february 18-19, 2010 660 newport center drive, suite 710 newport beach, ca 92660 economic and...

TRANSCRIPT

February 18-19, 2010660 Newport Center Drive, Suite 710

Newport Beach, CA 92660

Economic and Investment OutlookPresented by Girard Miller, CFA

Senior StrategistPFM Asset Management LLC

PFMAgenda

1. Economic cycle drives investment decisions

2. What’s looking up?

3. What’s to worry about?

4. Where are the data two-faced?

5. Risks

6. Market observations for treasury and cash management

7. Long-term investment perspective

2© 2010 PFM Asset Management LLC

PFMBusiness Cycle Should Drive Investment Strategy

Peak• Interest rates high• Full employment• High inflation

Trough• Interest rates low• High unemployment• Low inflation

Contraction

• Production slows

• Corporate profits down

• Stock market losses

• Unemployment rises

• Interest rates decline

• Inflation falls

Expansion

• Production increases

• Construction rebounds

• Corporate profits rise

• Stock market gains value

• Unemployment falls

• Consumer confidence grows

• Interest rates rise

• Inflation increases

3© 2010 PFM Asset Management LLC

We are here.

PFMCurrent Economic Conditions

4© 2010 PFM Asset Management LLC

Indicators Current Condition

Production Increases

Construction Rebounds

Corporate Profits Rise

Stock Market Gains Value

Unemployment Falls

Consumer Confidence Grows

Interest Rates Rise

Inflation Increases

PFMFirst, A Look at the Bright Side

• Leading Indicators show strength

• Labor market improving

• Improvements in housing market

• Exports

• ISM

5© 2010 PFM Asset Management LLC

PFMLeading Economic Indicators Show Strength

• The Index of Leading Economic Indicators has ten components including average weekly hours, manufacturers’ new orders, building permits, stock prices, and money supply, among others.

6© 2010 PFM Asset Management LLC

Source: Bloomberg

Index of Leading Economic IndicatorsJanuary 2005 - December 2009

PFMLabor Market Has Improved Dramatically: Less Worse

• The economy would need 2- to 3-years of rapid job growth in order to recover the more than 7 million jobs lost since the recession began in December of 2007.

7© 2010 PFM Asset Management LLC

Source: Bloomberg

Avg Growth = 200K per month Avg Growth = 110K per month

PFM

Source: Bloomberg

Housing Market Shows Signs of Bottoming

• Recent improvements in the housing market were partly due to:– The first time homebuyer tax credit– The Federal Reserve’s program to purchase mortgage backed

securities, which helped reduce mortgage rates to historic lows

8© 2010 PFM Asset Management LLC

Freddie Mac National Mortgage Commitment RateJanuary 2005 - January 2010

10-Year Average 6.3%

PFMHousing Affordability Increases

9© 2010 PFM Asset Management LLC

National Association of Realtors Home Affordability IndexJanuary 2000 – December 2009

Source: Bloomberg

• 61% of Inland Empire households can now afford a median house – vs 17% in 2007

PFMWeaker Dollar Promotes Exports

10© 2010 PFM Asset Management LLC

• Expansion of exports adds to GDP

• A weaker dollar raises the price of imports and may have long term implications for inflation

Source: Bloomberg

U.S. Trade Weighted Real Broad Dollar IndexDecember 2004 - December 2009

U.S. Trade Balance ($ Billions)November 2004 - November 2009

PFMISM Surveys Are Positive

• The Institute for Supply Management (ISM) releases monthly indices that measure whether the manufacturing economy and the services economy are in expansion or contraction.

11© 2010 PFM Asset Management LLC

Source: Bloomberg

Expansion

Contraction

Institute for Supply Management CompositesJanuary 2005 – January 2010

Are services stalling?

PFMEquity Indices Point to Strong Recovery

• Foreign equity has recovered faster than domestic equity.

• High-tech stocks are up more than highly capitalized stocks.

12© 2010 PFM Asset Management LLC

Source: Bloomberg

Equity IndicesJanuary 2007 - December 2009

NA

SD

AQ

an

d S

&P

50

0

MS

CI

EA

FE

“The recovery in equity prices is not inconsequential.” ~ Alan Greenspan

PFMRisk of Deflation Eases

13© 2010 PFM Asset Management LLC

Source: Bloomberg

Consumer Price Index (Year-Over-Year % Change)January 2005 - December 2009

Are we back to “normal” inflation?

