financial adviser pocket guide - mentor - mentor education · pdf filetaxationtaxation mentor...

TRANSCRIPT

FinancialAdviserPocket Guide

FinancialAdviserPocket Guide2016 - 20172016 - 2017

Mentor Education 2

Financial Adviser Pocket Guide 2016 - 2017

TaxationTax Rates 3Other Tax Rates 5Tax Offsets 6

SuperannuationContributions 8Taxation of Superannuation 12Superannuation Income Streams 15Employment Termination Payments 18

Social SecurityAge Pension 20Life Tables, Australia, 2010 – 2012 24

Online Resources

3 ..

8 ..

20 ..

27 ..

TaxationTaxation

Mentor Education 3

Financial Adviser Pocket Guide 2016 - 2017

Tax RatesResident personal tax rates (2016/2017)

Taxable Income

$0 – $18,200

$18,201 – $37,000

$37,001 – $80,000

$80,001 – $180,000

$180,001 & over

Nil

19c for each $1 over $18,200

$ 3,572 plus 32.5c for each $1 over $ 37,000

$17,547 plus 37.0c for each $1 over $ 80,000

$54,547 plus 47.0c for each $1 over $180,000

Nil

19.0%

32.5%

37%

47.0%**

*The above rates exclude Medicare levy of 2.0% on taxable income for residents.

**Includes the 2.0% Temporary Budget Repair Levy from 1 July 2014 to 30 June 2017 (for all individuals)

Note: The 2016-17 Federal Budget contains a proposal to raise the 32.5% bracket from $80,000 to $87,000.

Marginal Rate* Tax Payable

Medicare levy (2015/2016)

Single

Couple

Single

Couple

$26,668 & over

$45,002 & over

$42,172 & over

$58,708 & over

$0 – $21,335

$0 – $36,001

$0 – $33,738

$0 – $46,966

*Note: Reduced Medicare levy is 10c (shade in rate) for every dollar over the ‘lower threshold. The full

2.0% is applicable where taxable income is over the ‘upper threshold’ for the reduced Medicare levy.

No levy

$21,336 – $26,667

$36,002 – $45,001

$33,739 – $42,171

$46,967 – $58,707

Reduced levy* Full 2.0%

All other taxpayers other than those eligible for SAPTO (2015/2016)

Eligible for SAPTO (2015/2016)**

Add $3,306 to the ‘lower threshold’ for each dependent child or student.

Add $44,133 to the upper threshold for each dependent child or student.

Mentor Education 4

Financial Adviser Pocket Guide 2016 - 2017

Non-resident personal tax rates (2016/2017)

Taxable Income

$0 – $80,000

$80,001 – $180,000

$180,001 & over

32.5c for each $1

$26,000 plus 37.0c for each $1 over $ 80,000

$63,000 plus 47.0c for each $1 over $180,000

32.5%

37.0%

47.0%**

*Medicare levy does not apply to non-residents.

**Includes the 2.0% Temporary Budget Repair Levy from 1 July 2014 to 30 June 2017 (for all individuals).

Marginal Rate* Tax Payable

Tax rate for Minors – unearned income (2016/2017 )

Eligible Income

$0 – $416

$417 – $1,307

$1,307 & over

Nil

66.0%** of each $1 over $416

47.0%** of the entire income

Note: ‘Earned income’ is taxed at adult marginal rates. LITO is not available for ‘unearned income’ of

minors.

**Includes the 2.0% Temporary Budget Repair Levy from 1 July 2014 to 30 June 2017.

Marginal rate

Medicare levy surcharge (2016/2017)

Tier 1

Tier 2

Tier 3

1.00%

1.25%

1.50%

$ 90,001 – $105,000

$105,001 – $140,000

$140,001 & over

*Note: *The threshold includes taxable income, reportable fringe benefits, reportable super contribu-

tions and total net investment loss, and is increased by $1,500 per child after the first. Single parents and

couples (including de facto couples) are subject to family tiers. Medicare levy surcharge only applies if not

covered by private health insurance. The annual indexation of the Medicare levy surcharger income

levels is frozen for three years from 2015/16 to 30 June 2018.

Single

$180,001 – $210,000

$210,001 – $280,000

$280,001 & over

Family Surcharge

Other Tax Rates

$0 – $416

Superannuation fund:

Complying

Non-complying

Insurance and Friendly Society Bonds

30%

15%

47%**

30%

**Includes the 2.0% Temporary Budget Repair Levy from 1 July 2014 to 30 June 2017.

Tax Rate

Fringe benefit tax rate (1 April 2016 to 31 March 2017)

Mentor Education 5

Financial Adviser Pocket Guide 2016 - 2017

After 30/06/2000 which have been eligible

to an input tax credit under GST regime

FBT rate is 49.0%** and calculated on the tax-inclusive

value of the fringe benefit provided in the year.

2.1463

Does not attract an input tax credit 1.9608

**includes the 2.0% Medicare Levy and the 2.0% Temporary Budget Repair Levy.

Gross-up rateFringe benefit provided

Capital gains tax

Capital gains tax exempt

For assets held for more than 12 months, taxpayers can choose to either:

Pay capital gains tax on 50% of the difference between the original cost base and the

disposal price) OR

Pay capital gains tax on the difference between the indexed cost base and the disposal

price. The indexed cost base is the original cost base multiply by the frozen CPI index

(68.7) as at September 1999 divide by the CPI index for quarter of acquisition.

For assets held for less than 12 months, capital gains tax is payable on the whole gain.

The assessable capital gain is included in the individual’s taxable income and is taxed at marginal tax rate.

Asset bought before 20 September 1985

Asset bought between 20 September 1985 and 20 September 1999

Tax OffsetsTax offsets, previously known as rebates, reduce the tax payable by an individual.

