Scientific Research Institute of Animal Protection

VPSS Veterinary and Phytosanitary Surveillance Service

WB World Bank

WTO World Trade Organization

Russian Federation - Meat sector review

xi

ExECuTivE SummAry

Market development and business considerations

The Russian Federation in the global meat market

World food demand has seen massive changes, including a shift from staple foods to animal proteins and vegetable oils. In the short to medium term, this trend in global food demand will continue. There will be an increased demand for vegetable oils, meat, sugar, dairy products and livestock feed made from coarse grains and oilseed meals.

There are numerous mid-term forecasts for the Russian Federation’s meat sector. Most of them agree on the following trends: (i) the consumption of poultry and pork meat will increase; (ii) the consumption of beef will decrease or stabilize; and (iii) the Russian Federation will remain a net importer of meat on the world market.

According to OECD and FAO projections, meat imports from the Russian Federation will decrease from 3 to 1.3 million tonnes, owing to an anticipated growth in domestic chicken meat and pork production. The country’s share in global meat imports is anticipated to decrease from 12 percent in 2006–2010, to 4 percent in 2021. While the Russian Federation will continue to play an important role in the international meat market, it will fall from its position as the largest meat importing country in 2006–2010 to the fourth largest global meat importer by 2021, behind Japan, sub-Saharan African countries, and Saudi Arabia.

A growing and evolving domestic market

Between 2005 and 2010, the value of the Russian meat market increased by 75 percent, reaching about RUR 930 billion in current prices (equivalent to USD 31 billion) due to growing meat consumption. As a result of higher consumers income, meat consumption in the Russian Federation has been on the rise since the late 1990s. From 2005–2010, the per capita consumption of all meats and meat products increased by 22 percent to reach 64 kg per person per year. Poultry meat consumption increased by 31 percent between 2005 and 2010 to reach 25 kg per person, while pork consumption increased by 38 percent to reach 21 kg per capita. On the other hand, the per capita consumption of beef

xii

and veal decreased by 0.5 percent, down to only 17 kg, during the same period.

Despite a significant anticipated growth by 2021, the per capita consumption of meat in the Russian Federation will most likely remain below that in the United States of America (USA), Brazil, Argentina, Australia and the European Union EU-27, but will exceed the consumption of meat in Ukraine, Mexico, South Korea and China. In recent years, the Russian meat market has experienced some notable transformations, in particular (i) a shift from beef to poultry meat consumption; (ii) the progressive exit of household farms from the market and the expansion of larger commercial farms involved in meat production; and (iii) an increased supply of fresh, chilled meat at the expense of frozen products. The emergence of a large newly affluent urban population in Russian cities has also boosted the development of the retail sector in the country, which has influenced the way meat is sold and consumed. Chicken meat, especially in the form of chicken meat cuts, has replaced beef in everyday diets. However, pork consumption is likely to grow even faster, as it is consumed in many processed ways: sausages, smoked meat, meat delicacies and other value-added products.

From 2005 to 2010, total meat production increased from 7.7 million tonnes to 10.6 million tonnes, with chicken meat production growing from 1.4 million tonnes to 2.8 million tonnes and pork production increasing from 1.6 million tonnes to 2.3 million tonnes, according to official statistics. On the other hand, beef production decreased by 5 percent from 1.8 to 1.7 million tonnes during the same period, reflecting ongoing adjustments in the closely related dairy sector.

The production, processing and supply structure of the meat sector has shown a clear trend towards vertical integration, with inefficient producers going bankrupt and an increased share of commercial farms at the expense of smallholder producers. The share of larger commercial farms in poultry meat production increased from 79 percent in 2005 to 88 percent in 2010 and from 33 to 53 percent in the pork sector, with the remainder being produced by smallholder farms. As beef production is not generally considered profitable by commercial farms, their share in cattle meat production decreased from 36 percent in 2005 to 32 percent in 2010, while the remaining share of smallholders and individual farms increased.

Russian Federation - Meat sector review

xiii

Decreasing role of imports

Imports of meat and edible meat offal decreased by 27 percent from 3.3 million tonnes in 2007 to 2.4 million tonnes in 2012, mostly due to a drastic 64 percent decrease in poultry meat imports during that period. Prior to 2010, poultry meat was the main kind of meat imported into the Russian Federation. It is now the third most important type of imported meat after pork and beef. Imports of edible meat offal for further processing have been quite stable at about 300 000 tonnes per year and are an important source of raw material for meat processors.

Significant room to improve production efficiency

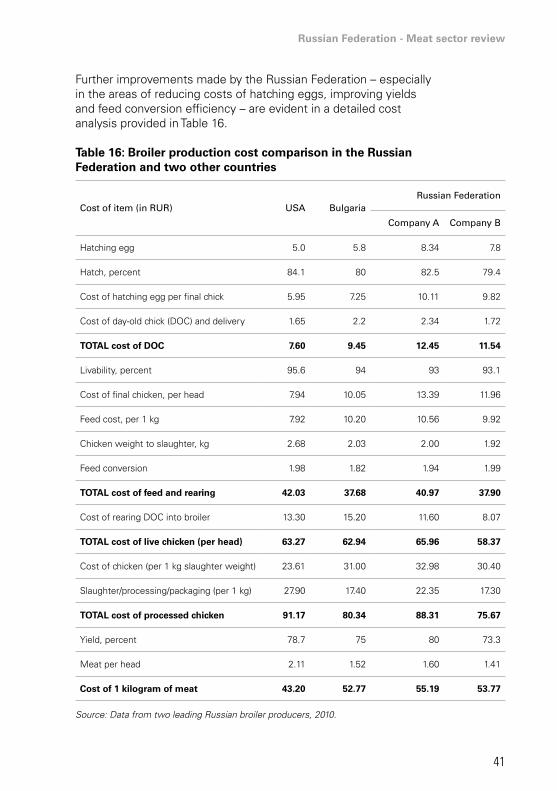

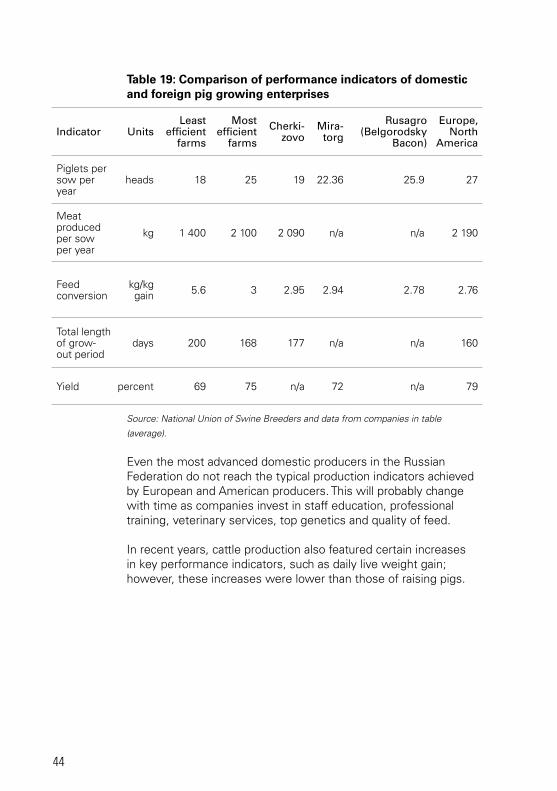

Although Russian meat producers have been effectively protected from import competition by high-tariff and non-tariff barriers, some improvements in meat production efficiency have taken place thanks to an increase in competition among domestic producers. For instance, broiler meat production indicators considerably improved from 2005–2010 thanks to better feeding and nutrition, as well as investment in the modernization of production facilities. As a result, the average daily weight gain of broilers increased from 32 grams in 2000 to 47 grams in 2010. The feed conversion improved from 2.7 kg to 1.85 kg of feed per 1 kg of broiler. However, only leading Russian producers such as Cherkizovo or Miratorg reach feed conversion rates of 1.68 – a level that compares to what Brazilian producers achieve to date. Despite certain improvements in livestock production performance, Russian pork producers lag behind major pork producers from countries such as the USA, Brazil, and the EU.

