financial statement analysis: methods overview financial statement analysis: methods overview

Post on 19-Dec-2015

278 views

TRANSCRIPT

Financial Statement Analysis:

Methods Overview

Financial Statement Analysis:

Methods Overview

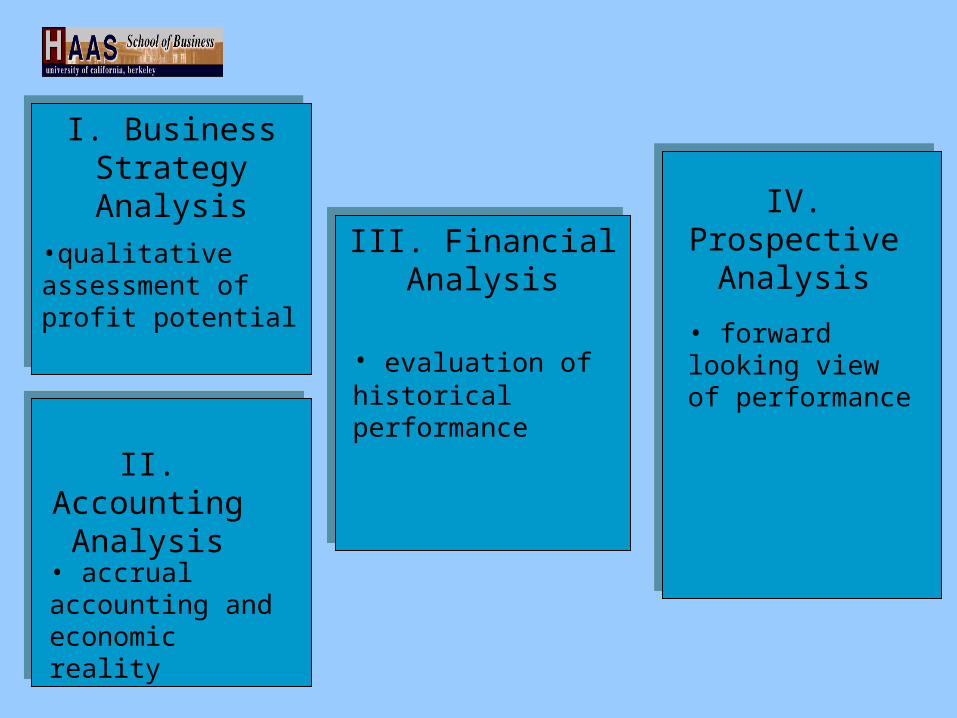

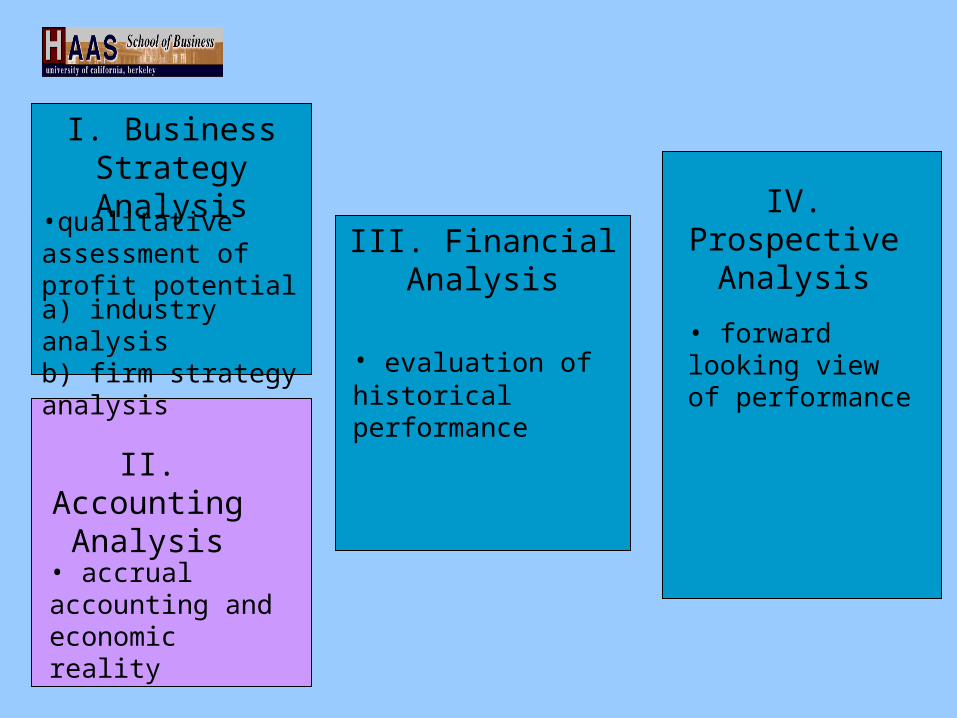

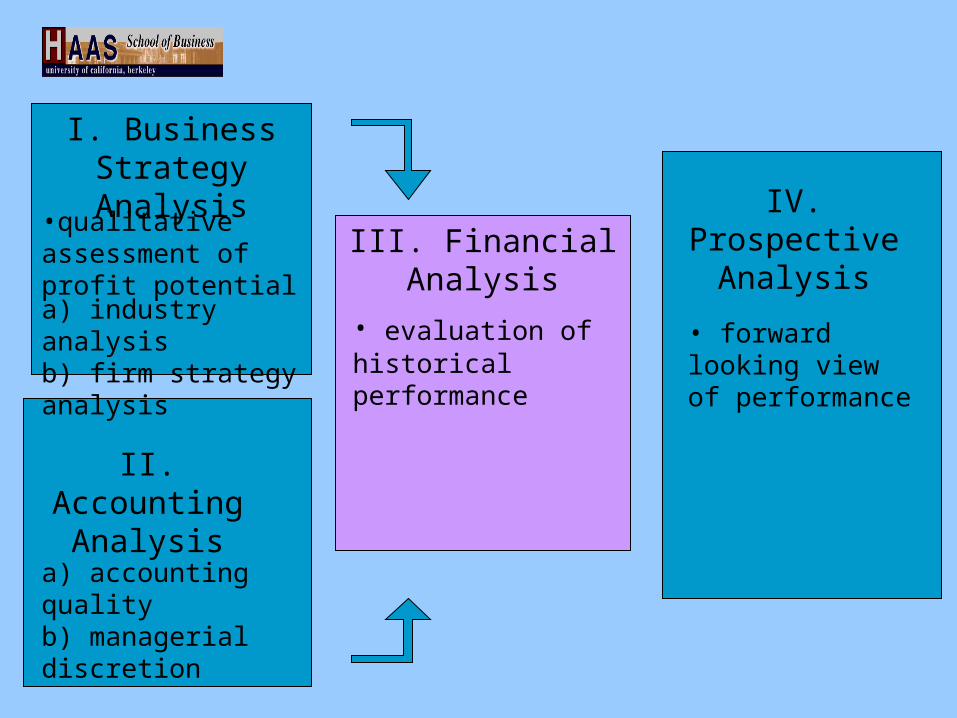

