finance and market presentation 02.01.2012

TRANSCRIPT

The Moore Group LLCPresentation

of Finance and Market Report

toXXXXXXX

February 1, 2012

1

Private and Confidential

The Moore Group LLC

2

Table of Contents

The Moore Group LLC

Table of ContentsFinancial Modeling Analysis & Summary

Pages 4 -13

PPA Market Trends and Analysis Pages 14 -15

Project Finance Market Overview Pages 16 -18

Senior Debt Market and Overview Pages 19 -22

Tax Equity Market and Overview Pages 23 – 33

Review of Capital Structure Pages 34 - 40

Plan of Execution for Project Financing

Pages 41 -42

Key Decision Items Page 43 - 44

3The Moore Group LLC

Summary of Financial Modeling

4The Moore Group LLC

Summary Results of Financial Modeling

Case AnnualMWH ofProduction

CostPer kWh(AC) Basis

LeverageIRR

NoLeverageIRR

Leverage20 yearNPV @10%

NoLeverageNPV @8%

PV 300 MW (DC) Base Case

666,461 $3,757

31.52%

11.32%

$2,745 $1,336

PV 300 MW (DC) Revised

666,461 $3,102

15.68%

8.85% $781 $232

PV 75 MW (DC) 166,615 $3,182

18.07%

10.28%

$286 $143

XXXXXX 440 MW (AC) 1,196,791

$2,893

19.27%

10.17%

$1,151 $607

XXXXXX 300 MW (AC) 815,994 $2,860

16.42%

9.54% $648 $314

XXXXXX 200 MW (AC) 543,996 $2,833

19.08%

10.16%

$510 $271 5The Moore Group LLC

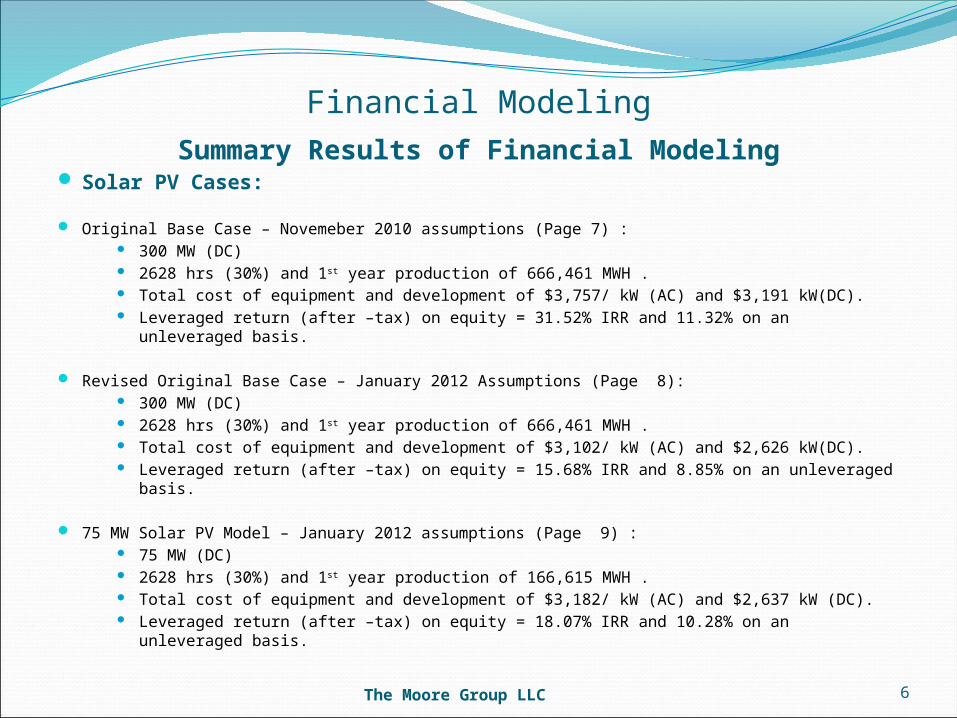

Financial ModelingSummary Results of Financial Modeling

Solar PV Cases:

Original Base Case – Novemeber 2010 assumptions (Page 7) : 300 MW (DC) 2628 hrs (30%) and 1st year production of 666,461 MWH . Total cost of equipment and development of $3,757/ kW (AC) and $3,191 kW(DC). Leveraged return (after –tax) on equity = 31.52% IRR and 11.32% on an unleveraged

basis.

Revised Original Base Case – January 2012 Assumptions (Page 8): 300 MW (DC) 2628 hrs (30%) and 1st year production of 666,461 MWH . Total cost of equipment and development of $3,102/ kW (AC) and $2,626 kW(DC). Leveraged return (after –tax) on equity = 15.68% IRR and 8.85% on an unleveraged basis.

