final expense training everest / world financial ...€¦ · final expense training everest / world...

TRANSCRIPT

Final Expense TrainingEverest / World Financial GroupEverest / World Financial Group

Golden Solution PlanGolden Solution PlanGo de So u oGo de So u o(Final Expense)(Final Expense)(Final Expense)(Final Expense)

Agent Use Only: Not for public distribution

G ld S l i FG ld S l i FGolden Solution FeaturesGolden Solution FeaturesIssue Ages 50-85 (Age Last)Issue Ages 50-85 (Age Last)3 Versions Depending on How Health Questions Are Answered1. Immediate Death Benefit – pays 100% of face amount immediately upon death

Maximum Coverage $35,000 (Issue Ages 50 – 75)Maximum Coverage $20,000 (Issue Ages 76 – 85)

2. Graded Death Benefit – pays 30% of Death Benefit if Death Occurs in 1st year, 70% in the 2nd year, 100% in the 3rd year and after. Pays 100% for accidental death.

Maximum Coverage $20,000 (All Ages)g ( g )3. Return of Premium Death Benefit:

• If Issue Age is Less Than 65, Pays Return of Premiums paid plus 10% Annual Interest if Death Occurs within the First 3 years (Thereafter 100% of Face Amount)*

• If Issue Age is 65 or Greater Pays Return of Premiums paid plus 10% Annual InterestIf Issue Age is 65 or Greater, Pays Return of Premiums paid plus 10% Annual Interest if Death Occurs within the First 2 years (Thereafter 100% of Face Amount)*Maximum Coverage $20,000 (All Ages)

• Pays 100% of Face Amount if Accidental Death

Agent Use Only: Not for public distribution

G ld n S l ti nG ld n S l ti nGolden Solution Golden Solution Determining EligibilityDetermining EligibilityDetermining EligibilityDetermining Eligibility

If th i “Y ” t ti b (1 3) th th li t i t li ibl fIf the answer is “Yes” to any question above (1-3), then the applicant is not eligible for coverage.

Agent Use Only: Not for public distribution

Golden SolutionGolden SolutionGolden SolutionGolden SolutionDetermining EligibilityDetermining EligibilityDetermining EligibilityDetermining Eligibility

If the answer is “Yes” to any question above (4-7), then the applicant is eligible for the ROP Death Benefit only.

Agent Use Only: Not for public distribution

G ld n S l ti nG ld n S l ti nGolden SolutionGolden SolutionDetermining EligibilityDetermining EligibilityDetermining EligibilityDetermining Eligibility

If the answer is “Yes” to the question above (8), then the applicant is eligible for the Graded Death Benefit.

Agent Use Only: Not for public distribution

G ld S l iG ld S l iGolden Solution Golden Solution Determining EligibilityDetermining EligibilityDetermining EligibilityDetermining Eligibility

If all the health questions on the application (1-8) are answered “No”, then the applicant should apply for the , pp pp y

Immediate Death Benefit.

Agent Use Only: Not for public distribution

G ld S l tiG ld S l tiGolden Solution Golden Solution Determining EligibilityDetermining EligibilityDetermining EligibilityDetermining Eligibility

If box is checked, there will not be an amendment due to a change of Death Benefit Plan.

Agent Use Only: Not for public distribution

G ld S l i RidG ld S l i RidGolden Solution RidersGolden Solution RidersGrandchild Rider (also covers Great Grandchildren)

Provides $5,000 (per unit) on each grandchild through age 20. Available in 1 or 2 units Convertible to an individual policy for up to $25,000 (Guarantee Insurability).$12 00 per grandchild per year / unit selected$12.00 per grandchild per year / unit selected.In the event of the Death of the Primary Insured, the coverage under this rider will be “Paid Up”.*

Nursing Home Waiver of Premium RiderNursing Home Waiver of Premium RiderWaives payment of policy premiums if confined in a nursing home for 90 consecutive days. Issue Ages 50-85Rider coverage duration is same as the base policyAvailable on the Immediate Death Benefit Plan only

