fiduciary oversight: a process & approach to best practices charles a. bruder, esq. scott...

Post on 21-Dec-2015

216 views

TRANSCRIPT

Fiduciary Oversight:A Process & Approach to Best Practices

Charles A. Bruder, Esq.

Scott Rappoport

The material provided herein is for informational purposes only and is not intended as legal advice or counsel.

2

Please help yourself to food and drinksPlease let us know if the room temperature is too hot or coldBathrooms are located past the reception desk on the rightPlease turn OFF your cell phonesPlease complete and return surveys at the end of the seminar

Fiduciary Oversight &

Timely Topics For Benefit Plan Sponsors

4

Fiduciary Oversight In The Spotlight

LaRue v. DeWolff (Supreme Court 10/2007) ERISA litigation up 25%/year (past 4 years) Pension Protection Act (2006) DOL disclosure initiatives (2008) Changes to Form 5500

5

Who is a Fiduciary?Any person who:

Exercises any discretionary authority or discretionary control in managing the plan or who has any authority or control in managing or disposing of its assets;

Has any discretionary authority or responsibility in administrating the plan; or

Renders investment advice for a fee or compensation with respect to any monies or other property belonging to the plan.

6

Responsibilities Of a Fiduciary Under ERISA

Fiduciaries are required to perform their duties solely in the interest of the plan participants and their beneficiaries.

Fiduciaries must exercise the care, skill, prudence, and the diligence of a prudent person who is acting in a like capacity and is familiar with such matters.

7

What are Fiduciaries’ Exposures Under ERISA?

Fiduciary liability is personal, absolute and unlimited. ERISA

holds fiduciaries personally liable for their actions.

8

Safe Harbors

Voluntary

May insulate from liability

Must demonstrate compliance with requirements: Prudent selection Prudent Monitoring Acknowledgement of fiduciary status

9

404(a) Safe Harbor Provisions

Investment decision delegated to “prudent expert” Experts selected by due diligence process Experts exercise discretion over assets Expert acknowledges co-fiduciary status in writing Fiduciary must ensure that experts perform the

agreed upon tasks using agreed upon criteria

10

404(c) Safe Harbor Provisions

Requires notification in writing of intent to comply with 404(c) safe harbor

Three different investment options with differing risk/return profiles

Information and education on the different investment options

Opportunity to change investments with appropriate frequency.

11

Fiduciary Adviser Safe Harbor Provisions

Select a qualified fiduciary adviser who:

Acknowledges fiduciary status in writing

Discloses all conflicts of interest Discloses all forms of compensation

12

Qualified Default Investment Alternative (QDIA)

Plan sponsor can avoid liability for participant investment decisions by offering QDIA

Age-based funds or models Risk-based funds or models Age-based managed accounts Money market accounts for 90-120 days

13

Fiduciary Oversight Benefit Sources & Solutions Best Practices

Creation of the Investment Policy Statement/Governing Body Document

Creation of the Investment Committee Designation of qualified professional investment

counsel Ongoing monitoring & reporting

14

Monitoring & ReportingBenefit Sources & Solutions Best Practices

Review actual Portfolio for MPT Statistics Appropriate Index Peer group

Compare investment expenses for risk & reward Create a quarterly correlation matrix Review operational quality of investment managers Disclose plan expenses and revenue sharing Create “plain English” quarterly “minutes” for plan

sponsor tied to an annual IPS review Standards defined in the IPS

15

Monitoring & Reporting

Investment Committee Meeting Minutes

Information that is provided must be evaluated andactions that are considered must be documented

Watch list procedures must be followed

16

How Can Benefit Sources & Solutions Help

Fiduciary Review Checklist Mutual Fund Review Source of technical information 888-560-5171

