finance case 2

DESCRIPTION

A simple ppt of a Corporate Finance Case StudyTRANSCRIPT

1

ExtraOrdinary General Meeting

OCTOBER 23, 2014

ExtraOrdinary General Meeting

2

1.BACKGROUND

2.GOVERNANCE STRUCTURE

3.TIMING

4.PRICING METHODOLOGY

5.RECOMMENDATIONS

6.CONCLUSION

SCOPE

ExtraOrdinary General Meeting

3

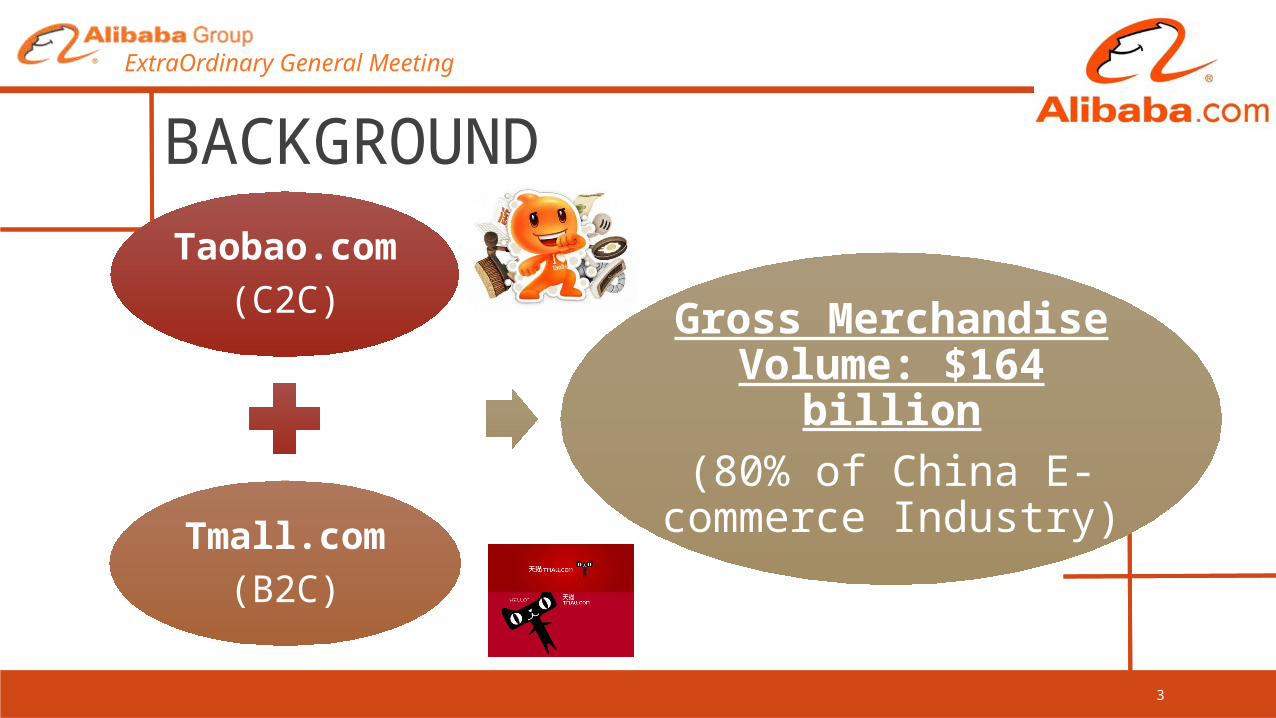

BACKGROUND

Taobao.com(C2C)

Tmall.com(B2C)

Gross Merchandise Volume: $164 billion

(80% of China E-commerce Industry)

ExtraOrdinary General Meeting

4

Online Payment System

Mobile Internet Services

Partnership with Internet Industry

Acquisitions in US Markets

Total Debt : $11.7 billionTotal Asset: $17.2 billion

Total Liabilities

Expected Benefits:

Total revenue: $8.6 billionNet Income: $3.5 billion

Expansions & Acquisitions

ExtraOrdinary General Meeting

5

• Estimates by Analysts:• 612 millions of Chinese Internet users in

2014• 25% of China’s retail market will be occupied

by online retailers by 2028

• Major Domestic Competitors:• Tencent: A market capitalization of $149

billion

• Baidu: 80% of China’s search market

Market & Competitors

ExtraOrdinary General Meeting

6

Hong Kong (HKEx):

Pros:o Being the home market for Mainland Chinao Having the title of raising the largest IPO in the world since 2010o Current listing technology firms constitute about 7% of all the firmso Daily Trade Volume $64 Million

Cons:o Dwindling demands of investors due to weaker market sentimento Stringent restriction and regulations for listingo Catered to Retail Investors

The Stock Exchange

ExtraOrdinary General Meeting

7

US market: Highest market capitalization of listed firms, with strong bullish sentiment amongst investors

NYSE NASDAQ

Average Daily Trade Volume $58 million $33 million

Technology Firm Proportion 5.54% 16.34%

Positive Policies for Attracting Technology Firms

Not Requiring two years of profitability for any

company listed

NASDAQ Private Market: a platform for private

companies to trade on

The Stock Exchange

ExtraOrdinary General Meeting

8

What is the partnership structure?

One share, one vote. Right to nominate majority of the Board, subject to approval of shareholders.

Right to appoint an interim Board, not subject to approval of shareholders.

GOVERNANCE STRUCTURE

ExtraOrdinary General Meeting

9

“This structure is our solution for preserving the culture shaped by our founders while at the same time accounting for the fact that founders will

inevitably retire from the company.”

Culture

ExtraOrdinary General Meeting

10

Culture

ExtraOrdinary General Meeting

11

Discounting of shares due to a dual class structure tends to “disappear in bull markets or when investors perceive they have an opportunity to co-invest

alongside a business or tech luminary”

Deloitte

Valuation

ExtraOrdinary General Meeting

12

Agency Costs of Equity

Agency Problems

Agency Costs Litigation Costs Insurance Costs

ExtraOrdinary General Meeting

13

“An IPO is significant in the life cycle of a company,

but when is the right time?”

TIMING

ExtraOrdinary General Meeting

14

Future acquisitions of firms that provide synergies Increasing Liabilities Opportune for restructuring Prevents debt eroding value

Expansion Opportunities

ExtraOrdinary General Meeting

15

Investment ClimateInvestors’ appetite to risk correlates to investment climate

Post Subprime Recession Improved Market Indices Overly optimistic Investors

DJI NASDAQ S&P 500 HSI

ExtraOrdinary General Meeting

16

Financial StabilityStrong financial stability is associated with increased demand and valuation

Asset Size of $17,222 Million Expected Revenue in 2014 of $8.6 Billion Matured operations (15 years) As of December 31, 2013

(in millions)

Cash and cash equivalent 7,876 Current bank borrowings 193

Investment securities 2,463 Secured borrowings 1,429

Property and equipment

(net)

961 Redeemable preference

shares

-

Goodwill and intangible

assets

2,131 Non-current bank borrowings 4,862

Total liabilities 11,712

Convertible preference shares 1,647

Others 20

Total mezzanine equity 1,667

Total equity 3,843

Total assets 17,222 Total liabilities and equity 17,222

ExtraOrdinary General Meeting

17

PRICING METHODOLOGYMultiples of EBITDA

Estimation of Investors’ market valuation using EBITDA approximating cash flow

Benefits Readily available comparisons with industry competitors Determine the pricing differences between the two exchange Approximates cash flow relevant to investors Ignores forecast estimation based on assumptions

ExtraOrdinary General Meeting

18

Market Capitalization AnalysisHong Kong Exchange New York Exchange

Competitors Enterprise Value/EBITDA(ttm) Competitors Enterprise Value/EBITDA(ttm)