PFMMost Economists Expect Modest Recovery

• The first release of GDP for the fourth quarter 2009 showed the economy expanding at an annual rate of 5.7%, the largest increase in six years.

14© 2010 PFM Asset Management LLC

Source: U.S. Department of Commerce – Bureau of Economic Analysis and Bloomberg Survey of Economists median forecasts

January 2010Bloomberg

Survey MedianForecasts

Change in Gross Domestic ProductFourth Quarter 2004 – Fourth Quarter 2009

PFMNow a Look at the Darker Side

• Housing foreclosures and delinquencies

• Residential mortgage resets

• Commercial real estate

• Budget deficits worldwide

• Bank failures

• Sovereign debt and contagion risk

15© 2010 PFM Asset Management LLC

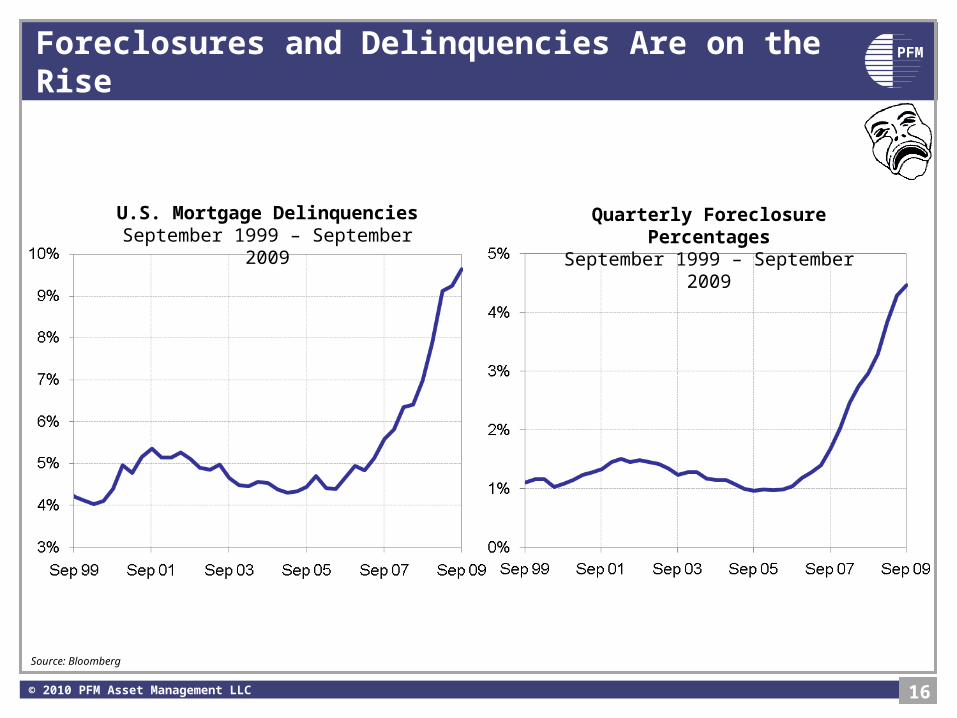

PFMForeclosures and Delinquencies Are on the Rise

16© 2010 PFM Asset Management LLC

U.S. Mortgage DelinquenciesSeptember 1999 – September 2009

Quarterly Foreclosure PercentagesSeptember 1999 – September 2009

Source: Bloomberg

PFMToxic Residential Mortgages Are Still Unwinding

• Despite some positive signs in the housing sector, foreclosures are still rising as the latest wave of ARM rate resets begin in 2010.

17

Adjustable Rate Mortgage Reset ScheduleJanuary 2007 – January 2013

Source: Credit Suisse Fixed Income Mortgage Strategy

2010 2011 2012

© 2010 PFM Asset Management LLC

PFMCommercial Real Estate: The sub-surface iceberg?

• $1.4 trillion of commercial mortgages and loans come due in 3.6 years

• Over half are underwater (Wall St Journal 2/9/10)

• Estimated 30-35% loss ratios(Note: CalPERS marked down its real estate by 50% last year)

• Will drag on overall economy

• Poses major continued risk in bank sector – especially smaller banks– Undoubtedly will cause more bank failures

• Problem is a close cousin to the Japanese ‘Zombie Bank’ syndrome– Which caused the “lost decade”

18© 2010 PFM Asset Management LLC

PFMConsumer Credit Deleveraging: Paradox of Thrift

• As consumers tighten their wallets and pay off credit card debt, the consumption component of GDP has slowed.