17

18

ARRA COBRA Subsidy

Became Law February 17, 2009 Involuntary Terminees from 9/1/2008-12/31-2009 Effective March 1, 2009 65% Premium Subsidy COBRA Beneficiary remits 35% of 102% Difference is offset by payroll tax credit Employer is not responsible for determining income

eligibility

19

ARRA Notice Requirements

By April 18, 2009, notice of new COBRA eligibility enrollment option to eligible beneficiaries who did not elect COBRA

9 Month Subsidy period

20

Children’s Health Insurance Program (CHIP)

Effective April 1, 2009 Applies to all plans including self insured Children eligible for premium assistance under state

programs can elect employer sponsored plans This necessitates new eligibility period for those

choosing the employer sponsored plans. SPD’s for Medical and Cafeteria plans require

updated language.

21

Do These Things Keep You Awake at Night?

Controlling Expenses Employee Retention Leveraging Resources Human Capital Challenges Lack of Control Regulatory Burden

22

Why Benchmarking

Does the “annual train wreck” work for you? Do you have a benefits and comp philosophy? Desire to be a competitive employer Turnover Issues Morale Issues Communications

23

About the SurveyConducted Q1 & Q2 2008

Joint effort of 142 UBA Members

12,680 Employers Survey

168,019 Health Plans

National In Scope

24

Who is United Benefit Advisors?

Consortium of 140 of the Nation’s Premiere Benefits Firms

Community of peers learning, sharing & focusing on better serving their clients

Leverage our connections, experience & wisdom to enhance the client experience

Work in tandem to maximize the impact technology has on improving business processes

25

Full-Time Eligibility Requirements

4.9%

8.3%

53.5%

7.1%4.6%

17.6%

3.9%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

20 Hrs. 25 Hrs. 30 Hrs. 32 Hrs. 35 Hrs. 40 Hrs. Other

26

Full-Time Employee Waiting Period

8.0%

5.3%

2.1%

8.6%

0.8%

11.9%

19.8%

7.3%

30.5%

3.3%2.3%

0%

5%

10%

15%

20%

25%

30%

35%

0 Days 30 Days 60 Days 90 Days 180+Days

0 Days 30 Days 60 Days 90 Days 180+Days

Other

Immediately Following First of Month Following

27

54.2%

21.3%

10.2%12.6%

1.1% 0.6%

0%

10%

20%

30%

40%

50%

60%

PPO HMO POS CDHP EPO FFS

Type of Plan Offered

28

Annual Cost Per Employee - Total Cost

$7,597

$6,736

$8,060

$6,456

$7,252

$9,960

$7,327

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

PPO HMO POS CDHP EPO FFS ALL

29

$281$351

$433

$370

$691

$859

$1,065

$901

$0

$200

$400

$600

$800

$1,000

$1,200

Single Family

Total Monthly Premiums

25th Percentile Median 75th Percentile Average

30

6.3%

12.0%

18.0%

12.9%

1.5%

8.0%

13.0%

7.4%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Initial Offer - Last Plan Anniversary Final Change - Last Plan Anniversary

Changes to Total Premiums

25th Percentile Median 75th Percentile Average

31

15.0%

25.0%

40.0%

27.7%25.0%

48.6%

60.5%

46.0%

0%

10%

20%

30%

40%

50%

60%

70%

Single Family

Monthly Employee Share –% of Premium

25th Percentile Median 75th Percentile Average

32

$21 $27$44

$100

$416

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

PCP SCP Urgent Care Center Emergency Room Per Admission CoPayor Deductible

Average CoPays

33

$500

$1,000

$1,500

$1,105$1,000

$2,000

$3,000

$2,554

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

Single Family

In-Network Deductibles

25th Percentile Median 75th Percentile Average

34

$500

$1,000

$2,250$1,768

$1,200

$3,000

$6,000

$4,131

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

Single Family

Out-of-Network Deductibles

25th Percentile Median 75th Percentile Average

35

9.8%

28.8%

5.6%

55.6%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

% Offering WellnessProgram

Cash to Premium, 401(k),FSA, etc.