*Reduces by 1.5c for each $1 of taxable income over $37,000. LITO makes the tax free threshold

effectively $20,542, but $21,335 is where no Medicare Levy is applicable.

Low income tax offset (LITO) 2016/2017

Senior and Pensioners tax offset (SAPTO) 2015/2016

Single

Couple (each)

Couple separated due to illness (each)

$50,119

$41,790

$47,599

$2,230

$1,602

$2,040

*The maximum offset reduces by 12.5c for every dollar of rebate income over the shade-out threshold

and erodes entirely at the cut-out threshold. Rebate income includes taxable income, adjusted fringe

benefits, reportable super contributions and total net investment loss.

Max. offset*

$32,279

$28,974

$31,279

Shade-out threshold

Cut-out thresholdLow income aged person

Mentor Education 6

Financial Adviser Pocket Guide 2016 - 2017

For assets held for more than 12 months, taxpayer pay capital gains tax on 50% of the

difference between the cost base and the disposal price. Only the 50% discount applies. No

indexation is available. For assets held for less than 12 months, capital gains tax is payable on

the whole gain.

Assets bought on or after 21 September 1999

Low income earner $66,667$445

Max. Offset*

$37,000

Shade-out threshold Cut-out threshold

*Note: *The threshold includes taxable income, reportable fringe benefits, reportable super contributions

and total net investment loss, and is increased by $1,500 per child after the first. Single parents and

couples (including de facto couples) are subject to family tiers. The annual indexation of the health

insurance rebates income levels is frozen for three years from 2015/16 to 30 June 2018.

The Net Medical Expenses Offset (NMETO) is being phased out over the period 1 July to 30 June

2018. Transitional arrangements allow claims for disability aids, attendant care or age care expens-

es to be made until 30 June 2019.

For singles and couples or families with adjusted taxable income up to and including $90,000 and

$180,000 respectively, an offset is 20% of whatever is left (or ‘the excess’) of net medical expenses

over $2,265 that were paid in a financial year may be claimed. Net medical expenses are the total

amount spent on medical expenses (on behalf of the taxpayer and their dependants) minus any

reimbursement paid by private health insurance or Medicare. There is no upper limit on the

amount that can be claimed.

Note:

Singles and couples or families with adjusted taxable income above the thresholds can only claim

an offset of 10% of net medical expenses over $5,343 (all thresholds are indexed annually).

Private health insurance (PHI) Rebate (2016/2017)

Net medical expenses tax offset NMETO (2015/2016)

Tier 1

Tier 3

$180,000 or less

$180,001 – $210,000

$280,001 & over

Family

26.791%

17.861%

Tier 2 $210,001 – $280,000 8.930%

nil

<65

31.256%

22.326%

13.395%

nil

65-69

35.722%

26.791%

17.861%

nil

70+

Tier 1

Tier 3

$ 90,000 or less

$ 90,001 – $105,000

$140,001 & over

Single

26.791%

17.861%

Tier 2 $105,001 – $140,000 8.930%

nil

<65

31.256%

22.326%

13.395%

nil

65-69

35.722%

26.791%

17.861%

nil

70+

Mentor Education 7

Financial Adviser Pocket Guide 2016 - 2017

Contributions

Concessional contributions are sometimes known as ‘before-tax’ contributions and include:

Contributions made by an employer for an employee, including SG contributions, contributions

made under a salary sacrifice arrangement; and

Personal contributions that are claimed as a tax deduction (where the person is eligible to

claim).

Acceptance of contributions

Concessional Contributions

Mentor Education 8

Financial Adviser Pocket Guide 2016 - 2017

SuperannuationSuperannuation

Age of member

Under age 65

Age 65 to 69

Age 75 & over

Made by or on behalf of member at any time.

Mandated contributions; or

Made by or on behalf of the member provided the

member meets the work test*.

Age 70 to 74 Mandated contributions; or

Made by the member or voluntary employer

contributions (including salary sacrifice) provided the

member meets the work test* and the contributions

are received within 28 days of the end of the month in

which the member reaches age 75.

Mandated contributions under an industrial Award or

workplace agreement.

*Work test – member has been gainfully employed for a minimum of 40 hours

over 30 consecutive days during the financial year in which the contributions

are made.

Fund may accept contributions that are:

Non-concessional contributions are sometimes known as ‘after-tax’ contributions and include:

Personal contributions that an income tax deduction has not been claimed for, such as

contributions made from take-home pay;

Contributions made by a contributing spouse to a receiving spouse’s super fund (but not a

contribution as an employer); and

Transfers from foreign super fund (but are not assessable income to the fund).

Non-Concessional Contributions

Mentor Education 9

Financial Adviser Pocket Guide 2016 - 2017

Contributions Cap (2016/2017)

Excess Concessional Contributions

Contribution

Concessional contribution < age 49

Concessional contribution > age 49

Non-concessional contribution - No

work test if < age 65 and no ‘bring

forward if > age 65.

See full explanation below**

See full explanation below**

See full explanation below**

$ 30,000 pa

$ 35,000 pa

$180,000 pa

$540,000 (3 year limit)

**Excess concessional contributions also count towards the non-concessional contributions cap.

Note: Contributions made by employers or the self-employed are fully tax deductible up to age 75.

Individuals who exceed their concessional contributions cap will have the excess amount included in

their assessable income, and taxed at their marginal tax rate. They will also have to pay the excess

concessional contributions (ECC) charge on the increase in tax liability. This charge is applied to recognise

that the tax on excess concessional contributions is collected later than normal income tax. To reduce

the tax liability, the ATO will apply a 15 tax offset to account for the contributions tax that has already

been paid by the super fund. The individual may elect to withdraw up to 85% of the excess concessional

contributions from their super fund to help pay their income tax assessment. Any excess concessional

contributions withdrawn from their fund will not count towards their non-concessional contributions

cap.

