final pdf-maz

TRANSCRIPT

startupmagazinethe

Yourfunding options:

which is rightfor you?

Illustration inspired by the original work of Rudolph de Harak (April 10, 1924 – April 24, 2002)

Who made this issue?

Busin

ess,

but

not

as

you

know

it

Adam OskwarekAdam is a data-driven digital product developer and marketer; helping startups with Lean, UX and Growth Marketing. He’s on a mission to build better startups. @ACharles_writer

Adrian LloydAdrian is co-founder and Partner at Episode 1, a venture capital firm that focuses on early stage software companies. Adrian is a former management and strategic consultant for Marakon Associates, has an MBA from Stanford Business School and a Masters Degree in Chinese Studies from Oxford University. @AdsLloyd

Alexander GuyAlex is the Global Marketing Manager at Startupbootcamp and formerly worked for 3 years as the Product Marketing Manager at a cloud computing company. He also serves as the City Mayor for Entrepreneur Cafe, a global coffee meetup for startups and entrepreneurs. @alexanderguy19

Craig SniderCraig Snider is Head of Risk and Due Diligence at Crowd2Fund, an innovative platform that brings together investors and small businesses to facilitate investment using 5 different models spanning debt and equity funding. Before joining Crowd2Fund, Craig was central to the development of Funding Circle’s property lending policy, and worked in distressed asset management within the Royal Bank of Scotland’s Shipping team. @_snid

Duncan PetersFounder of eRipple, an online platform harnessing the power of technology to connect individuals to the mentors that will provide them the expertise they need to flourish. @eRippleApp @duncanpeters_

Frederick GroenkvistCo-Founder and Limited Partner of ChinaImportal.com, a Shanghai based information services company who provides startups and small businesses with an online system for managing sourcing and production in Asian countries.

Gary YantinGary is a solicitor and Managing Director of High Street Lawyer.

Mark EdwardsVice President and General Manager of Rocket Lawyer UK, a Google Venture backed cloud legal company that helps startups and small businesses with their legal issues. Prior to joining Rocket Lawyer in 2012, Mark led the UK business development team for LexisNexis, a global information and software provider, and was responsible for developing and launching new online products. Mark is a former user experience consultant, with a PhD in artificial intelligence.

Mike SouthonMike is a successful serial entrepreneur and best-selling business author. He co-founded his first company in the 1980s and then worked with seventeen others before co-authoring The Beermat Entrepreneur in 2002. Today, he speaks at events and provides mentoring for entrepreneurs. His specialist subjects are: entrepreneurship, sales, company growth, The Beatles, Sir Richard Branson and The Meaning of Life. @mikesouthon

Office of the publisher:The Startup MagazineInternational House1 Saint Katharine’s wayLondon E1W 1UN

Web: www.thestartupmag.com Letters to the editor: [email protected] and sponsorship: [email protected] services: [email protected]: @thestartupmag

issue 01 · May 2015 · City of Lon

don

FROM THE EDITOR Natasha Hussein

Welcome to the first premium edition of the Startup Magazine. In the making of this debut issue, the Startup Magazine team has taken a reflective look at where we have taken our readers in the past and where we would like to take them in the future. Since its inception in 2012, the Startup Magazine has been using its online presence to connect the startup community to the expert knowledge that facilitates innovation – covering topics including finance, law, personal development and startup culture, among many others. In the process, we have garnered a strong tribe of forward thinking readers united by an enthusiasm for creativity, technology and getting shit done.

Although our mission in 2015 remains the same, through our magazine for tablet and smartphone we will be bringing you a new way to enjoy the expertise of members from the community, including exclusive content unavailable elsewhere. Going forward, we also aspire to go deeper into startup clusters than any other publication. In addition to featuring products and the founders behind them, we want to tap into an even more diverse set of brains within the startup scene, including venture capitalists, growth hackers, data scientists and product managers among many others; showcasing the people that don’t just allow startups survive, but ensure they thrive.

Inside this issue you will learn about how to raise finance for your startup from Adrian Lloyd, a partner of VC firm Episode 1. Richard Phelps, the Accountable Executive for Entrepreneurs at Barclays, shares his outlook on the startup ecosystem, and Paul Lindley, Founder and CEO of Ella’s Kitchen, gives us an insight into the importance of a social mission and what it takes to build the largest baby food brand in the UK. Deputy Editor, Rio Hodges, analyses which regions around the world are the best for startups to succeed.

Thank you to those who have been with us over the years, helping us to get to this day and a warm welcome to our new readers. We hope that the Startup Magazine will be a tool that will help propel you forwards for many years to come.

issue 01 · May 2015 · City of Lon

don

IS YOUR TECH STARTUP INVESTABLE AND HOW DO YOU RAISE FINANCE?by Adrian Lloyd

In case you had not heard, venture capital fundraising is on the rise. In fact, it jumped 62% last year – partly due to record-breaking financing rounds by the likes of Uber, but also thanks to a rapidly growing appetite among investors for growth tech. In London, technology firms secured more than $1.4bn in venture capital financing during 2014, double the amount raised in 2013. How can you secure your slice of this apparent avalanche of money?

Venture capital investor Adrian Lloyd at Episode 1 Ventures is on hand to give you some helpful advice.

Busin

ess,

but

not

as

you

know

it ·

FIN

AN

CE

The truth is that, while there is undoubtedly an enormous volume of cash flooding into tech companies, this is no repeat of the dot com era. Only a small minority of the startups popping up everywhere from here to Hong Kong are able to raise venture capital. Crowdfunders may be unloading their money into curious ventures at high valuations, but the experienced money – the kind that will also help you grow your business – is harder to find.

Where do you start?

The first step is to establish what stage your company is at. Do you need investment to turn your idea into a business, or is your company up and running and generating revenue? This will determine the kind of investors you should be talking to; whether you are at seed stage – in which case angels (or friends and family) will help you get off the ground, build a team and develop a product and launch – or if you have already launched, in which case you will be closer to institutional funding.

As a firm, we operate between seed and series A. We support companies that can demonstrate some kind of customer traction, investing £0.25m to £1m in rounds of up to £2m in software businesses that have reached product/market fit in a massive, and usually global, market. The vast majority of companies that are backed by VCs do not become the huge success stories that hit the headlines. As investors, the odds are stacked against us so we have to focus on companies that have the potential to deliver very substantial rewards.

What do we look for?

First and foremost, we are looking for a world-class CEO and team. The individuals in the business are the single most important factor when determining the chance of success. We will want to meet a complementary leadership team that covers both the product and commercial sides of the business – an

entrepreneur that covers both would be even better, but this is extremely rare. We will want to review relevant past experience of the leadership and find that they are consistently successful. We also like them to be data-driven and show an ability to hire great people and delegate to them effectively. We will expect them to operate their business in a lean fashion, be able to listen and speak clearly and be able to quickly demonstrate that they have exceptional knowledge of the customer and the problem that they are solving. Yes, we expect a lot from our entrepreneurs, but if you were making 1 of 25 bets that this fund will make, so would you.

At minimum, we need to see referenceable users and a clear path to revenues plus a clear customer acquisition plan. At best, you will be generating early revenues of £5k to £50k/month and are executing on a clear and affordable customer acquisition strategy.

How big is your market?

All venture firms think alike – we want each exit to be a ‘fund returner’. Our fund is £40m, and we are likely to own 10 to 15% of an exiting company (we aim to start with 20% and get diluted over subsequent rounds, usually against our will), so a fund returner needs to exit for £266m to £400m. How do you exit for £400m? If your market is worth over £1bn and you have typically high software margins, this suggests a large enough global market to grow into a great sized business for Episode 1, but we use that only as a rule of thumb. Market size is a key consideration, so it is important that you are able to quantify this, as well as explain how you made your calculation.

We love SaaS!