Strong meat prices will result in sustained export earnings for major global exporters, which will encourage large meat exporting countries to further invest in improving and expanding production and exports despite the high prevailing incidence of food safety and sanitary import bans. These investments in exporting countries will likely put a greater pressure on Russian producers to improve their production efficiency.

As consumers become increasingly aware of sanitary issues, meat producers and processors in the Russian Federation will need to pay more attention to ensuring food safety. Despite improvements in this area and the adoption of the national hazard analysis and critical control points (HACCP) standards, not all meat producers meet national food safety regulations. Producers need to pay particular attention to bacteriological contamination and maximum residue levels. Independent research on salmonella

xiv

prevalence revealed that salmonella was present for 32 percent of whole chickens sold in the Russian Federation, compared to 4 to 16 percent in the USA and the EU. Continuous improvements and investment in food safety will be a key factor for local producers to gain market shares.

Recent investments, risks and profitability

The Russian meat sector has recently experienced an investment boom due to high profits and growing demand sustained by market protection and state support programmes. According to available information on ongoing and planned investments for 2009–2014, the Russian meat sector has attracted a total of USD 7.2 billion in investment. Poultry production on its own has attracted about 44 percent of all meat sector investments, while pork and beef production have attracted 33 percent and 15 percent respectively. An additional USD 540 million in investment was also observed in the meat processing sector. It should be noted, however, that the recent global economic recession has forced some Russian companies to review their ambitious business expansion plans and put some meat production projects on hold.

Similar to those in other countries, Russian meat producers face a number risks: (i) adverse production conditions and poor infrastructure (low production efficiency, poor feed quality, exposure to volatile feed grain prices, difficult access to transportation infrastructure, power outages, etc.); (ii)) animal and poultry disease outbreaks and food safety hazards (avian influenza, African swine fever, foot-and-mouth disease, etc.); (iii)) investment and financial risks (increase in interest rates, etc.); and (iv) policy-related risks (changing government priorities, high level of market protection, etc.). These are described in Chapter 2 of this report.

The analysis conducted in this review shows that, while investments in new broiler meat production can still be profitable in the Russian Federation under standard market assumptions on local input/output prices and the cost of capital, such investments have a rather long average payback period of nine years and are highly sensitive to feed price increases. An increase in feed costs of only 10 percent would make these investments unprofitable. At the same time, a reasonable improvement in feed conversion would increase the investments internal rate of return (IRR) from 15 to 18 percent and decrease the payback period to eight years.

Russian Federation - Meat sector review

xv

Foreseen meat processing consolidation

Russian meat processing, unlike poultry meat production, is characterized by rather low consolidation owing to the country’s vast national territory, consumers’ preferences for local regional producers and trademarks, and a general lack of the processors’ capacity to market brands at the national level. It is very likely that sector consolidation will occur in the near future. In order to meet its potential, the private sector needs to modernize and improve its basic production efficiency. These improvements would require substantial private investment in areas such food safety and biosecurity, environmental sustainability through the introduction of better livestock management practices, and improved breeding stock.

Policy considerations

The fast growth experienced by the meat sector in the Russian Federation in recent years has been supported by policy measures, including import tariffs and domestic support. Although competitiveness features as one of Russia’s main agricultural policy goals, the country’s agricultural support system has been driven by a progressive policy orientation towards import substitution and higher self-sufficiency in meat and other food products. While livestock production may play an important role in economic growth and the need for adequate investment in that sector is clear, Russia’s food self-sufficiency approach may be questioned from an economic point of view.

Meat market protection and support come at a high price

Russia’s agricultural policy objectives have been pursued at a relatively high cost to Russian taxpayers and consumers. Most support is provided through market price support, supply of inputs and fixed capital (investment subsidies and interest rates), all of which are among the most market distorting policy measures.

According to OECD’s monitoring of annual monetary transfers from consumers and taxpayers to farmers, measured as the Producer Support Estimate (PSE), Russian producers of grains and oilseeds – the main sources of feed protein in the country – appear to be “taxed”. At the same time, annual transfers to domestic producers of poultry and livestock averaged RUR 227 billion (USD 6,3 billion) throughout 2008–2010. More specifically, 20 percent of gross income received by beef and veal farmers, 45 percent of incomes from pork and 34 percent of incomes from poultry meat came from consumers and taxpayers. Russia’s main interventions in the sector consist of market-price support. Due to tariff and non-tariff

xvi

measures, domestic prices for beef, pork and poultry end up being much higher that international reference prices.

Improving competitiveness

Russian meat producers have a favourable access to feed grains and meals as the country is a net exporter of wheat, barley, corn and sunflower meals and other compound feed ingredients. Therefore, improving the competitiveness of Russian meat producers primarily means bridging the gap between the domestic and import parity prices. The gap between domestic and international prices increased considerably from USD 470–900 per tonne of various kinds of meat in 2001 to USD 900–1 200 in 2010. Domestic pork prices were often twice as high as international pork prices at import parity levels. Domestic beef appeared to be more competitive with imports than poultry and pork.

Protectionist policies will not help the domestic meat industry to become competitive in the long-term. While the level of domestic market protection and state support remain very high in the Russian Federation, other major meat producers, like the USA and Brazil, have limited price-distorting support measures or, as it is the case for the EU, tend to reduce their support measures to meat producers.

WTO accession

The Russian Government managed to defend a substantial domestic market protection level at World Trade Organization (WTO) accession, including Tariff-Rate Quotas (TRQs) for poultry meat and beef with high out-of-quota rates. For pork, the Russian Federation has agreed to a TRQ of 400 000 tonnes for fresh, chilled and frozen pork with a zero in-quota tariff. As of 1 January 2020, the Russian Federation will adopt a tariff-only regime for pork with a bound duty of 25 percent. Therefore, the domestic pork market will be more open to import competition.

State support programmes

State support programmes focus on extending long-term credit at low interest rates to livestock breeding and other regional programmes. They have attracted many entrepreneurs. For example, interest rate subsidies for livestock production from the federal budget – aimed at supporting the construction, reconstruction and modernization of livestock and poultry facilities – totaled RUR 2.36 billion (USD 66 million) and attracted RUR 155 billion (USD 4,3 billion) worth of credit to 492 projects

Russian Federation - Meat sector review

xvii

in 2010 alone. In 2011, overall state subsidies to the livestock and poultry industries, disbursed under various support programmes, amounted to RUR 22.8 billion (USD 636 million). As domestic meat markets appear to be highly distorted, the extent to which investment decisions have been driven by rational business considerations is unclear. Many companies also complain about the excessive documentation requirements and the lack of transparency in decision making by officials responsible for the distribution of state support.

To ensure the long-term competitiveness of Russia’s meat sector, it would be highly desirable to refocus domestic budget support to food safety improvements, feed quality monitoring, research, education, training and other non-distorting support measures. Effective food safety vs. sanitary-based trade restrictions

While ensuring food safety is a paramount task for all governments, it appears that the attention of Russia’s food safety authorities primarily focuses on imported meat products. Furthermore, some WTO member countries have pointed out that Russia’s sanitary regulations regarding maximum residue levels are often not scientifically based.

