fin4320 - sample final exam fixed income...

TRANSCRIPT

FIN4320 - Sample Final Exam Fixed IncomeSecurities

1

1 Problem 1

a) Write the price function and plot the price of a 15 year bond, nominalvalue 1000, coupon 5.5% with annual payment, as a function of the yield tomaturity. Use a range of yields from 0 to 20% with increments of 2%.b) Compute the $duration analytically and numerically when the yield is

6%.Usei) 1 basis point increment for the numerical approximationii) use a smaller increment equal to :0000001. Do you notice any di¤erence

in the two numerical approximations?c) Explain what does this number measure.d) Plot the linear approximation of the bond function about the 6% yield.e) What is the error from the approximation when the yield is 6%.f) What is the error when the yield is 5.99%.g) What is the error when the yield is 12%e) Comment on e, f , and g.

P (y) =15Xt=1

55(1+y)t

+ 1000(1+y)15

0.00 0.02 0.04 0.06 0.08 0.10 0.12 0.14 0.16 0.18 0.200

200

400

600

800

1000

1200

1400

x

y

2

P (:06) = 951: 438 755 061 30

Numeric duration

P (:06+:0001)¡P (:06):0001

= ¡9388: 77P (:06+:0000001)¡P (:06)

:0000001= ¡9394: 95

Analytic duration

15Xt=1

¡t55(1+:06)t+1

+ ¡15¤1000(1+:06)16

= ¡9394: 95Linear approximation

L(y) = P (:06)¡ 9394: 95(y ¡ :06)

Error when rate is 6% and increase is 0L(:06)¡ P (:06) = 0:0Error when rate is 5:99%L(:0599)¡ P (:0599) = 952: 378 ¡952: 379 = ¡0:001Error when rate is 12%L(:12)¡ P (:12) = 387: 742 ¡557: 294 = ¡169: 552

2 Problem 2

This is a big problem for practice. You will not be required to do it all, butonly part of it and to explain.Assume that you manage a portfolio that includes several dozens of dif-

ferent bonds. The characteristics of the portfolio are

Value Yield Modi�ed Duration Convexity$103 768 :81 5:5% 7: 438 073 5 70: 949 696

Assume that in the market there are three bonds with the following spec-i�cations.

