final results presentation - the vault · pdf filefinal results presentation 11 november 2013....

TRANSCRIPT

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

Final Results Presentation

11 November 2013

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

Ben Magara - Chief Executive Officer

Introduction

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

Lonmin United

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

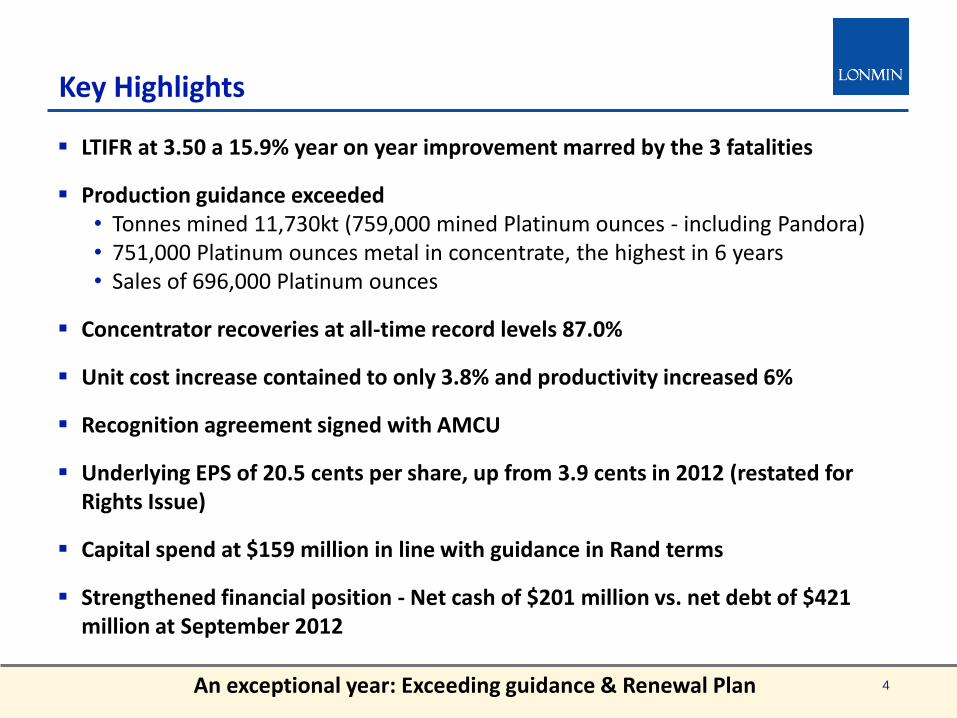

Key Highlights

LTIFR at 3.50 a 15.9% year on year improvement marred by the 3 fatalities

Production guidance exceeded • Tonnes mined 11,730kt (759,000 mined Platinum ounces - including Pandora) • 751,000 Platinum ounces metal in concentrate, the highest in 6 years • Sales of 696,000 Platinum ounces

Concentrator recoveries at all-time record levels 87.0%

Unit cost increase contained to only 3.8% and productivity increased 6%

Recognition agreement signed with AMCU

Underlying EPS of 20.5 cents per share, up from 3.9 cents in 2012 (restated for Rights Issue)

Capital spend at $159 million in line with guidance in Rand terms

Strengthened financial position - Net cash of $201 million vs. net debt of $421 million at September 2012

4 An exceptional year: Exceeding guidance & Renewal Plan

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

Simon Scott - Chief Financial Officer

Operational Review

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

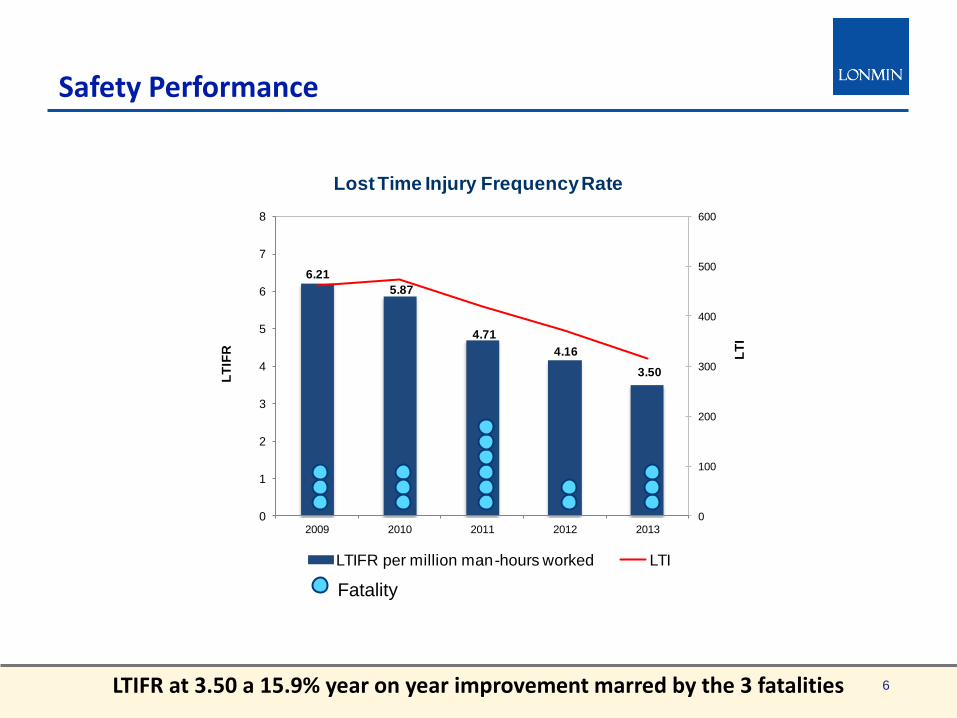

Safety Performance

6 LTIFR at 3.50 a 15.9% year on year improvement marred by the 3 fatalities

6.21

5.87

4.71

4.16

3.50

0

100

200

300

400

500

600

0

1

2

3

4

5

6

7

8

2009 2010 2011 2012 2013

LT

I

LT

IFR

Lost Time Injury Frequency Rate

LTIFR per million man-hours worked LTI

Fatality

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

7

Mining Operational Performance

0

2

4

6

8

10

12

2009 2010 2011 2012 2013

To

nn

es

(millio

ns)

