federal reserve bankof dallas - dallasfed.org · michael nieswiadomy* and ... federal reserve...

TRANSCRIPT

No. 9006

ARE NET DISCOUNT RATIOS STATIONARY?:THE IMPLICATIONS FOR

PRESENT VALUE CALCULATIONS

by

Joseph H. Haslag*

Michael Nieswiadomy*

and

Research Paper

Federal Reserve Bank of Dallas

This publication was digitized and made available by the Federal Reserve Bank of Dallas' Historical Library ([email protected])

No. 9006

ARE NET DISCOUNT RATIOS STATIOT{ARY?:THE IUPLICATIONS FOR

PRESENT VALUE CALCULATIONS

by

Joseph 11. Ilaslag*

Uichael Nlesnladomlr*

and

D , J . S l o t t j e *

Uarch L9 90

*Economis t , Research Depar tnent , Federa l Reserve Bank o f Da lLas ; EconomicsDepartruent, University of North Texas, Denton, Texas; and EcononicsDepar tment , Southern Method is t Un ivers i ty , Da l las , Texas respec t ive ly . Theviews expressed in this article are solely those of the authors and should notbe attributed to the Federal Reserve Bank of Dallas, the Federal ReserveSysten, the University of North Texas or Southern Methodist University.

Abstract

This paper analyzes the relat ionship between real interestrates and real growth rates in wages. The stationarity of thesetine series has been discussed in the l i terature. Hov/ever, sincethe net dis.count rat io, (1 + gJ/Q * r"), is a nonl ineartransformation, i t is not necessari ly stat ionary even' i f theinterest rate and growEh rate in wages series are each stationary.on the other hand, the net discount rat io, (L + S)/ (1 + rr), naybe stationary even if the interest rate and growEh rate series areboth stationary. The significant finding of this paper is thatthis net discount rat io, (1 + g.)/(1 * rr), is stat ionary. Thisconclusion appears robust since it holds for at Ieast fourdifferent Treasury securities analyzed: 3 nonth, 5 nonth, 1 year'and 3 year. Therefore a real. net discount rat io, (L + grl / ( I +rr), can be used with confidence in constructing present vafueforecasts of expected earnings.

j

d

j

1 I ntroducti on

Present value calculat ions are required for a nult i tude of

reasons. One of the most connon (and practical) reasons is to

determine the value of future lost earnings. Estirnating the

present value of future lost earnings, hovever, is a process

cornplicated by rnany factors. Sorne of the issues that have been

topies of recent research include the appropriate rnethods of

analyzing expected earnings (Becker and A1ter, 1987), the

age-earnings l i fe cycle (Lane and Glennon, 1985t Lambrinos and

Harnon, 1989) , f r inge benef i t s (N ieswiadorny and S lo t t je , 1988) ,

lost household services, disabi l i ty effects (Nies!.t iadony and

Si lberberg , 1988) , rned ica l care (Anderson and Rober ts f L989) and

the inpact of state and federal taxes (vernon, 1985). One topic,

though, appears to have received rnore attention than any other;

namely, the problern of determining the correct growth rate for

forecasting future earnings and deternining the correct interest

rate for discounting these earnings to the present.

The purpose of this paper is to explore the relat ionshi.p

between interest rates and growth rates using standard

s ta t i s t i ca l tes t fo r s ta t ionar i ty . l Spec i f i ca1 ly , th is paper

wiI l test for stat ionarity of the net discount rat io. Section

two discusses some of the past approaches in the l i terature to

determining the appropriate discount rate and grov/th rate. In

section three, unit root tests on the real growth rate in wages,

several real interest rates and several real net discount rat ios

are discussed. The nonlinear transfornation of the gror.t th rate

ln real wages and real interest rate that yields the net di.scount

rat io is discussed. Even i f the gror^rth rate of real wages and

rea] interest rates are stat ionary, this f inding would not inply

that the net discount rate is stationary. Section four presents

the enpir ical results obtained fron the unit root tests.

2 . Past Approaches

The nunber of different approaches to deter$ining the proper

growth rate and discount rate is considerably 1arge. Yet. even

in their disagreernent, nost researchers apparently agree on the

use of historical data in forrnulat ing their argunents, Perhaps

it is due to the bel ief that I 'History repeats i tself ' r . whether

or not this old adage applies to grolrth rates in earnings and

discount rates is the subject of this paper. l4ore specif ical ly,

this paper vi l l analyze the stabi l i ty of the relat ionship betr ieen

real wages and real interest rates using historical data.

