financial management 1 (fm101) - imm …imm-gsm.s3.amazonaws.com/2014/docs/semester2/learner...

TRANSCRIPT

IMM GSM© Page 1 of 141 FM101

Financial Management 1 (FM101)

The copyright of all IMM Graduate School of Marketing material is held by the IMM

GSM. No publications may be reproduced without prior written permission from the

IMM GSM.

November 2010

IMM GSM© Page 2 of 141 FM101

Table of contents

Section A

1. Word of welcome

2. How to use this guide

3. The overall purpose of the subject

4. Pre-knowledge

5. The relationship with other subjects

6. The NQF level and number of credits

7. Prescribed textbook and resources required

8. Curriculum

9. Specific learning outcomes

10. Critical Cross-field Outcomes

11. Assessment details

12. Time-line

4

5

6

7

7

8

8

10

11

12

14

15

Section B

Study Unit 1: Basic accounting concepts and the accounting

equation

1. The nature and roles of accounting and finance

2. Users of accounting information

3. Forms of business ownership

4. Financial and management accounting

5. Financial accounting concepts and terminology

6. The accounting equation

Study Unit 2: Basic accounting concepts and financial statements

1. Basic accounting

2. Company financial statements

19

20

21

23

29

31

36

42

43

62

IMM GSM© Page 3 of 141 FM101

Study Unit 3: Determine the selling price of merchandise

1. Value added tax (VAT)

2. Determining selling prices

Study Unit 4: Cost classification and terminology

1. Introduction

2. Cost classification in relation to the product or period

3. Cost classification in relation to volume of production

4. Cost classification for control or evaluation

5. Cost classification for decision making

Study Unit 5: Materials

1. Classification of materials

2. Stock control

3. Stock valuation methods

Study Unit 6: Labour, overheads costing

1. Classification of labour

2. Overheads

3. Job costing (absorption costing)

4. Marginal costing

Study Unit 7: Budgetary control and sales variance

1. Operational budgets

2. Flexible budgets

3. Cash budgets

4. Sales variances

Bibliography

84

85

91

97

98

98

99

101

101

106

107

108

113

117

118

118

119

123

127

128

130

133

135

141

IMM GSM© Page 4 of 141 FM101

Section A

1. Word of welcome

Welcome to financial management, a central part of the management function

in the firm. Financial management addresses accounting and finance concepts

relevant to all marketers, regardless of the extent of their involvement in the

direct financial affairs of the firm. Decisions to invest in products or markets or

to sell particular products depend to a great extent on the quality of information

provided by the accounting and finance function.

In this learner guide you will find a structured and integrated schedule of

learning material, tutorial notes, time-lines, self-assessment questions and one

assignment. In order to assist you in planning and managing your studies, the

learner guide has been structured according to:

an organisational component (Section A), and

a learning component (Section B).

The purpose of the organisational component is, amongst other things, to

orientate you towards financial management and to inform you about

administrative issues, whilst the purpose of the learning component is to

structure the syllabus in terms of manageable study units. The learning

component will explain what topics are covered, in how much depth, where to

find relevant information pertaining to the subject and ultimately help you to

study the subject as realistically and practically as possible.

To ensure you get the maximum benefit from the study time you have available

it is recommended that you work through the learning guide. This will help you

identify the time you will need to complete the programme and by doing this you

will be able to draw up a detailed and workable study schedule.

Everyone connected with marketing should be a little ‘streetwise’ about

accounting and finance because financial decisions influence every aspect of

IMM GSM© Page 5 of 141 FM101

business operations. Financial management is a fascinating and enjoyable

subject and it provides frameworks and techniques you will be able to apply in

your day-to-day marketing work.

Good luck and enjoy your studying.

2. How to use this guide

We aim to make you a confident user of financial and management accounting

techniques. The most effective way to achieve this will be to ensure that you

understand and enjoy the module.

The learner guide is especially designed for a student who studies at a

distance. The guide will provide an overview of the total curriculum and will

indicate the learning outcomes, which are essentially the core of this guide. It

will provide you with each major topic that has to be covered, along with the

learning outcomes for each topic, which are systematically explained. The

guide will also indicate how the learning material must be prepared for

examination.

The learner guide should be studied in conjunction with the textbook and does

not replace the textbook.

At the end of each study unit you will find some typical examples of examination

questions which should be used for self-evaluation.

The following icons appear in all of the learning guides of the IMM Graduate

School of Marketing:

IMM GSM© Page 6 of 141 FM101

indicates learning outcomes.

indicates the sections in the prescribed textbook that you need

to study.

indicates the self-evaluation questions.

3. The overall purpose of the subject

The fundamental aim of this course is to equip you with a thorough

understanding of important financial concepts. These concepts are important

and are applied to and integrated with other areas of learning within the

marketing field of study.

The overall course objectives for Financial Management 1 are to develop

financial literacy on a theoretical and practical level, by

explaining accounting concepts and terminology,

determining selling price of merchandise,

classifying costs into various categories,

demonstrating knowledge of concepts related to materials management,

demonstrating knowledge of concepts related to labour, overheads and

job costing, and

demonstrating an understanding of budgets and budgetary control.

IMM GSM© Page 7 of 141 FM101

4. Pre-knowledge

It is essential that you are competent in mathematics at NQF level four. If you

are not confident in your mathematical abilities at this level, it is strongly

recommended that you improve or refresh your basic mathematical knowledge

and skills. There are a number of firms offering short skills programmes in

mathematical literacy.

You should know or be able to do the following:

Know the order of mathematical operations

Work with formulas

Calculate ratios

Calculate percentages

Construct, read and interpret graphs and charts.

We will provide you with brief explanations in your learner guide where it is

deemed necessary. It is, however, not possible to create a comprehensive

mathematical guide within this text.

You can also refer to the following book related to business calculations:

Zidel, D. 2004. Basic Business Calculations. Johannesburg: Penguin Books.

An ability to use spreadsheets, such as MS Excel, to do financial calculations

and create charts and graphs is an added advantage.

5. The relationship with other subjects

Financial Management I should not be seen as an entity on its own, but in the

context of the diploma/degree as a whole, since a number of concepts are also

dealt with in other courses.

IMM GSM© Page 8 of 141 FM101

This course covers fundamental financial concepts that you are required to

know on a theoretical and practical level. The terminology and other topics

included are integrated with other IMM subjects, which in turn, help you to

identify and recognise your prior learning.

Finance as a topic can be boring if you don’t understand the concepts. It can

be, however, an interesting topic or course when being studied in the marketing

context because marketing strategy affects the financial performance of the firm

by generating sales and incurring costs.

6. The NQF level and number of credits

This module forms a compulsory module for the Diploma in Marketing

Management and BBA degree in Marketing Management.

In terms of the new National Qualifications Framework (NQF) it is designed as a

20-credit module offered on NQF level 5.

The IMM Graduate School of Marketing regards Financial Management I as a

first year subject.

7. Prescribed textbook and resources required

The prescribed textbook for this module is:

Cloete, M., and Marimuthu, F. 2008. Basic Accounting for Non-

Accountants. Pretoria: Van Schaik.

The textbook is written in a clear and systematic manner. Always start your

studies by consulting the learner guide and then study the relevant sections in

the prescribed textbook. It is unlikely that you will pass this module if you have

only consulted the learner guide without studying the content of the textbook.

The following textbooks are also recommended:

IMM GSM© Page 9 of 141 FM101

Marx, J., de Swart, C., Beaumont Smith, M., and Erasmus, P. 2009.

Financial Management in Southern Africa. 3rd edn. Cape Town:

Pearson.

Pizzey, A. 1998. Finance and Accounting for Non-Specialist Students.

Harlow: Prentice-Hall.

Niemand, A., Meyer, L., Botes, V.L., and Van Vuuren, S.J. 2006.

Fundamentals of Cost and Management Accounting. Revised 5th edn.

Durban: LexisNexis.

We would also like to encourage you to make a habit of reading business and

financially orientated literature, magazines and newspapers such as:

1. Business Day

2. Business Report

3. Engineering News

4. Financial Mail

5. FinWeek

You can also subscribe to various newsletters published online by financial

institutions or financially orientated magazines and portals such as:

Financial Mail at http://fm.co.za/

Finance Week at http://www.fin24.co.za/FinWeek

The IMM Marketing Information Centre specialises in the provision of

information for your project and work related needs. They have

over 1500 marketing related books,

prescribed and recommended IMM textbooks,

a range of over 30 marketing and business related journals.

IMM GSM© Page 10 of 141 FM101

Calculators

You will need a basic calculator that is typically used at

schools and universities, similar to the one displayed in

the picture. It can perform a variety of functions,

including fraction calculations, percentage calculations,

scientific calculations and statistical calculations.

This type of calculator is adequate for the basic business

calculations that you will have to perform during this

course.

8. Curriculum

This section addresses the overall content of the module. The Financial

Management I curriculum is divided into seven study units. The seven study

units with the corresponding chapters in the prescribed textbook (Cloete &

Marimuthu 2008) are as follows:

Unit Description Relevant Chapters

1 Accounting concepts and terminology Chapters 1 to 4

2 Financial statements Chapter 5

3 Determine selling price of merchandise Chapters 4, 7

4 Cost classification Chapter 8

5 Material and stock management Chapter 9

6 Labour, overhead and job costing, marginal

costing

Chapters 10, 13

7 Budgets and budgetary control Chapters 11, 12

IMM GSM© Page 11 of 141 FM101

9. Specific learning outcomes

The aim of this course is to emphasise the need for financial literacy on the part

of the marketing specialists. This will be by developing your ability to interpret

financial reports, to apply basic financial techniques to marketing operations

and to understand the essential indicators of the firm’s financial position.

Study

Unit Description Learning Outcomes

1 Explain

accounting

concepts and

terminology

Define the purpose and users of accounting.

