financial statements of - casdsm documents/2014-03-31 children's aid-englis… · financial...

TRANSCRIPT

Financial Statements of

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Years ended March 31 2014 and March 31 2013

KPMG LLP Telephone (705) 675-8500 Chartered Accountants Fax (705) 675-7586 Claridge Executive Centre In Watts (1-800) 461-3551 144 Pine Street PO Box 700 Internet wwwkpmgca Sudbury ON P3E 4R6

INDEPENDENT AUDITORS REPORT

To the Board of Directors of The Childrens Aid Society of the Districts of Sudbury and Manitoulin

We have audited the accompanying financial statements of The Childrens Aid Society of the Districts of Sudbury and Manitoulin which comprise the statements of financial position as at March 31 2014 March 31 2013 and April 1 2012 the statements of operations changes in net assets (deficiency) cash flows and the statements of remeasurement gains and losses for the years ended March 31 2014 and March 31 2013 and notes comprising a summary of significant accounting policies and other explanatory information

Managementrsquos Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in

accordance with Canadian public sector accounting standards and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement whether due to fraud or error

Auditorsrsquo Responsibility

Our responsibility is to express an opinion on these financial statements based on our audits We conducted our audits in accordance with Canadian generally accepted auditing standards Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement

An audit involves performing procedures to obtain audit evidence about the amounts and disclosure in the financial statements The procedures selected depend on our judgment including the assessment of the risks of material misstatement of the financial statements whether due to fraud or error In making those risk assessments we consider internal control relevant to the entityrsquos preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances but not for the purpose of expressing an opinion on the effectiveness of the entityrsquos internal control An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management as well as evaluating the overall presentation of the financial statements

We believe that the audit evidence we have obtained in our audits is sufficient and appropriate to provide a basis for our audit opinion

Opinion

In our opinion the financial statements present fairly in all material respects the financial position of The Childrens Aid Society of the Districts of Sudbury and Manitoulin as at March 31 2014 March 31 2013 and April 1 2012 and its results of operations its changes in net assets (deficiency) its cash flows and the remeasurement gains and losses for the years ended March 31 2014 and March 31 2013 in accordance with Canadian public sector accounting standards

KPMG LLP is a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity KPMG Canada provides services to KPMG LLP

Other Matters

Our audit was made for the purpose of forming an opinion on the basic financial statements taken as a whole The supplementary information included in the Schedule is presented for purposes of additional analysis and is not a required part of the basic financial statements Such information has been subjected to the auditing procedures applied in the audit of the financial statements and in our opinion is fairly stated in all material respects in relation to the basic financial statements taken as a whole

Emphasis of Matter

Without qualifying our opinion we draw attention to Note 13 in the financial statements which indicates that The Childrens Aid Society of the Districts of Sudbury and Manitoulin has experienced accumulated operating losses This may cast doubt about The Childrens Aid Society of the Districts of Sudbury and Manitoulinrsquos ability to continue as a going concern

Chartered Professional Accountants Licensed Public Accountants

June 10 2014

Sudbury Canada

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Statements of Financial Position

March 31 2014 March 31 2013 and April 1 2012

March 31 March 31 April 1

2014 2013 2012

Assets

Current assets Cash $ 2883252 1173655 1642401 Accounts receivable

Due from the Ministry of Children and Youth Services 214793 515071 358142 Other 221874 184863 198110

Prepaid expenses 216590 199116 173901

3536509 2072705 2372554

Capital assets (note 3) 4980929 5231292 5503390

$ 8517438 7303997 7875944

Liabilities and Net Assets (Deficiency)

Current liabilities Accounts payable and accrued liabilities (note 6) $ 3153287 2903964 3134981 Vacation payable 558233 570376 552008 Health spending account 79378 270000 260000 Deferred revenue - Ontario Child Benefit Equivalent 407625 530742 673257 Current portion of long-term debt (note 5) 219443 228175 216064

4417966 4503257 4836310

Employee future benefits (note 4) 5127474 4683179 4395570 Long-term debt (note 5) 3794911 4080048 4308223 Interest rate swaps (note 5) 599060 817284 807174

13939411 14083768 14347277

Net assets (deficiency) Unrestricted

Operating (24403) (1362001) (1435684) Employee related (5765085) (5523555) (5207578) Interest rate swaps (807174) (807174) (807174)

Capital (note 7) 966575 923069 979103

(5630087) (6769661) (6471333)

Accumulated remeasurement gains and losses 208114 (10110) -

(5421973) (6779771) (6471333) Commitments (note 8) Contingencies (note 9) Future operations (note 13)

$ 8517438 7303997 7875944

See accompanying notes to financial statements

1

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Statements of Operations

Years ended March 31 2014 and March 31 2013

2014 2013 Operating Capital Total Total (Schedule)

Revenue Ministry of Children and Youth Services

- Child Welfare Operating $ 37129680 - 37129680 37635554 - Ontario Child Benefit Equivalent 559947 - 559947 550263 - Other 104825 - 104825 104825

Childrens special allowance 1391890 - 1391890 1372000 Maintenance from other societies 309400 - 309400 240030 Childrens pensionbenefits 2979 - 2979 7894 Maintenance from parents 1150 - 1150 4072 Interest 31029 - 31029 20242 Rental income 245355 - 245355 217598 Recoveries 386418 - 386418 420693 Gain on debt retirement - 17499 17499 -Other 18492 - 18492 33012

40181165 17499 40198664 40606183

Expenses Wages 14747159 - 14747159 15009750 Benefits 4209724 - 4209724 4012471 Travel 1790964 - 1790964 1824012 Training and recruitment 104713 - 104713 100171 Building occupancy 898223 - 898223 796775 Amortization - 290714 290714 300195 Interest on long-term debt 218585 - 218585 234482 Purchased services - non-case related 270976 - 270976 166505 Purchased services - case related 819082 - 819082 1039468 Boarding rates 13356922 - 13356922 13844683 Client personal needs 1999109 - 1999109 1923564 Medical and related services 735668 - 735668 746514 Promotion and publicity 18324 - 18324 18612 Office 390501 - 390501 452360 Technology 227999 - 227999 307260 Miscellaneous 312645 - 312645 287593

40100594 290714 40391308 41064415

Excess (deficiency) of revenue over expenses before undernoted 80571 (273215) (192644) (458232)

Provincial subsidy for funding of prior years deficit 1332218 - 1332218 159904

Excess (deficiency) of revenue over expenses $ 1412789 (273215) 1139574 (298328)

See accompanying notes to financial statements

2

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Statements of Changes in Net Assets (Deficiency)

Years ended March 31 2014 and March 31 2013

Operating

March 31 2014

Unrestricted

Employee Interest Total related Rate Swaps Unrestricted Capital Total

Net assets beginning of year

Excess (deficiency) of revenue over expenses

Net change in investment in capital assets

$ (1362001)

1654319

(316721)

(5523555)

(241530)

-

(807174)

-

-

(7692730)

1412789

(316721)

923069

(273215)

316721

(6769661)

1139574

-

Net assets end of the year $ (24403) (5765085) (807174) (6596662) 966575 (5630087)

Operating

March 31 2013

Unrestricted

Employee Interest Total related Rate Swaps Unrestricted Capital Total

Net assets

April 1 2012 (note 2a)) $ (1435684) (5207578) (807174) (7450436) 979103 (6471333)

Excess (deficiency) of revenue over expenses

Net change in investment in capital assets

317844

(244161)

(315977)

-

-

-

1867

(244161)

(300195)

244161

(298328)

-

Net assets end of the year $ (1362001) (5523555) (807174) (7692730) 923069 (6769661)

See accompanying notes to financial statements

3

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Statements of Cash Flows

Years ended March 31 2014 and March 31 2013

2014 2013

Cash flows from operating activities Excess (deficiency) of revenue over expenses Adjustment for

Amortization of capital assets Provision for employment-related obligations Gain on debt retirement

Change in non-cash working capital Decrease (increase) in due from the Ministry of Children and Youth Services Decrease (increase) in accounts receivable - other Increase in prepaid expenses Increase (decrease) in accounts payable

and accrued liabilities Increase (decrease) in vacation payable Increase (decrease) in health spending account Decrease in deferred revenue - Ontario Child Benefit Equivalent