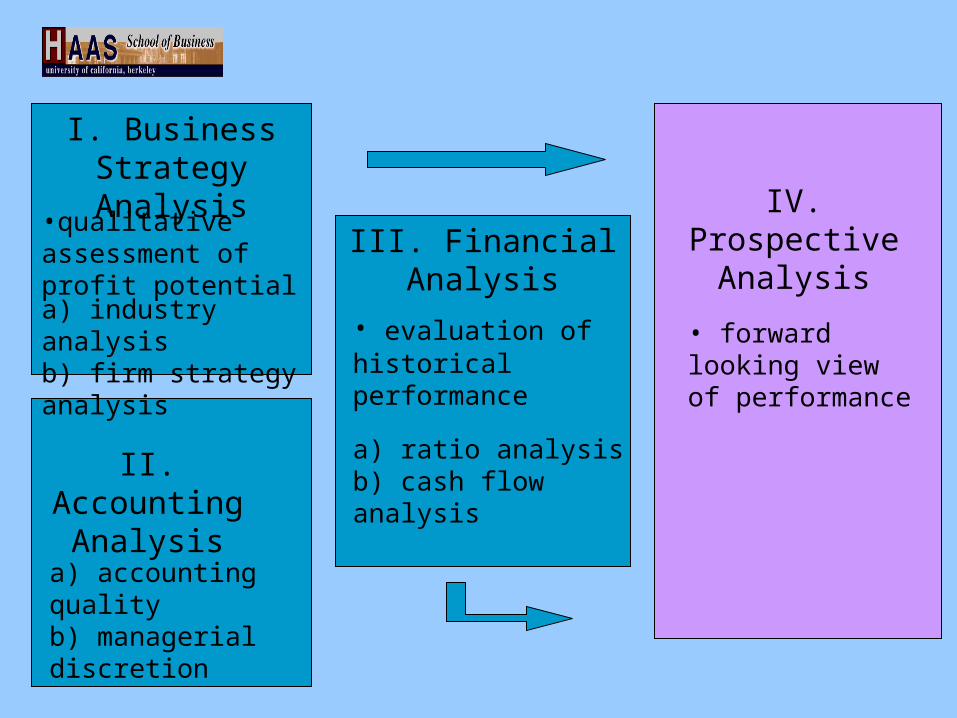

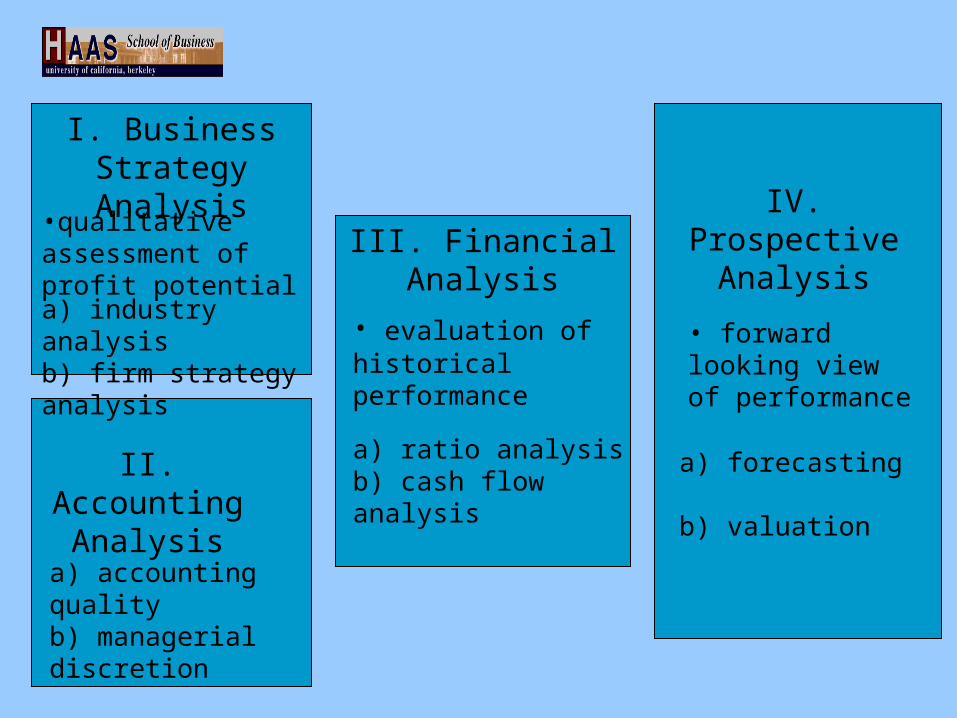

I. Business Strategy Analysis

II. Accounting Analysis

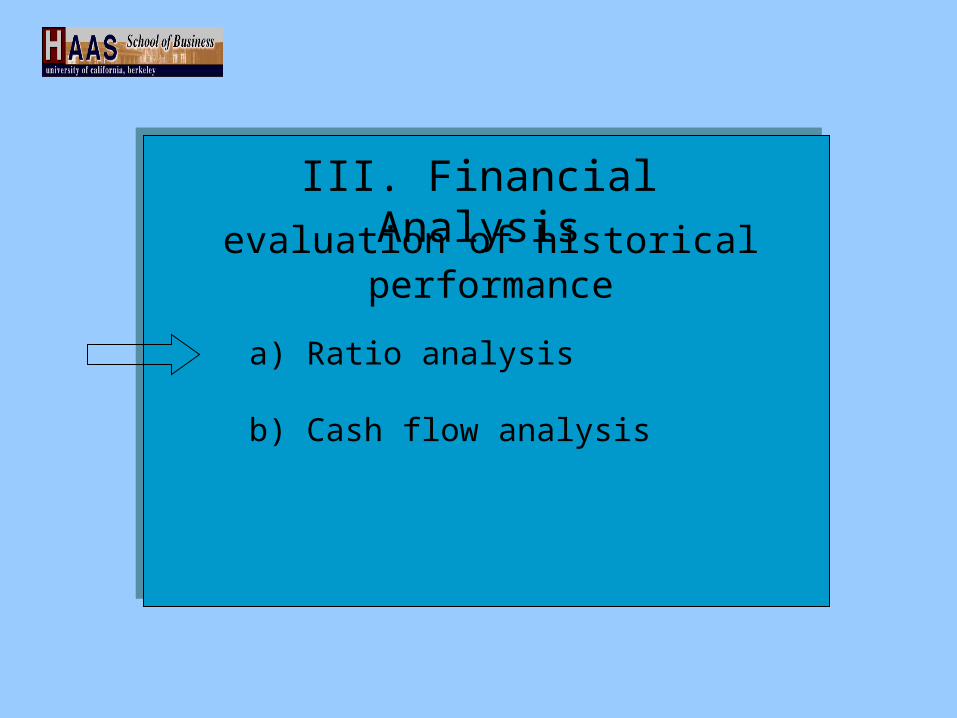

III. Financial Analysis

IV. Prospective Analysis

• accrual accounting and economic reality

• evaluation of historical performance

• forward looking view of performance

•qualitative assessment of profit potential