Classify items as assets, liabilities or owner’s

equity.

Show the effect of various transactions on the

basic accounting equation.

2 Reading

financial

statements

Describe the accounting cycle.

Explain what year-end adjustments are and its

impact on the financial statements.

Interpret an income statement and balance sheet.

3 Determine

selling price of

merchandise

Calculate cost of sales.

Explain VAT concepts and calculate VAT.

Calculate mark-ups on cost price and selling price.

Calculate selling price (inclusive and exclusive of

VAT).

4 Classify costs

into various

categories

Classify cost in relation to product or period.

Classify behaviour of cost in relation to volume of

production.

Classify cost for control or evaluation.

Classify relevant and non-relevant costs for

decision making.

IMM GSM© Page 12 of 141 FM101

5 Demonstrate

knowledge of

concepts

related to

materials

management

Distinguish between direct and indirect materials.

Describe stock control concepts, calculate stock

levels and EOQ.

Describe stock valuation methods and calculate

the value of closing inventories using FIFO and the

weighted average method.

6 Demonstrate

knowledge of

concepts

related to

labour

overheads

and job

costing

Distinguish between direct and indirect labour.

Identify overhead costs.

Calculate the cost of a product or a job.

Distinguish between marginal and absorption

costing.

7 Demonstrate

an

understanding

of budgets

and budgetary

control

Describe components of an operational budget.

Draft operational, flexible and cash budgets.

Calculate and interpret sales variances.

10. Critical cross-field outcomes

The critical cross-field outcomes, also known as transferable skills as identified

by the South African Qualifications Authority (SAQA), are essential for your

development as a student within the education and training system, regardless

of the specific area of learning. It is these outcomes that are deemed critical for

your development in the capacity of life-long learning.

IMM GSM© Page 13 of 141 FM101

The critical cross-field outcomes adopted by SAQA are as follows:

(1) Identify and solve problems in which responses display that responsible

decisions using critical and creative thinking have been made.

(2) Work effectively with others as a member of a team, group, organisation,

and community.

(3) Organise and manage oneself and one’s activities responsibly and

effectively.

(4) Collect, analyse, organise and critically evaluate information.

(5) Communicate effectively using visual, mathematical and/or language

skills in the modes of oral and/or written presentation.

(6) Use science and technology effectively and critically, showing

responsibility towards the environment and health of others.

(7) Demonstrate an understanding of the world as a set of related systems

by realising that problem solving contexts do not exist in isolation.

(8) Reflecting on and exploring a variety of strategies to learn more

effectively.

(9) Participating as responsible citizens in the life of local, national and

global communities.

(10) Being culturally and aesthetically sensitive across a range of social

contexts.

(11) Exploring education and career opportunities.

(12) Developing entrepreneurial opportunities.

IMM GSM© Page 14 of 141 FM101

The transferable skills identified in this course are as follows:

Taught Practised Assessed

Problem solving X X X

Working in teams

Self-management X X X

Information gathering/research

skills

X X X

Communication skills X X X

Analytical skills X X X

Learning strategies X X X

Responsible citizenship

Cultural sensitivity X

Career development X X

Entrepreneurship

11. Assessment details

There are two assessments involved in terms of the Financial Management 1

module:

Assignment: The assignment contributes 20% to the overall mark for the

module. Assignments will focus on selected chapters, and need to be

typed. Please ensure that you adhere to the general rules of the IMM

Graduate School of Marketing pertaining to the style and format of

assignments. You will be issued with a separate instruction in this

regard.

Examination: The exam incorporates all content covered in the workbook

and constitutes 80% of the final mark for the Financial Management 1

module. The duration of the examination is three hours and the paper

will count 100 marks. The examination paper will consist of multiple

IMM GSM© Page 15 of 141 FM101

choice and short question type answers, but the majority of the questions

will require an ability to perform calculations as set out in the practice

questions in this guide. Examination results are usually released within

six weeks of sitting the examination.

The final mark, consisting of an assignment mark and an examination mark, is

released in the form of a final percentage (mark out of 100). The grading

system is as follows:

Percentage Scale Description

75% or more Pass with Distinction

50% - 74% Pass

0% - 49% Fail

A timetable of the assessment programme for the semester, including dates for

the assignment to be submitted during the course of the year, is available in the

Calendar of Events for that year. Please refer to the current issue of the IMM

GSM Prospectus. This document and the Student Yearbook provide details of

the IMM GSM assessment policy.

12. Time-line

With distance education, it is very important that you track your progress

against the time-line. The following time-line can be used as a starting point to

set up your personal time-line.

Week Topic/study theme

1 Introduction to accounting, concepts and terminology

2 Accounting equation and accounting cycle

3 Accounting for stock, year-end adjustments

4 Year-end adjustments

IMM GSM© Page 16 of 141 FM101

5 Company financial statements

6 VAT, mark-up

7 Cost classification

8 Material and stock management

9 Stock valuation

10 Labour, overhead, job costing

11 Marginal costing

12 Budgets and budgetary control

13 Budgetary control and sales variances

IMM GSM© Page 17 of 141 FM101

SECTION B

Why do I need to know about finance and accounting?

“There is not a chief executive or financial director these days who will deny the vital

importance of establishing and strengthening the bond between the brand and its

users. The problem arises in the language used by marketing people to communicate

the value of those relationships at management forums…

“…It is the way marketing people try to communicate the complex ideas about the

sensitive work they do in creating bonds between brands and their users. This is the

language used to motivate an increase in marketing investment. I have frequently been

told that if we could only prepare analyses and schedules that support a request for a

budget increase in the same way the factory manager motivates money for a new

piece of machinery; we would have a smoother ride.

“But we persist in trying to communicate in ‘soft’ terms that confuse more than explain,

and which marginalises marketing rather than raising the standing of its practitioners to

where they belong, which is at the very front line of income generation. The

gatekeepers of the shareholders’ purse strings want to hear how the new branding

programme will affect the bottom line and what return it will achieve rather than be told

about the consumer psychology behind the campaign. And they want to hear it stated

in financial terms not the obtuse coded vernacular of the world of branding.”

Source: http://www.brandsandbranding-online.co.za/corporate-finance-101-for-marketers/

The effectiveness of marketing operations can be measured through the

application of various financial analysis activities. None of these analytical

activities can be performed if a person does not have a basic understanding of

accounting and finance fundamentals.

IMM GSM© Page 18 of 141 FM101

Most of these financial analyses fall into one of four financial activities as

explained below:

The financial situation analysis determines how well marketing activities are

doing. It involves the study of trends, comparative analyses, and assessment of

present financial strengths and limitations of the product, brand or business unit.

Financial information is used to evaluate alternatives as whether to introduce

new products, move into new markets, eliminate a product, expand the sales

force or change the distribution channel.

Financial planning involves the projection of sales, cost forecasts and budgets,

once it has been decided to implement a specific marketing action.

Financial control is about comparing actual results to planned results, with the

objective of keeping an unfavourable results gap as narrow as possible.

IMM GSM© Page 19 of 141 FM101

Study Unit 1: Basic accounting concepts and the accounting equation

This study unit covers the introduction to accounting, discusses financial

accounting concepts and terminology, and explains the accounting equation.

Mastering the accounting equation is critical in understanding this study unit and

creates the foundation of the remainder of this subject and for future studies in

financial management.

Specific Learning Outcomes

After studying this unit, you should be able to:

Define the purpose of accounting.

Identify the main users of accounting information.

Classify items as assets, liabilities or owner’s equity.

Show the effect of various transactions on the basic accounting equation.

.

1. The nature and roles of accounting and finance

IMM GSM© Page 20 of 141 FM101

Reading reference

Study Cloete & Marimuthu 2008: Chapter 1 – Definition of accounting.

Financial management addresses accounting and finance concepts relevant to

all marketers, regardless of the extent of their involvement in the financial

information and decisions in the business. Decisions to invest in products or

markets or to sell particular products all depend on the basis of information

provided by the accounting and finance function.

The main purpose of accounting is to provide users with financial information

that will assist them in making informed decisions.

Accounting is a system comprising the following elements:

Gathering financial information that has an effect on a specific business.

Analysing how the financial information will affect the business.

Recording the financial information through proper accounting

processes.

Reporting all financial information for a given period of time so that it can

be read and understood.

Interpreting the summarised information to allow users to make

informed decisions about the business.

You should now be able to master outcome 1.

IMM GSM© Page 21 of 141 FM101

2. Users of accounting information

Reading reference

Study Cloete & Marimuthu 2008: Chapter 1 – Users of accounting information,

and how useful is accounting information.

2.1 Identifying users of financial information

Financial decisions are influenced by several factors such as the realities of the

external environment, past strategies, management value systems, goals of the

executive management team and internal power relationships. Stakeholders

have expectations or demands, which can influence decisions depending on the

power of the stakeholder or groups of stakeholders. We can define a

stakeholder as an individual or group that can influence the firm’s objectives or

are affected by decisions made by the firm.

Stakeholders can be classified or grouped into two groups, namely internal and

external users of financial information:

Internal External

• Owners

• Managers

• Employees and their

representatives.

• Customers

• Competitors

• Lenders

• Government

• Suppliers

• Investment analysts.

IMM GSM© Page 22 of 141 FM101

2.2 The needs of users of financial information

Financial information should possess a number of qualities in order to fulfil the

needs of the users thereof. It should be relevant, reliable, provide means to do

comparisons with the past or across different businesses and it should be clear

so that users can understand it. In addition to these qualities, financial

information should also achieve a threshold of materiality or significance,

meaning that it should only be included within reports if it does not clutter them

up or interfere with the user’s ability to interpret financial results.