Several researchers have suggested bypassing the entire

issue by using the rrtotal offset methodrt (also referred to as the

trAlaska Methodrt), whereby the grolrth rate in wages effect ively

o f fse ts the d iscount ra te (Franz , 1978t sch iL l ing , 1 "985) , As a

just i f icat ion for this nethod, i t is often argued that the

expected rate of inf lat ion is the prirnary force that inf luences

both the norninal wage growth rate and interest rates. This

nethod, however, makes the inpl ici t assunption that there is a

{

-a

stabl-e relationship betereen the two series

Furthermore, the growtti rate of wages and

assuned to be egual . Not everyone agrees

as we discuss be1ow.

Many researchers agree that grourth and discount rates nust

be expl ici t ly analyzed. Nonetheless, there is disagreenent over

many points. First, there is the question of analyzing growth

and discount rates independently or dependently (Laber, L9771.

Second, there is often disagreenent concerning the appropriate

tem to rnaturity of the security used for the discount rate,

although i t is general ly agreed that r iskless (as close as

possible) U.S. governnent securit ies should be used. Harris

(1983) argues that the rate on current short-tertn securit ies is

appropriate for discounti lrg. Carpenter et aI. (1986) argue for

the use of the average rate of return on inmediate annuity

contracts, nhi le Jones (1985, p. 147) argiues that qthen "interest

is high by historic standards, those high long-tern rates are

appropriate for discountingrt. StiLL other experts have

recornrnended a nix of high grade corporate bonds and governnent

securit ies be used in determining the discount rate (Hickrnan,

L9771 i others have suggested using long-tern Treasury issues

(BeI I and Taub, 1977, p . 126) i o r le t the rec ip ien ts leveL o f

investing sophist icat ion deterrnine the appropriate rate (Edwards,

1975). Third, there is the question of which industr ial sectorrs

rtage should be used (Lane and clennon, 1985,' Anderson and

Roberts, 1989 ) .

are equal .

the discount rate are

with this assunption,

- { .

rt

Returning to the question of dependence of growth rates and

discount rates, there is considerable variance in opinions.

several studies have found that the relat ionship is errat ic.

Leuthold (1981) uses 188 years of average consuDer Price Index

inf lat ion from 17,93 to L979 and concludes that the re).at ionship

between inf lat ion and interest rates is not stable. Hosek (1982)

argues that r l the usb of historical averages and relat ionships

provides a weak basis for estinating future grolrth rates in

income and future rates of interest so that one nust exercise

extrene caution ln the use of past datart. He provided evidence

vhich suggested that nominal wage rates and norninal interest

rates are nonstat ionary t irne series. Since nonstat ionary series

have moments that are functions of t ime, Hosekrs f indings inply

that historical data wit l_not provide useful advice for future

forecasts. Indeed, in the case where the t ime series has one

unit root, shocks in the data are perrnanent. schi l l ing (1985) '

using historical data (L900-1982) to make out-of-sample

forecasts, finds that the A1aska Method is the best of several

nethods, although none of the nethods perfonns very weII.

Several studies have found that there is a stable

relat ionship betlreen growth rates and discount rates. Lambrinos

(1985) found that real wages and real interest rates do exhibit

stat ionarity, and thus are appropriate for forecasting the

fu tu re . Anderson and Rober ts (1989) , us ing L952-82 da ta , f ind

that the relat ive dif ference betlreen the average annual after-tax

interest rate on short-tern securit ies and the averase annual

gtrosrth rate in after-tax earnings is stable. Their study differs'

frorn Schi l l ingts (1985) in two primary ways. First, they

consider short-tern reinvestment strategies, whereas schi l l ing

(198.5) used long-term bonds. Secondly, their t ine series (L952-

1982) was subs tan t iaLLy d l f fe ren t than Sch i l l i ngrs (1985) (1900-

1982). Bryan and Linke (1988) also f ind that the dif ference

between interest rates and wage gronth rates are reasonably

constant when analyzing the covariance between the rates of

growth of norkers I earnings and interest rates. They find the

average differential to be betvreen zero and one percent for one

year ancl twenty year Treasury securit ies over the L953-1984

period.