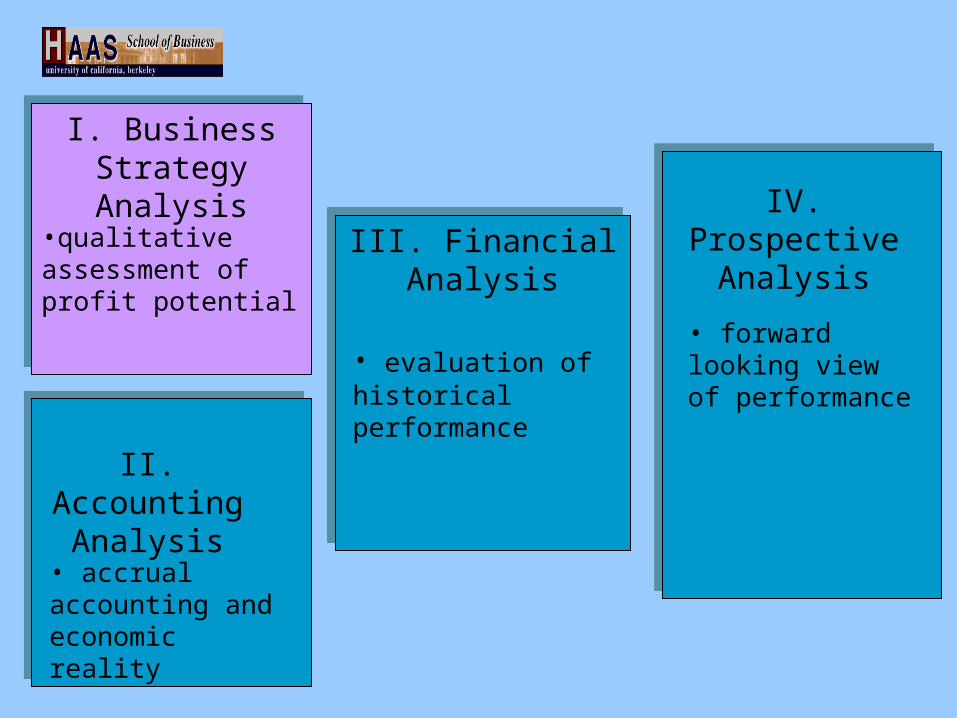

I. Business Strategy Analysis

II. Accounting Analysis

III. Financial Analysis

IV. Prospective Analysis

• accrual accounting and economic reality

• evaluation of historical performance

• forward looking view of performance

•qualitative assessment of profit potential

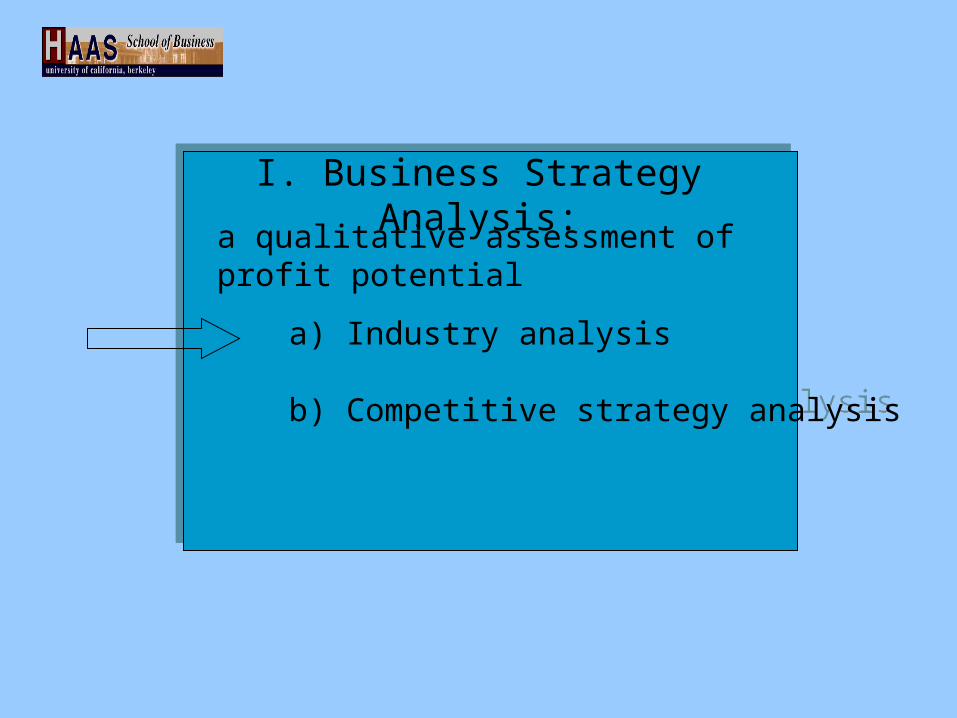

a) Industry analysis