Extra Paid Time Off Gift Certificates or HealthClub Dues

Incentives Included

Wellness Programs and Incentives

36

Wellness Programs & Components

78.7%

34.5%

40.2% 39.1%

51.0%

12.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Health RiskAssessment

Seminars /Workshops

Physical Exam orBlood Draw

Coaching Incentives /Rewards

Other

37

HRA And HSA Plans

4.5% 5.8%

71.0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

% Offered % Enrolled % With FirstDollar Preventive

8.3%5.4%

85.4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

% Offered % Enrolled % With FirstDollar Preventive

HRAs HSAs

38

Annual HRA Funding Levels

$1,000

$1,209

$2,000

$2,274

$0

$500

$1,000

$1,500

$2,000

$2,500

Median Single Average Single Median Family Average Family

39

Type(s) of employee communication tools utilized:

41.9%

83.5%

91.1%Employeemeetings

Non-personalizedhandout materials

Individuallypersonalized

handout materials

(Note: More than one response could be selected, so the percentage of the total responses exceeds 100%)

40

Type(s) of employee communication tools utilized:

30.7%

23.1%

6.1%

3.0%

Dedicated website for all company-provided employee benefits(employee benefits portal)

Personalized employee total pay andbenefits cost statements (hidden

paycheck)

Telephonic call center

Interactive Voice Response (IVR)communications

(Note: More than one response could be selected, so the percentage of the total responses exceeds 100%)

41

Employer-Paid group benefit programs:

51.8%

67.2%

72.9%

84.2%

15.4%

10.8%

10.0%

4.3%

6.9%

5.4%

3.5%

2.8%Group Term Life

Group Dental

Group LongTerm Disability

Group ShortTerm Disability

In Place / Likely Next Year Would Like Someday More Info

42

19.5%

43.5%

50.5%

64.7%

No

Yes, via phone-basedconsultations

Yes, via in-person consultations

Yes, via printed material frominvestment vendors

Employee access to financial advice regarding retirement plan savings and investment options:

(Note: More than one response could be selected, so the percentage of the total responses exceeds 100%)

43

Employee programs or services in place or planned:

33.2%

55.4%

78.9%

19.5%

16.2%

4.4%

9.2%

8.3%

1.3%Casual dress day

Flexible hours

Work-at-home(telecommuting)

policy

In Place / Likely Next Year Would Like Someday More Info

44

Participate in the 2009 Benefit Sources & Solutions/UBA Survey and Receive Custom Benchmarking Report Results

Go to www.benefitsource.com and see National Health Plan Survey

Fiduciary Oversight:A Process & Approach to Best Practices

Charles A. Bruder, Esq.Norris McLaughlin & Marcus, P.A.

46

I may have violated the provisions of a company sponsored retirement plan…

what can I do?

47

Fiduciary Duties and Corrective Action – A Practical Approach

• Several available options– Do nothing, and hope that the problem is not discovered– “Self correct” the potential fiduciary breach– Disclose the breach to the appropriate government

agency/program

• The key to addressing a breach of a fiduciary duty is identifying the available correction methods and determining the appropriate course of action