$ 1139574

290714 444295 (17499)

1857084

300278 (37011) (17474)

249323 (12143)

(190622)

(123117)

2026318

$ (298328)

300195 287609

-

289476

(156929) 13247

(25215)

(231017) 18368 10000

(142515)

(224585)

Cash flows from financing activities Principal repayments on long-term debt (276371) (216064)

Cash flows from capital activities Capital asset additions (40350) (28097)

Net increase (decrease) in cash 1709597 (468746)

Cash beginning of year 1173655 1642401

Cash end of year $ 2883252 $ 1173655

See accompanying notes to financial statements

4

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Statements of Remeasurement Gains and Losses

Years ended March 31 2014 and March 31 2013

March 31 2014 Total

Accumulated remeasurement losses April 1 2013

Unrealized gains attributable to Derivative - interest rate swap

Accumulated remeasurement gains March 31 2014

$

$

(10110)

218224

208114

March 31 2013 Total

Accumulated remeasurement gains and losses April 1 2012

Unrealized losses attributable to Derivative - interest rate swap

Accumulated remeasurement losses March 31 2013

$

$

-

(10110)

(10110)

See accompanying notes to financial statements

5

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements

Years ended March 31 2014 and March 31 2013

The Childrens Aid Society of the Districts of Sudbury and Manitoulin (the Society) provides child protection services in the territorial districts of Sudbury and Manitoulin It is incorporated without share capital under the Laws of Ontario and is registered as a tax-exempt charitable organization under the Federal Income Tax Act

On April 1 2013 the Society adopted Canadian Public Sector Accounting Standards The Society has also elected to apply the 4200 standards for government not-for-profit organizations These are the first financial statements prepared in accordance with these public sector accounting standards

In accordance with the transitional provisions in Canadian Public Sector Accounting Standards the Society has adopted the changes retrospectively subject to certain exemptions allowed under these standards The transition date is April 1 2012 and all comparative information provided has been presented by applying public sector accounting standards

A summary of transitional adjustments recorded to net assets (deficiency) and excess (deficiency) of revenue over expenses is provided in note 2

1 Significant accounting policies

(a) Revenue recognition

The Society accounts for contributions which include donations and government grants under the deferral method of accounting as follows

Operating grants are recorded as revenue in the period to which they relate

Grants and donations relating to future periods are deferred and recognized in the subsequent period when the related activity occurs

Grants approved but not received are accrued

Unrestricted contributions are recognized as revenue when received or receivable if the amounts can be reasonably estimated and collection is reasonably assured

Externally restricted contributions are recognized as revenue in the period in which the related expenses are recognized

Contributions restricted for the purchase of capital assets are deferred and amortized into revenue at rates corresponding to those of the related capital assets

6

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

1 Significant accounting policies (continued)

(b) Capital assets

Capital assets are recorded at cost Amortization of capital assets is recorded as follows

Asset Basis Period

Buildings Straight-line 30 years Furniture and equipment Straight-line 10 years Computer equipment Straight-line 3 years

(c) Employee future benefits

Vacation entitlements and banked overtime are accrued for as entitlements are earned

The health spending account reflects the provision for the annual discretionary employee health spending of up to $1000 annually

The Society accrues its obligations for post-employment benefit plans as the employees render the services necessary to earn the benefits The actuarial determination of the accrued benefit obligation uses the projected benefit method prorated on service (which incorporates managementrsquos best estimate of future salary levels other cost escalation retirement ages of employees and other actuarial factors) Under this method the benefit costs are recognized over the expected average service life of the employee group

Actuarial gains and losses on the accrued benefit obligation arise from differences between actual and expected experience and from changes in the actuarial assumptions used to determine the accrued benefit obligation The Society elected to recognize these on transition The most recent actuarial valuation of the sick leave plan and the benefit plan was as of April 1 2012

For the post-employment benefits (continuation of life medical and dental during LTD) these benefits are accounted for on a terminal basis in comparison to the non-pension post-retirement benefit which is accounted for on an accrual basis This means that the liability for the post-employment benefit is accrued only when a LTD claim occurs For these benefits the full change in the liability is being recognized immediately as an expense in the year

Substantially all of the employees of the Society are eligible to be members of the Ontario Municipal Employeesrsquo Retirement Fund (ldquoOMERSrdquo) which is a multi-employer defined benefit final average earnings and contributory pension plan Defined contribution plan accounting is applied to OMERS as the Society has insufficient information to apply defined benefit accounting (note 10)

7

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

1 Significant accounting policies (continued)

(d) Use of estimates

The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting periods Items subject to such estimates are valuation of capital assets and employee future benefits Actual results could differ from those estimates These estimates are reviewed periodically and as adjustments become necessary they are reported in earnings in the year in which they become known

(e) Financial instruments

All financial instruments are initially recorded on the statement of financial position at fair value

All investments held in equity instruments that trade in an active market would be recorded at fair value Management has elected to record investments at fair value as they are managed and evaluated on a fair value basis

Unrealized changes in fair value would be recognized in the statement of remeasurement gains and losses until they are realized when they would be transferred to the statement of operations

Transaction costs incurred on the acquisition of financial instruments measured subsequently at fair value are expensed as incurred

Where a decline in fair value is determined to be other than temporary the amount of the loss

is removed from accumulated remeasurement gains and losses and recognized in the statement of operations On sale the amount held in accumulated remeasurement gains and losses associated with that instrument is removed from net assets and recognized in the

statement of operations

8

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

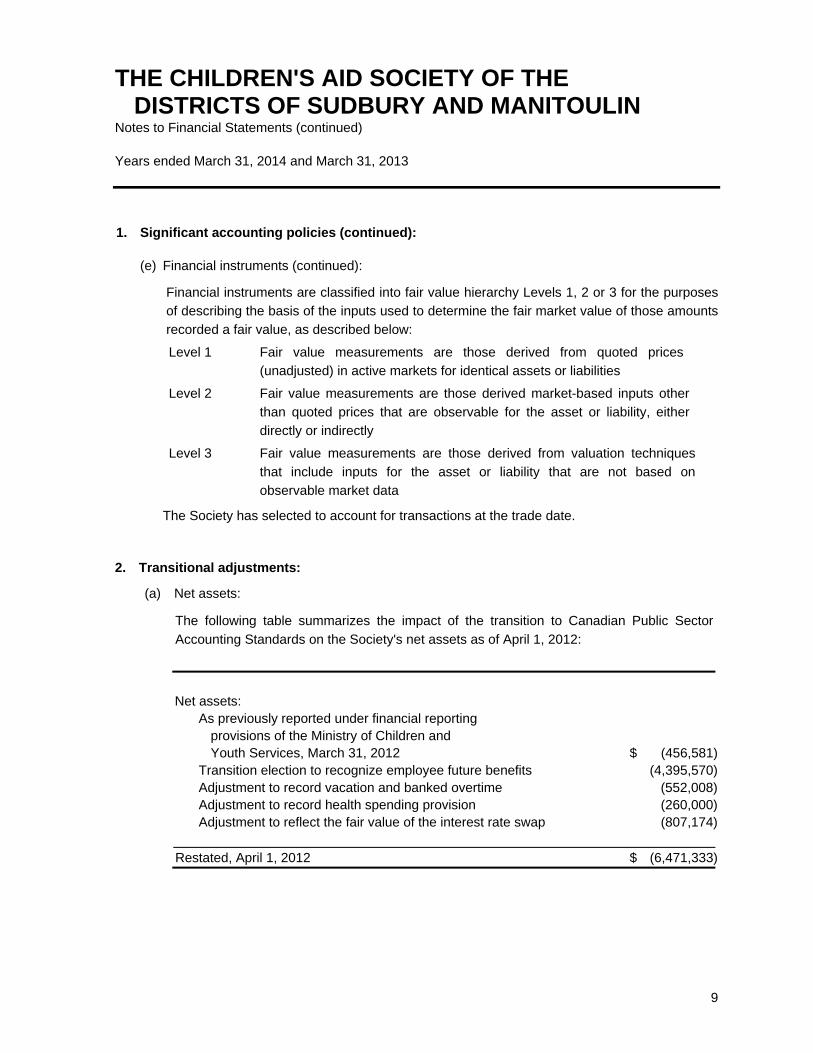

1 Significant accounting policies (continued)

(e) Financial instruments (continued)