b) Competitive strategy analysis

a) Industry analysis

b) Competitive strategy analysis

I. Business Strategy Analysis:

a qualitative assessment of profit potential

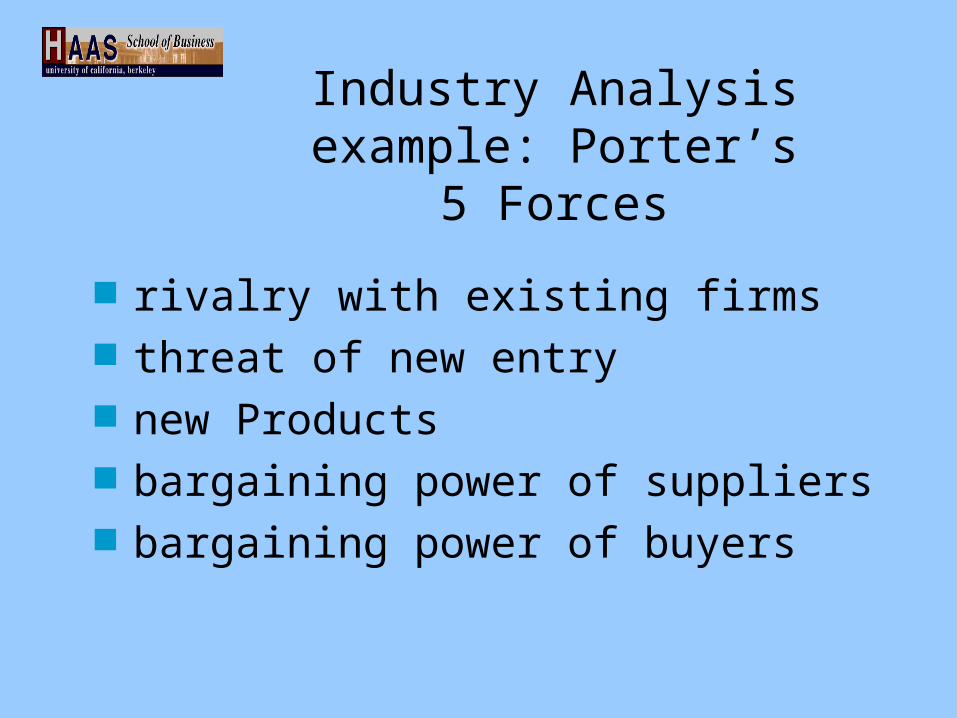

Industry Analysisexample: Porter’s 5 Forces

rivalry with existing firms threat of new entry new Products bargaining power of suppliers bargaining power of buyers

