financial institution network and the certification value of bank loans

TRANSCRIPT

Financial institution network and the certification value of bank loans

Christophe J. GodlewskiUHA & EM Strasbourg

Bulat SanditovTelecom EM

AFFI Conference 2015, Cergy-Pontoise

Take away

2

• Financial institutions network and reputation

• Certification value of bank loans

• European syndicated loans (2001-11)

• Social network analysis + event study methodologies

• Presence of central and reputable lenders increase

borrower’s stock market reaction to a loan announcement

• Stronger effect when informational frictions are important

• Effect vanishes away during severe distruption in the

functioning of financial markets

Background & motivations

3

• Banks produce private information on borrowers (Diamond 1984…)

• Bank loans bear a certification value => AR > 0 for borrower’s stock around the date of bank loan announcement (James 1987…)

• Maintaining reputation for diligent screening & monitoring => mitigate informational frictions & agency problems

• Syndicated loans market (4.7 trln $, 2014): lead bank reputation is crucial (Ross 2010…)

• Lead bank = structure deal, negotiate loan terms, organize syndicate

• Reputable leader => enhance monitoring, attract participants, signal quality, reduce agency costs…

Background & motivations (cont.)

4

• Lender reputation trust & reciprocity = critical forms of social capital (Song 2009) driven by social networks (Cagno& Sciubba 2010)

• Social network features of syndicated lending market = information & capital networks (Baum et al. 2003, 2004)

• Repeated interactions => trust & reciprocity => solve informational frictions => mitigate agency problems• => important for firms seeking external financing

(Brander et al. 202, Wang & Wang 2012)• => affect pricing and structure of bank loan agreements

(Cai 2009, Godlewski et al. 2012, Gatti et al. 2013)

Aim & contributions

5

• Do banks’ network/reputation affect certification value of

bank loans?

1. Impact of bank network/reputation on certification value

of bank loan => borrower AR / event study methodology

2. Social network metrics (Centrality centrality) to proxy

reputation => richer / comprehensive measure

3. European focus => bank private debt = main source of

external financing for companies

Empirical design | Data

6

• Loan and syndicate characteristics : Bloomberg

• Amount, spread, maturity, announcement date…

• Number of lenders, roles (titles)…

• Borrower characteristics : Factset

• Balance sheet & stock market information

• Country characteristics : GFDD (WB) + Djankov et al. (2007)

• European non-financial companies (24 countries)

• January 2001 – June 2011

• 254 companies / 465 loans / 906 lenders

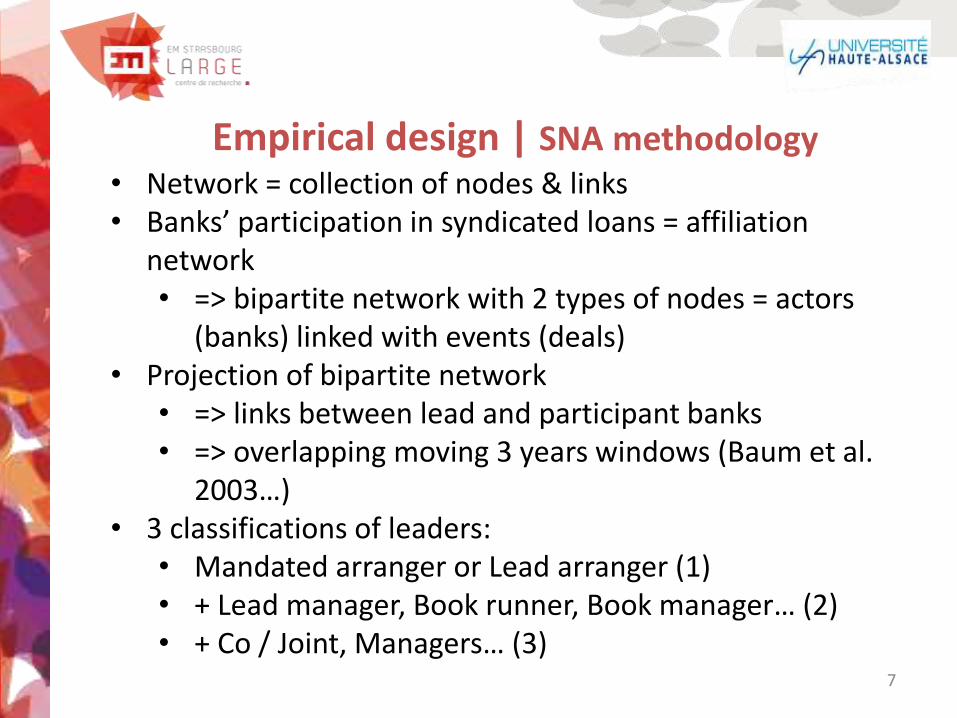

Empirical design | SNA methodology

7

• Network = collection of nodes & links• Banks’ participation in syndicated loans = affiliation

network• => bipartite network with 2 types of nodes = actors

(banks) linked with events (deals)• Projection of bipartite network

• => links between lead and participant banks• => overlapping moving 3 years windows (Baum et al.

2003…)• 3 classifications of leaders:

• Mandated arranger or Lead arranger (1)• + Lead manager, Book runner, Book manager… (2)• + Co / Joint, Managers… (3)

Empirical design | SNA methodology (cont.)

8

(a)

(b)

1 2 3 4 5 6 7 8 9 10

A B C

Lenders

Loans

11

D

1

2

3

4

5

6

7

8

9

10

11

Empirical design | SNA methodology (cont.)