Financial instruments are classified into fair value hierarchy Levels 1 2 or 3 for the purposes of describing the basis of the inputs used to determine the fair market value of those amounts recorded a fair value as described below

Level 1 Fair value measurements are those derived from quoted prices (unadjusted) in active markets for identical assets or liabilities

Level 2 Fair value measurements are those derived market-based inputs other

than quoted prices that are observable for the asset or liability either directly or indirectly

Level 3 Fair value measurements are those derived from valuation techniques

that include inputs for the asset or liability that are not based on observable market data

The Society has selected to account for transactions at the trade date

2 Transitional adjustments

(a) Net assets

The following table summarizes the impact of the transition to Canadian Public Sector

Accounting Standards on the Societys net assets as of April 1 2012

Net assets As previously reported under financial reporting

provisions of the Ministry of Children and Youth Services March 31 2012 $ (456581)

Transition election to recognize employee future benefits (4395570) Adjustment to record vacation and banked overtime (552008) Adjustment to record health spending provision (260000) Adjustment to reflect the fair value of the interest rate swap (807174)

Restated April 1 2012 $ (6471333)

9

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

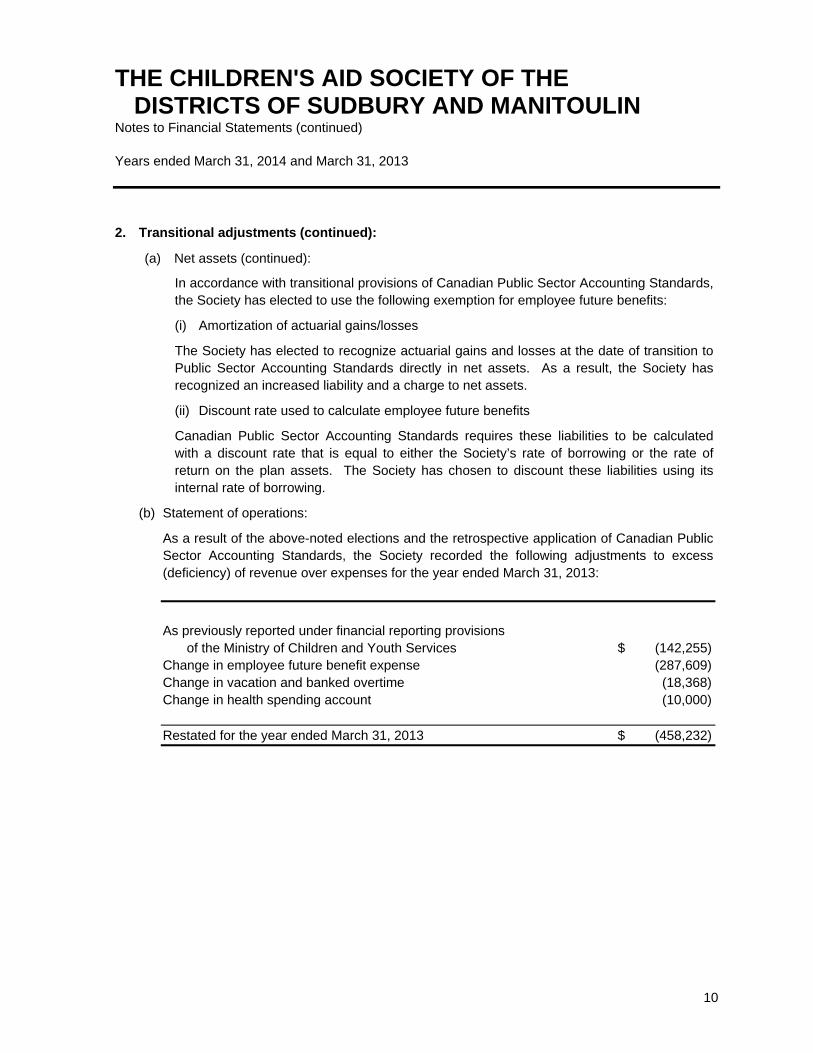

2 Transitional adjustments (continued)

(a) Net assets (continued)

In accordance with transitional provisions of Canadian Public Sector Accounting Standards the Society has elected to use the following exemption for employee future benefits

(i) Amortization of actuarial gainslosses

The Society has elected to recognize actuarial gains and losses at the date of transition to Public Sector Accounting Standards directly in net assets As a result the Society has recognized an increased liability and a charge to net assets

(ii) Discount rate used to calculate employee future benefits

Canadian Public Sector Accounting Standards requires these liabilities to be calculated with a discount rate that is equal to either the Societyrsquos rate of borrowing or the rate of return on the plan assets The Society has chosen to discount these liabilities using its internal rate of borrowing

(b) Statement of operations

As a result of the above-noted elections and the retrospective application of Canadian Public Sector Accounting Standards the Society recorded the following adjustments to excess (deficiency) of revenue over expenses for the year ended March 31 2013

As previously reported under financial reporting provisions of the Ministry of Children and Youth Services

Change in employee future benefit expense Change in vacation and banked overtime Change in health spending account

$ (142255) (287609) (18368) (10000)

Restated for the year ended March 31 2013 $ (458232)

10

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

3 Capital assets

March 31 2014 Cost AccumulatedAmortization

Net book value

Land Buildings Furniture and equipment Computer equipment

$ 675000 54099621045628

167153

$ 7297743

ndash 1315264

879772 121778

2316814

675000 4094698

165856 45375

4980929

March 31 2013 Cost AccumulatedAmortization

Net book value

Land Buildings Furniture and equipment Computer equipment

$ 675000 5409962 1017503

250971

$ 7353436

ndash 1122290

835712 164142

2122144

675000 4287672

181791 86829

5231292

April 1 2012 Cost AccumulatedAmortization

Net book value

Land Buildings Furniture and equipment Computer equipment Leasehold improvements

$ 675000 5409962 1017503

339738 238255

$ 7680458

ndash 929316 791458 218039 238255

2177068

675000 4480646

226045 121699

ndash

5503390

11

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

4 Employee future benefits

The Society maintains defined benefit and defined contribution plans providing other retirement and employee future benefits to most of its employees

The costs of other post-employment benefits (including medical benefits dental care life insurance and certain compensated absences) related to the employeesrsquo current service is charged to income annually The cost is computed on an actuarial basis using the projected benefit method estimating the usage frequency and cost of services covered and managementrsquos best estimates of investment yields salary escalation and other factors Plan assets are valued at fair value for purposes of calculating the expected return on plan assets

The fair values of plan assets and accrued benefit obligations were determined by independent actuaries on behalf of the Society as at April 1 2012

The accrued benefit obligations accrued at March 31 2014 amounted to $5127474 (March 31 2013 - $4683179 April 1 2012 - $4395570) The benefits paid out in the year were $53866 (March 31 2013 - $55280)

The discount rate used is 43 (March 31 2013 ndash 4) Health care costs are presumed to increase at 8 commencing the first year and grading to 4 in 2022

5 Long-term debt

March 31 March 31 April 1 2014 2013 2012

CIBC debt due April 2 2027 $ 4014354 4222616 4420270 Unsecured promissory note payable with interest

at 80 due December 20 2016 ndash 85607 104017 4014354 4308223 4524287

Current portion of long-term debt (219443) (228175) (216064)

$ 3794911 4080048 4308223

Interest rate swaps $ 599060 817284 807174

12

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

5 Long-term debt (continued)

The CIBC debt due April 2 2027 is secured by a first fixed charge on the land and building to which it relates The debt was advanced under a variable rate credit facility with interest adjusted monthly To reduce the interest rate cash flow risk on this debt the Society has entered into an interest rate swap contract that entitles the Society to receive interest at floating rates on the notional principal amount and obliges it to pay interest at a fixed rate of 524 over the entire term of the debt The fair value of the interest rate swap has been determined using Level 3 of the fair value hierarchy The net interest receivable or payable under the contract is settled monthly with the CIBC which is a Canadian chartered bank