Example: - Excess Concessional Contributions

During 2014-15, Mary (age 45) salary sacrificed to super, her total concessional contributions were

$40,000. Because Mary’s concessional cap was $30,000, her excess concessional contributions was

$10,000. Mary has taxable income of $70,000. The ATO includes the $10,000 and increases Mary’s taxable

income to $80,000. She will be assessed at her effective marginal tax rate of 34.5% (including 2.0%

Medicare levy).

Cap Excess Contribution Tax (ECT)

The additional tax payable as a result of the excess concessional contributions is $3,450. Mary is entitled

to a tax offset equal to 15% of her excess concessional contributions, decreasing her tax liability by

$1,500. With the inclusion of the excess concessional contributions (ECC), Mary’s tax liability has

increased by $1,950 ($3,450 - $1,500), and the ECC charge will be applied to this amount.

The daily ECC charge rate is based on the monthly average yield of 90-day Bank Accepted Bills plus an

uplift factor of 3%. For January to March 2015 it was 5.75% and for April to June 2015 it is 5.36%. The ECC

charge period is calculated from the start of the income year in which the ECC were made and ends the

day before the tax is due to be paid under the first income tax assessment for the year that includes the

ECC.

Excess Non-Concessional Contributions

Excess non-concessional contributions tax of 47% (including Medicare levy) is payable on excess

non-concessional contributions.

Contributions Tax

The regular contributions tax on concessional contributions is a flat rate of 15%, but for individuals with

incomes over $300,000 (including concessional contributions) some or all of their concessional

contributions may be taxed 30%. The extra 15% tax is known as the ‘Division 293 tax’. If an individual has

an income of $280,000 and concessional contributions of $25,000, the total of the two amounts comes to

$305,000. The amount over $300,000 is $5,000, which means $5,000 of the concessional contributions

will be taxed at 30% and $20,000 of the concessional contribution will be taxed of 15%. However, if the

individual’s income is over $300,000 (without concessional contributions), all of the concessional

contributions will be taxed at 30%.

Example: - Excess Concessional Contributions

During 2014-15, Mary (age 45) salary sacrificed to super, her total concessional contributions were

$40,000. Because Mary’s concessional cap was $30,000, her excess concessional contributions was

$10,000. Mary has taxable income of $70,000. The ATO includes the $10,000 and increases Mary’s taxable

income to $80,000. She will be assessed at her effective marginal tax rate of 34.5% (including 2.0%

Medicare levy).

Mentor Education 10

Financial Adviser Pocket Guide 2016 - 2017

The additional tax payable as a result of the excess concessional contributions is $3,450. Mary is entitled

to a tax offset equal to 15% of her excess concessional contributions, decreasing her tax liability by

$1,500. With the inclusion of the excess concessional contributions (ECC), Mary’s tax liability has

increased by $1,950 ($3,450 - $1,500), and the ECC charge will be applied to this amount.

The daily ECC charge rate is based on the monthly average yield of 90-day Bank Accepted Bills plus an

uplift factor of 3%. For January to March 2015 it was 5.75% and for April to June 2015 it is 5.36%. The ECC

charge period is calculated from the start of the income year in which the ECC were made and ends the

day before the tax is due to be paid under the first income tax assessment for the year that includes the

ECC.

The minimum SG contribution rate is 9.5% of an eligible employee’s ordinary time earnings (OTE).

The SG rate will remain at 9.5% until 30 June 2021. The maximum contribution earnings base

requiring SG support in 2016/2017 is $51,620 per quarter (i.e. $206,480 pa., maximum SG of

$19,615.60). The minimum earnings base that requires SG contributions to be paid is $450 per

month.

No SG is payable where:

Earnings of less than $450 a month

Part-time employees under 18 years, working under 30 hours per week

Superannuation Guarantee (SG) Contribution (2015/2016)

Must make a personal super contribution and earn 10% or more of total income from carrying on a

business, eligible employment, or combination of both to be eligible.

Spouse super contribution offset (2016/2017)

Spouse assessable income (SAI)

$0 – $10,800

$10,801 – $13,799

$13,800

MC or actual contribution

MC or actual contribution

Nil

$3,000

$3,000 – (SAI – $A10,800)

Nil

An offset of 18% is available on spouse super contributions up to $3,000. The maximum offset of

$540 is available when the spouse’s total income (assessable income, reportable fringe benefits and

reportable employer super contributions) is $10,800 or less. The offset cuts out at $13,800.

Max. contribution (MC) Max. offset (18% of the lesser of)

Contribution equal to 15% of concessional contribution up to maximum of $500 (minimum

payable is $20)

Paid to superannuation fund or retirement savings account (RSA)

Adjusted taxable income must be less than $37,000

Must earn 10% or more of total income from carrying on a business, employment or

combination of both

The Coalition government has extended it until 2016/2017.

Low income superannuation contribution (LISC) was proposed to be abolished from 1 July 2013

Mentor Education 11

Financial Adviser Pocket Guide 2016 - 2017

Government Co-Contribution (2016/2017)

Adjusted Taxable Income (ATI)

$0 – $36,021

$36,022 – $51,021

$500 (50% of $1,000 non-concessional contribution)

$500 – [(ATI – $36,021) x 0.03333]

$51,021+ Nil

Maximum Government Co-Contribution

Lifetime CGT retirement exemption limit – $500,000.

Must satisfy basic conditions applying to all CGT small business concessions. The amount chosen

to be exempt must not exceed remaining CGT retirement exemption limit and:

If under 55 exempt amount must be contributed into a complying superannuation fund or

retirement savings account (RSA); or

If 55 or over don’t have to pay any amount into a complying superannuation fund or RSA.