• This Feature of this Rider is Available only on Immediate and Graded DB Plans (Rider Form # 9579);This Feature of this Rider is Available only on Immediate and Graded DB Plans (Rider Form # 9579); Not on the ROP DB Plan (Rider Form # 9581)

Agent Use Only: Not for public distribution

G ld S l i RidG ld S l i RidGolden Solution RidersGolden Solution RidersChildren’s Insurance Agreement*Childrens Insurance Agreement Accidental Death Benefit Rider*

No Cost Riders:No Cost Riders:Terminal Illness Accelerated Benefit Rider:

Can receive up to 100% of the death benefit when insured has a life f 12 h lexpectancy of 12 months or less.

Accelerated Benefits Rider - Confined Care**:• Full Time, Permanent Residence in Nursing Home• Fixed Monthly Pmt of 5.0% of face amount

* Not available with Return of Premium Plan

** Available only on the Immediate Death Benefit Plan Not available in: CA CT DC FL IL IN Available only on the Immediate Death Benefit Plan. Not available in: CA, CT, DC, FL, IL, IN, MA, NC, NJ, OH, SD, VA & VT)

Agent Use Only: Not for public distribution

Sales MaterialsSales MaterialsSales MaterialsSales Materialswww.everestfuneral.com/wfgwww.everestfuneral.com/wfg--ususwww.everestfuneral.com/wfgwww.everestfuneral.com/wfg usus

Application Agent Guide g“Eight Reason” Brochure Grandchild Rider Brochure Confined Care Rider BrochureConfined Care Rider Brochure Nursing Home WP Rider Brochure Quoting Sheets HIPAA Form And more…

Agent Use Only: Not for public distribution

Golden SolutionGolden SolutionGolden Solution Golden Solution UnderwritingUnderwriting

No medical exams or blood work required

UnderwritingUnderwritingApplicationMedical Information Bureau (MIB) Pharmacy Database CheckTelephone Interview (all sales except for ROP)

POS D i i A il bl (A i l)POS Decision Available (Apptical)Available in multiple languages

B ild ChBuild Chart Agent Use Only: Not for public distribution

Field UnderwritingField UnderwritingField UnderwritingField UnderwritingTools in Agent GuideTools in Agent GuideTools in Agent GuideTools in Agent Guide

Agent Use Only: Not for public distribution

Fi l E A t G idFi l E A t G idFinal Expense Agent GuideFinal Expense Agent GuideMedication ListingMedication Listing

• Common Use(s)• Common Use(s)

• Rx Fill Criteria (if applicable)• Rx Fill Criteria (if applicable)

Pl R d tiPl R d ti• Plan Recommendation• Plan Recommendation

Medication Common Uses RX Fill Within Plan Eligibility

Furosemide HypertensionCHF

N/AN/A

ImmediateReturn of Premium

14

Fi l E A t G idFi l E A t G idFinal Expense Agent GuideFinal Expense Agent GuideImpairment GuideImpairment Guide

• Criteria• Criteria

• Plan Recommendation• Plan Recommendation

• Indicates Question # on Application• Indicates Question # on ApplicationIndicates Question # on ApplicationIndicates Question # on Application

Condition/Concern Criteria Plan to

Apply ForQuestion on App

Congestive Have you ever been medically diagnosed Return ofgHeart Failure

(CHF)

Have you ever been medically diagnosed,treated, or taken medication for

Return of Premium 6

15

Final Expense Agent Guide: Build ChartFinal Expense Agent Guide: Build ChartFinal Expense Agent Guide: Build ChartFinal Expense Agent Guide: Build ChartMaximum Weight for Plan Minimum Weight for Plan