We have a particular fondness for software-as-a-service (SaaS) businesses and other subscription models. These businesses are able to scale more easily and deliver very predictable revenues.

We also like businesses that are marketing-savvy, so if you can demonstrate an affinity with the needs of the media and know exactly which customer segments to target and the impact this can deliver your business, then this would be an additional motivation. As an example, we were extremely impressed by online estate agent eMoov’s ability to drive media coverage; this was an important consideration when we valued the company and backed the business.

No copycats please

The Samwer brothers have made a considerable fortune from replicating other businesses and rolling them out in smaller markets, but that is not our game. We also do not like products with no business model and no prospect of sales traction in the very near future (we know that means we would not have invested in Facebook and Twitter or Pinterest, but hey).

Preparation is key

We always advise companies to meet us early so that we can track their progress and gauge their ability to execute over time. Meet with investors before you need to raise finance as this will make it easier for them to make a decision. The last thing you want when you are running out of money is investors needing time to think through their decision. If you meet our criteria then there is no need to be shy. We may ask difficult questions and give you frank advice, but we have been entrepreneurs too and have had to raise money so we know how helpful this can be. If you can impress us with your presentation then in a few short weeks you may have all the money you need.

One last word of advice – do not sell yourself short and do not assume you need investment more than your investors need you. If you have a great business then make sure you get the best possible investors on the best possible terms.

issue 01 · May 2015 · City of Lon

don

FUNDING YOUR BUSINESS – CHOOSING AND ATTRACTING DEBT OR EQUITY INVESTORS

by Craig SniderIn an ideal world, every entrepreneur would start

off with the savings they need to get their business off the ground, or even better, every good business would be self-funding from the start. The reality, though, is that growing a business burns cash quickly – salaries, rents, product design and creation all cost money upfront, even if the long-term benefits justify the investment.

There is of course, no ‘one-size-fits-all’ style of funding for a growing business. Some businesses can be very inexpensive to operate in the early days – key staff may be willing to work unpaid for a period of time (if they are founders or have an ownership stake) and the business may be able to operate out of a home with just a PC and a couch to work on for a while. Alternatively, the business may require large-scale development, manufacturing, and all sorts of professional consultation to get it off the ground, which will necessitate a large upfront investment. As an entrepreneur, you will need to think objectively about what costs you are likely to incur, when you are likely to incur them, and when the business is likely to start generating cash – because unfortunately these do not often happen at the same time.

Choosing the right funding structure could be the single most defining decision you will make for the trajectory of your business. It may determine how long you are able to concentrate on building the business and how much you can invest on the product before profit and cash flow become a priority. It may also have an impact on how much of the business you own in the long run, who you work with and how big your customer base is – marketing and geographic reach often both require investment. It is very easy to get carried away in the excitement and potential that comes from starting a new business, but everyone has heard the expression about failing to plan, and laying out what your costs are likely to be can avoid a lot of unpleasant surprises.

Busin

ess,

but

not

as

you

know

it ·

FIN

AN

CE

When you decide you need to start looking for funding, remember that anyone providing cash to your business – be it a bank, a venture capitalist, or a partner – will be very likely to expect a return on the money they provide. You will need to factor this into your expectations in order to treat them fairly, because keeping them happy will improve your ability to access funds again in the future. If you are unsure whether the more appropriate route for your business is debt funding or equity funding, in simplest terms it comes down to whether or not your historic profits show that the business can cover debt repayments; in which case, you may be looking at debt financing. If they do not cover debt repayments, and you are asking investors to look to profits you intend to make, then you are likely to have more success obtaining equity funding.

Before you start thinking about raising funds, here are a few exercises you can do to get your business and yourself ready to have those tough conversations.

The ‘what’s in it for me’ response: think about what you have to show as proof of your ability to give investors or lenders a return on their money. For equity investment, this will generally be growth in the value of the business, and for debt this will mean being able to demonstrate your ability to cover the debt and interest payments.

The sceptic response: take a few moments and write down all the potential pitfalls, risks, and vulnerabilities of your business – the crunch points where it could potentially go wrong. This will feel really uncomfortable for an enthusiastic investor like yourself, but the more you beat up the concept, the better your proposition will be. Next, consider all of the strengths in your business that will counter each one. Some will be easy, and the others not so much – but when you have finished your list you will know where to focus your attention and it will be apparent to investors that you understand your challenges.

Knowing the figures: write out the next 12 months, and underneath each one, list out what your expenditures are likely to be for each of them. Some you may be able to juggle between months, and some might span multiple months (if so, divide them accordingly). For each month, give a worst-case scenario figure for income, and a best-case scenario of income. Tally it up at the bottom of the page, and without even trying you have created a cash flow forecast, which shows where you have got a deficit and where you are building cash. When a potential investor or the bank manager asks you for it, you may surprise yourself by confidently and calmly being able to give them your forecast figures, which will go a long way to building your credibility as a business.

issue 01 · May 2015 · City of Lon

don

FUNDING YOUR BUSINESS – SECURING LOAN FUNDING

by Craig SniderBorrowing money is always attractive to the

entrepreneur, because money today is particularly valuable for a growing business compared to tomorrow’s money. However, it is important to keep in mind that the debt investor’s profits are only the interest they receive, and they gain nothing from growth in the business. Because profits from lending money are reasonably modest – usually under 10% annually – they do not want to take a chance on losing their investment outright.

Busin

ess,

but

not

as

you

know

it ·

FIN

AN

CE

For that reason, the debt investor will look at what the business has achieved in the past to decide if you are likely to be able to repay in the future. As unfair as it may seem, past performance is considered to be the best indicator of future results, so as a rule of thumb, investors will look at net profits and compare it to the debt repayments to decide what the likelihood is of the business being able to afford the loan. If net profits (or more likely, earnings before interest, taxes, depreciation and amortisation (EBITDA) if you are familiar with the term) are less than one times the required annual repayments, investors will be likely to expect increased compensation in the form of higher interest costs. If a lender is asking you for pay-day loan-style interest payments, then you have to stop and wonder why lenders consider your business so risky, and perhaps there is a better way to raise funding.

Debt investment is also much more formula-based than equity investing – nearly every lender will have its ‘tick-box’ criteria. In some cases, it is not even a matter of being a healthy business, but being the right business to fit into a lender’s loan criteria, so do not take it personally if yours does not fit into a lender’s criteria. It can be as simple as a particular lender wanting to diversify their portfolio, and they may consider themselves

overexposed to businesses very similar to yours. Brokers can be helpful when it comes to knowing where your business fits, but be prepared to pay potentially substantial fees if you involve a broker; in many cases you may not even know you are paying them, as the broker may be paid by the lender, who will add the fees to your loan. Many brokers add little value, aside from completing the application forms on your behalf, so consider whether this is a service you need if cost is a concern.

If your business has been trading for less than two years, you will probably find it quite difficult to raise debt, as this is the cut-off for many of the biggest lenders. To address the need for funding with businesses who sit in the growth phase between startups raising equity and established businesses who qualify for debt, Crowd2Fund are currently trialling a new product, called the Revenue Loan. The minimum criteria is for the business to have been trading for at least six months and to be profitable, and rates start at 10% p/a.

There are a few things you can do to increase your chances of success when applying for a loan:

Consider the personal credit rating of the company directors – if one of the directors has a poor track record, this will often reflect on the credit score of a small business and could be a major hurdle to receiving funding. It could be worth asking directors to request a credit check before applying to weed out any errors, mistakes, or easy fixes that may be viewed as problematic by a lender. As part of this, make sure each director is registered on the voter’s roll (as ludicrous as it sounds, many lenders consider this part of their criteria).

If there is an aspect of your business that might cause problems, it is better to highlight it and explain to the lender than hide it. Underwriters by very nature will assume the worst, and if there is a good reason, for example, why two directors resigned last year or profits turned to losses, then send in an explanation along with your application. If nothing else, it may encourage them to reach out to you rather than giving you a ‘computer says no’ style response.

