financial estate planning considerations and tax strategies for executives and business owners...

TRANSCRIPT

Financial Estate Planning Considerations and

Tax strategies for Executives and Business

Owners

Whitney Hammond CFP, CLU Scott Sadler FSA, FCIA Steve Shillington CA, CFP, TEP

Agenda

1. Comprehensive planning

2. Tax and estate planning strategies

3. Life insurance ‘tax shelter’

4. Questions

Total Planning

• Financial, estate, tax and business exit strategy planning can’t be done in isolation from personal goals and values

• Business exit strategy and succession planning can’t be isolated from:– Personal estate planning– Personal financial planning– Personal tax planning

Planning Pyramid

Community(Social

Capital Legacy)

1

3

2

Financial Status Financial Goals

Values,Goals & Objectives

Family(Family Legacy)

Self (Financial Independence)

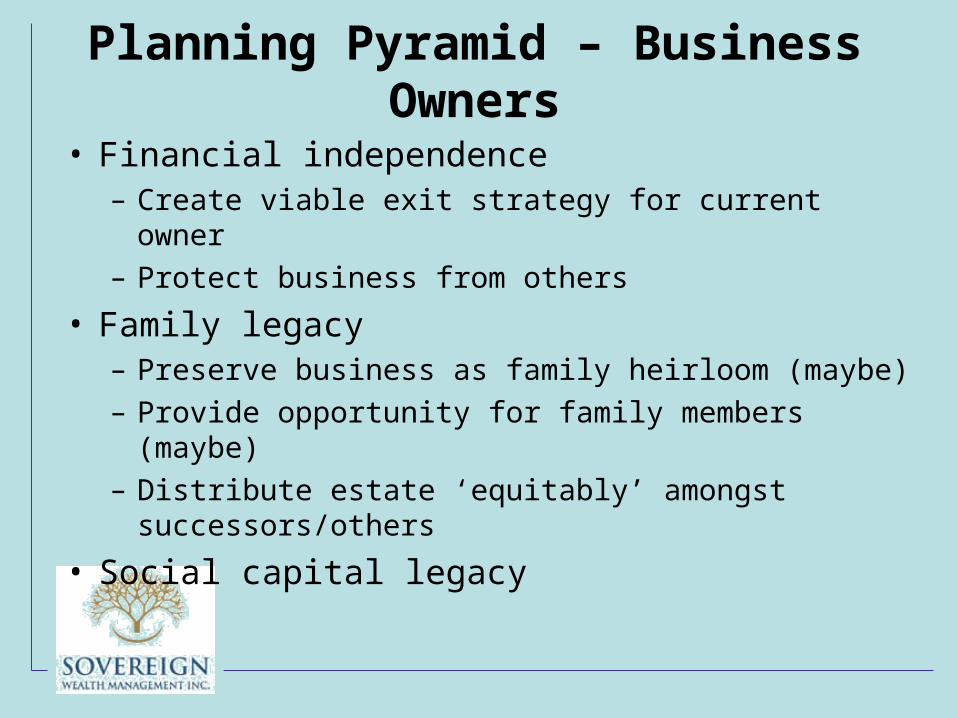

Planning Pyramid – Business Owners

• Financial independence– Create viable exit strategy for current owner– Protect business from others

• Family legacy– Preserve business as family heirloom (maybe)– Provide opportunity for family members (maybe) – Distribute estate ‘equitably’ amongst