19© 2010 PFM Asset Management LLC

Source: Bloomberg

Outstanding Consumer CreditJanuary 2000 – December 2009

PFMDeficits Matter: A Global View

20© 2010 PFM Asset Management LLC

Source: PIMCO, Reuters EcoWin

PFMEmployment Is a Lagging Indicator

• Unemployment rate usually peaks after recessions end.

21© 2010 PFM Asset Management LLC

Source: Bloomberg

PFMConundrums: Risks, Wild Cards and Conflicting Data

• Terrorism and Geopolitical Risk

• China

• Housing – positives and negatives expected in 2010

22© 2010 PFM Asset Management LLC

PFMTerrorism and Geopolitical Risk Will Haunt Markets

23© 2010 PFM Asset Management LLC

PFM

Will China’s Moves in 2010 Support or Hinder Growth?

24© 2010 PFM Asset Management LLC

PFMHousing: Green Shoots – or Black Holes?

25© 2010 PFM Asset Management LLC

PFMMarket Update and Perspectives

• Steep yield curve

• Historically low rates

• Fed actions take time

• Forecasts for unemployment, inflation, and rates

26© 2010 PFM Asset Management LLC

PFMTreasury Yields Remain Below Historical Averages

27© 2010 PFM Asset Management LLC

Source: Bloomberg

U.S. Treasury Yield Curve10-Year Average vs. February 8, 2010

PFM2-Year U.S. Treasury Rates at Historic Lows

• With the exception of a few periods of volatility, 2-Year U.S. Treasury Notes traded below 1.00% for the majority of 2009.

28© 2010 PFM Asset Management LLC

Source: Bloomberg

10-Year Average

3.2%

2-Year U.S. TreasuryFebruary 2000 – February 2010

PFM

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1965 1967 1970 1972 1975 1977 1980 1982 1985 1987 1990 1992 1995 1997 2000 2002 2005 2007 2010

10-Year U.S. Treasury Yields1965 - 2010

Fixed Income Market: Longest Bull Market in History

Source: Bloomberg

Longest Bull Market in History

© 2010 PFM Asset Management LLC 29

10-Year U.S. Treasury Yields1965 – 2010

PFMYields on Short-Term Securities Track Fed Funds

30© 2010 PFM Asset Management LLC

Source: Bloomberg

Federal Funds Target Rate vs. 3-Month Treasury and Federal Agency RatesJanuary 2005 - January 2010

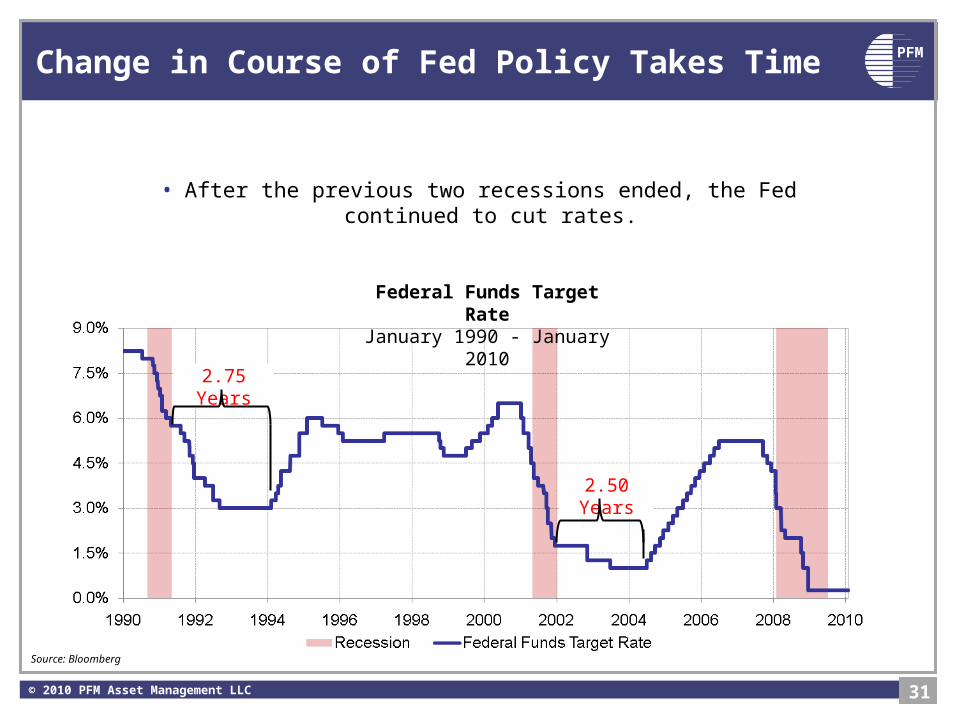

PFMChange in Course of Fed Policy Takes Time

• After the previous two recessions ended, the Fed continued to cut rates.