Do not be afraid to ask lenders if there is any part of your business that could make it challenging for them to lend to you. You may be surprised by how candid they may be about their criteria and the types of businesses they will lend to.

issue 01 · May 2015 · City of Lon

don

Busin

ess,

but

not

as

you

know

it ·

FIN

AN

CE

Startup funding is a white knuckle roller coaster. Can crowdfunding help?

by Adam Oskwarek Having an idea for a startup is like a

nagging itch at the back of your mind. It’s going to be a challenge to reach it, but sometimes you just have to find a way to scratch. It is well publicised that funding early- to mid-stage businesses is challenging; they are ultra high risk, full of assumptions and often only have limited real world validation.

A recent Nesta and Cambridge University report highlighted growth in UK alternative finance and crowdfunding from £267m in 2012 to a whopping forecasted £4.4bn by 2015; it’s now a viable option for many startups and businesses. Awareness from the crowd can also be a kickstart for early stage businesses.

There does not appear to be a ‘one-size-fits-all’ path, so choosing the right options for your business is an important consideration from the beginning.

Over recent years, startups and businesses have used crowdfunding options in parallel with their development stage; anything from small pre-seed and seed rounds all the way up to sizeable multi-million series A equivalents. That is quite some breadth for entrepreneurs

when raising funding.

This said, there can be a disconnect in the motivation between what the entrepreneur expects and what an investor requires to make a contribution.

After each milestone completion, there is a requirement (perhaps duty?) to provide a more solid story based on evidence, thereby justifying the valuation with data. At each round, the weight of validation associated with your startup increases. Investors will be looking to see how much quantifiable proof you have and increasing value created by each milestone. If you cannot demonstrate this, you are expecting too much from investors; it will likely be too high risk. Avoid this by making it easy for everyone to see your early stage hustle, and avoid being more noise.

With donation-based crowdfunding specifically, the obvious US-based players are great for market validation and creating buzz. However it is more about marketing and pre-orders (which can help to raise follow-on rounds) than the equity-based options. From a technology startup perspective, it is great for hardware businesses with physical products, but not really that useful for other use cases – investors making a bet on you want skin in the game (Oculus Rift, anyone?).

Advice

Have a look at successful crowdfunding campaigns, see who has funded and the story behind that successful campaign, plus what stage they were at. The following advice will also help:

Bring your own audience – you are probably going to need 30–40% funding before the crowd will engage. If you already have customers, then giving them the first opportunity to invest is often a nice touch. Alternatively, bringing your offline investors to your online campaign is a necessity.

Be realistic about the funding you will need to hit the next solid milestone – burning out before your next milestone will make it harder to raise in future.

Be sensible with your market sizing and consider the actual addressable market within your sector (this will give more justification and credibility than ‘x% of £€$20bn please!’)

Bootstrap until you can support a decent story about why there is a market. Investors want to see you believe enough to put your money in to get the wheels moving. Plus very few startups hit their crowdfunding goal without some early validation or traction (and the ones that do generally just raise pre/early seed amounts that will not provide much runway).

Do not be a single founder – you will need a team to execute.

When you have the luxury, follow the smart money – networks are invaluable and risk reducing.

Be realistic with equity valuations – if you are at the early stage, do not ask investors to shoulder your risk without appropriate upside potential. At mid-stage, this is less pertinent an issue if the story and growth curve look good.

Be good to your crowdfunding investors – if you deliver what you said you would, they will likely support you through further rounds.

Choose your crowdfunding platform carefully – is their investor base big enough as well as relevant for your business? Will they ‘get it’?

Create a joined-up, cross-channel campaign – as with most things you need to be creative about how you market your crowdfunding. Like your startup idea – if you build it, they probably

issue 01 · May 2015 · City of Lon

don

won’t just come and hand over their hard earned cash.

Bear in mind when raising at early- to mid-stage (wherever it comes from) how the equity sacrifice and dilution will impact or add complexity to future rounds you might wish to undertake.

Crowdfunding can also be complementary when combined with other sources of funding – there are some great examples out there where campaigns were partially funded by an institutional player and closed by the crowd.

As a (perhaps obvious) side note: it is preferable to reach the break even point as soon as possible, reinvest earnings and use raised funds to scale while accelerating growth – being conscious of not trying to scale before you are able to capitalise on that effort. This will increase value created, drive valuation and improve investor (of whatever kind) sentiment for the next round – more exponential value creation than you can shake a stick at.

These are, of course, all opinions based on experience with crowdfunding over the last few years as it has grown to be a player in the ecosystem. From an investor standpoint – despite tax incentives – there probably have not been enough further rounds/exits, in particular in the equity space, to judge the return to risk ratio crowdfunding plays for them and their portfolios. That said, it is still a great way to get exposure to early-stage businesses, even if it can be a bit of a gamble.

Entrepreneurs should consider what type of investors are most valuable at each stage and whether the crowd is a suitable place to finance all or part of their next round. For high potential growth, truly disruptive ideas, it is about the right money, not just any money; the crowd is now big and active enough to help you get there, if the deal – as well as the story – is right.

It will be bumpy, so enjoy the ride.

THE UNDERDOG MYTH: COMPARING ENTREPRENEURIAL ENVIRONMENTS AROUND THE WORLD

by Rio HodgesPopularised by success stories born out of

New York and San Francisco, the US seems to be where startup dreams are made. With more foreign entrepreneurs flocking to the States every year, the US certainly seems like the go-to destination for the ambitious and daring. It is however, far from an exclusive club. In fact, European cities have dramatically expanded their repertoire to include and accelerate some very exciting startups. London’s Silicon Roundabout and Berlin’s Silicon Allee highlight this very phenomenon.

What is then the difference between Silicon Valley and its European counterparts? Does Europe simply lag behind the United States in every way? What about other countries and areas?