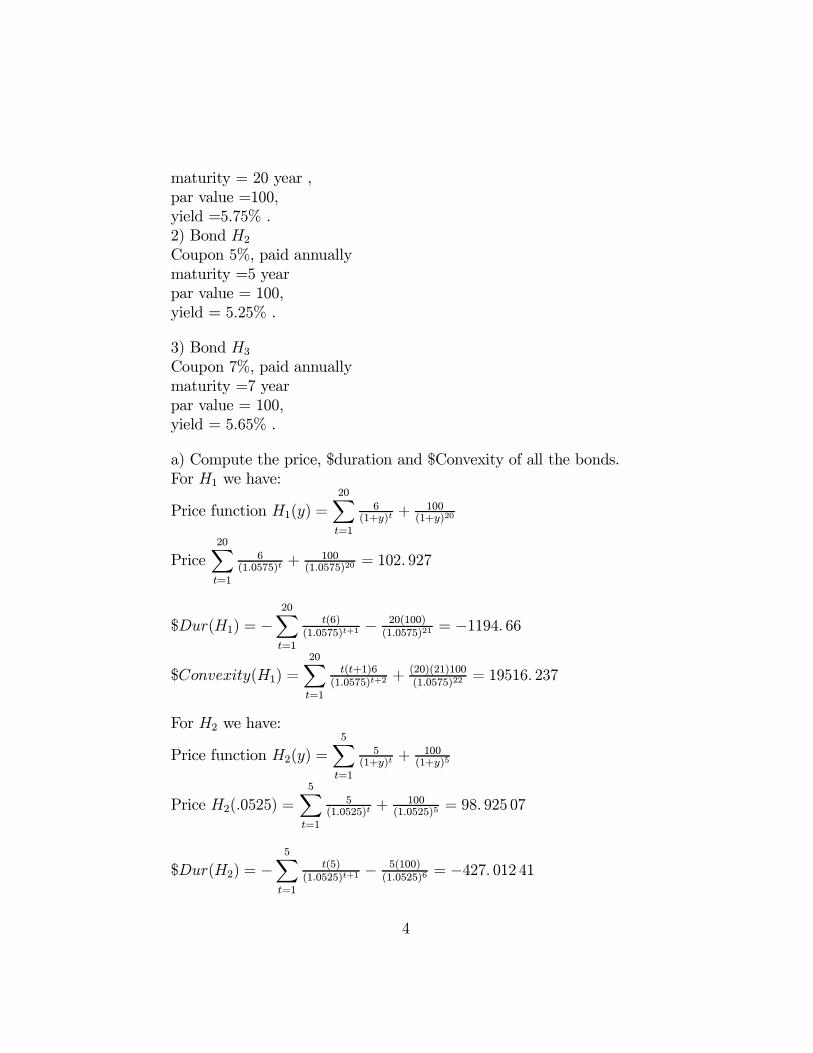

1) Bond H1Coupon 6%, paid annually.

3

maturity = 20 year ,par value =100,yield =5:75% .2) Bond H2Coupon 5%, paid annuallymaturity =5 yearpar value = 100,yield = 5:25% .

3) Bond H3Coupon 7%, paid annuallymaturity =7 yearpar value = 100,yield = 5:65% .

a) Compute the price, $duration and $Convexity of all the bonds.For H1 we have:

Price function H1(y) =20Xt=1

6(1+y)t

+ 100(1+y)20

Price20Xt=1

6(1:0575)t

+ 100(1:0575)20

= 102: 927

$Dur(H1) = ¡20Xt=1

t(6)(1:0575)t+1

¡ 20(100)(1:0575)21

= ¡1194: 66

$Convexity(H1) =20Xt=1

t(t+1)6(1:0575)t+2

+ (20)(21)100(1:0575)22

= 19516: 237

For H2 we have:

Price function H2(y) =5Xt=1

5(1+y)t

+ 100(1+y)5

Price H2(:0525) =5Xt=1

5(1:0525)t

+ 100(1:0525)5

= 98: 925 07

$Dur(H2) = ¡5Xt=1

t(5)(1:0525)t+1

¡ 5(100)(1:0525)6

= ¡427: 012 41

4

$Convexity(H2) =5Xt=1

t(t+1)5(1:0525)t+2

+ (5)(6)100(1:0525)7

= 2354: 732 8

For H3 we have:

Price function H3(y) =7Xt=1

7(1+y)t

+ 100(1+y)7

H3(:0565) =7Xt=1

7(1:0565)t

+ 100(1:0565)7

= 107: 630 87

$Dur(H3) = ¡7Xt=1

t7(1:0565)t

¡ 7(100)(1:0565)8

= ¡600: 557 21

$Convexity(H3) =7Xt=1

t(t+1)7(1:0565)t+2

+ (7)(8)100(1:0565)9

= 4196: 22

b) Use the �rst bond above to hedge your portfolio to the �rst orderchange in y. In other words, form a portfolio that is duration neutral. Howmany unit of the bond should you buy or sell? Report the number q.Since the value of the portfolio is a function of the yield we write P (y)We denote the change in P (y) as dP (y).

For a small change in the yield we know that dP (y) can be approximatedby @P (y)

@ydy:

So we write

dP (y) ¼ @P (y)