75 MW Solar PV Model – January 2012 assumptions (Page 9) : 75 MW (DC) 2628 hrs (30%) and 1st year production of 166,615 MWH . Total cost of equipment and development of $3,182/ kW (AC) and $2,637 kW (DC). Leveraged return (after –tax) on equity = 18.07% IRR and 10.28% on an unleveraged

basis.

6The Moore Group LLC

Financial ModelingSummary Results of Financial Modeling

Amonix Cases:

440 MW Revised - January 2012 Assumptions (Page 10): 440 MW (AC) 2,720 hrs (31.1%) and 1st year production of 1,196,791 MWH . Total cost of equipment and development of $2,893/ kW (AC) and $2,419 kW(DC). Leveraged return (after –tax) on equity = 19.27% IRR and 10.17% on an unleveraged

basis.

300 MW (AC) Revised – January 2012 Assumptions (Page 11): 300 MW (AC) 2,720 hrs (31.1%) and 1st year production of 815,994 MWH . Total cost of equipment and development of $2,860/ kW (AC) and $2,392 kW(DC). Leveraged return (after –tax) on equity = 16.42% IRR and 9.54% on an unleveraged basis.

200 MW (AC) Revised – January 2012 Assumptions (Page 12): 200 MW (AC) 2,720 hrs (31.1%) and 1st year production of 543,996 MWH . Total cost of equipment and development of $2,833/ kW (AC) and $2,328 kW (DC). Leveraged return (after –tax) on equity = 19.08 % IRR and 10.16% on an unleveraged

basis.

7The Moore Group LLC

Financial Modeling Original Base Case submitted in November 2010, assumptions:

300 MW (DC) of solar PV on dual axis trackers. PPA priced at 11.4 cents/ kWh with TOD equated to 15.6 cents/ kWh 2,628 hrs. of production (30%) and 1st year generation of 666,641 MWH. Utility interconnect cost of $45 million. Equipment and installation costs updated as follows:

Solar modules: $1.10/watt Trackers: $.30/watt Inverters: $.20/watt Balance of System: $.25/watt Installation: $1.00/watt

All in equipment cost, including installation and development expenses equal to $3,757/kW on an AC basis and $3,191/ kW on a DC basis.

Original model assumed 50% leverage against total cost

Sources Uses Percentage Project Dev.: $47,251 Debt: $526,598 50% Equipment: $910,050 Tax Equity: $421,278 40% Soft Costs: $95,895 Equity: $105,320 25% Total $1,053,196 1,053,196 100%

Project investment equity returns (after tax) = 15.68% IRR on a leveraged basis and 8.85% on an unleveraged basis.

8The Moore Group LLC

Financial Modeling• Revised original model with updated cost and PPA assumptions and revised leverage:

300 MW (DC) of solar PV on dual axis trackers. PPA priced at 11.5 cents flat with no escalation. 2,628 hrs. of production (30%) and 1st year generation of 666,641 MWH. Utility interconnect cost of $56 million. Equipment and installation costs updated as follows:

Solar modules:$.90/watt Trackers: $.40/watt Inverters: $.25/watt Balance of System: $.15/watt Installation: $.55/watt

All in equipment cost, including installation and development expenses equal to $3,106/kW on an AC basis and $2,626/kW on a DC basis.

Leverage reduced to 35% due to concerns in tax equity market and reduced PPA pricing

Sources Uses Percentage Project Dev.: $31,750 Debt: $300,109 35% Equipment: $756,050 Tax Equity: $342,982 40% Soft Cost: $69,654 Equity: $214,363 25% Total $857,454 $857,454 100%

Project investment equity returns (after tax) = 15.68% IRR on a leveraged basis and 8.85% on an unleveraged basis.

9The Moore Group LLC

Financial Modeling 75 MW model with updated cost, PPA and leverage assumptions. Model assumes that

XXXXXXX develops three 75MW projects utilizing ½ of the project site.

75 MW (DC) of solar PV on dual axis trackers. 2,628 hrs (30.0%) and 1st year energy production of 166,615 MWH. PPA priced at 11.5 cents flat with no escalation. Utility interconnect cost is 1/3 of $56 million. All in equipment cost, installation and development cost of $3,182 kW on an AC

basis and $2,637/kW on a DC basis. Leverage reduced to 35% of capital cost

Sources Uses Percentage Project Dev.: $6,415 Debt: $73,863 35% Equipment: $194,084Tax Equity: $84,416 40% Soft Cost: $10,540 Equity: $52,760 25% Total $211,039$211,039100%

Project investment equity returns (after tax) = 18.07% IRR on a leveraged basis and 10.28% on an unleveraged basis.

Note that the return on the 75MW model is better than the revised 300 MW due to better utilization of land lease.

10The Moore Group LLC

Financial Modeling XXXXXX 440 MW (AC) Revised Base Model – This model assumes revised PPA pricing

and leverage assumptions .

