financial services: digital trends & innovations

TRANSCRIPT

Financial Services: Digital Trends &

Innovations

Ruth Lewin-Chen, Hamutal Schieber, Meital Yachin

April, 2017

Introduction

• This presentation examines trends and innovations in financial services (focusing on

banking, insurance, credit cards). It is the 3rd report in the series, with the 1st published in

2014.

• The presentation is built on the Schieber Research model, which examines:

unmet / new needs created by macro trends

Enablers

Adoption of innovation

Market Trends

new & promising start up companiesaffecting the industry

Trend-setters

competitors ahead of the curve

Best in class

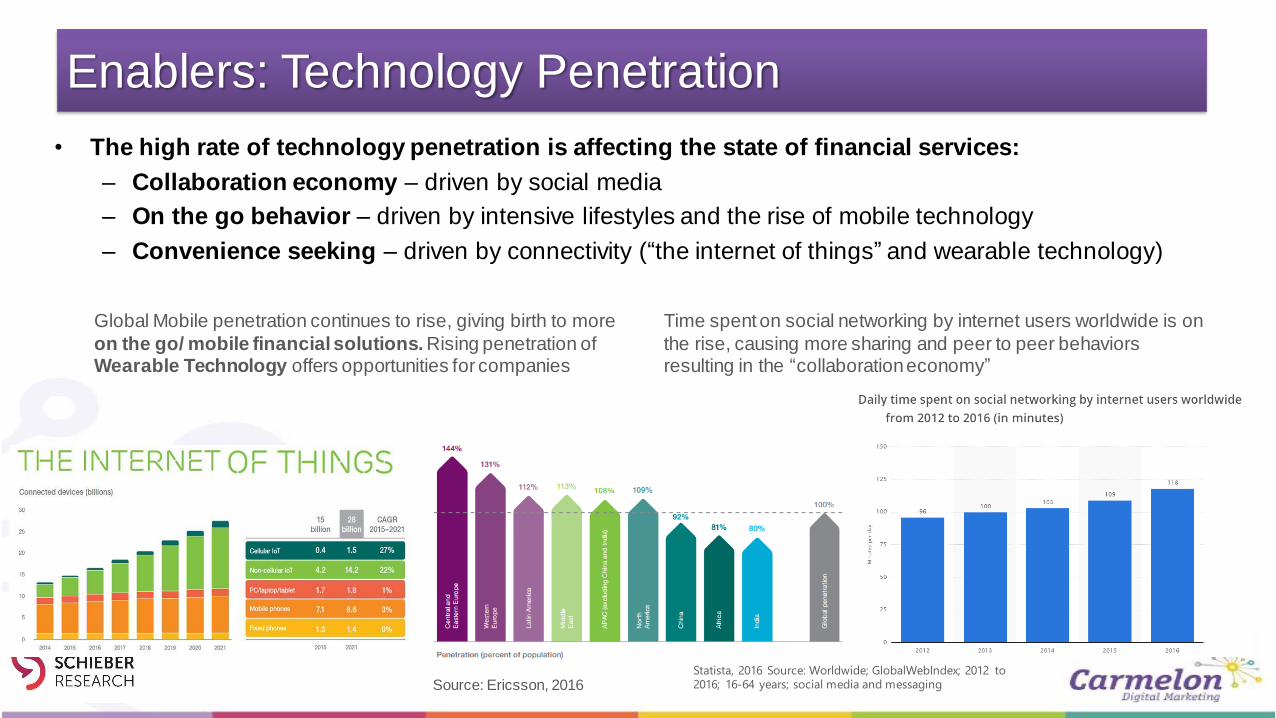

Enablers: Technology Penetration

• The high rate of technology penetration is affecting the state of financial services:

– Collaboration economy – driven by social media

– On the go behavior – driven by intensive lifestyles and the rise of mobile technology

– Convenience seeking – driven by connectivity (“the internet of things” and wearable technology)

Global Mobile penetration continues to rise, giving birth to more

on the go/ mobile financial solutions. Rising penetration of Wearable Technology offers opportunities for companies

Source: Ericsson, 2016

Time spent on social networking by internet users worldwide is on

the rise, causing more sharing and peer to peer behaviors resulting in the “collaboration economy”

Statista, 2016 Source: Worldwide; GlobalWebIndex; 2012 to 2016; 16-64 years; social media and messaging

Online and Mobile Banking

• As a result of the digital consumer behavior, the market is undergoing a shift towards digital financial services.

• Online banking adoption rates are 49% in the EU, but in some countries, as well as in the USA, penetration surpassed 50%. In Scandinavia penetration rates of online banking surpassed 80%.