Busin

ess,

but

not

as

you

know

it ·

CU

LTU

RE

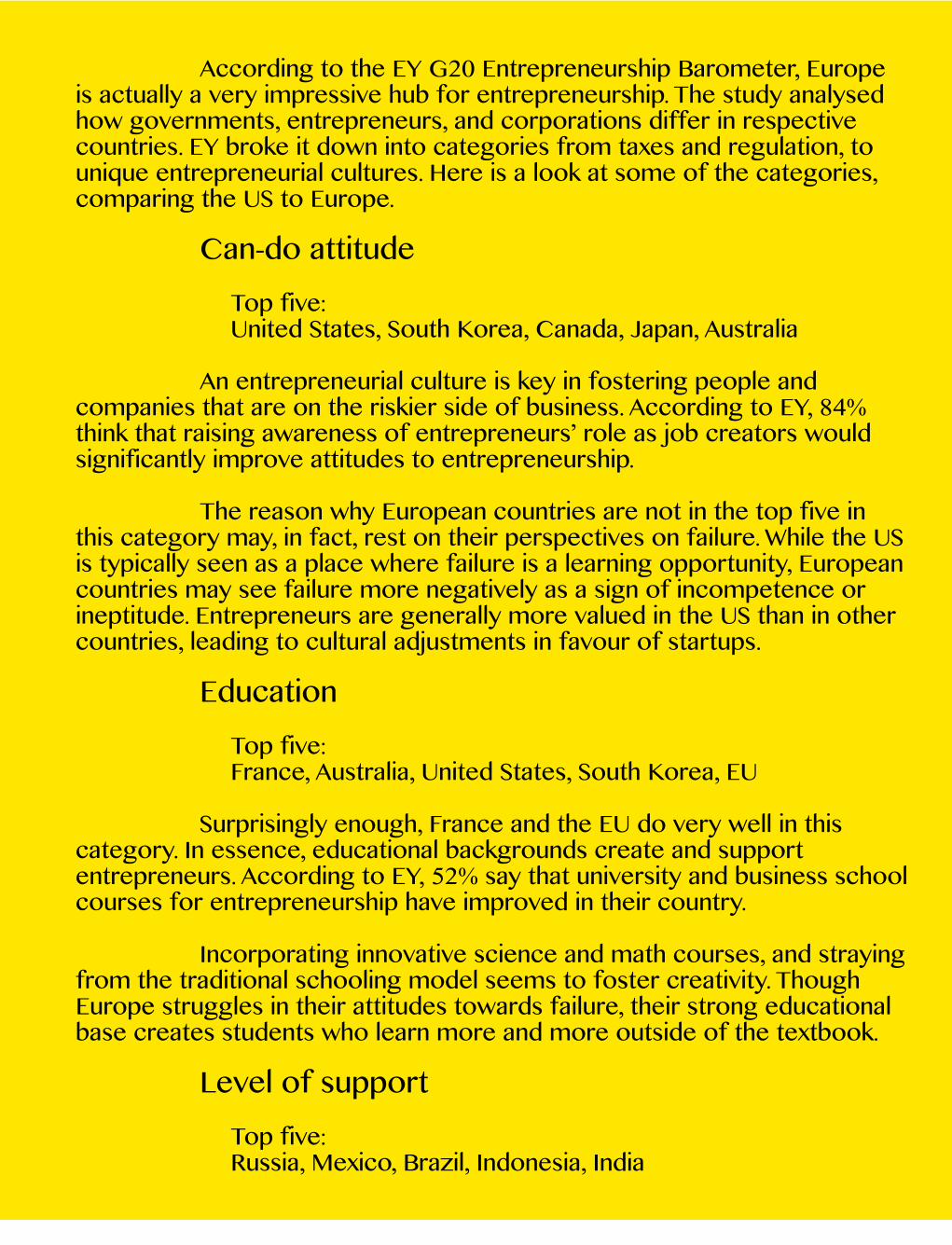

According to the EY G20 Entrepreneurship Barometer, Europe is actually a very impressive hub for entrepreneurship. The study analysed how governments, entrepreneurs, and corporations differ in respective countries. EY broke it down into categories from taxes and regulation, to unique entrepreneurial cultures. Here is a look at some of the categories, comparing the US to Europe.

Can-do attitude Top five:United States, South Korea, Canada, Japan, Australia

An entrepreneurial culture is key in fostering people and companies that are on the riskier side of business. According to EY, 84% think that raising awareness of entrepreneurs’ role as job creators would significantly improve attitudes to entrepreneurship.

The reason why European countries are not in the top five in this category may, in fact, rest on their perspectives on failure. While the US is typically seen as a place where failure is a learning opportunity, European countries may see failure more negatively as a sign of incompetence or ineptitude. Entrepreneurs are generally more valued in the US than in other countries, leading to cultural adjustments in favour of startups.

EducationTop five:France, Australia, United States, South Korea, EU

Surprisingly enough, France and the EU do very well in this category. In essence, educational backgrounds create and support entrepreneurs. According to EY, 52% say that university and business school courses for entrepreneurship have improved in their country.

Incorporating innovative science and math courses, and straying from the traditional schooling model seems to foster creativity. Though Europe struggles in their attitudes towards failure, their strong educational base creates students who learn more and more outside of the textbook.

Level of supportTop five: Russia, Mexico, Brazil, Indonesia, India

Here is the biggest surprise from the EY report. The highest levels of support for novel enterprise comes from a lot of the BRIC countries rather than the G7. It seems simple to assume that more developed countries would have the resources to support startups, but this underestimates the ability of the BRIC countries to be startup-friendly environments.

Countries like Russia have been extremely effective at creating coordinated environments to accelerate startups. Bringing government institutions, non-profits, investors, and entrepreneurs closely together is something that the G7 countries do more independently. The projects that are coordinated by the national governments of some of the BRIC countries seems to be a more effective way to boost innovation.

Though the US ranks in the upper quartile of the EY report on the G20 countries, it is far from alone. The UK, Australia, South Korea, and Canada also rank among the top of the pack. These specific categories, detailing how well certain countries do to foster entrepreneurship, show some surprising results.

But how can countries like the UK move up in the rankings and compete with the bold and risk-taking US?

With respect to venture capital funding, European countries have a gap that must be filled. Though there are plenty of top tier VC firms, the UK and Europe lack lower level funding for startups. According to the EY study, only 15% of entrepreneurs say their country has a culture that supports startups. By increasing the number of VC firms offering smaller investment packages, entrepreneurs can be supported at specifically tailored financial levels to try and kick start their ideas.

Besides financial encouragement, Europe needs to foster a learning environment for budding startups. Mentors are the key source of knowledge and encouragement at early stages of small businesses. A study by the Enterprise Partnership found that 70% of businesses who have mentors survive five years or longer. That’s a lifetime in the startup world.

The rest of the world is not necessarily playing catch up with the US. However, that does not mean there is not work to do. The ‘can-do’ attitude of Silicon Valley can be replicated. It is a matter of encouragement and support from all levels, giving new ideas the chance to become big businesses.

issue 01 · May 2015 · City of Lon

don

Under the hood with Startupbootcamp: Choosingthe right

acceleratorby Alexander Guy

With the first few months of the year already behind us, startups have ditched their excess holiday weight and are running full speed into 2015. This means a fresh cocktail of pitch competitions, MVPs and all-nighters. For many, this also is the time of the year to consider joining an accelerator.

Popularised in the proverbial Silicon Valley tech melting pot, accelerators have become a mainstay in startup ecosystems all over the world. As caretakers of talented mentors, investors with full wallets and vital press contacts, accelerators have proliferated to virtually every corner of the globe. Early-stage startups looking for an accelerator are often spoiled for choice.

Busin

ess,

but

not

as

you

know

it ·

CU

LTU

RE

How can you tell an accelerator that will give you the kick start you need from one that will silently slink away with a slice of equity in the dead of night?

I cannot stress enough of the importance of doing your homework before you even think about spending your next three to six months entrenched in an accelerator’s community. I am hardly the first person to emphasise how vital research is in your accelerator decision process. The Global Accelerator Network have also written about accelerator match-making.

There are several key aspects to ensure you are headed in the right direction as you look into which accelerator is right for your startup.

Have a clear idea of your desired resultAccelerators are powerful resources that can provide

the skills, connections and momentum to grow successfully. To really take advantage of all an accelerator can offer, startups should have a good idea going into a programme of what they want to get out of their next few months. Are you looking for seed funding? Do you want to meet potential partners? Is raising your public profile in a specific community important? Knowing your desired output can help refine the list of accelerators that fit with your startup’s goals and vision.

Know your industryAlthough all kinds of feedback and coaching is

undoubtedly valuable, many accelerators tailor their curriculum to specific industries and stockpile relevant experts as mentors. This provides a targeted and specific approach that can greatly impact your startup’s success. Wouldn’t it be great

to learn from a group of financial allstars if you are a mobile payment startup?

Industry-focused accelerators are also often connected with major brands and companies in their field, forging important relationships that extend beyond the walls of your co-working space.

Build a relationship first Most accelerators offer a combination of open days,

pitch events, conference speaking sessions or office hours. Make sure you try to attend some of these and begin building a relationship early in the process. This is an often overlooked piece of the equation because it is not seen as essential to being accepted into an accelerator.

Your startup could very well get into a program and have a fulfilling few months without ever participating in an accelerator’s hackathon, but getting accepted is just a piece of a larger question. Startups should take the time to make sure an accelerator’s culture, activity and energy matches their own. At Startupbootcamp, we incorporate relationship building as a fundamental element of our recruitment process. Getting face time with an accelerator is not difficult – make it a priority to get to know the organisation before you apply.