Ht. Immediate Graded ROP* Immediate ROP**4’10’ 211 212 ‐ 220 221 ‐ 230 92 87 ‐ 914 10 211 212 ‐ 220 221 ‐ 230 92 87 ‐ 914’11” 218 219 ‐ 228 229 ‐ 238 94 89 ‐ 935’ 225 226 ‐ 236 237 ‐ 246 96 91 ‐ 955’1” 233 234 ‐ 244 245 ‐ 254 99 94 ‐ 985’2” 241 242 ‐ 252 253 ‐ 262 101 96 ‐ 1005’3” 248 249 ‐ 260 261 ‐ 271 105 100 ‐ 1045’4” 256 257 ‐ 268 269 ‐ 280 107 102 ‐ 1065’5” 264 265 ‐ 276 277 ‐ 288 110 105 ‐ 1095’6” 273 274 ‐ 285 286 ‐ 297 112 107 ‐ 1115’7” 281 282 294 295 306 116 111 1155 7 281 282 ‐ 294 295 ‐ 306 116 111 ‐ 1155’8” 289 290 ‐ 303 304 ‐ 316 119 114 ‐ 1185’9” 298 299 ‐ 312 313 ‐ 325 123 118 ‐ 1225’10” 307 308 ‐ 321 322 ‐ 335 126 121 ‐ 1255’11” 315 316 ‐ 330 331 ‐ 344 131 126 ‐ 1303 5 3 33 33 344 3 36’ 324 325 ‐ 339 340 ‐ 354 135 130 ‐ 1346’1” 334 335 ‐ 349 350 ‐ 364 139 134 ‐ 1386’2” 343 344 ‐ 359 360 ‐ 374 142 137 ‐ 1416’3” 352 353 ‐ 368 369 ‐ 384 146 141 ‐ 1456’ ” 6 6 8 86’4” 361 362 ‐ 378 379 ‐ 394 149 144 ‐ 148

* Above the weight on the high end of this range is a decline**Below the weight on low end of this range is a decline

Telephone Intervie sTelephone Intervie sTelephone InterviewsTelephone Interviews

Telephone Interviews (2 Ways to Complete):1. Point of Sale (Preferred Method)Completed at Time of Application from Client’s HomeCompleted at Time of Application from Client s HomeAll Interviews are RecordedCall Vendor using Toll Free NumberId if Y lf C P d B i A li d f (G ldIdentify Yourself, Company, Product Being Applied for (Golden Solution)Applicant Completes the Rest of the Interview on their ownIndicate on Application that Interview has been completedResults of Interview Transmitted to Home Office electronically

Agent Use Only: Not for public distribution

Telephone Interviews (Con’t)Telephone Interviews (Con’t)Telephone Interviews (2 Ways to Complete):

2. After Point of SaleIndicate on Application that Interview has NOT been completed, and provide Applicant’s Phone #, and a “Best Time to Call”Vendor will contact Applicant to complete Interview or scheduleVendor will contact Applicant to complete Interview or schedule a time to complete Results of Interview Transmitted to Home Office electronically

Agent Use Only: Not for public distribution

Telephone Interviews Telephone Interviews –– AppticalAppticalDual purpose medications (4 main categories)◦ Congestive heart failure (CHF)

122 mm nl s d m di ti ns t tr t CHF b t th n ls b s d t tr t122 commonly used medications to treat CHF but they can also be used to treat Hypertension

◦ Chronic Obstructive Pulmonary Disease (COPD)13 l d di i h l b d h13 commonly used medications that can also be used to treat asthma

◦ Seizures12 commonly used medications that can be prescribed for another condition

◦ Parkinson’s Disease7 commonly used medications that can be prescribed for another condition

D i th i t i if f th di ti i id tifi d thDuring the interview if one of these medications is identified, the interviewer will ask a clarifying question:

• EX: The Rx provider returned a prescription for Furosemide or its other brand name or generic forms. “Was this prescribed for Congestive Heart Failure (CHF)?”

Agent Use Only: Not for public distribution

Golden SolutionGolden Solution –– UnderwritingUnderwritingRe-Writes on Same Insured:

Golden Solution Golden Solution –– UnderwritingUnderwriting

If a second application is written on the same individual (1) within 6 months of the first policy being issued or (2) which increases the face amount to the maximum allowable for that age, medical records will be ordered on that individual by the Underwriting Department.g p

Agent Use Only: Not for public distribution

What is the Problem?

