finance shared services benchmark highlights - … · leveraged apqc’s benchmarking methodology...

TRANSCRIPT

Copyright © 2015 ScottMadden, Inc. All rights reserved. Report _2015

Finance Shared Services Benchmark

Highlights

2015 ScottMadden Finance Shared Services Benchmarking

Study

January 2016

Copyright © 2015 by ScottMadden, Inc. All rights reserved.

About the Survey

Survey Project and Timeline

■ Identified gaps in Finance Shared Services performance benchmarks

■ Engaged APQC to conduct custom study; ScottMadden designed questions

• First cycle – spring/summer 2014

• Second cycle – spring/summer 2015

■ Leveraged APQC’s benchmarking methodology and member network

Survey scope covers four major areas:

Introduction

1

Scope of Services

Performance

Delivery Model

Staffing

16 Metrics, 26 Qualitative Questions

Copyright © 2015 by ScottMadden, Inc. All rights reserved.

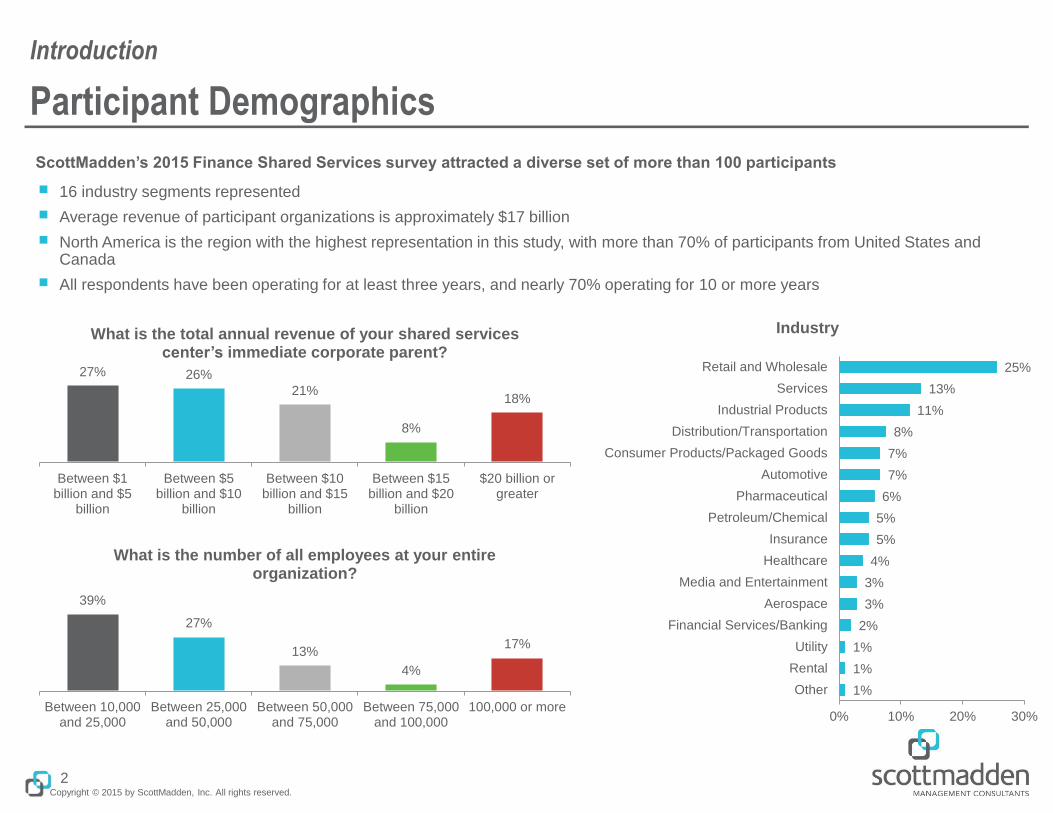

Participant Demographics

ScottMadden’s 2015 Finance Shared Services survey attracted a diverse set of more than 100 participants

■ 16 industry segments represented

■ Average revenue of participant organizations is approximately $17 billion

■ North America is the region with the highest representation in this study, with more than 70% of participants from United States and Canada

■ All respondents have been operating for at least three years, and nearly 70% operating for 10 or more years