440 MW (AC) of XXXXXX installed system. 2,720 hrs (31.1%) and 1st year energy production of 1,196,791 MWH. PPA with two off-takers at 11.5 / kWh flat with no escalation. Utility interconnect cost of $91 million combined at XXXXXX and XXXXXX. All in cost of equipment, including interconnect and development cost would

be $1.273 billion or $2,893 per kW (AC) / $2,419 per kW (DC). Leverage is revised from original at 35% of asset cost

Sources Uses Percentage Project Dev.: $39,050 Debt: $488,856 35% Equipment: $1,233,890 Tax Equity: $558,693

40% Soft Cost: $123,793 Equity: $349,183 25% Total $1,396,733 $1,396,733 100%

Project investment equity returns (after tax) = 19.27% IRR on a leveraged basis and 10.17% on an unleveraged basis.

11The Moore Group LLC

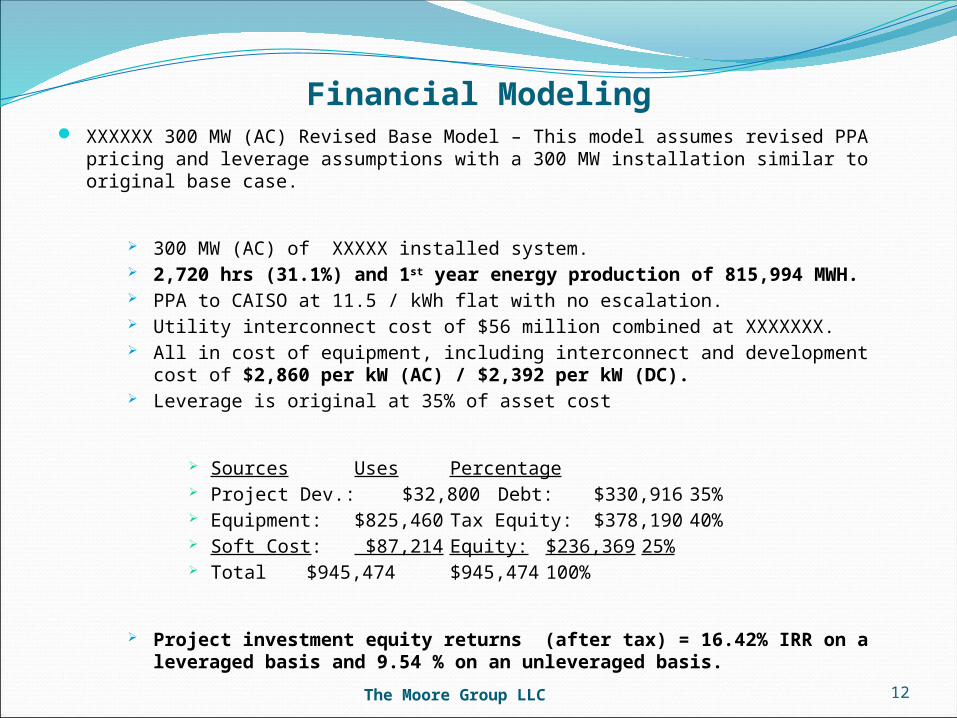

Financial Modeling XXXXXX 300 MW (AC) Revised Base Model – This model assumes revised PPA pricing

and leverage assumptions with a 300 MW installation similar to original base case.

300 MW (AC) of XXXXX installed system. 2,720 hrs (31.1%) and 1st year energy production of 815,994 MWH. PPA to CAISO at 11.5 / kWh flat with no escalation. Utility interconnect cost of $56 million combined at XXXXXXX. All in cost of equipment, including interconnect and development cost of

$2,860 per kW (AC) / $2,392 per kW (DC). Leverage is original at 35% of asset cost

Sources Uses Percentage Project Dev.: $32,800 Debt: $330,916 35% Equipment: $825,460 Tax Equity: $378,190 40% Soft Cost: $87,214 Equity: $236,369 25% Total $945,474 $945,474 100%

Project investment equity returns (after tax) = 16.42% IRR on a leveraged basis and 9.54 % on an unleveraged basis.

12The Moore Group LLC

Financial Modeling XXXXXX 200 MW model – This model assumes that the XXXXXXX site is split in half and

developed on half the site and power sold to XXXXXX/ XXXXX

200 MW (AC) of XXXXXX installed system. 2,720 hrs (31.1%) and 1st year energy production of 543,996 MWH. PPA with XXXXXX for 11.5 cents/ kWh flat with no escalation. Utility interconnect cost of $35 million at XXXXXXX substation. All in equipment cost, including interconnect and development cost equal to $2,833/

kW (AC) / $2,368/ kW (DC). Leverage is original at 35% of asset cost

Sources Uses Percentage Project Dev.: $19,546 Debt: $217,653 35% Equipment: $546,985 Tax Equity: $248,746 40% Soft Cost: $55,335 Equity: $155,466 25% Total $621,866 $621,866 100%

Project investment equity returns (after tax) = 19.08% IRR on a leveraged basis and 10.16 % on an unleveraged basis.

