finance education: what works? - open.ac.uk · pufin-mas project. #pufin @oubschool @truepotential_...

TRANSCRIPT

#PUFin @OUBSchool @TruePotential_ #FinCap17

True Potential PUFin Annual Conference

Church House Conference Centre

Tuesday 14 November 2017

Finance Education: What Works?

#PUFin @OUBSchool @TruePotential_ #FinCap17

WELCOME AND HOUSEKEEPING

Nigel Cassidy

Financial Journalist

#PUFin @OUBSchool @TruePotential_ #FinCap17

INTRODUCTION

Professor Janette Rutterford

Research Professor, True Potential PUFin,

The Open University Business School

The Money Advice Service

The journey from childhood skills to adult financial capability

Dr Gavan Conlon (London Economics)

Kirsty Bowman-Vaughan (Money Advice Service)

Tuesday 14th November 2017

The Money Advice ServiceThe Money Advice Service

1. Background

The journey from childhood skills to adult financial capability

5

The Money Advice Service

Project OverviewKey Aims

• To understand the relationship between CYP skills and adult financial outcomes

• To understand the relationship between adult financial outcomes and other adult outcomes

The journey from childhood skills to adult financial capability

6

The Money Advice Service

1970 British Cohort Study

• Covers 17,000 individuals born in England, Scotland and Wales in a single week of 1970

• Has tracked the same individuals over the last 47 years

• Contains information on health, physical, educational, social development, economic & labour market circumstances & other characteristics at different ages

• Previous research has found links between CYP skills and adult employment outcomes

The 1970 British Cohort Study does not cover today’s CYP

– in fact, some of them are parents of today’s CYP –

but provides a unique opportunity to explore the links between CYP skills and adult outcomes

The journey from childhood skills to adult financial capability

7

The Money Advice Service

Key indicators in BCS70

8

Cognitive skills

General intelligence tests

Literacy/reading

Numeracy

O Level performance

CYP skills (ages 5, 10, 16)

Behaviour

Agreeableness

Conscientiousness

Emotional health

Extraversion

Good conduct

Neuroticism

Non-cognitive skills

Academic self-concept

Challenge

Locus of control

Self-esteem

Self-control

Social skills

Unless stated otherwise, the analysis controls for childhood personal and socioeconomic characteristics (gender, ethnicity, household size, parents’ education & employment status, social class & family income, child rearing attitudes)