Introduction

2

1%

1%

1%

2%

3%

3%

4%

5%

5%

6%

7%

7%

8%

11%

13%

25%

0% 10% 20% 30%

Other

Rental

Utility

Financial Services/Banking

Aerospace

Media and Entertainment

Healthcare

Insurance

Petroleum/Chemical

Pharmaceutical

Automotive

Consumer Products/Packaged Goods

Distribution/Transportation

Industrial Products

Services

Retail and Wholesale

Industry

27% 26%

21%

8%

18%

Between $1billion and $5

billion

Between $5billion and $10

billion

Between $10billion and $15

billion

Between $15billion and $20

billion

$20 billion orgreater

What is the total annual revenue of your shared services center’s immediate corporate parent?

39%

27%

13%

4%

17%

Between 10,000and 25,000

Between 25,000and 50,000

Between 50,000and 75,000

Between 75,000and 100,000

100,000 or more

What is the number of all employees at your entire organization?

Copyright © 2015 by ScottMadden, Inc. All rights reserved.

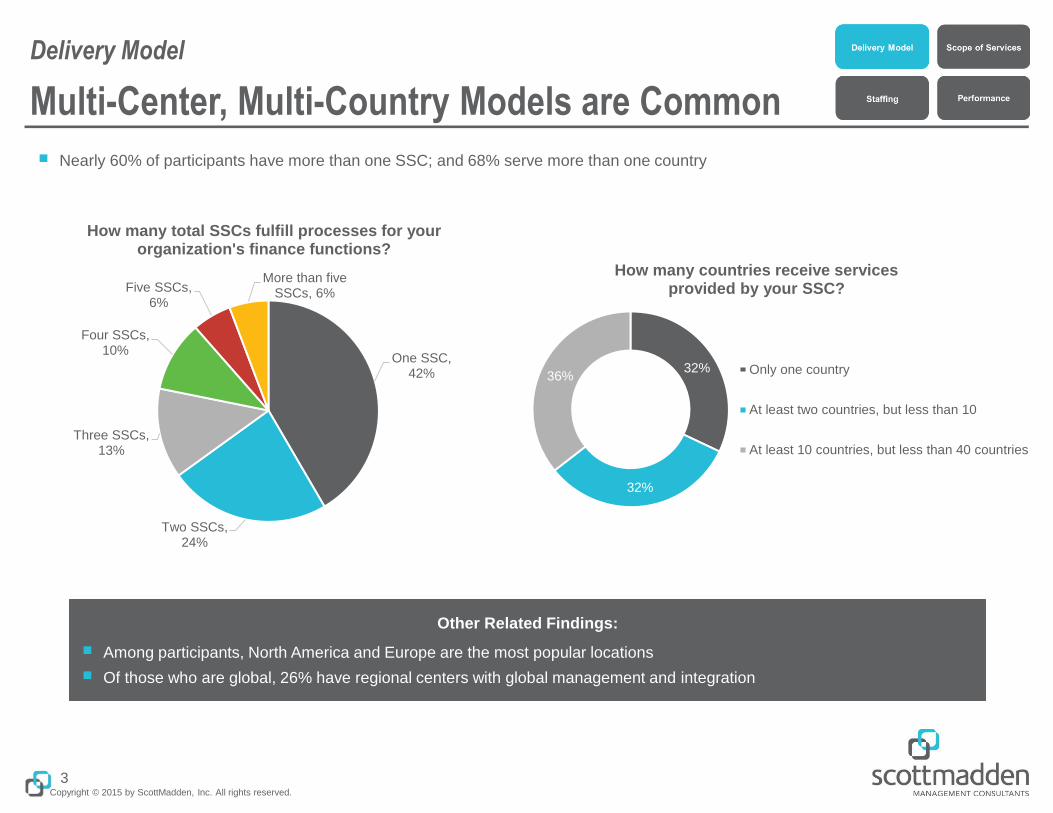

Multi-Center, Multi-Country Models are Common

■ Nearly 60% of participants have more than one SSC; and 68% serve more than one country

Delivery Model

3

One SSC, 42%

Two SSCs, 24%

Three SSCs, 13%

Four SSCs, 10%

Five SSCs, 6%

More than five SSCs, 6%

How many total SSCs fulfill processes for your organization's finance functions?