9

• Leaders social network metrics => focus on Centrality centrality• => how well leader is positioned within a network• => control over the flow of information/capital• => interaction, reciprocity, trust => social capital =>

proxy of reputation• Formally = number of the shortest paths between all pairs

of lenders in a network, which pass through a lender, deflated by the number of alternative shortest paths

• Compute average, median and interquartile of Centrality centrality by syndicate• => 3 measures of centrality + 3 classifications of leaders

= 9 measures of network/reputation

Empirical design | Event study methodology

10

• Multi-event and multi-country setting• Modified market model 𝐴𝑅𝑖 = 𝑅𝑖 − 𝑅𝑚 (Fuller et al. 2002)• Use local-currency national market indexes (Campbell et al.

2010)• Bank loan announcement date = event date (day 0)• Excluding contaminated events• Compute three-day period CAR (-1,1)• Multivariate analysis relies on OLS (robust s.e. clustered at

loan level) :𝐶𝐴𝑅 −1, 1 = 𝛼 + 𝛽 × 𝐿𝑒𝑛𝑑𝑒𝑟𝑠 𝑐𝑒𝑛𝑡𝑟𝑎𝑙𝑖𝑡𝑦

+ 𝛾 × 𝐿𝑜𝑎𝑛 𝑣𝑎𝑟𝑖𝑎𝑏𝑙𝑒𝑠 + 𝜃 × 𝐵𝑜𝑟𝑟𝑜𝑤𝑒𝑟 𝑣𝑎𝑟𝑖𝑎𝑏𝑙𝑒𝑠 + 𝜗× 𝐶𝑜𝑢𝑛𝑡𝑟𝑦 𝑣𝑎𝑟𝑖𝑎𝑏𝑙𝑒𝑠 + 𝜀

Results | (some) Descriptive statistics

11

0

2

4

6

8

10

12

14

16

18

20

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Pe

rce

nta

ge

Year

0.0000

0.0050

0.0100

0.0150

0.0200

0.0250

0.0300

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Ce

ntr

alit

y

Year

avg Betweenness (1) med Betweenness (1) iqr Betweenness (1)

Loan

sSy

nd

icat

e ce

ntr

alit

y

Results | (more) Descriptive statistics

12

Variable Mean SD Median

Y = CAR (-1,1) 0.0544 0.0776 -0.0035

avg. Centrality (1) 0.0185 0.0133 0.0173

med. Centrality (1) 0.0100 0.0144 0.0046

iqr. Centrality (1) 0.0224 0.0181 0.0208

Loan amount (mln $) 1300.0000 1900.0000 729.0000

Maturity (y) 5.5236 3.3988 5.0000

Term loan 0.5125 0.4999 1.0000

Secured 0.2022 0.4017 0.0000

Covenants 0.1639 0.3702 0.0000

Syndicate (n) 19.4737 23.0466 13.0000

Tranches (n) 2.2484 2.4971 2.0000

League table 0.4865 0.4999 0.0000

First loan 0.5899 0.4919 1.0000

Loan

var

iab

les

Ce

ntr

alit

y va

riab

les

Results | (more) Descriptive statistics

13

Variable Mean SD Median

Rating 0.3287 0.4698 0.0000

Sales (mln $) 12200.0000 24400.0000 5440.0000

Debt ratio 0.3225 0.1741 0.3240

Ebitda margin -1.5600 94.2942 0.1140

Stock market 0.9289 0.4273 0.8945

Private credit 1.3470 0.4557 1.2992

French law 0.5297 0.4992 1.0000

German law 0.1405 0.3475 0.0000

Creditor rights 2.1323 1.3658 2.0000

Bank Z score 14.5010 6.6430 13.8325

Bank concentration 0.6806 0.1665 0.6558

Crisis 0.2022 0.4017 0.0000

Co

un

try

vari

able

sB

orr

ow

er

vari

able

s

Results | Main regression results

14

Variable avg. Centrality med. Centrality iqr. Centrality

1 2 3 4 5 6 7 8 9

Baseline results (loan & syndicate var.)

Centrality 2.0545 2.1096 2.4473 2.3471 2.7250 2.7259 0.3337 -0.0505 -0.6432

With firm characteristics

Centrality 1.0409 0.8847 0.8788 0.4168 0.3827 0.2190 0.2902 0.3967 0.3133

With country characteristics

Centrality 2.8043 2.2539 2.5384 2.5948 2.4133 2.5824 0.9349 -0.4434 -0.8280

OLS regressions, Y = CAR(-1,1), robust s.e. clustered at loan levelControls = loan currency, purpose, year; borrower industry, countryBold coef. = significant at 10% min. (*)

Results | Interaction terms

15

VariableSmall loan

Short maturity

Secured CovenantsSmall

syndicateLeague table

avg Centrality (1) 0.6244 2.1705 2.0629 3.8361 -3.9506 3.5214avg. Centrality (1) x Variable

2.2794 -0.4267 -0.0232 -9.8643 6.5792 -3.6920

VariableLowsales

Low debtLow

profit

avg Centrality (1) -0.2916 0.4310 1.0274

avg. Centrality (1) x Variable

1.8076 1.0551 0.0530

VariableLowstock

market

Low privatecredit

Low bankz score

High bankconcentration

Weakcreditorrights

Crisis

avg Centrality (1) 2.0932 4.5575 10.0746 3.3854 0.7350 3.2628avg. Centrality (1) x Variable

1.9213 -3.4674 -12.8608 -2.0184 5.1910 -4.3345

Ibid.Interaction variable = dummy (use of sample median for cont. Variables)

Conclusion

16

• Syndicate centrality / reputation matter for certification value of bank loans in Europe

• Presence of central / reputable leaders increase stock market reaction (AR) to a loan announcement

• Impact on AR reinforced when informational frictions are important but effect vanishes away during financial crisis of 2008

• Contribution to recent literature on the role of reputation and networks in financial intermediation

• Important for the development of credit markets, especially in Europe

• Limits = potential endogeneity in matching of borrowers and lenders