fedglobal international payments jorge jimenez [email protected] federal reserve bank of...

TRANSCRIPT

FedGlobal International Payments

Jorge [email protected]

Federal Reserve Bank of AtlantaRetail Payments Office

2

International opportunity

2

IAT Volume Projections

Source: Federal Reserve Banks. Spring 2011.

Countries

2009 Business account to

account payments

2011 Business account to

account payments

2009 Consumer account to cash

payments

2011 Consumer account to cash

payments

Mexico* n/a 68% n/a 55%

Europe 37% 66% 21% 24%

China 25% 58% 13% 13%

Japan 18% 42% 9% 13%

Central America 18% 24% 14% 21%

3

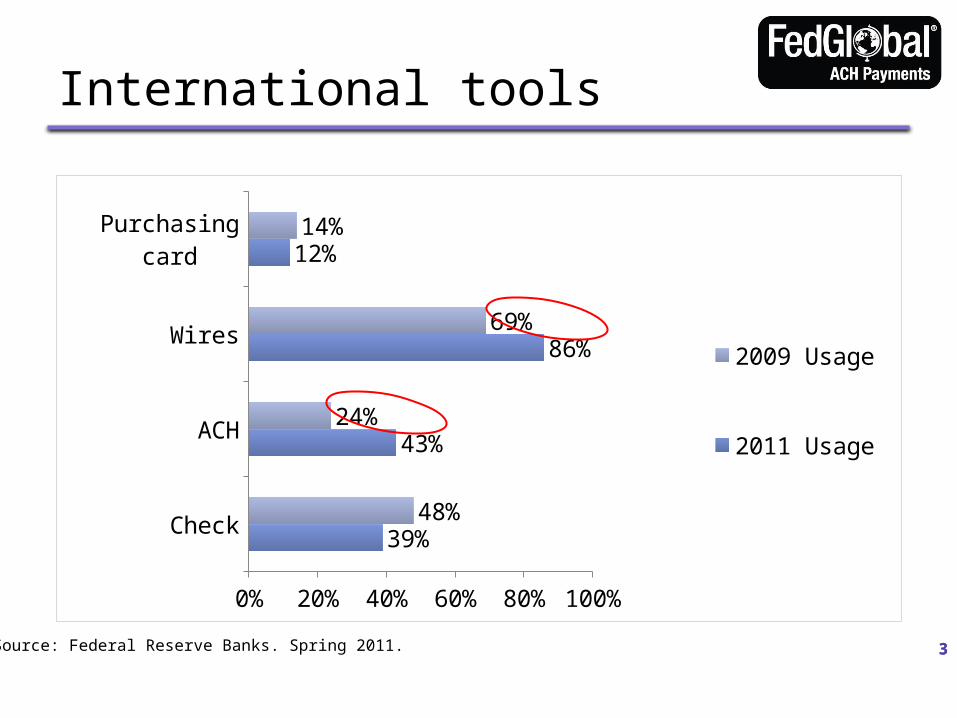

International tools

3

Check

ACH

Wires

Purchasing card

0% 20% 40% 60% 80% 100%

39%

43%

86%

12%

48%

24%

69%

14%

2009 Usage

2011 Usage

Source: Federal Reserve Banks. Spring 2011.

International Business Payments

International Payments Today

Traditionally only offered by the largest global banks

High fees compared to domestic

Beneficiaries paying beneficiary deductions

5

Remittances Today

Workers Remittances

P2P

Traditionally offered by Money Transfer Providers in non banking channels

Today many senders have bank accounts

International Consumer Wires are now considered remittances too

Workers Remittances

P2P

International Business Payments

ACH

International

Expanding ACH

FedGlobal: expanding FedACH’s reach

7

LiveSouth America

Argentina, Brazil, Columbia, Peru, Uruguay (A2R) D + 1

Central America

Costa Rica, El Salvador, Guatemala, Honduras, Nicaragua (A2R) D + 1

Panama D + 2

North America

Canada D + 1

Mexico (A2A and A2R) D + 1

Mexico – F3X (Mexican Peso) D + 1

Region Countries Funds to RDFI

Europe Austria, Belgium, Cyprus, Czech Rep., Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxemburg, Malta, Netherlands, Poland, Portugal, Slovakia, Slovenia, Spain, Sweden, Switzerland, United Kingdom