32%

32%

36%

How many countries receive services provided by your SSC?

Only one country

At least two countries, but less than 10

At least 10 countries, but less than 40 countries

Other Related Findings:

■ Among participants, North America and Europe are the most popular locations

■ Of those who are global, 26% have regional centers with global management and integration

Copyright © 2015 by ScottMadden, Inc. All rights reserved.

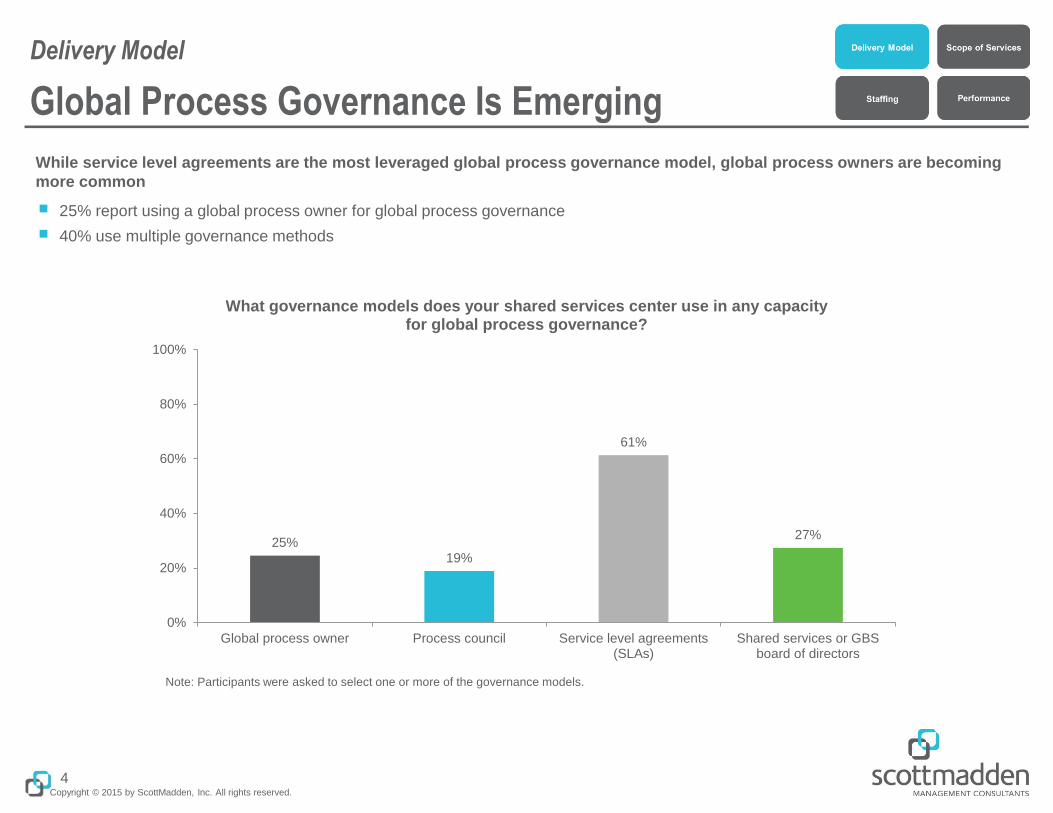

Global Process Governance Is Emerging

While service level agreements are the most leveraged global process governance model, global process owners are becoming

more common

■ 25% report using a global process owner for global process governance

■ 40% use multiple governance methods

Delivery Model

4

25% 19%

61%

27%

0%

20%

40%

60%

80%

100%

Global process owner Process council Service level agreements(SLAs)

Shared services or GBSboard of directors

What governance models does your shared services center use in any capacity for global process governance?

Note: Participants were asked to select one or more of the governance models.

Copyright © 2015 by ScottMadden, Inc. All rights reserved.