The timely flow of information helps managers to compare actual performance

to planned performance. Accounting information helps owners of the business

to assess if the managers of the business are also pursuing the goal of wealth

maximisation.

The reasons for using accounting information by different users are set out in

the table below:

User Use

• Owners

• Managers

• Employees

• Customers

• Competitors

• Lenders

• Government

• Suppliers

• Investment

analysts

Determine profitability and financial viability.

Ensure business operates efficiently and solve problem

areas highlighted.

Determine if employer is able to provide stable

employment and remuneration.

Determine if business can provide products over long

period of time.

Competitor intelligence, to maintain competitive edge.

Determine if business can repay loans and interest.

Determine how much taxes and levies should be paid.

Determine if business can pay for goods purchased on

credit.

Determine if business would be good investment, and to

assess risk and return of an investment in business.

You should now be in a position to master outcome 2.

IMM GSM© Page 23 of 141 FM101

3. Forms of business ownership

Reading reference

Please read Cloete & Marimuthu 2008: Chapter 1 – Basic business forms in

South Africa.

No learning outcome is set for this section but regard the reading as important

background information.

An understanding of the different forms of business ownership is necessary as

the nature of ownership will in the first instance have an impact on the treatment

of owners’ claims, and secondly, the reporting and treatment of financial

information in the financial statements.

3.1 Forms of business ownership in South Africa

In South Africa you may find that businesses are operated as a:

Sole proprietary

Partnership

Close Corporation – Name followed by CC

Private company with limited liability – Name followed by (Pty) Ltd

Public company with limited liability – Name followed by Ltd

Important note:

The Companies Act was signed by the President on the 08th April 2009 and gazetted

in the Gazette No. 32121 (Notice 421). The Act comes into operation on a date still to

be fixed by the President by proclamation in the Gazette.

This Act affects Close Corporations, Private companies and Public companies as

mentioned above.

IMM GSM© Page 24 of 141 FM101

The new Companies Act has identified two types of companies to be

incorporated under the new act. A company can either be a profit company or a

non-profit company.

A profit company is defined as a company incorporated for the purpose of

financial gain for its shareholders.

A non-profit company is incorporated for public benefit and the income and

property are not distributable to its incorporators. A non-profit company may be

regarded as a successor to the previous Section 21 companies in the current

act.

Profit companies can be:

1) a state-owned company (SOC);

2) a private company (Proprietary Limited) if it is not state-owned and the

Memorandum on Incorporation prohibits it from offering its securities to

the public and restricts the transferability of its securities;

3) a personal liability company (Incorporated) if it meets the criteria for a

private company and the Memorandum of Incorporation states that it is a

personal liability company;

4) a public company (Limited) in any other case.

One of the effects of the new Companies Act of 2008 is the phasing out of close

corporations. No new close corporations may be formed once that Act comes

into operation. Existing close corporations can elect to continue to exist until

deregistered, dissolved or converted into a private company governed under the

new Companies Act. It will be possible for businesses to continue to run their

operations out of an existing close corporation if they so wish.

Another effect is that a private company will still be prohibited from offering its

shares to the public and the transferability of its shares will be restricted but, it

will no longer be subject to a limitation of 50 shareholders.

IMM GSM© Page 25 of 141 FM101

3.2 Distinguishing between forms of ownership

A sole proprietary dissolves upon the death or retirement of the proprietor. A

partnership must be dissolved upon the death or retirement of one of the

partners and a new partnership agreement has to be drawn up.

We will further distinguish between the forms of ownership on the basis of

liability for debts and capital formation.

Business

Form

Liability Capital

Sole

proprietary

Owner bears unlimited liability

for debts – may lose personal

assets.

Owner provides own capital or

borrows from financial institution.

Partnership Partners jointly and severally

liable for debt of business – may

lose personal assets.

Partners provide own capital or

borrow from financial institution.

Close

Corporation

Members’ liability limited to

amount of money invested in

business – may under certain

circumstances lose limited

liability.

Members provide own capital or

borrow from financial institution.

Private

company

Shareholders’ liability limited to

amount of capital invested in

shares.

Capital is raised by issuing

shares to owners (not public) or

borrowing from financial

institution.

Public

company

Shareholders’ liability limited to

amount of capital invested in

shares.

Capital is raised by issuing

shares to shareholders, or

borrowing from public through

debentures or borrowing from

financial institutions.

IMM GSM© Page 26 of 141 FM101

3.3 Accounting and legal requirements

We will summarise the differences in accounting requirements between different

forms of business ownership in South Africa.

Business

Form

Legal Financial

statements

Taxation

Sole

proprietary

Very little legal

requirements.

Not regulated. Owner pays tax

in personal

capacity, not as

business.

Partnership Very little legal formalities.

Partnership Agreement.

Not regulated. Partners pay

tax in personal

capacity, not as

business.

Close

Corporation

Founding Statement.

Certificate of Incorporation.

Association Agreement to

regulate relationship

between members.

Financial

statements

prepared but not

required to be

audited.

CC pays tax on

profits of

business – at

preferential

rates available

to CC below

certain

turnover.

Private

company

Memorandum of

Association and

Articles of Association.

Certificate of Incorporation.

Financial

statements

prepared but not

required to be

audited or lodged

with Registrar of

companies.

Company pays

tax on its

profits.

Public

company

Memorandum of

Association and

Articles of Association.

Certificate of Incorporation.

Prospectus.

Minimum subscription

fulfilled.

Certificate to Commence

Business.

Financial

statements audited

and lodged with

Registrar of

companies.

Company pays

tax on its

profits.

IMM GSM© Page 27 of 141 FM101

Transferring of ownership of shares in public companies (if they are members

and their shares are listed on the JSE) takes place at the JSE Securities

Exchange South Africa (‘the JSE’). The JSE was formally established on 8

November 1887 as a market-place for the shares of South Africa’s many mining

and financial companies.

3.4 Types of business activity

Please read Cloete & Marimuthu 2008: Chapter 1 – Types of business activity.

No outcome is set for this section but regard the reading as important

background information.

We can classify business types by various types of activities, including service

businesses, manufacturers, wholesalers and retailers.

Service businesses

These businesses provide services for which they charge fees. Typical

examples include attorneys, accountants, architects and information,

communication and technology (ICT) companies.

Manufacturers

Manufacturers buy raw materials that they then transform into finished products

which are sold to wholesalers and retailers.

Wholesalers

The term middleman is often associated with wholesalers, because they buy in

bulk from manufacturers and then supply the goods in smaller quantities to

retailers, or the public.

IMM GSM© Page 28 of 141 FM101

Retailers Retailers buy goods from the wholesalers or manufacturers and sell the goods

to the general public. It is also stated that retailers can be viewed as service

providers for reasons listed below:

Bring goods within reach of the consumer

Allow the consumer to buy on credit

Pay attention to the need of their consumers

Sell goods in small quantities

Make consumers aware of new products on the market

Offer convenience shopping.

The format of financial statements will vary by the type of business. For

instance, service businesses may have a category ‘Fees Collected’ instead of

‘Sales’. One also needs to consider Work-In-Progress as part of inventory in a

manufacturing environment, and that you will not find in a service business.

IMM GSM© Page 29 of 141 FM101

4. Financial and management accounting

Reading reference

Study Cloete & Marimuthu 2008: Chapter 1 – The accounting field.

Accounting accumulates data for reporting to external and internal users (with

different objectives).

Management accounting seeks to meet the need of the business managers in

the firm and financial accounting seeks to meet the needs of all the other users.

The major differences between the two types of accounting can be found in:

Nature of the reports produced

Level of detail provided in the reports

Regulatory requirements related to the format and timing of accounting

reports

Interval at which reports are prepared

Time horizon – historical or forward looking

Range and quality of information.

You should now be able to master outcome 2.