It would be highly desirable for the Russian Federation to build a comprehensive national food safety monitoring system. This system would monitor microbiological, antibiotic and other residue levels on a continuous basis and keep track of improvements in food safety over time, thus building consumer confidence regardless of product origin.

As knowledge becomes increasingly important in the livestock and poultry sectors, public investment in education and training will also be critically important. For the moment, the lack of professional skills at all levels – from nutritionists to farm managers – often forces private companies to invest in their own educational programmes. Public-private partnerships in the field of agricultural education could also address this critical gap.

Russian Federation - Meat sector review

1

Chapter 1 - global medium-term meat market outlook with focus on the russian Federation

Production

Global demand for meats will increase and mostly stem from large economies in Asia, crude oil exporting countries and Latin America according to the FAO-OECD Agricultural Outlook (2012)2. Poultry meat will lead this anticipated growth as the cheapest and most accessible source of meat protein overtaking pork as the largest meat sector by 2021 (see Figure 1).

Figure 1: World beef, pork and poultry production and forecast, 1998-2021

0

20

40

60

80

100

120

140

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

Forecast

mill

ion

to

nn

es

Poultry meat (rtc)Pig meat (cwe)Beef and veal (cwe)

Source: OECD-FAO Agricultural Outlook 2012.

High feed costs in 2010-2012, a slowdown in demand and weak economic conditions combined to reduce producer returns in the livestock sector, encouraging producers to reduce animal inventories, which slowed total meat production in the years prior

2 This chapter includes findings from the FAO-OECD Agricultural Outlook and its medium-term projections for the period 2012-2021. Because FAO and OECD Secretariats revise projections on an annual basis, the readers are encouraged to refer to the latest projections available. The outlook database, including historical data and projections, is available through the joint OECD-FAO internet site: www.agri-outlook.org.

2

to 2012. Higher producer prices, with feed costs easing in the short term, can be expected to improve meat margins and set the stage for some expansion in production of red meats and poultry in 2012-2013.

It is anticipated that global production of beef, pork and poultry meat will increase from 262 million tonnes in 2005-2010 (average annual) to 330 million tonnes in 2021 (up 26 percent) in response to growing demand. During the same period, production of the same kinds of meat in the Russian Federation is anticipated to increase from 6 million tonnes to 9.4 million tonnes (up 56 percent). Because of anticipated increases in poultry meat, the Russian Federation will increase its share in global meat production from 2 percent in 2006-2010 (on average) to 3 percent by 2021 (see Figure 2).

Figure 2: Global meat production, share of the Russian Federation’s production and forecast, 2001-2021

7,3-

200

250

mill

ion

to

nn

es

350

300

150

100

50

20012005

20062010

20112012

20132014

20152016

20172018

20192020

2021

234262

278 282 286 292 298 303 309 314 319 325 330

4.6 6.0 7.3 7.7 8.0 8.3 8.4 8.6 8.7 8.9 9.0 9.2 9.4

percen

t

Share of Russian Federationin production (right axis)

Russian production(left axis)

World production(left axis)

3

2

1

0

Source: OECD-FAO Agricultural Outlook 2012.

Note: The meat total combines beef, pork and poultry meat only.

Global bovine production, which has stagnated in recent years, is anticipated to start growing more rapidly as herds rebuild. However, poultry will likely remain the fastest growing sector (2.2 percent p.a.) and will produce the highest volume of all meats worldwide by 2021.

Productivity growth throughout the global meat production chain has been significant in recent years. Herds have improved through better breeding and herd management practices, especially improved feeding practices. These improvements have enabled

Russian Federation - Meat sector review

3

growth in meat production efficiency. Despite rising input costs, meat production has grown about 300 percent in the past50 years, and livestock inventories – the number of cattle, swine, chicken and ovine animals – have grown by 57 percent, 137 percent, 400 percent and 49 percent respectively. The change in offtake3, or the quantity of meat produced per animal, has therefore increased substantially over time.

Historical growth in offtake ratios has been high for a number of emerging countries, particularly Brazil and China. In India and the Russian Federation, growth in offtake ratios has been for pork (see Table 1). The offtake ratios depend on many factors, such as the type of meat production system (intensive, pastoral, etc.), consumer preferences and other factors that vary greatly among countries. For instance, offtake ratios and their growth appear very low for some countries in Africa as animals may be kept for farm and work purposes.

Apart from increased farm productivity, improvements in supply chain management, in particular cold chain management, have and will continue to have a very important impact on the growth of this sector. This is especially true in many developing countries where storage and transportation of meat have been limited.

3 Offtake ratios are computed as gross meat production divided by animal inventories.

4

Tab

le 1

: Tre

nd

s in

mea

t o

ffta

ke r

atio

s in

sel

ecte

d c

ou

ntr

ies

Bov

ine

mea

tPo

rkPo

ult

ry m

eat

Off

take

ra

tio

Gro

wth

Pro

ject

edO

ffta

ke

rati

oG

row

thPr

oje

cted

Off

take

ra

tio

Gro

wth

Pro

ject

ed

2005

-09

1985

-201

120

12-2

120

05-0

919

85-2

011

2012

-21

2005

-09

1985

-201

120

12-2

1

kg/h

ead

per

cen

t/yr

per

cen

t/yr

kg/h

ead

per

cen

t/yr

per

cen

t/yr

kg/h

ead

per

cen

t/yr

per

cen

t/yr

Arg

entin

a60

0.5

0.3

122

4.2

2.3

144.

62.

5A

ustr

alia

158

1.3

0.7

144

1.2

0.7

91.

40.

8B

razi

l45

2.5

1.5

835.

33.

29

4.4

2.7

Can

ada

126

0.1

017

42

1.1

70.

70.

4

Chi

na55

8.5

4.9

108

31.

7 3

3.2

1.8

EU

-27

910.

10

144

10.

78

0.5

0.3

Japa

n13

3-0

.3-0

.213

0-0

.2-0

.113

1.8

1.1

Ru

ssia

n

Fed

erat

ion

80-2

.7-1

.712

23.

22

58.

41.

1

Sou

th A

fric

a57

1.1

0.5

139

2.9

1.5

7.7

0.1

0U

nite

d S

tate

s of

Am

eric

a12

00.

80.

515

30.

90.

58

1.4

0.8

Wor

ld42

0.3

0.3

111

1.5

1.2

4.6

1.2

0.8

Sou

rce:

OE

CD

and

FA

O S

ecre

taria

ts.

Not

e: G

row

th e

stim

ates

for

the

Eur

opea

n U

nion

(EU

-27)

and

the

wor

ld a

re li

mite

d to

the

per

iod

star

ting

from

199

6, t

he R

ussi

an F

eder

atio

n fr

om 1

992.

Russian Federation - Meat sector review

5

Trade

The latest available OECD-FAO projections at the time of preparing this report suggested that global imports of beef, pork and poultry meat will increase from 24 million tonnes per year (on average) in 2006-2010 to 31 million tonnes in 2021, an increase of 27 percent. The Russian Federation will decrease its meat imports from 3 to 1.3 million tonnes in the same period (down 57 percent) due to anticipated growth in domestic chicken meat and pork production. The share of the Russian Federation in global meat imports will also decrease from 12 percent in 2006-2010 to about 4 percent in 2021 (see Figure 3). From being the largest meat importers in the world in 2006-2010, by 2021 the Russian Federation is anticipated to move to the fourth position on the global import list after Japan, the sub-Saharan African countries and Saudi Arabia (see Figure 4). Figure 3: Global imports of meat, share of the Russian Federation’s imports and forecast, 2001-2021

19

2427 27 28 28 28 29 29 30 30 30 31

2.4 3.0 2.3 2.0 1.9 1.7 1.7 1.6 1.6 1.5 1.5 1.3 1.3

1312

9

77

6 6 6 5 5 54 4

0

5

10

15

20

25

30

35

20112012

20132014

20152016

20172018

20192020

2021

0

2

4

6

8

10

12

14

mill

ion

to

nn

es

percen

t

2006-2010

2001-2005

Share of Russian Federationin production (right axis)

Russian imports(left axis)

World trade(left axis)

avg

avg

Source: OECD-FAO Agricultural Outlook 2012.