a) Industry analysis

b) Competitive strategy analysis

a) Industry analysis

b) Competitive strategy analysis

I. Business Strategy Analysis:

a qualitative assessment of profit potential

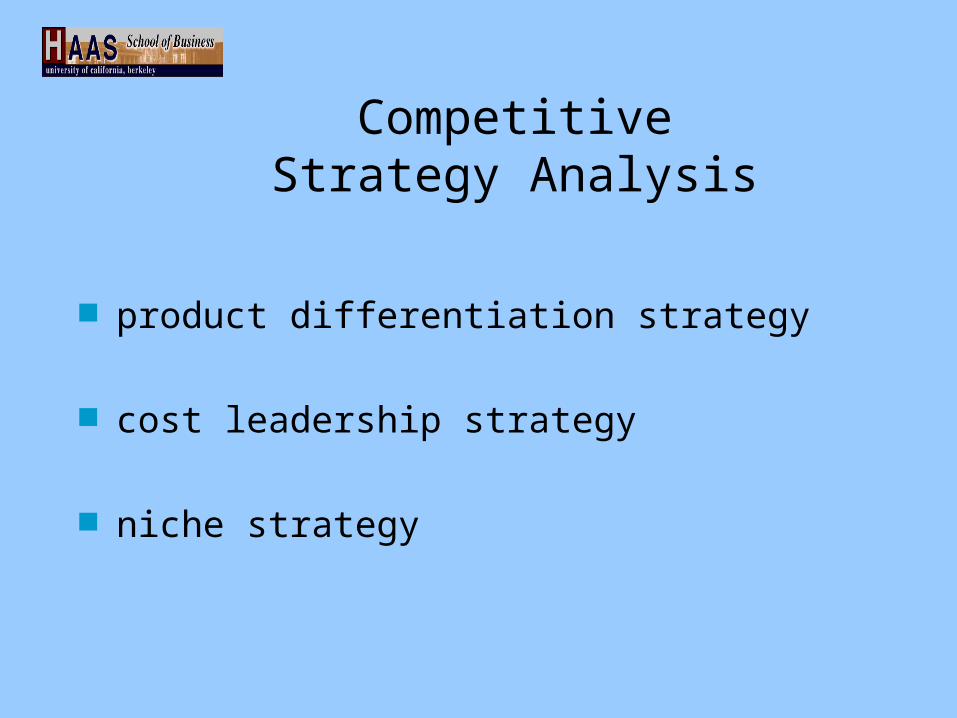

Competitive Strategy Analysis

product differentiation strategy

cost leadership strategy

niche strategy

I. Business Strategy Analysis

II. Accounting Analysis

III. Financial Analysis

IV. Prospective Analysis

• accrual accounting and economic reality

• evaluation of historical performance

• forward looking view of performance

•qualitative assessment of profit potential

a) industry analysisb) firm strategy analysis

a) evaluate accounting quality

b) understand managerial reporting discretion

consequences of accrual accounting

II. Accounting Analysis

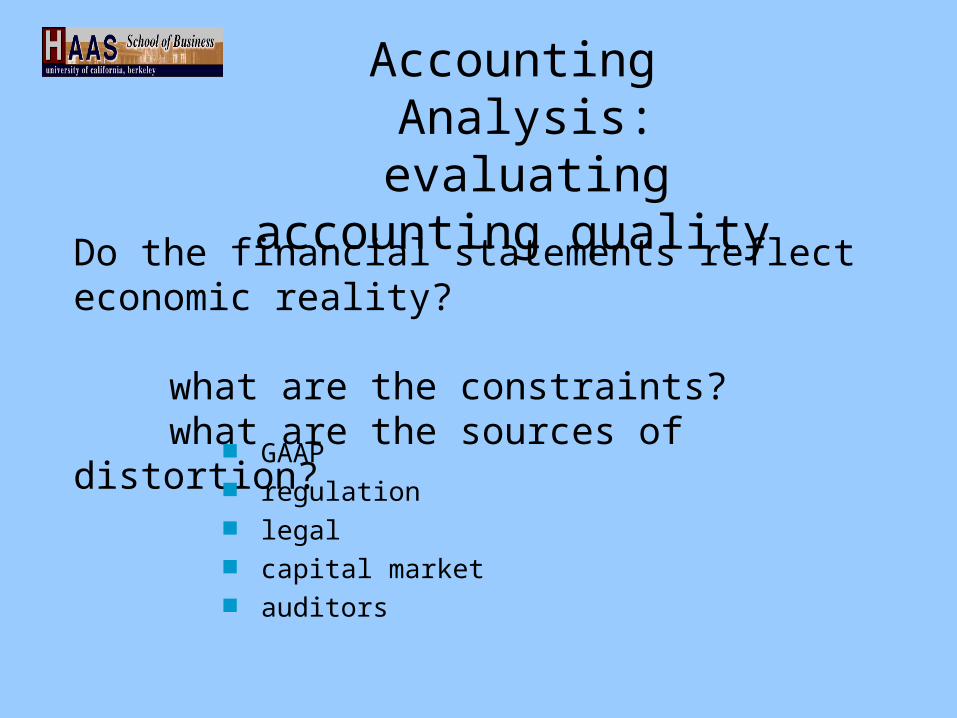

Accounting Analysis:evaluating accounting quality

Do the financial statements reflect economic reality?

what are the constraints?what are the sources of distortion?