IMM GSM© Page 30 of 141 FM101

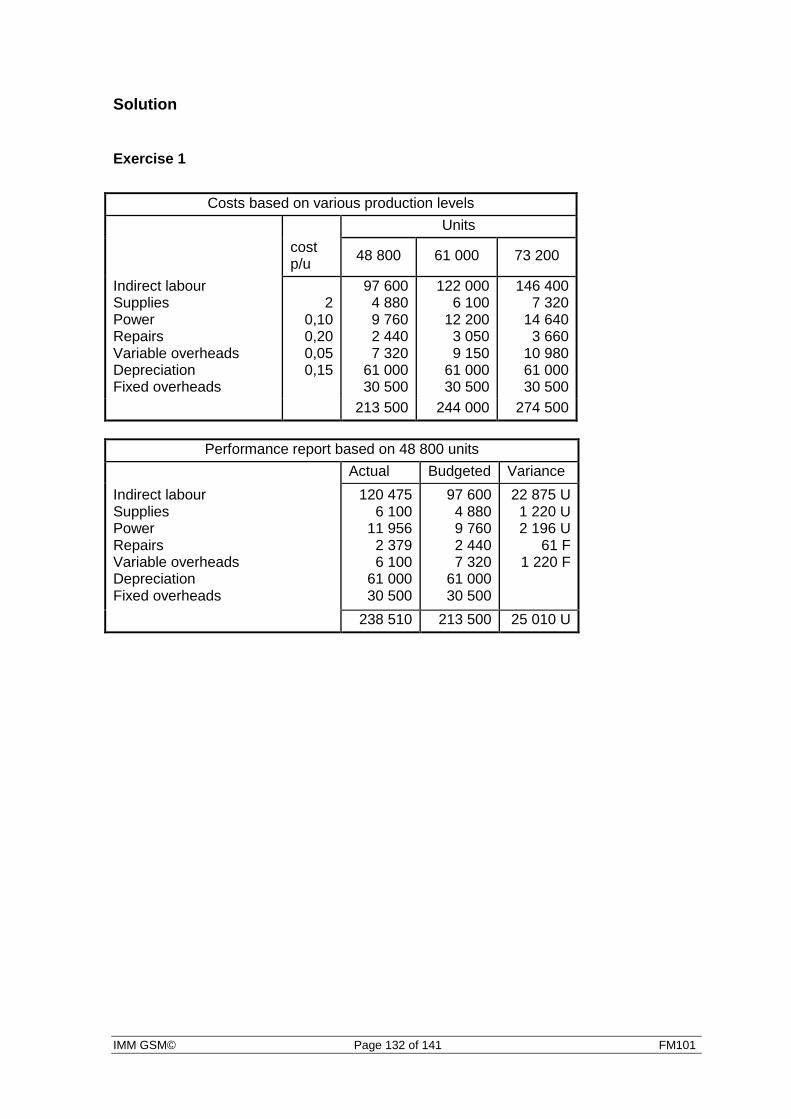

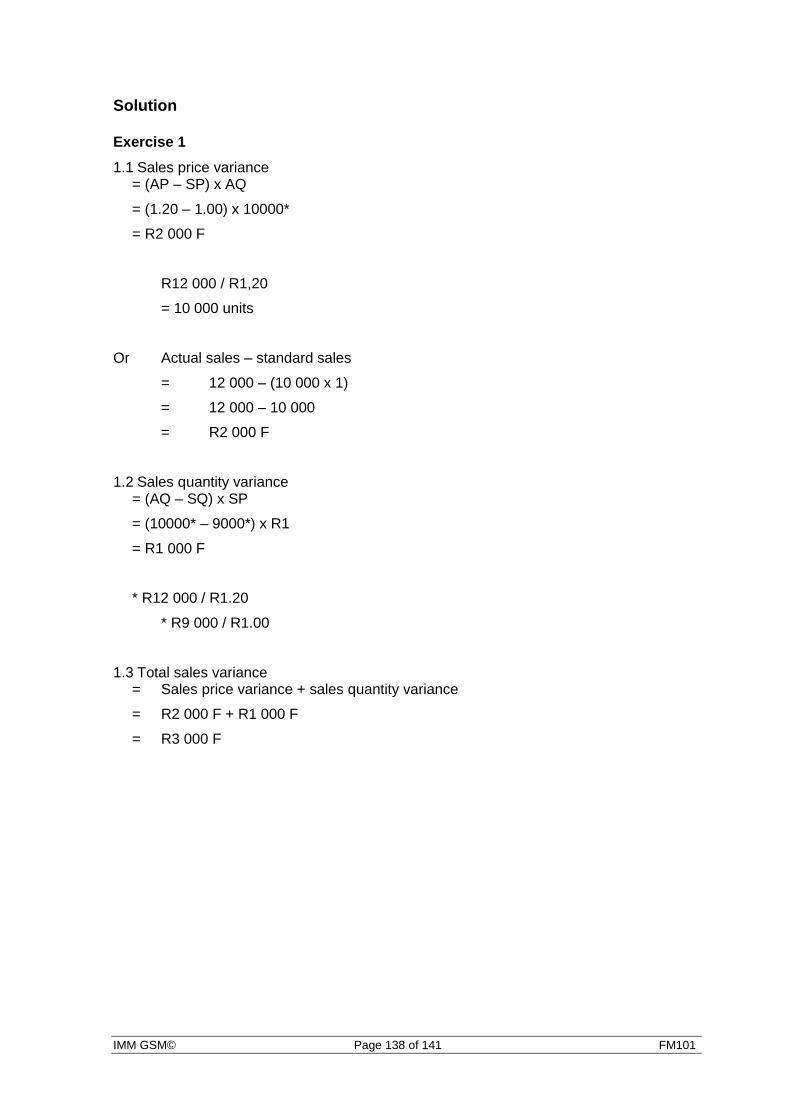

Self-assessment exercise

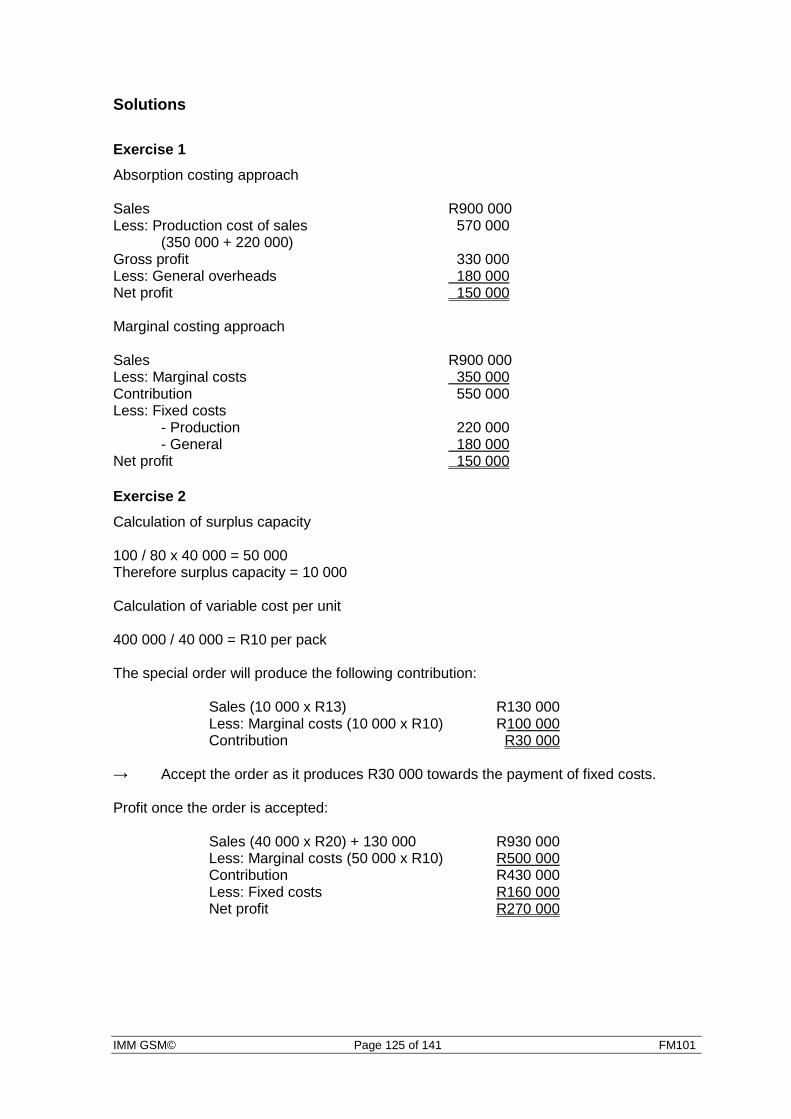

Now do Exercise 1 and Exercise 2 in Cloete & Marimuthu 2008: Chapter 1.

Solutions

Exercise 1

1. c

2. a

3. e

4. b

5. d

Exercise 2

2.1 d

2.2 b

2.3 d

2.4 d

2.5 c

2.6 c

2.7 c

IMM GSM© Page 31 of 141 FM101

5. Financial accounting concepts and terminology

Study reference

Study Cloete & Marimuthu 2008: Chapter 2.

Wealth of a business is measured through the measurement:

Assets – Liabilities = Owner’s equity

It is important to define the terms that will be used throughout this subject and in

subsequent studies in financial management.

Term Definition

Assets Resources controlled by an entity resulting from past events

out of which future economic benefits will flow.

OR

In financial accounting, assets are economic resources.

Anything tangible or intangible that is capable of being

owned or controlled to produce value and that is held to

have positive economic value is considered an asset.

Simply stated, assets represent ownership of value that can

be converted into cash (although cash itself is also

considered an asset).

Non-current assets An item of value with a lifespan of more than one year.

Property, plant and equipment

Financial assets (e.g. investments)

Intangible assets (e.g. patents, trade marks).

Current assets An item of value with a lifespan of less than one year.

Cash

Debtors

Stock.

Liabilities Present obligations resulting from past events, the

settlement of which leads to decreases in economic

benefits.

IMM GSM© Page 32 of 141 FM101

OR

In financial accounting, a liability is defined as an

obligation of a firm arising from past transactions or events,

the settlement of which may result in the transfer or use of

assets, provision of services or other yielding of economic

benefits in the future.

Non-current liabilities Obligations of the business which are payable over a period

of more than one year.

Long-term loan

Bond from bank over property.

Current liabilities Obligations of the business which are payable within one

year.

Bank overdraft

Creditors.

Owner’s equity Owner’s interest in the business and comprises capital

contribution less drawings, plus net profit, where:

Income – expenses = Net profit

Income Receipts by a business for normal operations.

Sales

Fees earned

Rent received

Interest received.

Expenses Amounts spent by a business during normal operations

(excluding capital expenses)

Rent paid

Interest paid

Advertising

Salaries.

We will return to a more comprehensive discussion of these terms later in this

unit.

IMM GSM© Page 33 of 141 FM101

Self-assessment exercise

Complete Exercise 1 and Exercise 2 in Cloete & Marimuthu 2008: Chapter 2.

You will now be able to master outcome 3

IMM GSM© Page 34 of 141 FM101

Solutions

Exercise 1

NCA CA NCL CL OE I E

a) Capital X

b) Delivery vehicle X

c) Weekly wages X

d) Sales X

e) Trading stock X

f) Mortgage loan X

g) Telephone account X

h) Debtors (accounts receivable) X

i) Computer X

j) Interest received X

k) Creditor (accounts payable) X

l) Interest paid X

m) Property X

n) Discount allowed X

o) Discount received X

p) Depreciation X

q) Stationery used X

r) Stationery unused (stationery on hand)

X

s) Bank overdraft X

t) Drawings X

u) Photostat machine X

v) Shop fittings X

IMM GSM© Page 35 of 141 FM101

Exercise 2

ASSET LIABILITY INCOME EXPENSE

a) The monthly rental paid for the shops

X

b) A loan raised from Bee Bank X

c) Amounts owed to Megacity by customers

X

d) Petty cash on hand. X

e) The stock of clothes on hand in each shop

X

f) Amounts owed by Megacity to its suppliers of stock

X

g) Warehouse owned by Megacity used for storing stock

X

h) Wages paid to the shop assistants

X

i) Receipts from customers for the sale of clothes

X

k) Cash at the bank X

IMM GSM© Page 36 of 141 FM101

6. The accounting equation

Study reference

Study Cloete & Marimuthu 2008: Chapter 3 – The basic accounting equation.