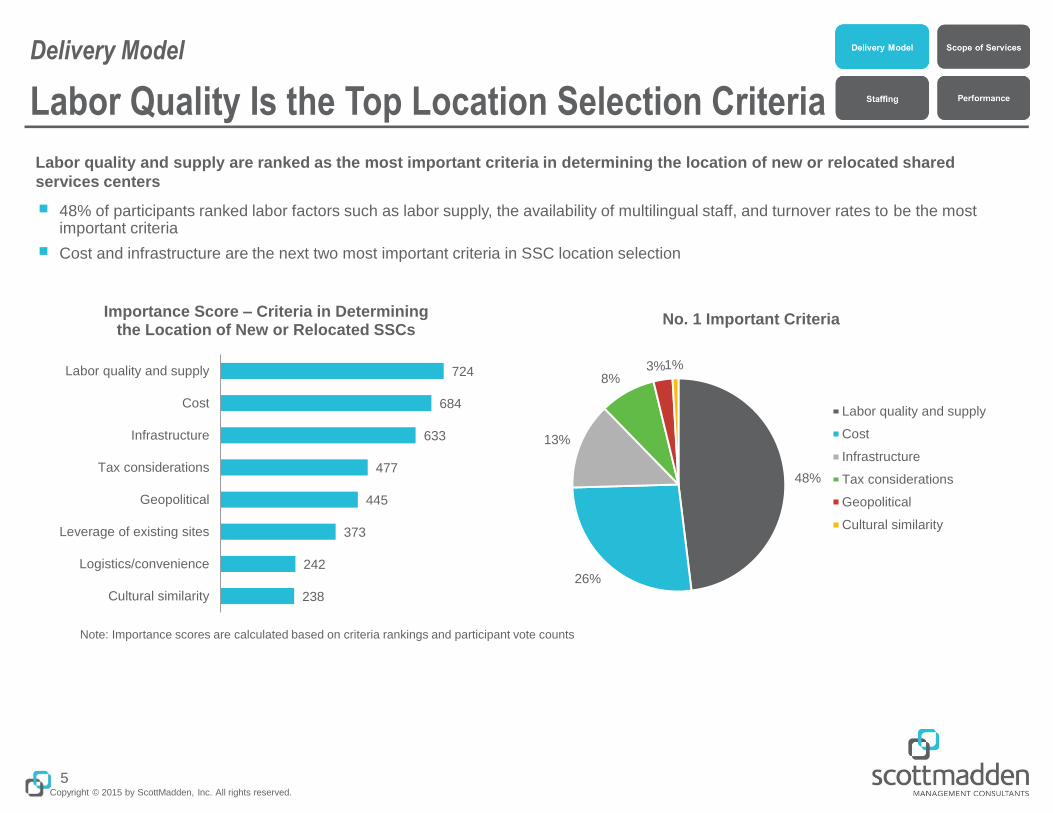

Labor quality and supply are ranked as the most important criteria in determining the location of new or relocated shared

services centers

■ 48% of participants ranked labor factors such as labor supply, the availability of multilingual staff, and turnover rates to be the most important criteria

■ Cost and infrastructure are the next two most important criteria in SSC location selection

Labor Quality Is the Top Location Selection Criteria

Delivery Model

5

Note: Importance scores are calculated based on criteria rankings and participant vote counts

238

242

373

445

477

633

684

724

Cultural similarity

Logistics/convenience

Leverage of existing sites

Geopolitical

Tax considerations

Infrastructure

Cost

Labor quality and supply

Importance Score – Criteria in Determining the Location of New or Relocated SSCs

48%

26%

13%

8% 3% 1%

No. 1 Important Criteria

Labor quality and supply

Cost

Infrastructure

Tax considerations

Geopolitical

Cultural similarity

Copyright © 2015 by ScottMadden, Inc. All rights reserved.

63%

63%

84%

85%

92%

92%

94%

95%

96%

98%

100%

Manage and process collections

Develop and manage pricing

Manage cash

Process customer credit

Process accounts receivable

Perform due-diligence

Perform financial reporting

Perform cost accounting and control

Invoice customer

Process accounts payable

Perform general accounting

Which of the following processes are in-scope for your shared services center?

Scope Continues to Move up the Value Chain

High-value services have made a significant appearance

■ Cost accounting, due diligence, and pricing are all provided by more than 60% of participating SSOs

■ Major transactional processes are most often outsourced

Scope of Services

6

Copyright © 2015 by ScottMadden, Inc. All rights reserved.