31© 2010 PFM Asset Management LLC

2.75 Years

2.50 Years

Source: Bloomberg

Federal Funds Target RateJanuary 1990 - January 2010

PFMWhat’s the Fed’s Game Plan?

• Job #1 is to reliquify and recapitalize the banking sector– A central bank’s role for 300 years

• This requires a steep yield curve– Give cheap money to banks and let them earn profits to rebuild capital– Requires low Fed Funds rate

• Meanwhile, perform Keynesian function of macro-monetary stimulus– Bernanke is a student of the Great Depression (right guy for the job)– Cannot afford to repeat 1937

• Yet must convince the world that inflation won’t return and dollar will stabilize– Hence, a lot of talk about “exit strategies”– Paying interest on reserves– Could snug a quarter point without any real tightening

32© 2010 PFM Asset Management LLC

PFMOutlook for Federal Funds Target Rate

33© 2010 PFM Asset Management LLC

Source: Bloomberg January Survey

Economists' Forecasts for Federal Fund Target RateFirst Quarter 2010 - Fourth Quarter 2010

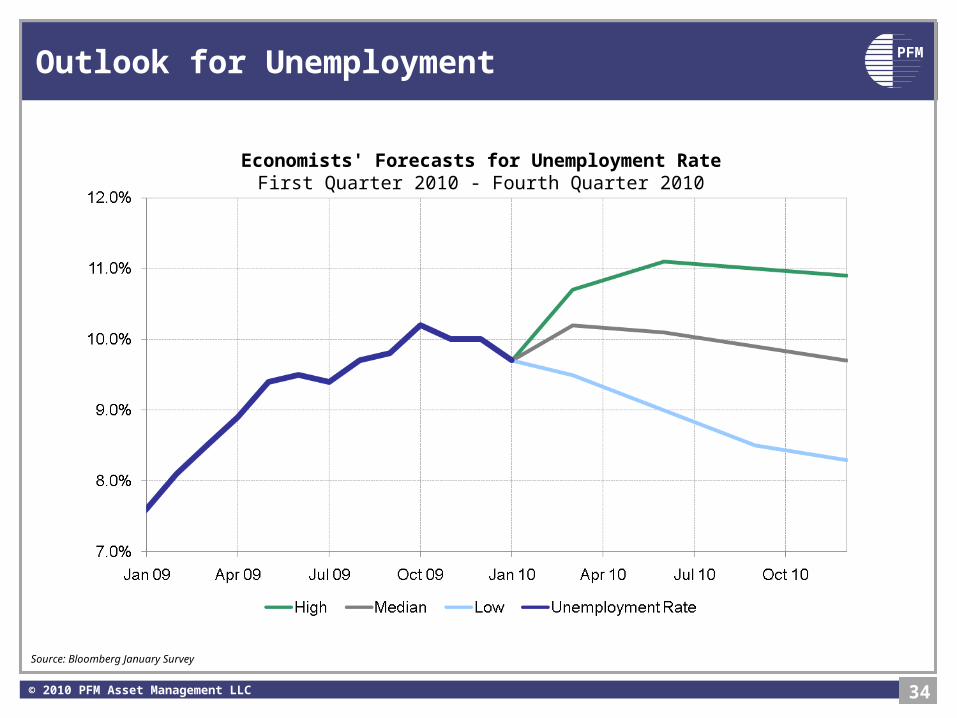

PFMOutlook for Unemployment

34© 2010 PFM Asset Management LLC

Source: Bloomberg January Survey

Economists' Forecasts for Unemployment RateFirst Quarter 2010 - Fourth Quarter 2010

PFMOutlook for Inflation

35© 2010 PFM Asset Management LLC

Source: Bloomberg January Survey

Economists' Forecasts for Consumer Price Index (Year-Over-Year % Change)First Quarter 2009 - Fourth Quarter 2010

PFMOutlook for 2-Year U.S. Treasury Note Yield

36© 2010 PFM Asset Management LLC

Source: Bloomberg, Bloomberg January Survey

Economists' Forecasts for 2-Year U.S. Treasury Note First Quarter 2010 – Fourth Quarter 2010

PFMPortfolio Management Risks

• If economists are right and rates rise, longer maturities will suffer price losses

• Spreads are too narrow to pay for credit risk

– Market risks for Agencies

– Credit risk for corporates

37© 2010 PFM Asset Management LLC

PFMHow Duration Affects Returns

Source: Bloomberg

• Duration is a primary factor in return volatility.