@ydy = $Dur(P )dy

dH(y) = $Dur(H)dydP (y) = $Dur(P )dy

dP (y) + qdH(y) = 0implies(q$Dur(H) + $Dur(P ))dy = 0

since dy 6= 0 by assumption, it must be that

$Dur(P )¡ q$Dur(H) = 0

5

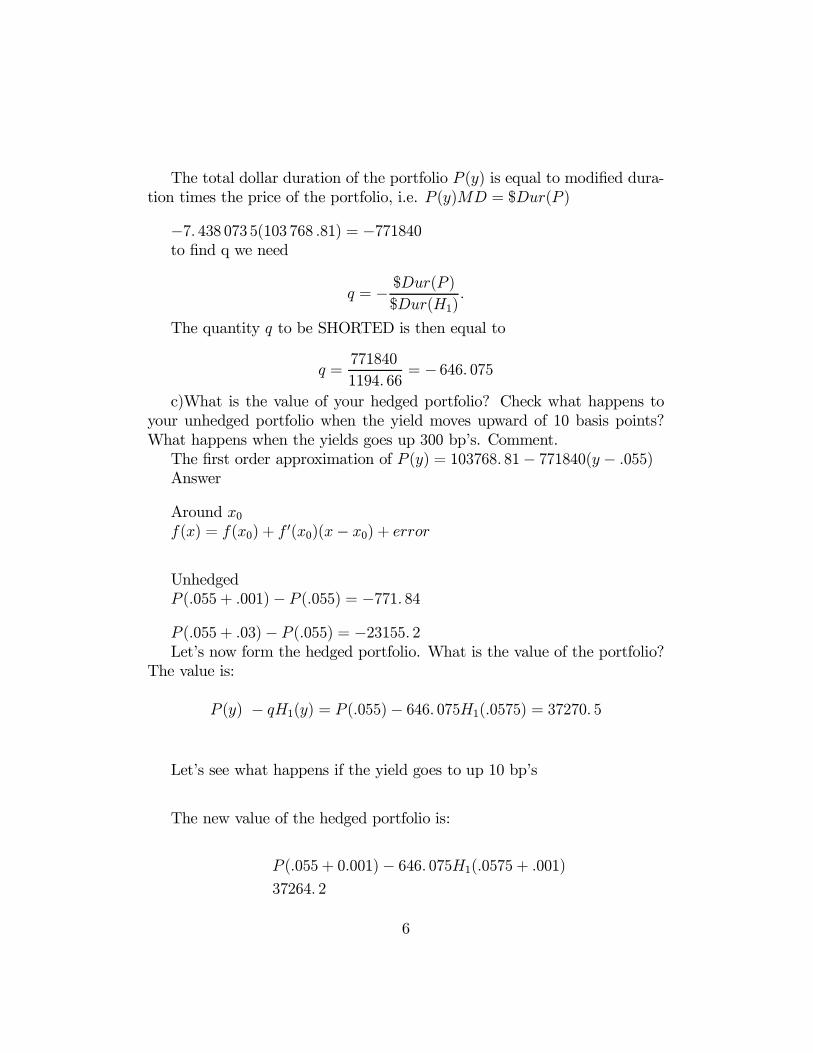

The total dollar duration of the portfolio P (y) is equal to modi�ed dura-tion times the price of the portfolio, i.e. P (y)MD = $Dur(P )

¡7: 438 073 5(103 768 :81) = ¡771840to �nd q we need

q = ¡ $Dur(P )$Dur(H1)

:

The quantity q to be SHORTED is then equal to

q =771840

1194: 66= ¡ 646: 075

c)What is the value of your hedged portfolio? Check what happens toyour unhedged portfolio when the yield moves upward of 10 basis points?What happens when the yields goes up 300 bp�s. Comment.The �rst order approximation of P (y) = 103768: 81¡ 771840(y ¡ :055)Answer

Around x0f(x) = f(x0) + f

0(x0)(x¡ x0) + error

UnhedgedP (:055 + :001)¡ P (:055) = ¡771: 84P (:055 + :03)¡ P (:055) = ¡23155: 2Let�s now form the hedged portfolio. What is the value of the portfolio?

The value is:

P (y) ¡ qH1(y) = P (:055)¡ 646: 075H1(:0575) = 37270: 5

Let�s see what happens if the yield goes to up 10 bp�s

The new value of the hedged portfolio is:

P (:055 + 0:001)¡ 646: 075H1(:0575 + :001)37264: 2

6

P (:055 + 0:001) = 102997¡646: 075H1(:0575 + :001) = ¡65732: 7P (:055 + 0:001)¡ 646: 075H1(:0575 + :001) = 37264: 2102997¡ 65732: 7 = 37264: 3The new value of the hedged portfolio is:

The loss is 37264: 3¡ 37270: 5 = ¡6: 2Let�s see what happens if the yield increases 300 bps

The new value of the hedged portfolio is:

P (:055 + :03)¡ 646: 075H1(:0575 + :03) =

The new value isP (:055 + :03) = 80613: 6H1(:0575 + :03) = 74: 442 8P (:055 + :03)¡ 646: 075H1(:0575 + :03) = 32518: 0and the loss is32518: 0¡ 37270: 5 = ¡4752: 5d) Use bonds H1 and H2 and H3 above to hedge your portfolio to the

second order changes in y, while keeping the value of portfolio unchanged. Inother words, form a portfolio that is duration neutral and convexity neutral.This means that you want to �nd 3 quantities q1; q2; and q3 such that theduration and convexity of your portfolio are both equal to zero, and the totalinvestment necessary to hold the position is unchanged. Report the systemthat you have set up and the solution, i.e. q1; q2; and q3:

Answer

Or we can write the system in the form

0 = q1H1(y) + q2H2(y) + q3H3(y)

P0(y) = ¡q1H 0

1(y)¡ q2H0

2(y)¡ q3H0

3(y)

¡P 00(y) = q1H

00

1 (y) + q2H00

2 (y) + q3H00

3 (y)

7

We can now use the information about our bonds to set the hedgeThe total duration of the portfolio P (y) is equal to the number of certi�-

cates times the $duration of each certi�cate.$Convexity = 103 768 :81(70: 949 696) = 7: 362 37£ 106Hence

0 = q1103 + q299 + q3108

771840 = ¡q11195¡ q2427¡ q3601¡7362365: 5 = q119516 + q22355 + q3419624 0

771840¡7362366

35 =24102: 926 60 98: 925 07 107: 630 87¡1194: 66 ¡427: 012 41 ¡600: 557 2119516: 237 2354: 732 8 4196: 22

35 24q1q2q3

35So we have24102: 926 60 98: 925 07 107: 630 87¡1194: 66 ¡427: 012 41 ¡600: 557 2119516: 237 2354: 732 8 4196: 22

35¡1 24 0771840:¡7362366:

35 =24 237: 959 567357: 534 6¡6989: 974 1

35=

24q1q2q3

35These are the q’s we are looking for.f) Consider now the hedged portfolio. Compute its value at the time the

hedge is set up. Then check what happens to your hedged portfolio when theyield moves upward of 10 basis points? What happens when the yields goesdown 300 bp’s. (Hint, do not forget to de�ne a QUADRATIC price functionfor the portfolio). Comment.Answer. As expected the hedged portfolio is worth at the time of the

hedge

P (:055)+237: 959 6H1(:0575)+7357: 534 6H2(:0525)¡6989: 974 1H3(:0565) =103768: 78Rede�ne the portfolio quadratic functionP (y) = 103768: 81¡ 771840(y ¡ :055) + 7362366

2(y ¡ :055)2

Let’s apply a 10 basis points change to the 3 bonds

8

P (:055+ :001)+237: 959 6H1(:0575+ :001)+7357: 534 6H2(:0525+:001)¡6989: 974 1H3(:0565 + :001) = 103712: 87Total loss without hedgingP (:055 + :001)¡ P (:055) = ¡768: 158 82The loss with hedging is 103712: 87¡ 103768: 81 = ¡55: 94

Let’s apply a 300 basis points change to the 3 bondsP (:055+:03)+237: 959 6H1(:0575+:03)+7357: 534 6H2(:0525+:03)¡6989:

974 1H3(:0565 + :03) = 102284: 63

Loss without hedging

P (:055 + :03)¡ P (:055) = ¡19842: 135Now the loss with hedging is102284: 63¡ 103768: 81 = ¡1484: 18

3 Problem 3

Nelson and Siegel propose to �t the yield curve with a function of the fol-lowing form.

R(0; µ) = ¯0 + ¯1

Ã1¡ e¡ µ

¿

µ¿

!+ ¯2

Ã1¡ e¡ µ

¿

µ¿

¡ e¡ µ¿

!Here µ; is the maturity, and ¿ is a scaling parameter.a) Brie�y, explain the meaning of the parameters ¯0; ¯1; and ¯2.b) Estimate the ¯0; ¯1; and ¯2 and ¿; for the U.S. government securities

constant maturities on 1/2/2004, using the data in the data sheet. Convertto continuos compounding. Report the parameters estimates and the valueof the minimized loss function, i.e. the sum of the squared di¤erences of therates.6:0217% ¡ 5:3243% ¡ 0:1437% 3:33loss function = 4:69407E ¡ 06

9

c) Use the curve that you have estimated to price a 15 year U.S. govern-ment year bond, with annual coupon 5%. and face value equal to 1000. Usecontinuos compounding for the discount factor.