successors/others

• Social capital legacy

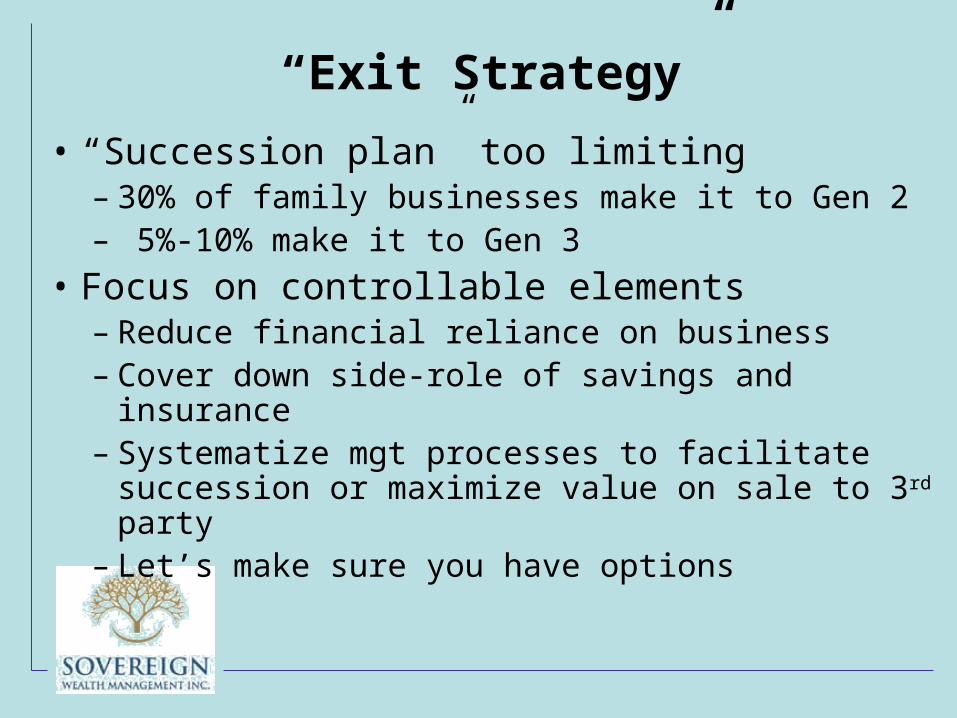

“Exit Strategy”

• “Succession plan” too limiting– 30% of family businesses make it to Gen 2 – 5%-10% make it to Gen 3

• Focus on controllable elements– Reduce financial reliance on business – Cover down side-role of savings and insurance– Systematize mgt processes to facilitate

succession or maximize value on sale to 3rd party– Let’s make sure you have options

Incorporation (professionals)

• Creditor protection (business creditors)

• Tax deferral if not spending all you earn

• Income splitting– Salary to spouse and children (must support $$)– Dividends

• With spouse (Where spouse allowed to own shares) • With children age 18+ (to avoid ‘kiddie tax’)

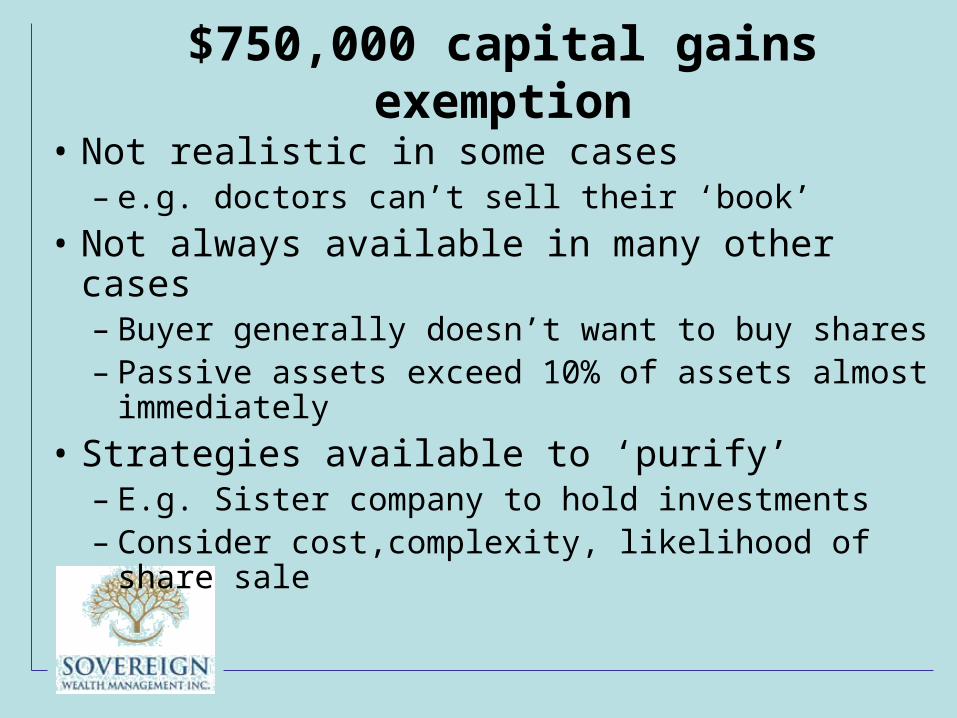

$750,000 capital gains exemption

• Not realistic in some cases– e.g. doctors can’t sell their ‘book’

• Not always available in many other cases– Buyer generally doesn’t want to buy shares – Passive assets exceed 10% of assets almost

immediately

• Strategies available to ‘purify’ – E.g. Sister company to hold investments– Consider cost,complexity, likelihood of share sale

New Tax Rates: Change in Plans?