13The Moore Group LLC

Market Trends in PPA Market

14The Moore Group LLC

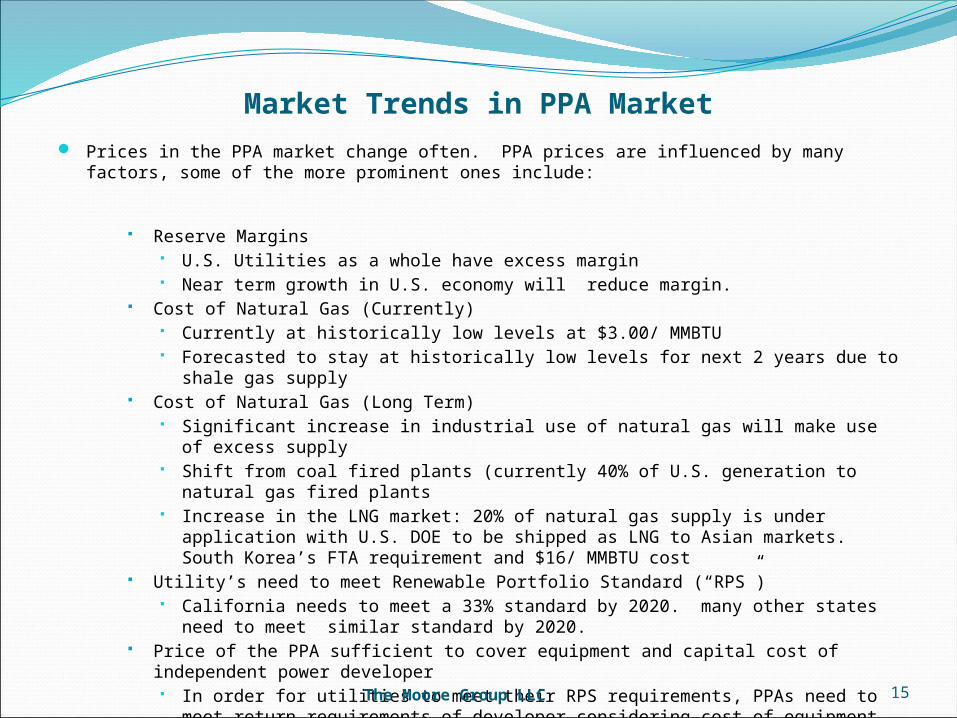

Market Trends in PPA Market Prices in the PPA market change often. PPA prices are influenced by many factors, some of

the more prominent ones include:

Reserve Margins U.S. Utilities as a whole have excess margin Near term growth in U.S. economy will reduce margin.

Cost of Natural Gas (Currently) Currently at historically low levels at $3.00/ MMBTU Forecasted to stay at historically low levels for next 2 years due to shale gas

supply Cost of Natural Gas (Long Term)

Significant increase in industrial use of natural gas will make use of excess supply

Shift from coal fired plants (currently 40% of U.S. generation to natural gas fired plants

Increase in the LNG market: 20% of natural gas supply is under application with U.S. DOE to be shipped as LNG to Asian markets. South Korea’s FTA requirement and $16/ MMBTU cost

Utility’s need to meet Renewable Portfolio Standard (“RPS”) California needs to meet a 33% standard by 2020. many other states need to

meet similar standard by 2020. Price of the PPA sufficient to cover equipment and capital cost of independent power

developer In order for utilities to meet their RPS requirements, PPAs need to meet return

requirements of developer considering cost of equipment, capital structure and cost of capital.

15The Moore Group LLC

Project Finance Market Overview

16The Moore Group LLC

Project Financing Market

Type 2011 2012 2013Other $0.6 Billion $0.8 Billion $1.0 BillionCSP $9.9 Billion $13.4 Billion $16.0 BillionPV $9.5 Billion $12.9 Billion $15.0 BillionWind $11.2 Billion $14.1 Billion $17.0 Billion

17

Renewable Energy Project Finance Demand Estimates 2011 - 2103

The chart above was compiled by a joint research effort of Mintz Levin and GTM Research. These amounts reflect the total capital being sought Including direct equity, tax equity, and senior and subordinated debt

Totals $31.2 Billion $ 41.2 Billion $48.9 Billion

The Moore Group LLC

Project Financing Market

18

The actual amount of project financing that is expected to be secured

Technology 2011 2012 2013

Other $0.5 Billion $0.6 Billion $0.7 Billion

CSP $6.5 Billion $8.0 Billion $9.6 Billion

PV $7.6 Billion $10.3 Billion $12.0 Billion

Wind $10.0 Billion $11.3 Billion $11.9 Billion

Totals $24.6 Billion $30.2 Billion $34.2 Billion

Mintz Levin and GTM Research estimate that given the expiration of the1603 Credit and the difficulties facing commercial banks that there will be a decline inDevelopers securing project financing of approximately 5% per yearThey estimate that $30.2 billion (74% of market) will achieve project financing in2012 and $34.2 billion or (70% of market) will get financing in 2013.

