february 2, 2005 victor schoenmakers - american ... · february 2, 2005 victor schoenmakers. 2 ......

TRANSCRIPT

AAPA meeting MiamiExecutive Management Conference

Latin america / Carribean

February 2, 2005

Victor Schoenmakers

2

“What is the True Potential of your Port, and How Can it Compete under Current Conditions”Content of the presentation

1. Facts and figures

2. Port potential

3. Current conditions political, geographical, business

4. Competition industry, containers and distribution

5. Future challenges Capacity, globalisation, transport growth, conditions

6. Conclusions

3

World

RotterdamRotterdam

4

European Union (EU)

Rotterdam

FinlandFinlandSwedenSweden

GreeceGreece

ItalyItalySpainSpainPortugalPortugal

FranceFrance AustriaAustria

GermanyGermany

IrelandIreland

Great BritainGreat Britain

BelgiumBelgium

LuxembourgLuxembourg

TheNetherlandsTheNetherlands

DenmarkDenmark

PolandPoland

CzechRepublicCzechRepublic

SlovakiaSlovakia

HungaryHungary

SloveniaSlovenia

LithuaniaLithuania

EstoniaEstonia

LatviaLatvia

MaltaMaltaCyprusCyprus

5

The Netherlands

RotterdamRotterdam

6

1. Facts and figures - Port of Rotterdam

Area: 10.500 ha Direct employment: 65.000

Leased land: 4.940 ha Indirect employment: 250.000

Quay walls:80 km Added value (direct and indirect): € 25 billion

Through put: 354 million tons Share in GNP: 7,3%

315.000 people

7

1. Facts and figures - Throughput in Rotterdam, 2004

Total throughput: 354.2 million tons *

Dry bulk cargo: 90.3 million tons (25.5%)*

Liquid bulk cargo: 161.9 million tons (45.7%)*

Containers (8.2 Million TEU): 82.2 million tons (23.2%)*

Other general cargo: 19.8 million tons (5.6%)*

* Latest estimates

From 1962 – 2003 the Port of Rotterdam was the largest port in the world. In 2004 Shanghai took over that position.

8

1. Facts and figures - World’s major ports, 2003

0

50

100

150

200

250

300

350

RotterdamSingaporeShanghaiHong KongNingboGuangzhouTianjinNagoyaAntwerpQingdao

9

1. Facts and figures - European ports, 2003

0

50

100

150

200

250

300

350

RotterdamAntwerpHamburgMarseillesLe HavreAmsterdamAlgecirasGenoaLondonDunkirk

Unit: x 1 million tons (m)

10

1. Facts and figures - World container ports, 2003

0

2

4

6

8

10

12

14

16

18

20

Hong KongSingaporeShanghaiShenzhenBusanKaohsiungLos AngelesRotterdamHamburgAntwerp