• We expect Mobile financial services to grow at a faster rate, due to the increase in solutions offered through mobile devices as well as younger demographics demand for ultra-convenient solutions.

• According to the Federal Reserve, in the USA, use of mobile banking continues to rise but is yet to reach the rates of online banking:

• 43% of all mobile phone owners, and 53% of all smartphone owners with a bank account, had used mobile banking in the 12 months prior to the survey, compared to 71% who used online banking on a desktop, laptop or tablet computer in the same period.

• Source: Consumers and Mobile Financial Services, Board of Governors of the Federal Reserve System, March 2016

• Founded in 2014, Atom Bank is the UK's first

mobile-only bank, offering all of its services

through a smartphone app.

• The company raised another £83 million ($102

million) in funding led by BBVA, the Spanish

bank (and owner of Simple in the US). BBVA

also led Atom’s previous $128 million round in

November 2015 (source: Techcrunch, March

2017).

• Established competitors, as well as

emerging competitors, use a mix of

strategies to maintain competitive

advantage in the financial services field,

including adoption of new technologies (using enabling start ups), innovation labs

(to provide access to trend setting

technologies) and M&As (of disruptive

start ups).

• The main challenge in mobile financial

services is keeping them simple and

intuitive, as financial services can be

complex.

In 2017, Mastercard announced a massive expansion of its Qkr Platform to six

additional markets - Brazil, Canada, Ireland, Singapore, South Africa and the United States, in addition to Australia, Colombia, Mexico and the United Kingdom.

Qkr Is a mobile order-ahead and payment platform developed by Mastercard Labs.

Qkr enables consumers to seamlessly order and pay for goods and services via their smartphone without having to wait in line or for a restaurant server. The app uses Masterpass. (B2B Innovation – aimed at retailers)

Competitor Strategies

Disruptors

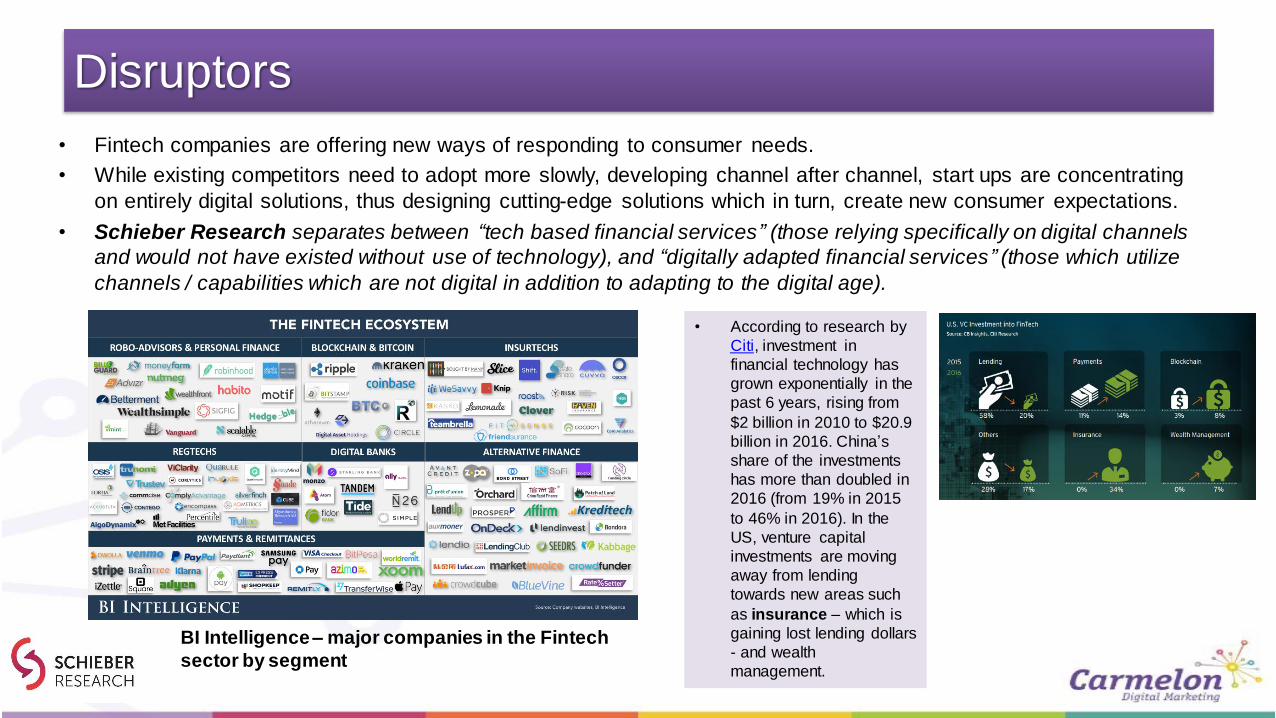

• Fintech companies are offering new ways of responding to consumer needs.