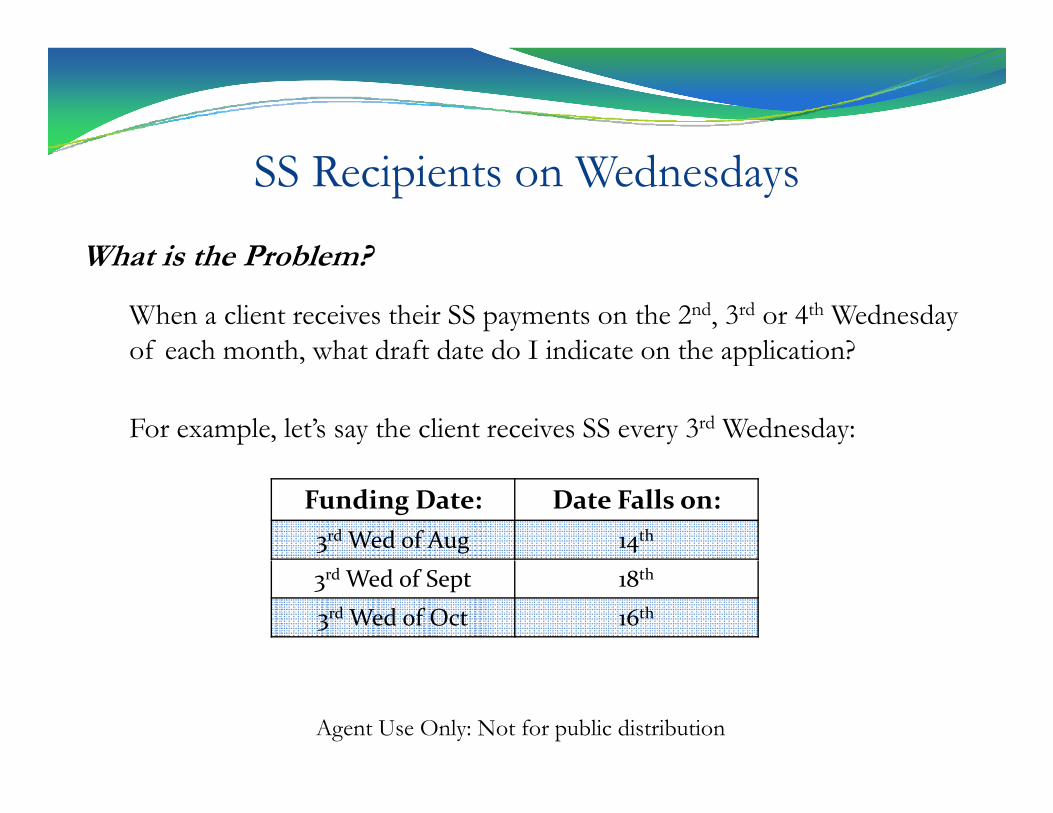

SS Recipients on Wednesdays

What is the Problem?

When a client receives their SS payments on the 2nd, 3rd or 4th Wednesday of each month what draft date do I indicate on the application?of each month, what draft date do I indicate on the application?

For example, let’s say the client receives SS every 3rd Wednesday:

Funding Date: Date Falls on:3rd Wed of Aug 14th

3rd Wed of Sept 18th

3rd Wed of Oct 16th

Agent Use Only: Not for public distribution

O S l i

SS Recipients on WednesdaysOur Solution:

Modify our system to collect on the 2nd, 3rd or 4th

W d d f h h i b iWednesday of the month on an on-going basis.◦ 1st Company with this capability

R d f NSF◦ Reduces occurrences of NSF◦ Instead of indicating a specific draft date on application;

simply indicate a draft day of “2W”, “3W” or “4W”◦ Immediate Drafts still optional

Agent Use Only: Not for public distribution

Family SolutionFamily SolutionyyPlanPlan

Agent Use Only: Not for public distribution

F il S l i Pl FF il S l i Pl FFamily Solution Plan FeaturesFamily Solution Plan Features2 Versions Depending on How Health Questions Are Answered2 Versions Depending on How Health Questions Are Answered