The Ministry of Children and Youth Services has approved the use of operating funds for the purpose of mortgage repayments To protect their interest on the land and building the Ministry has entered into a Mortgage Funding Agreement with the Society The Agreement which has been registered with the Lands Registration Office gives the Ministry rights on the use and disposition of the property

The unsecured promissory note was obtained to finance leasehold improvements

Principal due within each of the next five years on the long-term debt is as follows

2015 $ 219442 2016 231221 2017 243633 2018 256710 2019 270489

6 Accounts payable and accrued liabilities

Included in accounts payable and accrued liabilities are government remittances payable of $18693 (March 31 2013 - $32859 April 1 2012 - $32051) which includes amounts payable for HST and payroll related taxes

13

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

7 Capital

The equity in capital assets is calculated as follows

March 31 March 31 April 1 2014 2013 2012

Capital assets $ 4980929 5231292 5503390

Less Long-term debt (4014354) (4308223) (4524287)

$ 966575 923069 979103

8 Commitments

The rental obligations for leased property in Little Current and Chapleau are as follows

2015 $ 120676 2016 45029 2017 45029 2018 45029 2019 45029 2020 45029 2021 3752

9 Contingencies

The Society is involved in certain legal matters and litigation the outcome of which is not presently determinable The loss if any from these contingencies will be accounted for in the periods in which the matters are resolved Management is of the opinion these matters are mitigated by adequate insurance coverage

10 Pension agreement

The Society makes contributions to OMERS which is a multi-employer plan on behalf of certain members of its staff The plan is a defined benefit plan which specifies the amount of the retirement benefit to be received by the employees based on the length of service and rates of pay

The amount contributed to OMERS for 2014 was $1467897 (March 31 2013 - $1370016) for current service

14

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

11 Financial risks

(a) Credit and market risk

The Society has no significant exposure to credit or market risks

(b) Liquidity risk

Liquidity risk is that the Society will be unable to fulfill its obligations on a timely basis or at a reasonable cost The Society manages its liquidity risk by monitoring its operating requirements The Society prepares budget and cash forecasts to ensure it has sufficient funds to fulfill its obligations

(c) Interest rate risk

Interest rate risk is the potential for financial loss caused by fluctuations in fair value or future cash flows of financial instruments because of changes in market interest rates

The Society is exposed to this risk through its interest bearing investments bank loans and term debt

The Society mitigates interest rate risk on its term debt through derivative financial instrument (interest rate swaps) that exchanges the variable rate inherent in the term debt for a fixed rate (see note 5) Therefore fluctuations in market interest rates would not impact future cash flows and operations relating to the term debt

There have been no significant changes from the previous year in the exposure to risk or policies procedures and methods used to measure the risk

12 Public Sector Disclosure Act

For the calendar year ended December 31 2013 the Society is in compliance with the Public Sector Disclosure Act 1996 and the Public Sector Salary Disclosure Amendment Act 2004

13 Future operations

These financial statements have been prepared on the going concern basis notwithstanding the effect of accumulated operating losses The Societyrsquos ability to realize its assets and discharge its liabilities in the normal course of business is dependent upon the continued support of its funding Ministry and its creditors which is anticipated by Management

15

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Schedule of Operations by Program

Years ended March 31 2014 and March 31 2013

Ontario Child Employment Benefit Targeted Total Total

Child Welfare Related Equivalent Subsidies Independence 2014 2013

Revenue Ministry of Children and Youth Services

- Child Welfare Operating $ 37077430 $ - $ - $ 52250 $ - $ 37129680 $ 37635554 - Ontario Child Benefit Equivalent - - 559947 - - 559947 550263 - Other - - - - 104825 104825 104825

Childrens special allowance 1391890 - - - - 1391890 1372000 Maintenance from other societies 309400 - - - - 309400 240030 Childrens pensionbenefits 2979 - - - - 2979 7894 Maintenance from parents 1150 - - - - 1150 4072 Interest 31029 - - - - 31029 20242 Rental income 245355 - - - - 245355 217598 Recoveries 386418 - - - - 386418 420693 Other 18492 - - - - 18492 33012

39464143 - 559947 52250 104825 40181165 40606183

Expenses Wages 14676272 (12143) - - 83030 14747159 15009750 Benefits 3934255 253673 - - 21796 4209724 4012471 Travel 1790964 - - - - 1790964 1824012 Training and recruitment 104713 - - - - 104713 100171 Building occupancy 898223 - - - - 898223 796775 Interest on long-term debt 218585 - - - - 218585 234482 Purchased Services - non-case related 270976 - - - - 270976 166505 Purchased Services - case related 819082 - - - - 819082 1039468 Boarding rates 13356922 - - - - 13356922 13844683 Client personal needs 1386912 - 559947 52250 - 1999109 1923564 Medical and related services 735668 - - - - 735668 746514 Promotion and publicityPromotion and publicity 18 32418324 - - - - 18 32418324 18 61218612 Office 390501 - - - - 390501 452360 Technology 227999 - - - - 227999 307260 Miscellaneous 312645 - - - - 312645 287593

39142041 241530 559947 52250 104826 40100594 40764220

Excess (deficiency) of revenue over expenses before undernoted items 322102 (241530) - - (1) 80571 (158037)

Provincial subsidy for funding of prior years deficit 1332218 - - - - 1332218 159904

Excess (deficiency) of revenue over expenses 1654320 (241530) - - (1) 1412789 1867

Transfer for capital purchases (40350) - - - - (40350) (28097)

Repayment of long-term debt principal (276371) - - - - (276371) (216064)

Net assets (deficiency) beginning of year (1362001) (5523555) - - - (6885556) (6643262)

Net assets (deficiency) end of year $ (24402) $ (5765085) $ - $ - $ (1) $ (5789488) $ (6885556)

1616

KPMG LLP Telephone (705) 675-8500 Chartered Accountants Fax (705) 675-7586 Claridge Executive Centre In Watts (1-800) 461-3551 144 Pine Street PO Box 700 Internet wwwkpmgca Sudbury ON P3E 4R6

INDEPENDENT AUDITORS REPORT

To the Board of Directors of The Childrens Aid Society of the Districts of Sudbury and Manitoulin

We have audited the accompanying financial statements of The Childrens Aid Society of the Districts of Sudbury and Manitoulin which comprise the statements of financial position as at March 31 2014 March 31 2013 and April 1 2012 the statements of operations changes in net assets (deficiency) cash flows and the statements of remeasurement gains and losses for the years ended March 31 2014 and March 31 2013 and notes comprising a summary of significant accounting policies and other explanatory information

Managementrsquos Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in

accordance with Canadian public sector accounting standards and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement whether due to fraud or error

Auditorsrsquo Responsibility

Our responsibility is to express an opinion on these financial statements based on our audits We conducted our audits in accordance with Canadian generally accepted auditing standards Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement

An audit involves performing procedures to obtain audit evidence about the amounts and disclosure in the financial statements The procedures selected depend on our judgment including the assessment of the risks of material misstatement of the financial statements whether due to fraud or error In making those risk assessments we consider internal control relevant to the entityrsquos preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances but not for the purpose of expressing an opinion on the effectiveness of the entityrsquos internal control An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management as well as evaluating the overall presentation of the financial statements

We believe that the audit evidence we have obtained in our audits is sufficient and appropriate to provide a basis for our audit opinion

Opinion

In our opinion the financial statements present fairly in all material respects the financial position of The Childrens Aid Society of the Districts of Sudbury and Manitoulin as at March 31 2014 March 31 2013 and April 1 2012 and its results of operations its changes in net assets (deficiency) its cash flows and the remeasurement gains and losses for the years ended March 31 2014 and March 31 2013 in accordance with Canadian public sector accounting standards

KPMG LLP is a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (ldquoKPMG Internationalrdquo) a Swiss entity KPMG Canada provides services to KPMG LLP

Other Matters

Our audit was made for the purpose of forming an opinion on the basic financial statements taken as a whole The supplementary information included in the Schedule is presented for purposes of additional analysis and is not a required part of the basic financial statements Such information has been subjected to the auditing procedures applied in the audit of the financial statements and in our opinion is fairly stated in all material respects in relation to the basic financial statements taken as a whole

