financial accounting 1 lecture – 26 recap with the increase in business, it becomes difficult to...

TRANSCRIPT

Financial Accounting

1

Lecture – 26

Recap

• With the increase in business, it becomes difficult to maintain separate accounts for every Debtor and every Creditor.

• Control Accounts are opened in the ledger for both Debtors and Creditors.

• Control Accounts are part of double Entry system.

• Subsidiary ledgers are not part of double entry system.

• Control Account system is used only for credit sale and credit purchase.

Financial Accounting

2

Lecture – 26

Subsidiary Books

• To reduce the volume of general ledger, number of books are opened that are called Subsidiary books.

Financial Accounting

3

Lecture – 26

Subsidiary Books- Debtors

• Three subsidiary books are maintained in case of sales / debtors. Sales Journal / Sales Day Book – individual invoice wise

sales are recorded in this Journal. Sales Return / Return Inward Journal – in case the

volume of returns is also high then these are also recorded in a separate register.

Debtors Ledger – this ledger maintains record of individual debtor.

• Cash sale is not included in the debtors control accounts.

Financial Accounting

4

Lecture – 26

Information for Control Accounts

Opening balance of debtors List of debtors balances drawn up to the end of previous period confirms with the aggregate balance of the Control Account.

Credit Sales Periodically total of sales journal is posted into the debtors control account.

Sales Return In case the transaction volume of sales return is high then these are recorded in the sales return journal. Periodically the total is posted in the debtors control a/c.

Cheques / Cash Received List of receipts is extracted from cash and bank book. Or a separate column is maintained in cash and bank books for this purpose

Closing Balance This is the balancing figure. It can also be checked with the total of balances in debtors Control Account.

Financial Accounting

5

Lecture – 26

Recording of Sales

Sales Journal

Date Invoice #

Name / Debtor

Amount

Jan 01, 20-- 01 A 10,000

Jan 15, 20-- 02 B 12,500

Jan 30, 20-- 03 C 15,000

Total 37,500

Debtors Ledger

A Account

Debit

01/1 10,000

Credit

Bal 10,000

B Account

Debit

15/1 12,500

Credit

Bal 12,500

C Account

Debit

30/1 15,000

Credit

Bal 15,000

Financial Accounting

6

Lecture – 26

Recording of Sales

Sales Journal

Date Invoice # Name / Debtor Amount

Jan 01, 20-- 01 A 10,000

Jan 15, 20-- 02 B 12,500

Jan 30, 20-- 03 C 15,000

Total 37,500

General LedgerSales Account

Debit side.

Bal 37,500

Credit side.

Jan Sales 37,500

Debtors Control Account

Debit side.

Jan Sales 37,500

Credit side.

Bal 37,500

Financial Accounting

7

Lecture – 26

Recording of Sales

• Now if we total the balance of three accounts of the debtors

ledger on Jan 30,:A

10,000B 12,500C 15,000Total 37,500

• It will be the same as the balance in the debtors control account of the general ledger.

Financial Accounting

8

Lecture – 26

Recording of Sales Return

Sales Journal

Date Name / Debtor Amount

Jan 15, 20-- A 1,000

Jan 20, 20-- A 500

Jan 25, 20-- B 2,500

Total 4,000

General Ledger

Debtors Control Account

Debit side.

Jan Sales 37,500

Credit side.

Jan Ret 4,000

Bal 33,500

Sales Account

Debit side.

Jan Ret 4,000

Bal 33,500

Credit side.

Jan Sales 37,500

Financial Accounting

9

Lecture – 26

Recording of Sales Return

Sales Journal

Date Name / Debtor Amount

Jan 15, 20-- A 1,000

Jan 20, 20-- A 500

Jan 25, 20-- B 2,500

Total 4,000

A Account

Debit

01/1 10,000

Credit

15/1 1,000

20/1 500

Bal 8,500

B Account

Debit

15/1 12,500

Credit

25/1 2,500

Bal 10,000

C Account

Debit

30/1 15,000

Credit

Bal 15,000

Debtors Ledger

Financial Accounting

10

Lecture – 26

Recording of Sales Return

• Again if we total the balance of three accounts of the debtors ledger on Jan 30,: A 8,500 B 10,000 C 15,000 Total 33,500

• It will be the same as the balance in the debtors control account of the general ledger.