Total Tonnes Mined - Annual Trend

Marikana underground Marikana opencast Pandora opencast

Pandora underground Limpopo

Mining output momentum restored

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

8

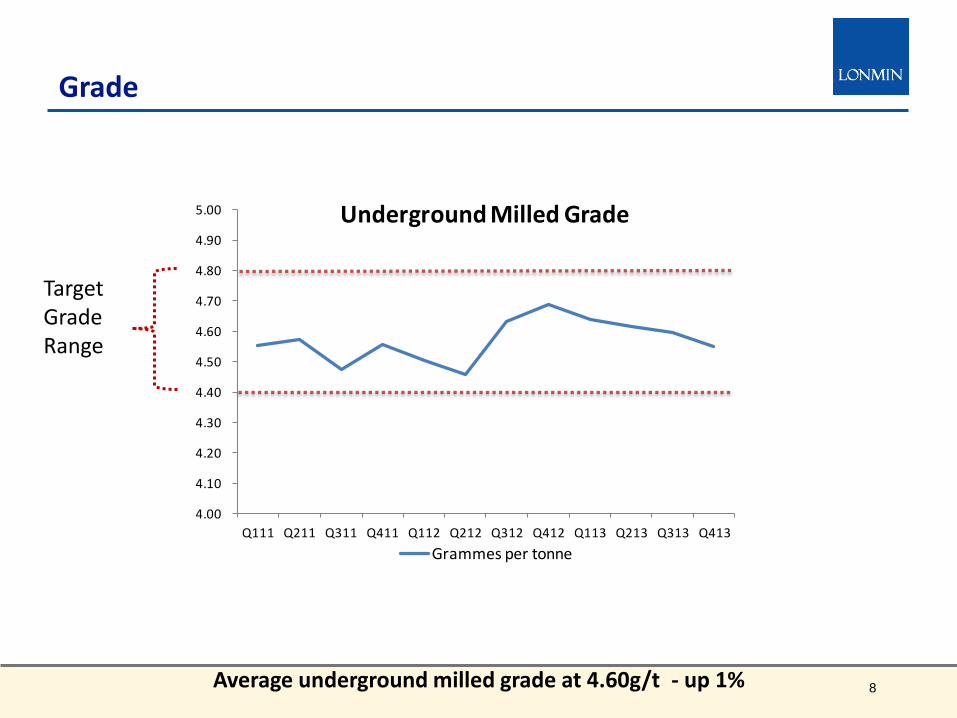

Grade

Target Grade Range

Average underground milled grade at 4.60g/t - up 1%

4.00

4.10

4.20

4.30

4.40

4.50

4.60

4.70

4.80

4.90

5.00

Q111 Q211 Q311 Q411 Q112 Q212 Q312 Q412 Q113 Q213 Q313 Q413

Underground Milled Grade

Grammes per tonne

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

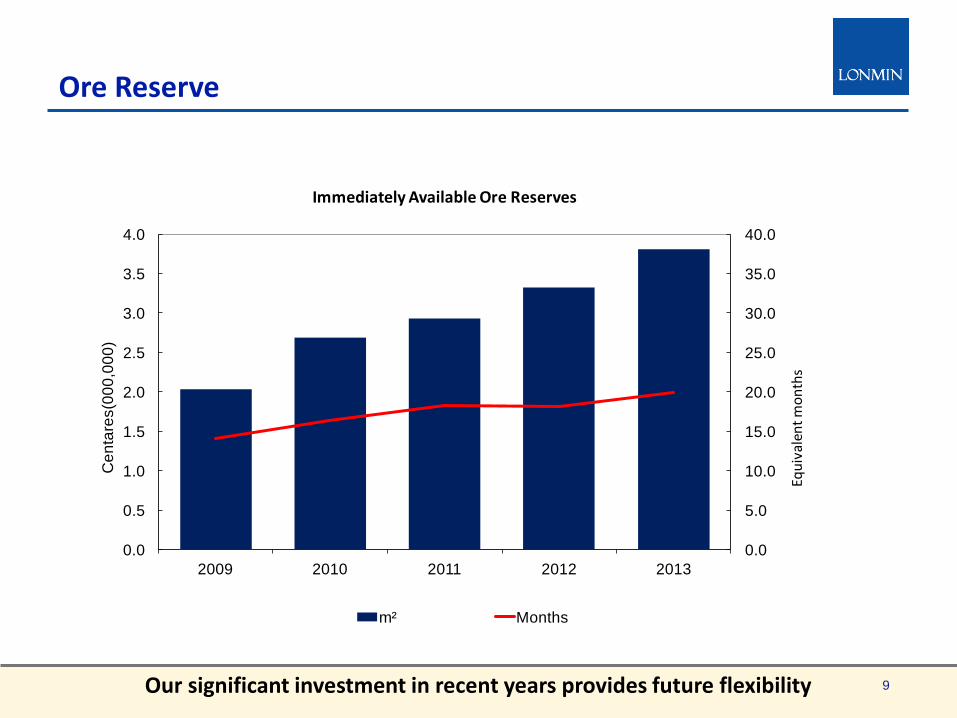

Ore Reserve

9 Our significant investment in recent years provides future flexibility

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2009 2010 2011 2012 2013

Equ

ival

ent

mo

nth

s

Ce

nta

res(0

00

,00

0)

Immediately Available Ore Reserves

m² Months

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

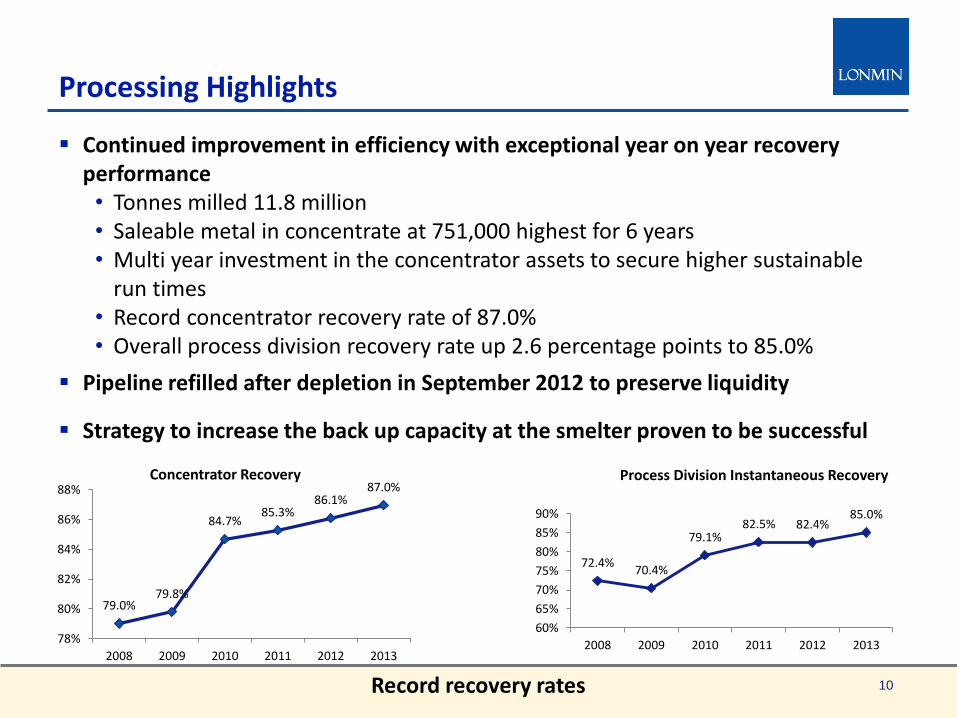

Processing Highlights

10

Continued improvement in efficiency with exceptional year on year recovery performance • Tonnes milled 11.8 million • Saleable metal in concentrate at 751,000 highest for 6 years • Multi year investment in the concentrator assets to secure higher sustainable

run times • Record concentrator recovery rate of 87.0% • Overall process division recovery rate up 2.6 percentage points to 85.0%