1. Immediate Death Benefit – pays 100% of face amount immediately upon deathupon death

Maximum Coverage: $35,000 (Issue Ages 0-49)

2 R f P i D h B fi2. Return of Premium Death Benefit:• Pays Return of Premiums paid plus 10% Annual Interest if

Death Occurs within the First 3 years (Thereafter 100% of Face Amount)Maximum Coverage $20,000 (Issue Ages 18-49)

• Pays 100% of Face Amount if Accidental DeathPays 100% of Face Amount if Accidental Death

Agent Use Only: Not for public distribution

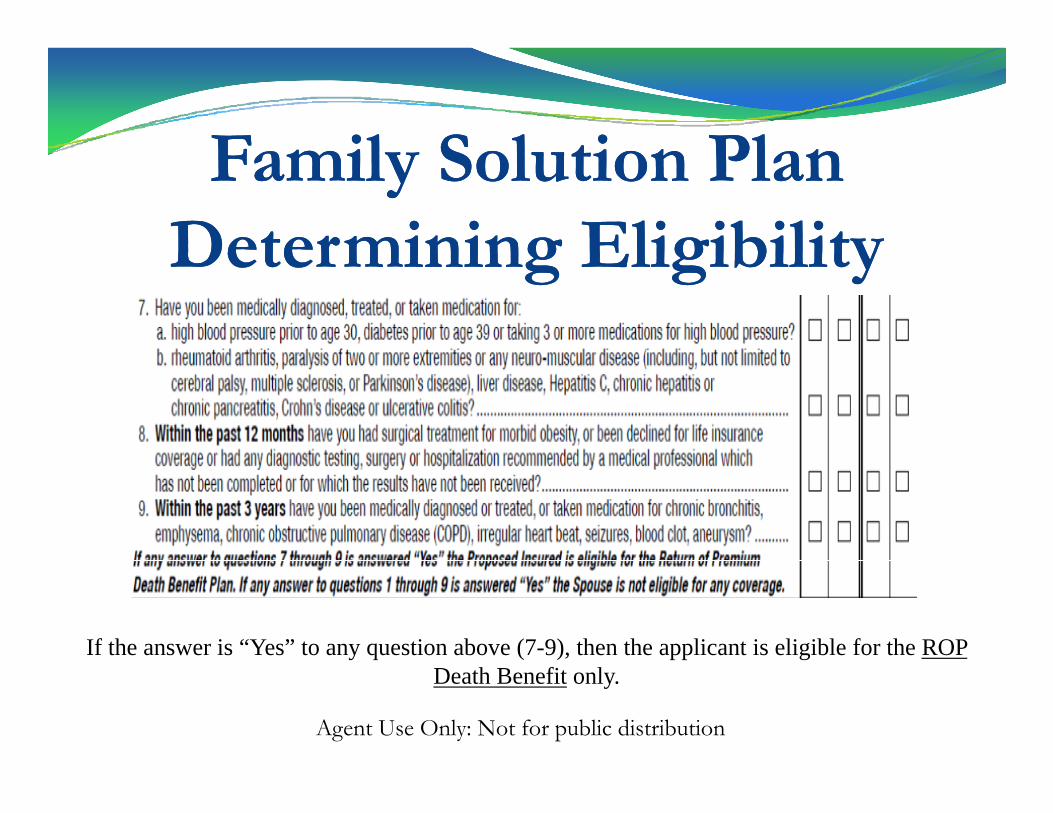

F il S l i PlF il S l i PlFamily Solution Plan Family Solution Plan Determining EligibilityDetermining EligibilityDetermining EligibilityDetermining Eligibility

If the answer is “Yes” to any question above (1-6), then the applicant is not eligible for coverage.