48

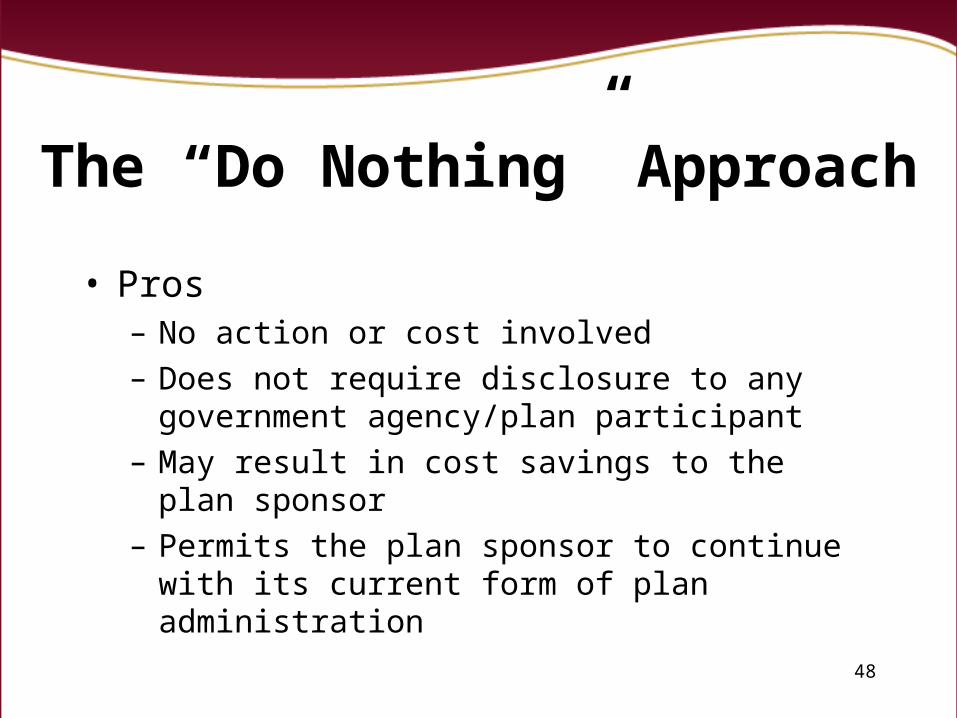

The “Do Nothing” Approach

• Pros– No action or cost involved– Does not require disclosure to any government

agency/plan participant– May result in cost savings to the plan sponsor – Permits the plan sponsor to continue with its

current form of plan administration

49

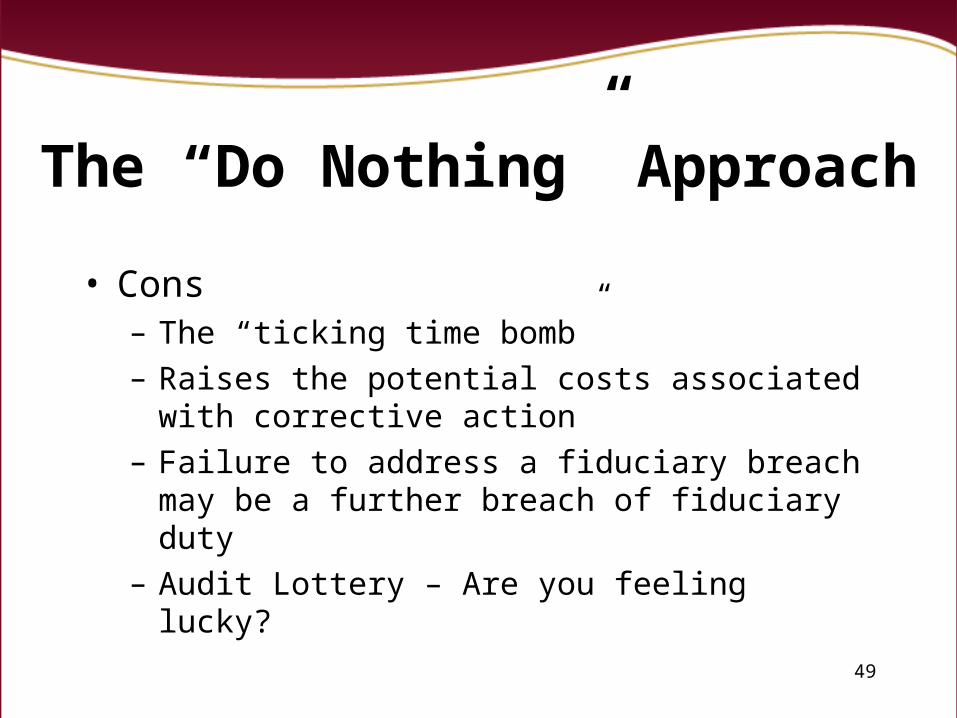

The “Do Nothing” Approach

• Cons– The “ticking time bomb”– Raises the potential costs associated with

corrective action– Failure to address a fiduciary breach may be a

further breach of fiduciary duty– Audit Lottery – Are you feeling lucky?