• While existing competitors need to adopt more slowly, developing channel after channel, start ups are concentrating

on entirely digital solutions, thus designing cutting-edge solutions which in turn, create new consumer expectations.

• Schieber Research separates between “tech based financial services” (those relying specifically on digital channels

and would not have existed without use of technology), and “digitally adapted financial services” (those which utilize

channels / capabilities which are not digital in addition to adapting to the digital age).

• According to research by

Citi, investment in

financial technology has

grown exponentially in the

past 6 years, rising from

$2 billion in 2010 to $20.9

billion in 2016. China’s

share of the investments

has more than doubled in

2016 (from 19% in 2015

to 46% in 2016). In the

US, venture capital

investments are moving

away from lending

towards new areas such

as insurance – which is

gaining lost lending dollars

- and wealth

management.

BI Intelligence – major companies in the Fintech

sector by segment

Disruptors: “Unicorns”

• Selected Fintech “Unicorns” (worth over $ 1 billion, according to CBInsights)

Avant: personal loans. $1.7B in funding. Kabbage: small business loans. $1.5B in funding.

Stripe: payments online and in mobile apps. $690M in funding

The Internet of Things & Wearables

• On May 2016, Intelligent Environments

launched Interact, an IoT banking platform.

• Through the platform, smart devices such as

Nest Thermostat and the Pavlok wearable device can be connected to the user’s bank

account and maximum spending for bills can be set, monitored and notified.

• On March 2017, Visa unveiled a

new payment-enabled sunglasses prototype.

• Consumers need to tap the Visa payment-enabled sunglasses on

enabled payment terminal in order to make a payment.

• Visa is currently testing to see if there is a demand for the

sunglasses and if brands or banks want to sponsor the product.• Alibaba is launching VR Pay

– goggle-based virtual reality payments.

Digital Wallet

• Apple Pay, Samsung Pay, and Android Pay are the

largest competitors in the digital wallet market, with 150

million users together.

• According to a recent report by Juniper Research, Apple

leads the digital wallet market and is expected to nearly

double Apple Pay userbase in 2017. The study

estimates that Apple Pay will hit 86 million users in 2017

globally, up from 45 million in 2016.

0

20

40

60

80

100

120

140

160

2015 2016 2017

Leading Digital Wallet Competitors (source: Juniper Research)

Apple Pay Samsung Pay Android Pay

Walmart Pay, the retailer’s alternative to Android Pay and Apple Pay,

allows shoppers so pay using their mobile app instead of a credit card or

cash

Payment Apps

• Owned by PayPal, US Millennials’ popular payment app Venmo processed $17.6 billion in 2016 in mobile payments,

up 135% from the prior year.

On the Go Payment

Mobile apps such as “First Bus” and "NJ Transit“

offer buying bus passes or tickets securely and getting transit options on mobile devices.

• Consumers can buy Uber gift cards online (e-gift card) or in-store (plastic).

The gift cards can be added to Uber account in the mobile app. Uber gift cards can be only used for rides or UberEATS orders.