One final thought…Set realistic expectations for your accelerator

experience. No matter which one you choose, it will be a three to six month caffeine-fuelled crash course. Taking the time to choose which accelerator is best for you will make all the difference.

issue 01 · May 2015 · City of Lon

don

Darwin’s theory of startups

by Yoav Farbey

Darwin’s finches are a set of different bird species, approximately 15 different groups of birds. All of these birds were found and studied by Charles Darwin on the Galapagos Islands.

To briefly summarise the theory of Darwin’s finches; Darwin hypothesised evolution; that the different species of Galapagos finches descended from mainland finches that had reached the islands sometime in the past. Over time they evolved and gradual changes occurred to the island finches. Eventually they were different enough from the mainland finches to be

Busin

ess,

but

not

as

you

know

it ·

CU

LTU

RE

considered a new species. Darwin proposed the island had become inhabited by many different but related species of finches.

How does all of this biological science relate a startup company?

Startup companies, especially technology startups, share similar patterns to those proposed in Darwin’s evolution theory. Businesses can be grouped in to sets (species), revolving around solving one problem. For example, businesses that evolve around email may have one set of businesses who are the email inbox providers such as Gmail, Hotmail, or Yahoo! Mail. The second set of businesses could be email clients, which includes Sparrow, Thunderbird and Outlook, the list can go on.

Looking at Twitter and its API as an example of comparing Darwin’s finches, modern businesses and startup companies, there are many different types of startups that have evolved from Twitter’s API.

Startup companies like Hootsuite and Tweetdeck for scheduling tweets, and Bit.ly for shortening URLs so they can fit in a tweet. All of these startups have different interfaces, functionalities and use-cases, however they all originate from Twitter, and function around Twitter, through harnessing Twitter’s API.

This comparison can be applied to any cluster of companies, not necessarily just technology startups.

What can a startup company take from this?

If you are building a business that has evolved from a similar product or service, you need to define what value you bring when using your product or service. Using the Twitter example, with Tweetdeck tweets can be scheduled, without the necessity to be logged in to Twitter when the tweet is published.

When starting a business, or running a startup, you need to be aware of your market, and understand that there are other companies similar to yours. What you should do is study your competitors and find what defines you as the successful business in your market.

I have demonstrated that there are some similarities between Darwin’s evolution theory and 21st century startup companies. It is now for you to distinguish your company in your market, and succeed.

issue 01 · May 2015 · City of Lon

don

THE STARTUP GUIDE TO NON-DISCLOSURE AGREEMENTS AND CONFIDENTIALITY

by Mark EdwardsIt is the one document that could

have changed Facebook history as we know it – the non-disclosure agreement (NDA), also known as a confidentiality agreement. Had such a document been produced by the Winklevoss brothers while Mark Zuckerberg was lending his skills to their website, the face of social networking could be very different today. Of course this is an infamous case, but it still has the utmost relevance for businesses across the UK today who are constantly creating and sharing ideas and information.

Busin

ess,

but

not

as

you

know

it ·

LAW

What is an NDA?

An NDA is a legally binding document that is the first step to protecting your ideas and intellectual property when sharing valuable and confidential information with others (individuals and businesses). It is the easiest and most common way of ensuring that this information is not compromised, made public or exploited in any way. It also means that in the eventuality of any breach of contract, you can take legal action to implement any solution needed to rectify or prevent further breaches and recover damages.

Why do you need an NDA?

You may have a brilliant business or creative idea along with the strategy on how it will be brought to market or implemented; you may also have important business plans, marketing information or financials and statistics that are at the crux of your business. At some point you will need to share some of this information with others to help further the growth of your company – be they internal employees or external consultants and contractors – but you do not want such valuable information to be made public or fall into the wrong hands. An NDA will allow you to discuss this confidential information openly with those you choose without fear of it later being misused or shared without your authorisation.

Which type of NDA do you need?

If only you are sharing information, use a one-way confidentiality agreement to protect your intellectual property. This should cover the terms under which the confidential information can be used, who is allowed to receive the information, the restrictions placed on it to maintain its confidentiality, as well as remedies and damages should there be a breach of contract.

If both parties are exchanging sensitive information, use a mutual confidentiality agreement that covers all the above,

but also ensures that both parties are fully protected. An NDA like this allows you to get to know each other better so you can decide whether to enter into a longer-term deal or partnership.

When you first start sharing information, or if you frequently do so, and quickly need to agree an NDA to protect your information, use a letter of confidentiality. This document provides the same level of protection but is ideal for less formal situations or when time is of the essence.

Where do you go to create a NDA?

It is important that you have confidence in your confidentiality agreement and that it has been properly drafted – if not, you are putting your business at risk. Always create a tailored agreement to fit the specific needs of your business, that way you ensure all aspects of your confidential information is protected, leaving nothing to chance. Plus, it does not need to be complicated, time-consuming or expensive, which are the most common reasons cited for not creating such a simple legal document.

A legal service such as Rocket Lawyer, who provide startups and small businesses with easy-to-create legal documents online and help from affordable specialist lawyers, allows you to create your own bespoke NDA (from a template that has been drafted by a lawyer) via an online interview process, in your own time and in as little as 10 minutes. Plus, take advantage of their free trial and you can even create the agreement and consult an On Call lawyer for free.

Drafted carefully and dutifully signed off by the relevant parties, the NDA is the first and single most effective legal document there is to protect the interests of your startup or small business. Protect it before you share it.

issue 01 · May 2015 · City of Lon

don

PATENTS AND INTELLECTUAL PROPERTY FOR STARTUPS

by Dominic HigginsAn invention with great

commercial potential; a catchy business name; artworks and innovative designs. Intellectual property is the most important asset of many startups. Failing to protect it legally could result in your business being ruined if someone steals your idea. Here is a summary of the main forms of intellectual property protection in the UK.

Patents

Patents protect inventions. To be eligible for a patent, the idea must be genuinely inventive and capable of industrial application. You apply for a patent to the UK Intellectual Property Office or the European Patents Office (which gives protection throughout the EU). Unfortunately, the application

Busin

ess,

but

not

as

you

know

it ·

CU

LTU

RE

process is very slow and can take two to four years in the UK and even longer for an EU patent. Once a patent is granted you have the exclusive right to produce and sell the invention for 20 years. You can sell, license or even mortgage your patent.

Designs

A registered design relates to the visual appearance of a product. Designs can be registered for objects as well as two-dimensional items, such as patterns and graphic symbols. To register a design it must be new and have ‘individual character’. Applications can be made via the UK Intellectual Property Office or the European Trademarks and Design Registry and, once granted, give you monopoly rights over the use of the design for 25 years (subject to renewal every five years).

Copyright

Copyright protects original creative works like writing, songs, photos, graphics and source code. Owners of copyright can prevent others using their work without permission. You do not need to apply for copyright as it is automatically assigned to the creator of the work (or their employer if created in the course of employment). However, to enforce your copyright you need to prove that you were the first to have the idea. There is no guaranteed effective way to prove copyright, but examples include using copies of web pages saved by Google cache or the web archive, or asking a solicitor to keep a record of the date the work was created.

Trademarks

Trademarks exist to prevent other businesses ‘piggybacking’ on your brand to poach customers or damage your reputation. Representations of a brand including the name, slogans, jingles and logos can be protected under the Trademarks Act 1994. Trademarks can be applied for from the UK Intellectual Property Office and you can protect your brand at a European Level through the Community Trademark. You can prevent other businesses using something resembling your trademark to sell similar goods and services if this would be likely to confuse the public into thinking they were you. It is important to remember that the trademark and website domain name registration processes are separate; registering a trademark does not give you the right to the domain names containing your brand name.

Intellectual property is one of the most important legal issues for startups. If your business has significant intellectual assets, it is advisable to take advice from a specialist solicitor to ensure these are effectively protected.

issue 01 · May 2015 · City of Lon

don

LEGAL INSIGHT: THE IMPORTANCE OF GOOD NON-DISCLOSURE AGREEMENTS

by Gary Yantin

Anyone who has seen the film ‘The Social Network’ about the creation of Facebook will appreciate the importance of guarding a good secret and ascertaining where the idea originated. Billions of pounds can be at stake by not properly protecting the sacred information of your business. Just look at the Apple versus Samsung litigation to see the effect.