D + 3

F3X (Euro and UK Pound) D + 2/D+3

FedGlobal benefits

No Beneficiary Deductions

Lower Costs

True Innovation in BankingConsistent Delivery Times

Best Foreign Exchanges

International Offering Accessible to all

institutions regardless of size

FI can also handle own exchange

International Business Payments

ACH

International

Improves transparency for customers

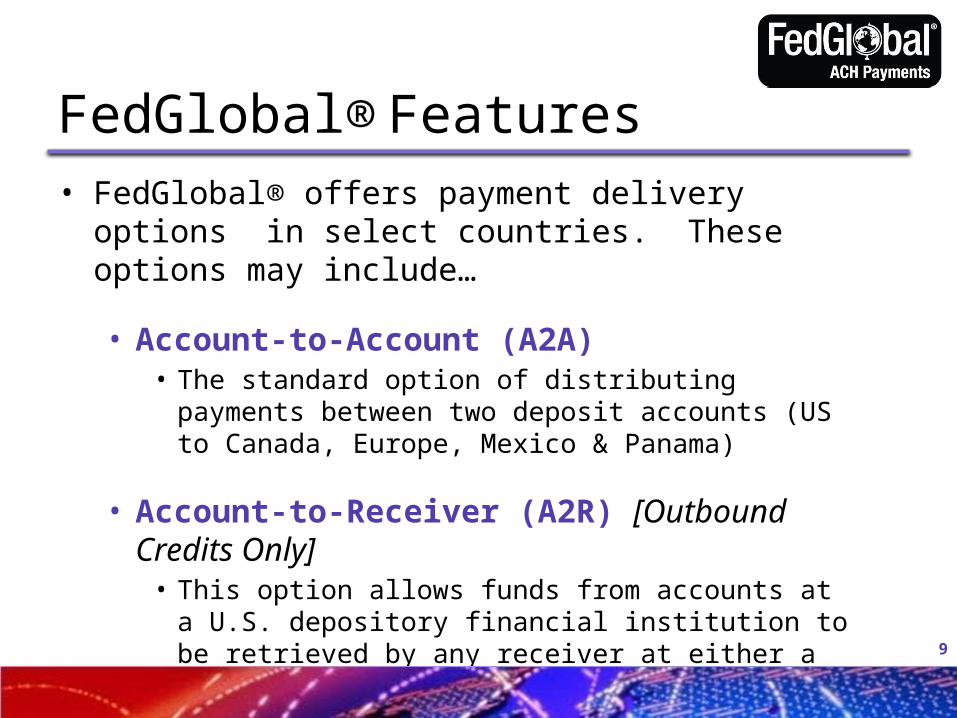

FedGlobal® Features• FedGlobal® offers payment delivery options in select

countries. These options may include…

• Account-to-Account (A2A)• The standard option of distributing payments between two

deposit accounts (US to Canada, Europe, Mexico & Panama)

• Account-to-Receiver (A2R) [Outbound Credits Only]• This option allows funds from accounts at a U.S. depository

financial institution to be retrieved by any receiver at either a participating bank location or at a trusted, third-party provider in certain receiving countries. ($1,000 or less per item)

9

Foreign Exchange Options• The FedGlobal Service accommodates the following foreign

exchange options [varies by service country]:

• Fixed-to-Variable: USD to Local Currency • FX rate conversion performed by Foreign Gateway Operator

• Fixed-to-Fixed: USD to USD• Transfer and receipt of USD to U.S. dollar-denominated accounts

• Fixed-to-Fixed: Local Currency to Local Currency (“F3X”)• FX performed by ODFI• Settlement process is outside of U.S. ACH Network