Financial Accounting

11

Lecture – 26

Receipts From Debtors

• When control accounts are used we maintain cash and bank books with separate pages for receipts and payments i.e. two column cash/bank books are not used.

• On the receipts side of the cash and bank book a column is added in which receipts from debtors are separately noted.

• This type of cash / bank book is also called multi column cash / bank book.

Financial Accounting

12

Lecture – 26

Recording of Receipts – Multi Column Cash Book

Cash / Bank Book

Receipt Side

Date No Narration / Particulars

LedgerCode

Receipt Amount

Receipt fromDebtors

10,000

500

Received from A 5,000 5,000

300

Received from B 2,500 2,500

Received from A 1,000 1,000

Received from C 1,500 1,500

950

1,000

Total 22,750 9,000

Financial Accounting

13

Lecture – 26

Subsidiary Books- Creditors

• The recording of creditors is similar to debtors. The subsidiary books maintained in case of purchases / creditors are: Purchase Journal / Purchase Day Book – individual

purchases are recorded in this Journal. Purchase Return / Return outward Journal – in case the

volume of returns is also high then these are also recorded in a separate register.

Creditors Ledger – this ledger maintains record of individual creditors.

• Cash purchase is not included in the creditors control accounts.

Financial Accounting

14

Lecture – 26

Subsidiary Books - Creditors

Opening balance of Creditors List of creditors balances drawn up to the end of previous period confirms with the aggregate balance of the Control Account.

Credit Purchases Periodically total of purchase journal is posted into the creditors control account.

Purchase Return In case the transaction volume of purchase return is high then these are recorded in the purchase return journal. Periodically the total is posted in the creditors control a/c.

Cheques / Cash Paid List of payments is extracted from cash and bank book. Or a separate column is maintained in cash and bank books for this purpose

Closing Balance This is the balancing figure. It can also be checked with the total of balances in creditors Control Account.

Financial Accounting

15

Lecture – 26

Recording of Purchases

Purchase Journal

Date Name / Debtor Amount

Apr 01, 20-- X 15,000

Apr 10, 20-- Y 20,000

Apr 25, 20-- Z 10,000

Total 45,000

General Ledger

Creditors Control Account

Debit side.

Bal 45,000

Credit side.

Apr Purch 45,000

Purchases Account

Debit side.

Apr Purch 45,000

Credit side.