3. stat ionaritv Issues for waqes and Interest Rates

Stationarity is an irnportant and welL known concept in tirne

ser ies analysis. Essent ial ly, a t i rne ser ies is said to be

statlonary if the generating function for the series does not

i tsel f change through t i rne (Granger, L989, p. 66). This concept,

however, has not received much attention in the estimation of the

present value of expected earnings. This is unfortunate since

ser ious problems can ar ise when non-stat ionary data are used to

est imate the relat ionship between two var iables. Indeed, drawing

appropr iate stat ist ical inference is cornpl icated by potent ial

spur ious correlat ion. Enqle and Granger (L987) sho!, that non-

stat ionary t ine ser ies may be represented as polynornial funct ions

of t ine with a f ixed start ing point. I f two series share a

connon relati.onship with tine, then the chances that the

coeff icient, is signif icant wi l l be higher; that is, the estimated

correlat ion is potential ly spuriousz.

As the brief survey of the literature indicated, rnany

researchers have examined the irnportant issue of the relationship

between the growth rate and the discount rate. T\rro studies

(Hosek, 1982t Larnbrinos, 1985) have expl ici t ly exarnined the issue

of stat ionarity. while i t should be noted that these studies (as

veII as others) have nade a significant contribution to this

l i terature, the analysis should be extended further. Both Hosek

and Lambrinos examined the stationarity of the wage grohrth rate

and the interest rate as separate t irne series. But i t should be

recal led that the ult inat-e reason for analyzing the stat ionarity

of these t irne series is to determine i f the (1 + 9t)/ (1 + r")3

series is i tself stat ionary, lrhere rrr l stands for the real

interest rate and trgrr stands for the growth rate in real $rages.

Because the net discount rat io, (I + S"') / ( l - + rr), is a non-

linear transformation of the real interest rate and the growth

rate of real wages, there renains an addit ional concern even i f

r i and gr are each stat ionary. As Hallnan and Granger (L989)

have shown, non-l inear transforrnations applied to non-stat ionary

t ime serj-es can yield stat ionary series, and vice-versa.

Consequently, using stat ionary series such as r" and 9., i f they

are found to be stat ionary, does not inply that the net discount

ra t io , (L + g t l / (L + r t ) , i s s ta t ionary .

To test for stat ionarity, i t is necessary to determine the

order of integration of the t ine-series being considered. f f the

order of integration is equal to zero, then the series is said to

be stat ionary. I f , on the other hand, the series is integrated

of order d (denoted I(d)), where d is sorne posit ive integer, then

differencing the series d t ines yields a stat ionary series,

Hence the series i tself is non-stat ionary. Note that d also

corresponds to the nunber of unit roots ln the t ine series.

Univariate analysis (unit root test ing) is conducted to determine

the order of integration. For this study we analyze the average

hourly r.rage in the private nonagricultural sector (defLated by

the cPI) and the real interest rate on different Treasury

securit ies.

Several nethods to test for the presence of unit roots are

avai lable. In this paper, the augmented Dickey-Fuller (1979)

specif icat ion is adopted. Fornal ly, this is represented as

( 1 ) Ax , =c * Fx t - r4

+ t 6 , A x ._ , .i = 1 "

The presence or absence of a unit root depends on the value of

the coeff icient p. The nuLL hypothesis is that the coeff icient

on the variable, xi-1 is zero, I f so, then x. has (at least) one

unit root. f f the test stat ist ic indicates that the coeff icient

is signif icantly less than zero, the series, x" , does not have a

unit root. Hence, the variabl.e is stat ionary.

The test statistic is of the fonn of the usual s tudent rs t

4 .

for B, but the distr ibution of the test stat ist ic is non-nornal

even asynptotical ly. The appropriate cumulative distr ibution is

provided in -FuLler

(L976r. Frorn this cumulative distr ibution,

the probab i l i t y tha t the t -s ta t i s t i c i s Iess than -2 .88 ( i .e . ,

the probabil i ty of a Type-I error) is f ive percent.

Unit-Root Tests for stationarity

The data are monthly and are available for the period

l-964:1-1989:4.4 To calculate the ex post real return, we used

the nominal interest rate and subtracted the inflation rate

(rneasured as the annualized rate of change in the cPf) that

existed unti l that security matured. For example, the norninal

return that was registered (on average) for 3 nonth bills in

Januaryr less the inf lat ion rate over the period January to

Apri l , yields the real return. The presurnption here is that the

expected inf lat ion level equals actual inf lat ion. Thus, the

model inposes the condit ion that expectat ions are rat ional . with

n' = r, the real return is, therefore, the norninal. return less

the inflation rate for the period during !,thich the Treasury

security was outstanding ' 5

Equation (L) is est imated using levels of the t ine series of

interest rates and real wages. I t should be noted that the leveL

of real interest rates is trrrr. However, the real wage rate rnust

be converted to percentage changes to yield grr, the growth

variable (rvi th which lre are concerned). Four dif ferent Treasury

securit ies are analyzed: 3-r[onth, 5-nonth, l-year, and 3-year.