The Moore Group LLC

Senior Debt

19The Moore Group LLC

Senior DebtProminent Project Finance lenders in U.S. market since

2007:

20

2007 2008 2009 2010

Banco Santander Banco Espirito Santo Banco Espirito Santo Banco Santander

Bayern LB Banco Sabadell Banco Santander Bank of Montreal

BBVA BBVA BNP Paribas Barclays

Dexia BTMU BTMU BBVA

Fortis Credit Agricole Credit Agricole BTMU

HSH Nordbank Citibank Co Bank Caja Madrid

JP Morgan Chase Dexia Credit Suisse Credit Agricole

Mizuho HSH Nordbank Dexia Credit Suisse

Natixis ING Helaba Deutsche Bank

Nord LB Lloyds TSB HSH Nordbank Dexia

Prudential Morgan Stanley John Hancock Helaba

RBS Nord LB Key Bank ING

Union Bank Prudential LBBW John Hancock

RBS Lloyds TSB Key Bank

Scotia Bank Nord LB LBBW

UniCredit Prudential Morgan Stanley

Union Bank RBS Natixis

Scotia Bank Prudential

Societe Generale Rabobank

UniCredit RBS

Union Bank Societe Generale

West LB UniCredit

Union Bank

West LB

The Moore Group LLC

Senior DebtTop Project Finance Lead Arrangers in U.S. in

2011

1. Mitsubishi UFJ Financial Group (“BTMU” as shown in previous chart)

2. Bank of Montreal3. Credit Agricole4. ING5. Credit Suisse6. Barclays7. Sumitomo Mitsui8. CIBC9. Royal Bank of Scottland (“RBS”)10. Royal Bank of Canada (“RBC”)

21The Moore Group LLC

Senior Debt Current Terms and Conditions

Amount: From $100 million+100% construction financing is available if equity is committed under guarantee or LOC

Term: 5 year mini perms up to 20 years Pricing: 1.75% to 3.50% over LIBOR

LIBOR will need to be swapped current 20 year swap rate <3.0% Minimum

DSCR: 1.35X Other Conditions:

Committed capital in place at construction finance closing Senior lender will likely want EPC Contractor / Equipment Supplier

and Sponsor to cover elements of construction and performance risk.

Senior Lender will be particularly focused on long term performance of equipment and level of warranties provided and/or maintenance reserve in deal.

Inter-Creditor Agreement- Senior lender will require pledge of all assets, permits and contracts of the project with rights to “Step In”

22The Moore Group LLC

Tax Equity

23The Moore Group LLC

Tax Equity

Tax equity investors are traditionally large investment banks, commercial banks, insurance companies and even large public utilities with a high tax burden.

Tax equity investors receive a return based primarily on federal and state tax benefits generated by the project and secondarily from cash flow from the project.

Tax equity is a passive ownership interest and tax equity investors do not get involved in management of the project.

Renewable energy project developers typically do not have tax liabilities large enough to utilize the full amount of tax credits available for large projects

Project developers can pair with a tax equity partner to better utilize a project’s tax benefits (investment tax credit & MACRS depreciation)

24The Moore Group LLC

Tax Equity

The ITC and MACRS depreciation are tax benefits that will be "sold" together to a tax investor(s) who will receive these tax benefits from the project through their investment into the special purpose company that will be set up to own and operate the project.

Tax equity investor(s) will be passive investors in the special purpose company and will invest with the intention of getting a large percentage of their return from the ITC and the tax losses that the project will produce in the first five years of operation from the MACRS depreciation.

25The Moore Group LLC

Tax Equity

Investment Tax Credit The principal federal incentive for developing and installing solar

power is the Investment Tax Credit (ITC) under Section 48 of the Internal Revenue Code

The ITC is a 30% tax credit on the solar facility cost

The ITC is a direct reduction in federal income tax owed. Federal income tax liability is needed in order to utilize it.

The DOT 1603, which expired on 12/31/11, was a cash grant option for ITC-eligible projects to receive the value of the ITC as a direct cash grant instead of as a tax credit. The 1603 credit was put in place due to the lack of tax equity appetite during the financial crisis of 2008 – 2009.