Financial outcomes

Regular saving

Pension saving

Debt/income ratio

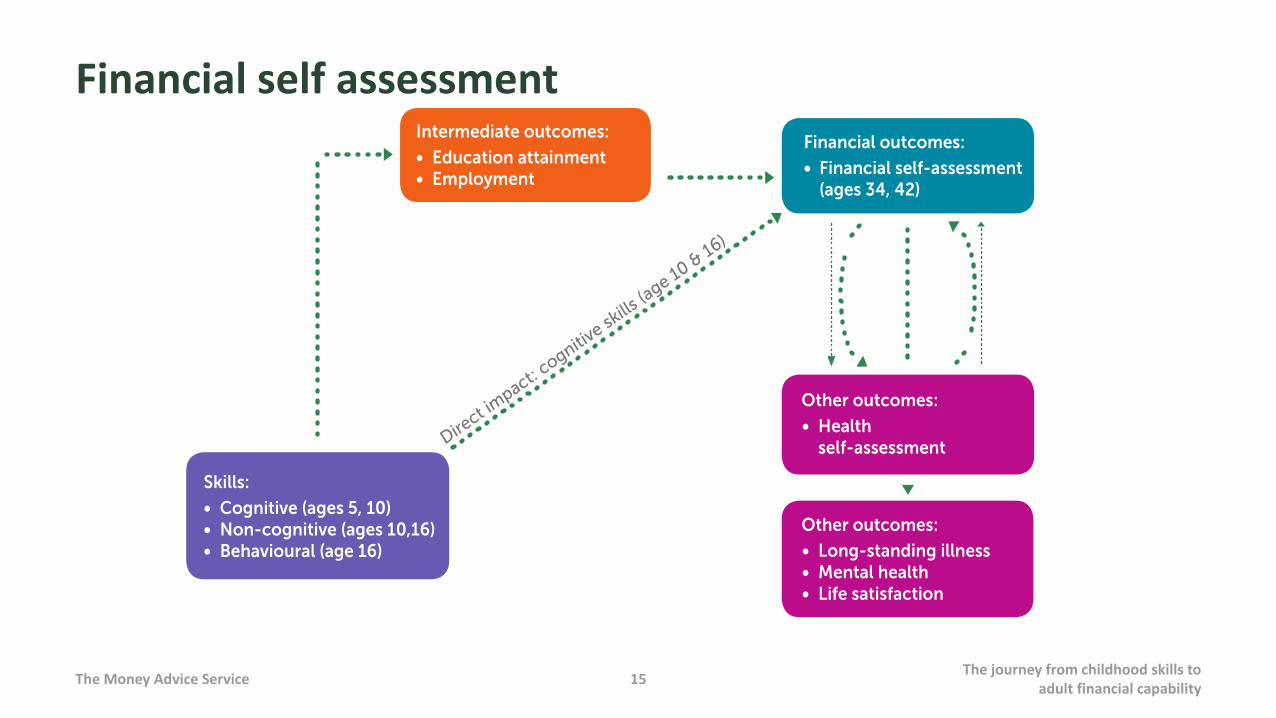

Financial self-assessment

Adulthood (ages 34, 42)

The journey from childhood skills to adult financial capability

The Money Advice ServiceThe Money Advice Service

2. Findings

The journey from childhood skills to adult financial capability

9

The Money Advice Service

CYP skills & financial outcomes

The journey from childhood skills to adult financial capability

10

The Money Advice Service

1970 British Cohort Study

11

Skill measureRegular saving

(age 34)Pension saving

(age 34)

Low debt-to-income ratio

(age 42)

Financial self-assessment

(age 42)

Age 5

Cognitive ability

Non-cognitive ability - - - - - - - - - - - - - - - - - - - - - - - Not captured - - - - - - - - - - - - - - - - - - - - - - -

Behavioural score

Age 10

Cognitive ability

Non-cognitive ability

Behavioural score

Age 16

Cognitive ability

Non-cognitive ability

Behavioural score

The journey from childhood skills to adult financial capability

The Money Advice Service

Role of intermediate outcomes

The journey from childhood skills to adult financial capability

12

Intermediate outcomes

Educationalattainment

Employment status

Income

Marital status

Home ownership

The Money Advice Service

Financial and other adult outcomes

The journey from childhood skills to adult financial capability

13

Other adultoutcomes

Health self-assessment

Mental health

Absence of long-standing

illness

Life satisfaction

The Money Advice Service

Pension saving

The journey from childhood skills to adult financial capability

14

The Money Advice Service

Financial self assessment

The journey from childhood skills to adult financial capability

15

The Money Advice ServiceThe Money Advice Service

3. Implications

The journey from childhood skills to adult financial capability

16

The Money Advice Service

The journey from childhood skills to adult financial

capability17

Key Aims

• Starting young matters

• It’s more than just cognitive skills

• Money doesn’t exist in isolation

• Improved targeting

• Improved content?

#PUFin @OUBSchool @TruePotential_ #FinCap17

Martin Upton

Director, True Potential PUFin,

The Open University Business School

Getting school-leavers ready for financial independence

(New course: Managing My Money for Young Adults)

#PUFin @OUBSchool @TruePotential_ #FinCap17

Building on the trilogy of free personal finance courses

Over 300,000 registrations

Now..Managing My Money for Young Adults

Kindly supported by the Chartered Accountants’ Livery Company Charity

#PUFin @OUBSchool @TruePotential_ #FinCap17

The clear need for help

- Our research - youngsters in debt

- FCA - young adults struggling with money

- StepChange - under 25s in growing trouble with debt

#PUFin @OUBSchool @TruePotential_ #FinCap17

Course covers timeline from 16 years

- Financial products- Budgeting at home and away from home- Financing higher education

#PUFin @OUBSchool @TruePotential_ #FinCap17

Course covers timeline from 16 years

- Living in a shared rental- Being smart in the market place- Borrowing sensibly- Planning for the future

#PUFin @OUBSchool @TruePotential_ #FinCap17

Three-year programme

- Course production- Launch and roll-out - Individual and classroom delivery- Assess effectiveness

#PUFin @OUBSchool @TruePotential_ #FinCap17

Here’s the coursehttp://www.open.edu/openlearn/money-business/managing-my-money-young-adults/content-section-overview

..and here’s the budgeting web-appwww.managingmybudget.com

#PUFin @OUBSchool @TruePotential_ #FinCap17

The mission to educate will continue….