First $500,000

$500,000-$1,500,000 M&P

$500,000-$1,500,000 Other

Over $1,500,000 M&P

Over $1,500,000 Other

Investment income

2009

16.5%

34.3%

37.3%

31.0%

33.0%

48.7%

2013

15.5%

25.0%

25.0%

25.0%

25.0%

44.7%

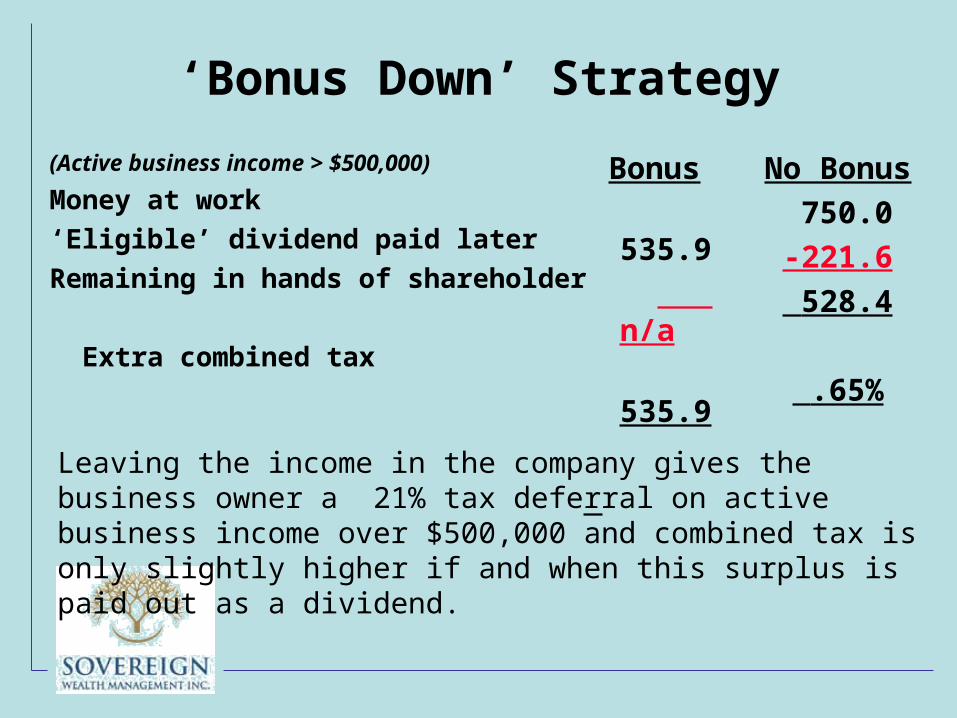

‘Bonus Down’ Strategy

(Active business income > $500,000)

Corporate active business income

Bonus

Remaining income

Corporate tax (2012+)

Remaining in the company

Salary

Personal tax (assuming highest rate)

After tax personally

Money at work after tax

Bonus

1,000.0

-1,000.0

0.0

-0.0

0.0

1,000.0

-464.1

535.9

535.9

No Bonus

1,000.0

-0.0

1,000.0

-250.0

750.0

0.0

0.0

0.0

750.0

‘Bonus Down’ Strategy

(Active business income > $500,000)

Money at work

‘Eligible’ dividend paid later

Remaining in hands of shareholder

Extra combined tax

Bonus

535.9

n/a

535.9

No Bonus

750.0

-221.6

528.4

.65%

Leaving the income in the company gives the business owner a 21% tax deferral on active business income over $500,000 and combined tax is only slightly higher if and when this surplus is paid out as a dividend.

‘Bonus Down’ Strategy

• Consider not ‘bonusing down’ to $500,000

• Some of the other considerations– Maximize CPP? (if not done with base salary)– Maximize RRSP? (if not done with base salary)– Creditor protection (bonus and loan back net if

no holding company)– Maintain eligibility for $750K capital gains

exemption

Holding Company

Before After

Owner Owner 100% 100%

100%

Business

Holding Company

Business

• Holding company

Holding Company

• Benefits– Asset protection

• Tax-free dividend up to Holdco• Loan back as secured note - maintain working capital • Out of reach of general creditors of business

– Real estate and portfolio investments• Sisterco to maintain Opco eligibility for $750K CGE

– Income splitting-dividends-shares to children(18+)