Note: The meat total combines beef, pork and poultry meat.

6

Figure 4: Net meat trade balance in 2006-2010 and forecast for 2021 of major exporters and importers

-3 000 -1 000 1 000 3 000 5 000 7 000JapanSub Sharan AfricaSaudi ArabiaRussian FederationKoreaMexicoViet NamEgyptPhilippinesRepublic of South AfricaChinaIndonesiaMalaysiaTurkeyKazakhstanUkraine

UruguayNew Zealand

ArgentinaIndia

ThailandAustraliaCanada

European Union-27United States

Brazil

2021 (forecast)2006-2010 (average)

Source: OECD-FAO Agricultural Outlook 2012.

Note: The meat total combines beef, pork and poultry meat.

The growth in world meat imports is forecast despite strong anticipated meat prices through 2021. Population, income growth and high-income elasticity of demand will drive meat imports of developing countries.

Led mostly by an expansion of poultry and beef shipments, world meat exports will increase to respond to the growing demand. The bulk of the growth is expected to originate largely from North and South America, which will account for nearly 70 percent of the total increase in all meat exported by 2021. The two largest contributors to export growth are the USA and Brazil, both of which will strengthen their dominance in world meat trade. By 2021, the USA and Brazil will generate nearly 80 percent of the expansion of world poultry trade.

Russian Federation - Meat sector review

7

Brazil, Australia, India, Canada, Argentina, New Zealand, Uruguay and Paraguay will be the main exporters of beef. Japan, the Russian Federation, the USA, Korea and Egypt will be its major importers. It is also expected that Iran and Viet Nam will continue increasing beef imports in the future.

The EU, USA, Canada and Brazil will remain the main exporters of pork with Japan, the Koreas, Mexico, the Russian Federation and the sub-Saharan Africa countries being the main buyers by 2021. As for poultry meat, Brazil, the USA, Thailand, the EU and Argentina are expected to be the main exporters with the sub-Saharan Africa countries, Saudi Arabia, Viet Nam, Mexico and China being the main poultry meat importers by 2021.

Consumption

World consumption of beef, pork and poultry meat will continue to grow at one of the highest rates among major agricultural commodities. Together with other factors such as changing consumer attitudes and preferences and relative prices, overall meat demand will be affected by two factors: population and income growth. In the past 30 years worldwide population growth contributed 60 percent to the overall growth in meat consumption with the remaining 40 percent being attributed to an increase of per capita income and per capita consumption growth. As shown on Figure 5, average global meat per capita consumption directly correlated4 with the per capita gross national income (GNI) measured at the purchasing price parity basis (PPP).

4 The correlation index between per capita meat consumption and gross national income (GNI) in 1980-2009 was 0.978 – pointing to a very strong correlation. Although the correlation was direct, it was less than proportionate. An average of 4.79 percent annual increase in per capita GNI generated an average 1.06 percent annual increase in per capita meat consumption, as consumers were also allocating income to other products and services.

8

Figure 5: World per capita meat consumption and income, 1980-2009

2 000

4 000

6 000

8 000

10 000

12 000

19801982

19841986

19881990

19921994

19961998

20002002

20042006

2008

18

23

28

33

38

43

PPP GNI per capita (left axis)

cur

rent

inte

rnat

iona

l dol

lars

kg

0

Consumption per capita (right axis)

Source: Authors’ calculations based on FAO Stat and World Bank Data.

It is expected that global per capita meat consumption will increase until 2021 with poultry accounting for 70 percent of anticipated growth (see Figure 6).

Growth in developing countries is forecast to capture 82 percent of the additional global consumption by 2021. The per capita consumption of meat in the USA, the EU and Japan is not anticipated to change significantly from the levels observed in 2006-2010. However, it is anticipated to increase considerably in Uruguay, Brazil, Argentina, Chile, Malaysia, the Russian Federation, Ukraine and other countries, reflecting consumer income growth. In Eastern Europe, consumption of red meat still has a substantial growth potential and will also increase.

Russian Federation - Meat sector review

9

Figure 6: Annual per capita meat consumption in 2006-2010 and forecast until 2021

Isra

el

Uru

guay

Uni

ted

State

s

Brazil

Argen

tina

Austra

lia

Chile

Euro

pean

Uni

on-2

7

Russi

an F

eder

atio

nM

alay

sia

Ukr

aine

Korea

Mex

ico

China

Kanza

khst

an

Saudi

Ara

bia

Viet N

am

Japa

n

Wor

ld a

vera

ge

Turk

eyTh

aila

nd

Repub

lic o

f Sau

th A

frica

7597 87

78 7861 65

50 50 38 44 46 41 42 41 38 35 33 31 18 19

97 97 93 90 87 8370 64 61 60 54 53 53 52 49 49 47 46

34 3425 2371

2006 - 2010 (average)

120

100

80

60

40

20

0

2021 (average)

kg

Source: OECD-FAO Agricultural Outlook 2012.

Note: The meat total combines of beef, pork and poultry meat. Data may differ from

official consumption estimates made by the Russian Government provided in this report.

Uncertainties

The meat sector is highly sensitive to macroeconomic conditions policy conditions and animal health and food safety issues; this poses a significant risk to the validity of the projections provided in this chapter. Changes in oil prices and civil unrest have the potential to impact world meat trade. Animal diseases and changes in food safety regulations have the potential to affect domestic and regional meat production and consumers’ preferences. For instance, the Russian Federation imposed sanitary restrictions on meat imports from a number of Brazilian states in May 2011. The ban resulted in a substantial contraction of bilateral trade on beef and pork and the end of two years of almost uninterrupted monthly increases of world meat prices.

Increasing consumer awareness of the livestock sector’s use of water resources, its contribution to greenhouse gas emissions and animal welfare issues will also likely affect demand for different kinds of meat, especially in developed countries. These factors affecting demand also need to be considered by potential investors.

10

It is currently expected that strong meat prices will result in sustained export earnings, which will encourage large meat exporting countries to further invest in production and exports despite the high incidence of food-safety and sanitary import bans. This investment in exporting countries will likely put increased competitive pressure on producers in the Russian Federation as the country is expected to liberalize meat imports in line with its WTO commitments.

Russian Federation - Meat sector review

11

Chapter 2 - The russian Federation meat sector in brief

Importance of the meat sector for the economy

Agriculture accounted for about 6 percent of Russian Federation’s gross domestic product (GDP) in 2010. The livestock sector inclusive of all livestock, dairy and poultry – accounted for about 50-55 percent of agriculture output with the remaining output coming from crops and plant products (mostly grain, oilseeds, pulses, fruits, vegetables, etc.). Beef, veal, pork, poultry, sheep, goat and other kinds of meat accounted for about 38-43 percent of overall livestock sector production in 2005-2010 and 19-23 percent of the total agricultural production (see Table 2).