Bal 45,000

Financial Accounting

16

Lecture – 26

Recording of Purchases

Purchase Journal

Date Name / Debtor Amount

Apr 01, 20-- X 15,000

Apr 10, 20-- Y 20,000

Apr 25, 20-- Z 10,000

Total 45,000

Creditors Ledger

X Account

Debit

Bal 15,000

Credit

1/4 15,000

Y Account

Debit

Bal 20,000

Credit

10/4 20,000

Z Account

Debit

Bal 10,000

Credit

25/4 10,000

Financial Accounting

17

Lecture – 26

Recording of Purchases

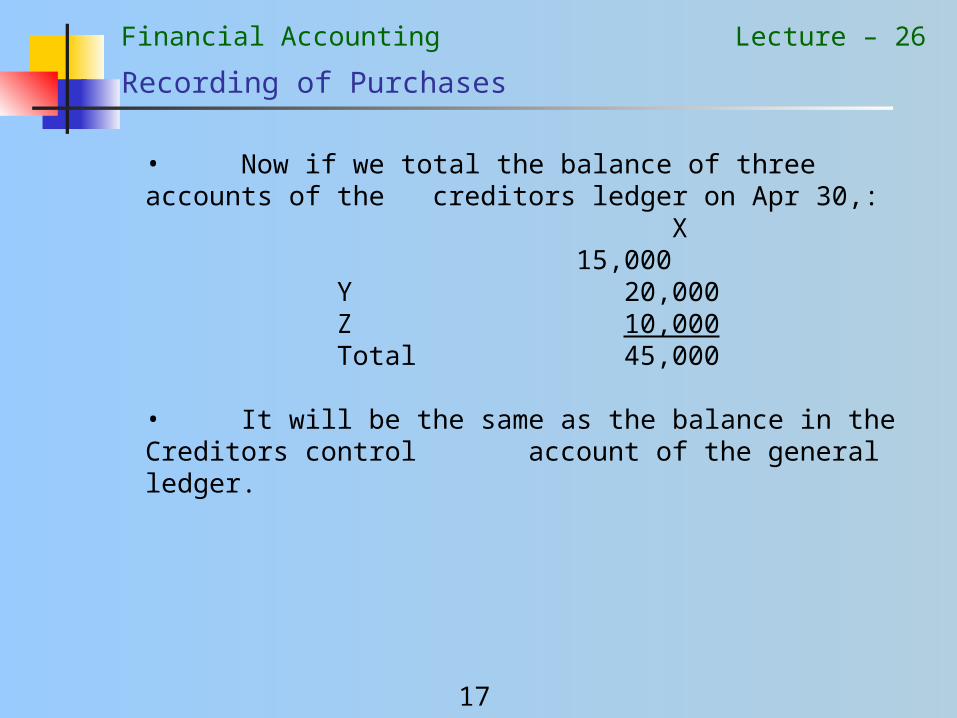

• Now if we total the balance of three accounts of the creditors ledger on Apr 30,:

X15,000

Y 20,000Z 10,000Total 45,000

• It will be the same as the balance in the Creditors control account of the general ledger.

Financial Accounting

18

Lecture – 26

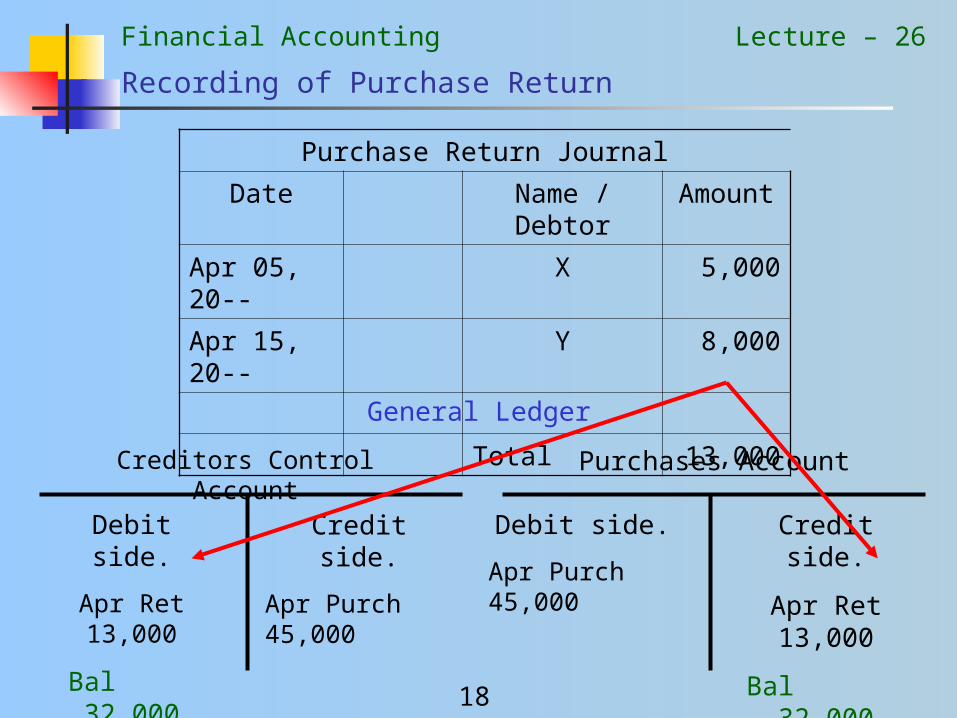

Recording of Purchase Return

Purchase Return Journal

Date Name / Debtor Amount

Apr 05, 20-- X 5,000

Apr 15, 20-- Y 8,000

Total 13,000

General Ledger

Creditors Control Account

Debit side.