50

Fiduciary Duties and Corrective Action – A Practical Approach

Available Corrective Programs1. Employee Plans Compliance Resolution System

(“EPCRS”)

2. Voluntary Fiduciary Correction Program (“VFCP”)

3. Internal Revenue Service (“IRS”) Notice 2008-113

51

Employee Plans Compliance Resolution System

• EPCRS contains three correction programs:– Self-Correction Program (SCP)– Voluntary Correction Program (VCP)– Audit Closing Agreement Program (Audit CAP)

52

Employee Plans Compliance Resolution System

Qualification Failures• Plan Document Failure

– Plan provision (or absence of provision) that violates the Code

• Operational Failure– Plan document complies with the Code but plan

doesn’t operate in accordance with its provisions

53

Employee Plans Compliance Resolution System

Principles and Correction Methods• Full correction required for all plan years• Acceptable correction methods & retroactive plan

amendments– Expanded definition of “reasonable and appropriate”

• Model correction methods provided in Appendices A & B of Rev. Proc. 2008-50

54

Employee Plans Compliance Resolution System

SCP – Self Correction Program• No disclosure to IRS, no fee, no sanctions• Can only correct operational failures• Must have a favorable IRS Determination

Letter• Must have established practices &

procedures to assure ongoing compliance• Corrective action requires documentation

55

Employee Plans Compliance Resolution System

SCP – Self Correction Program• Insignificant vs. significant failures

– Applicable corrective period – choosing the right one

– Factors in determining the type of failure which may be self-corrected

• What if the failure cannot be self-corrected?

56

Employee Plans Compliance Resolution System

VCP – Voluntary Compliance Program• Single program and single-admission process• Submission procedures• Ends with a compliance statement – Don’t

need to sign statement• Determination Letter/Retroactive Plan

Amendment may result in Determination Letter if plan on-cycle

57

Employee Plans Compliance Resolution System

SCP versus VCP• Distinction between insignificant and significant errors• List of Factors to Consider

– whether failure occurred during period of exam– % of assets/contributions involved– # of years involved– % of participants affected– % of participants who could have been affected– correction within reasonable period– reason for the failure

• Uncertainty for plan sponsor

58

Employee Plans Compliance Resolution System

Rev. Proc. 2008-50: New Fee Schedule• VCP fee unchanged• Compliance fee for §401(a)(9) failures reduced to

$500• Fee for failure to amend for EGTRRA good-faith

amendments, §401(a)(9) interim amendments, and amendments required to implement optional law changes: flat $375

59

Employee Plans Compliance Resolution System

Audit CAP• Higher sanction• Factors used in determining sanction:

– Practices in place to identify and prevent plan failures

– Steps taken to correct failures– Reason for the failures

60

Employee Plans Compliance Resolution System

Audit CAP• Length of time that failures occurred• Number of NHCEs affected if plan is disqualified • Existence of a favorable Determination Letter• Whether the error involves a demographic failure• Whether the only failure is an employer eligibility