What if you have you got a business idea that you need to discuss with other people? You may need to take soundings on the viability of your idea or start talking to potential backers. However, as paranoia seeps in that those you want to collaborate with may steal your amazing idea, your desire to communicate

Busin

ess,

but

not

as

you

know

it ·

LAW

with them diminishes.

What can you do to ensure that you achieve maximum advantage from partnering with others without losing your shirt?

There are various pros and cons to asking potential partners to sign a non-disclosure agreement (NDA). Which form to use and whether to use one at all will depend on many factors.

If you are passing sensitive or confidential data to someone for review purposes or for them to assess whether a business relationship should be pursued a simple NDA is all that is required. The main element of the NDA is to put the receiving party on notice that the information that they will receive is regarded as commercially sensitive. The agreement will stipulate who the information can be shared with; such as accountants and lawyers, how it should be stored and what should happen if the relationship does not proceed. Where most data is shared electronically, consider how likely it will be that the receiving party can properly protect your sensitive data and destroy it when the relationship is not to be pursued.

If the other party is also going to be sharing their information with you, a mutual NDA will be best so that both parties are subject to the same obligations. This may not be as strong as a one-sided NDA, but it shows the other party that you can also abide by promises of confidentiality.

Very few ideas are entirely new and elements of your idea may already be known to the recipient or in the public domain. The NDA should clarify whether it covers sensitive information about your idea that the recipient may have seen elsewhere. They will not want to be responsible for keeping secret something that is already widely known.

Experienced investors, angel networks and private equity houses receive hundreds of pitches, many of which have

a similar theme and possibly similarities with ideas that they may be developing themselves, especially if they are already in your sector. Their ability to protect your information and keep it separate – physically and theoretically – from other ideas that they have seen is often impaired. Many such investors will not agree to be bound by NDAs for this reason. A confidentiality notice or an undertaking in correspondence may be the best you will get. Whether you want to share information with a party that does not want to sign your NDA will be a delicate balance of how useful they may be to moving your idea to the next level. Of course, the more your idea is shared the harder it gets to keep it a secret.

You should always:

Keep good records of everyone who has seen your sensitive data.

Keep a record of who has signed the NDA and whether they made any changes to it before signing it.

Number all documents that you send out to keep track of the data flying around.

Ask that any documents are returned to you if the matter does not proceed.

An NDA is a contract between two parties and is enforceable provided it is proportionate to the type of information being shared. Imposing huge sanctions on a receiving party for breaching the agreement are unlikely to be upheld.

Drafting a NDA does not have to cost a fortune and a good template or precedent can be easily modified for different scenarios.

Ultimately, the purpose of the NDA is to notify the other party that you are serious, that you care about what you are sending them and that it has commercial value. Whether your idea is a success will have to rely on a whole host of other factors.

issue 01 · May 2015 · City of Lon

don

DOES A STARTUP NEED A LAWYER

by Yoav Farbey It is possible to take a DIY

approach when dealing with the legal issues that arise when setting up a business. Entrepreneurs should tread carefully though – both in terms of identifying all the areas that need to be considered and in making sure the position of the business is safeguarded.

Busin

ess,

but

not

as

you

know

it ·

LAW

Are small business owners keen to call the lawyer?

Does ‘lawyering up’ offer genuine value for money for a startup or is it an expensive luxury? As with all professional services, this depends on the specific work that needs doing and whether the business has the resources, expertise (and time) to deal with those issues in-house.

Research suggests reluctance on the part of small businesses to turn automatically to solicitors when a legal issue arises. A report from the Legal Services Board and YouGov showed that only 8% of the 9,703 small businesses surveyed had contractual retainers in place with law firms; suggesting the type of arrangement whereby businesses put all legal matters in the hands of a lawyer as a matter of course is relatively rare. The same research also showed more than half of respondents opted to deal with legal problems without outside help. Only 13% thought lawyers offer a cost-effective way to resolve legal issues.

Resolving routine problems (e.g. credit disputes with other businesses, employee relations and compliance) is one thing. At the seed stage, however, a number of specific and complex matters can arise. Trying to deal with these particular issues without expert input can be potentially very problematic.

Setting up an appropriate structure

The larger the number of people involved, the greater the need for clarity when it comes to defining the rights and obligations of each of the parties. For many businesses, setting up a limited company is the most appropriate way forward (not least, as a way of limiting the personal liability of the company owners). The formation of a new company is generally a relatively pain-free (and potentially, lawyer-free) process, thanks to the Companies House Web Incorporation Service. The shareholders’ agreement though, is often less straightforward. Will there be majority and minority shareholders? How will their relationship be regulated? What is the exit strategy? Are third-party investors involved in the business? Who will represent their interests on the board?

Where there are only close friends or family involved, the temptation may be to reject the idea of professionally drafted arrangements. Beware though: even the closest relationship can be tested under the strain of keeping a fledgling business afloat.

Protecting your ideas

An online trademark search through the UK Intellectual Property Office

is an easy and effective way of reducing the risk of inadvertent infringement with your proposed business or product name

Whereas checking you are not stepping on anyone else’s toes is something you may feel comfortable about doing without legal help, safeguarding your own innovations may be a different story. The protection of designs, inventions and brand ought to be a primary concern from day one. As a recent report from the Intellectual Property Office reminds us, the value of intellectual property (IP) is all too often overlooked by small and medium-sized enterprises (SMEs). The same report showed IP protection could give a business a marked competitive advantage when seeking equity investment. Why take any risks with what is potentially your company’s most valuable asset?

Building a team

Taking on an employee is a big milestone for any startup. The idea of rejecting lawyer-drafted bespoke employment contracts in favour of suitably tweaked standard templates will appeal to many small businesses. Take care to ensure the contract defines your desired employee/employer relationship accurately – and remember that merely lifting a template from the web and putting your company name at the top can increase the scope for disputes further down the line. Special care should be taken with senior and highly skilled employees – especially if you wish to impose non-competition clauses. Imprecise, irrelevant or overly harsh terms will be deemed unenforceable.

Striking a balance

There are, in fact, many solicitors’ firms who offer services geared squarely at SMEs – and startups in particular, which is far removed from the stereotypical image of unscrupulous lawyers fleecing small businesses with high fees for routine work. Technology plays its part, with solicitors making available to their clients a host of templates, how-to guides and other resources. The emphasis is on arming clients with the knowledge to do as much as possible themselves – with the fall back of being able to call on their help when needed.

It is potentially the best of both worlds: the reassurance of being able to call on assistance from lawyers covered by professional indemnity insurance for solicitors – along with just the right amount of guidance for up-and-coming businesses to do what they can, when they can.

issue 01 · May 2015 · City of Lon

don

MENTORSHIP I N S I G H T SY O U R G R O W T H I N 2 0 1 5

by Mike Southon

Now the recession seems to be behind us, I am sure many of you have ambitious plans for growth in 2015. If so, this is the time to start expanding your network of mentors.

I often say that the primary success factor for any entrepreneur is their ability to find and retain good mentors; people who are happy to give them the advice they need, for free.

Success is not about the merits of your idea. I have never ever heard a completely unfeasible elevator pitch, though some of the pitches did assume that the elevator got stuck for a couple of hours!

Business is all about execution, about doing simple things well. Hence, the need for people who can give you good quality free input on the merits of your ideas, and even introductions to potential first customers. After that, it is down to you to make your business work and to move through a number of simple and well-understood growth phases.

by Mike Southon

Busin

ess,

but

not

as

you

know

it ·

MEN

TORS

HIP

INSI

GH

TS

I still use the model that Chris West and I developed in The Beermat Entrepreneur. A large number of people (about 50% of the population) have an aspiration to start a business, perhaps initially in parallel with their regular employment.