Agent Use Only: Not for public distribution

F mil S l ti n Pl nF mil S l ti n Pl nFamily Solution Plan Family Solution Plan Determining EligibilityDetermining EligibilityDetermining EligibilityDetermining Eligibility

If the answer is “Yes” to any question above (7-9), then the applicant is eligible for the ROP Death Benefit only.

Agent Use Only: Not for public distribution

F mil S l ti n Pl nF mil S l ti n Pl nFamily Solution Plan Family Solution Plan Determining EligibilityDetermining EligibilityDetermining EligibilityDetermining Eligibility

If all the health questions on the application (1-9) are answered “No”, then the applicant ( ) , pp

should apply for the Immediate Death Benefit.

Agent Use Only: Not for public distribution

F il S l i Pl RidF il S l i Pl RidFamily Solution Plan RidersFamily Solution Plan RidersChildren’s Insurance Agreement*Children s Insurance Agreement

Provides $3,000 per unit (max of 3 units) on children until age 25 or Primary Insured is age 65. Convertible at a rate of up to 5 times the CIA coverageConvertible at a rate of up to 5 times the CIA coverage. $8.50 per unit per year. Available from 15 days to 17 years old.

Spouse Term RiderProvides 20 year level term coverage on the spouse. Minimum - $5,000

* N t il bl ith R t f P i Pl

$ ,Maximum - $35,000 (not to exceed base face amount)Issue Ages 15 to 49. * Not available with Return of Premium Plan

Agent Use Only: Not for public distribution

F il S l i Pl RidF il S l i Pl RidFamily Solution Plan RidersFamily Solution Plan RidersAccidental Death Benefit Rider* Waiver of Premium Benefit*

No Cost Riders:Terminal Illness Accelerated Benefit RiderTerminal Illness Accelerated Benefit RiderAccelerated Benefits Rider - Confined Care**

* Not available with Return of Premium Plan

** Available only on the Immediate Death Benefit Plan. Not available in: CA CT DC FL IL IN MA NC NJ OH SD VA & VT)CA, CT, DC, FL, IL, IN, MA, NC, NJ, OH, SD, VA & VT)

Agent Use Only: Not for public distribution

Sales MaterialsSales MaterialsSales MaterialsSales Materialswww.everestfuneral.com/wfgwww.everestfuneral.com/wfg--ususwww.everestfuneral.com/wfgwww.everestfuneral.com/wfg usus

Application Agent Guide gConfined Care Rider Brochure Quoting Sheets HIPAA FormHIPAA Form Juvenile Questionnaire – required if issue age is 0 to 17A dAnd more…

Agent Use Only: Not for public distribution

F il S l ti PlF il S l ti PlFamily Solution PlanFamily Solution PlanUnderwritingUnderwriting

No medical exams or blood work required

UnderwritingUnderwritingApplication

Medical Information Bureau (MIB)

Ph D b Ch kPharmacy Database Check

Telephone Interview (ages 40-49)

Can be done Point-of-Sale (preferred)Can be done Point-of-Sale (preferred)

Available in multiple languages

Build Chart

Agent Use Only: Not for public distribution

Field UnderwritingField UnderwritingField UnderwritingField UnderwritingTools in Agent GuideTools in Agent GuideTools in Agent GuideTools in Agent Guide

Same Items as Golden SolutionMedication GuideImpairment GuidepBuild Chart

Customized for the Family PlanCustomized for the Family Plan

Agent Use Only: Not for public distribution

3rd Party Payors◦ We do not accept Family Choice applications when a 3rd Party

Payor is involved and the applicant is age 30 and over

3rd Party Payors

Payor is involved and the applicant is age 30 and over◦ Defined as a premium payor other than the primary insured,

the spouse, or a business or business partnerp p◦ Examples would include brothers, sisters, in-laws, parents,

grandparents, aunts, uncles, and cousins◦ The rule does not apply on Final Expense sales (ages 50-85);

it does apply to our other life products◦ Why do we have our 3rd Party Payor rule?◦ Why do we have our 3 Party Payor rule?◦ Anti-selection◦ Adverse claims experience◦ Poor persistency

Agent Use Only: Not for public distribution

Questions???Q