Pipeline refilled after depletion in September 2012 to preserve liquidity

Strategy to increase the back up capacity at the smelter proven to be successful

72.4% 70.4%

79.1% 82.5% 82.4%

85.0%

60%

65%

70%

75%

80%

85%

90%

2008 2009 2010 2011 2012 2013

Process Division Instantaneous Recovery

79.0% 79.8%

84.7% 85.3%

86.1% 87.0%

78%

80%

82%

84%

86%

88%

2008 2009 2010 2011 2012 2013

Concentrator Recovery

Record recovery rates

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

Simon Scott - Chief Financial Officer

Financial Review

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

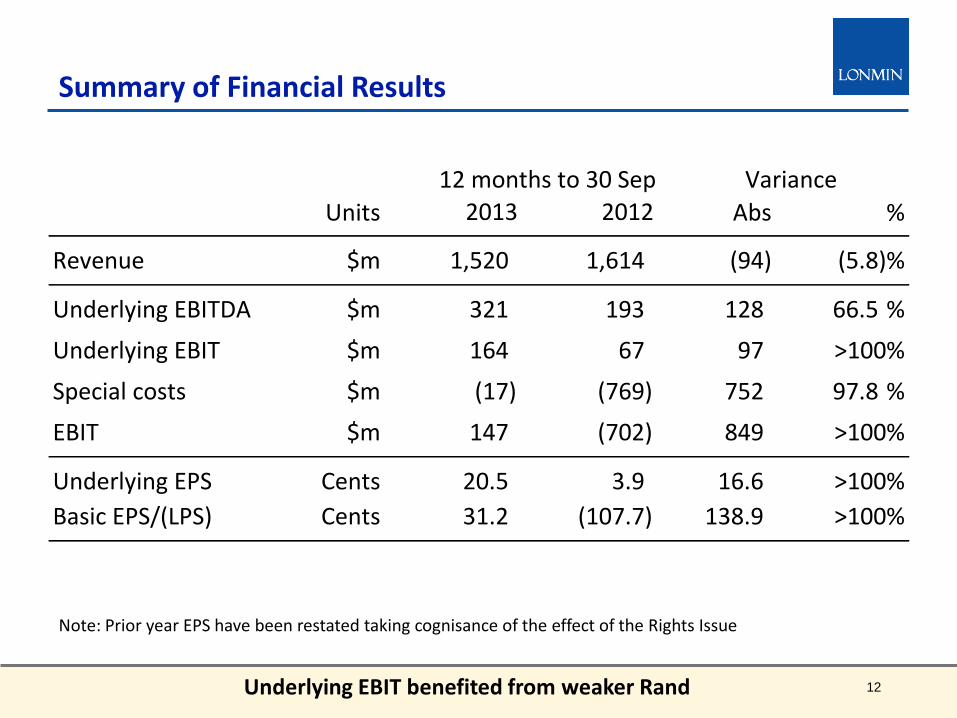

12

Summary of Financial Results

Underlying EBIT benefited from weaker Rand

Note: Prior year EPS have been restated taking cognisance of the effect of the Rights Issue

Units 2013 2012 Abs %

Revenue $m 1,520 1,614 (94) (5.8)%

Underlying EBITDA $m 321 193 128 66.5 %

Underlying EBIT $m 164 67 97 >100%

Special costs $m (17) (769) 752 97.8 %

EBIT $m 147 (702) 849 >100%

Underlying EPS Cents 20.5 3.9 16.6 >100%

Basic EPS/(LPS) Cents 31.2 (107.7) 138.9 >100%

Variance12 months to 30 Sep

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

Renewal Plan

Full year highlights

• Production and sales targets exceeded coupled with record safety achievements

• Restructuring complete and on track to deliver R200 million annualised savings from 2014

• Delivered R110 million TCO savings versus a target of R100 million

• Capital spend contained at $159 million / R1.5 billion – within guidance

• Mining division capital spend limited to $99 million

• Process division spent $52 million

• Social Labour Plan / other commitments including housing $8 million

Board has recommended no dividend this year in line with Renewal Plan

13 Exceeding the renewal plan

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

Disclosure Change: Cost Reporting

More inclusive and transparent reporting

Included in reports going forward • Detailed disclosure on cost of sales as it relates to the PGM operations

• Excludes Akanani, Exploration and London companies

Unit cost measure changed to “Cost of Production” replacing C1 unit cost • Difference is that Cost of Production includes sales and marketing costs, audit

costs, capital administration costs and management costs from our South African head office