GAAP regulation legal capital market auditors

a) evaluate accounting quality

b) understand managerial reporting discretion

consequences of accrual accounting

Accounting Analysis

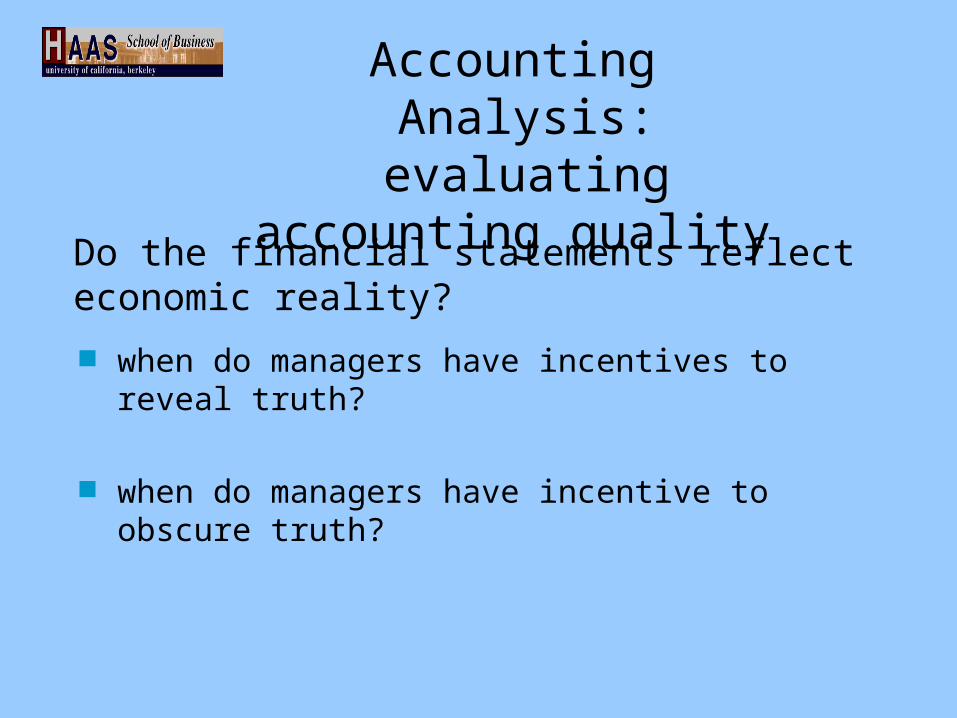

Accounting Analysis:evaluating accounting quality

Do the financial statements reflect economic reality?

when do managers have incentives to reveal truth?

when do managers have incentive to obscure truth?