Tencent Holdings (China) 34.59 Amazon (US) 35.9

HC International (China) 30.07 EBay (US) 13.18

Kingsoft Corporation (China) 25.93 SINA (China) 16.73

China Binary Sale Technology Ltd

(China)

16.48 Baidu (China) 28.84

Industry Average 26.76 Industry Average 23.66

Alibaba Enterprise Value 102,685 million

Alibaba Enterprise Value 90,769 million

Alibaba Market Capitalization 98,849 million

Alibaba Market Capitalization 86,933 million

Capitalization was derived by taking Enterprise Value + Cash and Equivalent - Debts

ExtraOrdinary General Meeting

19

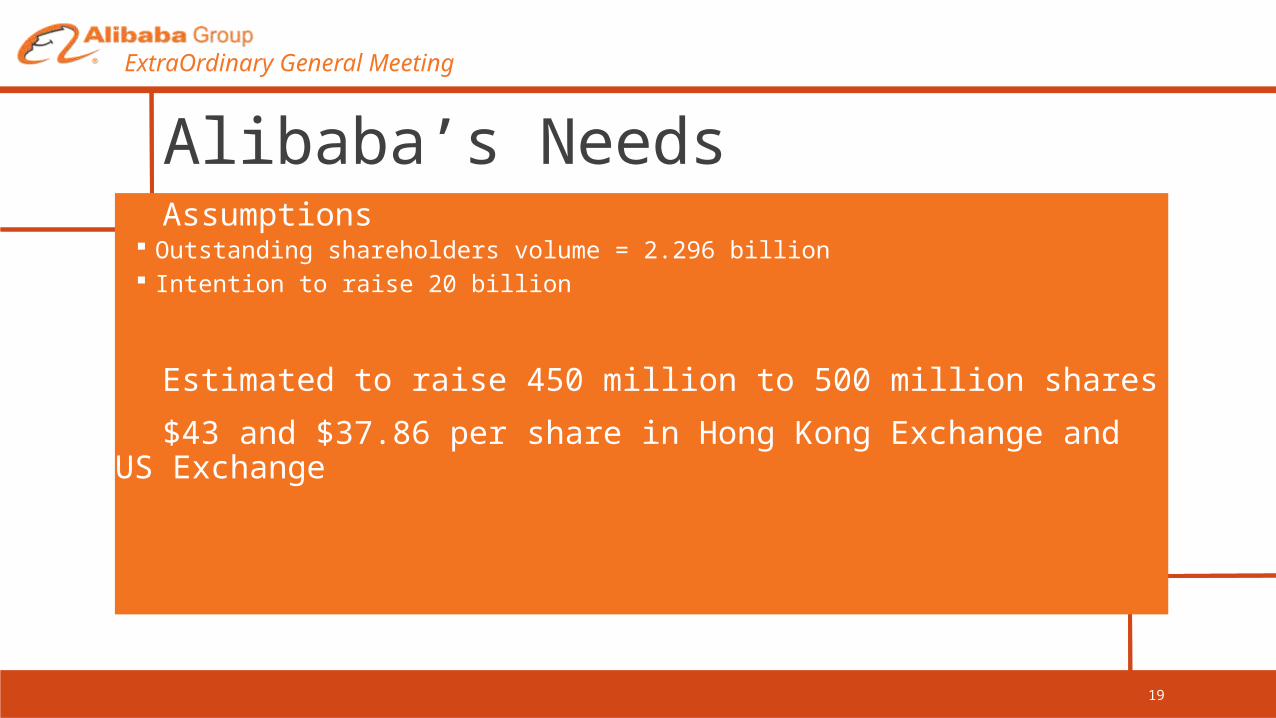

Alibaba’s NeedsAssumptions

Outstanding shareholders volume = 2.296 billion Intention to raise 20 billion

Estimated to raise 450 million to 500 million shares

$43 and $37.86 per share in Hong Kong Exchange and US Exchange