14 Primary costs disclosed

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

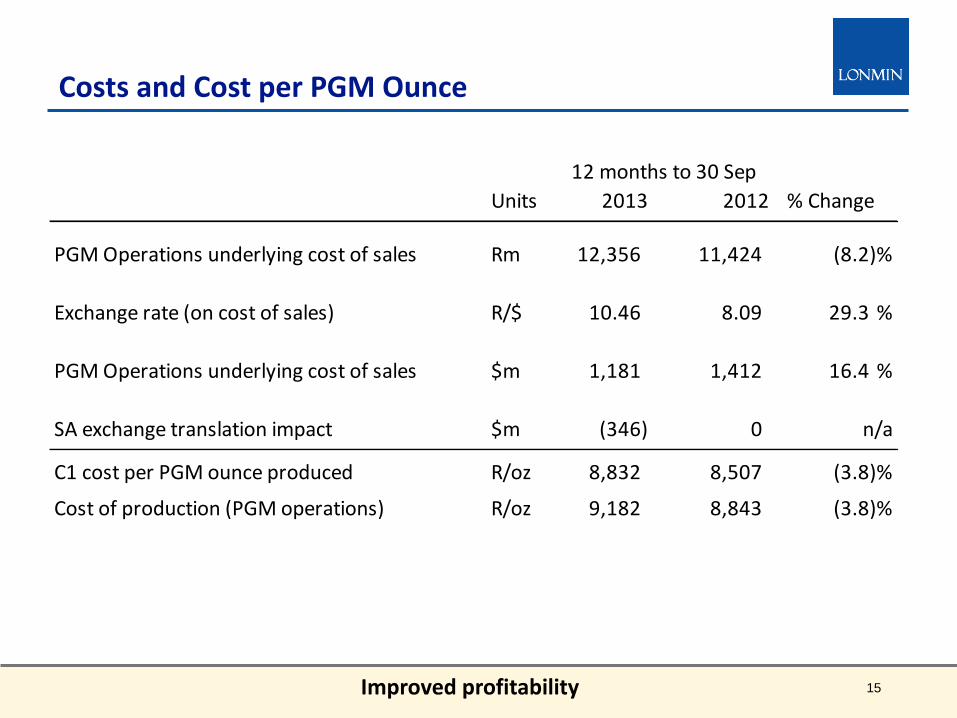

15

Costs and Cost per PGM Ounce

Units 2013 2012 % Change

PGM Operations underlying cost of sales Rm 12,356 11,424 (8.2)%

Exchange rate (on cost of sales) R/$ 10.46 8.09 29.3 %

PGM Operations underlying cost of sales $m 1,181 1,412 16.4 %

SA exchange translation impact $m (346) 0 n/a

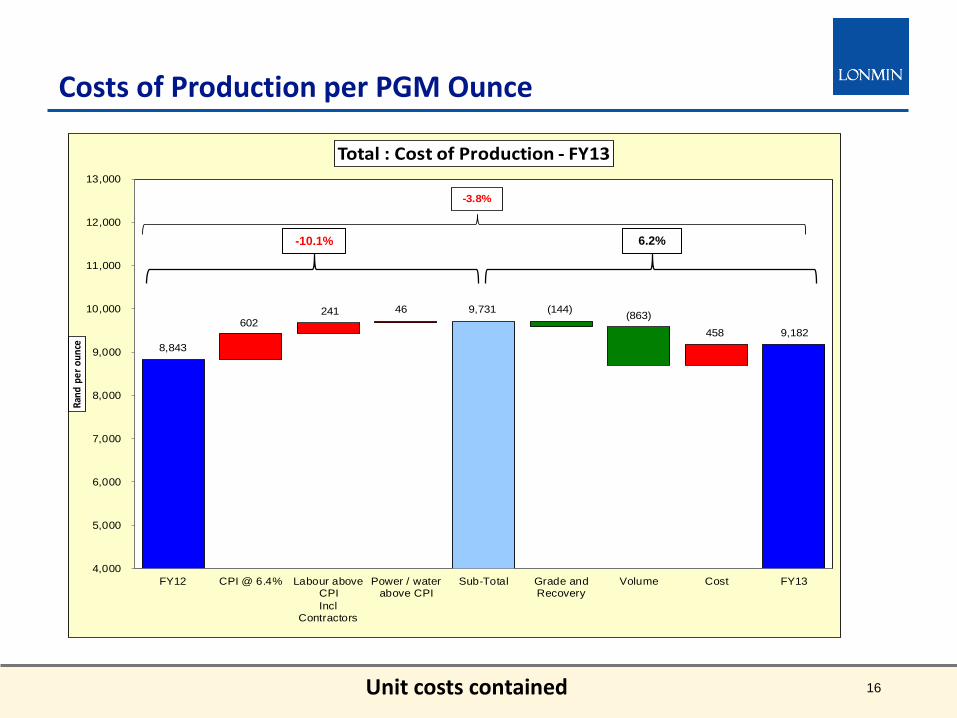

C1 cost per PGM ounce produced R/oz 8,832 8,507 (3.8)%

Cost of production (PGM operations) R/oz 9,182 8,843 (3.8)%

12 months to 30 Sep

Improved profitability

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

16

Costs of Production per PGM Ounce

8,843

602 241 46 9,731 (144)

(863)

458 9,182

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

FY12 CPI @ 6.4% Labour aboveCPI

InclContractors

Power / waterabove CPI

Sub-Total Grade andRecovery

Volume Cost FY13

Rand

per

oun

ce

Total : Cost of Production - FY13

-3.8%

-10.1% 6.2%

Unit costs contained

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

17

Underlying EBIT Variance Analysis

EBIT impacted by weaker Rand

67

393 (90)

4 (11) 3

194 (396)

164

0

100

200

300

400

500

600

700

800

PY12 Stock movement PGM volume PGM price Base metals PGM Mix FX incltranslation fx

Costs & depn(like-for-like)

FY13

$m

2013 positive stock movements as a result of refilling the pipeline and the stock lock-up combined with a stock decrease in 2012

Favourable foreign exchange impact. Rand weakened from

R8.30 to R9.99

Higher production volumes resulting in higher costs

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

(421)

767

304 (2) (32)(189)

(24)(33)

(159)

(11) 201

(500)

(400)

(300)

(200)

(100)

-

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

Opening net

debt

Rights Issue EBITDA Debtors Creditors Stock Deferred

Revenue

Net

financing

Capex Dividends Closing net

cash

$m

$223m

18

Net Cash

Rights Issue proceeds used to pay down debts

• Replenishment of the pipeline stock which was depleted in September 2012 to protect liquidity

• Inventory lock up due to smelter incident in 2013 and higher levels of finished goods

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

Ben Magara - Chief Executive Officer

Market Outlook

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

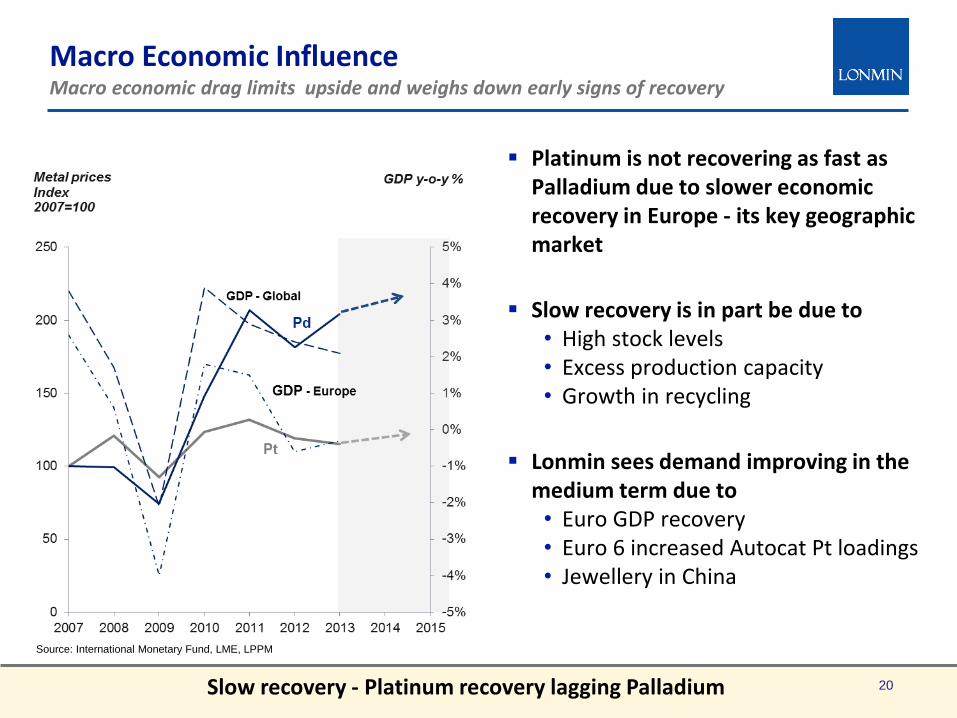

More colours Main colours Macro Economic Influence Macro economic drag limits upside and weighs down early signs of recovery