Emphasis of Matter

Without qualifying our opinion we draw attention to Note 13 in the financial statements which indicates that The Childrens Aid Society of the Districts of Sudbury and Manitoulin has experienced accumulated operating losses This may cast doubt about The Childrens Aid Society of the Districts of Sudbury and Manitoulinrsquos ability to continue as a going concern

Chartered Professional Accountants Licensed Public Accountants

June 10 2014

Sudbury Canada

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Statements of Financial Position

March 31 2014 March 31 2013 and April 1 2012

March 31 March 31 April 1

2014 2013 2012

Assets

Current assets Cash $ 2883252 1173655 1642401 Accounts receivable

Due from the Ministry of Children and Youth Services 214793 515071 358142 Other 221874 184863 198110

Prepaid expenses 216590 199116 173901

3536509 2072705 2372554

Capital assets (note 3) 4980929 5231292 5503390

$ 8517438 7303997 7875944

Liabilities and Net Assets (Deficiency)

Current liabilities Accounts payable and accrued liabilities (note 6) $ 3153287 2903964 3134981 Vacation payable 558233 570376 552008 Health spending account 79378 270000 260000 Deferred revenue - Ontario Child Benefit Equivalent 407625 530742 673257 Current portion of long-term debt (note 5) 219443 228175 216064

4417966 4503257 4836310

Employee future benefits (note 4) 5127474 4683179 4395570 Long-term debt (note 5) 3794911 4080048 4308223 Interest rate swaps (note 5) 599060 817284 807174

13939411 14083768 14347277

Net assets (deficiency) Unrestricted

Operating (24403) (1362001) (1435684) Employee related (5765085) (5523555) (5207578) Interest rate swaps (807174) (807174) (807174)

Capital (note 7) 966575 923069 979103

(5630087) (6769661) (6471333)

Accumulated remeasurement gains and losses 208114 (10110) -

(5421973) (6779771) (6471333) Commitments (note 8) Contingencies (note 9) Future operations (note 13)

$ 8517438 7303997 7875944

See accompanying notes to financial statements

1

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Statements of Operations

Years ended March 31 2014 and March 31 2013

2014 2013 Operating Capital Total Total (Schedule)

Revenue Ministry of Children and Youth Services

- Child Welfare Operating $ 37129680 - 37129680 37635554 - Ontario Child Benefit Equivalent 559947 - 559947 550263 - Other 104825 - 104825 104825

Childrens special allowance 1391890 - 1391890 1372000 Maintenance from other societies 309400 - 309400 240030 Childrens pensionbenefits 2979 - 2979 7894 Maintenance from parents 1150 - 1150 4072 Interest 31029 - 31029 20242 Rental income 245355 - 245355 217598 Recoveries 386418 - 386418 420693 Gain on debt retirement - 17499 17499 -Other 18492 - 18492 33012

40181165 17499 40198664 40606183

Expenses Wages 14747159 - 14747159 15009750 Benefits 4209724 - 4209724 4012471 Travel 1790964 - 1790964 1824012 Training and recruitment 104713 - 104713 100171 Building occupancy 898223 - 898223 796775 Amortization - 290714 290714 300195 Interest on long-term debt 218585 - 218585 234482 Purchased services - non-case related 270976 - 270976 166505 Purchased services - case related 819082 - 819082 1039468 Boarding rates 13356922 - 13356922 13844683 Client personal needs 1999109 - 1999109 1923564 Medical and related services 735668 - 735668 746514 Promotion and publicity 18324 - 18324 18612 Office 390501 - 390501 452360 Technology 227999 - 227999 307260 Miscellaneous 312645 - 312645 287593

40100594 290714 40391308 41064415

Excess (deficiency) of revenue over expenses before undernoted 80571 (273215) (192644) (458232)

Provincial subsidy for funding of prior years deficit 1332218 - 1332218 159904

Excess (deficiency) of revenue over expenses $ 1412789 (273215) 1139574 (298328)

See accompanying notes to financial statements

2

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Statements of Changes in Net Assets (Deficiency)

Years ended March 31 2014 and March 31 2013

Operating

March 31 2014

Unrestricted

Employee Interest Total related Rate Swaps Unrestricted Capital Total

Net assets beginning of year

Excess (deficiency) of revenue over expenses

Net change in investment in capital assets

$ (1362001)

1654319

(316721)

(5523555)

(241530)

-

(807174)

-

-

(7692730)

1412789

(316721)

923069

(273215)

316721

(6769661)

1139574

-

Net assets end of the year $ (24403) (5765085) (807174) (6596662) 966575 (5630087)

Operating

March 31 2013

Unrestricted

Employee Interest Total related Rate Swaps Unrestricted Capital Total

Net assets

April 1 2012 (note 2a)) $ (1435684) (5207578) (807174) (7450436) 979103 (6471333)

Excess (deficiency) of revenue over expenses

Net change in investment in capital assets

317844

(244161)

(315977)

-

-

-

1867

(244161)

(300195)

244161

(298328)

-

Net assets end of the year $ (1362001) (5523555) (807174) (7692730) 923069 (6769661)

See accompanying notes to financial statements

3

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Statements of Cash Flows

Years ended March 31 2014 and March 31 2013

2014 2013

Cash flows from operating activities Excess (deficiency) of revenue over expenses Adjustment for

Amortization of capital assets Provision for employment-related obligations Gain on debt retirement

Change in non-cash working capital Decrease (increase) in due from the Ministry of Children and Youth Services Decrease (increase) in accounts receivable - other Increase in prepaid expenses Increase (decrease) in accounts payable

and accrued liabilities Increase (decrease) in vacation payable Increase (decrease) in health spending account Decrease in deferred revenue - Ontario Child Benefit Equivalent

$ 1139574

290714 444295 (17499)

1857084

300278 (37011) (17474)

249323 (12143)

(190622)

(123117)

2026318

$ (298328)

300195 287609

-

289476

(156929) 13247

(25215)

(231017) 18368 10000

(142515)

(224585)

Cash flows from financing activities Principal repayments on long-term debt (276371) (216064)

Cash flows from capital activities Capital asset additions (40350) (28097)

Net increase (decrease) in cash 1709597 (468746)

Cash beginning of year 1173655 1642401

Cash end of year $ 2883252 $ 1173655

See accompanying notes to financial statements

4

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Statements of Remeasurement Gains and Losses

Years ended March 31 2014 and March 31 2013

March 31 2014 Total

Accumulated remeasurement losses April 1 2013

Unrealized gains attributable to Derivative - interest rate swap

Accumulated remeasurement gains March 31 2014

$

$

(10110)

218224

208114

March 31 2013 Total

Accumulated remeasurement gains and losses April 1 2012

Unrealized losses attributable to Derivative - interest rate swap

Accumulated remeasurement losses March 31 2013

$

$

-

(10110)

(10110)

See accompanying notes to financial statements

5

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements

Years ended March 31 2014 and March 31 2013

The Childrens Aid Society of the Districts of Sudbury and Manitoulin (the Society) provides child protection services in the territorial districts of Sudbury and Manitoulin It is incorporated without share capital under the Laws of Ontario and is registered as a tax-exempt charitable organization under the Federal Income Tax Act

On April 1 2013 the Society adopted Canadian Public Sector Accounting Standards The Society has also elected to apply the 4200 standards for government not-for-profit organizations These are the first financial statements prepared in accordance with these public sector accounting standards

In accordance with the transitional provisions in Canadian Public Sector Accounting Standards the Society has adopted the changes retrospectively subject to certain exemptions allowed under these standards The transition date is April 1 2012 and all comparative information provided has been presented by applying public sector accounting standards

A summary of transitional adjustments recorded to net assets (deficiency) and excess (deficiency) of revenue over expenses is provided in note 2

1 Significant accounting policies

(a) Revenue recognition

The Society accounts for contributions which include donations and government grants under the deferral method of accounting as follows

Operating grants are recorded as revenue in the period to which they relate

Grants and donations relating to future periods are deferred and recognized in the subsequent period when the related activity occurs

Grants approved but not received are accrued

Unrestricted contributions are recognized as revenue when received or receivable if the amounts can be reasonably estimated and collection is reasonably assured

Externally restricted contributions are recognized as revenue in the period in which the related expenses are recognized

Contributions restricted for the purchase of capital assets are deferred and amortized into revenue at rates corresponding to those of the related capital assets