The resuLts are presented in Table 1. As Table L indicates' the

estirnated coeff icients on the Iagged value of al l of the Treasury

securit ies variabl-es are negative. Sirni lar ly, the coeff icient on

the lagged value of the (Iog of) real average hourly earnings is

negative.€ In aII of the cases, however, the t-stat ist ics, are

snaller ( in absolute value) than -2.14. since the 5* cri t ical

val-ue is -2.88, the evidence is consistent with the levels of

average hourly earnings and real interest rates having a

unit-root, and hence, al l of the series are nonstat ionary when

considered individual ly. of course the stat ionarity of the real

wage growth rate (g) still nust be tested, but we have already

found that real interest rates are not stat ionary. This f inding

does not agree with Larnbrinos' (1985) conclusion that real

interest rates are stat ionary. Hortever, Lambrinos ' ( l -985)

conclusion l tas based on correlograns, not unit-root test ing.

Thus no unanbiguous statistical inferential properties could be

attached to his conclusion.

In the second test, a t ine trend variable is included in the

regression as shown in Equation (2).

(2 )4

A X t = c * F x t - r + : 5 t A x r - i + t t. l - .

'

The nuLl hypothesis is that the coeff ic ients on the lagged level

of the series under scrut iny and on the t ine variable are joint ly

equal to zero. The intuit ion behind this test is that the series

nay be made.up of both determinist ic and stochastic trend

components.t The F-stat ist ic for this nul] hypothesis wil l

exceed i ts cr i t ical value i f ei ther ( i) the determinist ic trend,

here captured by the coefficient on the tirne trend variable,

explains a large port ion of the t ime series (which is ref lected

in the coefficient on the tirne variable belng different froIrL

zero) i or ( i i ) the stochastic trend is srnal l (which results in

the coeff icient on the lagged value beinq signif icantly less than

zero), The results of this second test are consistent with those

in the f irst test; that is, under the nul l hypothesis' the

F-stat ist ics are al l less than 3.82 for the real interest rates.

The F-stat ist ic is 4.42 f1r average hourly earnings. In al-1

cases, therefore, the values of the F-stat ist ics are well below

the cri t ical value of 6.34' so that we fai l to reject the nul l

hypothesis. Thus, even with a trend adjustnent, the various

interest rate and growth rate series are not stationary.

The next step is to determine whether a second unit root is

present in the data. I f so, then the f irst dif ferences are

non-stat ionary. Equation (L) is also estimated witb f irst

dif ferences of the various real interest rates (r) and the growth

rate (g) of real average hourly earnings. The resu.Lts of these

estirnations are also presented in Table L ( in the second colunn) .

Under the nu).1 hypothesis that the coefficient on the lagged

first dif ference of the Treasury interest rate is less than zero,

10

the t-stat ist ics range fron -5.11 to -9.5o. In each case the

evidence suggests that the f irst dif ference of these real

interest rate series are stat ionary. This indicates that these

Treasury interest rate series rnust be first differenced before

any forecasting is done using these individual series. However,

the grorth rate of the real average hourly earning series is

stationary since the nodel using the growth rate (g) in real

average hourly earnings has a t-stat ist ic of -5.33. Furthernore,

nhen a tine trend is included in the nodels, the conclusions

based on the F-statistics in the last column of Table l are

congruent with the unit-root tests in equation (L): the f irst

dif ferenced real interest rate series are stat ionary, and the

growth rate in real wages is stat ionary. ?his second resuLt is

consistent with Larnbrinos_l (1985) conclusion that the gror^tth rate

ln real wages is stat ionary, according to his correlogran.

In short, the evidence is consistent with the real interest

rates not being stationary but the growth rate of real average

hourly earnings being stat ionary. This result could present

serious problens for forecasting the present vaLue of expected

future earnings since only one of the series are stat ionary.

Holrever, as noted above, i t is possible that the (L + gL) / (L +

r") series is stationary even though the real interest rate is

not stat ionary since this series is a non-l inear transformation

of the r" and g" series.