The ITC remains a 30% tax credit for all projects placed in service before December 31, 2016 when it reverts to 10%. 26The Moore Group LLC

Tax Equity

MACRS

In addition to the ITC, owners of a renewable energy project are also able to accelerate the depreciation of qualifying renewable energy equipment through MACRS (Modified Accelerated Cost Recovery System)

MACRS allows tangible property to be depreciated on an accelerated basis according to a detailed schedule specified by the Internal Revenue Service (IRS)

A five year depreciation schedule is allowed for all ITC-eligible technologies including solar

MACRS is a significant tax benefit, reducing the owner’s taxable income considerably in the first years of operation thus improving the project’s overall return

Typically about 40% (depending on the level of tax losses generated by the project) of a solar PV system’s installed cost can be recovered when combining MACRS with the 30% ITC

27The Moore Group LLC

Tax Equity Investors The tax equity market peaked in 2007 with 20 institutional tax equity investors and

$6.1 billion in tax equity investment After a large drop in 2009, there are currently 16 “institutional” tax equity investors

active in renewable energy as of 2011. This list is not inclusive of all of the TEIs in the market just the most prominent ones. There does exist a number of “boutique” investment banking firms that will put together tax equity investments for an assortment of passive investors that can utilize the tax benefits generated by renewable energy projects. These boutique firms may play an increasingly important role in the post 1603 credit era.

28The Moore Group LLC

TEI Market U.S. tax equity supply for renewable energy projects essentially

disappeared in late 2008, but has begun a resurgence and reached $3.7 billion in 2010 and 2011 and expected to be at the same level in 2012.

While this growth trend is a positive, tax equity capacity still remains below pre-crisis levels.

29The Moore Group LLC

TEI - Requirements

Project with:Proven technology and quality equipmentSize greater than USD$100 millionWell structured utility scale project with fixed PPAModest leverage and/or high debt service coverage

ratios (DSCRs) with minimal variability. Investment grade risk characteristics

Developer with:Experience in utility scale renewable energy projects Strong financial capabilitiesSignificant capital at risk (“skin in the game”)

30The Moore Group LLC

TEI Yields Investor yields are correlated with supply & demand (more so than

interest rates) and have remained stable

31The Moore Group LLC

TEI Comments

The range of returns that TEI’s are seeking are typically given in articles or by industry participants at conferences without qualifying the particulars of a deal. The required return that a TEI would seek for a deal with commercial risk (PPAs are with non-investment grade off-takers) will be dramatically different then the return that a TEI would require for a project similar to the Nevada 300 project that has structured away the operating risk and has a long term PPA with a large investment grade utility.

XXXXXX Project is a large scale utility project that has utility type risk . The risk is the that the utility does not pay the XXXXXX Project under its long term contractual agreement (PPA) with the Project.

The current long term (20+ yrs.) debt cost for utilities in the U.S. is in the <5% range (pre-tax). An "institutional investor" looks at investing in the XXXXXX Project as an attractive "risk arbitrage" to investing in one of those long term bonds that they could otherwise invest in.

32The Moore Group LLC

TEI Comments

XXXXXXX still assumes a 9% yield (after tax) for a utility risk profile. The risk of non-performance in the project is structured away through the PPA, the equipment warranties and the minimal variability in solar insolation levels at the XXXXXXX Project site.

An investor cannot justify required returns of >15% (after-tax) for a structured investment that has a risk profile very similar to what they would have by buying a fixed income bond from this same utility with an after tax yield in the 3 - 4% range.

As technology matures and has greater history of operating performance the required yields from all segments of the capital structure will be reduced. As a case in point Solar PV is becoming much prevalent in the market and the differences in the cost of money between PV and Wind is becoming smaller. Some lenders and TEI’s now actually prefer solar PV to wind due to portfolio concentrations. In time expectations are that Solar PV will be below that of wind, since wind can have much greater volatility in its operating performance.