• Historically, portfolios with longer durations have higher returns, but also higher volatility.

© 2010 PFM Asset Management LLC

Risk/Return of Various Benchmarks10 Years ended December 31, 2009

Merrill LynchTreasury Index

Duration(years)

OverallReturn

Cumulative Value of $50 million

Quarters withNegative Return

3-Month 0.15 2.98% $67,109,823 0 out of 40

1-Year 0.91 3.80% $72,626,141 3 out of 40

1-3 Year 1.84 4.48% $77,501,317 4 out of 40

3-5 Year 3.82 6.00% $89,571,019 14 out of 40

38

PFMEconomists Are Forecasting Higher Interest Rates

• If median forecast is accurate, then longer maturities would suffer.

39© 2010 PFM Asset Management LLC

Yield Increases That Would Result In Negative ReturnsOver 12 Month Period for Treasury Securities

PFM

Treasury to Agency Spreads Have Dipped Below Pre-Crisis Levels

• The spread between 2-year U.S. Treasury and Federal Agency notes has narrowed dramatically to below pre-credit-crisis levels, signaling increased investor confidence in the Government-Sponsored Enterprises.

• GSE securities are over-valued at these levels.

40© 2010 PFM Asset Management LLC

Source: Bloomberg

Difference in Yield Between 2-Year U.S. Treasury and Federal Agency NotesFebruary 2005 – February 2010

PFMAmount of Commercial Paper Issued at 10 Year Lows

• Reduced supply may have contributed to declines in commercial paper yields.

• Total commercial paper issuance declined 47% from mid-2007 to December 2009; asset backed commercial paper issuance declined over 60% during the same period.

41© 2010 PFM Asset Management LLC

Source: Bloomberg

Commercial Paper OutstandingJanuary 1991 - December 2009

PFM2-Year Corporate Spreads

• Spreads have almost returned to “bubble” levels (pre-Lehman).

42© 2008 PFM Asset Management LLC

Difference in Yield Between 2-Year U.S. Treasury and AA Corporate NotesFebruary 2005 – February 2010

Source: Bloomberg

PFMIssuer Risk: Exhibit A

43© 2008 PFM Asset Management LLC

Reminder that credit risk is not all financial

PFMMarket Strategies to Consider

• Conservative approaches are required, given ultimate risk of economic expansion and higher interest rates with impact on fixed-income securities

• Need to evaluate both level and slope of yield curve

– Calculate breakevens and duration risk

– Consider potential returns from rolling on the curve

• Need to consider opportunity costs of:

– Passive buy-and-hold

• vs. risks and costs of active management and/or outsourcing

44© 2010 PFM Asset Management LLC

PFMOpportunities With a Steep Yield Curve

Yield CurvesFebruary 8, 2010

Maturity Treasury Agency

3 month 0.10% 0.16%

6 month 0.17% 0.22%

1 year 0.29% 0.34%

2 year 0.77% 0.94%

3 year 1.26% 1.58%

5 year 2.42% 2.62%

10 year 3.60% 3.91%

30 year 4.55% 5.19%

Source: Bloomberg

32© 2010 PFM Asset Management LLC

PFM

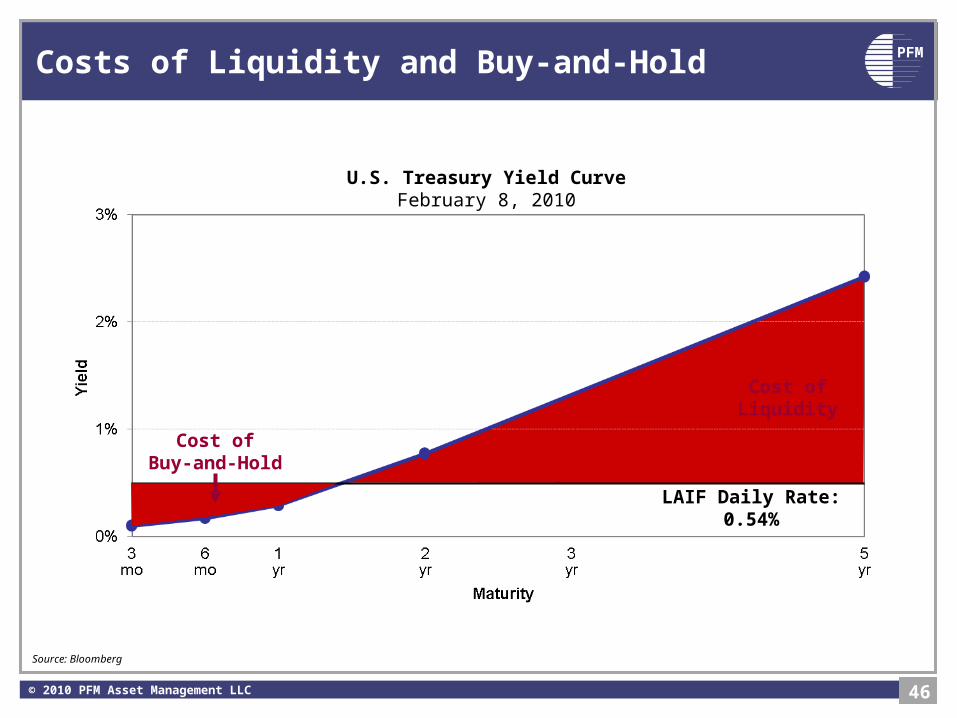

Cost ofLiquidity

Costs of Liquidity and Buy-and-Hold

46© 2010 PFM Asset Management LLC

Source: Bloomberg

U.S. Treasury Yield CurveFebruary 8, 2010

LAIF Daily Rate: 0.54%

Cost ofBuy-and-

Hold

PFM

30

• The steep curve also provides the benefit of “roll down.”

• The strategy begins with buying a security at point A.

• After a period of time, because security is closer to maturity, its yield would be lower at point B.*

• The investor then has the option to sell the security, realizing gains, and reinvest proceeds at point A.

– If LAIF or an LGIP or MMMF offers a higher return at point B, then active management enhances returns even more

* Assumes yield curve is positively sloped; Rising rates may render this approach ineffective, and like any longer-term purchase might result in losses.

• Investing in intermediate-term securities allows for “rolling down” the currently steep yield curve, increasing market value gains.

• Presently, the 3-year section of the curve shows value vs. duration risk and breakevens

Rolling Down the Yield Curve

© 2010 PFM Asset Management LLC

PFM

31

Better Total Returns Through “Roll-Down”

• Although interest rates have been at historically low levels for more than a year, portfolio managers who recognized the “roll down” potential of the steep yield curve could produce superior returns

PurchasePurchase

DateOriginal

YTM

Total Return as of 1/29/10

A. FHLB Note

1/22/09 1.91% 3.73%

B. FHLB Note

7/31/09 1.97% 5.17%

C. FHLB Note

10/9/09 1.57% 3.17%

2-Year U.S. Treasury Yield November 2008 – January 2010

Source: Bloomberg

© 2010 PFM Asset Management LLC

PFM

32

• The chart below provides examples how active management can increase or decrease the portfolio’s life (duration) based on interest rate levels.

2-Year U.S. Treasury YieldDecember 2007 to January 2010

92% of benchmark 102% of

benchmark

85% of benchmark

70% of benchmark

69% of benchmark

Duration Management Adds Value in Uncertain and Volatile Markets

Source: Bloomberg

© 2010 PFM Asset Management LLC

PFMTake-Away Pointers for Cash Managers

• Many economists expect a modest recovery

• Unemployment likely to remain near 10%, declining to 9% range by year-end

• Deflation pressures have waned; inflation risk is longer-term

• Short-term rates to remain low until mid-year and probably through 2010

• U.S. Treasury yields remain below historical averages– A modest increase in yields could push fixed-income returns negative

• Fixed-income portfolios should be managed defensively– Shorten duration– Overweight Treasuries unless spreads justify otherwise– Maintain reserves in cash/cash equivalents for future opportunities– Avoid exotic strategies that may have hidden risk

50© 2010 PFM Asset Management LLC

PFMLong-Term Investment Perspectives

• Pensions and OPEB

• Retirement investment strategies

• Perspectives on current equity market valuations

51© 2010 PFM Asset Management LLC

PFMFunding Shortfalls Nationwide After 2008

• CalPERS investment losses are typical of public plans

– Recent performance worse than average public plan after stronger returns previously

– Riskier portfolio strategies as they reached for yields

– Doubling of unfunded liabilities nationally

52

Underperformedbenchmark by940 bps in 2009!