I. Business Strategy Analysis

II. Accounting Analysis

III. Financial Analysis

IV. Prospective Analysis

a) accounting qualityb) managerial discretion

• evaluation of historical performance

• forward looking view of performance

•qualitative assessment of profit potential

a) industry analysisb) firm strategy analysis

a) Ratio analysis

b) Cash flow analysis

a) Ratio analysis

b) Cash flow analysis

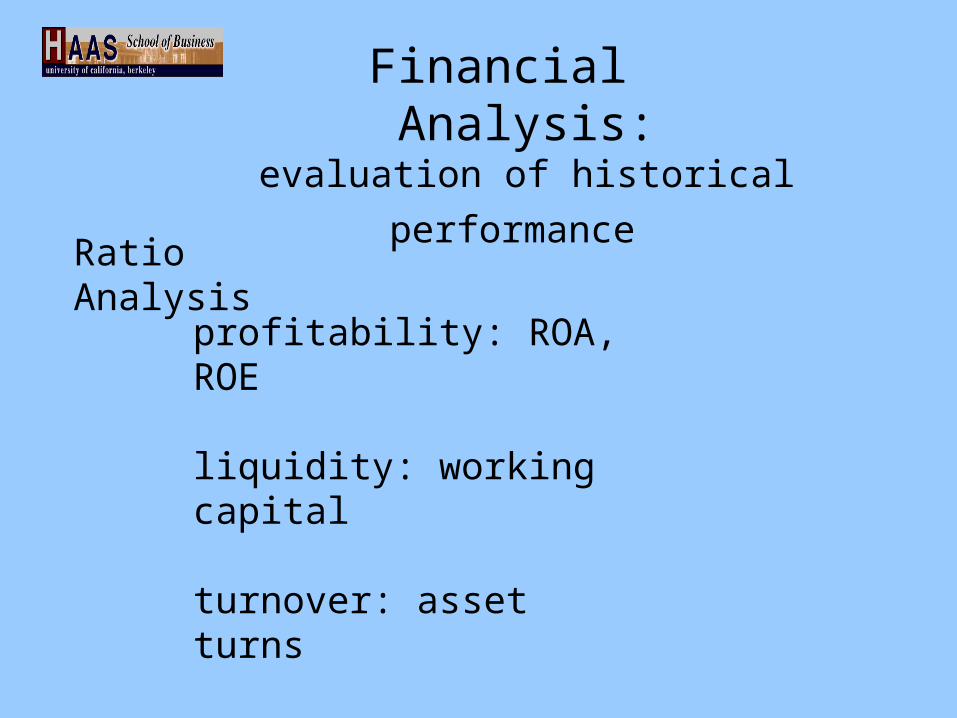

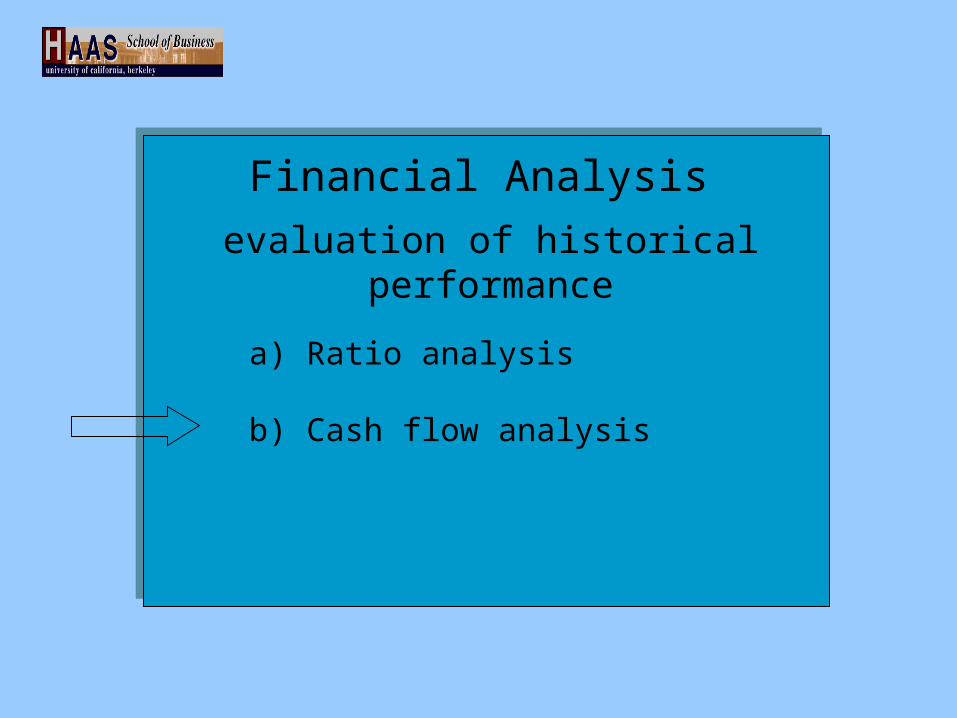

III. Financial Analysis

evaluation of historical performance

Financial Analysis:evaluation of historical performance

Ratio Analysis

profitability: ROA, ROE

liquidity: working capital

turnover: asset turns

leverage: debt to equity

a) Ratio analysis

b) Cash flow analysis

a) Ratio analysis

b) Cash flow analysis

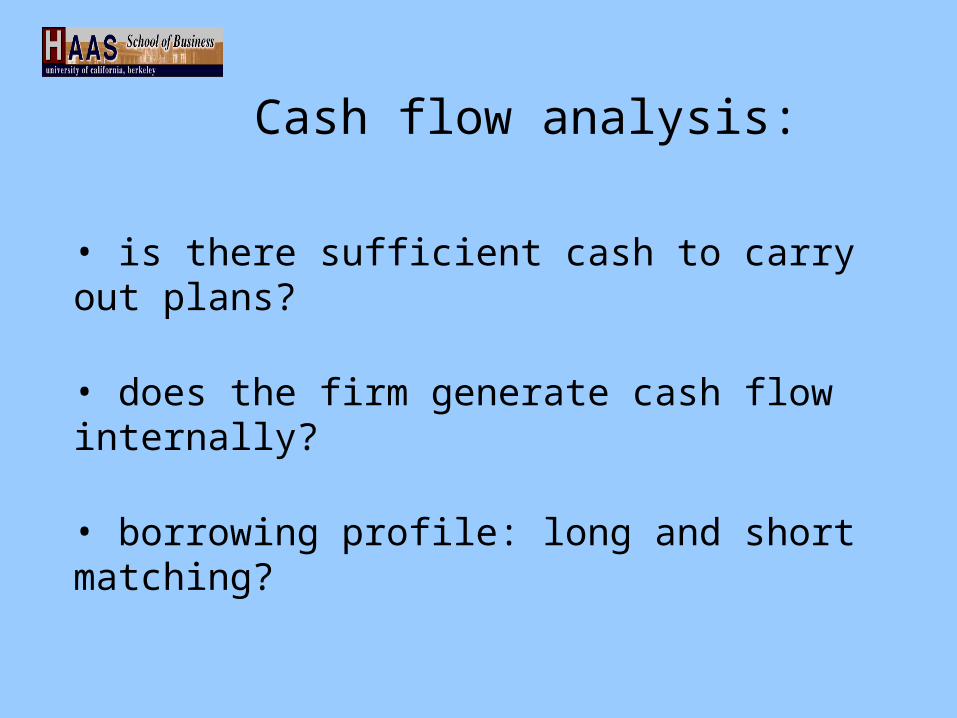

Financial Analysis

evaluation of historical performance

Cash flow analysis:

• is there sufficient cash to carry out plans?

• does the firm generate cash flow internally?

• borrowing profile: long and short matching?