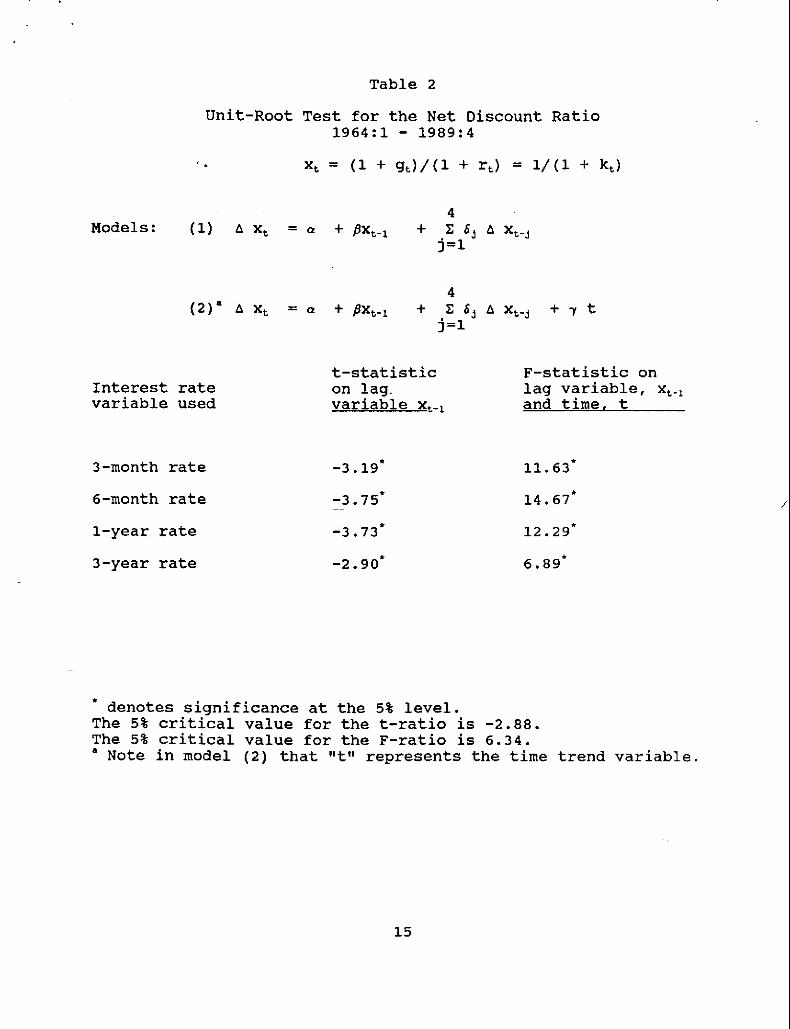

Unit root tests on the net discount rat io,

(L + g" r / (L + r r ) , a re p resented in Tab le 2 . These tests were

t1

conducted ln a sirni lar fashion to the ones described in Tabl.e 1.

Four dif ferent net discount rat ios are constructed, one for each

of the dif ferent real interest rates under consideration, rvhi le

the sane growth rate in real wages is used each tirne. The

results indicate that the net discount ratj.o is stationary in

each case. This concl-uslon holds whether the time trend is

included or not. These results appear to be guite robust trith

respect to the choice of different Treasury securities used in

constructing the net discount ratio.

sone sunnary stat ist ics are shown in Table 3. of interest

is the nean values of the net discount rate, k = (r - q/G + g).

These nean values range from approxirnately zero to plus two

percent. Thus, based on the t ime period under consideration, the

Alaska rule does not appear to general ly hold.

5. Conclusion

This paper has found that_the growth rate in real wages is

stat ionary, as Lanbrinos (1985) concluded. Our results dif fer

with Lambrinosr (1985) conclusion, however, because real interest

rates are not stat j .onary. However, the issue of individual

stat ionarity of the interest rate and growth rate series is

real ly moot. Ult imately, the concern is over the stat ionarity of

the net discount series, (7 + qJ/ (1 + rr), because this is the

variable of interest. I t has'been noted (Hallnan and Granger,

L2

1989) that stat ionarity of individual- series does not guarantee

stat ionarity of a non-l inear transfonoation such as (1 + 9r)/ ( l +

r"). The signif icant f inding of this paper is that this net

d iscount ra t io , (L + g ) / (1 + r r ) , i s s ta t ionary . Th is

conclusion appears robust since it holds for at Least four

dif ferent Treasury securit ies analyzed: 3 nonth, 6 month' 1 year,

and 3 year. Therefore a real net discount rat io, (I + gE)/ (L +

rr), can be used with confidence in constructing present value

forecasts of expected earnings.