6

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

1 Significant accounting policies (continued)

(b) Capital assets

Capital assets are recorded at cost Amortization of capital assets is recorded as follows

Asset Basis Period

Buildings Straight-line 30 years Furniture and equipment Straight-line 10 years Computer equipment Straight-line 3 years

(c) Employee future benefits

Vacation entitlements and banked overtime are accrued for as entitlements are earned

The health spending account reflects the provision for the annual discretionary employee health spending of up to $1000 annually

The Society accrues its obligations for post-employment benefit plans as the employees render the services necessary to earn the benefits The actuarial determination of the accrued benefit obligation uses the projected benefit method prorated on service (which incorporates managementrsquos best estimate of future salary levels other cost escalation retirement ages of employees and other actuarial factors) Under this method the benefit costs are recognized over the expected average service life of the employee group

Actuarial gains and losses on the accrued benefit obligation arise from differences between actual and expected experience and from changes in the actuarial assumptions used to determine the accrued benefit obligation The Society elected to recognize these on transition The most recent actuarial valuation of the sick leave plan and the benefit plan was as of April 1 2012

For the post-employment benefits (continuation of life medical and dental during LTD) these benefits are accounted for on a terminal basis in comparison to the non-pension post-retirement benefit which is accounted for on an accrual basis This means that the liability for the post-employment benefit is accrued only when a LTD claim occurs For these benefits the full change in the liability is being recognized immediately as an expense in the year

Substantially all of the employees of the Society are eligible to be members of the Ontario Municipal Employeesrsquo Retirement Fund (ldquoOMERSrdquo) which is a multi-employer defined benefit final average earnings and contributory pension plan Defined contribution plan accounting is applied to OMERS as the Society has insufficient information to apply defined benefit accounting (note 10)

7

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

1 Significant accounting policies (continued)

(d) Use of estimates

The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting periods Items subject to such estimates are valuation of capital assets and employee future benefits Actual results could differ from those estimates These estimates are reviewed periodically and as adjustments become necessary they are reported in earnings in the year in which they become known

(e) Financial instruments

All financial instruments are initially recorded on the statement of financial position at fair value

All investments held in equity instruments that trade in an active market would be recorded at fair value Management has elected to record investments at fair value as they are managed and evaluated on a fair value basis

Unrealized changes in fair value would be recognized in the statement of remeasurement gains and losses until they are realized when they would be transferred to the statement of operations

Transaction costs incurred on the acquisition of financial instruments measured subsequently at fair value are expensed as incurred

Where a decline in fair value is determined to be other than temporary the amount of the loss

is removed from accumulated remeasurement gains and losses and recognized in the statement of operations On sale the amount held in accumulated remeasurement gains and losses associated with that instrument is removed from net assets and recognized in the

statement of operations

8

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

1 Significant accounting policies (continued)

(e) Financial instruments (continued)

Financial instruments are classified into fair value hierarchy Levels 1 2 or 3 for the purposes of describing the basis of the inputs used to determine the fair market value of those amounts recorded a fair value as described below

Level 1 Fair value measurements are those derived from quoted prices (unadjusted) in active markets for identical assets or liabilities

Level 2 Fair value measurements are those derived market-based inputs other

than quoted prices that are observable for the asset or liability either directly or indirectly

Level 3 Fair value measurements are those derived from valuation techniques

that include inputs for the asset or liability that are not based on observable market data

The Society has selected to account for transactions at the trade date

2 Transitional adjustments

(a) Net assets

The following table summarizes the impact of the transition to Canadian Public Sector

Accounting Standards on the Societys net assets as of April 1 2012

Net assets As previously reported under financial reporting

provisions of the Ministry of Children and Youth Services March 31 2012 $ (456581)

Transition election to recognize employee future benefits (4395570) Adjustment to record vacation and banked overtime (552008) Adjustment to record health spending provision (260000) Adjustment to reflect the fair value of the interest rate swap (807174)

Restated April 1 2012 $ (6471333)

9

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

2 Transitional adjustments (continued)

(a) Net assets (continued)

In accordance with transitional provisions of Canadian Public Sector Accounting Standards the Society has elected to use the following exemption for employee future benefits

(i) Amortization of actuarial gainslosses

The Society has elected to recognize actuarial gains and losses at the date of transition to Public Sector Accounting Standards directly in net assets As a result the Society has recognized an increased liability and a charge to net assets

(ii) Discount rate used to calculate employee future benefits

Canadian Public Sector Accounting Standards requires these liabilities to be calculated with a discount rate that is equal to either the Societyrsquos rate of borrowing or the rate of return on the plan assets The Society has chosen to discount these liabilities using its internal rate of borrowing

(b) Statement of operations

As a result of the above-noted elections and the retrospective application of Canadian Public Sector Accounting Standards the Society recorded the following adjustments to excess (deficiency) of revenue over expenses for the year ended March 31 2013

As previously reported under financial reporting provisions of the Ministry of Children and Youth Services

Change in employee future benefit expense Change in vacation and banked overtime Change in health spending account

$ (142255) (287609) (18368) (10000)

Restated for the year ended March 31 2013 $ (458232)

10

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

3 Capital assets

March 31 2014 Cost AccumulatedAmortization

Net book value

Land Buildings Furniture and equipment Computer equipment

$ 675000 54099621045628

167153

$ 7297743

ndash 1315264

879772 121778

2316814

675000 4094698

165856 45375

4980929

March 31 2013 Cost AccumulatedAmortization

Net book value

Land Buildings Furniture and equipment Computer equipment

$ 675000 5409962 1017503

250971

$ 7353436

ndash 1122290

835712 164142

2122144

675000 4287672

181791 86829

5231292

April 1 2012 Cost AccumulatedAmortization

Net book value

Land Buildings Furniture and equipment Computer equipment Leasehold improvements

$ 675000 5409962 1017503

339738 238255

$ 7680458

ndash 929316 791458 218039 238255

2177068

675000 4480646

226045 121699

ndash

5503390

11

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

4 Employee future benefits

The Society maintains defined benefit and defined contribution plans providing other retirement and employee future benefits to most of its employees

The costs of other post-employment benefits (including medical benefits dental care life insurance and certain compensated absences) related to the employeesrsquo current service is charged to income annually The cost is computed on an actuarial basis using the projected benefit method estimating the usage frequency and cost of services covered and managementrsquos best estimates of investment yields salary escalation and other factors Plan assets are valued at fair value for purposes of calculating the expected return on plan assets

The fair values of plan assets and accrued benefit obligations were determined by independent actuaries on behalf of the Society as at April 1 2012

The accrued benefit obligations accrued at March 31 2014 amounted to $5127474 (March 31 2013 - $4683179 April 1 2012 - $4395570) The benefits paid out in the year were $53866 (March 31 2013 - $55280)

The discount rate used is 43 (March 31 2013 ndash 4) Health care costs are presumed to increase at 8 commencing the first year and grading to 4 in 2022

5 Long-term debt

March 31 March 31 April 1 2014 2013 2012

CIBC debt due April 2 2027 $ 4014354 4222616 4420270 Unsecured promissory note payable with interest

at 80 due December 20 2016 ndash 85607 104017 4014354 4308223 4524287

Current portion of long-term debt (219443) (228175) (216064)

$ 3794911 4080048 4308223

Interest rate swaps $ 599060 817284 807174

12

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

5 Long-term debt (continued)

The CIBC debt due April 2 2027 is secured by a first fixed charge on the land and building to which it relates The debt was advanced under a variable rate credit facility with interest adjusted monthly To reduce the interest rate cash flow risk on this debt the Society has entered into an interest rate swap contract that entitles the Society to receive interest at floating rates on the notional principal amount and obliges it to pay interest at a fixed rate of 524 over the entire term of the debt The fair value of the interest rate swap has been determined using Level 3 of the fair value hierarchy The net interest receivable or payable under the contract is settled monthly with the CIBC which is a Canadian chartered bank

The Ministry of Children and Youth Services has approved the use of operating funds for the purpose of mortgage repayments To protect their interest on the land and building the Ministry has entered into a Mortgage Funding Agreement with the Society The Agreement which has been registered with the Lands Registration Office gives the Ministry rights on the use and disposition of the property