I. Business Strategy Analysis

II. Accounting Analysis

III. Financial Analysis

IV. Prospective Analysis

a) accounting qualityb) managerial discretion

• evaluation of historical performance

• forward looking view of performance

•qualitative assessment of profit potential

a) industry analysisb) firm strategy analysis

a) ratio analysisb) cash flow analysis

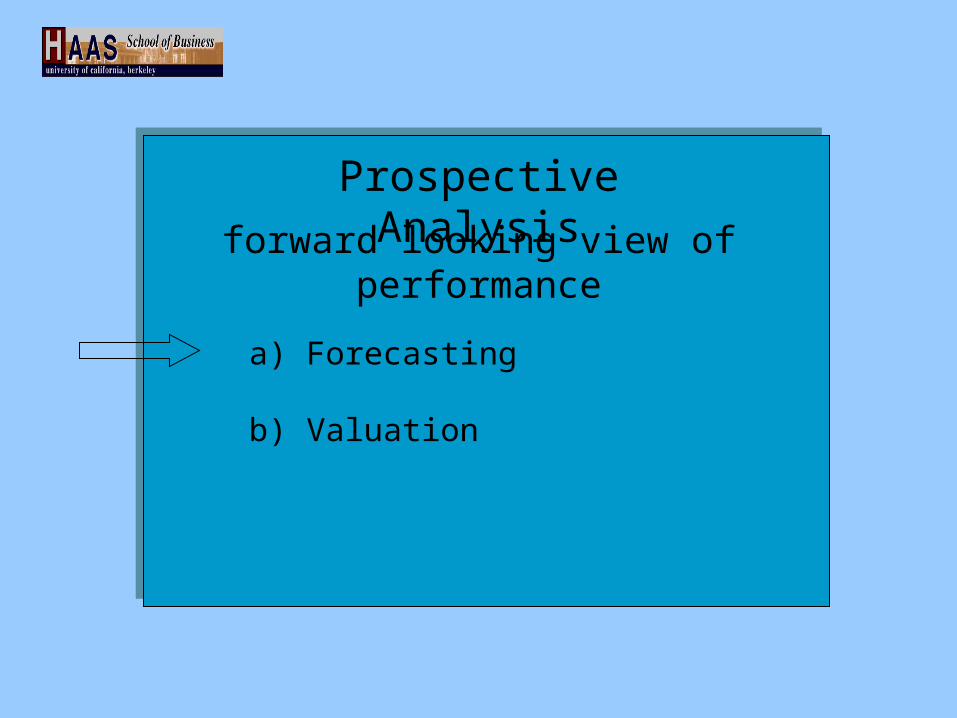

a) Forecasting

b) Valuation

a) Forecasting

b) Valuation

Prospective Analysis

forward looking view of performance

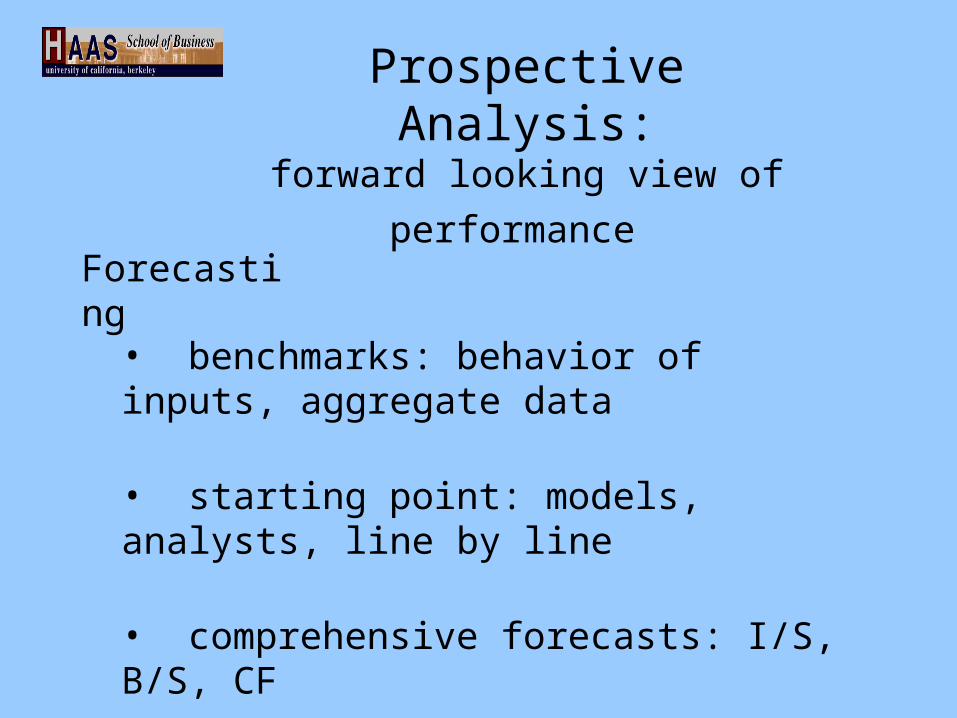

Prospective Analysis:forward looking view of performance

• benchmarks: behavior of inputs, aggregate data

• starting point: models, analysts, line by line

• comprehensive forecasts: I/S, B/S, CF

Forecasting

a) Forecasting

b) Valuation

a) Forecasting

b) Valuation

Prospective Analysis

forward looking view of performance

Prospective Analysis:forward looking view of performance

• DCF

• comparables, Multiples

• accounting based valuation

Valuation

I. Business Strategy Analysis

II. Accounting Analysis

III. Financial Analysis

IV. Prospective Analysis

a) accounting qualityb) managerial discretion

• evaluation of historical performance

• forward looking view of performance

•qualitative assessment of profit potential

a) industry analysisb) firm strategy analysis

a) ratio analysisb) cash flow analysis

a) forecasting

b) valuation