Small business CGT retirement exemption

Preservation Age

Date of Birth

Before 1 July 1960

1 July 1960 – 30 June 1961

55

56

1 July 1961 – 30 June 1962 57

On or after 1 July 1964 60

1 July 1962 – 30 June 1963 58

1 July 1963 – 30 June 1964 59

Preservation Age

Not required to make contributions.

Contributions which are made can be claimed as a tax deduction where less than 10% of

assessable income (which includes reportable fringe benefits plus reportable super contribu-

tions and net investment loss) is received from employment as an employee (i.e., eligible

employment).

Self Employed

Mentor Education 12

Financial Adviser Pocket Guide 2016 - 2017

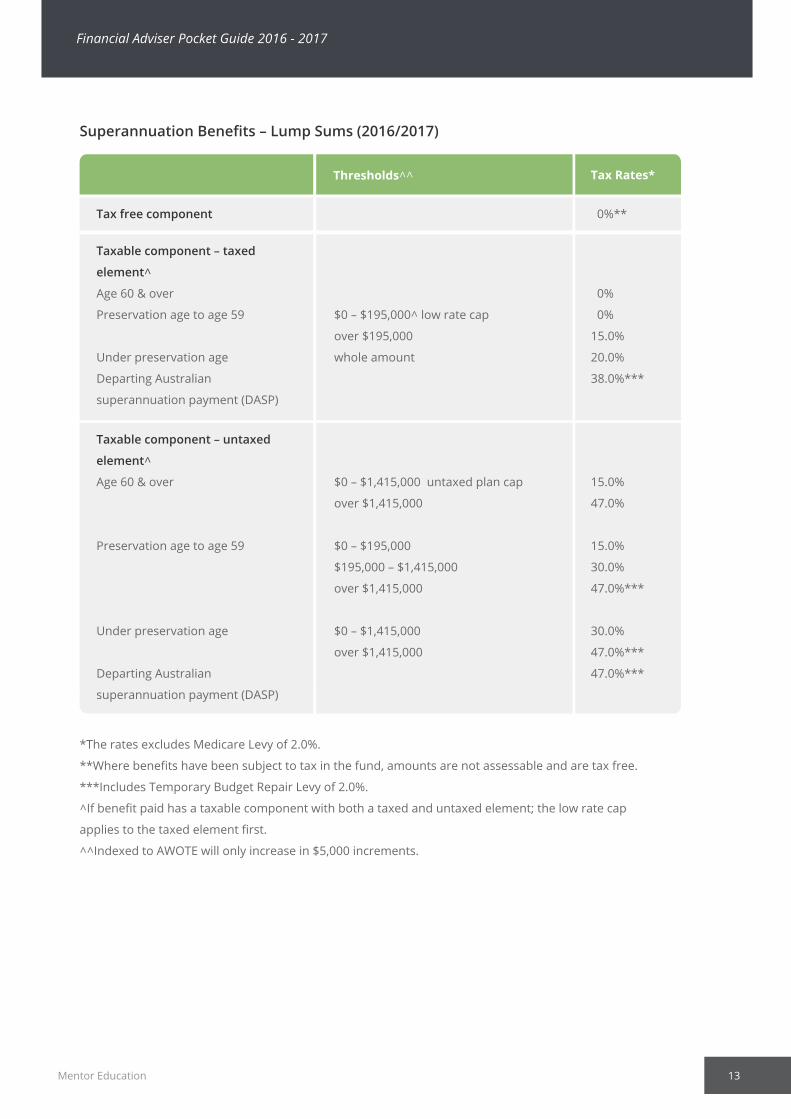

Taxation of Superannuation

*The rates excludes Medicare Levy of 2.0%.

**Where benefits have been subject to tax in the fund, amounts are not assessable and are tax free.

***Includes Temporary Budget Repair Levy of 2.0%.

^If benefit paid has a taxable component with both a taxed and untaxed element; the low rate cap

applies to the taxed element first.

^^Indexed to AWOTE will only increase in $5,000 increments.

Tax free component 0%**

Taxable component – taxed

element^

Age 60 & over

Preservation age to age 59

Under preservation age

Departing Australian

superannuation payment (DASP)

0%

0%

15.0%

20.0%

38.0%***

$0 – $195,000^ low rate cap

over $195,000

whole amount

Taxable component – untaxed

element^

Age 60 & over

Preservation age to age 59

Under preservation age

Departing Australian

superannuation payment (DASP)

15.0%

47.0%

15.0%

30.0%

47.0%***

30.0%

47.0%***

47.0%***

$0 – $1,415,000 untaxed plan cap

over $1,415,000

$0 – $195,000

$195,000 – $1,415,000

over $1,415,000

$0 – $1,415,000

over $1,415,000

Thresholds^^ Tax Rates*

Superannuation Benefits – Lump Sums (2016/2017)

Mentor Education 13

Financial Adviser Pocket Guide 2016 - 2017

**Where benefits have been subject to tax in the fund, amounts are not assessable, not exempt income.

Medicare levy (2.0%) will apply to assessable amounts.

Tax free component

Taxable component – taxed element^

Age 60 & over

Preservation age to age 59

Under preservation age

0%**

Marginal tax rate with 15% tax offset

Marginal tax rate with no tax offset

Taxable component – untaxed element^

Age 60 & over

Age 59 & under

Under preservation age

Marginal tax rate with 10% tax offset

Marginal tax rate with no tax offset

Marginal tax rate with no tax offset

Thresholds^^

Superannuation Benefit – Income Streams (2016/2017)

Medicare levy (2.0%) will apply to assessable amounts.