- Bespoke courses targeting specific social groups- Financial education at the point of transacting

- And learning from our testing of ‘what works’

#PUFin @OUBSchool @TruePotential_ #FinCap17

Jeanette Makings

Close Brothers Asset Management

SESSION 1 DISCUSSANT

Head of Financial Education Services,

#PUFin @OUBSchool @TruePotential_ #FinCap17

Facilitator: Nigel CassidyDr Gavan Conlon

PANEL DISCUSSION AND Q&A

Kirsty Bowman-VaughanMartin Upton

Jeanette Makings

Jonquil Lowe

#PUFin @OUBSchool @TruePotential_ #FinCap17

Please return to your seats by 14:45

COFFEE BREAK

#PUFin @OUBSchool @TruePotential_ #FinCap17

Will Brambley

Research Associate, True Potential PUFin,

The Open University Business School

Financial capability for Just About Managing (JAMs): results of

PUFin-MAS project

#PUFin @OUBSchool @TruePotential_ #FinCap17

Adults who most need financial education don’t look for it• Prevention is better than cure: it’s much easier to prevent financial difficulties than get

out of them

• Finance is boring: people don’t look for help until something triggers them to engage,

usually a negative shock putting them into difficulty

• Fin Ed appeals to the financially capable: those interested enough to seek it out already

doing ok

• Reaching those who most need help tends to require expensive and intensive

interventions

Stylised Fact #1

#PUFin @OUBSchool @TruePotential_ #FinCap17

Resilience is vital but most people are Just About Managing

• 80% do not have recommended 3 months’ income saved to weather redundancy or

illness

• 35-50% aren’t saving anything

• 25% have negative financial wealth & could withstand no shock

• £1000 in household savings would stop half of all problem debt from occurring –

500,000 per year

Stylised Fact #2

#PUFin @OUBSchool @TruePotential_ #FinCap17

The problem is more psychology than knowledge

• If you ask people what proportion of their income they should save for a rainy

day, what’s the most common answer?

– 10%

• Most people know ‘the right thing’ to do

• Most people don’t do what they think is ‘the right thing’