33The Moore Group LLC

Review of Capital Structures

34The Moore Group LLC

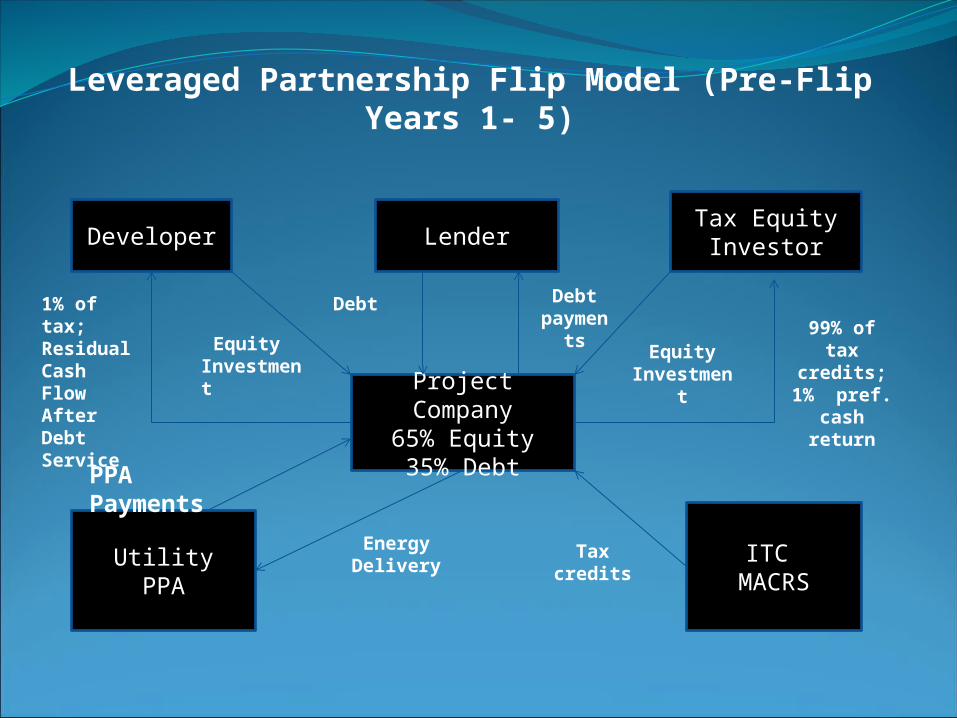

Leveraged Partnership Flip Model (Pre-Flip Years 1- 5)

Developer LenderTax EquityInvestor

Project Company

65% Equity35% Debt

UtilityPPA

ITC MACRS

Debt payments

Equity Investment

99% of tax credits;

1% pref.cash return

Debt

Equity Investment

PPA Payments

1% of tax;Residual Cash FlowAfter DebtService

Energy Delivery

Tax credits

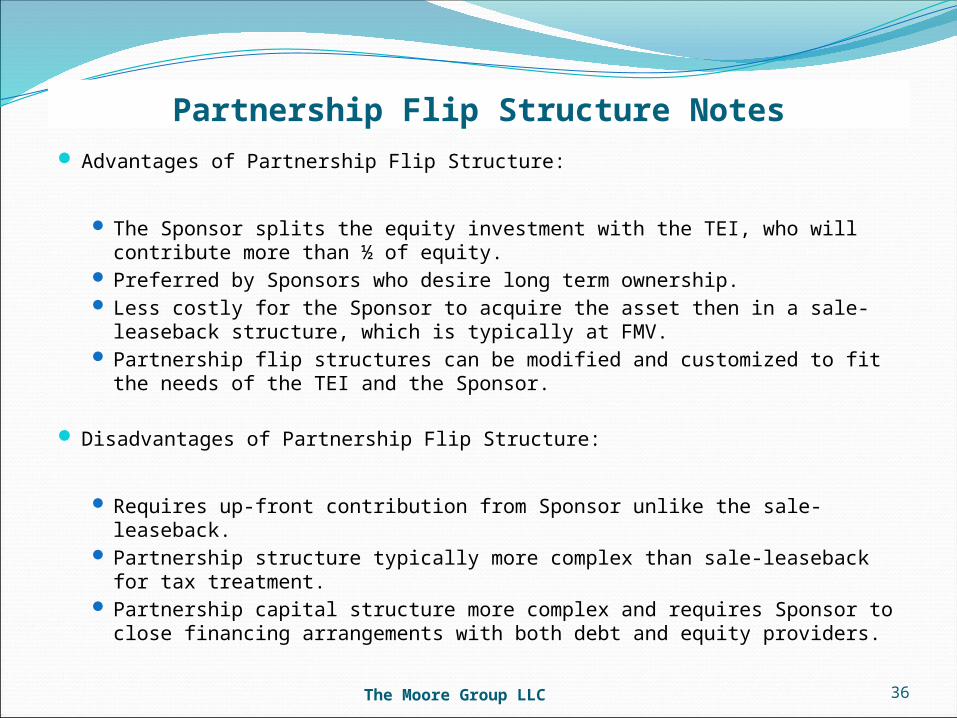

Partnership Flip Structure Notes Advantages of Partnership Flip Structure:

The Sponsor splits the equity investment with the TEI, who will contribute more than ½ of equity.

Preferred by Sponsors who desire long term ownership. Less costly for the Sponsor to acquire the asset then in a sale-leaseback

structure, which is typically at FMV. Partnership flip structures can be modified and customized to fit the

needs of the TEI and the Sponsor.

Disadvantages of Partnership Flip Structure:

Requires up-front contribution from Sponsor unlike the sale-leaseback. Partnership structure typically more complex than sale-leaseback for

tax treatment. Partnership capital structure more complex and requires Sponsor to

close financing arrangements with both debt and equity providers.