LUMP SUM – paid to dependent

LUMP SUM – paid to non-dependent

Tax free component

Taxable component:

Taxed element

Untaxed element

0%

15.0%

30.0%

0%

PENSION – deceased/primary

beneficiary over 60

0%

PENSION – Primary beneficiary under 60

Tax free component

Taxable component

0%

Marginal tax rate with 15% tax offset for

individuals between preservation age

and age 60

Maximum tax rates

Superannuation Death Benefit Payments (2016/2017)

Mentor Education 14

Financial Adviser Pocket Guide 2016 - 2017

Superannuation Income Streams

The following percentage factors are used to calculate the minimum pension payments for

account-based income streams commenced on or after 20 September 2007.

ACCOUNT-BASED PENSION

Minimum income stream percentage factors*

Minimum income stream standard

Mentor Education 15

Financial Adviser Pocket Guide 2016 - 2017

Age

Under 65

2016/2017 year

4.00%

65 – 74 5.00%

*Amount calculated on 1 July each year, unless first year of

account-based income stream, then pro-rated from

commencement day. Minimum amount rounded to nearest

$10.

Must make minimum payment at least annually. No payment required in first

year if person commenced between 1 June and 30 June.

Maximum 10% pa for ‘transition to retirement’ pension.

75 – 79 6.00%

80 – 84 7.00%

85 – 89 9.00%

90 – 94 11.00%

95 and over 14.00%

Preservation Age

Account based income stream payments

Maximum payment

Minimum payment Account balance x percentage factor

No limit*

Mentor Education 15

Financial Adviser Pocket Guide 2016 - 2017

Must be paid annually. Minimum payment must ensure withdrawal value is equal to no

more than 100% of the purchase price of the pension, or be a lifetime pension and

have no residual capital and the first year pension equal to or more than the purchase

price of the pension multiplied by respective percentage factor.

Existing income streams are deemed to satisfy the minimum income stream

requirements.

Non-account based income streams (from 20/9/07)

Minimum payment

Age Min

50

51

52

53

54

55

56

57

58

59

60

61

21.5

21.2

20.9

20.5

20.1

19.8

19.4

19.0

18.6

18.2

17.8

17.4

Max

9.9

9.9

9.8

9.7

9.7

9.6

9.5

9.4

9.3

9.1

9.0

8.9

Age Min

62

63

64

65

66

67

68

69

70

71

72

73

17.0

16.6

16.2

15.7

15.3

14.9

14.4

14.0

13.5

13.1

12.6

12.2

Max

8.7

8.5

8.3

8.1

7.9

7.6

7.3

7.0

6.6

6.2

5.8

5.4

Age Min

74

75

76

77

78

79

80

81

82

83

84

85

11.7

11.3

10.8

10.4

10.0

9.5

9.1

8.7

8.3

7.9

7.5

7.1

Max

4.8

4.3

3.7

3.0

2.2

1.4

1.0

1.0

1.0

1.0

1.0

1.0

Purchase price of income stream x percentage factor

For pensions and annuities that commenced prior to 1 January 2006, providers can choose the

percentage factors for the minimum income stream percentage factors or the pension valuation

factors (PVF).

ALLOCATED PENSIONS AND ANNUITIES

Minimum and Maximum Pension Valuation Factors (PVF)

Mentor Education 16

Financial Adviser Pocket Guide 2016 - 2017

Age Min

50

51

52

53

54

55

56

57

58

59

60

61

22.8

22.5

22.2

21.8

21.5

21.1

20.8

20.4

20.1

19.7

19.3

18.9

Max

12.0

11.9

11.8

11.8

11.7

11.5

11.4

11.3

11.2

11.0

10.9

10.7

Age Min

62

63

64

65

66

67

68

69

70

71

72

73

18.5

18.1

17.7

17.3

16.8

16.8

16.0

15.5

15.1

14.6

14.2

13.7

Max

10.5

10.3

10.1

9.9

9.6

9.3

9.1

8.7

8.4

8.0

7.6

7.2

Age Min

74

75

76

77

78

79

80

81

82

83

84

85

13.3

12.8

12.3

11.9

11.4

10.9

10.5

10.0

9.6

9.1

8.7

8.3

Max

6.7

6.2

5.7

5.1

4.5

3.8

3.1

2.3

1.4

1.0

1.0

1.0

For pensions and annuities that commenced from 1 January 2006 to 20 September 2007, providers

can choose the percentage factors for the minimum income stream percentage factors or the

pension valuation factors (PVF).

ALLOCATED PENSIONS AND ANNUITIES

Minimum and Maximum Pension Valuation Factors (PVF)

Mentor Education 17

Financial Adviser Pocket Guide 2016 - 2017

TermRemaining

(years) Min

45

44

43

42

41

40

39

38

37

36

35

31

34

33

32

22.50

22.28

22.06

21.83

21.60

21.36

21.10

20.84

20.57

20.29

20.00

18.74

19.70

19.39

19.07

PaymentFactor

TermRemaining

(years)

15

14

13

12

11

10

9

8

7

6

5

1 or less

4

3

2

11.52

10.92

10.30

9.66

9.00

8.32

7.61

6.87

6.11

5.33

4.52

1.00

3.67

2.80

1.90

PaymentFactor

TermRemaining

(years)

30

29

28

27

26

25

24

23

22

21

20

16

19

18

17

18.39

18.04

17.67

17.29

16.89

16.48

16.06

15.62

15.17

14.70

14.21

12.09

13.71

13.19

12.65

PaymentFactor

TERM ALLOCATED PENSIONS (TAP) AND ANNUITIES

Payment Factors

Employment Termination PaymentsAn employment termination payment (ETP) is a payment made in consequence of the termination of

employment. It can include:

*The rates excludes Medicare Levy of 2.0%

**Includes Temporary Budget Repair Levy of 2.0%

^Indexed to AWOTE and will only increase in $5,000 increments.