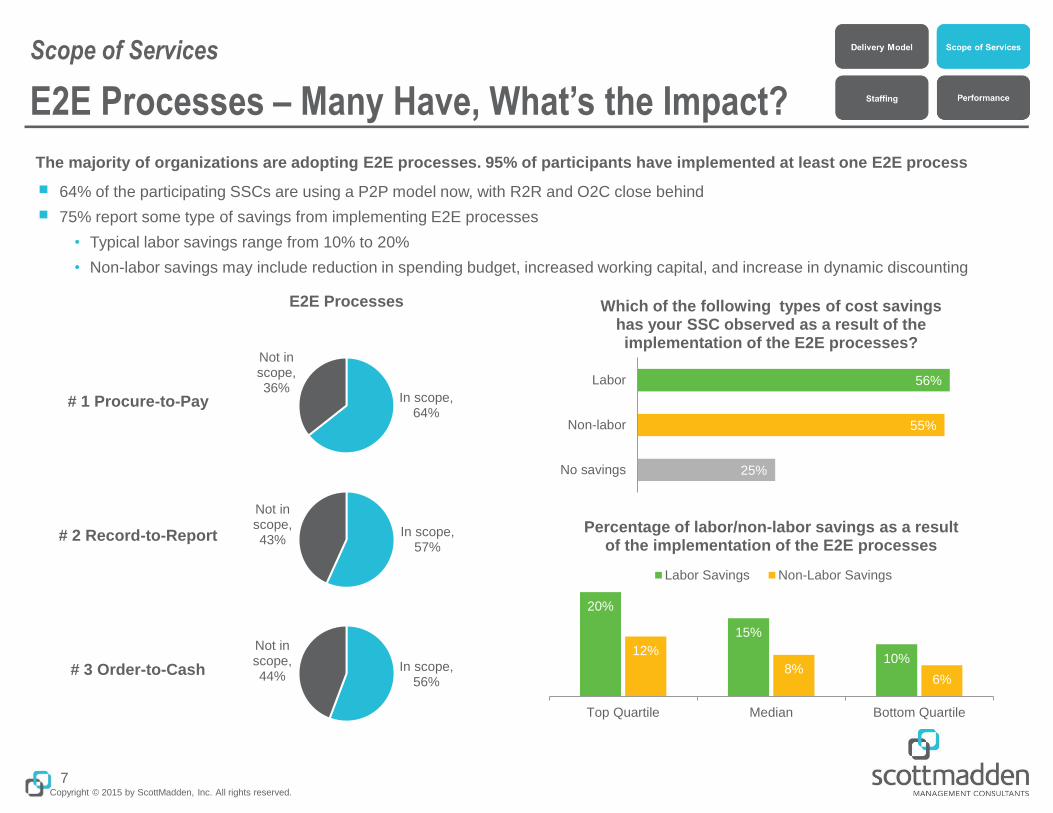

E2E Processes – Many Have, What’s the Impact?

The majority of organizations are adopting E2E processes. 95% of participants have implemented at least one E2E process

■ 64% of the participating SSCs are using a P2P model now, with R2R and O2C close behind

■ 75% report some type of savings from implementing E2E processes

• Typical labor savings range from 10% to 20%

• Non-labor savings may include reduction in spending budget, increased working capital, and increase in dynamic discounting

Scope of Services

7

In scope, 64%

Not in scope, 36%

In scope, 57%

Not in scope, 43%

In scope, 56%

Not in scope, 44%

# 1 Procure-to-Pay

# 2 Record-to-Report

# 3 Order-to-Cash

E2E Processes

25%

55%

56%

No savings

Non-labor

Labor

Which of the following types of cost savings has your SSC observed as a result of the implementation of the E2E processes?

20%

15%

10% 12%

8% 6%

Top Quartile Median Bottom Quartile

Percentage of labor/non-labor savings as a result of the implementation of the E2E processes

Labor Savings Non-Labor Savings

Copyright © 2015 by ScottMadden, Inc. All rights reserved.