failure

61

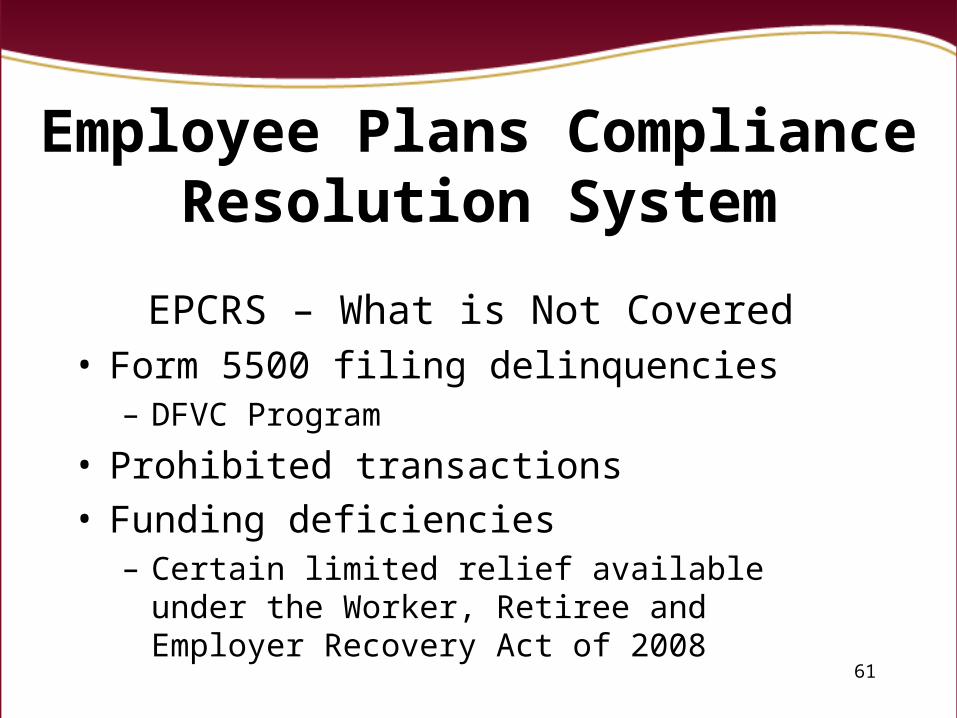

Employee Plans Compliance Resolution System

EPCRS – What is Not Covered• Form 5500 filing delinquencies

– DFVC Program

• Prohibited transactions• Funding deficiencies

– Certain limited relief available under the Worker, Retiree and Employer Recovery Act of 2008

62

Fiduciary Duties and Corrective Action – A Practical Approach

Voluntary Fiduciary Corrective Program• Corrective program sponsored by the U.S.

Department of Labor– Certain enumerated transactions which may be

corrected• Prohibited purchases• Sales and exchanges• Improper loans• Delinquent contributions• Improper plan expenditures

63

Fiduciary Duties and Corrective Action – A Practical Approach

Why VFCP?• Type of corrective action required• Avoidance of civil penalties imposed by the IRS• Obtain a DOL “no action” letter• Avoidance of the imposition of excise taxes if the

class exemption provisions are met• Processing/corrective costs• Forum shopping

64

Voluntary Fiduciary Correction Program

VFCP – Class Exemptions • Six classes of prohibited transactions covered

– Failure to transmit contributions/loan payments in a timely manner

– Loans made to parties in interest– Sales of property with parties in interest– Sales of real property to a plan with a leaseback to the

employer– Purchase of an illiquid asset by a plan– Certain plan expense issues

65

EPCRS or VFCP?

• Which program is appropriate for correction of a fiduciary breach?– Type of action (or inaction) which resulted in the

breach of fiduciary duty– Appropriate correction method

• Crossover issues

– Cost/benefit analysis– Processing time

66

Fiduciary Duties and Corrective Action – A Practical Approach

Code Section 409A• Although not technically a “fiduciary duty,” a

potential source of financial woe for an employer• Code section has broad application to a variety of

arrangements• IRS Notice 2008-113 provides a model correction

program– Expands the program established under IRS Notice

2007-100

67

IRS Notice 2008-113• Program scope

– No relief for documentary compliance failures• Includes required amendments

– Limited relief available for “insiders”– Applicable to “inadvertent and unintentional” errors– “Full” correction is required– Avoidance of excise taxes

68

IRS Notice 2008-113Eligibility Provisions

• “Inadvertent and unintentional” operational errors– Impermissible payments made to an employee

• Demonstrable steps must be taken to avoid future errors

• Recipient’s income tax return for the year in which the error occurred cannot be under IRS audit

• The error has been fully corrected– IRS guidelines for full correction

• The company cannot be in financial distress– Significant risk of non-payment?