10

11

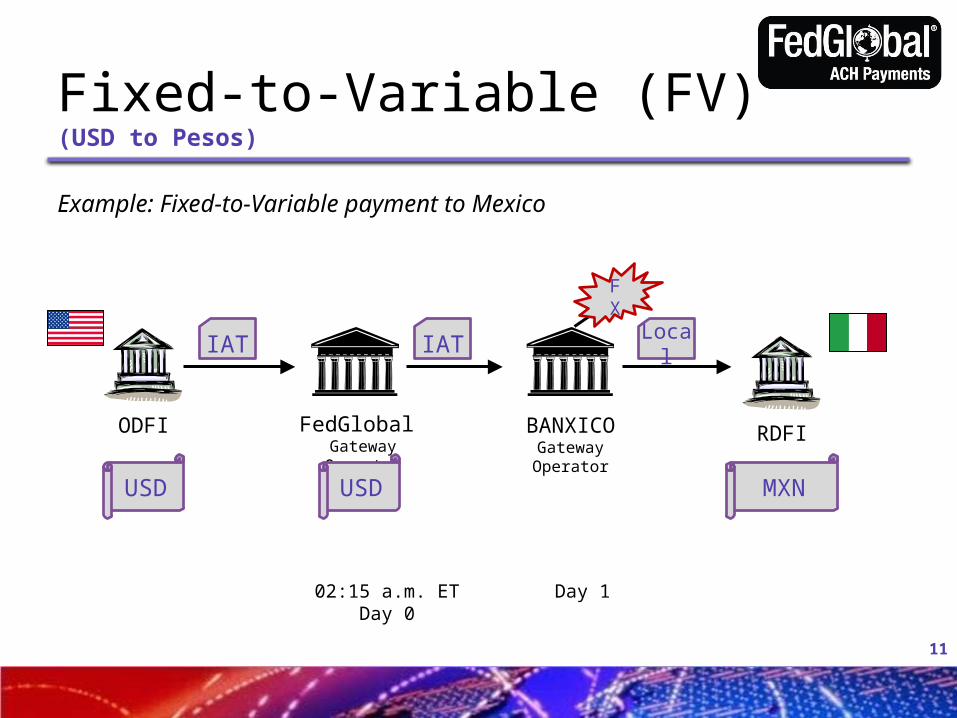

Fixed-to-Variable (FV)(USD to Pesos)

Example: Fixed-to-Variable payment to Mexico

11

ODFI FedGlobal Gateway Operator

RDFIBANXICO Gateway Operator

IAT IAT Local

USD USD MXN

FX

02:15 a.m. ETDay 0

Day 1

A2R Latin America (including Mexico)• Allows payments from accounts at a U.S. depository financial institution to

be retrieved by any receiver at either a participating bank location or at a trusted, third-party provider in certain receiving countries.

• Delivery to Latin America leverages the Federal Reserve’s Gateway Operators: Banco de Mexico in Mexico and Banco Rendimento through MFIC reaching another 10 countries in the region

• More than 8,000 delivery points

• Millions of potential Receivers

12

Domestic vs International ACH

In domestic transactions you can use US ABA# and Account number, but what about International transactions?

13Image Source Page: http://howtogeekon.com/2010/05/18/fit/square-peg-in-a-round-hole_0565/

International

A2A Gateway RT and Canada: CPA # and Account numberPanama:RT# and Account numberMexico: ABM# and CLABE (18 digits)Europe: BIC# and IBAN

14

International

A2RGateway RT andMexico: 647R (ABM)

Password (acc#)Latin America: CO00212336750000023642

(table from fedglobala2r.com)

525565656511(phone number)

15

Driving compliance provisions include:

• Financial Recordkeeping and Reporting of Currency and Foreign Transactions Act of 1970” – (BSA)

• Money Laundering Control Act of 1986• USA PATRIOT Act of 2001 • CIP provisions (Sec. 326 USA Patriot ACT)• Office of Foreign Assets Control • 1073 Dodd-Frank

Your Regional Payments Association can help you stay updated

16

Compliance Fundamentals

17

FedGlobal ComplianceFedGlobal monitors payments processed and maintains a compliance program which includes:

1) OFAC and Anti-Money Laundering policies and procedures;

2) Transaction monitoring in support of OFAC and AML due diligence

3) Establishing compliance obligations for payment processing in agreements with gateway operators and third-party service providers;

4) Risk assessments of FedGlobal offerings that include evaluations of gateway operators and third-party service providers as well as country risk assessments

All Consumer originated transactions are now considered Remittances and fall under Reg.E. Consumers need to be provided with the following disclosures at time of origination among other provision

• Exact Foreign Exchange (or Estimated in some FedGlobal cases)• Exact fees and taxes applied at origination• Exact fees and taxes applied at receipt• Exact day of funds availability to beneficiary

While Industry impact still uncertain, your Regional Payments Association can help you stay updated

18

Dodd-Frank: Some considerations

Working past the SilosWhen thinking of implementing FedGlobal we suggest you include

representatives from…

…

19

Treasury Services Compliance

Community Development International Desk (if present)

Retail Banking Operations

Opportunity

20

While there is a significant margin available, the transaction itself is not normally the primary revenue objective but rather the financial institution’s overall relationship and cumulative sum of business revenue with the customer.

Overall customer relation involves:

• quantifying customer retention and acquisition

• quantifying revenue potential on cross-selling opportunities

Country Surcharge to financial institutions

Average cost to consumers

Account to:Account (A2A)

Unbanked (A2R)

Mexico $0.67 $3.45 $12.59 Brazil . $4.40 $13.34

Colombia . $4.40 $21.05

El Salvador . $4.40 $11.08

Guatemala . $4.40 $13.64

Honduras . $4.40 $10.34

Peru . $4.40 $15.27 Europe $1.25 . $30-$70Panama $0.72 . $30-$70

www.remittanceprices.worldbank.org/countrycorridors. August 2010

Not official data for Europe and Panama . Anecdotal data based on limited customer data

Marketing tools

Questions & Answers

Federal Reserve Bank of AtlantaRetail Payments Office

Copyright © Federal Reserve Bank of Atlanta (USA) 2010