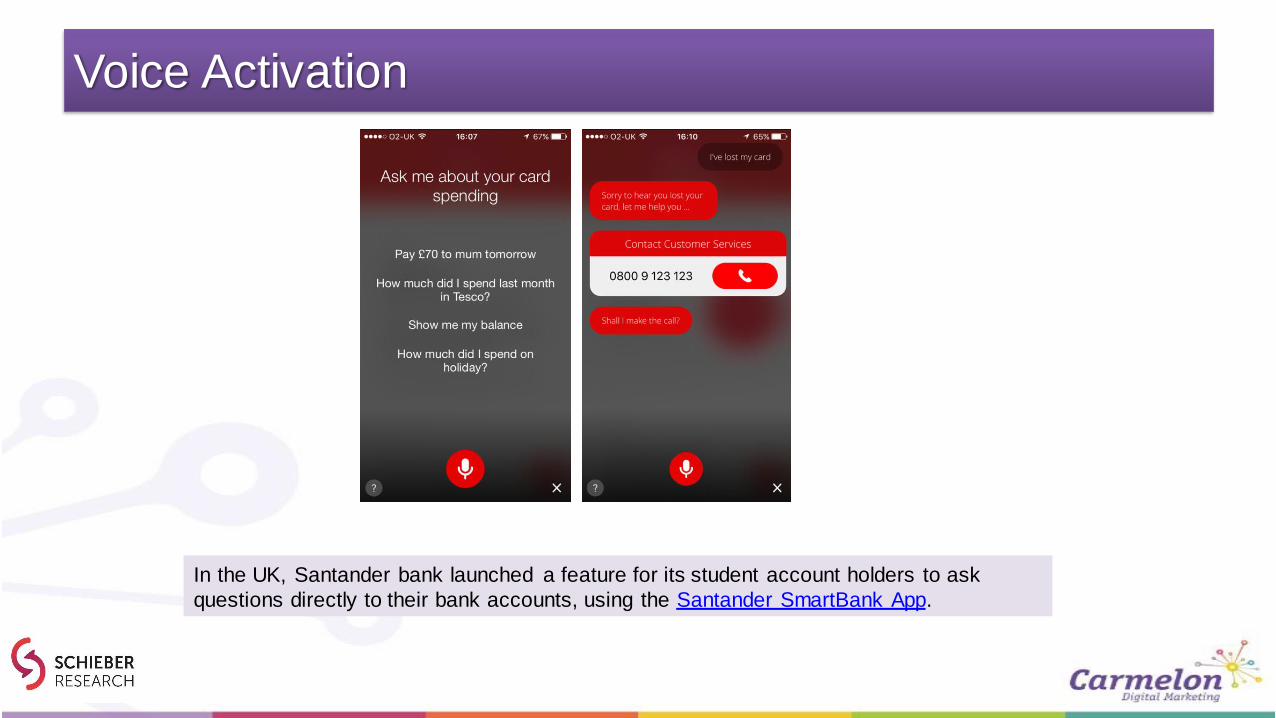

Voice Activation

In the UK, Santander bank launched a feature for its student account holders to ask

questions directly to their bank accounts, using the Santander SmartBank App.

Cardless Transactions

• “Cash” customers – those who don’t have a bank account or a debit card – account for 27%

of American consumers, according to a 2015 FDIC report. Companies are responding.

PayPal My Cash Card lets you add funds to your online

PayPal account, using cash from your wallet. It also has a barcode-only service, powered by Green Dot.

In April 2017, Amazon announced the launch of Amazon Cash, a new

service that allows consumers to add cash to their Amazon.com balance by showing a barcode at a participating retailer, then having the cash applied immediately to their online Amazon account. The service will support

adding any amount between $15 and $500 in a single transaction.Amazon Cash will be available at brick-and-mortar retailers across the

U.S., including CVS Pharmacy, Speedway, Sheetz, Kum & Go, D&W Fresh Market, Family Fare Supermarkets, and VG’s Grocery. Other stores will be added in the future.