6.1 Basic accounting equation

The three main elements of accounting fit together as follows:

Assets = Owner’s equity + Liabilities

The right hand side of this equation represents all the money that is available to

the business in the long term from the owners and the outside providers of

funds to purchase assets (the left hand side of the equation).

This equation is the Basic Accounting Equation. (BAE)

Important!

Please work through illustrative examples 1, 2 and 3 in the textbook.

Self-assessment exercise

Now do Exercise 1 and Exercise 2 in Cloete & Marimuthu – Chapter 3

You should now be in a position to master outcome 4

IMM GSM© Page 37 of 141 FM101

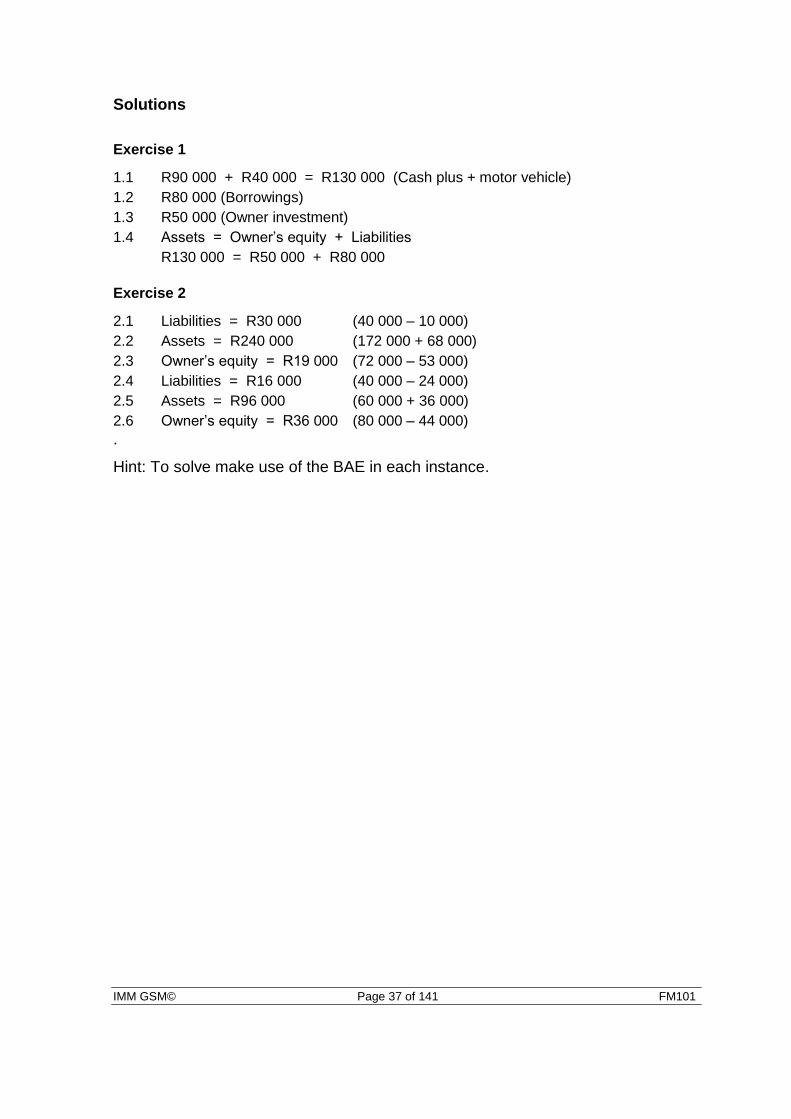

Solutions

Exercise 1

1.1 R90 000 + R40 000 = R130 000 (Cash plus + motor vehicle)

1.2 R80 000 (Borrowings)

1.3 R50 000 (Owner investment)

1.4 Assets = Owner’s equity + Liabilities

R130 000 = R50 000 + R80 000

Exercise 2

2.1 Liabilities = R30 000 (40 000 – 10 000)

2.2 Assets = R240 000 (172 000 + 68 000)

2.3 Owner’s equity = R19 000 (72 000 – 53 000)

2.4 Liabilities = R16 000 (40 000 – 24 000)

2.5 Assets = R96 000 (60 000 + 36 000)

2.6 Owner’s equity = R36 000 (80 000 – 44 000)

.

Hint: To solve make use of the BAE in each instance.

IMM GSM© Page 38 of 141 FM101

6.2 Effect of transactions on the basic accounting equation

Study reference

Study Cloete & Marimuthu 2008: Chapter 3 – The effect of transactions on the

basic accounting equation.

This section is to strengthen your understanding of the BAE and is part of

learning outcome 3.

Every financial transaction, however simple or complex, affects the basic

accounting equation.

Important!

Please ensure that you now work through the examples in the textbook of

transactions affecting the BAE:

Transactions that affect assets and equities only

o Capital contributions

o Loans

o Purchase of assets for cash

o Buying assets on credit

o Payments to creditors

o Withdrawals by the owner

Transactions that give rise to income and expenditure

o Income (cash)

o Income (credit)

o Expenditure (cash)

o Expenditure (credit)

Transactions involving payments by debtors.

It should be noted that the accounting equation neither answers the question as to how

much profit the business has generated nor the question about the financial position of

the business. The accounting equation must therefore be adapted into an income

statement (indicating profits made) and a balance sheet (statement of financial

position).

IMM GSM© Page 39 of 141 FM101

Self-assesment exercise

Now do Exercises 5, 6 and 7 in Cloete & Marimuthu 2008: Chapter 3.

IMM GSM© Page 40 of 141 FM101

Solutions

Exercise 5

DATE ASSETS = OWNERS EQUITY +

LIABILITIES

Vehicles Equipment Debtors Bank Capital/

drawings Income/expense

Loan Creditors

1 +15000 +15000

2 +60000 -6000 +54000

3 -2000 -2000

10 +15000 +15000

12 -500 -500

14 +20000 +20000

15 +10000 +10000

17 -3000 -3000

20 -800 +800

24 -1500 -1500

26 -8000 +8000

28 -250 -250

31 +75000 +75000

Exercise 6

DATE ASSETS = OWNERS EQUITY +

LIABILITIES

Vehicles Equipment Debtors Bank Capital/

drawings Income/expense

Loan Creditors

1 +2800 +2800

2 -110 -110

3 -1100 +1100

5 +6000 +6000

6 -200 -200

7 -8400 +8400

8 -1200 -1200

9 +4000 +4000

11 +2600 +2600

12 -1200 -1200

13 -300 -300

IMM GSM© Page 41 of 141 FM101

Exercise 7

DATE ASSETS = OWNER’S EQUITY +

LIABILITIES ACCOUNT

DEBIT ACCOUNT

CREDIT

1 +18 000 +18 000 Bank Loan

2 -100 -100 Loss on theft

of asset Equipment

3 +70 +70 Bank Loss on theft

of asset

4 +10 000 -10 000 Buildings Bank

5 -120 -120 Drawings Bank

6 +3 000 +3 000 Debtors Sales

7 -800 -800 Wages Bank

+20 050 +2 050 +18 000

IMM GSM© Page 42 of 141 FM101

Study Unit 2: Basic accounting concepts and financial statements

This study unit addresses basic accounting matters such as the conceptual

framework of basic accounting, the accounting cycle, year-end adjustments and

an introduction to company financial statements.

Mastering the year-end adjustments and an understanding of the components

of the respective financial statements is critical to read financial statements.

Specific learning outcomes

After you have studied this module you should be able to:

Describe the accounting cycle.

Explain what year-end adjustments are and its impact on the financial

statements.

Interpret an income statement and balance sheet.

IMM GSM© Page 43 of 141 FM101

1. Basic accounting

Study reference

Please read Cloete & Marimuthu 2008: Chapter 4, Section 4.1 – Conceptual

framework.

1.1 Accounting conceptual framework

Qualitative characteristics are the attributes that make the information provided

in financial statements useful to users. The four (4) qualitative characteristics

are understandability, relevance, reliability and comparability.

Understandability

An essential quality of the information provided in financial statements is that it

is easily understood by all users. For this purpose, users are assumed to have a

reasonable knowledge of business, economic activities, accounting, and a

willingness to study the information with reasonable diligence.

Relevance

Information must be relevant and useful to the decision-making needs of users.

Information has the quality of relevance when it influences the economic

decisions of users by helping them evaluate past, present or future events or

confirming, or correcting their past evaluation.

Reliability

Information must be reliable. Information has the quality of reliability when it is

free from material error and bias and can be depended upon by the users to

represent faithfully that which it either purports to represent or could reasonably

be expected to represent.

IMM GSM© Page 44 of 141 FM101

Comparability

Users must be able to compare the financial statements of a firm through time,

in order to identify trends in its financial position and performance. Users must

also be able to compare the financial statements of different firms in order to

evaluate their relative financial position, performance and changes in their

financial position. Hence the measurement and display of the financial effect on

like transactions and other events must be carried out in a consistent way

throughout a firm and over time for that firm and in a consistent way for different

firms.

Accounting statements rest on four important principles which are so important

that a note to the accounts must warn users if this is not the case. These

principles are:

The going concern – it is assumed that a business is going to continue

its operations in the future.