Table 2: Role of livestock and meat in Russian agriculture and economy, billion RUR, 2005-2010

Indicator 2005 2006 2007 2008 2009 2010

GDP 21 610 26 917 33 248 41 277 38 809 45 166

of which:

Agricultural products 1 381 1 571 1 932 2 461 2 516 2 619

Agricultural products, % GDP 6.4 5.8 5.8 6 6.5 5.8

of which:

Livestock sector 711 806 929 1 155 1 277 1 439

of which:

Meat from livestock and poultry 295 328 367 442 556 591

Meat, % GDP 1.4 1.2 1.1 1.1 1.4 1.3

Meat, % ag output 21.4 20.9 19 18 22.1 22.6

Meat, % livestock sector 41.5 40.7 39.5 38.3 43.6 41.1

Source: Based on Federal Service of State Statistics (FSSS) of Russian Federation.

Note: Found in “Russian Classification of Economic Activities (OKVED), # 01.02, under

subsection DA 15.1 “Production of meat and meat products”.

12

The percentage of the population employed in agriculture (including both crop and livestock production) declined from 10 percent in 2005 to 8 percent in 2011 according to official statistics (FSSS) as trade, finance, construction and other sectors attract more employees.

According to official statistics, 606 000 people were employed in meat production in 20105. As their productivity increases, the number of employees involved in meat production and processing declines and incomes increase (see Table 3).

Table 3: Employees and incomes in meat and meat product production, 2005-2010

2005 2006 2007 2008 2009 2010Change 2011 vs.

2005

Payroll fund for all employees, RUR billion/year

50 54 63 72 77 82 65%

Average number of all employees, thousand persons

1 167 1 003 888 695 639 606 - 48%

Average annual gross income per employee, RUR/month

3 544 4 515 5 948 8 583 10 056 11 294 219%

Source: FSSS.

Note: Income in current prices.

The meat processing industry alone accounts for about 7 percent of the 2.5 million people employed in the country’s food processing industry. The number of employees in the meat processing sector increased from 165 000 people in 2005 to 189 000 people in 2010, reflecting an overall expansion. This expansion underlines the importance of the industry as a source of local job creation.

In addition to formal employment, raising livestock and poultry play a significant role in informal or self-employment in the Russian Federation as smallholder producers still account for a sizable share in total livestock production. Despite the decreasing share of smallholder farms in total livestock production – from 54 percent (2.7 million tonnes of livestock in slaughter height) in 2003 to 34

5 Found in “Russian Classification of Economic Activities (OKVED), # 01.02, under subsection DA 15.1 “Production of meat and meat products”.

Russian Federation - Meat sector review

13

percent (2.5 million tonnes) in 2011,compared with commercial farms that increased livestock production from 2.2 to4.8 million tonnes – small livestock producers are still an important source of rural employment and incomes in the Russian Federation. Poultry, pork and beef account for 91 percent of all meat products in the Russian Federation (2010, FAO Stat) namely: poultry meat for 38 percent of all meat output, pork for 32 percent and beef and veal for 21 percent. According to national statistics, mutton and lamb are important meats especially in the Southern and North Caucasian Federal Districts. The latter types of meat were not included in this review because sheep meat accounts for only 2 percent, horse meat for 1 percent and other types of meat for 4 percent of the nation-wide total meat output.

Meat market development and outlook until 2021

The Russian meat sector has been undergoing a major transition, which is largely unprecedented in modern history and has followed the breakup of the Soviet Union in 1991. The downward trend in cattle inventories began in 1990. Cattle numbers declined from 59 million heads to 28 million heads in 2000 and then below 21 million heads in 2010, thus registering a tremendous 65 percent decrease in livestock numbers since 1990. This downward trend has slowed in recent years, but it is still ongoing. Amongst all transition economies in the EBRD regions of operation, only Ukraine witnessed such a drastic decrease in the number of cattle herds: from 25 million heads in 1990 to 5 million in 2010, or an 80 percent decrease.

The decrease in livestock inventories can partially be attributed to the adjustments in the closely related dairy sector. As farmers increased productivity of the milk heard, they continued slaughtering dairy and dual-purpose cows. Specialized beef production is almost non-existent in the Russian Federation, so dairy and dual-purpose cows slaughter has been reflected in lower cattle inventories and decrease of domestic beef production potential. This downward trend in cattle inventories inevitably resulted in decreased domestic beef production and increased imports.

Swine inventories also decreased dramatically from 40 million heads in 1990 to 18 million in 2000. But the downward trend was reversed in 2005 owing to generous state support and trade measures. Nevertheless, the Russian Federation still witnessed a 57 percent decrease in swine numbers from 1990 to 2010. Poultry production has witnessed the fastest recovery during the

14

same period, because it is a sector that allows for a shorter payback period on investments as compared with pork and beef production. In 2006, poultry meat became the most important meat type produced in the Russian Federation, and by 2010 farmers produced 180 percent more chicken meat than in the early 1990s.

There are number of outlooks on the short- and medium-term perspectives of the Russian meat sector. These outlooks are prepared at national and international levels and use different approaches. Box 1 below briefly discusses the main sector development forecasts available.

Russian Federation - Meat sector review

15

Box 1: Mid-term meat production forecasts for the Russian Federation and their various sources

According to official statistics, production of all kinds of meat in Russia has been growing fast while meat imports have decreased since 2009 (see Table 4). The Russian Government, in its Strategy of Livestock Production Development in the Russian Federation untill 20201, forecasts that the total production of all types of meat will reach 9.6 million tonnes, imports will decrease to 0.6 million and domestic consumption will increase to 9.9 million tonnes by 2020. The same strategy envisages that Russia will export 0.6 million tonnes of meat, including 400 000 tonnes of poultry and 200 000 tonnes of pork (Table 4).

The latest available forecast by OECD-FAO at the time of report finalization2 suggested that the Russian meat production (beef, pork and poultry) might increase to 9.4 million tonnes by 2020 – an estimate very similar to the Russian Ministry of Agriculture’s. The latest results of meat trade simulations conducted by FAO in February 2013 suggest that meat imports may decrease from earlier forecasted levels; however, it is doubtful that the Russian Federation would be able to export 0.6 million tonnes of all kinds of meat considering its strong domestic demand.

In this review, forecasts from both the government of the Russian Federation and the OECD-FAO Mid-term Agricultural Outlook are mostly used.

Similar to OECD-FAO Agricultural Outlook, there are other sources of mid-term market outlook that are based on global partial-equilibrium econometric models. For instance, the USDA’s international baseline projections3, suggest that Russian meat production will increase to 12.5 million tonnes by 2020 (including 6.7 million tonnes of beef, 2.4 million tonnes of pork and 3.4 million tonnes of poultry meat) while imports will remain high at about 2 million tonnes (e.g. will not show signs of drastic decrease and will reflect more rapidly increasing domestic consumption).

Interested readers can also refer to the outlook by the Food and Agricultural Policy Research Institute (FAPRI), which covers beef, pork and poultry sectors in the Russian Federation and Ukraine among other countries.

1 Approved by the Order No. 267 by the Russian Federation Ministry of Agriculture, dated 10 August 2011; published by the Ministry of Agriculture of the Russian Federation in August 2011, http://mcx.ru/documents/document/show/16974.77.htm, Russian version only).

2 May 2012, http://www.oecd.org/site/oecd-faoagriculturaloutlook).

3 (January 2013), available at http://www.ers.usda.gov/data-products/international-baseline-data aspx.

16

Figure 7 shows a historical perspective of beef and veal, pork and poultry meat production in the Russian Federation starting in 1998. It also provides a medium-term OECD-FAO meat production outlook until 2021 based on the 2012 projections.