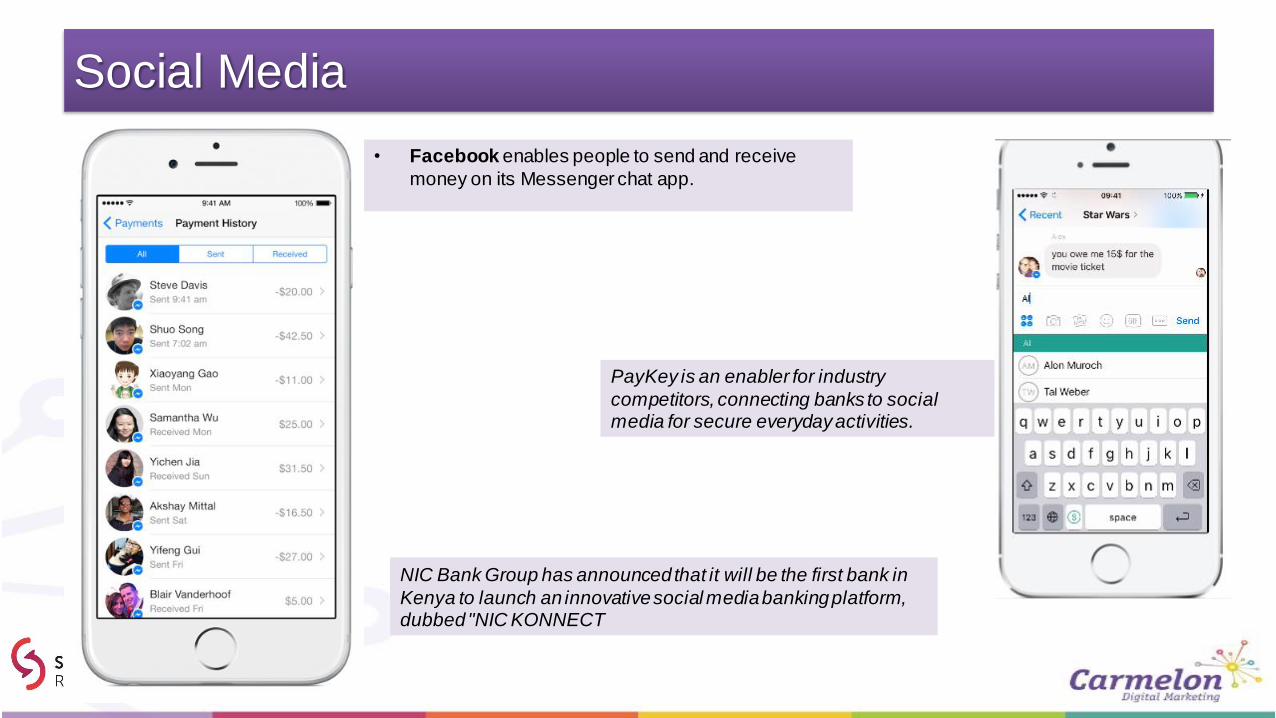

Social Media

• Facebook enables people to send and receive

money on its Messenger chat app.

PayKey is an enabler for industry

competitors, connecting banks to social media for secure everyday activities.

NIC Bank Group has announced that it will be the first bank in

Kenya to launch an innovative social media banking platform, dubbed "NIC KONNECT

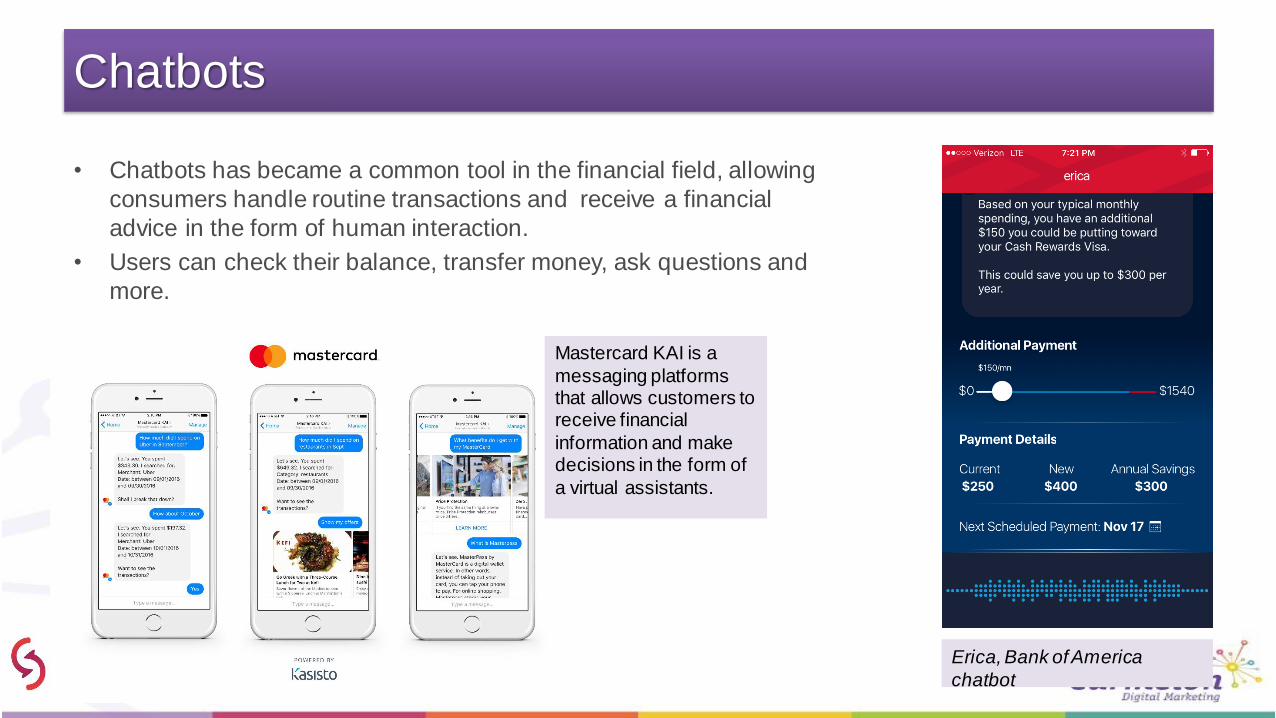

Chatbots

• Chatbots has became a common tool in the financial field, allowing

consumers handle routine transactions and receive a financial

advice in the form of human interaction.

• Users can check their balance, transfer money, ask questions and

more.

Erica, Bank of America

chatbot

Mastercard KAI is a

messaging platforms that allows customers to receive financial

information and make decisions in the form of

a virtual assistants.

Chatbots

• Transferwise is a Facebook Messenger based bot, claiming to transfer money with real exchange rate.