69

IRS Notice 2008-113

Same Year Corrective Method• Early payments must be returned to the

company• Late payments must be to the employee

- Non-insiders may take up to 24 months from income tax return due date to repay

- Requires immediate and heavy financial need

• Interest payments may be required• Avoidance of Code Section 409A penalties

70

IRS Notice 2008-113

Post Year Corrective Method• Non-insiders• Corrective methods are similar to the “same

year” correction guidelines• Employee may be required to make interest

payments• Avoidance of Code Section 409A penalties

71

IRS Notice 2008-113Other Key Features

• Correction of impermissible stock right grants– “Reset” feature

• Limited corrective opportunity for other operational errors– $16,500 ceiling in 2008

• Other corrections permitted but will not avoid the 20% excise tax

• Employer notice requirements

72

Code Section 125 New Proposed Treasury Regulations

• Effective for plan years commencing on or after January 1, 2009

• Apply to all arrangements which qualify for beneficial income tax treatment under Code Section 125– Group Medical Insurance Plans (“Flex Plans”)– Premium Only Plans– Medical Flexible Spending Accounts– Dependant Care Flexible Spending Accounts

73

• Treasury Regulations clarify that Code Section 125 is the exclusive means under which nontaxable group health benefits may be provided to employees– If your company plans do not satisfy the provisions

of the new proposed Treasury Regulations, benefits paid under these plans will be taxable to the participants.

Code Section 125 New Proposed Treasury Regulations

74

Code Section 125 Proposed Treasury Regulations –

What Has Changed?Written Plan Requirement

– Plans must include the following items:• Specific details concerning all benefits available under the

plan• Eligibility provisions for participation (employees only)• Rules governing benefits elections, maximum elective

contribution limits• Rules governing the irrevocability of elections• Details concerning employer contributions• Definition of plan year

– Plans must be operated in accordance with stated terms

75

Code Section 125 Proposed Treasury Regulations -

What Has Changed?Nondiscrimination Testing Required

– Cafeteria plans cannot discriminate in favor of highly compensated employees

– Similarly situated employees must have a uniform opportunity to elect to receive benefits

– Objective nondiscrimination testing formula is provided in the Treasury Regulations

– “Safe Harbor” for premium-only cafeteria plans

76

Code Section 125 Proposed Treasury Regulations –

What Should Employers Do?• Treasury Regulations apply to plan years

commencing on or after January 1, 2009• Need to carefully review plan documents

– Summary plan descriptions– Intranet/employee communications– Cafeteria plan forms brochures

• Amend plan documents currently (if necessary)• Create a compliance manual

77

COBRA Subsidy – Notice Requirements

• By April 18, 2009, group health plans subject to COBRA must issue to “assistance eligible individuals” notice of the extended election period of COBRA coverage and the COBRA subsidy provisions.– A model notice is to be issued by the Secretary of Labor by March

19, 2009.– 60 day election period

• The notice must include specific information including:– The forms necessary to establish eligibility for the premium

reduction; – Contact information for the plan administrator regarding the

premium reduction;– A description of the extended election period;– A description of the individual’s obligation to notify the plan

administrator of eligibility for subsequent group health plan coverage; and

– A description of the eligible individual’s right to a coverage.

78

COBRA Subsidy -Notice Requirements

• Notices must be provided to assistance eligible individuals who became entitled to elect COBRA continuation coverage during the period September 1, 2008 through December 31, 2009

• Notice regarding the special election provisions must be provided to all persons who terminated employment (for reasons other than gross misconduct) from September 1, 2008 through December 21, 2009.

Questions & Answers

Thank you for coming!