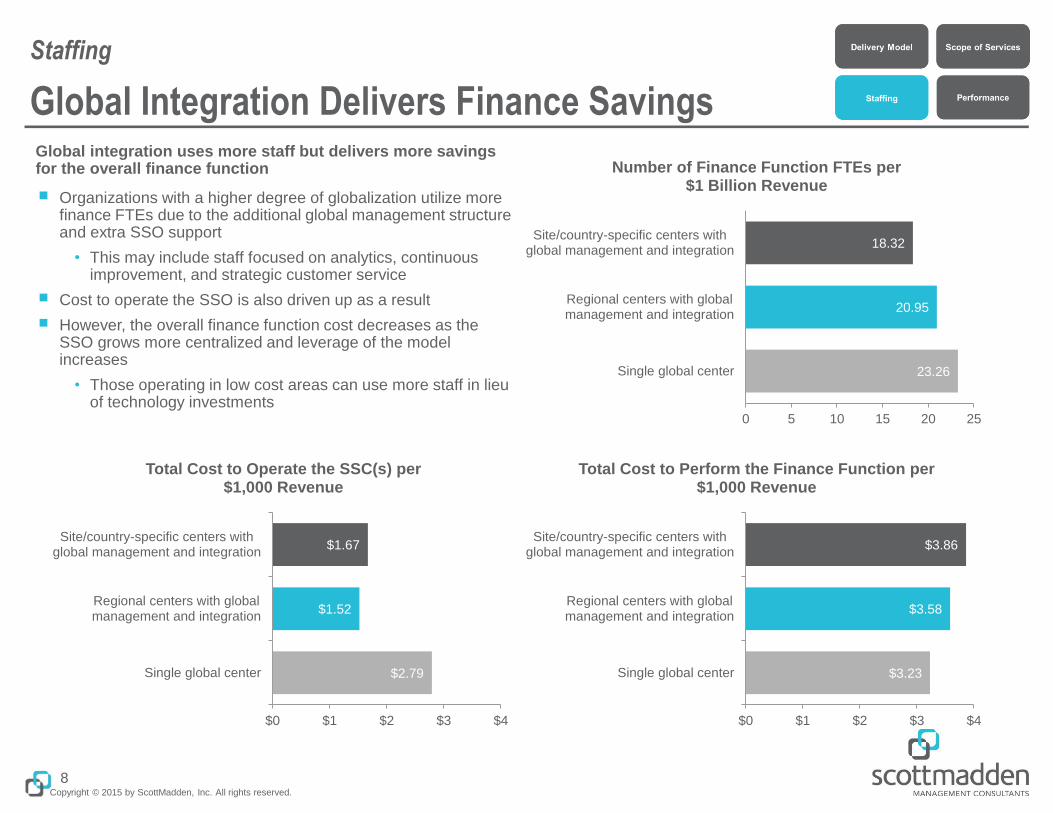

Global Integration Delivers Finance Savings Global integration uses more staff but delivers more savings for the overall finance function

■ Organizations with a higher degree of globalization utilize more finance FTEs due to the additional global management structure and extra SSO support

• This may include staff focused on analytics, continuous improvement, and strategic customer service

■ Cost to operate the SSO is also driven up as a result

■ However, the overall finance function cost decreases as the SSO grows more centralized and leverage of the model increases

• Those operating in low cost areas can use more staff in lieu of technology investments

Staffing

8

18.32

20.95

23.26

0 5 10 15 20 25

Site/country-specific centers withglobal management and integration

Regional centers with globalmanagement and integration

Single global center

Number of Finance Function FTEs per $1 Billion Revenue

$1.67

$1.52

$2.79

$0 $1 $2 $3 $4

Site/country-specific centers withglobal management and integration

Regional centers with globalmanagement and integration

Single global center

Total Cost to Operate the SSC(s) per $1,000 Revenue

$3.86

$3.58

$3.23

$0 $1 $2 $3 $4

Site/country-specific centers withglobal management and integration

Regional centers with globalmanagement and integration

Single global center

Total Cost to Perform the Finance Function per $1,000 Revenue

Copyright © 2015 by ScottMadden, Inc. All rights reserved.