Source: International Monetary Fund, LME, LPPM

Platinum is not recovering as fast as Palladium due to slower economic recovery in Europe - its key geographic market

Slow recovery is in part be due to • High stock levels • Excess production capacity • Growth in recycling

Lonmin sees demand improving in the medium term due to • Euro GDP recovery • Euro 6 increased Autocat Pt loadings • Jewellery in China

20 Slow recovery - Platinum recovery lagging Palladium

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

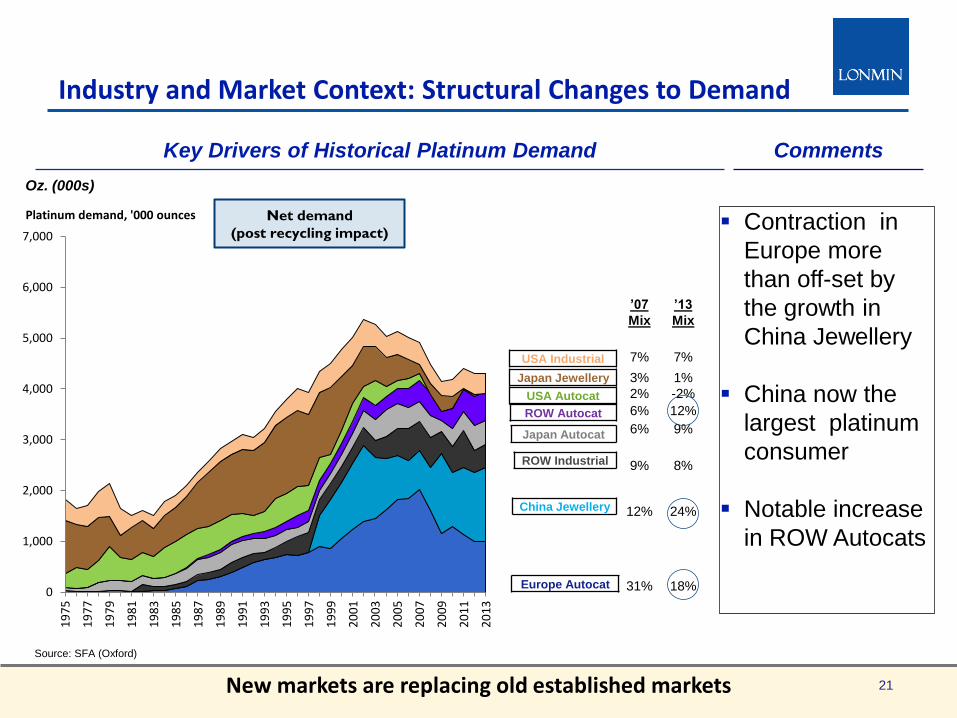

Industry and Market Context: Structural Changes to Demand

Source: SFA (Oxford)

Oz. (000s)

Key Drivers of Historical Platinum Demand

Europe Autocat

China Jewellery

ROW Industrial

Japan Autocat

ROW Autocat

USA Autocat

Japan Jewellery

USA Industrial

Comments

’07

Mix

7%

3%

2%

6%

6%

9%

12%

31%

New markets are replacing old established markets 21

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

Platinum demand, '000 ounces Net demand

(post recycling impact)

’13

Mix

7%

1%

-2%

12%

9%

8%

24%

18%

Contraction in

Europe more

than off-set by

the growth in

China Jewellery

China now the

largest platinum

consumer

Notable increase

in ROW Autocats

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

Long Term PGM fundamentals attractive due to captive demand

PGM prices have been held back by fragile European auto markets and near-term over supply

Primary supply is likely to contract in the short term, primarily as a result of disruption and restructuring in SA

Passenger car and heavy-duty on- and non-road emission legislation ensures captive demand:

• Euro 6 in Europe which started in 2013 (HDV), but will include light duty and non-road (Tier 4) from 2014

• California LEVIII (2014), USA-wide Tier 3 (2017) • Euro 6 in South Korea (2014, 22% diesel market) • India role out of Euro 5 eq. for passenger cars possible

before the end of the decade (40% diesel market)

Medium to long-term outlook for vehicle sales in emerging markets and recovering industrial demand to be positive

Even excluding Euro 5 loadings upside, platinum demand in India is forecast to double by 2018

Other demand drivers such as Chinese jewellery demand to remain positive

Emission Regulations

2014-2015 still tough with emission legislation leading longer term recovery

22

Bharat 5

P P8

Euro 6

Bharat 5

Comments

Timing unconfirmed

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

Ben Magara - Chief Executive Officer

Strategic Imperatives

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

24

Key Management Themes

Our People and Relationships

Operational Credibility and Excellence

Value Optimisation Management (VOMA)

Our Sustainability and Social Agenda

Our Focus Areas:

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

Our People and Relationships A stable and predictable industrial relations environment is essential for business and requires a step change in approach

Reclaiming our relationship with employees and their wellbeing has become business critical

Continuing to reclaim our role as managers and rebuilding trust with employees Improving wellbeing and living conditions for employees and communities

Mining Charter opportunity to increase equity participation for employees and

communities so that they feel the partnership Greater collaboration with government through public-private partnerships to

accelerate delivery of social infrastructure Enhancing participation in key industry and stakeholder forums

• CEO elimination of fatalities forum • ICMM • Market development and emissions legislation advocacy