Stylised Fact #3

#PUFin @OUBSchool @TruePotential_ #FinCap17

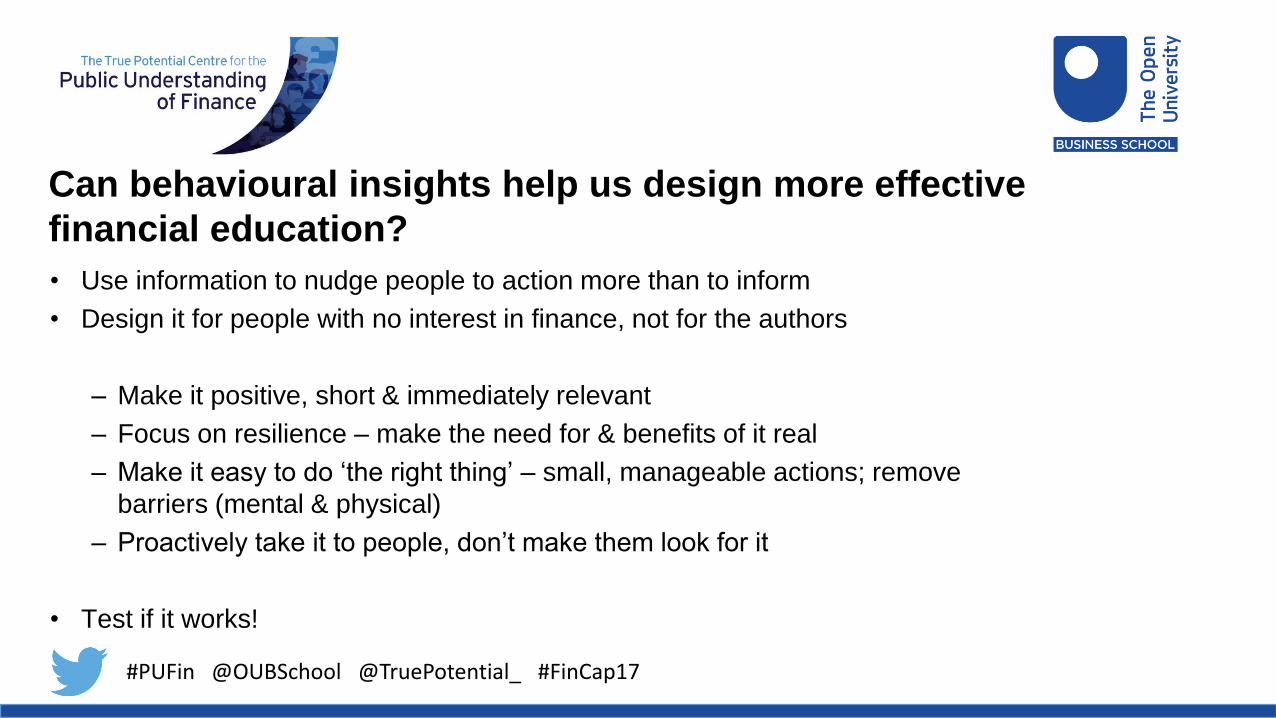

Can behavioural insights help us design more effective

financial education?

• Use information to nudge people to action more than to inform

• Design it for people with no interest in finance, not for the authors

– Make it positive, short & immediately relevant

– Focus on resilience – make the need for & benefits of it real

– Make it easy to do ‘the right thing’ – small, manageable actions; remove

barriers (mental & physical)

– Proactively take it to people, don’t make them look for it

• Test if it works!

#PUFin @OUBSchool @TruePotential_ #FinCap17

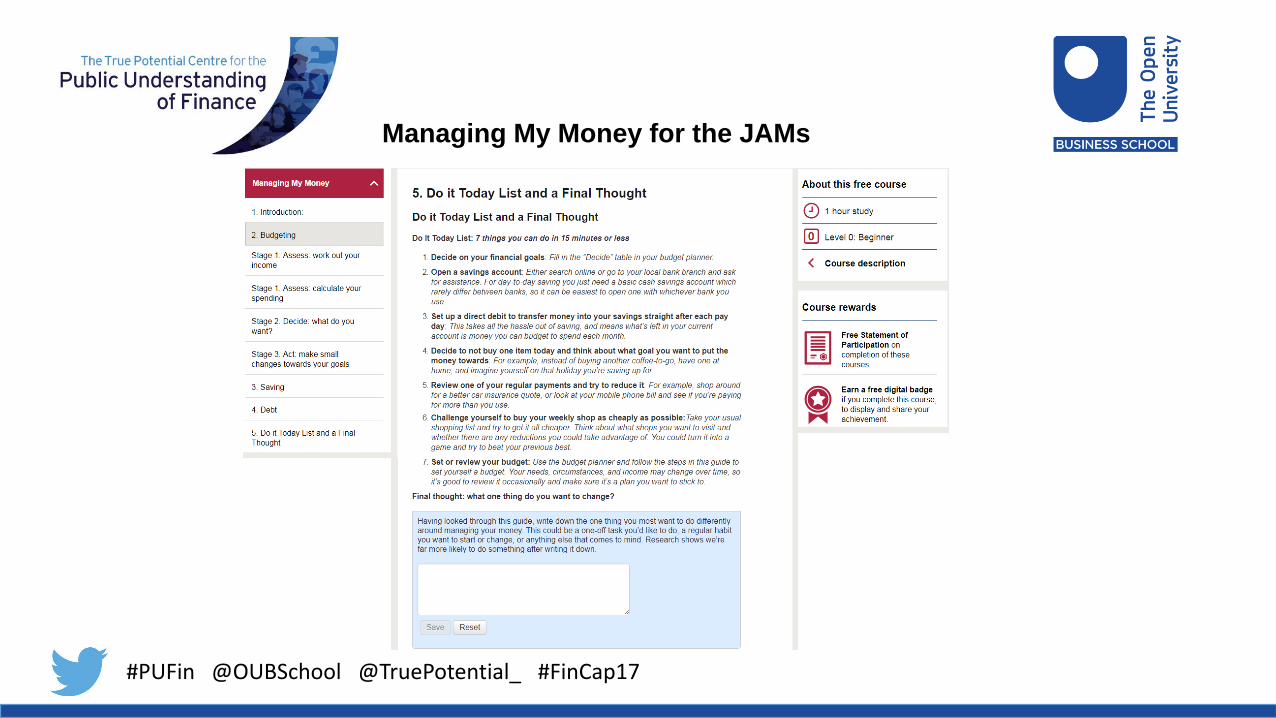

Managing My Money for the JAMs

#PUFin @OUBSchool @TruePotential_ #FinCap17

Managing My Money for the JAMs

#PUFin @OUBSchool @TruePotential_ #FinCap17

Has it worked?