13

Table 1

Unit-Root Test for Real Interest Ratesand Rea I Wages , 1964 :L - 1989 :4

4Mode l s : ( 1 ) AX t : d * Px t - r + t 6J a x ! - J

- l - 1

4(2 ) 'Ax i =d * Fx t - r + 5 6J a x r - J + r t

j =r.

t-stat ist ic F-stat ist ic onon lag lag var iabl€, Xt-rvar iable xr-r and t ine, t

Var iable

3-rnonth rate

6-rnonth rate

1-year rate

3-year rate

real wage

Leve} Chanqe Level chanqe

-1 .99 -9 .60 ' 3 .48 46 ,08 *

-? . r4 - - 7 . 60 ' 3 .82 28 .96 '

- 1 .90 -5 .00 ' 2 .75 1 -7 .98 '

- 1 .48 -5 . 11 - 1 . 46 15 . L4 -

-o .8 t - 5 .33 ' ' b 4 .42 L5 .59 ' ' b

' denotes signif icanee at the 5* level.

The 58 cri t ical value for the t-rat io is -2.88.The 58 c r i t i ca l va lue fo r the F- ra t io i s 5 .34 .o Note in nodel (2) that rrt tr represents the t ime trend variable,o The growth rate in real hrages is used,

Table 2

Unit-Root Test for the Net Discount Ratio1964 :1 - 1989 :4

x" = (1 + 9J / (1 + r t ) = l rz (1 + k r )

4l , lodeLs: (1) A Xr = c * Fxt ,_r + E 6J A xr_ j

j=r

4(2 ) ' A x r = c * Px t - r + . t 6 l A x r - l + t t

j =1

Interest ratevariable used

3-nonth rate

6-month rate

1-year rate

3-year rate

t-stat ist ic F-stat ist ic onon lag, lag var iabL€, xt-rEEleb"lc-Jr-r andline-i

- 3 .19 '

-1 .7s-

- J . / J

-2 . go*

11 .53 -

L4 . 67 '

t -2 .29*

6 .89 .

' denotes significance at the 5* Ievel .

The 5t cr i t ical value for the t-rat io is -2.88.The 5* c r i t i ca l va lue fo r the F- ra t io i s 6 .34 .' Note in rnodel (2) that rt tr t represents the t irne trend variabte,

I 3

Table 3

Sunmary Statist ics forRatios and Rates,

the Net Discount1964-1989

Net Discount

Using the followingTreasurv securit ies

3 -nonth6-nonthL-year3 -year

Rat io : (1 + q ' l / ( L + t )

Mean

1 .010 .980 .980 .98

standardDev iat i on

0 .050 .0s0 .050 .06

Net D iscount Rate : k = ( r - S) / (7 + g )

Using the followingTreasurv securities

3 -month6-monthL-year3 -year

l'lean

0 .02-0 .003

0 .010 .02

StandardDeviat i on

0 . 050 .050 .050 . 05

1 6

References

Anderson, cary A. and David L. Roberts, 1989, rrstabi l i ty in thePresent Value Assessment of Lost Earningsrr ' Journal of Risk andInsurance, 55 : 50-55 .

Anderson, cary A. and David L. Roberts, 1989, rrAn Histor icafPerspect ive on the Present Value Assessnent of uedical care. "Journaf of l isk andlnsuEance. 56:. 2L8-32.

Becker, Wi] l iarn E, and ceorge c. Al ter, 1987, rrThe Probabif i ty ofLife and workforce status in the Calculation of ExpectedEarn ings , t t @, 54a 364 -75 .

Bel1, Edward B. and A}]an J. Taub, 1977, ' rAddit ional comnent ' r tJournal of Risk and Insurance, 542 L22-29.

Bryan, wi l l ian R. and Charles l , ! . L inke, L988, ' rEst inat ing PresentVaLue of Future Earnings: Experience with Dedicated Port fol ios, "Journal of Risk and Insurance, 551. 273-86.

carpenter, Michael D., David R. Lange, Donald s. Shannon andWil l ian Thornas Stevens, 1985, " l i tethodologies of Valuing LostEarnings: A Review, A Criticisn, and A Recomnendation, tt J.9U-&a.Io f R i sk and Insu rance , 53 : 104 -18 .

Edwards, N. Fayne, 1975, I tselect ing the Discount Rate in Personalfnjury and wrongful Death cases,t t @,52 . 342 -45 .

Engle, R,F. and C,W.J. Granger, 1977, t tgo-Integrat ion, and Error-correct ion: Representat ion, Est inat ion and Test ing,rrEconone t r i ca , 55 : 251 -76 .