I now call these people ‘Apprentice Entrepreneurs’, characterised as being ‘pre-revenue’. As soon as someone gives you money for your products and services, you become a ‘Seedling’, typically working from home at first.

Nowadays, there is no reason to have a formal office. If you are successfully and profitably running your home-based business, you can be a Seedling for as long as you like.

You may never even have to write a formal business plan; you just make sure you have cash left at the end of each month. You are essentially a ‘one-person band’, though you can have any number of self-employed sub-contractors working for you at any particular time.

As you grow, you may decide there is a genuine need to have a formal office. You might want to move your enterprise out of your home to keep work and family separate. You might now have full-time staff and other colleagues who need to communicate on a daily basis. You might need to appear more substantial and professional to key customers.

There are now many excellent options for cheap office space, including ‘hot desks’ and serviced offices, all on very flexible terms. But if you do take the big step of having a ‘proper’ office address, you certainly need to have your finances under control.

The only reason companies go broke is because they

run out of cash, so it is important to have proper financial management systems in place and someone who is on top of your cash flow on a daily basis. This can be a part-time accountant or even a virtual finance director, even if they are only formally engaged for one or two days a month.

Once you are established in your office, you have now become a Sapling, and have the basis of a sustainable long-term business. As your revenues and profits increase, you can then take on extra staff, and you really get the feeling you now have a ‘proper’ business.

I always enjoy visiting Sapling companies; there really is ‘buzz’ about the organisation. But as they approach 25 people, I always advise them to take a pause, and then decide exactly where they want to go in the future.

There is a very strong argument for keeping a company below 30 people – a ‘boutique business’. All your members of staff, as well as your key customers are your personal friends. Communication works well, often with everyone meeting in a restaurant on a Friday night. You can increase your prices and your customers do not mind, due to the excellent products and services that you provide.

You can run a ‘boutique’ Sapling business for as long as you like and be extremely profitable. Eventually, you can pass your business down to your family or staff. Your retirement will be very comfortable.

However, you may be ambitious to grow your company past 30 people, to make some serious money or to make a difference to the world. If this is you, then I have some simple advice: hire ‘grown-ups’.

Ambitious entrepreneurs who stumble unknowingly past 30 people suddenly find that life is no longer as much fun as it used to be. Employees say that nobody tells them anything anymore, while at the same time complaining about the large numbers of internal e-mails. Pointing out that if they read all the e-mails, they would know what was going on only seems to make things worse.

Employees feel disconnected from the entrepreneur. The entrepreneur feels besieged with a new set of people-related problems, such as the need to let underperforming staff go, who then reappear at industrial tribunals. There never seems to be enough hours in the day.

The company is now making the transition into a ‘Mighty Oak’, which happens a great deal earlier than people suspect, at around 30 people. To grow past this stage requires not only formal systems (such a lock on the stationery cupboard and timesheets) but people experienced enough to implement those systems effectively and fairly: grown ups.

This is often the hardest growth phase for any entrepreneur. They have to take a long, hard look at their own strengths and weaknesses and then hire people better than themselves in key positions.

The right grown-ups are definitely out there, usually working for large companies where they feel they are unlikely to make a real difference. Your company, with its proven business model and ambitions for growth, is the entrepreneurial opportunity they have been looking for. You just need to find them, and once they are in place, let them get on with it, without ‘meddling’.

issue 01 · May 2015 · City of Lon

don

WHERE DO I FIND A MENTOR?

by Mike Southon‘You don’t get something for

nothing’. It’s a well-worn phrase that entrepreneurs understand more than most of us care to admit – after all, that is business. And yet, mentoring – getting advice from an experienced businessperson – is commonplace, fun for both mentor and ‘mentee’, and great for startups. If done correctly, you can find yourself with a sizeable chunk of helpful advice for nothing more than your time and a little effort.

By following a few basic rules, finding a mentor can be the most useful thing you do when starting a new business. New experiences and challenges will be daily occurrences on your road to success, and someone who can advise you from a position of experience is invaluable when navigating choppy waters.

Busin

ess,

but

not

as

you

know

it ·

MEN

TORS

HIP

INSI

GH

TS

Someone who has ‘seen it, done it and bought the t-shirt’ is perfectly placed to tell you how to solve problems or progress the business. And if they cannot, they should be able to recommend someone who can. Mentoring is far from an exclusive relationship; networking is one of the obvious advantages of working with a successful, well-connected person so it would be a mistake not to take advantage of this. The number of mentors you have is down to you: I have been both a mentee in my own right and mentor to many hundreds of early-stage business people. I have learnt more about business this way than perhaps any other. Some people employ ‘serial mentoring’, where they have a series of short-term mentors. Others stick with a single trusted mentor over a sustained period of time. Either way, your best bet is to keep an ever-growing network of effective advisors you can call on in the future. Do not make a habit of falling out with people!

Mentoring should be a mutually beneficial relationship based on trust and respect: there is no cost, obligation or, most importantly, motive.

When choosing a mentor, consider who you would normally turn to for truthful advice with your best interests at heart. Friends and family should be your first port of call as the relationship you are looking for is already in place. Invite old business colleagues out for a coffee; perhaps do the same for clients with whom you have got on well in the past. If there is no one in your immediate circle who fits the bill, cast your net one step further: their friends, colleagues and associates. This theory of ‘one degree of separation’ instantly adds dramatically to your available network. You will be amazed how many diversely qualified people fit into your ‘friends of friends’ network. Furthermore, a meeting where both parties are personally recommended by a mutual friend is a great platform from which to build a strong relationship.

If no one you know, or know of, seems suitable, you are going to have to find them yourself. There is no magical database to search (actually, there are some options online, but do please stick to face-to-face recommendations if possible), so here are some basic, but by no means exhaustive tips:

Look for someone with at least some understanding of the type of business you want to run. Manufacturing is different to retail; biotechnology is nothing like graphic design.

Look for skills that you do not have. If you are hopeless with financials, get help with those skills – do not just pick someone who shares the same interests as you.

Mentoring is like any other relationship: you are looking for someone you like, and who likes you too. A great test of whether you have chosen the right person is how enjoyable the process of meeting them actually is. If they enjoy your company and you enjoy learning from them, this bodes very well.

Never, ever pay. Mentoring is always free. If it is not, then it is consultancy; and that is another beast altogether.

Even though this is a business relationship, mentoring needs to be enjoyable for both parties and benefits from a lack of formality. You are gaining the time, advice and insight of an experienced professional, so be flexible wherever possible. Meet at your mentor’s convenience, act on their advice quickly and make the fruits of the relationship as clear as possible. Success stories will strengthen your relationship.

On that subject, do listen to your mentor and follow their advice. If your mentor feels that you are wasting their time, they will soon give up on you. Many people who should, frankly, not be running businesses offer excuses such as: ‘I would have done it, but...’; ‘I couldn’t do that because...’ etc. These are all phrases to which experienced business people are attuned – and it makes them seethe. Anyone can come up with compelling reasons why problems remain unsolved. As an entrepreneur, you are being credited enough intelligence to go out and find solutions. I have found this the single most frustrating aspect in my time mentoring: your mentor is not a self-help guru, the advice they give is valuable, proven and they will rightly expect it to be acted upon.

The mentoring process, reduced to its core, is a matter of respect. In choosing them, you have identified your mentor as a successful business person whom you admire and respect. By setting aside time to give you the benefit of their experience, they have done the same. No money is changing hands and no deal is being struck; it is an honest exchange of knowledge, ideas and experience. If harnessed correctly, it will take your business forward and save you from mistakes that are entirely avoidable, because a queue of other people have made them before.

issue 01 · May 2015 · City of Lon

don

Harnessing the power of

technology to find the

right mentorsby Duncan Peters

Do you think you are getting the

best out of your startups?