ExtraOrdinary General Meeting

20

Listing RequirementsNYSE HKEx NASDAQ

Market Capitalization

- HK$ 200 Million – HK$ 4 Billion

US$ 75 Million

Market Value of Public Share

US$ 60 Million HK$ 50 Million US$ 20 Million

Fulfils Listing Requirements No restrictions choosing between the 3 exchanges

ExtraOrdinary General Meeting

21

RECOMMENDATIONS

ExtraOrdinary General Meeting

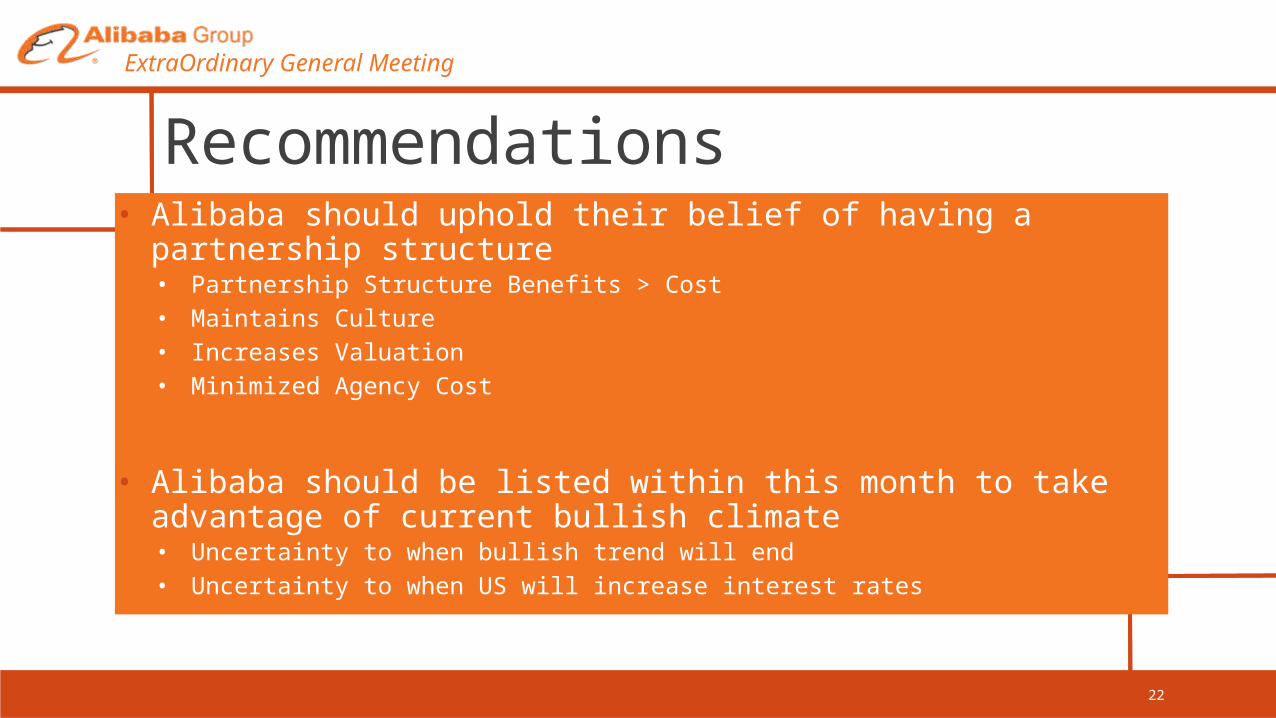

22

• Alibaba should uphold their belief of having a partnership structure• Partnership Structure Benefits > Cost• Maintains Culture• Increases Valuation• Minimized Agency Cost

• Alibaba should be listed within this month to take advantage of current bullish climate• Uncertainty to when bullish trend will end• Uncertainty to when US will increase interest rates