• Note: doesn’t help with 750K CGE purification

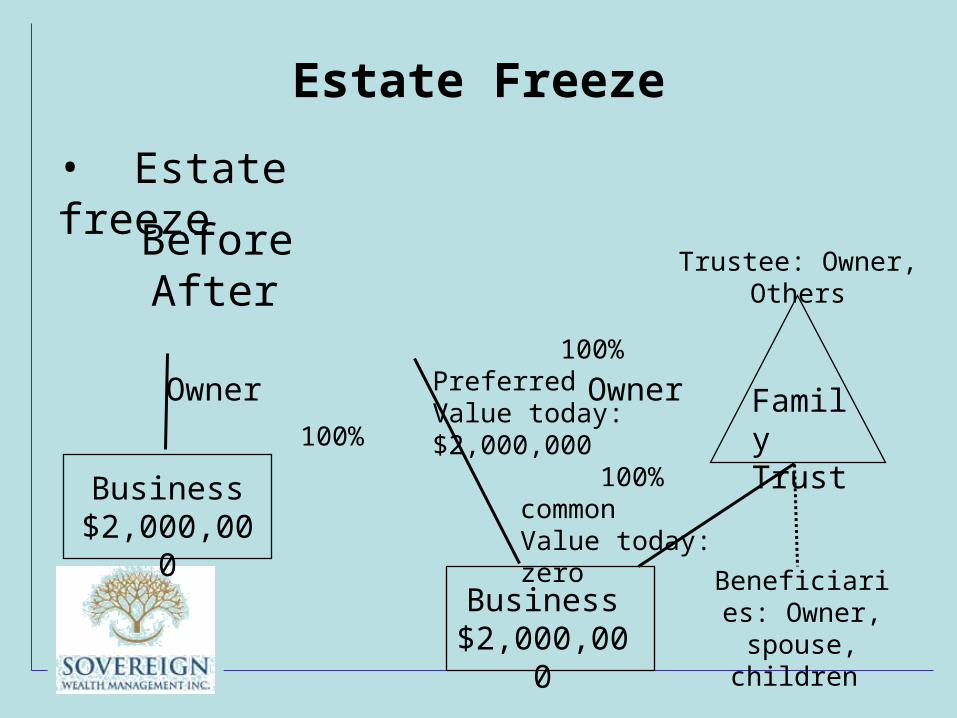

Estate Freeze

Before After

Owner Owner

100%

Business $2,000,000

Business $2,000,000

Family Trust

100% commonValue today: zero

100% PreferredValue today: $2,000,000

Trustee: Owner, Others

Beneficiaries: Owner, spouse,

children

• Estate freeze

Estate Freeze

• Benefits of a freeze– On future growth (above $2,000,000 in this case)

• Defer tax at death by one or more generations• Multiply $750,000 capital gains exemption

– Sprinkle dividends to low income family members

• Benefits of discretionary family trust– Defer decision on who gets shares (by 21 years)– Ability to reverse freeze – distribute to parents

Personal strategies-Investments

• TFSA: re-contribution pitfall

• Spousal loan

• Gift of marketable securities

Will and Probate Planning

• Estate administration tax (EAT) – Probate of a will:

• Establishes legitimacy of the ‘executor/administrator’ • Frees financial institutions to release assets• A ‘probate’ judge certifies the will

– Probated will subject to EAT (‘probate tax’)• $5/$1,000 on 1st $50,000, $15/$1,000 on excess• Applicable to ALL assets that pass through that will

e.g. $2,000,000 estate attracts $30,000 of EAT

Strategies to Reduce EAT

• Dual wills – separate will for shares of and debt receivable from private companies

• Spouses hold assets in joint tenancy • Named beneficiaries on RRSPs, insurance• Inter-vivos Trust• Don’t let EAT planning drive bad decisions

– e.g. Insufficient assets to pay tax/final expenses– e.g. Joint ownership with children -triggers capital gain

Testamentary Trusts • Control and protection

– Creditor protection– Protection from family law claims

• Spousal– Assets must ‘vest indefeasibly’

• Children and grandchildren– Allow beneficiary to become trustee– Don’t force the trust to be wound up at certain age

• Tax savings– Annual tax savings of up to $18,000/yr.– Depends on size of trust and other income of beneficiary

Estate Gifts

• Will must name charity

• Will must specify dollar amount or % of residual

• Donation can be used on final tax return of deceased or by estate

Insured Gift of Private Corp. Shares

• Will amended to bequeath shares to charity• Insurance equal to value of shares purchased• At death

– Shares bequeathed to charity by Estate– Company redeems shares using insurance proceeds– Residual capital dividend account created by insurance

proceeds-used to distribute other surplus or future earnings to the heirs as tax free capital dividends