SPO

NSO

RED

ART

ICLE

You could have the finest mentors in your industry be one of the most promising startups in your space and have incredible, up-to-date technology, but only when all of these components are working in unity, will you maximise your chances of success.

As we are all aware, forging connections between small businesses and mentors is crucial to their survival rate beyond the first five years. However, as it stands, only 20% of those mentored experience growth during this time (FSB). If making connections has got us this far, imagine what forging the right connections could do.

Much like dating, mentoring is a matching game. Expectations, interests, schedules and personality all need to be synchronised, for a connection to prove fruitful. And just like dating, these ‘ideal’ connections are hard to come by. Sometimes you need technology to lend a hand in the process – this is where eRipple comes in.

Our technology can help you find the people who meet your specs, but it is much more than that. Through personality, risk and motivation testing, combined with CV data access, calendar synching and messaging functions, eRipple aims to be a one-stop network for the mentor-mentee process.

Startupbootcamp FinTech

With a well-established mentoring structure from across the wider SBC network – over 1,500 across Europe – the accelerator is already at the forefront of the global FinTech scene. Ever keen to innovate, however, Nektarios Liolios, MD, was interested in reassessing the way their connections were made to see if they could add more than the traditional value to their startups.

Startupbootcamp FinTech in isolation boasts 332 mentors. This is an impressive number, but a daunting prospect for any startup looking to find the right match. Among these mentors, we helped to identify the 1,324 unique skills they bring to the table, making the skills searchable to allow for startups to pinpoint exactly what they require and to approach mentors accordingly.

Thanks to Startupbootcamp, we have a detailed understanding of what mentors and mentees consider necessary to constructive relationships, but even better, we have investigated our personality, risk, motivation and business philosophy and have protoyped the core matching algorithm for eRipple’s software.

We are really looking forward to developing eRipple’s applications even further, to see if we can help double that 20% growth figure in the near future.

issue 01 · May 2015 · City of Lon

don

Interview with Pankaj Chaddah,

Co-founder, Zomato by Yoav FarbeyWhat is Zomato?Zomato is a restaurant discovery platform and has a

global presence spanning 132 cities across 22 countries. Zomato currently lists over 335,000 restaurants, caters to over 30+ million consumers and employs 800 people worldwide.

What inspired the creation of Zomato?

My partner Deepinder Goyal and I started scanning delivery menus when we were working at Bain & Co in New Delhi in an attempt to save time while looking for restaurants to lunch at. This soon snowballed into an idea for a business and ‘Foodiebay’ (as Zomato was then called) germinated from that idea in 2008. The idea rapidly gained strength and in under two years, we rebranded ourselves to ‘Zomato’, had started attracting investors and were also working on our international expansion blueprint.

In the UK alone, we list in-depth information for over 22,000 restaurants, including menus, reviews, directions, opening times, contact information, etc. Our mobile app has been featured as one of the best new iOS apps, often makes it to the top apps of the Food and Drink section and is available across all mobile platforms i.e. iPhone, Windows, Android and Blackberry.

Who is your startup aimed at?

The simple answer to that is – Zomato is aimed at anyone who is hungry!

On one end of the spectrum, the service is directed at consumers who are looking to discover new places to eat. For instance, there are over 22,000 restaurants in London, but people are not able to

Busin

ess,

but

not

as

you

know

it ·

INTE

RVIE

WS

make an educated decision while choosing a new place to dine at. They do not want to take a risk and end up revisiting the same five places they usually eat at. Zomato offers people exhaustive information, including reviews and ratings on these places so they can make an informed choice.

On the other end of the spectrum, we have restaurants that use Zomato to showcase their brand to the end-consumer. Currently we cater to over 1.5 million users in London and this is a massive target audience for restaurants. We track ROI month on month for these restaurants and have an active measurement system in place to help them make the best of their partnership with us.

How does your startup stand out against its competitors?

The consumer internet space is massively crowded. Having said that, in the UK, while a number of services cater to consumers in the deals, bookings and delivery space, there is no single comprehensive discovery platform in the information and restaurant space. Zomato’s unique selling point lies in the fact that we offer exhaustive and updated information on all the restaurants in the city. Every three months, we update restaurant information and all this is done manually by meeting the restaurants directly. We also have a strong ‘vertical social network’, offering independent and very relevant reviews from people the user chooses to trust.

Also, we are never, ever complacent about our product. With every new market that we enter, we customise the product to suit that market. For instance, in London, in the summer we had a separate section for rooftop venues and more recently, following user trends, we have introduced among other Collections, the Ramen and Street food Collections! It has not been easy – but we have always believed in ensuring that our product speaks for itself.

What is your business background, and what got you interested in startups?

I am a mechanical engineer by education and worked at Bain & Company for over two years. Yes, neither of the two has anything to do with the concept of Zomato. To be frank, I never thought I would start something of my own. When we started Zomato, we were doing this as a hobby and before we knew it we could see huge business potential. It was the pure merit of the opportunity that led us to quit our cushy jobs and jump into the chaos without any safety nets.

How long has your startup been in the making, and who is the team behind the business?

Zomato originated as ‘Foodiebay’ in 2008, when it was just Deepinder and me dabbling with the idea, while handling our full time jobs at Bain. We continued working on Zomato (then Foodiebay) on the side for 18 months before quitting in December 2009.

Deepinder and I both come from engineering (Deepinder graduated in 2005 and I graduated in 2007), then consulting backgrounds. We had a core team of five to six members for the first year, all of whom are still with us and managing their respective teams. It may sound cliched, but everyone who is (and has been) with Zomato is the reason that we are where we are today.

What has been your biggest challenge so far as a startup owner?

Getting the right people has been our biggest challenge. The growth of the business, the personality of the brand and the firm’s culture – all depend on the people who work with you and carry things forward. We grew by 400 people in the last one year and we have still not cracked the talent sourcing problem, I doubt anyone in the world has! The team we have right now, is our biggest achievement. And scaling it up – the biggest challenge!

In the coming year, what would you like to achieve with your business?

International expansion will continue to be the principal focus area. We tend to get bored easily and have an inclination towards setting seemingly impossible targets and testing the mettle of our team. 15 new countries and 100 new cities in under 12 months would otherwise have not been possible. We’re moving into the U.S. and Canada soon with teams already setting up shop in Australia and Italy. Also, we’ve just acquired UrbanSpoon, our 7th acquisition on a global level in the last three months – so integrating these new companies into Zomato will keep us busy well into the foreseeable future.

If you could give one piece of advice to someone thinking about starting a business, what would it be?

Never start a business because you want to ‘start something of your own’, or ‘be your own boss’ – it never works out. Start a venture because you are confident there is an opportunity for it to do well.

issue 01 · May 2015 · City of Lon

don

Interview with Maz Nadjm,

Founder, SoAmpliby Yoav FarbeyWhat is SoAmpli?

SoAmpli is a web and mobile employee amplification platform that extends the reach of companies’ digital communications. It provides a secure platform for employees and stakeholders to be social media advocates of a company’s products, not only increasing awareness and sales, but also boosting employee engagement and motivation. The three strongest features of the platform are that it is measurable, controllable and very cost effective.

Coming from a social media consulting background, what was your ‘eureka moment’ to think of SoAmpli?

SoAmpli came out of an eight-month consultative project with NewsCorp VP of Global Internal Communication and Global SVP of HR around the launch of FOX Sports 1 with an estimated 90 million viewers. Throughout I just realised that what I was doing on a one-time base could become an automated process numerous companies could benefit from. After that, I simply went back to my basement, started working and building the product. We finally launched three months ago.

SoAmpli has already a portfolio of impressive customers, how did you approach working with companies much larger than yours?

Busin

ess,

but

not

as

you

know

it ·

INTE

RVIE

WS