The unsecured promissory note was obtained to finance leasehold improvements

Principal due within each of the next five years on the long-term debt is as follows

2015 $ 219442 2016 231221 2017 243633 2018 256710 2019 270489

6 Accounts payable and accrued liabilities

Included in accounts payable and accrued liabilities are government remittances payable of $18693 (March 31 2013 - $32859 April 1 2012 - $32051) which includes amounts payable for HST and payroll related taxes

13

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

7 Capital

The equity in capital assets is calculated as follows

March 31 March 31 April 1 2014 2013 2012

Capital assets $ 4980929 5231292 5503390

Less Long-term debt (4014354) (4308223) (4524287)

$ 966575 923069 979103

8 Commitments

The rental obligations for leased property in Little Current and Chapleau are as follows

2015 $ 120676 2016 45029 2017 45029 2018 45029 2019 45029 2020 45029 2021 3752

9 Contingencies

The Society is involved in certain legal matters and litigation the outcome of which is not presently determinable The loss if any from these contingencies will be accounted for in the periods in which the matters are resolved Management is of the opinion these matters are mitigated by adequate insurance coverage

10 Pension agreement

The Society makes contributions to OMERS which is a multi-employer plan on behalf of certain members of its staff The plan is a defined benefit plan which specifies the amount of the retirement benefit to be received by the employees based on the length of service and rates of pay

The amount contributed to OMERS for 2014 was $1467897 (March 31 2013 - $1370016) for current service

14

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

11 Financial risks

(a) Credit and market risk

The Society has no significant exposure to credit or market risks

(b) Liquidity risk

Liquidity risk is that the Society will be unable to fulfill its obligations on a timely basis or at a reasonable cost The Society manages its liquidity risk by monitoring its operating requirements The Society prepares budget and cash forecasts to ensure it has sufficient funds to fulfill its obligations

(c) Interest rate risk

Interest rate risk is the potential for financial loss caused by fluctuations in fair value or future cash flows of financial instruments because of changes in market interest rates

The Society is exposed to this risk through its interest bearing investments bank loans and term debt

The Society mitigates interest rate risk on its term debt through derivative financial instrument (interest rate swaps) that exchanges the variable rate inherent in the term debt for a fixed rate (see note 5) Therefore fluctuations in market interest rates would not impact future cash flows and operations relating to the term debt

There have been no significant changes from the previous year in the exposure to risk or policies procedures and methods used to measure the risk

12 Public Sector Disclosure Act

For the calendar year ended December 31 2013 the Society is in compliance with the Public Sector Disclosure Act 1996 and the Public Sector Salary Disclosure Amendment Act 2004

13 Future operations

These financial statements have been prepared on the going concern basis notwithstanding the effect of accumulated operating losses The Societyrsquos ability to realize its assets and discharge its liabilities in the normal course of business is dependent upon the continued support of its funding Ministry and its creditors which is anticipated by Management

15

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Schedule of Operations by Program

Years ended March 31 2014 and March 31 2013

Ontario Child Employment Benefit Targeted Total Total

Child Welfare Related Equivalent Subsidies Independence 2014 2013

Revenue Ministry of Children and Youth Services

- Child Welfare Operating $ 37077430 $ - $ - $ 52250 $ - $ 37129680 $ 37635554 - Ontario Child Benefit Equivalent - - 559947 - - 559947 550263 - Other - - - - 104825 104825 104825

Childrens special allowance 1391890 - - - - 1391890 1372000 Maintenance from other societies 309400 - - - - 309400 240030 Childrens pensionbenefits 2979 - - - - 2979 7894 Maintenance from parents 1150 - - - - 1150 4072 Interest 31029 - - - - 31029 20242 Rental income 245355 - - - - 245355 217598 Recoveries 386418 - - - - 386418 420693 Other 18492 - - - - 18492 33012

39464143 - 559947 52250 104825 40181165 40606183

Expenses Wages 14676272 (12143) - - 83030 14747159 15009750 Benefits 3934255 253673 - - 21796 4209724 4012471 Travel 1790964 - - - - 1790964 1824012 Training and recruitment 104713 - - - - 104713 100171 Building occupancy 898223 - - - - 898223 796775 Interest on long-term debt 218585 - - - - 218585 234482 Purchased Services - non-case related 270976 - - - - 270976 166505 Purchased Services - case related 819082 - - - - 819082 1039468 Boarding rates 13356922 - - - - 13356922 13844683 Client personal needs 1386912 - 559947 52250 - 1999109 1923564 Medical and related services 735668 - - - - 735668 746514 Promotion and publicityPromotion and publicity 18 32418324 - - - - 18 32418324 18 61218612 Office 390501 - - - - 390501 452360 Technology 227999 - - - - 227999 307260 Miscellaneous 312645 - - - - 312645 287593

39142041 241530 559947 52250 104826 40100594 40764220

Excess (deficiency) of revenue over expenses before undernoted items 322102 (241530) - - (1) 80571 (158037)

Provincial subsidy for funding of prior years deficit 1332218 - - - - 1332218 159904

Excess (deficiency) of revenue over expenses 1654320 (241530) - - (1) 1412789 1867

Transfer for capital purchases (40350) - - - - (40350) (28097)

Repayment of long-term debt principal (276371) - - - - (276371) (216064)

Net assets (deficiency) beginning of year (1362001) (5523555) - - - (6885556) (6643262)

Net assets (deficiency) end of year $ (24402) $ (5765085) $ - $ - $ (1) $ (5789488) $ (6885556)

1616

Other Matters

Our audit was made for the purpose of forming an opinion on the basic financial statements taken as a whole The supplementary information included in the Schedule is presented for purposes of additional analysis and is not a required part of the basic financial statements Such information has been subjected to the auditing procedures applied in the audit of the financial statements and in our opinion is fairly stated in all material respects in relation to the basic financial statements taken as a whole

Emphasis of Matter

Without qualifying our opinion we draw attention to Note 13 in the financial statements which indicates that The Childrens Aid Society of the Districts of Sudbury and Manitoulin has experienced accumulated operating losses This may cast doubt about The Childrens Aid Society of the Districts of Sudbury and Manitoulinrsquos ability to continue as a going concern

Chartered Professional Accountants Licensed Public Accountants

June 10 2014

Sudbury Canada

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Statements of Financial Position

March 31 2014 March 31 2013 and April 1 2012

March 31 March 31 April 1

2014 2013 2012

Assets

Current assets Cash $ 2883252 1173655 1642401 Accounts receivable

Due from the Ministry of Children and Youth Services 214793 515071 358142 Other 221874 184863 198110

Prepaid expenses 216590 199116 173901

3536509 2072705 2372554

Capital assets (note 3) 4980929 5231292 5503390

$ 8517438 7303997 7875944

Liabilities and Net Assets (Deficiency)

Current liabilities Accounts payable and accrued liabilities (note 6) $ 3153287 2903964 3134981 Vacation payable 558233 570376 552008 Health spending account 79378 270000 260000 Deferred revenue - Ontario Child Benefit Equivalent 407625 530742 673257 Current portion of long-term debt (note 5) 219443 228175 216064

4417966 4503257 4836310

Employee future benefits (note 4) 5127474 4683179 4395570 Long-term debt (note 5) 3794911 4080048 4308223 Interest rate swaps (note 5) 599060 817284 807174

13939411 14083768 14347277

Net assets (deficiency) Unrestricted

Operating (24403) (1362001) (1435684) Employee related (5765085) (5523555) (5207578) Interest rate swaps (807174) (807174) (807174)

Capital (note 7) 966575 923069 979103

(5630087) (6769661) (6471333)

Accumulated remeasurement gains and losses 208114 (10110) -

(5421973) (6779771) (6471333) Commitments (note 8) Contingencies (note 9) Future operations (note 13)

$ 8517438 7303997 7875944

See accompanying notes to financial statements

1

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Statements of Operations

Years ended March 31 2014 and March 31 2013

2014 2013 Operating Capital Total Total (Schedule)

Revenue Ministry of Children and Youth Services

- Child Welfare Operating $ 37129680 - 37129680 37635554 - Ontario Child Benefit Equivalent 559947 - 559947 550263 - Other 104825 - 104825 104825