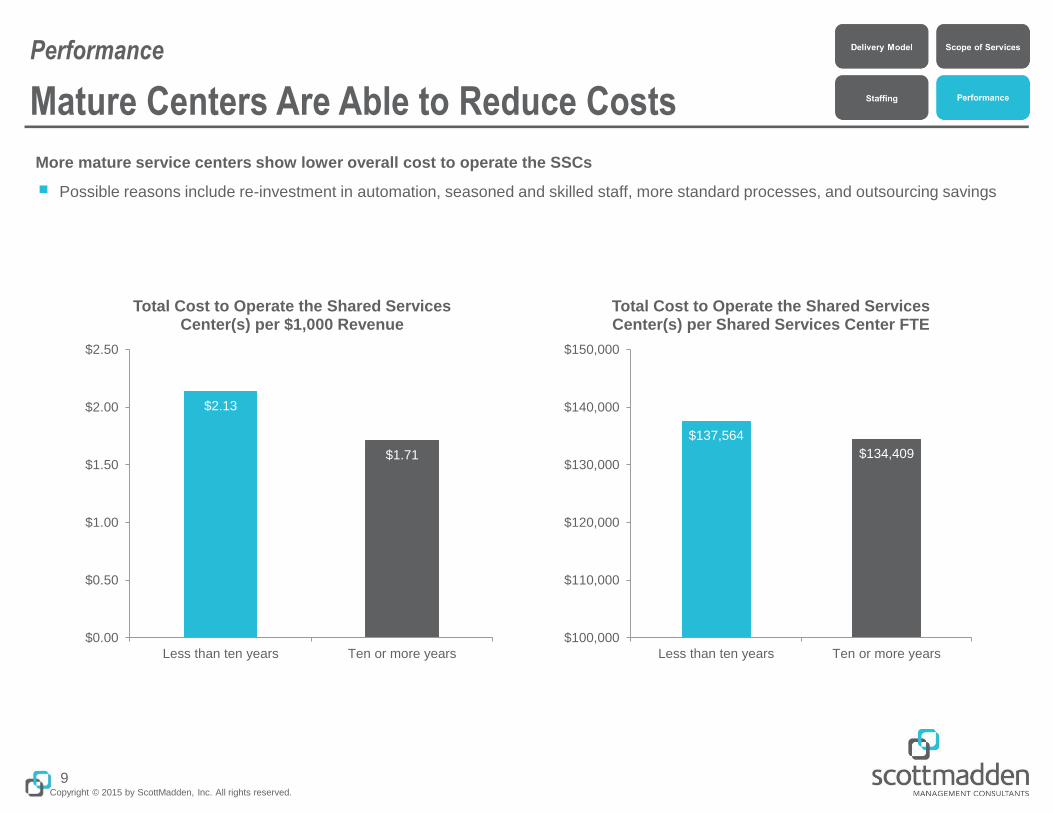

Mature Centers Are Able to Reduce Costs

More mature service centers show lower overall cost to operate the SSCs

■ Possible reasons include re-investment in automation, seasoned and skilled staff, more standard processes, and outsourcing savings

Performance

9

$2.13

$1.71

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

Less than ten years Ten or more years

Total Cost to Operate the Shared Services Center(s) per $1,000 Revenue

$137,564

$134,409

$100,000

$110,000

$120,000

$130,000

$140,000

$150,000

Less than ten years Ten or more years

Total Cost to Operate the Shared Services Center(s) per Shared Services Center FTE

Copyright © 2015 by ScottMadden, Inc. All rights reserved.