Figure 7: Russian Federation’s production of beef, pork and poultry in 1998-2011 and mid-term outlook until 2021

4 500

4 000

3 500

3 000

2 500

2 000

1 500

1 000

500

0

10

9

8

7

6

5

4

3

2

11998

20002002

20042006

20082010

20142020

20182016

2012

th

ou

san

d t

on

nes

percen

t

4 113

3 1191

2 068

3 179

2 461

1 710

Beef and veal (cwe) (left axis) Pigmeat (cwe) (left axis)

Poultry meat (rtc) (left axis)

Share of Russian Federation in world poultry meat (right axis)

Share of Russian Federation in world pigmeat meat (right axis)

Share of Russian Federation in world beef and veal production (right axis)

Source: OECD-FAO 2012.

Production of meat in the Russian Federation has been growing fast while meat imports have decreased since 2009, according to official statistics. This trend is expected to continue in the future (see Table 4 and for more details Box 1).

Table 4: All meats supply and demand, thousand tonnes, 2005-2020

2005 2006 2007 2008 2009 2010 2015* 2020*

Production 4 920 5 209 5 722 6 202 6 648 7 090 8 688 9 636

Consumption 7 505 7 894 8 505 9 134 9 072 9 139 9 678 9 876

Import 2 585 2 685 2 784 2 935 2 423 1 930 1 050 640

Export 0 0 1 3 6 19 100 600

Source: FSSS of Russian Federation, Meat Union of Russia and Meatinfo.

* Forecast from Strategy on Livestock Production Development in the Russian Federation until 2020.

Russian Federation - Meat sector review

17

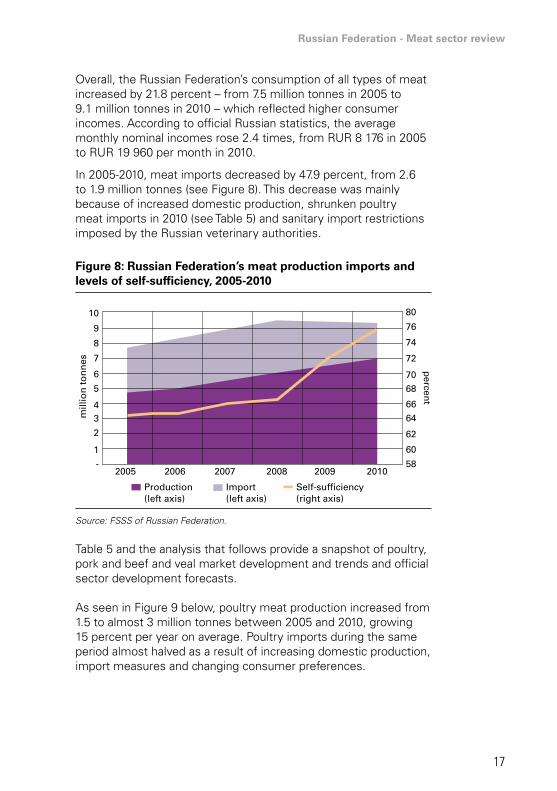

Overall, the Russian Federation’s consumption of all types of meat increased by 21.8 percent – from 7.5 million tonnes in 2005 to 9.1 million tonnes in 2010 – which reflected higher consumer incomes. According to official Russian statistics, the average monthly nominal incomes rose 2.4 times, from RUR 8 176 in 2005 to RUR 19 960 per month in 2010.

In 2005-2010, meat imports decreased by 47.9 percent, from 2.6 to 1.9 million tonnes (see Figure 8). This decrease was mainly because of increased domestic production, shrunken poultry meat imports in 2010 (see Table 5) and sanitary import restrictions imposed by the Russian veterinary authorities.

Figure 8: Russian Federation’s meat production imports and levels of self-sufficiency, 2005-2010

10

6

8

7

9

5

4

2

1-

2005 2006 2007 2008 2009 2010

64

62

6870

66

72

74

60

58

3mill

ion

to

nn

es percen

t

80

76

Import(left axis)

Production(left axis)

Self-sufficiency(right axis)

Source: FSSS of Russian Federation.

Table 5 and the analysis that follows provide a snapshot of poultry, pork and beef and veal market development and trends and official sector development forecasts.

As seen in Figure 9 below, poultry meat production increased from 1.5 to almost 3 million tonnes between 2005 and 2010, growing 15 percent per year on average. Poultry imports during the same period almost halved as a result of increasing domestic production, import measures and changing consumer preferences.

18

Table 5: Supply and demand for different types of meat and its forecast, thousand tonnes, 2005-2020

Indicator 2005 2006 2007 2008 2009 2010 2015* 2020*

Production 1 388 1 632 1 925 2 217 2 555 2 847 3 850 4 251

Poultry

Consumption** 2 706 2 906 3 219 3 438 3 541 3 512 4 030 3 941

Import 1 318 1 274 1 295 1 224 986 661 240 90

Export 0 0 1 3 6 19 *** 60 400

Pork

Production 1 569 1 699 1 930 2 042 2 170 2 331 2 925 3 389

Consumption 2 154 2 361 2 615 2 864 2 836 2 970 3 165 3 439

Import 585 662 685 822 667 639 240 50

Export 0 0 0 0 0 0 40 200

Beef

Production 1 809 1 722 1 699 1 769 1 741 1 727 1 715 1 786

Consumption 2 484 2 456 2 488 2 643 2 502 2 463 2 285 2 286

Import 674 734 789 874 760 621 570 500

Export 0 0 0 0 0 0 0 0

Source: FSSS, Meat Union of Russia and Meatinfo.

* Forecast from Strategy on Livestock Production Development in the Russian

Federation until 2020.

** Consumption of meat and meat products calculated as raw meat equivalent. Data

exclude pork fat and edible by-products.

*** Other sources state 15 000 tonnes.

Russian Federation - Meat sector review

19

Figure 9: Russian Federation’s production, imports and self-sufficiency in poultry meat, 2005-2010

4.0

3.5

3.0

2.5

2.0

1.5

1.0

0.5

- 0

10

20

30

40

50

60

70

80

2005 2006 2007 2008 2009 2010

Production(left axis)

Import(left axis)

Self-sufficiency(right axis)

mill

ion

to

nn

es percen

t

Source: FSSS of Russian Federation

Poultry inventories, slaughter and live weight (yield6) directly influenced meat production, and Table 6 illustrates these relations in the Russian Federation using chicken inventories and slaughter. It is clear that the growth in chicken inventories and slaughter was the main reason behind increased meat production. It should be noted that the information provided in Table 6 includes all chickens, those raised by private households for meat and eggs as well as the meat received from spent hens at the commercial egg production farms.

In six years, from 2005 to 2011, chicken slaughter increased by 91 percent, while meat yield increased by only 13 percent, from 1.4 kg per head in 2005 to 1.58 kg per head in 2011. Broiler yields are believed to have increased even more rapidly.

6 Meat yields indicate the carcass weight equivalent after animal slaughter (for cattle or swine) or ready-to-cook equivalent for poultry meat.

20

Table 6: Chicken inventories, slaughter, yields and meat production in the Russian Federation, 2005-2011

2005 2006 2007 2008 2009 2010 2011Change 2011 vs.

2005

Chicken inventories as of Jan. 1, mln head

329 343 358 351 366 391 406 24%

Chicken slaughter, mln head 96 108 125 132 151 166 184 91%

Chicken meat production, mln tonnes

1.35 1.58 1.87 2.00 2.31 2.56 2.91 116%

Yield, kg/head 1.40 1.47 1.50 1.52 1.53 1.55 1.58 13%

Source: FAO Stat based on official Russian statistics.

Note: Includes only chicken inventories and production.