Unit: Number x 1 million TEU’s

11

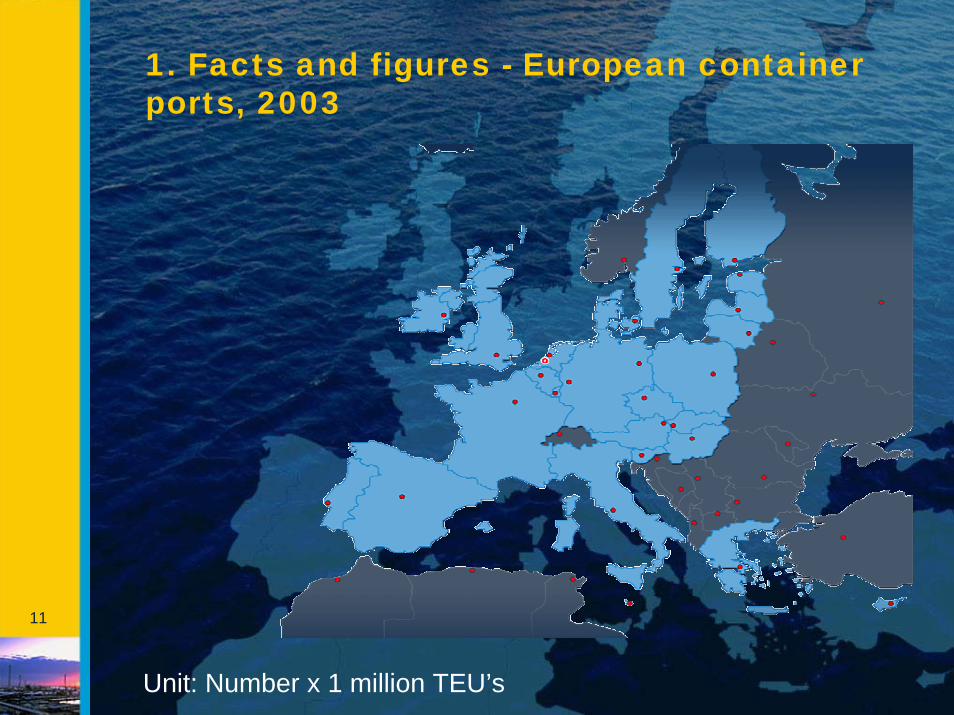

1. Facts and figures - European container ports, 2003

Unit: Number x 1 million TEU’s

12

2. Port potential

• The Port of Rotterdam is a Port Industrial Complex • Industry & containers & distribution

• PoR is the largest port in Europe (by far)• Economies of scale

• PoR has a lot of comparative advantages• Deep sea open access• Inland barge connections – river Rhine• Good rail and road hinterland connections

• Densely populated and high standard of living

13

3. Conditions - Rotterdam mainport

RotterdamRotterdam

1,300 km (800 miles)350 million people

950 km (600 miles)220 million people

500 km (300 miles)160 million people

contents

14

3. Conditions – the natural hinterland

Barcelona

Madrid

Paris

Basel, Bern, Zurich

Munich

Berlin

Hamburg

MilanLyon

Flanders

RuhrLondon

LiverpoolManchester

FrankfurtMannheim

Stuttgart

Randstad

Marseilles

Trieste

Stuttgart

Prague

BudapestWien

Warszawa

Genoa

1

15

3. Conditions - Hinterland connections

RailRoad

Shortsea - feederPipeline

Inland shipping

16

3. Conditions - the modal split

• 48% Inland shipping

• 5% Rail

• 21% Pipeline (oil)

• 26% Road

contents

17

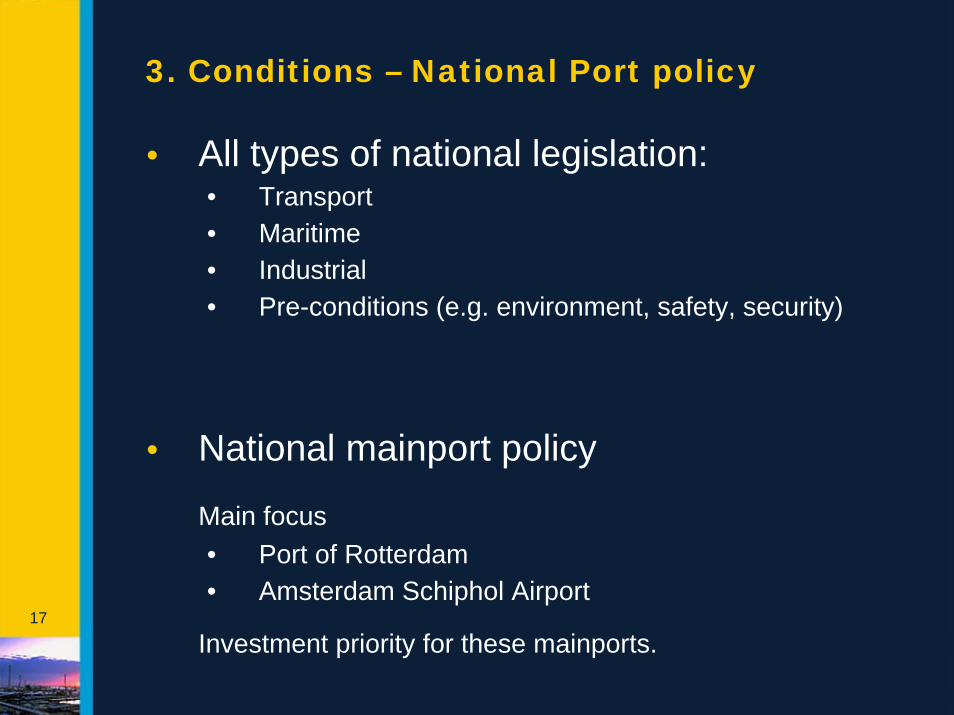

3. Conditions – National Port policy

• All types of national legislation:• Transport• Maritime• Industrial• Pre-conditions (e.g. environment, safety, security)

• National mainport policy

Main focus• Port of Rotterdam• Amsterdam Schiphol Airport

Investment priority for these mainports.