© 2010 PFM Asset Management LLC

For more details, attend my session onSustainable Solutions for OPEB/Pensions

PFMLA Times: January 20, 2010

“CalPERS' Investments Underperform in 2009”By Marc Lifsher

• The retirement system's portfolio earned only 11.8% in returns, trailing its internal benchmark of 21.2%, as its real estate holdings plummeted.

• Heavy losses in real estate holdings battered 2009 investment returns at California's giant public pension fund, although the portfolio overall rose in value for the year.

• The portfolio had dived 27.1% in 2008.

• CalPERS said its real estate holdings plunged 47.5% for the year, compared with a 15.4% drop for its benchmark index.

© 2010 PFM Asset Management LLC 53

PFMWhat role for stocks in retirement plan portfolios?

•Pension funds

•OPEB portfolios

•457 and 401 plans

54© 2010 PFM Asset Management LLC

PFMHistorical Analysis of Stock Market Returns

• Historically, stocks have returned about 10+ percent annually compounded since 1926

• Thus, equities are the superior investment asset class over long periods

• BUT stock prices fluctuate, and the risk of loss in a recession must be evaluated carefully

55© 2010 PFM Asset Management LLC

PFM

Historical Review of Bull & Bear Markets:1926 to Present• Traditional definitions of bull and bear stock markets have focused on the % change rather than

economic causation

– PFM chooses instead to identify GDP bull markets and GDP bear markets

• Business cycle corresponds closely with stock market performance

– Of the 14 identifiable stock market cycle bottoms, only 2 occurred outside a GDP recession declared by the National Bureau of Economic Research

• 2001 recession – stocks bottomed one (1) year later

• 1942 “Pearl Harbor Scare” – not a GDP recession, but similar market action

• Stock market prices tend to rise about three times more during a bull market than they fall during a bear market

– Stock market prices rise approximately 89% on average (median) during a bull market

– Stock market prices fall approximately 30% on average (median) during a bear market

• A bull market typically lasts twice as long as a bear market

– Bull markets have historically averaged 39 months in duration

– Bear markets have lasted approximately 20 months

56© 2010 PFM Asset Management LLC

PFMBull and Bear Stock Market Phases: Quantified

57© 2010 PFM Asset Management LLC

Source: Bloomberg

PFMPast Bull and Bear Markets vs. Today’s

• Average bull market since 1926 ran for 39 months and stocks gained 89% from their previous bottom

• Average bear market lasted 20 months and stocks lost 30% from their peak

• The 2007-09 bear market lasted 16 months and stocks lost 53% from their peak

• Since the 2009 stock-market bottom, the S&P 500 rallied about 55% through last week (recovering 45% of its bear-market losses)

58© 2010 PFM Asset Management LLC

PFM

Phases of Market and Business Cycles:Green, Yellow and Red Zones

59© 2010 PFM Asset Management LLC

PFM

Historical Green, Yellow and Red Windows: 1927 to Present – Using Benefits Bonds Paradigm Only

KEY) % of S&P rise during Green (B.B.) Window

# of months the Green (B.B. ) Window is open

Median 58% 21

60© 2010 PFM Asset Management LLC

Source: Bloomberg

PFMWhat Is the “Green” Equity-Tilt Window?

GreenWindow

• Historically, the period of time when new money could be invested in the stock market without witnessing lower stock prices in the subsequent economic recession

• Measured ex post from the bottom of the stock market (which typically corresponds to the trough of an economic business cycle) until the stock market ‘breakeven’ level with the subsequent stock market bottom

• Theoretically, the period in which the risk of subsequent-cycle loss is < 50%

61© 2010 PFM Asset Management LLC

PFM

Stock Market Recovery During ‘Green and Yellow Equity Windows’

Recessionv

Height of the Green Window

(% change in S&P 500)

Length of the Green Window

(# months open)