Childrens special allowance 1391890 - 1391890 1372000 Maintenance from other societies 309400 - 309400 240030 Childrens pensionbenefits 2979 - 2979 7894 Maintenance from parents 1150 - 1150 4072 Interest 31029 - 31029 20242 Rental income 245355 - 245355 217598 Recoveries 386418 - 386418 420693 Gain on debt retirement - 17499 17499 -Other 18492 - 18492 33012

40181165 17499 40198664 40606183

Expenses Wages 14747159 - 14747159 15009750 Benefits 4209724 - 4209724 4012471 Travel 1790964 - 1790964 1824012 Training and recruitment 104713 - 104713 100171 Building occupancy 898223 - 898223 796775 Amortization - 290714 290714 300195 Interest on long-term debt 218585 - 218585 234482 Purchased services - non-case related 270976 - 270976 166505 Purchased services - case related 819082 - 819082 1039468 Boarding rates 13356922 - 13356922 13844683 Client personal needs 1999109 - 1999109 1923564 Medical and related services 735668 - 735668 746514 Promotion and publicity 18324 - 18324 18612 Office 390501 - 390501 452360 Technology 227999 - 227999 307260 Miscellaneous 312645 - 312645 287593

40100594 290714 40391308 41064415

Excess (deficiency) of revenue over expenses before undernoted 80571 (273215) (192644) (458232)

Provincial subsidy for funding of prior years deficit 1332218 - 1332218 159904

Excess (deficiency) of revenue over expenses $ 1412789 (273215) 1139574 (298328)

See accompanying notes to financial statements

2

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Statements of Changes in Net Assets (Deficiency)

Years ended March 31 2014 and March 31 2013

Operating

March 31 2014

Unrestricted

Employee Interest Total related Rate Swaps Unrestricted Capital Total

Net assets beginning of year

Excess (deficiency) of revenue over expenses

Net change in investment in capital assets

$ (1362001)

1654319

(316721)

(5523555)

(241530)

-

(807174)

-

-

(7692730)

1412789

(316721)

923069

(273215)

316721

(6769661)

1139574

-

Net assets end of the year $ (24403) (5765085) (807174) (6596662) 966575 (5630087)

Operating

March 31 2013

Unrestricted

Employee Interest Total related Rate Swaps Unrestricted Capital Total

Net assets

April 1 2012 (note 2a)) $ (1435684) (5207578) (807174) (7450436) 979103 (6471333)

Excess (deficiency) of revenue over expenses

Net change in investment in capital assets

317844

(244161)

(315977)

-

-

-

1867

(244161)

(300195)

244161

(298328)

-

Net assets end of the year $ (1362001) (5523555) (807174) (7692730) 923069 (6769661)

See accompanying notes to financial statements

3

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Statements of Cash Flows

Years ended March 31 2014 and March 31 2013

2014 2013

Cash flows from operating activities Excess (deficiency) of revenue over expenses Adjustment for

Amortization of capital assets Provision for employment-related obligations Gain on debt retirement

Change in non-cash working capital Decrease (increase) in due from the Ministry of Children and Youth Services Decrease (increase) in accounts receivable - other Increase in prepaid expenses Increase (decrease) in accounts payable

and accrued liabilities Increase (decrease) in vacation payable Increase (decrease) in health spending account Decrease in deferred revenue - Ontario Child Benefit Equivalent

$ 1139574

290714 444295 (17499)

1857084

300278 (37011) (17474)

249323 (12143)

(190622)

(123117)

2026318

$ (298328)

300195 287609

-

289476

(156929) 13247

(25215)

(231017) 18368 10000

(142515)

(224585)

Cash flows from financing activities Principal repayments on long-term debt (276371) (216064)

Cash flows from capital activities Capital asset additions (40350) (28097)

Net increase (decrease) in cash 1709597 (468746)

Cash beginning of year 1173655 1642401

Cash end of year $ 2883252 $ 1173655

See accompanying notes to financial statements

4

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Statements of Remeasurement Gains and Losses

Years ended March 31 2014 and March 31 2013

March 31 2014 Total

Accumulated remeasurement losses April 1 2013

Unrealized gains attributable to Derivative - interest rate swap

Accumulated remeasurement gains March 31 2014

$

$

(10110)

218224

208114

March 31 2013 Total

Accumulated remeasurement gains and losses April 1 2012

Unrealized losses attributable to Derivative - interest rate swap

Accumulated remeasurement losses March 31 2013

$

$

-

(10110)

(10110)

See accompanying notes to financial statements

5

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements

Years ended March 31 2014 and March 31 2013

The Childrens Aid Society of the Districts of Sudbury and Manitoulin (the Society) provides child protection services in the territorial districts of Sudbury and Manitoulin It is incorporated without share capital under the Laws of Ontario and is registered as a tax-exempt charitable organization under the Federal Income Tax Act

On April 1 2013 the Society adopted Canadian Public Sector Accounting Standards The Society has also elected to apply the 4200 standards for government not-for-profit organizations These are the first financial statements prepared in accordance with these public sector accounting standards

In accordance with the transitional provisions in Canadian Public Sector Accounting Standards the Society has adopted the changes retrospectively subject to certain exemptions allowed under these standards The transition date is April 1 2012 and all comparative information provided has been presented by applying public sector accounting standards

A summary of transitional adjustments recorded to net assets (deficiency) and excess (deficiency) of revenue over expenses is provided in note 2

1 Significant accounting policies

(a) Revenue recognition

The Society accounts for contributions which include donations and government grants under the deferral method of accounting as follows

Operating grants are recorded as revenue in the period to which they relate

Grants and donations relating to future periods are deferred and recognized in the subsequent period when the related activity occurs

Grants approved but not received are accrued

Unrestricted contributions are recognized as revenue when received or receivable if the amounts can be reasonably estimated and collection is reasonably assured

Externally restricted contributions are recognized as revenue in the period in which the related expenses are recognized

Contributions restricted for the purchase of capital assets are deferred and amortized into revenue at rates corresponding to those of the related capital assets

6

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

1 Significant accounting policies (continued)

(b) Capital assets

Capital assets are recorded at cost Amortization of capital assets is recorded as follows

Asset Basis Period

Buildings Straight-line 30 years Furniture and equipment Straight-line 10 years Computer equipment Straight-line 3 years

(c) Employee future benefits

Vacation entitlements and banked overtime are accrued for as entitlements are earned

The health spending account reflects the provision for the annual discretionary employee health spending of up to $1000 annually

The Society accrues its obligations for post-employment benefit plans as the employees render the services necessary to earn the benefits The actuarial determination of the accrued benefit obligation uses the projected benefit method prorated on service (which incorporates managementrsquos best estimate of future salary levels other cost escalation retirement ages of employees and other actuarial factors) Under this method the benefit costs are recognized over the expected average service life of the employee group

Actuarial gains and losses on the accrued benefit obligation arise from differences between actual and expected experience and from changes in the actuarial assumptions used to determine the accrued benefit obligation The Society elected to recognize these on transition The most recent actuarial valuation of the sick leave plan and the benefit plan was as of April 1 2012

For the post-employment benefits (continuation of life medical and dental during LTD) these benefits are accounted for on a terminal basis in comparison to the non-pension post-retirement benefit which is accounted for on an accrual basis This means that the liability for the post-employment benefit is accrued only when a LTD claim occurs For these benefits the full change in the liability is being recognized immediately as an expense in the year

Substantially all of the employees of the Society are eligible to be members of the Ontario Municipal Employeesrsquo Retirement Fund (ldquoOMERSrdquo) which is a multi-employer defined benefit final average earnings and contributory pension plan Defined contribution plan accounting is applied to OMERS as the Society has insufficient information to apply defined benefit accounting (note 10)

7

THE CHILDRENS AID SOCIETY OF THE DISTRICTS OF SUDBURY AND MANITOULIN

Notes to Financial Statements (continued)

Years ended March 31 2014 and March 31 2013

1 Significant accounting policies (continued)

(d) Use of estimates

The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting periods Items subject to such estimates are valuation of capital assets and employee future benefits Actual results could differ from those estimates These estimates are reviewed periodically and as adjustments become necessary they are reported in earnings in the year in which they become known

(e) Financial instruments

All financial instruments are initially recorded on the statement of financial position at fair value