The Russian Federation’s pork production expanded by 49 percent from 2005 to 2010 and was accompanied by a 38 percent increase in consumption. Imports continued to grow over the same period, however, even if at the low pace of 9 percent. In 2010 imported pork, which mostly goes for further processing, held 22 percent of the domestic market share, compared with 27 percent in 2005.

Figure 10: Russian Federation’s production, imports and self-sufficiency in pork, 2005-2010

Source: FSSS of Russian Federation.

percen

t

mill

ion

to

nn

es

3.5

3.0

2.5

2.0

1.5

1.0

-

0.5

2005 2006 2007 2008 2009 2010

80

76

78

74

72

70

68

66

Import(left axis)

Production(left axis)

Self-sufficiency(right axis)

Russian Federation - Meat sector review

21

Similar to the poultry sector, the main sources of increasing pork production in 2005-2011 were the rise of pig inventories and slaughter. Pig inventories in the Russian Federation increased from 13.4 million heads in 2005 to 17.2 million heads in 2011, or by 28 percent. The increase in slaughter during the same period was even more impressive at 59 percent (see Table 7). Although slaughter yields have remained almost unchanged at 84 kilograms per head, it should be noted that pork production efficiency has improved. In 2005, the number of slaughtered animals exceeded beginning pig inventories by 36 percent. In 2011, pig slaughter exceeded beginning inventories by 69 percent, pointing to intensified pork production, shorter growing cycles and faster animal turnover in swine production facilities.

Table 7: Pig inventories, slaughter, yields and meat production in the Russian Federation, 2005-2011

2005 2006 2007 2008 2009 2010 2011Change 2011 vs.

2005

Pig inventories as of Jan 1, mln head

13.4 13.5 15.9 16.3 16.2 17.2 17.2 28%

Pig slaughter, mln head 18.3 19.4 22.3 24.1 26.0 28.0 29.1 59%

Pig slaughter, percent of inventories

136 145 140 147 161 162 169 24%

Yield, kg/head 83 84 84 85 83 83 84 1%

Pork production, mln tonnes 1.52 1.64 1.87 2.04 2.17 2.33 2.43 60%

Source: FAO Stat based on official Russian statistics.

Unlike the increase of domestic production of poultry and pork, beef production has continued to decline. As can be seen in Figure 11, imports of beef experienced a peak in 2008 and then started declining, which resulted in a decreasing beef supply.

22

Figure 11: Russian Federation’s production, imports and level of self-sufficiency in beef, 2005-2010

2005 2006 2007 2008 2009 2010

3 000

2 500

2 000

1 500

1 000

500

0 0

74

72

70

68

66

64

Self-sufficiency(right axis)

Production(left axis)

Import(left axis)

mill

ion

to

nn

es percen

t

Source: FSSS of Russian Federation.

The beef and veal production decline has reflected decreasing cattle inventories and slaughter as indicated in Table 8. During the period of 2005-2011, Russian farmers continued cattle slaughter at a faster pace than the cattle heard was rebuilt owing to low profitability of raising animals. From 2005 to 2011, there was a decrease of three million cattle heads: a drop of 13 percent.

Another reason behind decreasing cattle inventories is ongoing adjustments in the dairy sector. As cow yields increase and feed conversion rates improve, farmers continue to decrease the number of dairy cows. Since Soviet Union times (and, to a considerable extent, now) beef has been a by-product of the milk production. Despite some success of the federal programme “Development of meat cattle breeding in Russia for 2009-2012” and the launch of several big projects, the pure-bred beef cattle inventories remain very low: between 450 and 500 thousand heads, according to different estimates.

The Russian beef sector has shown some signs of recovery in recent years. Farmers tend to feed their cattle better and slaughter them at higher slaughter weights. The average yield of cattle in the Russian Federation increased from 168 kilograms per head in 2005 to 190 kilograms in 2011: a 13 percent increase as indicated in Table 8.

Russian Federation - Meat sector review

23

Table 8: Cattle inventories, slaughter, yields and beef and veal production in the Russian Federation, 2005-2011

2005 2006 2007 2008 2009 2010 2011Change 2011 vs.

2005

Cattle inventories as of 1 Jan, mln head

23.0 21.5 21.5 21.5 21.0 20.7 20.0 -13%

Cattle slaughter, mln head 10.7 9.6 9.5 9.6 9.4 9.3 8.6 -20%

Yield, kg/head 168 177 178 184 185 185 190 13%

Beef and veal production, mln tonnes

1.8 1.7 1.7 1.8 1.7 1.7 1.6 -9%

Source: FAO Stat based on official Russian statistics.

Summary of main risks and opportunities in the meat industry

Table 9 summarizes the industry’s main risks, opportunities and risk mitigation options. The types of risks are divided into the following broad categories: production and infrastructure, animal disease and epizootic situation, investment-related and policy.

Table 9: Main risks, opportunities and risk mitigation options in the Russian meat sector

Type of risk

Risk description Possible consequencesMitigation and

opportunities

Pro

duct

ion/

Infr

astr

uctu

re

• high volatility in feed prices • additional costs for project’s startup development

• vertical integration with feed production

• poor quality of purchased feeds

• decreasing margin and lack of working capital

• feed price risk hedging for outsourced grain/feed

• lack of experience and knowledge of key staff and

(nutrition, vet services, management, etc.)

• low quality/food safety of the final product

• investment in staff training and education, outsourcing of key services to result in

better production indicators

• poor infrastructure (electricity outages, road transportation blocked in

winter, etc.)

• low competitiveness and loss of market share

• location in areas with well-developed infrastructure

• lack of effective food safety control/monitoring system

• inability to improve feed conversion and other efficiency indicators

24

Type of risk

Risk description Possible consequencesMitigation and

opportunities

Epi

zoot

ic

• African swine fever • risk of flocks/heard depopulation

• investment in veterinary services and biosecurity

measures

• avian influenza • loss of investment• work with local

communities to create buffer zones around production facilities

• other diseases

• trade disruptions and bans

• disease • significantly delayed

payback period

• significant additional expenditures on eradication

leading to bankruptcy

Inve

stm

ent

and

finan

cial

• long payback periods, especially in cattle/beef

production• limited expansion capacity

• investment planning at market rather than

subsidized interest rates

• cancellation or reduction of current interest rate subsidies due to policy

changes

• reduced profitability, increased costs

• legally binding commitments from

government/local authorities and banking

sector

• increase of credit interest rates

• reduced or negative margins and higher risks of loan

defaults

• lack of operating capital due to financial sector crisis.

• inability to purchase inputs and feed in a timely manner

(reduces production volumes and cash flow

income to critical levels)

Polic

y

• reduced availability of public funding due to lower budget

revenues or public focus shifting to other priorities

• higher interest rates and lack of state co-financing

• investment planning assuming stiffer import

competition and minimum tariff protection

• the Russian Federation’s accession to the WTO and

decreased import tariff protection

• lack of operating and investment capital as

financial institutions shift focus away from agriculture/

meat sector

• investment planning without price support

payments

• the need to restrict overall domestic support in line with WTO commitments

• reduced sales and incomes• plan investment

considering the latest environmental, animal

production and advanced food safety systems

• changes in standards and regulations (environmental,

waste treatment, food safety, animal welfare)

• slow growth, extended payback or bankruptcy

Source: Author/LMC International, based on calculations and estimates.