25

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

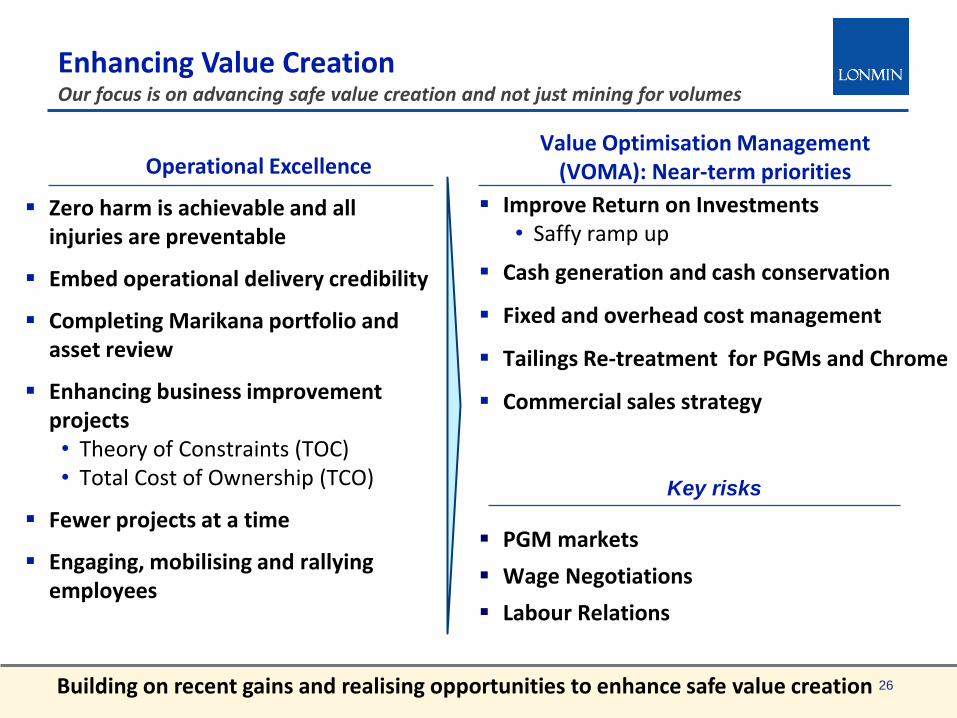

More colours Main colours Enhancing Value Creation Our focus is on advancing safe value creation and not just mining for volumes

Value Optimisation Management (VOMA): Near-term priorities Operational Excellence

Zero harm is achievable and all injuries are preventable

Embed operational delivery credibility

Completing Marikana portfolio and asset review

Enhancing business improvement projects • Theory of Constraints (TOC) • Total Cost of Ownership (TCO)

Fewer projects at a time

Engaging, mobilising and rallying employees

Building on recent gains and realising opportunities to enhance safe value creation

Key risks

Improve Return on Investments • Saffy ramp up

Cash generation and cash conservation

Fixed and overhead cost management

Tailings Re-treatment for PGMs and Chrome

Commercial sales strategy

PGM markets

Wage Negotiations

Labour Relations

26

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

Saffy Ramp Up Our ore reserves now allow us to increase our return on investment by moving crews from low margin shafts

27

Source: Lonmin

Saffy Available Ore Reserves Trend

We Doubled Available Ore Reserves in 2013

Saffy Operational Trend

Ramp up Drives Costs Down

Tonnes Hoisted (000)

500

550

600

650

700

750

800

850

900

950

1,000

600

800

1,000

1,200

1,400

1,600

1,800

2,000

'09A '10A '11A '12A '13A '14F '15F

Shaft Head Costs1 (ZAR/Tonne) M2 (000)

0

150

300

450

600

750

900

'09A '10A '11A '12A '13A '14F '15F

Drive to improve return on investment

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

Our Sustainability and Social Agenda Advancing our social and sustainability efforts to enhance our license to operate requires that we create value for all stakeholders through effective collaboration

Pursuing win-win solutions on the basis that a thriving business makes it possible

A cornerstone of the Renewal Plan

Employee Value Proposition

Community Value Proposition

Financial Value Proposition

What we have done

What we are doing

Contributed land for Integrated Human Settlements (employees and communities)

At least ZAR0.5 billion in five years to housing and community bulk services

Building bridges to enhance trust

Share economic realities (profits make it possible)

8% equity for ESOP and community trusts by December 2014

Championing collaboration through PPPs

Embedding SHE stewardship

28

Five Board Initiatives

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

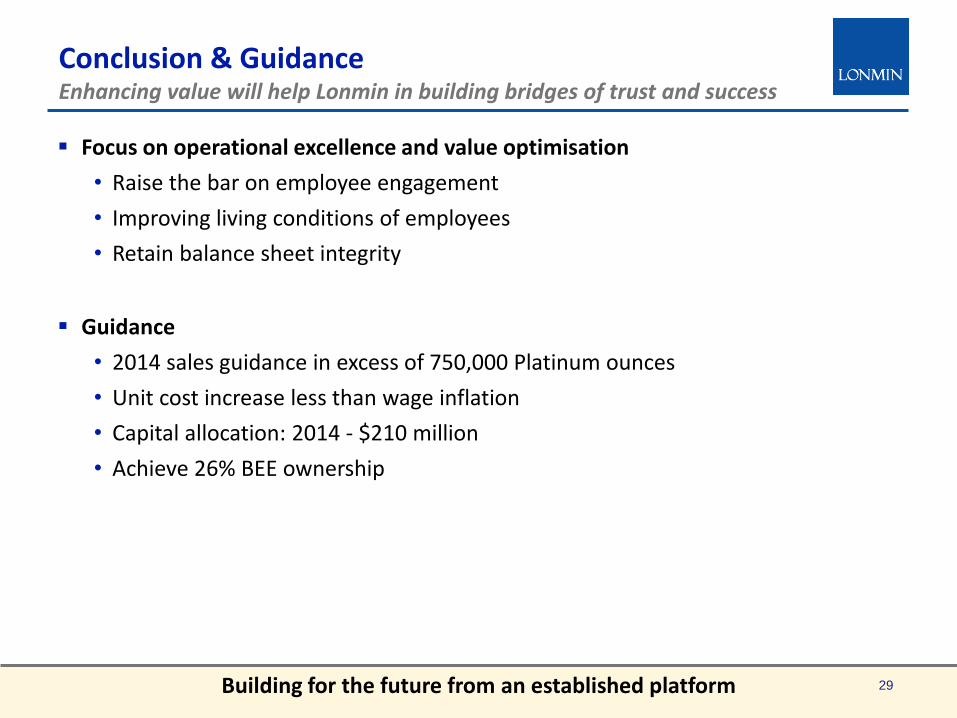

More colours Main colours Conclusion & Guidance Enhancing value will help Lonmin in building bridges of trust and success