• To soon to tell conclusively – small sample with before & after data

• Those who take it seem to increase use of budgeting & reduce missed/bounced

payments significantly, with moderate increase in regular savings

• Bigger impact on behaviour & smaller impact on confidence than previous

research on original Managing My Money course – matching the changed focus

of the tool

BUT

• Very few engage without personal contact

#PUFin @OUBSchool @TruePotential_ #FinCap17

Can we nudge people to act before they hit difficulty?

Yes, if we can get them to engage

• Behaviourally-informed techniques seem to work for those who do engage

– We can nudge people to act if we can get a tool to them

• A preliminary theme from this & other What Works Fund projects: no clear link between better tools & more

people using them

– Not “build it and they will come”

• Need to test more behavioural techniques to get people to use it:

– Follow-ups & more intensive communication

– Personal & social links: word of mouth & social media

– Do we need the “incessant & intrusive” style of notifications apps often employ to get us to use them?

#PUFin @OUBSchool @TruePotential_ #FinCap17

Helen White

Head of Financial Capability, Money Advice Service

Putting it into context: the financial capability strategy for the UK

BUILDING A FINANCIALLY RESILIENT AND FINANCIALLY SECURE POPULATION

The True Potential PUFin Conference, 14th November 2017

Mick McAteer, The Financial Inclusion Centre, www.inclusioncentre.org.uk

The Financial Inclusion

CentreFinancial services that work

for society, not the few

CONTENTS

• Why building financial resilience and financial security is one of the most important public policy challenges facing UK

• The causes of financial exclusion and underprovision – and why it is likely to get worse, not better

• What can we do about it – including a realistic assessment of role of financial capability and fintech

FINANCIAL RESILIENCE AND FINANCIAL SECURITY ROADMAP

The journey to financial resilience and longer term financial security

Stage Financial vulnerability/

insecurity

‘Square one’ Financial resilience Financial security

Definition Consumers in a ‘negative’

position, vulnerable and

exposed to shocks/ detriment

Consumers back to a ‘neutral’

position-still vulnerable but with

platform to build on

Ability to withstand financial

shocks/meet short term

financial needs

Sufficient means to meet

medium-long term financial

needs

Main factors Restricted access to

transactional bank account

Overindebted/ vulnerable to

subprime lending/trapped in

vicious cycle

No savings

Exposed to risk, no/little

insurance cover

No pension/ underpensioned

Housing problems,

mortgage/rent arrears

Low/unstable incomes, poverty

Poverty ‘premium’/ paying more

for basic goods and services

Effective budgeting/’making ends

meet’ (if possible- as may be outside

control)

In the financial system (functional

bank account)

Paid off unmanageable/

unproductive debt

Still underinsured/ underpensioned

Income surplus

Effective use of banking system

Emergency savings (3 mths

income)

Access to fair, affordable credit

Basic insurance cover

Some form of ‘safety net’

Beginnings of pension

provision/but still

underprovided for

Proper insurance cover, not just

for contents but income

replacement

Paying off/paid mortgage

Significant pension provision

Long term savings/ asset

accumulation

Debt/assets lifecycle model

positive territory

HOW FAR BACK ARE WE STARTING?

• 71% of households received unexpected bill last year (£200-£400) –

• 51% of ‘struggling’ households were able to use savings/ not have to cut back; but 42% had to cut back/ borrow/ couldn’t pay; 7% couldn’t recall (MAS)

• 11.6m (23% of adults) ‘struggling’ (struggle to keep up with bills, find it hard to build up savings buffer);

• 12.7m (25% of adults) ‘squeezed’ (significant financial commitments, little provision for income shocks) (MAS)

HOW FAR BACK ARE WE STARTING?

• 8 million overindebted (debt is a heavy burden, missed bills/ credit commitments in 3 of last 6 months) (MAS)

• Lower income households pay a ‘poverty premium’ of £490 a year (JRF)

• Some signs of deleveraging but unsecured credit appears to be growing again, now £200bn, low base rates conceals problems

HOW FAR BACK ARE WE STARTING?

• Credit card margins=17.7% (10.9% 5 years pre crisis), Overdraft margins=19.5% (11.6% 5 yrs pre crisis), ‘high risk’ borrowers paying up to 50% for credit cards, unauthorised O/Ds higher APRs than payday loans (Financial Inclusion Centre)

• Have to confront fact that much debt may not be ‘repaid’, 5.1m credit card a/cs will take 10 years to pay off debts (assuming no further borrowing) (FCA)

HOW FAR BACK ARE WE STARTING?