Russian Federation - Meat sector review

25

Chapter 3 - detailed review of the meat sector

Meat production structure: increasing the role of commercial farms

There are three main types of farms that raise livestock and poultry in the Russian Federation: agricultural enterprises (commercial farms), individual (peasant) farms and rural households (smallholders that produce food for own consumption and often have extra non-farm income). The recent growth in livestock and poultry inventories has been accompanied by the changing roles of different farm types. The role of commercial meat producers has increased considerably owing to their better access to state financing, economy of scale, growing industry consolidation, the decreasing role of traditional meat markets and the increasing role of modern retail chains. The latter demands steady meat supplies, high quantities, uniform quality and food safety standards. Most of the support programmes described later in this report require that farms be registered as official businesses to receive state support or qualify for an interest rate subsidy on credit.

Rural households decreased their inventories of all kinds of poultry (chickens, turkey, ducks, geese, etc.) from 113 million head in 2005 to 97 million head in 2010 (down 15 percent), and agricultural enterprises increased their poultry numbers from 241 million head in 2005 to 348 million during the same period (up 44 percent). Correspondingly, the share of agricultural enterprises in poultry inventories increased from 68 percent in 2005 to 77 percent in 2010 while the share of rural households decreased from 32 percent in 2005 to 21 percent in 2010 (see Figure 12).

Alongside economic reasons, social and demographic factors – such as an ageing rural population and migration of young people to urban areas – cause this decrease of livestock and poultry production by rural households. Gender does not play a significant role in the development of the meat sector in the Russian Federation and was not reviewed in this report.

The individual (peasant) farms have maintained 1 percent of poultry inventories in 2005-2010 (see Figure 12). The outgrowing farming schemes involving individual farmers contracted by meat processors

26

to raise chickens are not popular in the Russian Federation because individual farmers are not considered to be reliable suppliers. This may explain their low share in total poultry inventories.

Figure 12: Structure of poultry inventories by type of farm, 2005-2010

68% 68% 71% 74% 76%

1% 1% 1% 1% 1%

32% 31% 28% 25% 23%

77%

1%

21%

0

20

40

60

80

100

2005 2006 2007 2008 2009 2010

per

cen

t

Agricultural enterprise Individual (peasant) farm Rural households(smallholder)

Source: FSSS of Russian Federation.

While poultry production structure varies considerably by region, each subsector has its peculiarities. Raising chickens in rural households is popular in all rural territories of the Russian Federation as hens are mostly used to supply eggs for in-house consumption. However, in southern regions (Rostov, Krasnodar and Stavropol and North Caucasian Republics) backyard commercial broiler farms supply a considerable volume of broilers, turkeys, ducks and geese to the local meat markets. This is explained by availability of feed wheat, corn, sunflower and other feeds at affordable prices, favorable climate and a tradition of raising backyard poultry. Similar backyard production is registered in the Republics of Tatarstan and Bashkortostan. The regional production structure is described later in this report.

Similar trends were observed in the structure of pig inventories in 2005-2010: agricultural enterprises increased pig inventories from 7 million to 11 million heads (up 48 percent) while rural households decreased, from 6 million to 5.6 million heads (down 5.5 percent). Therefore, rural households’ share of total pig inventories decreased by 9 percent from 2005 until 2010 (see Figure 13). Individual farms also played a more important role in

Russian Federation - Meat sector review

27

pork production than in poultry as they accounted for 4 percent of all pig inventories.

Figure 13: Structure of pig inventories by type of farm, 2005-2010

4%

53%

5%

52%

5%

53%

5%

57%

4%

62%

5%

63%

43% 43% 41% 38% 34% 33%

per

cen

t

80

100

60

40

20

02005 2006 2007 2008 2009 2010

Agricultural enterprise Individual (peasant) farm Rural households(smallholder)

Source: FSSS of Russian Federation.

The cattle inventories held by both major types of farms continued to decline. Agricultural enterprises decreased cattle numbers from 11 million in 2005 to 9.3 million heads in 2010 (down 16 percent). Rural households also continued cattle slaughter although at a slower pace: from 9.6 million heads in 2005 to 9.2 million in 2010 (down 4 percent).

An emerging growth of individual farmers as producers is the main difference in cattle inventories and their structure as compared with poultry and swine. The cattle inventories held by the individual farmers increased from 0.9 million heads in 2005 to 1.5 million in 2010 according to official Russian statistics (up 58 percent). Correspondingly, the share of individual farmers in total cattle production increased from 4 percent in 2005 to 7 percent in 2010 (see Figure 14).

28

Figure 14: Structure of cattle inventories by type of farm, 2005-2010

0

20

40

60

80

100

2005 2006 2007 2008 2009 2010

per

cen

t

51% 49% 48% 48% 46% 46%

49% 48% 47% 46% 46%51%

4% 5% 6% 6% 7% 7%

Individual (peasant) farmAgricultural enterprise Rural household(smallholder)

Source: FSSS of Russian Federation.

As already mentioned, raising and slaughtering cattle is closely linked with dairy herd replacements (Box 2). Cattle inventories diminished as milk yields and production increased and farmers reduced cow numbers. In 2010, an average milk yield per cow in the Russian Federation was about 3 800 kg per year, or 18 percent more than in 2005. The increase in cow milk productivity occurred despite the decrease of cattle inventories from 9.6 million cows in 2005 to 8.3 million in 2010 (down 13 percent).

Box 2: Beef cattle production perspectives

According to the state scientific institution All-Russia Scientific Research Institute Of Meat Cattle Breeding, only about 5 percent of local beef comes from beef cattle or cross-breeds (more information on cattle breeds in the Russian Federation is provided in the Annex 2 of this report).

The Ministry of Agriculture of the Russian Federation identified two areas of improvement in its "Development of Beef Cattle in Russia 2009-2012" programme: (i) intensification of the use of cattle feedlots to increase daily weight gains and slaughter weights and decrease cattle age at slaughter to below 24 months; and (ii) increase in cattle inventories.

With regards to the beef market, high quality beef has become available only recently when the country started importing beef from the USA, Brazil, Australia, the EU and Argentina. Beef production will likely continue to develop as a niche market limited to the demand of high-income consumers in big cities.

Russian Federation - Meat sector review

29

Meat supply

In 2010, the Russian meat market (calculated in raw meat equivalent as domestic production, added to by meat imports and subtracted from by exports) increased by 22 percent as compared with 2005 (see Table 10).

Table 10: Meat market, thousand tonnes

Meat type 2005 2006 2007 2008 2009 2010Change2010 vs.

2005

Poultry 2 706 2 906 3 219 3 438 3 541 3 512 +30%

Pork 2 154 2 361 2 615 2 864 2 836 2 970 +38%

Beef 2 484 2 456 2 488 2 643 2 502 2 463 -0.8%

Other kinds of meat** 161 171 183 189 193 194 +20.5%

Total 7 505 7 894 8 505 9 134 9 072 9 139 +22%

Source: FSSS of Russian Federation, Meat Union of Russia and Meatinfo.

* Calculated as production + imports - exports = consumption.** Lamb and goat meat.

Within this trend, the poultry meat and pork subsectors experienced the highest growth rate of 30 and 38 percent respectively. Changes in the beef supply were insignificant (down 0.8 percent).

The major changes in the structure of the Russian meat market occurred because of the expansion of poultry production and reduction of beef supply (see Figure 15).

30

Figure 15: Recent developments in the meat market structure, 2005-2010

33%

29%

36%

31%

30%

37%

29%29%

31%

38%

28%

31%

39%

27%

33%

38%

0

10

20

30

40

50

60

per

cen

t

70

80

90

100

2005 2006 2007 2008 2009 2010

2% 2% 2% 2% 2% 2%

29%

31%

38%

PoultryVeal & beef Other types of meatPork

Source: FSSS of Russian Federation, Meat Union of Russia and Meatinfo.