Focus on operational excellence and value optimisation

• Raise the bar on employee engagement

• Improving living conditions of employees

• Retain balance sheet integrity

Guidance

• 2014 sales guidance in excess of 750,000 Platinum ounces

• Unit cost increase less than wage inflation

• Capital allocation: 2014 - $210 million

• Achieve 26% BEE ownership

29 Building for the future from an established platform

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

Appendices

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

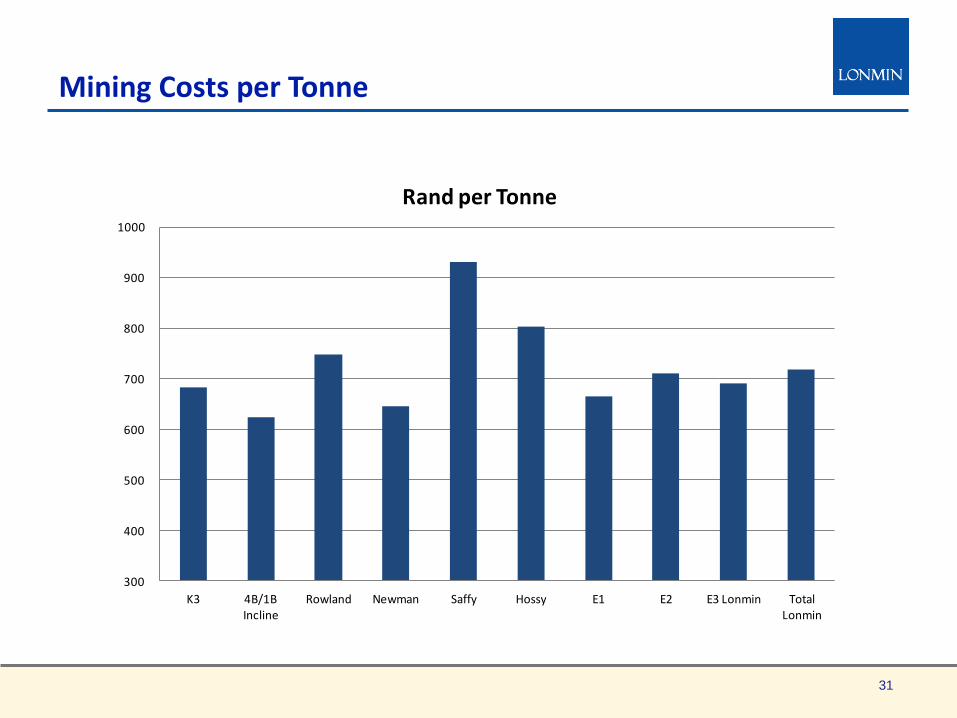

Mining Costs per Tonne

31

300

400

500

600

700

800

900

1000

K3 4B/1B Incline

Rowland Newman Saffy Hossy E1 E2 E3 Lonmin Total Lonmin

Rand per Tonne

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

Management Team

32

Simon Scott Chief Financial Officer

Simon joined Lonmin and the Board in September 2010,

became CFO in November 2010 and was appointed as Acting

CEO on 24 August 2012 in view of Mr Farmer’s illness. He is

a graduate with accounting and commerce degrees from the

University of the Witwatersrand, and has also attended the

management development program at the University of Cape

Town. A South African registered chartered accountant, he

has held a number of financial management roles in South

Africa with local and global employers including over eight

years with Anglo American. Most recently he was CFO of the

JSE-listed Aveng Limited, a globally active engineering and

construction group with significant involvement in the mining

sector.

Mark Munroe EVP Mining and Group Safety

Mark joined Lonmin in March 2008 in the Mining business,

becoming VP Capital Projects & Engineering before being

appointed as EVP Mining in June 2009. Mark joined Lonmin from

DRDGold, where he spent six years, holding a number of senior

management positions including General Manager of DRDGold

and CEO of DRDCapital. Prior to that, he worked for AngloGold for

12 years. He is a mining engineer and also has a degree in

economics.

Thandeka Ncube Business Transformation Manager,

Shanduka Resources

Thandeka works with Shanduka’s investee companies advising on

transformation and broad based empowerment. She holds a Social

Sciences degree from the City University of New York and an MBA

from Henley Business School. She began her career working with

various government institutions, developing strategy and policy for

small and medium enterprises, then joined the retail banking side of

Standard Bank, where she again focussed on the needs of SMEs.

Ben Magara Chief Executive Officer

Ben joined the Company and Board as Chief Executive on 1 July

2013. He is a graduate Mining Engineer from the University of

Zimbabwe and has attended various management programmes

including the Accelerated Development Programme at the London

Business School, UK and the AMP at GIBS, SA. Ben has extensive

mining experience in both underground and surface mining as well

as soft and hard rock mining. He also has experience in the energy

and logistics industries. Ben was the Chief Executive Officer of

Anglo Coal South Africa and the Executive Head responsible for

Engineering and Capital Projects at Anglo Platinum. Ben is a non-

executive director of Foskor and was previously a director of Anglo

American South Africa (2006-2013), was Chairman of Richards Bay

Coal Terminal and the Eskom 2008 Coal Working Group. He is also

a Trustee of the UNISA Foundation and is the Chairman of the

Board of Trustees at St Peters Prep School Foundation.

Abey Kgotle EVP Human Resources

Abey joined Lonmin in April 2008 as Senior Manager

Human Capital. He held several roles including

Executive Manager External Affairs and Executive

Manager Human Capital. He was appointed Executive

Vice President Human Resources in September 2013.

Prior to joining Lonmin, he worked in executive human

resources roles at GrafTech South Africa, City of

Johannesburg, Samancor Manganese and Denel.

Abey has extensive experience in human resource

management, labour relations, community investment

and stakeholder relations. He holds a Bachelor of

Social Sciences from the University of the North West

and a Masters Diploma in Human Resource

Management. Abey has also attended the Global

Executive Development Programme at Pretoria

University’s Gordon Institute of Business Science.

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

Management Team

33

Lerato Molebatsi

EVP Communications and

Public Affairs

Lerato joined Lonmin from the Department of Labour, where she was the

Deputy Director General; Corporate Services. Prior to joining the

Department of Labour in September 2011, Lerato worked in senior

management positions at Alexander Forbes and Old Mutual. She holds a

Bachelor of Arts degree in Psychology from the University of the North and

a Post Graduate Diploma in Rural Policy Development Policy and

Management from the University of Witwatersrand. She has also attended

the Senior Management Development programme at University of

Stellenbosch.

Albert Jamieson

Chief Commercial Officer

Albert joined Lonmin in 1989 after 8 years at Impala Platinum, where

he was responsible for their concentrator operations. At Lonmin, he

has held a number of senior management and executive positions in

the mine production and commercial areas of the business including

responsibility for investments in Africa, South America, North

America, Australia and Japan. The commercial portfolio currently

comprises business development, strategy, marketing and sales,

exploration, legal and life of business planning. Albert has a BSc in

Minerals Engineering from the University of Birmingham and an MBA

from the University of Cape Town.