• Savings ratio falling again, 1/2 households < £1,500

• Savings ratios (10 yr avg) -‘Anglo-Saxon’ countries: 0.2%; Continental Social Model (CSM): 8% (Euro area: 8.8%); ‘Family-centric’: 3.1% (Financial Inclusion Centre)

• Half of lower income households don’t have home contents insurance, compared to 1 in 5 of households on average incomes (Financial Inclusion Commission)

HOW FAR BACK ARE WE STARTING?

• Only 1 in 10 households have income/mortgage protection insurance (CII)

• Worrying levels of pension underprovision in key groups eg self-employed – 16% contributing (17% men/ 12% women), UK private pensions coverage heavily skewed towards 1st/ 2nd income deciles (FRS)

• Net wealth of UK households tripled since 1995, increase of £7trn,three-quarters(£5trn) accounted for by housing stock – huge intergenerational transfer of wealth (ONS)

HOW FAR BACK ARE WE STARTING?

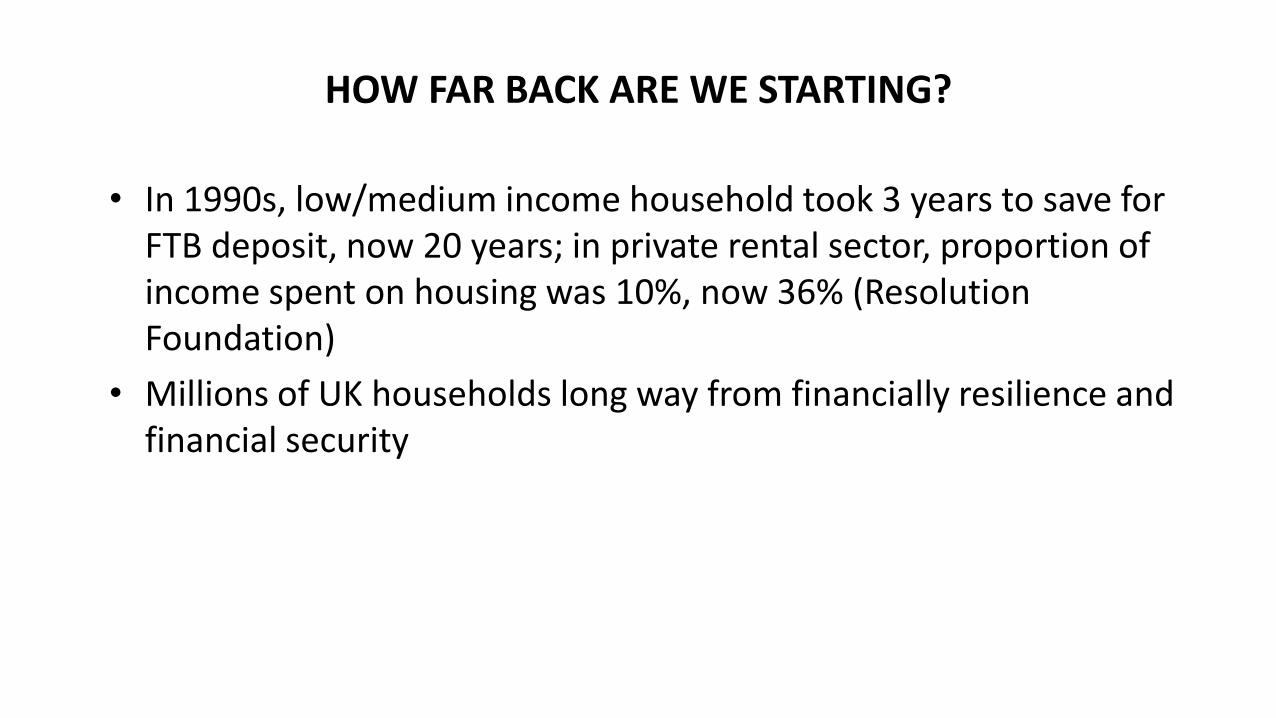

• In 1990s, low/medium income household took 3 years to save for FTB deposit, now 20 years; in private rental sector, proportion of income spent on housing was 10%, now 36% (Resolution Foundation)

• Millions of UK households long way from financially resilience and financial security

CAUSES OF FINANCIAL EXCLUSIONAND UNDERPROVISION - SOCIOECONOMIC

• Cause of financial exclusion and underprovision complex, but three broad categories – socio-economic, supply side and demand side (inc consumer confidence and financial capability)