• Sway is a Slack based financial services bot, aimed at small businesses. Slack also invested in the start-up.

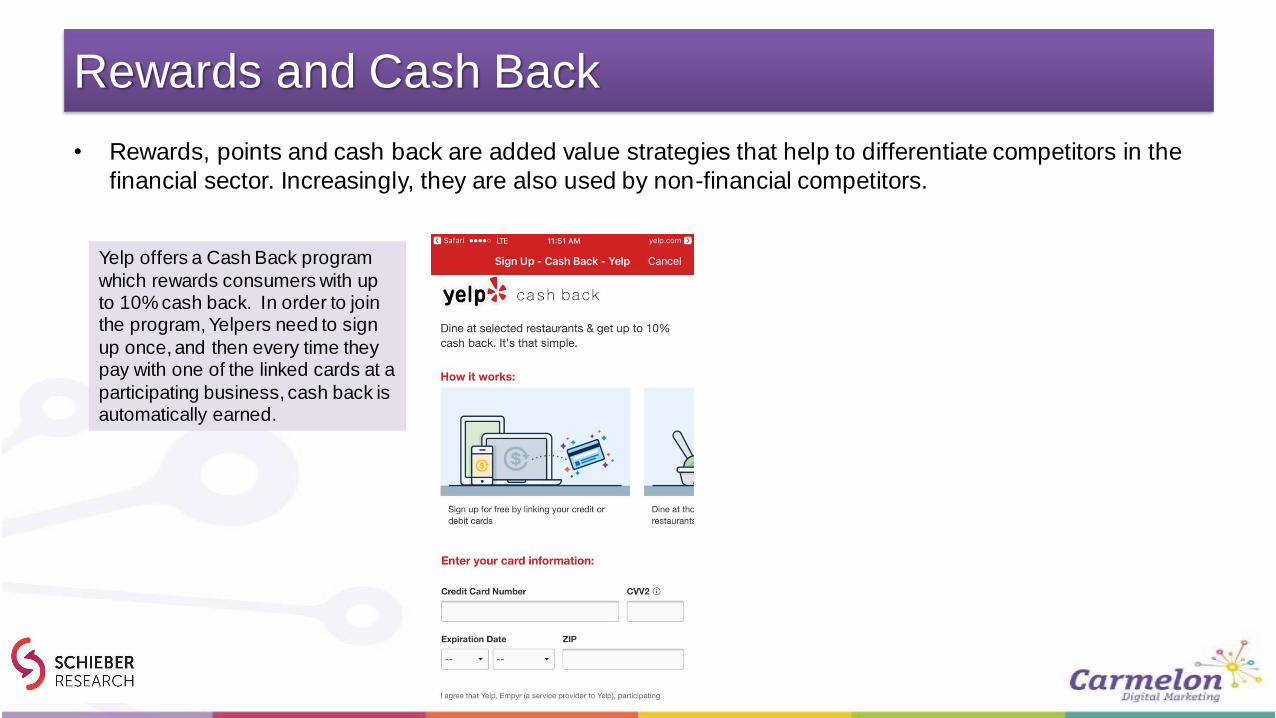

Rewards and Cash Back

• Rewards, points and cash back are added value strategies that help to differentiate competitors in the

financial sector. Increasingly, they are also used by non-financial competitors.

Yelp offers a Cash Back program

which rewards consumers with up to 10% cash back. In order to join the program, Yelpers need to sign

up once, and then every time they pay with one of the linked cards at a

participating business, cash back is automatically earned.

Peer-To-Peer Lending

• The term “peer–to–peer lending” has its origins in the facilitation of unsecured personal lending between individuals

(rather than a company) via digital tools.

• P2P lending are a major industry, and traditional competitors have been responding via partnering / acquiring /

investing in competitors. The leading competitors are Lending Club (with over $20 billion in loan issuance, offering

both consumer and small- and medium-sized enterprise loans), and Prosper (over $6 billion in loans, offers only

unsecured consumer loans and does not make SME loans).

• Some companies have identified the problem of low/ lacking credit score, offering “potential based” loans.

• Competitors such as Prosper and Klear are offering unique

services, further contributing to the overall market growth. For example, Klear claims to offer non-profit financial education.

• Peerform offers p2p lending services to borrowers

with a credit score as low as 600.