Natascha Viljoen

EVP Processing and Sustainability

Natascha joined Lonmin in 2008 from BHP Billiton, where she was

General Manager for Klipspruit mine. Her initial responsibility was for

managing Lonmin’s concentrators, and in May 2011 she was

promoted to her current role, covering all concentrating, smelting

and refining operations. She holds an engineering degree and is

currently busy with an executive MBA at University of Cape Town.

Her career stretches over various commodities and disciplines in the

mining industry with 9 years in senior management roles. Before

BHP Billiton she held positions with Anglo American Platinum and

AngloGold.

Barnard Mokwena

EVP Transformation

Barnard joined Lonmin in October 2005 as a Group Manager and

was subsequently promoted to his current position. He previously

worked in senior management positions in a range of sectors for a

number of companies including Sentech, the South African Rail

Commuter Corporation and the National Lottery Operator

(UTHINGO). He holds a BA Phil from Urban Pontifical University,

an MA Licentiate from Gregorian University and an EDP from

Pretoria.

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

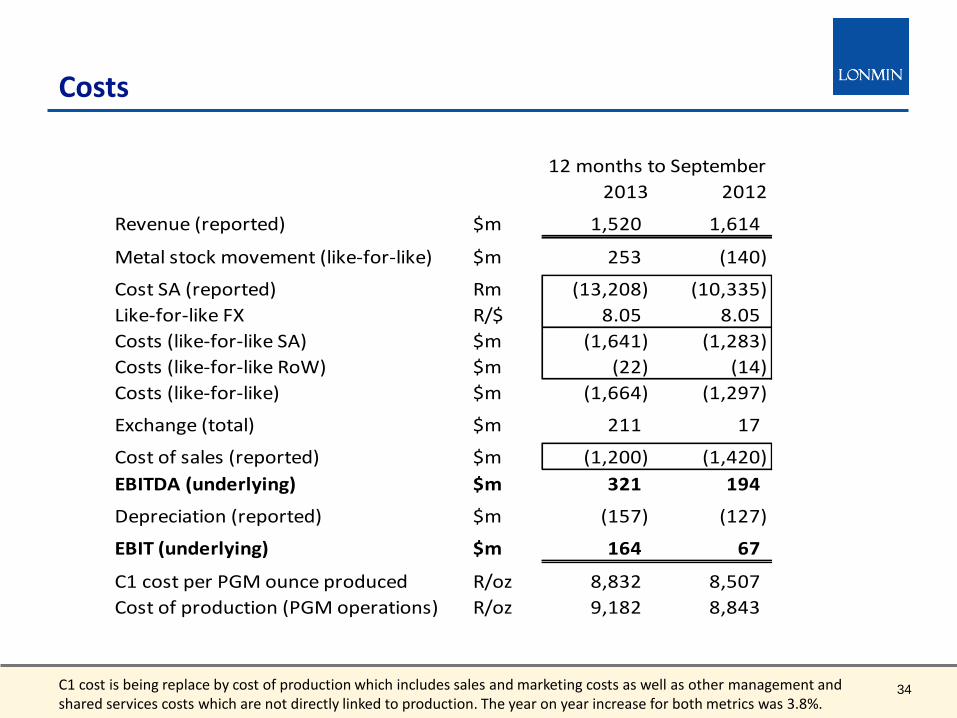

34

Costs

C1 cost is being replace by cost of production which includes sales and marketing costs as well as other management and shared services costs which are not directly linked to production. The year on year increase for both metrics was 3.8%.

2013 2012

Revenue (reported) $m 1,520 1,614

Metal stock movement (like-for-like) $m 253 (140)

Cost SA (reported) Rm (13,208) (10,335)

Like-for-like FX R/$ 8.05 8.05

Costs (like-for-like SA) $m (1,641) (1,283)

Costs (like-for-like RoW) $m (22) (14)

Costs (like-for-like) $m (1,664) (1,297)

Exchange (total) $m 211 17

Cost of sales (reported) $m (1,200) (1,420)

EBITDA (underlying) $m 321 194

Depreciation (reported) $m (157) (127)

EBIT (underlying) $m 164 67

C1 cost per PGM ounce produced R/oz 8,832 8,507

Cost of production (PGM operations) R/oz 9,182 8,843

12 months to September

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

Current Shaft Life Cycle

Source: Lonmin

Fewer than the ideal number of shafts in steady state 35

016

033

141

008

083

166

000

173

226

072

072

072

118

118

118

161

192

218

235

235

235

146

205

220

194

214

155

204

153

255

231

233

241

204

209

225

Table alternative highlight-light

Table alternative highlight-dark

Line chart colour 171

228

245

204

255

204

255

255

000

250

191

143

178

161

199

224

226

241

More colours Main colours

36

Disclaimer

This presentation, which is personal to the recipient, has been issued by Lonmin. This presentation includes forward-looking statements. All statements other than statements of historical fact included in this announcement, including without limitation those regarding Lonmin's plans, objectives and expected performance, are forward-looking statements. Lonmin has based these forward-looking statements on its current expectations and projections about future events, including numerous assumptions regarding its present and future business strategies, operations, and the environment in which it will operate in the future. Forward-looking statements generally can be identified by the use of forward-looking terminology such as 'ambition', 'may', 'will', 'could', 'would', 'expect', 'intend', 'estimate', 'anticipate', 'believe', 'plan', 'seek' or 'continue', or negative forms or variations of similar terminology. Such forward-looking statements involve known and unknown risks, uncertainties, assumptions and other factors related to Lonmin, including, among other factors: (1) material adverse changes in economic conditions generally or in relevant markets or industries in particular; (2) fluctuations in demand and pricing in the mineral resource industry and fluctuations in exchange rates; (3) future regulatory and legislative actions and conditions affecting Lonmin's operating areas; (4) obtaining and retaining skilled workers and key executives; and (5) acts of war and terrorism. By their nature, forward-looking statements involve risks, uncertainties and assumptions and many relate to factors which are beyond Lonmin‘ control, such as future market conditions and the behaviour of other market participants. Actual results may differ materially from those expressed in forward-looking statements. Given these risks, uncertainties, and assumptions, you are cautioned not to put undue reliance on any forward-looking statements. In addition, the inclusion of such forward-looking statements should under no circumstances be regarded as a representation by Lonmin that Lonmin will achieve any results set out in such statements or that the underlying assumptions used will in fact be the case. Other than as required by applicable law or the applicable rules of any exchange on which Lonmin's securities may be listed, Lonmin has no intention or obligation to update or revise any forward-looking statements included in this presentation after the publication of this presentation. This presentation is for information only and does not constitute or form part of any offer or invitation to sell, or any solicitation of any offer to purchase, any shares in Lonmin or any other securities, nor shall it or any part of it nor the fact of its distribution form the basis of, or be relied upon in connection with, any contract or investment decision related thereto. Information supplied by host presenters may not be used, referenced or published without the prior written consent of the author of the presentations.