*The rates excludes Medicare Levy of 2.0%

**Includes Temporary Budget Repair Levy of 2.0%

^Indexed to AWOTE and will only increase in $5,000 increments.

Tax free component

Taxable component

Under preservation age

Preservation age or over

$0 – $195,000^

Balance

$0 – $195,000^

Balance

30.0%

47.0%**

15.0%

47.0%**

0%

Thresholds^^ Maximum tax rate*

Life benefit employment termination payments (2016/2017)

Dependent

Tax free component

Taxable component $0 – $195,000^

Balance

0%

0%

47.0%**

Non-dependent

Tax free component

Taxable component $0 – $195,000^

Balance

0%

30.0%

47.0%**

Thresholds^^ Maximum tax rate*

Death benefit employment termination payments (2016/2017)

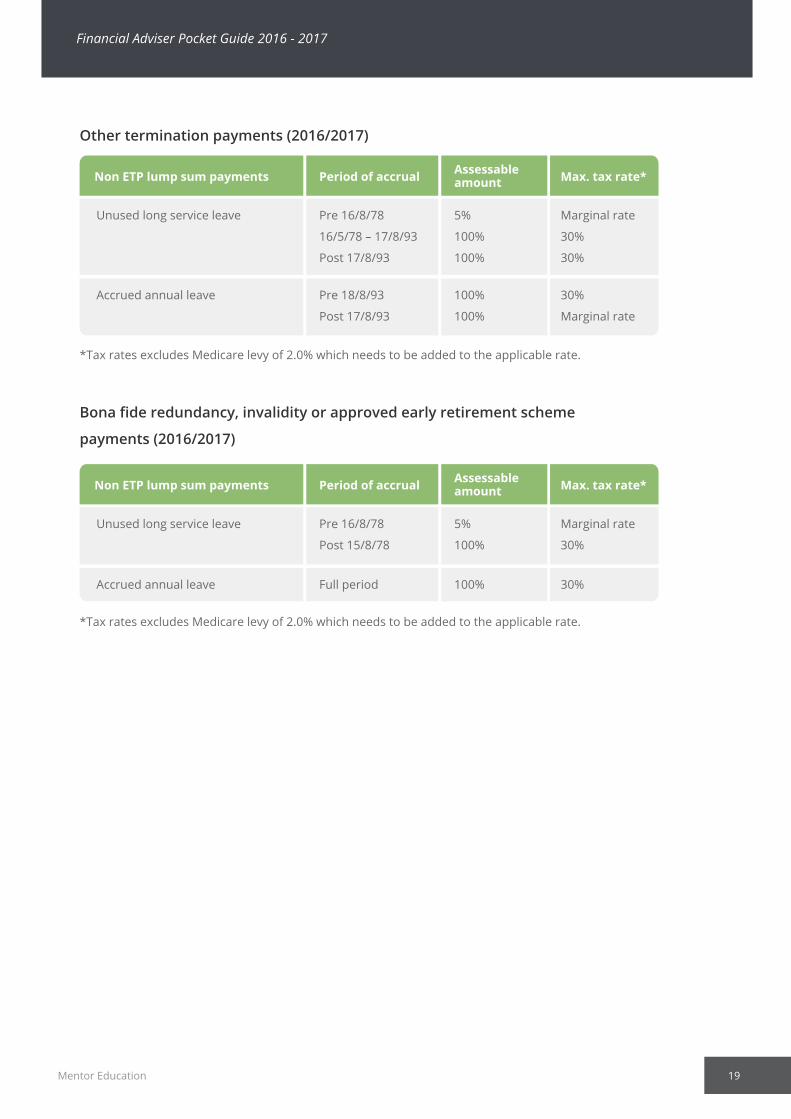

Bona fide redundancy Tax-Free Amount (2016/2017)

Mentor Education 18

Financial Adviser Pocket Guide 2016 - 2017

$9,936 (base amount) plus $4,969 (service amount) for each completed year of service. This is

non-ETP and cannot be rolled over to a super fund.

*Tax rates excludes Medicare levy of 2.0% which needs to be added to the applicable rate.

Unused long service leave Pre 16/8/78

16/5/78 – 17/8/93

Post 17/8/93

Marginal rate

30%

30%

Period of accrual

5%

100%

100%

Assessable amountNon ETP lump sum payments Max. tax rate*

Other termination payments (2016/2017)

Mentor Education 19

Financial Adviser Pocket Guide 2016 - 2017

Accrued annual leave Pre 18/8/93

Post 17/8/93

30%

Marginal rate

100%

100%

*Tax rates excludes Medicare levy of 2.0% which needs to be added to the applicable rate.

Unused long service leave Pre 16/8/78

Post 15/8/78

Marginal rate

30%

Period of accrual

5%

100%

Assessable amountNon ETP lump sum payments Max. tax rate*

Bona fide redundancy, invalidity or approved early retirement scheme

payments (2016/2017)

Accrued annual leave Full period 30%100%

Age PensionAcceptance of contributions

Basic Pension Rates (effective from 20 March to 19 September 2016)

Mentor Education 20

Financial Adviser Pocket Guide 2016 - 2017

Social SecuritySocial Security

Date of Birth

Men and Women

1 July 1952 – 31 December 1953

1 January 1954 – 30 June 1955

1 July 1955 – 31 December 1956

1 January 1957 – 30 June 1958

1 July 1958 – 31 December 1959

1 January 1960 – 30 June 1961

1 July 1961 – 31 December 1962

1 January 1963 – 30 June 1964

1 July 1964 – 31 December 1965

1 January 1966 and later

65.5

66.0

66.5

67.0

68.0

68.5

69.0

69.0

69.5

70.0

Eligible for Age Pension at Age

Family Situation

$873.90 $22,721.40

Couple (each)

Single

$658.70 $17,126.20

Maximum Benefit*(per fortnight)

Maximum Benefit*(per annum)

*These amounts do not include the Supplement amount of $65.00 a fortnight for singles and $49.00 a

fortnight for couples (each) or Clean Energy Supplement amount of $14.10 a fortnight for singles and

$10.60 a fortnight for couples (each). The ‘Pension Rates’ are adjusted twice yearly – in March and

September in line with increase in the cost of living. This includes the higher of the increase in the

Consumer Price Index (CPI) and the increase in the Pensioner and Beneficiary Living Cost Index (PBLCI).