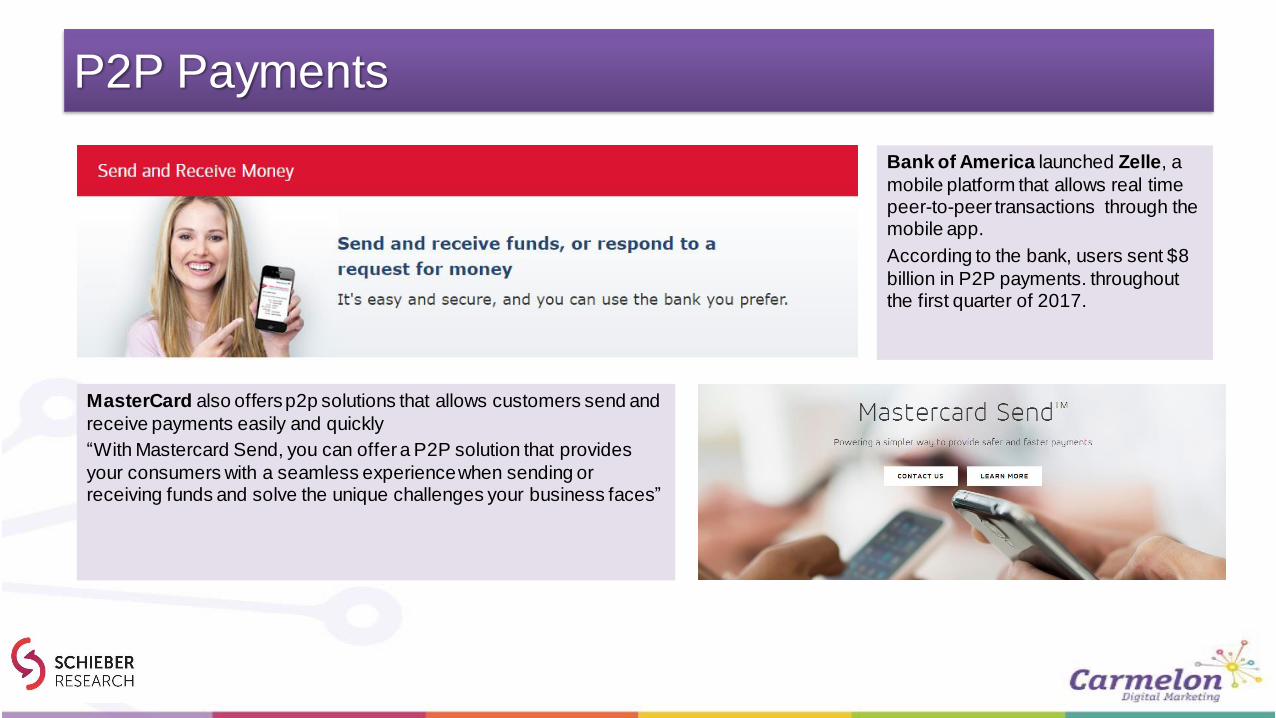

P2P Payments

Bank of America launched Zelle, a

mobile platform that allows real time peer-to-peer transactions through the mobile app.

According to the bank, users sent $8

billion in P2P payments. throughout the first quarter of 2017.

MasterCard also offers p2p solutions that allows customers send and

receive payments easily and quickly

“With Mastercard Send, you can offer a P2P solution that provides

your consumers with a seamless experiencewhen sending or receiving funds and solve the unique challenges your business faces”

Comparison Sites and Aggregators

• Complex insurance products and services are being disentangled by 3rd party websites. Therefore,

navigating between different companies’ solutions will become easier, and we expect that companies

will build specialties for specific market segments rather than a “one size fits all” attitude.

Mint offers personal

finances management Websites such as LearnVest.com and CountAbout.com help

consumers monitor and manage their finances online.

Digital ATMs – and Branches

• A number of banks launched cardless ATMs, to enable customers cash withdrawals from an ATM by tapping their

device when they’re in front of the ATM.

Wells Fargo offers cardlessATM access in USA.

Customers can use their Wells Fergo app and receive a one time token to conduct a transaction.

Bank of America ATMs: make withdrawals using your eligible smartphone.

The company has opened three completely automated branches in Feb. 2017, where customers can use ATMs and have video conferences with employees at other branches.