Price 1035:267

d) Estimate the $ sensitivities to changes in ¯0; ¯1; and ¯2 of a portfoliomade of 1000 certi�cates. Numerically, estimate all sensitivities with anincrement of :0001:Assume that you expect a 1% decrease of ¯1 and you have no view with

respect to ¯0; and ¯2:Assume in addition that you want the face value of the portfolio un-

changed, regardless of the strategy you take and that you can use the 1-year,5-year and 10-year bonds (recall that you have the data for the zeros) toimmunize your portfolio.

Report the system that you need to solve. You don’t need to solve it.

4 Problem 5

Merton (1973) suggests that the payo¤ of a limited liability company’s stockis akin to that of an option. For instance, consider a �rm with market valueV, and debt with face value K on date T. The value of the equity in the �rm,S(T ), at maturity of the debt, T, is the price of a hypothetical option on the�rm value.a) What type options is it? What is its payo¤ function?

b) Draw the payo¤ function ST (VT ) assuming that the strike price K,which in this case represents the value of the �rms’ debt, is equal to 8M

c) Consider the fundamental balance sheet identity. What type of optionsdoes the value of debt resembles? What is the payo¤ function of the bondB? Draw it. Comment on the economic meaning of the two pictures.

B = VT ¡ ST = VT ¡Max(VT ¡K; 0)=

½VT if VT < 66 if x > 6

10

The two pictures show that the equity payo¤ is similar to that of a calloption. It start to pay only after the debt has been fully repaid. On theother side, debt resembles short position in a put contract. If the value ofthe of the �rm is below those of debt, bond holders only get the value of the�rm. If it is higher than that of the bond, bond holders get the full principalback.

5 Other questions

5.1 Question

Provide a de�nition of yield to maturity and show how the de�nition thatyou provided applies to the case of a bond with 10 year maturity, semiannualpayment, coupon 9%, and 100 par value, that is traded at 93: 768 9.

Answer

It is the rate of discount the makes the present value of the future bondcash �ows equal to the price of the bond.Answer y is the solution to

93: 768 9 =20Xt=1

4:5(1+y=2)t

+ 100(1+:y=2)20

y=2 = :05y = 10%

5.2 Question

You have been hired by an investment bank. The CFO of your new clientcompany says that he has invented a bond with special characteristics thatwill make it very successful in the market. He wants to call it “The HappyNew Year Bond R°”. This bond has a par value of 100, the maturity is 50years. The bond is to be �oated on the �rst trading day of January 2008.The reason he thought about the name is that he wants the coupon paymentto be 5 dollars on July 1 of and 10 dollars on January 1 of each year. Assume