The matching principal – cost and revenue are matched to reflect the

same time period, i.e., cost of materials or stock purchased will only be

reflected against revenue generated by such materials or stock. Any

materials or stock purchased and not yet used will be carried as a short-

term asset in the balance sheet. This principal is also known as the

‘accruals’ principal.

Prudence (conservatism) – until a deal has been concluded and

completed, profit cannot be counted and the lower asset value or profit

alternatives will be reflected in the financial statements.

Consistency – once a method has been chosen by the accountant to

treat accounting entries, it is essential that the same method is applied in

future years. This will ensure that statements can be compared over

time.

IMM GSM© Page 45 of 141 FM101

1.2 The accounting cycle Study reference

Study Cloete & Marimuthu 2008: Chapter 4, Section 4.2 – The accounting

cycle.

The accounting cycle is the series of steps that take place in order for financial

statements to be accurately and uniformly produced at the end of an accounting

period which is typically the length of one month, quarter of a year, or a whole

year. Below is a list of the steps you would take to complete the accounting

cycle, listed in the order that you would perform them, and with a brief summary

of each step.

1. A transaction occurs between the business and some other entity. This

transaction could be the revenue from the sale of a product or a payment to

another business for services.

2. A source document is required to substantiate the transaction.

3. Analyse the transaction and how it relates to the accounting balance sheet.

For example, determine which accounts are affected by the transaction and

how they are affected. Record the transaction to a journal such as a sales

journal. Journals are kept in chronological order and may be updated

continuously, daily, or however often it is necessary.

4. Record the transaction to the general ledger. Take all of your entries and

categorise them by the account.

5. Perform a trial balance. Debits and credits need to be equal at the end of an

accounting cycle, so calculate the entries to ensure they match.

6. Prepare adjustments. Just because entries are recognised, does not mean

the work has been performed. Revenue can only be recognised when the

work has been completed, so adjust the entries accordingly. The

adjustment can also be the result of accounting policies, such as provision

for bad debts or depreciation on assets.

IMM GSM© Page 46 of 141 FM101

7. Perform trial balance with adjustments. Take the adjustments from Step 6

and prepare a trial balance. If the debits and credits do not match, then you

need to adjust them to make sure they do match.

8. Perform closing entries using a general journal. Close the accounts in

preparation of the next accounting cycle. Revenues and expenses need to

be closed out, which means they need to have zero balances. Balances are

moved to the next cycle.

9. Prepare a final trial balance after all closing entries have been made

(summary of the closing entries in the general ledger).

10. Prepare financial statements. From the adjusted trial balance, these

corrected balances are used to prepare the financial statements.

11. Analyse and interpret information contained in the financial statements.

While the actual terminology, timeline, and other factors of the accounting cycle

vary, the above steps represent the general steps included universally in the

accounting cycle. In realistic scenarios, a streamlined process, aided by

computer programs and other devices, allows an accountant to combine some

of these steps and complete the process in less time and with less effort. For

example, often, a computer program allows steps one and two to be combined

and allows the steps to accurately appear on the journal or general ledger

almost instantaneously. Also, calculations performed by a computer or

calculator work to eliminate human errors.

Self-assessment exercise

Now do Exercise 1 in Cloete & Marimuthu 2008: Chapter 4.

After you have studied this section you should be able to master learning outcome 1.

IMM GSM© Page 47 of 141 FM101

Solution

Exercise 1

Shiloh Clothing Income statement for the year ended 28 February 20x2

Sales Less: Cost of sales

63 750 42 500

Gross profit for the year Add: Other income

Dividends received Rent income

30 7 200

21 250 7 230

Gross income for the year Less: Operating expenses

Advertising Bank charges Interest paid Electricity and water Licence Wages Stationery and postage Telephone

540 165

2 860 160 225

7 920 140 270

28 480 12 280

Net profit for the year 16 200

IMM GSM© Page 48 of 141 FM101

Shiloh Clothing Balance sheet as at 28 February 20x2

Notes Cost price Accumulated depreciation

Book value

Non-current assets Premises

Vehicles

Equipment

70 000 12 500 12 100

70 000 12 500 12 100

94 600 94 600

Investment Shares: JSE

850

850

Current assets Stock Accounts receivable Bank Cash float

13 250 1 500

21 750 250

36 750

TOTAL ASSETS 132 200

Equity & liabilities Owner’s equity

1

99 700

Non-current liabilities Loan: PBS (17% p.a.) Mortgage bond (15% p.a.)

8 000 10 000

18 000

Current liabilities Accounts payable

14 500 14 500

TOTAL EQUITY & LIABILITIES

132 200

Notes: 1) Statement of changes in equity

Capital R98 000 Add: Net profit R16 200 Less: Drawings R14 500

R99 700

IMM GSM© Page 49 of 141 FM101

1.3 Year-end adjustments Study reference

Study Cloete & Marimuthu 2008: Chapter 4, Section 4.4 – Year-end

adjustments, depreciation.

A number of adjustments can be made at year end, including:

Depreciation

Provision for doubtful debts

Prepaid expenses

Accrued expenses

Accrued income

Income received in advance/prepaid income.

1.3.1 Depreciation

The benefits that a firm obtains from an asset extend over several years. The

life of production machinery may extend over many years, whereas a company-

owned motor car used by a salesman probably has a much shorter useful life.

By accepting that the life of a fixed asset is limited, the accounts of a firm need

to recognise the benefits of the fixed asset as it is ‘consumed’ over several

years. This ‘consumption’ of a fixed asset is referred to as depreciation.

A portion of the benefits of the fixed asset will be used up or consumed in each

accounting period of its life in order to generate revenue. To calculate profit for

a period, it is necessary to match expenses with the revenues they help earn.

In determining the expenses for a period, it is therefore important to include an

amount to represent the consumption of fixed assets during that period (that is,

depreciation).

IMM GSM© Page 50 of 141 FM101

The Receiver of Revenue (SARS) controls the rate at which depreciation may

be claimed in South Africa because it affects the profits, and consequently, the

amount of tax payable. The rate of depreciation for different types of assets is

published as schedules to Practice Notes. Special accelerated depreciation

rates may also be available as incentive to develop industries or regions.

The basics that underline depreciation are:

The asset should be used to generate income in the course of

conducting business.

The expense should be fairly allocated over the lifetime of the asset.

The asset should be fairly presented in the balance sheet, that is, at book

value.

Important!

Please ensure that you now work through the depreciation examples in the

textbook.

Self-assessment exercise

Now do Exercise 3 in Cloete & Marimuthu 2008: Chapter 4.

IMM GSM© Page 51 of 141 FM101

Solution

Exercise 3

TKZ Stores journal entry as at 30 June – Vehicles

Debit Credit

Depreciation Accumulated depreciation on vehicles

7 000 7 000

Workings R35 000 x 20% = 7 000 TKZ Stores journal entry as at 30 June – Furniture and fittings

Debit Credit

Depreciation Accumulated depreciation on furniture and fittings

5 355 5 355

Workings (R42 000 – 6 300) x 15% = 5 355 TKZ Stores income statement as at 30 June

Less: Operating expenses Depreciation (7 000 + 5 355) R12 355

TKZ Stores balance sheet as at 30 June Non-current assets

Cost Accumulated depreciation

Book value

Vehicles Furniture and fittings

35 000 42 000

25 000 (18 000 + 7 000)

11 655 (6 300 + 5 355)

10 000 30 345

IMM GSM© Page 52 of 141 FM101

1.3.2 Provision for doubtful debts Study reference

Study Cloete & Marimuthu 2008: Chapter 4 – Year-end adjustments, provision

for doubtful debts.

When sales are allowed on credit, the possibility exists that some of the debtors

will not pay their outstanding debt. It is prudent that some provision for doubtful

debt is created in order to give a more accurate report on the expected amount

of outstanding debt, including a provision for doubtful debt.

The amount provided for doubtful debt is estimated as a percentage of the total

amount of debt outstanding and is based on past experience and the economic

climate.

The following situations could arise that relate to the provision of bad debt:

Scenario Debit Credit

Write off a bad debt when a provision for bad debt does not exist

Bad debt acc.

(expense) increase

Debtors control acc.

(current asset) decrease

Create provision for doubtful debt

Bad debt acc.

(expense) increase

Provision for doubtful debt acc.

(negative asset) increase

Increase provision for doubtful debt

Bad debt acc.

(expense) increase

Provision for doubtful debt acc.

(negative asset) increase

Decrease provision for doubtful debt

Provision for doubtful debt acc.

(negative asset) decrease

Bad debt acc.

(expense) decrease

Write off a bad debt when provision for bad debt exists

Provision for doubtful debt acc.

(negative asset) decrease

Debtors control acc.

(current asset) decrease

IMM GSM© Page 53 of 141 FM101

Important!

Please ensure that you now work through the provision for doubtful debt

examples in the textbook.

Self-assessment exercise

Now do Exercise 4 in Cloete & Marimuthu 2008: Chapter 4.

IMM GSM© Page 54 of 141 FM101

Solution

Exercise 4

ZZ Traders journal entry as at 28 February – bad debts

Debit Credit

Bad debts

Debtors control

640

640

Write off bad debt

Debit Credit

Bad debts

Provision for doubtful debts

728

728

Adjust provision for doubtful debts to 5% of outstanding debtors

Outstanding debtors balance R 58 200 – 640 = R57 560

Provision for doubtful debts should be (57 560 x 5%) = R2 878

Currently the provision for doubtful debts is = R2 150

Therefore the provision must be increased by R728 in order to equal R2 878.