36The Moore Group LLC

Leveraged Partnership Flip Model (Post-Flip in Year 6)

Developer LenderTax EquityInvestor

Project Company

65% Equity35% Debt

UtilityPPA

ITC MACRS

Debt payments

Debt

PPA Payments

95% of free cash flow

Energy Delivery Tax credits

0.5% preferred return;5% of remaining cash flows

Sale Leaseback Model (Pre - Sale)

Developer Tax Equity Investor

Project Company

(100 % equity)

100% equityOwner

DevelopsProject

Cash for Project

Sale Leaseback Model (Post - Sale)

Developer Tax Equity Investor

Project Company

(100 % equity)

Lease Payments

100% ofCash flows

UtilityPPA

PPA Payments

Power Delivery ITC MACRS

100 % of tax credits

100% equity

100% tax benefits

OperatingCosts

Sale-Leaseback Notes

Advantages to Sponsor in Sale-Leaseback:

No up-front equity contribution. 100% financing Sponsor receives up-front cash flow in the form of asset sales,

establishes a track record and can undertake new project development opportunities.

Economic benefits are front-end loaded Ideal structure for poorly performing assets.

Disadvantages to Sponsor in Sale-Leaseback:

More costly than a partnership flip structure to buy out Lessor. Limited participation in project upside until early buy-out. Sacrifice of residual interest for up-front current cash flow.

40The Moore Group LLC

Execution Plan for Project Financing

41The Moore Group LLC

Execution Plan for Project Financing Project Financing will require a coordinated effort of approximately 16 months to

raise up to $1 billion.

Need for decisions on equipment and up-dated economic analysis .

Need to solidify PPA. PPA will become the critical path item for the financing this Spring.

Preparation of Information Memorandum (February – June 2012) Send out comprehensive overview of project, its economic profile, planned

equipment to be used, its unique characteristics, Sponsor, detailed summary of its contracts, most importantly the PPA and status on interconnect and all permits and licenses required for the construction and operation of the project.

Execution of Project Financing (July 2012 – April 2013) Negotiate with individual capital providers and decide on optimum capital

structure. Execute term sheets with all of the selected capital providers Execute inter-creditor agreement with all of the selected capital providers Minimize Sponsor’s at-risk capital prior to construction closing. Execute financial closing on the receipt of all necessary permits and licenses

42The Moore Group LLC

Key Decision Items

43The Moore Group LLC

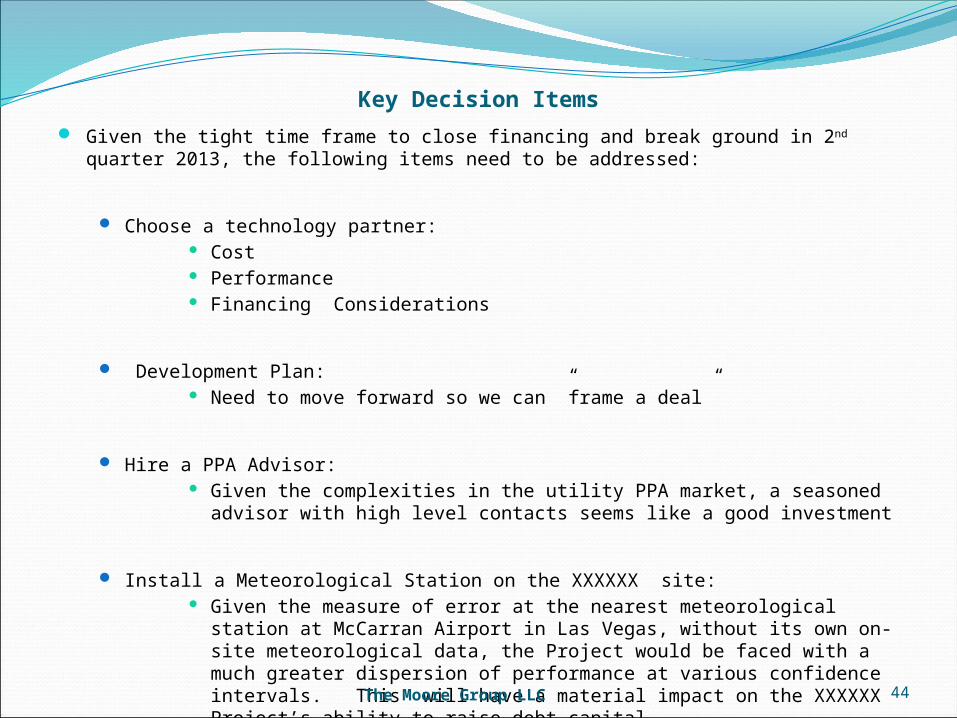

Key Decision Items Given the tight time frame to close financing and break ground in 2nd quarter 2013,

the following items need to be addressed:

Choose a technology partner: Cost Performance Financing Considerations

Development Plan: Need to move forward so we can ”frame a deal”

Hire a PPA Advisor: Given the complexities in the utility PPA market, a seasoned advisor

with high level contacts seems like a good investment

Install a Meteorological Station on the XXXXXX site: Given the measure of error at the nearest meteorological station at

McCarran Airport in Las Vegas, without its own on-site meteorological data, the Project would be faced with a much greater dispersion of performance at various confidence intervals. This will have a material impact on the XXXXXX Project’s ability to raise debt capital. 44The Moore Group LLC