Allowance Rates (effective from 20 March to 19 September 2016)

Mentor Education 21

Financial Adviser Pocket Guide 2016 - 2017

Family Situation

$527.60 $13,717.60

Single, 22 or over, with dependent children

Single, 22 or over, no children

$570.80 $14,840.80

$570.80 $14,840.80

Couple (each)

Single, 60 or over after 9 months

Single principal carer of a dependent child

(granted an exemption for foster

caring/home schooling/distance

education/large family)

$476.40 $12,386.40

$737.10 $19,164.60

Maximum Benefit*(per fortnight)

Maximum Benefit*(per annum)

Income Test for Pensions (effective from 1July to 19 September 2016)

Family Situation

$164 $1,911.80

Couple (combined)

Single

$292 $2,926.80

Couple separated due to illness (combined) $288 $3,787.60

Income Threshold*(per fortnight)

Income cut-out(per fortnight)

*These amounts include a Supplement amount for recipients under Age Pension age. Excludes

Pharmaceutical Allowance (PhA). PhA may be paid in certain circumstances. Payment may be deferred

where liquid assets equal or exceed $5,500 for singles or $11,000 for couples and those with depen-

dent children, Partner and Special Benefits.

*Income over these amounts reduces the rate of pension by 50 cents in the dollar (single), or 25 cents

in the dollar each (for couples). The lower threshold is normally adjusted in line with the Consumer

Price Index (CPI) on 1 July of each year. The upper threshold is adjusted on 1 July of each year, and

also adjusted on 20 March and 20 September of each year.

Income Test for Allowances (effective from 1 July to 19 September 2016)

Mentor Education 22

Financial Adviser Pocket Guide 2016 - 2017

Family Situation

$104 $1,023.00

Single, 22 or over, with dependent children

Single, 22 or over, no children

$104 $1,096.17

$104 $1,106.50

Couple (each)

Single, 60 or over after 9 months

Single principal carer of a dependent child

(granted an exemption for foster

caring/home schooling/distance

education/large family)

$104 $ 936.17

$104 $1,976.75

Income Threshold*(per fortnight)

Income cut-out(per fortnight)

*Fortnightly income between $104 and $254 reduces fortnightly allowance by 50 cents in the dollar.

For income above $250.00 per fortnight reduces fortnightly allowance by $75 plus 60 cents for each

dollar over $254. Partner income which exceeds cut-out point reduces fortnightly allowance by 60

cents in the dollar. This point is where the allowance would not be payable.

Deeming Rates (effective from 1 July t0 19 September 2016)

Family Situation

$0 – $49,200

Balance

1.75%

3.25%

Single

(Pension or Allowance)

$0 – $81,600

Balance

1.75%

3.25%

Couple – combined

(Pensioner)

Couple – for each allowee

(Neither is pensioner)

$0 – $40,800

Balance

1.75%

3.25%

FinancialInvestment Deeming Rate

Note: Deeming rates are set by agreement between the Ministers for the Department of Families,

Housing, Community Services and Indigenous Affairs (FaHCSIA) and the Department of Education,

Employment and Workplace Relations (DEEWR).

Assets Test Limits for Allowances and Parenting Paymt Single (effective from I Jul to 31 Dec 2016)

Family Situation

$202,000 $348,500

Couple (combined)

Single

$286,500 $433,000

One partner eligible (combined assets) $286,500 $433,000

Homeowner Non-Homeowner

Income Test for Allowances (effective from 1 July to 31 December 2016)

Mentor Education 23

Financial Adviser Pocket Guide 2016 - 2017

Family Situation

1 Jul 2016 to 31 Dec 2016 1 Jul 2016 to 31 Dec 2016

Single

Home owner

$209,000 $ 791,750

$296,500 $1,175,000

Couple separated due to illness (combined)

Couple (combined)

$296,500 $1,462,000

One partner eligible (combined assets) $296,500 $1,175,000

Single

Non-home owner

$360,500 $ 943,250

$448,000 $1,326,500

Couple separated due to illness (combined)

Couple (combined)

$448,000 $1,613,500

One partner eligible (combined assets) $448,000 $1,326,500

Lower Threshold* Upper Threshold

Assets over these amounts reduces the rate of pension by $1.50 per fortnight for every $1,000 above

the amount (single and couple combined). The lower threshold is normally adjusted in line with the

Consumer Price Index (CPI) on 1 July of each year. The upper threshold is adjusted on 1 July of each

year, and also adjusted on 20 March and 20 September of each year. From 1 January 2017 the assets

test free area and the assets taper rate will increase to $3 for every $1,000 above the new assets test

free areas:-

$250,000 for a single homeowner

$375,000 for a homeowner couple

$450,000 for a single non-homeowner

$575,000 for a non-homeowner couple.