Recommendations

ExtraOrdinary General Meeting

23

• Optimal price per share in US is recommended to be higher than $45.43• Base Price per share was estimated at $37.86• Price did not account for value creation• Governance Structure• Larger Investor Exposure• Prolong Optimism in Market

• Optimistic Adjustment to pricing when needed

Recommendations

-50%

-45%

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5% 0% 5% 10%

15%

20%

25%

30%

35%

40%

45%

50%

0

10

20

30

40

50

60

0%, Base

Price against % Change Due to Other Variables

Price

ExtraOrdinary General Meeting

24

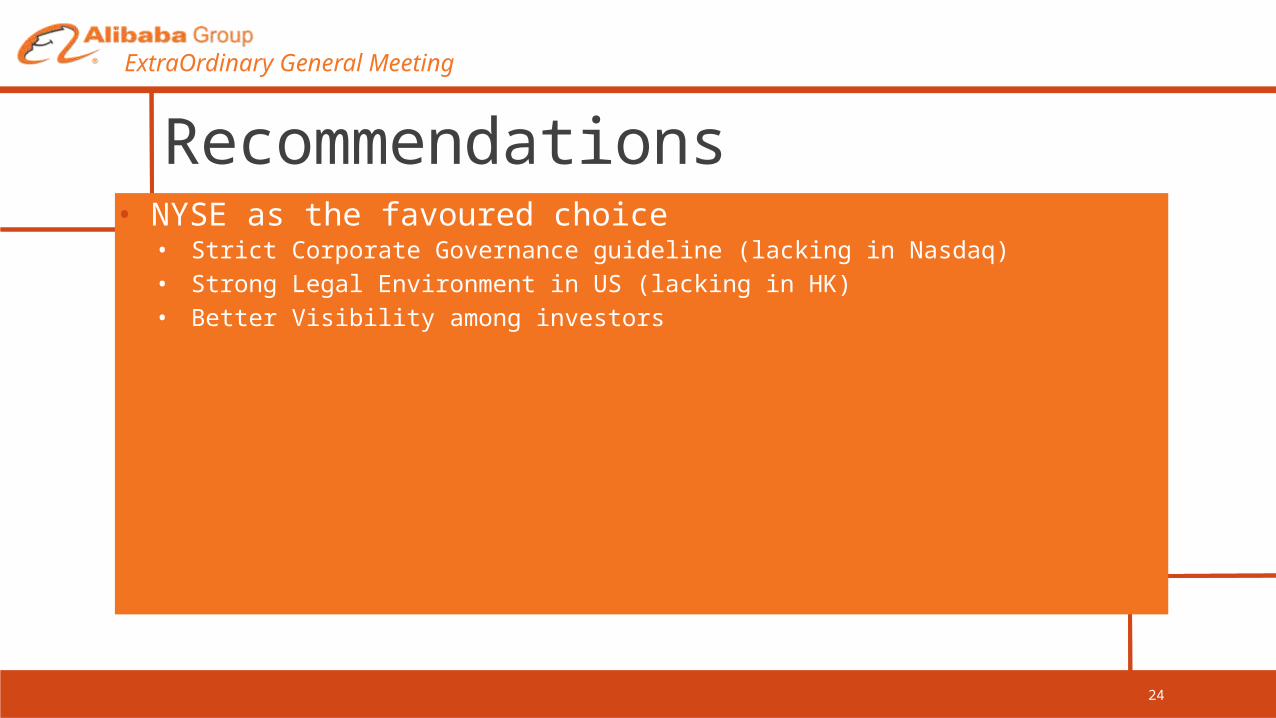

• NYSE as the favoured choice• Strict Corporate Governance guideline (lacking in Nasdaq)• Strong Legal Environment in US (lacking in HK)• Better Visibility among investors

Recommendations

ExtraOrdinary General Meeting

25

• Alibaba to follow through IPO now

• Alibaba to list on NYSE

• Alibaba to list with a minimum price of $45.43

CONCLUSION

ExtraOrdinary General Meeting

26

Thank You