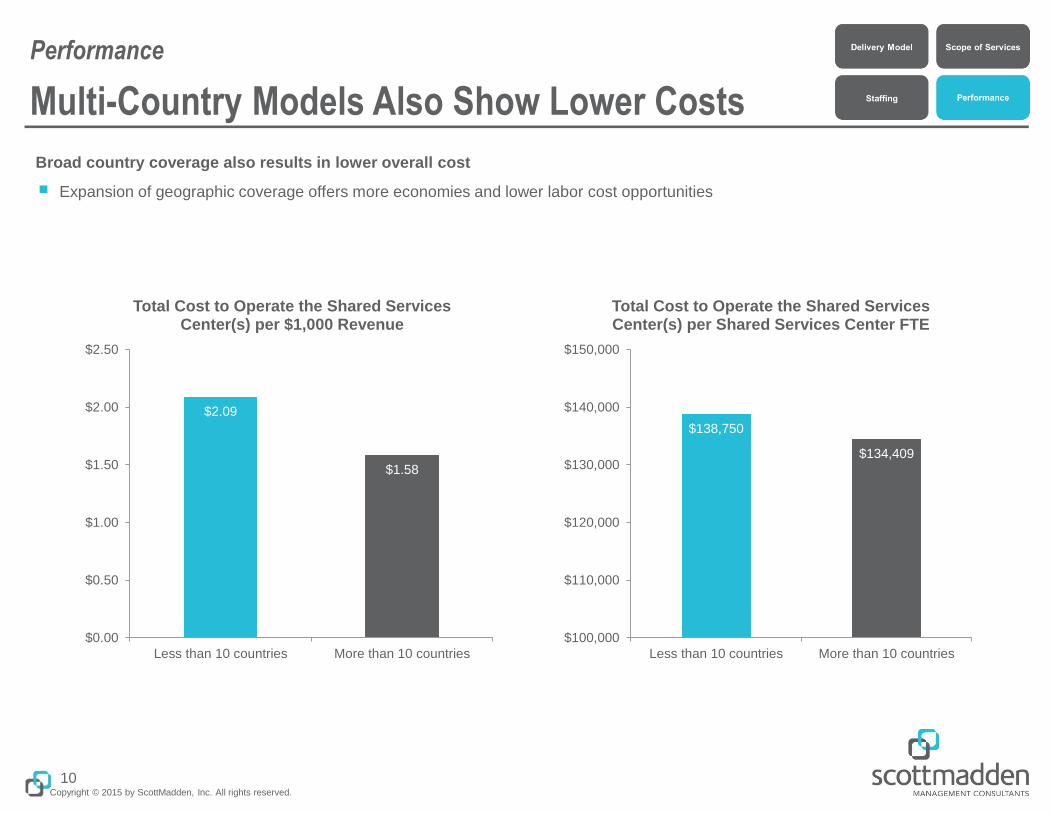

Multi-Country Models Also Show Lower Costs

Broad country coverage also results in lower overall cost

■ Expansion of geographic coverage offers more economies and lower labor cost opportunities

Performance

10

$2.09

$1.58

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

Less than 10 countries More than 10 countries

Total Cost to Operate the Shared Services Center(s) per $1,000 Revenue

$138,750

$134,409

$100,000

$110,000

$120,000

$130,000

$140,000

$150,000

Less than 10 countries More than 10 countries

Total Cost to Operate the Shared Services Center(s) per Shared Services Center FTE

Copyright © 2015 by ScottMadden, Inc. All rights reserved.

Key Takeaways

■ Global models are prevalent among participating SSOs with 68% providing services to more than one country

• 26% report regional models with global management and integration

■ Transactional finance services remain among the most common in-scope processes for shared services centers; however, there is increasing evidence that many have integrated advanced analytical, consultative, and advisory services in their SSOs

• Newer services such as pricing and due diligence are on the rise

■ E2E process adoption is high with 95% reporting they have implemented at least one E2E process

• 75% of those participants have realized cost savings from the change

• Labor savings for most ranges from 10% to 20%

■ Global process governance is emerging with 40% reporting use of multiple governance approaches

■ However, moving to GBS is not without challenges as half of participants cite regulatory and control issues as the biggest obstacle to overcome when implementing GBS

■ Global integration requires more finance FTEs and higher SSO cost but delivers more savings for the overall finance function

■ Mature centers and those with broad country coverage are able to operate at a lower cost

• Possible explanations include reinvestment in automation, increased standardization of processes, leverage of seasoned staff, and economies of scale gained from expanded geographic coverage and lower labor cost

11

Copyright © 2015 by ScottMadden, Inc. All rights reserved.

Contact Information

12

Trey Robinson

Partner

Finance & Accounting

and GBS

Office: 919-781-4191

Mobile: 919-522-1740

Brad DeMent

Partner

Finance & Accounting and GBS

Practice Lead

Office: 404-814-0020

Mobile: 678-524-2496