Franz, wolfgang w., 1978, I 'A Solut ion to Problens Ar is ing fromInf lation when Determlninq Danages , 'r J.9g-E!.e-1--91--&i.9.\--a.ndI-DEUIeA-DSC, 45: 323-33.

Ful ler, wayne A., I9 '76, Introduct ion to Stat ist ical Tine Series,Ne$r York: wi ley.

c ranger , c .w .J . , 1989 , Fo recas t i nq i n Bus iness and Economics ,Boston: Acadernic Press.

Ha l l nan , Je f f rey J . and C .W.J . Granger , r rThe A lgeb ra o f I (1 ) , "Journal of Time Series, forthcoming.

Har r i s , w i l l i an c . , L983 , r r l n f l a t i on R isk as De te rn inan t o f t heDiscount Rate of Tort settlements, " Jgg!rla_I___qc_3_ig_E--A_rl!!I !@gC, 50 : 265 -80 .

L7

Hickman, Edgar P., I97 7, rr Further Comment,,, J.9g.g!.e.1_!E_8iEI_g-!.9Insurance, 54.. 129-32.

Hosek. Wi l l ian R., 1982, rrProblens in the Use of Histor ical Datain Est imat ing Econonic Loss in Wrongful Death and Injury Cases,t lJou rna l o f 'R i sk and fnsu rance , 49 : 300 -308 .

Jones, David D., 1985, I t lnf lat ion Rates Irnpl ic i t in Discount ingPersonal Injury Econornic Losses, tt @,52 : L44 -L50 .

Laber, cer le, !977, rrThe Use of Inf lat ion Factors in DeterniningSett lenents in Personal In jury and Death sui ts: comment, t t Journalof Risk and Insurance, 44l . 469-73.

Lanbrinos, Janes, 1985, ' ron the Use of Histor ical Data in theEst i rnat ion of Econornic Losses,t ' @,52 r 464 -7 6 .

Lambrinos, Jarnes and oskar R. Harmon, 1989, nAn Enpir icalEvaluation of Trrro Methods For Estinating Econornic Danages,t'Journal of Risk and Insurance, 56a 733-39.

Lane, Jul ia and Dennis Glennon, 1985, [The Est imat ion ofAge/Earnings Prof i les in Wrongful Death and Injury cases, ' rJournal of Risk and fnsurance, 522 686-95.

Leuthold, steven c. , 1981; r lnterest Rates, Inf lat ion andDe f la t i on , t t @, i l an -Feb . . 28 -40 .

Nieswiadony, l . I ichael L. and Daniel J. Slot t je ' L988' rrEst inat ing

L,ost Future Earnings Using the New Workl i fe Tabfes: A Connent,r lJournal of Risk and Insurance. 55' . 539-44,

Nieswiadony, Michael t . and Eugene si lberberg, 1988, rrCalculat ingchanges in Workl.ife Expectancies and Lost Earnings in Personalfn ju ry Cases , t t @, 55? 492 -98 .

Pagan, A. R. and U.R. Wickens, 1989, [A Survey of RecentEcononetric tlethods , tt EE_.Eg.9.LgE!e--E9U-f.!-a.f. , 99 | 962-1025 .

schi l l ing, Don, 1985, "Est inat ing Present VaLue of Future incomelosses : An H is to r i ca l S imu la t i on 1900-1982 , r r Jou rna l o f R i sk and&-SgIA.nge, 52: 100-116.

sn i th , F rank l i n c . , L9?6 , I ' The Use o f I n f l a t i on Fac to rs i nDeterruining Sett lements in Personal In jury and Death sui ts, ' lJou rna l - o f R i sk and Insu rance , 43 r 369 -76 .

Stock, James H. and Mark w. Watson, L988, ' rvar iable Trends inEconoroic Tirne Series, rrThe Journal of Econonic Perspect ives,rr 2:L47 -74 .

18

vernon, Jack, 1985, t rDiscount ing After Tax Earnings with AfterTax Yields in Torts Sett lenents, tr Journal of Risk and Insurance,2 .696 -?03 .

19

Endnotes

L. The other factors such as tax rates and age earnings prof i leswhich inf luence speci f ic present value calculat ions are notanalyz'od in this paper. They do not s igni f icant ly af fect ourconclusions.