ZZ Traders income statement as at 28 February

Less: Operating Expenses

Bad Debts Expense (9 360 + 640 + 728) R10 728

ZZ Traders balance sheet as at 28 February

Current assets

Debtors (58 200 – 640) R57 560

Less: Provision for doubtful debts R2 878

IMM GSM© Page 55 of 141 FM101

1.3.3 Prepaid expenses Study reference

Study Cloete & Marimuthu 2008: Chapter 4 – Year-end adjustments, prepaid

expenses.

Prepaid expenses refer to payments made in one accounting period but are

only due in the following accounting period. The matching principle requires

that the amounts due in the following accounting period should be excluded

from the expense for the current accounting period.

Important!

Please ensure that you now work through the prepaid expenses examples in

the textbook.

Accrued expenses

Study Cloete & Marimuthu 2008: Chapter 4 – Year-end adjustments, accrued

expenses.

Accrued expenses refer to payments due in the current accounting period but

not yet paid. The matching principle requires that the amounts due in the

current accounting period should be written off against income in the current

accounting period.

Important!

Please ensure that you now work through the prepaid expenses examples in

the textbook.

IMM GSM© Page 56 of 141 FM101

1.3.4 Accrued income Study reference

Study Cloete & Marimuthu 2008: Chapter 4 – Year-end adjustments, accrued

income.

Accrued income refers to income earned in the current accounting period but

not yet received. The matching principle requires that the income earned in the

current year should be recorded in full in the current accounting period.

Important!

Please ensure that you now work through the prepaid expenses examples in

the textbook.

1.3.5 Income received in advance

Study Cloete & Marimuthu 2008: Chapter 4 – Year-end adjustments, income

received in advance.

Income received in advance refers to income earned in the current accounting

period but not yet received. The matching principle requires that the income

received in the current accounting period but only earned in the following

accounting period should be recorded in the following accounting period.

Important!

Please ensure that you now work through the prepaid expenses examples in

the textbook.

You should have mastered learning outcome 2 if you have studied the section and have attempted the exercises.

IMM GSM© Page 57 of 141 FM101

Self-assessment exercise

Now do Exercises 5, 6, 7and 8 in Cloete & Marimuthu 2008: Chapter 4.

Solution

Exercise 5

Purchases I/S Cost of sales Loan: ABC Bank B/S Current liab.

Prepaid income B/S Current liability

Depreciation (year)

I/S Expense

Debtors B/S Current asset Refreshments I/S Expense

Wages I/S Expense Equipment B/S Current asset

Rent paid I/S Expense Accumulated depreciation

B/S Non-current asset

Interest received I/S Income Drawings B/S Owner’s equity

Unused stationery

B/S Current asset Prepaid expenses B/S Current asset

Accrued income B/S Current asset Accrued expense B/S Current liability

IMM GSM© Page 58 of 141 FM101

Exercise 6

Angel Traders Income statement for period ended 30 June 20x0

R R

Gross profit xxx

Add: Other income 24 000

Rent received (13 200 / 11mnths = 1 200pm x 12mnths

14 400

Commission received (11 200 – 1 600) 9 600

Less: Expenses 65 380

Stationery (700 – 100) 600

Water and lights (3 600 + 320) 3 920

Bad debts (560 + 300) 860

Depreciation on machinery 60 000

Angel Traders Balance sheet at 30 June 20x0

ASSETS R R

Non-current assets Note 1 280 000

Current assets 23 300

Debtors (22 300 – 300) 22 000

Stationery on hand 100

Accrued income (rent income) 1 200

Owners equity & liabilities

Liabilities 1 920

Accrued expense (water and lights) 320

Prepaid income (commission received) 1 600

Note 1 Cost Accumulated depreciation

Carrying value

Machinery R400 000 R120 000 (60 000 +

60 000) R280 000

IMM GSM© Page 59 of 141 FM101

Exercise 7

Hot Chicks Income statement for the year ended 28 February 20x3

Sales Less: Sales returns

564 369

5 729

Net sales Less: Cost of sales

Opening stock Add: Purchases Less: Purchases returns Add: Carriage on purchases

36 982 364 965 (2 984)

3 696

558 640 360 630

Goods available for sale Less: Closing stock

402 659 (42 029)

Gross profit Add: Other income

Rent received Discount received

13 200 3 690

198 010 16 890

Gross income for the year Less: Operating expenses

Carriage on sales Rates and taxes Salaries and wages Telephone Stationery Repairs Insurance Bad debts (1 365 + 1 065) Depreciation (2 290 + 14 600)

5 642 4 320

67 420 3 622 2 913

995 1 985 2 430

16 890

214 900 106 217

Net profit for the year 108 683

IMM GSM© Page 60 of 141 FM101

Exercise 8

Pretty Princess Delivery Services Income statement for year ended 31 December 20x1

R R

Income: Fees received 49 000

Less: Expenses 31 750

Spares used 10 000

Insurance expense 2 000

Salaries 6 000

Municipal costs 1 500

Rental paid 3 000

Depreciation on office equipment 1 500

Depreciation on delivery 7 000

Interest payable 750

Net income 17 250

IMM GSM© Page 61 of 141 FM101

Pretty Princess Delivery Services Balance sheet at 31 December 20x1

ASSETS R R

Non-current assets Note 1 13 500

Current assets 62 000

Stock of spares (15 000 – 10 000) 5 000

Debtors 20 000

Expenses prepaid (insurance) (3 000 – 2 000) 1 000

Bank 36 000

Total assets 75 500

OWNER’S EQUITY AND LIABILITIES

OWNER’S EQUITY Note 2 44 250

Liabilities

Current liabilities 31 250

Creditors 30 500

Accrued expense (interest) 750

75 500

Note 1 Cost Accumulated depreciation

Carrying value

R R R

Office equipment 5 000 1 500 3 500

Delivery vehicles 17 000 7 000 10 000

13 500

Note 2 Statement of changes in equity

Capital 30 000 Add: Net profit 17 250 Less: Drawings (3 000)

44 250

IMM GSM© Page 62 of 141 FM101

2. Company financial statements Study reference

Study Cloete & Marimuthu 2008: Chapter 5, Sections 5.1 and 5.2 – GAAP and

company terminology.

2.1 Generally Accepted Accounting Principles (GAAP)

International Accounting Standards (IAS) are set by the International

Accounting Standards Board (IASB) which is the main body of The International

Accounting Standards Committee (IASC), located in London, England. The

IASB is an independent accounting standard-setting body, consisting of 14

members from nine countries, including the United States.

When the IASB sets a brand new accounting standard, a number of countries

tend to adopt the standard, or at least interpret it, and fit it into their individual

country’s accounting standards. These standards, as set by each

particular country’s accounting standards board, will in turn influence what

becomes Generally Accepted Accounting Principles for each particular country.

The acronym ‘GAAP’ stands for Generally Accepted Accounting Principles.

The IASC does not set GAAP, nor does it have any legal authority over GAAP.

The IASC can be thought of as merely a very influential group of people who

love making up accounting rules. However, a lot of people actually do listen

to what the IASC and IASB have to say on matters of accounting.

The best way to think of GAAP is as a set of rules that accountants follow. Each

country has its own GAAP, but on the whole, there aren’t many differences

between countries – interpretations might vary from country to country, but

everyone tends to agree that a company can’t simply make up billions of dollars

IMM GSM© Page 63 of 141 FM101

worth of revenue and put it on its books. Every country, in turn, influences the

other countries that follow GAAP.

GAAP are imposed on companies so that investors have a minimum level of

consistency in the financial statements they use when analysing companies for

investment purposes. GAAP cover such things as revenue recognition, balance

sheet item classification and outstanding share measurements. Companies are

expected to follow GAAP rules when reporting their financial data via financial

statements.

That said, keep in mind that GAAP is only a set of standards. There is plenty of

room within GAAP for unscrupulous accountants to distort figures. So, even

when a company uses GAAP, you still need to scrutinise its financial

statements. By law all companies have to use GAAP when preparing financial

statements.

For reporting periods beginning on or after 1 January 2005, South African

statements of GAAP are fully aligned with International Financial Reporting

Standards (IFRS).

2.2 Company terminology

The main difference that distinguishes a company from other forms of

ownership is its limited liability, that is, the owner’s personal assets are

protected.

Four types of profit companies can be identified according to the Companies

Act, 2008:

1) a state-owned company (SOC);

2) a private company (Proprietary Limited) if it is not state-owned and the

Memorandum on Incorporation prohibits it from offering its securities to

the public and restricts the transferability of its securities;

IMM GSM© Page 64 of 141 FM101

3) a personal liability company (Incorporated) if it meets the criteria for a

private company and the Memorandum of Incorporation states that it is a

personal liability company;

4) a public company (Limited) in any other case.

Of these companies, it is only the public company that can sell shares to the

general public.

2.2.1 Share capital

A public company can issue shares, which is known as share capital. Currently,

if companies have par value shares, it means that the fixed value and amount of

issued shares is indicated in the memorandum of association. In the case of

companies with no par value shares, the memorandum of association only

indicates the amount of issued shares as these shares do not have a fixed

value.

A major change introduced by the new Companies Act (Act No.71 of 2008), is

that a share will no longer have a fixed or nominal value (‘par value shares’), but

will be fixed in number only (‘no par value shares’).

Authorised share capital

Authorised share capital is the total number of shares a company is authorised

to issue according to its Memorandum of Incorporation (previously

memorandum of association) and approved by the Commission (previously the

Registrar of Companies).

A company’s Memorandum of Incorporation must set out the classes of shares,

and the number of shares of each class, that the company is authorised to

issue.

Issued share capital

Companies do not issue all their shares – they retain some of their shares as a

reserve. The portion issued is called the issued share capital. Any unissued

IMM GSM© Page 65 of 141 FM101

shares can be issued later by the directors, subject to the rules set out in the

Memorandum of Incorporation.