18

3. Conditions – International Port policy

• EU – policy & legislation: • Level Playing field• Transport (e.g. liberalization, modalities)• Industry (e.g. Kyoto CO-2 emissions)• Maritime (e.g. security, double hull)• Conditions (e.g. environment, safety)

• EU legal cases • state aid, competition

• IMO (Int. Maritime Organisation)• Port Security• Marpol (e.g. safety, environment, Law of

the Sea)

19

4. Competition – different sectors

• Industry – world wide competition • Antwerp, Singapore, Houston, et cetera

• Containers – Le Havre Hamburg range• Le Havre, Antwerp, Bremen, Hamburg• Mediterranean Sea, Baltic

• Distribution – Western Europe• Different supply chain concepts

20

4. Competition - the hinterland market sharein three circles (all cargo)

The Netherlands

Le Havre - Hamburg

Rest

Rotterdam 80% market share

35% market share

10% market share

BremerhavenHamburg

Antwerp

Le Havre

21

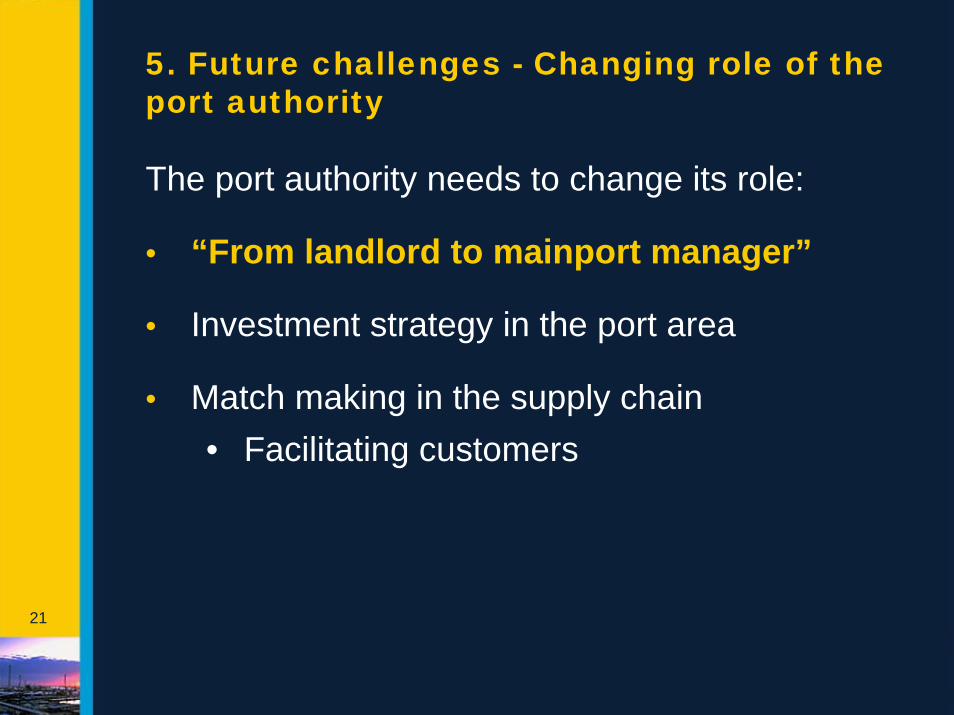

5. Future challenges - Changing role of the port authority

The port authority needs to change its role:

• “From landlord to mainport manager”

• Investment strategy in the port area

• Match making in the supply chain• Facilitating customers

22

5. Future challenges - Global trends in shipping and logistics

Liner companiesAPLCoscoDSREvergreenHanjinHapag-LloydHyundaiK LineMaerskMOLMSCNedlloydNOLNYKOOCLP&OSea-landUASCYang Ming

APLCoscoEvergreenHanjin/DSRHapag LloydHyundaiK LineMaerskMOLMSCNYKOOCLP&O NedlloydSea-landUASCYang Ming

Maersk/SealandGrand AllianceNew World AllianceUnited AllianceCosco/Yang Ming/K LineEvergreenMSCHanjin

1993 19981998 20032003

23

AIEASGNedlloydCargolinerDanzasDeutsche PostBiltspeditionSchenkerDeutsche BahnCircleEagle GlobalGATXAPLLUSCOKühne&NagelMark VIIIntexoMcGregor CoryMSASOcean GroupVitesseVan der GraafVan MierloDentressangle

DanzasDeutsche PostSchenkerDeutsche BahnEagle GlobalGATXAPLLKühne&NagelMSASOcean GroupVitesseABXPenskeVan MierloDentressangle

Deutsche PostDeutsche BahnEagle Global (USA)APLL (SIN)Kühne & Nagel (ZWI)Exel (ENG)Geodis (FRA)ABX (BEL)Penske (USA)Dentressangle (FRA)