Insured Gift of Private Corp. Shares

• Example– $2,000,000 of shares– $1,000,000 of life insurance

• Options– Do nothing– Estate gives $1,000,000 of shares to the Charity – Estate gives $1,000,000 of shares to the Charity and

the Company purchases $1,000,000 insurance to redeem those shares at death

Insured Gift of Private Corp. Shares

No

Donation

$ 1,536,000

$ 0

$ 464,000

$ 0

Donation of

$1,000,000

Shares

$ 1,000,000

$ 1,000,000

$ 0

$ 0

Insured

Donation

of Shares

$ 1,000,000

$ 1,000,000

$

$ 1,000,000

Family

Charity

Tax

CDA

Additional win for life insurance if it’s less expensive than alternatives for funding share redemption

Asset diversification

• Cash, fixed income, equities, real estate

• Private business– Entrepreneurs comfortable with heavy focus on

one investment (the business)– Foolish to suggest there are better investments– However, viewing business in context of

investment asset allocation is legitimate consideration

Net Worth Statement Mr. Mrs. Total Life insurance cash value 20,000 0 20,000 RRSP 95,000 18,000 113,000 Non-registered and RESP 3,000 2,000 5,000 Shares of holding company 4,775,000 0 4,775,000 Real estate 315,000 0 315,000 Financial assets Home

5,208,000 0

20,000 380,000

5,228,000 380,000

Household effects (est.) 40,000 40,000 80,000 Total assets 5,248,000 440,000 5,688,000 Total liabilities 0 33,000 33,000 Net worth 5,248,000 407,000 5,655,000

88% of financial net worth is in equities *including the business) and real estate

Value of Holding Company

Value of operating company (subsidiary)

Real estate

Investibles-equities

Investibles-fixed income

FMV of shares of holding company

2,275,000

1,500,000

500,000

500,000

4,775,000

Life Insurance Strategies

• Participating life insurance • a.k.a. ‘Investment grade’ permanent insurance• Return of profit mechanism (‘dividends’)• Values vest at each anniversary (can’t go down)• Stable patterns of cash and death benefit growth• Largely backed by fixed income

Insured Asset Transfer

• Reposition non-registered assets into permanent life insurance– Tax shelter fixed income – Cash value growth is tax deferred – Cash value growth is tax free to extent left

until death• Can be done personally or inside

corporation

Corporate Insured Asset Transfer an example

• Clients are married couple• Both age 55• Standard medical rating, non-smokers• $1,000,000 coverage suggested to cover

tax at death• Range of options considered:

– Minimum funded universal life – Participating whole life with maximum funding

Corporate Insured Asset Transfer an example

• Product: maximum funded whole life– 10 annual deposits of $42,582– Owned in holding company

• Compare to fixed income investments– Earning 5% interest– Taxed at 47.7% (passive income)

• Compare asset in company and net amount paid to executor of estate

Estate and Cash Position

$-

$1,000,000

$2,000,000

$3,000,000

65 75 85 95Age

Net Estate-InsuranceCorporate Asset-Insurance Cash Surrender Value

Corporate Asset-InvestmentNet Estate-Investment

No values guaranteed-not valid without accompanying illustrations of policy values including disclaimers and sensitivity analyses

Enhanced Retirement IncomeAssumptions

• Male 42, standard, non-smoker

• Considering $5M cash value life insurance policy to diversify portfolio

–Premiums are $170K x 5 years

• At age 65, assign insurance policy to a bank as collateral for annual loan advance

–Annual draw is $130K to age 90–Tax free under current Canadian tax law

Enhanced Retirement Income

• Deposits and loan advances occur at the beginning of year, values at end of year

• Life insurance cash values based on current dividend scale

• Collateral Loan based on 7.5% gross rate

• Loan interest is deductible

• Tax savings applied to reduce loan balance

Enhanced Retirement Income

Capital Efficiency Test • Life Insurance

– Annual $130K loan advance (tax-free) to age 90

• Equities– $169K pre-tax nets $130K @ 23.2% tax

• Fixed Income– $242K pre-tax nets $130K @ 46.4% tax

• Dividends– $189K pre-tax nets $130K @ 31.3% tax

Capital Efficiency Test

To Provide an Equivalent After-tax Income

Why Life Insurance?

• One tool in your financial planning toolkit

• Tax sheltered growth, no CRA deposit limit

• Creditor protected

• Free from probate if properly structured

• A private tool for wealth transfer to future generations

• An efficient use of fixed income assets

Questions

Thank you for participating in our presentation today.

Whitney Hammond and team can be reached at:

905-637-3500

627 Guelph Line, Burlington, L7R 3M7

www.sovereignwealth.ca