Life expectancy for people at each age

Mentor Education 24

Financial Adviser Pocket Guide 2016 - 2017

Age

Male Female

32.2050 35.67

31.2951 34.74

30.3852 33.80

29.4953 32.87

28.5954 31.95

27.7155 31.12

26.8356 30.10

25.9557 29.19

25.0958 28.28

24.2259 27.37

23.3760 26.47

22.5261 25.57

21.6862 24.68

20.8563 23.80

20.0364 22.92

19.2265 22.05

18.4166 21.18

17.6267 20.33

16.8468 19.48

16.0769 18.64

15.3170 17.80

14.5671 16.98

13.8372 16.18

13.1173 15.38

12.4074 14.60

11.7275 13.83

Life Expectancy (yrs) Age

Male Female

11.0576 13.08

10.4177 12.33

9.7878 11.61

9.1879 10.90

8.6080 10.21

8.0481 9.55

7.5182 8.90

7.0083 8.29

6.5284 7.70

6.0685 7.14

5.6486 6.61

5.2487 6.11

4.8788 5.65

4.5289 5.22

4.2190 4.82

3.9291 4.45

3.6692 4.12

3.4493 3.82

3.2494 3.55

3.0695 3.32

2.9196 3.11

2.7897 2.93

2.6798 2.77

2.5799 2.62

2.46100 2.50

2.46100+ 2.50

Life Expectancy (yrs)

The life tables depict the mortality experience of a hypothetical group of newborn babies throughout

their entire lifetime. It is based on the assumption that this group is subject to the age-specific

mortality rates of the referenced period.

Life Tables, Australia, 2010 – 2012

Consumer Price Index (CPI)

Mentor Education 25

Financial Adviser Pocket Guide 2016 - 2017

2015 106.8

Mar 31 Jun 30 Sep 30

2016 108.2

2014 105.4 105.9 106.4 106.6

107.5 108.0 108.4

2013 102.4 102.8 104.0 104.8

2012 99.9 100.4 101.8 102.0

2011 98.3 99.2 99.8 99.8

2010 95.2 95.8 96.5 96.9

2009 92.5 92.9 93.8 94.3

2008 90.3 91.6 92.7 92.4

2007 86.6 87.7 88.3 89.1

2006 84.5 85.9 86.7 86.6

2005 82.1 82.6 83.4 83.8

2004 80.2 80.6 80.9 81.5

2003 78.6 78.6 79.1 79.5

2002 76.1 76.6 77.1 77.6

2001 73.9 74.5

74.7 75.4

2000 69.7 70.2 72.9 73.1

1999 67.8 68.1 68.7 69.1

1998 67.0 67.4 67.5 67.8

1997 67.1 66.9 66.6 66.8

1996 66.2 66.7 66.9 67.0

1995 63.8 64.7 65.5 66.0

1994 61.5 61.9 62.3 62.8

1993 60.6 60.8 61.1 61.2

1992 59.9 59.7 59.8 60.1

1991 58.9 59.0 59.3 59.9

Dec 31

Continue nex page

Average Weekly Ordinary Time Earnings (AWOTE)

2007 $1,073.80

Mar 31 Jun 30 Sep 30

2008 $1,124.80 $1,131.10 $1,151.40 $1,165.30

$1,090.00 $1,105.10 $1,108.50

2009 $1,183.40 $1,195.60 $1,204.20 $1,226.80

2010 $1,243.90 $1,250.10 $1,258.80 $1,275.20

2011 $1,291.30 $1,304.70 $1,324.90 $1,330.10

2012 $1,348.10 $1,349.20 n.a.** $1,396.00

2013 n.a.** $1,420.90 n.a.** $1,437.00

2014 n.a.** $1,454.10 n.a.** $1,477.00

2015 n.a.** $1,483.10 n.a.** $1,500.50

2016 n.a.**

Dec 31

Note: The ABS changed the index reference base in September 2012 from 1989-90 to

2011-12. As a result all CPI rates have been rest and the previous rates no longer apply

and can no longer be used for tax and superannuation purposes.

**Changed to biannual, not quarterly.

Mentor Education 26

Financial Adviser Pocket Guide 2016 - 2017

1990 56.2 57.1 57.5 59.0

1989 51.7 53.0 54.2 55.2

1988 48.4 49.3 50.2 51.2

1987 45.3 46.0 46.8 47.6

1986 41.4 42.1 43.2 44.4

1985 37.9 38.8 39.7 40.5

Mentor Education 27

Financial Adviser Pocket Guide 2016 - 2017

Online ResourcesOnline Resources

Organisation Web Link Services

Mentor Education Group Financial services training for

industry professionals.

www.mentor.edu.au

Department of Education,

Employment and Workplace

Relations

Info on HECS – HELP and higher

education.

www.goingtouni.gov.au

My Aged Care Info on Government and

non-Government services for

Australians over 50.

http://www.myagedcare.gov.au/

Australian Taxation Office Info on individual taxation,

superannuation, business

taxation.

www.ato.gov.au

Australian Securities and

Investments Commission

Regulatory guidelines and

compliance information for

financial services industry

professionals.

Australian Securities and

Investments Commission

Consumer information on

money tips, financial calculators

and general financial literacy

education.

Australian Securities Exchange Info on stock quotes, market

data, share prices, tools and

resources as well as investment

information.

www.asic.gov.au

www.fido.asic.gov.au

www.asx.com.au

Centrelink Info on Govt allowances and

pensions, family tax and child

care benefits, health care cards,

study and training benefits,

carers, illness and disability

payments.

www.centrelink.gov.au

DISCLAIMER

Webwww.mentor.edu.au

PhoneAust: 1300 306 146

Int: +61 3 8317 2900

Our friendly student support

The financial information provided is believed to be accurate as at 8 August 2016. However, all financial

information is subject to regular rate changes and legislation amendments. Therefore, the information is

intended as a guide only and should be used in conjunction with the latest Government information.