5. Future challenges -Consolidation distribution

19971997 20002000 20022002

24

5. Future challenges - consolidation chemical industry

• Shell + BASF

• Lyondell + Bayer

• Exxon + Mobil

• Total + Fina + Elf

• BP + Amoco + Erdölchemie

• Chevron + Texaco

• Dow + Union carbide

• DSM + Catalytica

25

5. Future challenges - maritime transport growth / macro economic development

• Relation between GNP development and the turn-over of containers is less visible during recent years

GDP ontwikkeling EU en overslag TEU's HLH-range

-1-0,5

00,5

11,5

22,5

33,5

44,5

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

ontw

ikke

ling

GDP

0%

2%

4%

6%

8%

10%

12%

ontw

ikke

ling

over

slag

Real GDP EU (% change from previous period)

TurnoverTEU's HLH-range (% change from previous period)

26

5. Future challenges - maritime transport growth / macro economic development

• Reasons for this less visible relation:

• Globalization and network economy• Shift in location of production facilities creates

enormous increase in transport demand (comparative advantages) – “China factor”

• Exchange rate US Dollar ($) / Euro (€)• Growth of GNP of tradepartners

27

5. Future challenges - Projections total throughput

28

5. Future challenges - Projections container throughput in TEU’s

29

5. Future challengesMaritime transport growth – new port area

30

5. Future challenges – waterfront development

Recently: ‘Kop van Zuid’

31

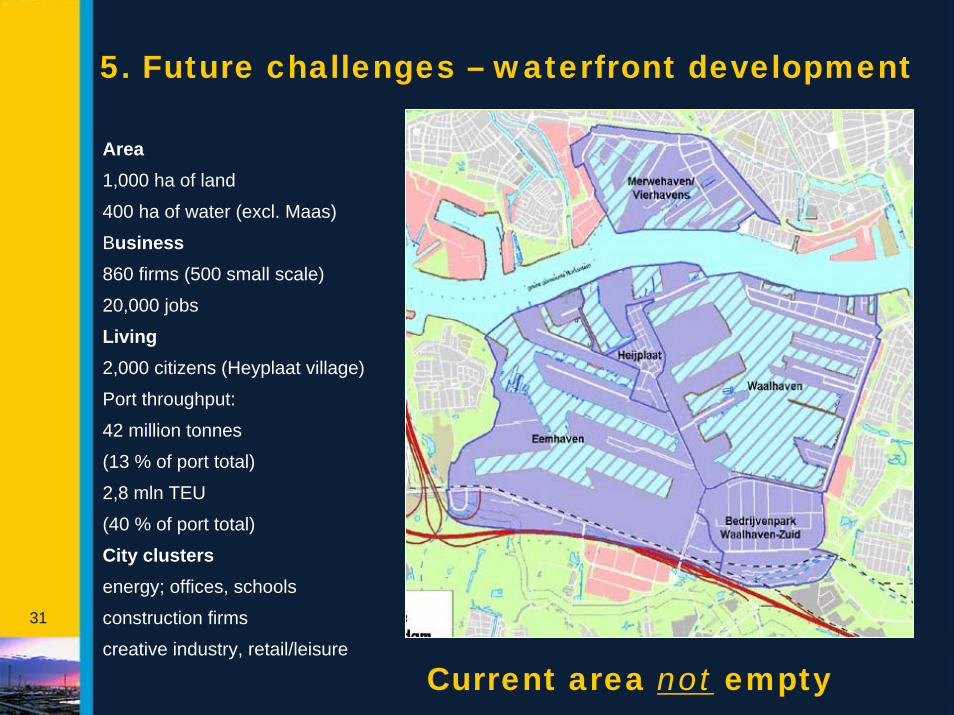

5. Future challenges – waterfront development

Current area not empty

Area1,000 ha of land

400 ha of water (excl. Maas)

Business860 firms (500 small scale)

20,000 jobs

Living2,000 citizens (Heyplaat village)

Port throughput:

42 million tonnes

(13 % of port total)

2,8 mln TEU

(40 % of port total)

City clustersenergy; offices, schools

construction firms

creative industry, retail/leisure

32

6. Conclusions

• The market rules• New production areas - Globalization• Enormous increase of transport demand• New port area needed - Increase in ship sizes• Rotterdam: from oil port to container port• Intensive (inter and intra) port competition

• Change of attitude of the port management• From landlord to mainport manager• Attracting new business (port operators / cargo)• Offering new ‘products’ to our customers

33