• Appalling performance on wage growth, average real wages -5% 2007-15, 2nd worse in OECD after Greece, 103/112 globally, biggest squeeze in earnings since Napoleonic times

• Growth in zero hours/ temporary work, self-employment – less predictable earnings

CAUSES OF FINANCIAL EXCLUSIONAND UNDERPROVISION - SOCIOECONOMIC

• Housing market changes, wealth inequalities

• Major regional differences in GVA, incomes post crisis – in most regions GVA per head and disposable incomes still not recovered

• Overindebtedness/ low savings ratio

CAUSES OF FINANCIAL EXCLUSIONAND UNDERPROVISION - SOCIOECONOMIC

• No real sign of improvement eg. earnings squeeze set to continue until 2022, expected to still be £22 a week (in real terms) below pre-crisis levels

• Welfare reforms have/ will have huge impact on lower/medium income households

• If we get Brexit wrong, the impacts will be even more severe

CAUSES OF FINANCIAL EXCLUSION AND UNDERPROVISION – SUPPLY SIDE

• Sad fact is financial services industry (esp savings/ investment) little direct relevance for millions of households

• Many households are not economically viable for commercial financial services providers – to be precise, cannot sell products on terms which make sense for the industry and consumers

• Bigger question to confront: is it possible to make decent profits fairly from lower income households?

CAUSES OF FINANCIAL EXCLUSION AND UNDERPROVISION – SUPPLY SIDE

• This will be more difficult in the new economic and financial reality – low rates, low returns, low costs are critical

• Became too easy to borrow, too hard to save

• Regulation has not created exclusion, it has exposed the true cost of doing business fairly, demands no more than would be expected of a well run business

CAUSES OF FINANCIAL EXCLUSION AND UNDERPROVISION – SUPPLY SIDE

• Fintech/ Big Data will improve economics for some consumer groups but will also exacerbate financial exclusion for greater numbers (segmentation associated with greater exclusion, easier to identify lower risk/ more profitable consumers)

• Culture gap emerging between experienced professionals who run firms and younger, more impatient innovators who develop fintech (source of misselling)

CAUSES OF FINANCIAL EXCLUSIONAND UNDERPROVISION – DEMAND SIDE

• Clear majority of consumers in recent survey have little/ no confidence that CEOs/ NEDs of financial services firms

– Put customers’ interests first

– Intend to treat them fairly

– Encourage ethical behaviour in the firm they run (see Annex for details of 3R Insights survey)

CAUSES OF FINANCIAL EXCLUSIONAND UNDERPROVISION – DEMAND SIDE

• Financial capability involves consumers having the: awareness of need to act; propensity to act; confidence to engage; capacity to make effective plans, decisions and choices, and act; and diligence to monitor and review plans

• But evidence shows that encouragement/financial capability interventions limited impact on changing demand side behaviours (that’s why needed AE/NEST)

CAUSES OF FINANCIAL EXCLUSIONAND UNDERPROVISION – DEMAND SIDE

• Commercial advice sector/ providers (which play critical role in persuading consumers to change behaviours) unable to serve large parts of the market (see previous slide)

• Pensions ‘freedom and choice’ will reverse progress made through AE/ NEST – AE filling the ‘pool’ of retirement savings, freedom and choice drains that pool of savings, pushes up cost of saving, exposes consumers to even greater risks

WHAT CAN WE DO ABOUT IT?

• No question, face huge challenges if we want to build financially resilient and secure households

• Need to address each of the major causes – socio-economic, supply side, demand side

• Economic policy outside scope of this speech but clearly government could do much:

– ease impact of welfare cuts

– reform pensions tax relief use savings to boost pensions of low income/ self-employed

– increase AE contribution rates

WHAT CAN WE DO ABOUT IT?

• Supply side reforms must include:

– FCA driving through efficiency gains in asset management (37% operating margins, 2nd highest after real estate)

– default decumulation option

– change balance of regulation to make it more difficult to borrow, easier to save

WHAT CAN WE DO ABOUT IT?

• On demand side, fintech will help some consumers, fincapps could help guide consumers into better decisions and choices, but of limited benefit, we have analogue regulation for digital finance world

• The new single financial guidance body has to work this time, there is no other realistic option for consumers who are not viable for commercial providers

ANNEXES

key findings from 3R Insights survey with Opinium, see www.3r-insights.com

CONSUMERS’ VIEWS ON FINANCIAL LEADERS (CEOs/ DIRECTORS)To what extent do they care about providing value for money?