Value of S&P 500 at the close of the Yellow

Window as a % of the previous stock market top

1 91% 33 27%

2 -10% 0 N/A

3 78% 36 103%

4 64% 32 121%

5 63% 21 143%

6 31% 11 106%

7 34% 35 118%

8 -13% 0 N/A

9 58% 20 85%

10 4% 1 99%

11 175% 81 210%

12 164% 79 222%

13 -10% 0 N/A

Average 56% 27 95%

Median 58% 21 103%

62© 2010 PFM Asset Management LLC

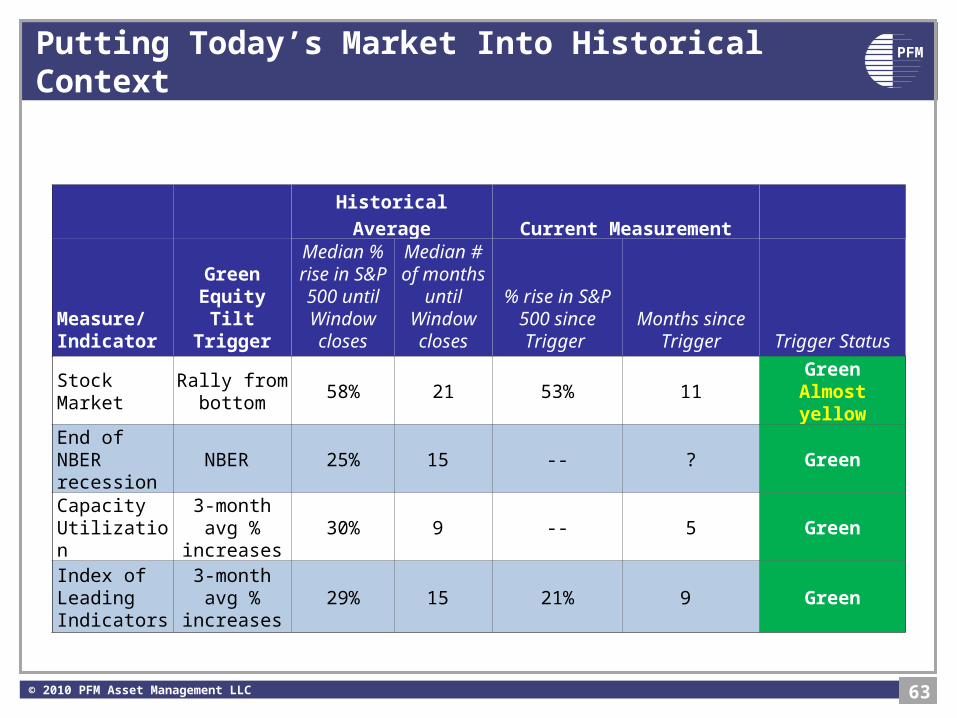

PFMPutting Today’s Market Into Historical Context

Historical Average Current Measurement

Measure/ Indicator

Green Equity Tilt Trigger

Median % rise in S&P

500 until Window closes

Median # of months

until Window closes

% rise in S&P 500 since Trigger

Months since Trigger Trigger Status

StockMarket

Rally from bottom

58% 21 53% 11Green

Almost yellow

End of NBER recession

NBER 25% 15 -- ? Green

Capacity Utilization

3-month avg % increases

30% 9 -- 5 Green

Index of Leading Indicators

3-month avg % increases

29% 15 21% 9 Green

63© 2010 PFM Asset Management LLC

PFMInverted Yield Curve as a Red Zone Trigger

64© 2010 PFM Asset Management LLC

Source: Bloomberg

PFMQuestions

65© 2010 PFM Asset Management LLC

Girard Miller, CFA, Senior StrategistPFM Asset Management LLC

(310) [email protected]

??

PFMDisclaimer

66© 2010 PFM Asset Management LLC

• The information in the immediately preceding section reflects preliminary findings from PFM proprietary research and is intended for educational purposes only.

• Nothing herein constitutes investment advice.

• Past market performance cannot assure future returns.

• The purpose of this section is to provoke strategic thinking and fruitful dialogue, not to sell or promote individual securities or money managers.

• This material is based on information obtained from sources generally believed to be reliable and available to the

public, however PFM Asset Management LLC cannot guarantee its accuracy, completeness or suitability. This

material is for general information purposes only and is not intended to provide specific advice or a specific

recommendation. All statements as to what will or may happen under certain circumstances are based on

assumptions, some but not all of which are noted in the presentation. Assumptions may or may not be proven correct

as actual events occur, and results may depend on events outside of your or our control. Changes in assumptions

may have a material effect on results. Past performance does not necessarily reflect and is not a guaranty of future

results. The information contained in this presentation is not an offer to purchase or sell any securities.