11

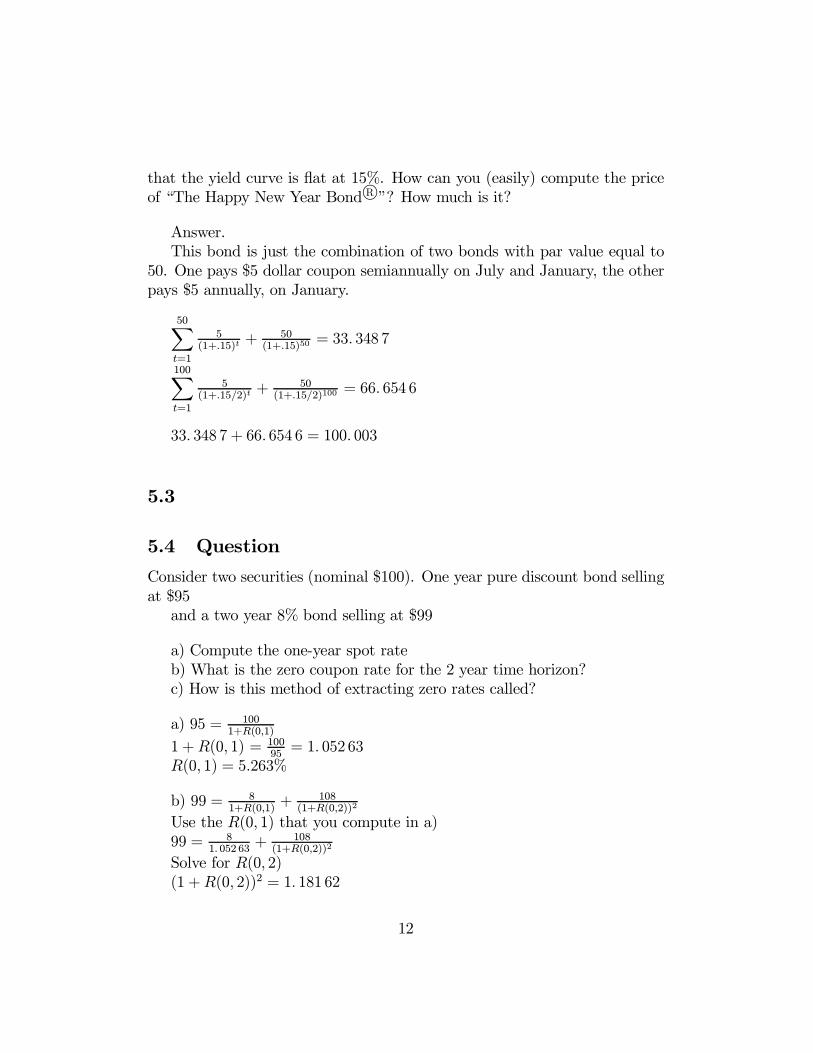

that the yield curve is �at at 15%. How can you (easily) compute the priceof “The Happy New Year Bond R°”? How much is it?

Answer.This bond is just the combination of two bonds with par value equal to

50. One pays $5 dollar coupon semiannually on July and January, the otherpays $5 annually, on January.

50Xt=1

5(1+:15)t

+ 50(1+:15)50

= 33: 348 7

100Xt=1

5(1+:15=2)t

+ 50(1+:15=2)100

= 66: 654 6

33: 348 7 + 66: 654 6 = 100: 003

5.3

5.4 Question

Consider two securities (nominal $100). One year pure discount bond sellingat $95and a two year 8% bond selling at $99

a) Compute the one-year spot rateb) What is the zero coupon rate for the 2 year time horizon?c) How is this method of extracting zero rates called?

a) 95 = 1001+R(0;1)

1 +R(0; 1) = 10095= 1: 052 63

R(0; 1) = 5:263%

b) 99 = 81+R(0;1)

+ 108(1+R(0;2))2

Use the R(0; 1) that you compute in a)99 = 8

1: 052 63+ 108

(1+R(0;2))2

Solve for R(0; 2)(1 +R(0; 2))2 = 1: 181 62

12

R(0; 2) = 1: 181 621=2 ¡ 1 = 8: 702 35%c) Bootstrapping

5.5 Question

Consider the following cubic spline with two splines

B(0; s) =

½B0(s) = d0 + c0s+ b0s

2 + a0s3 for s 2 [0; 3]

B10(s) = d10 + c10s+ b10s2 + a10s

3 for s 2 [3; 10]

a) Rewrite the spline eliminating the parameter d0 such that thespline is continuous at s = 3b) What other conditions do you need to impose to make this a suit-

able model for the yield curve? State these conditions formally, and explainwhat they are. You do not to actually solve for them.c) How many free parameters are left after you impose your condi-

tions?

Answer a).d0 = ¡ [c03 + b032 + a033] + d10 + c103 + b1032 + a1033

B(0; s) =

8<: B0(s) = ¡ [c03 + b032 + a033] + d10 + c103 + b1032 + a1033++c0s+ b0s

2 + a0s3 for s 2 [0; 3]

B10(s) = d10 + c10s+ b10s2 + a10s

3 for s 2 [3; 10]

b) B0(3) = B10(3); B00(3) = B010(3); B

"0(3) = B

"10(3); B0(0) = 1

c) 8¡ 4 = 4

13

5.6 Question

Assume that the you can borrow and lend at the following rates up to onemillion:

R(0,1) 5.5%R(0,2) 7%F(0,1,1) 8%Can you design a riskless strategy that earns you money?a) Describe the steps that you need to take to implement the strategy.

b) Compute your pro�ts0.005500 5,500.00

Long the 2-year and short the 1-year and the forward.

14