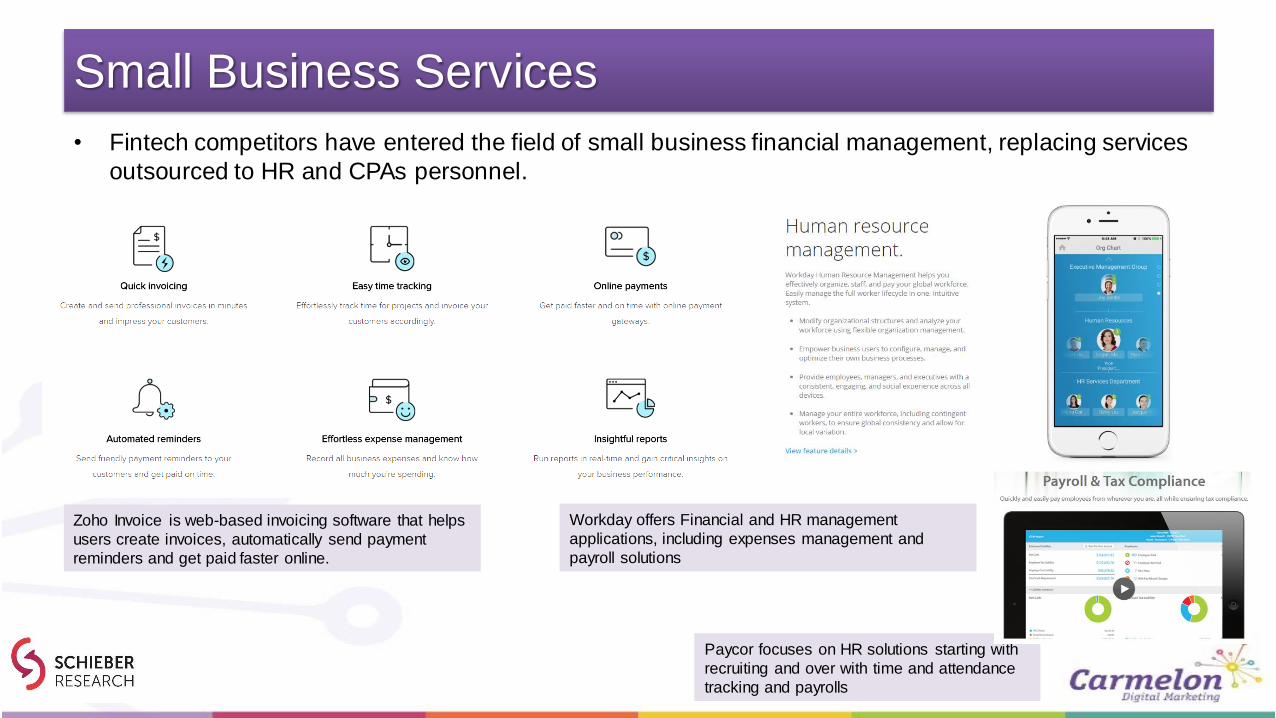

Small Business Services

• Fintech competitors have entered the field of small business financial management, replacing services

outsourced to HR and CPAs personnel.

Workday offers Financial and HR management

applications, including expenses management and

payroll solutions

Paycor focuses on HR solutions starting with

recruiting and over with time and attendance

tracking and payrolls

Zoho Invoice is web-based invoicing software that helps

users create invoices, automatically send payment

reminders and get paid faster online.

How to Utilize Digital for Growth?

• Financial Services brands must provide the following advantages in order to

attract new clients and cross-sell new services to new clients:

– Building Trust through: Personal connection (utilizing social platforms),

content ownership / expertise (utilizing blogs, micro sites etc.) and targeting

niches, through transparency.

– Offering Convenience. On time / on place (utilizing mobile devices). Self

service (utilizing mobile, online and tablet).

– Providing Personalization. Online / mobile customizable tools, device-

specific presentation (such as tablets).

– Offering Simplicity. The industry is perceived as complicated and

confusing. Digital channels are enabling new strategies such as

gamification and simple analysis tools.

Source: Schieber Research & Carmelon Digital Marketing, Digital-Inspired

Trends & Innovations in Financial Services, 2014

Time for AI

• Our 2014 report found that convenience, as well as simplicity, were the key growth drivers for the

industry, in terms of customer benefit: time saving, schlepping-free transactions, etc.; next in line were

money saving and personalization. And indeed, key competitors focused on delivering more

convenience through omni-channel tools, with a specific focus on mobile devices.

• The 2015-2016 reports identified personalization as the key driver for companies, as a result of the use

of Big Data, the rise of Internet of Things (including wearable devices, smart homes and smart cars);

and the growing competition from new industry disruptors, forcing companies to a deeper

understanding of micro-clusters needs, or a “mix and match” between products and services.

• In 2017, the advance in IoT, including smart home (e.g. Amazon’s Echo/ Alexa), as well as artificial

intelligence (AI) will create opportunities for seamless omni-channel transactions, and we also expect

rewards to make a “come back” with better value offers, as a point of differentiation.

Thank You

The research was conducted by: Ruth Lewin-Chen, Hamutal Schieber, Meital Yachin

Schieber Research | Market Research & Competitive Intelligence

www.researchci.com | [email protected]

More articles and researches on Carmelon Digital Marketing website:http://www.carmelon-digital.com