Apr Ret 13,000

Bal 32,000

Credit side.

Apr Purch 45,000

Purchases Account

Debit side.

Apr Purch 45,000

Credit side.

Apr Ret 13,000

Bal 32,000

Financial Accounting

19

Lecture – 26

Recording of Purchase Return

Purchase Return Journal

Date Name / Debtor Amount

Apr 05, 20-- X 5,000

Apr 15, 20-- Y 8,000

Total 13,000

Creditors Ledger

X Account

Debit

5/4Ret 5,000

Bal 10,000

Credit

1/4 15,000

Z Account

Debit

Bal 10,000

Credit

25/4 10,000

Y Account

Debit

15/4Ret 8,000

Bal 12,000

Credit

10/4 20,000

Financial Accounting

20

Lecture – 26

Recording of Purchase Return

• Again if we total the balance of three accounts of the Creditors ledger on Apr 30,:

A 10,000B 12,000C 10,000Total 32,000

• It will be the same as the balance in the creditors control account of the general ledger.

Financial Accounting

21

Lecture – 26

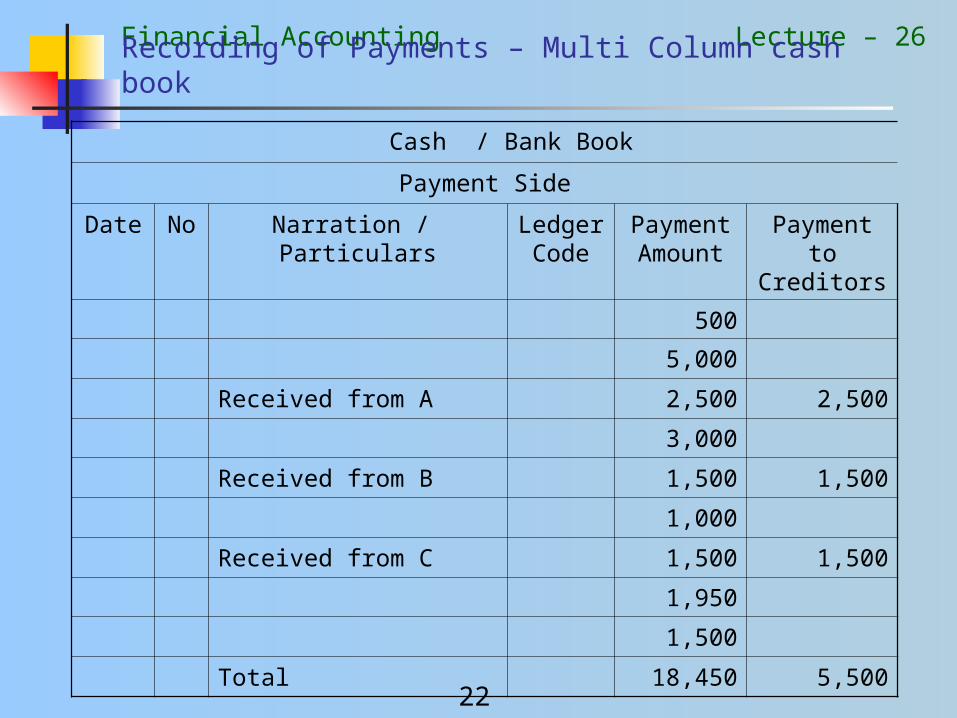

Payment to Creditors

• On the payment side of the cash and bank book a column is added in which payments to creditors are separately noted.

Financial Accounting

22

Lecture – 26

Recording of Payments – Multi Column cash book

•Cash / Bank Book

Payment Side

Date No Narration / Particulars

LedgerCode

Payment Amount

Payment to Creditors

500

5,000

Received from A 2,500 2,500

3,000

Received from B 1,500 1,500

1,000

Received from C 1,500 1,500

1,950

1,500

Total 18,450 5,500