All 18-34 >55Reasonable/

great extent

%

Little/ poor

extent

%

Reasonable/

great extent

%

Little/ poor

extent

%

Reasonable/

great extent

%

Little/ poor

extent

%

Insurers 17 70 21 60 15 76

Banks 18 70 26 57 15 78

Investment

Firms 22 63 26 53 20 68

CONSUMERS’ VIEWS ON FINANCIAL LEADERS (CEOs/ DIRECTORS)To what extent do they care about quality of service?

All 18-34 >55

Reasonable/

great extent %

Little/ poor

extent

%

Reasonable/

great extent %

Little/ poor

extent

%

Reasonable/

great extent %

Little/ poor

extent

%

Insurers 26 62 29 51 25 68

Banks 30 59 37 44 26 67

Investment

Firms 28 57 34 45 28 61

CONSUMERS’ VIEWS ON FINANCIAL LEADERS (CEOs/ DIRECTORS)Confidence that will put customers’ interests first

All 18-34 >55Some/

complete

confidence %

Little/ no

confidence %

Some/

complete

confidence %

Little/ no

confidence %

Some/

complete

confidence %

Little/ no

confidence %

Insurers 21 69 23 60 22 72

Banks 22 68 29 54 21 74

Investment

Firms 21 68 24 57 20 70

CONSUMERS’ VIEWS ON FINANCIAL LEADERS (CEOs/ DIRECTORS)Confidence that will treat customers fairly

All 18-34 >55Some/

complete

confidence %

Little/ no

confidence %

Some/

complete

confidence %

Little/ no

confidence %

Some/

complete

confidence %

Little/ no

confidence %

Insurers 24 66 28 57 24 70

Banks 28 63 34 52 27 67

Investment

Firms 25 62 29 53 24 66

CONSUMERS’ VIEWS ON FINANCIAL LEADERS (CEOs/ DIRECTORS)Extent to which ethical behaviour is encouraged

Overall 18-34 >55

Reasonable/

great extent %

Little/ poor

extent

%

Reasonable/

great extent

%

Little/ poor

extent

%

Reasonable/

great extent

%

Little/ poor

extent

%

Insurers 24 58 31 48 20 64

Banks 25 58 34 46 20 65

Investment

Firms 24 56 31 46 20 62

#PUFin @OUBSchool @TruePotential_ #FinCap17

Facilitator: Nigel Cassidy

Will Brambley

PANEL DISCUSSION AND Q&A

Helen WhiteMick McAteer

TECHNOLOGY IN FINANCE

Dr. Jamie Godwin

Lead Data Scientist, True Potential

14th November 2017

OVERVIEW

• What is “Technology in finance”?

• Why do we care?

• How are True Potential making a difference?

TECHNOLOGY IN FINANCE

• Anything that empowers clients to make better decisions

or improves their outcomes.

WHY DO WE CARE?

• People don’t make rational decisions!

THE SAVINGS GAP• Over 50% of UK workers have a poor understanding of

savings.

• 1 in 5 have less than a months worth of expenses saved.

• On average, people waste £143 per month they later

regret.

AUTO ENROLMENT• 22 year old

Pot: ~£309,000, approximately £15,450 income per

annum.

• 30 year old

Pot: ~£191,000, or approximately £9,600 income per

annum.

• 40 year old

Pot: ~£100,000, or approximately £5,000 income per

annum.

All of these are below the £23,000 needed to live

comfortably in retirement.

TECHNOLOGY: MAKING UP THE DIFFERENCE

• Lower the barriers to entry

• Help clients determine where they are

• Help clients determine where they want to be

• Do it on autopilot

£1

PENSIONS DASHBOARD

#PUFin @OUBSchool @TruePotential_ #FinCap17

Liz Moody

The Open University Business School

SESSION 3 DISCUSSANT

Senior Lecturer, Executive Education

#PUFin @OUBSchool @TruePotential_ #FinCap17

Facilitator: Nigel CassidyDr Jamie Godwin

PANEL DISCUSSION AND Q&A

Liz Moody

#PUFin @OUBSchool @TruePotential_ #FinCap17

CLOSING COMMENTS

Professor Janette Rutterford

Research Professor, True Potential PUFin,

The Open University Business School

#PUFin @OUBSchool @TruePotential_ #FinCap17

True Potential PUFin Annual Conference 2017

Thank you

Please join us for drinks and canapés

Finance Education: What Works?