2. Spurious correlation, hovrever, is not problenatic t{hen thetwo ser ies are co- integrated. Because a l inear cornbinat ionof the two ser ies is stat ionary, ( i .e. , not a polynonialfunct ion of t ine), the inferences about the correlat ioncoeff ic ient are val id. See Pagan and Wickens ( l -989) for adetai led, intui t ive discussion of integrated t ine ser ies andco-integrat ion.

3. This rat io is also sonet ines wri t ten as L/ ( I + kr) , where k.is referred to as the net discount rate (e.9. , Anderson andRoberts, 1989 ) .

4. 1964 was the f i rst year in vrhich nonthly changes in hour lyltagfe rates lrere available.

5. Mishkin (1988) uses this approach to calculate the ex postreturn ser ies.

6. The uni t-root test was also conducted for the level of thereal !'tage . As one rnight expect, $tith a unit root in the log-leve1 of the ser ies, the evidence indicated that a uni t -root

, was present in the real wage level as wel1.

7. See Stock and l {atson (1988) for a descr ipt ion of the breakdownof a ser ies into i ts determinist ic and stochast ic t rendconponents .

20

RESEARCH PAPERS OF THE RESEARCH DEPARTMENTFEDERAL RESERVE BANK OF DALI,AS

Awailable, at no chafge, froru the Research DepartmencFederal Reserve Bank of Dal las. Stat ion K

Dal las, Texas 7 5222

8901 An Xconometric-Analys ls of'{J.. S:--Oil Demand (Stephen P.A. Browrr andKei th R. Phi l l ips )

8902 Further Evidence on the Liquidity Effect Using an Effic ient - Marke tsApproach (Kenneth J. Robinson and Eugenie D. Short)

8903 As)nnmetric Infornation and the Role of Fed l^Iatching (Nathan Balke andJoseph H. Has lag)

8904 Federal Reserve System Reserve Requirements: 1959-88--A Note (JosephH. Haslag and Scot t E. Hein)

8905 Stock Returns and Inf la t lon: Fur ther Tests of the Proxy and Debt-Monetizatlon Hypothesis (David E1y and Kenneth J. Roblnson)

8906 Real Money Balances and the Tirning of Consumptlon: An EmpiricalInvest lgat ion (Evan F. Koenig)

8907 The Ef fects of F inancia l Deregulat ion on fnf la t ion, VeLoci ty Growth,and Monetary Targeting (W. Michael Cox and Joseph H. Haslag)

8908 Dayl ight Overdraf ts : Who Real ly Bears the Risk? (Robert T. Cla i r )

8909 Macroeconornic Policy and Income Inequality: An Error - Correct ionRepresentat ion (Joseph H. Haslag and Danie l J . S loct je)

8910 The Clearing House Tnterbank Pa1rments Systen: A Description of ItsOperations and Risk Management (Robert T. Clair)

8911 Are Reserve Requirement Changes Really Exogenous? An Exarnple ofRegulatory Acconunodation of lndustry Goals (Cara S. Lown and John H.Idoo d)

8912 A Dynamic Comparison of an Oil Tariff, a Producer Subsidy, and acasoLine Tax (Mine YuceL and Carol Dahl)

8913 Do Maquiladoras Take American Jobs? Sorne Tentatiwe EcononetricResults (Williarn c. cruben)

8914 Nominal GNP Growth and Adjusted Reserve Growth: Nonnested Tests ofthe St . Louis and Board Measures (Joseph H. Haslag and Scol t E. Hein)

8915 Are the Permanent - Incorne Model of Consuuption and the AcceleratorModel of Investment Compat ib le? (Evan F. Koenig)

8916 The Locat ion Quot ient and Centra l P lace Theory (R. in . Gi lmer, S. R.Kei I , and R. S. Mack)

89L7 Dynamlc Modeling and Testing of OPEC Behavior (Carol Dahl and MineYuceI )

9001 Another 'l l.eok - at the Credit-Output Link (Cara S. Lown and Donald W.Hayes )

9002 Demographics and the Forelgn Indebtedness of the United States (JohnK . H i l l )

9003 Inf la t ion, ReaI In terest Rates, and the Fisher Equat ion Slnce 1983(Kenneth M. Ernery)

9004 Banking Reform (Gerald P, O'Dr lscol l , Jr . )

9005 U.S. Oi l Dernand and Conservat ion (S.P.A. Brovrn and Kei th R. Phi l l ips)

9006 Are Net Discount Racios Stat ionary?: The lnp l icaf ions for PresentValue Calculat ions (Joseph H. Haslag, Michael Nieswiadomy and D.J.S l o t t i e )