Share premium

Previously if a share was sold at a premium, then the issue price will be the par

value plus an additional premium. So if a 1 cent nominal value share is issued

at R2.01, then the par value was 1 cent and the premium was R2.00 per share.

The company issuing the shares will receive R2.01 for each share issued.

Under the new Companies Act, 2008 shares will no longer have a par value and

the distinction between the par value and the share premium will fall away.

Types of shares

Shareholders of a company receive a share of the profits in the form of

dividends. Dividends are dependent on the type of share they have purchased

as well as the company’s dividend policy.

A company’s Memorandum of Incorporation must set out the classes of shares,

and with respect to each class of shares a distinguishing designation for that

class; and the preferences, rights, limitations and other terms associated with

that class.

2.2.2 Reserves

Reserves are profits retained in the business and can take various forms.

Non-distributable reserves

These reserves are non-trading profits that cannot be distributed to

shareholders and can for example arise from items such as revaluations of

assets and some foreign exchange movements.

Distributable reserves

Distributable reserves are trading profits that have not been paid out by the

company and may be distributed to shareholders at a later stage.

IMM GSM© Page 66 of 141 FM101

General reserves

Profits that have been retained by the company in order to purchase assets are

set aside under general reserves.

2.2.3 Profits, taxation, reserves and dividends

Companies are liable to pay tax as separate legal entities. Company tax is

payable on profit made during the course of business. Once taxation has been

calculated and provided for payment to the Receiver of Revenue, the remainder

of the profits can be divided between reserves, dividends and retained earnings.

Important!

Please ensure that you now work through Example 1 dealing with:

Provisional tax payments

Tax assessments

Interim dividends

Final dividends

Distribution of net profit earned.

Also work through Example 2 dealing with the preparation of financial

statements.

Self-assessment exercise

Now do Exercise 1 in Cloete & Marimuthu 2008: Chapter 5.

You should have mastered learning outcome 3 after you have studied the

text and have attempted the exercise.

IMM GSM© Page 67 of 141 FM101

Solution

Exercise 1

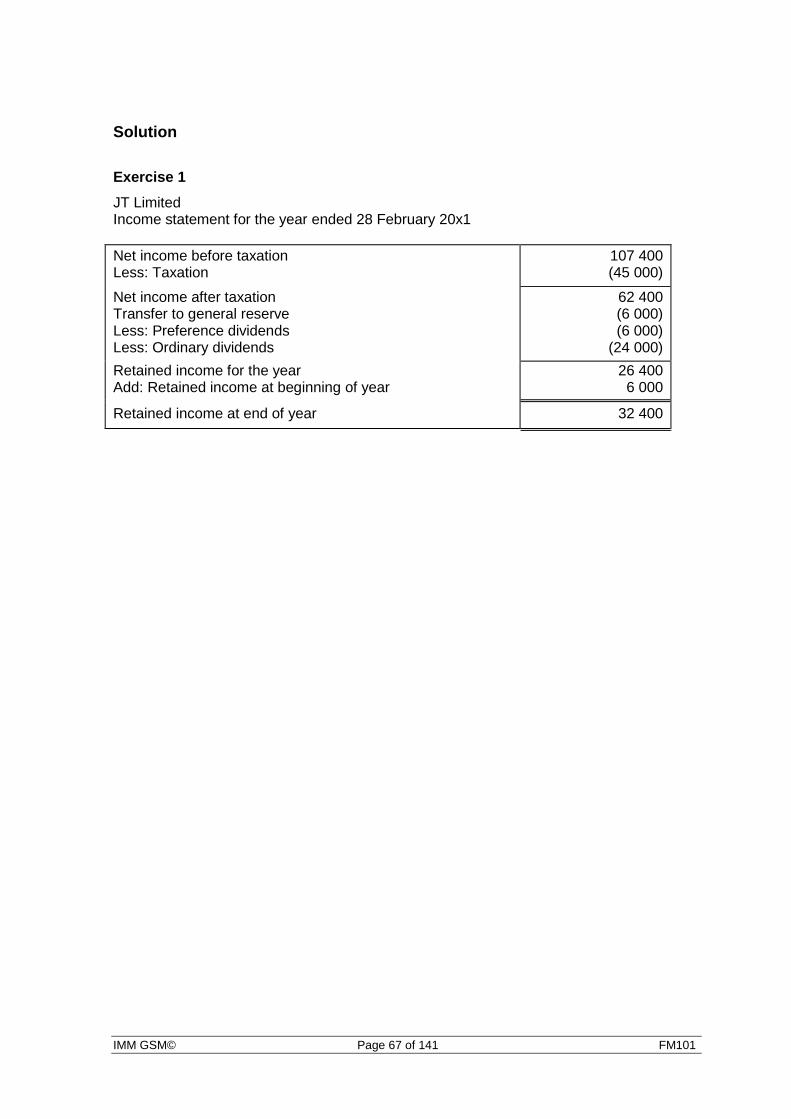

JT Limited Income statement for the year ended 28 February 20x1

Net income before taxation Less: Taxation

107 400 (45 000)

Net income after taxation Transfer to general reserve Less: Preference dividends Less: Ordinary dividends

62 400 (6 000) (6 000)

(24 000)

Retained income for the year Add: Retained income at beginning of year

26 400 6 000

Retained income at end of year 32 400

IMM GSM© Page 68 of 141 FM101

JT Limited Balance sheet as at 28 February 20x1

Cost Accumulated depreciation

Book value

ASSETS

Non-current assets

Land & buildings 180 000 180 000

Motor vehicles 72 000 26 400 45 600

Equipment 62 400 19 200 43 200

314 400 45 600 268 800

Investment 63 600

Current assets 273 000

Stock 114 000

Debtors 159 000

TOTAL ASSETS 605 400

EQUITY & LIABILITIES

Shareholders’ equity

Issued share capital

Ordinary share capital 240 000

Preference share capital 60 000

General reserve (12 + 6) 18 000

Retained income 32 400

350 400

Non current liabilities 96 000

Long-term loan 96 000

Current liabilities 159 000

Creditors 84 000

Bank overdraft 18 000

Receiver of Revenue (45 - 18)

27 000

Shareholders for dividends (24 + 6)

30 000

TOTAL EQUITY & LIABILITIES 605 400

Note to the balance sheet Authorised share capital

300 000 ordinary shares at R1 each

300 000

70 000 10% preference shares at R1 each

70 000

370 000

IMM GSM© Page 69 of 141 FM101

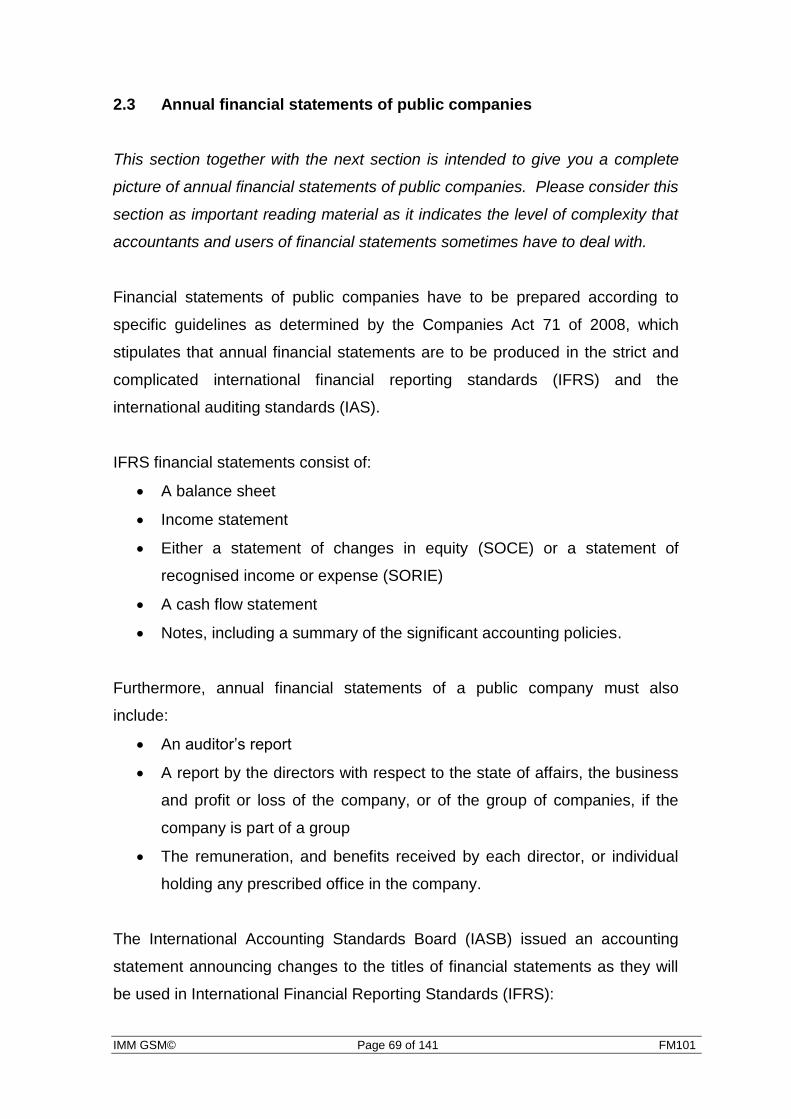

2.3 Annual financial statements of public companies

This section together with the next section is intended to give you a complete

picture of annual financial statements of public companies. Please consider this

section as important reading material as it indicates the level of complexity that

accountants and users of financial statements sometimes have to deal with.

Financial statements of public companies have to be prepared according to

specific guidelines as determined by the Companies Act 71 of 2008, which

stipulates that annual financial statements are to be produced in the strict and

complicated international financial reporting standards (IFRS) and the

international auditing standards (IAS).

IFRS financial statements consist of:

A balance sheet