financially speaking.. a student’s guide to understanding what financial institutions are talking...

TRANSCRIPT

Financially Speaking..A Student’s Guide to Understanding what

Financial Institutions are Talking About

Renting VS Buying a Home

What’s the difference?

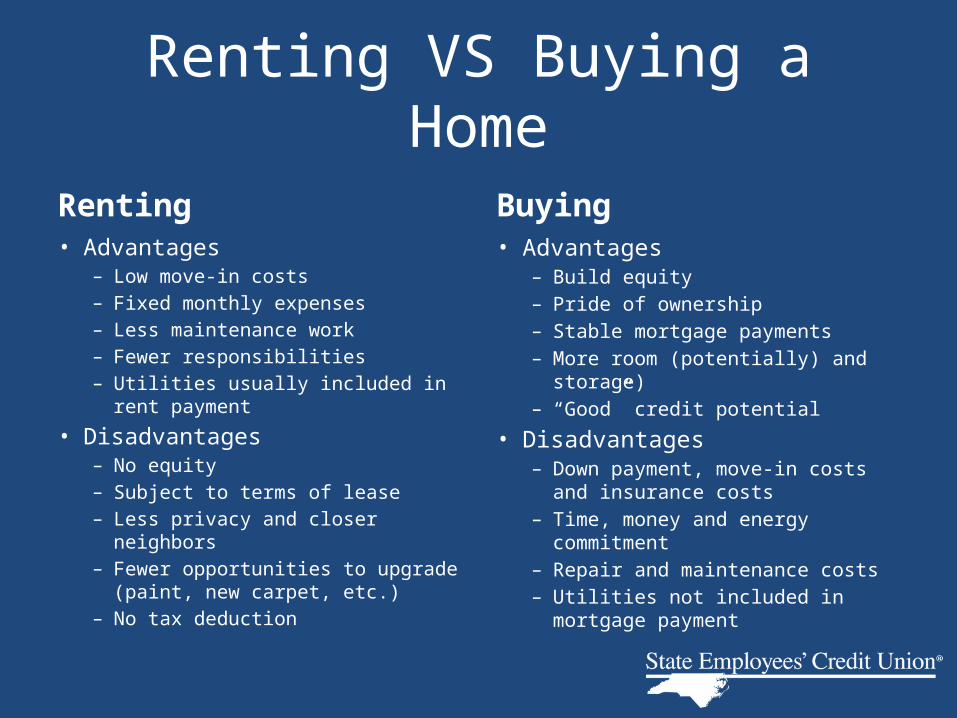

Renting VS Buying a Home

Renting • Advantages

– Low move-in costs– Fixed monthly expenses– Less maintenance work– Fewer responsibilities – Utilities usually included in rent

payment

• Disadvantages– No equity– Subject to terms of lease– Less privacy and closer neighbors – Fewer opportunities to upgrade

(paint, new carpet, etc.)– No tax deduction

Buying• Advantages

– Build equity – Pride of ownership– Stable mortgage payments– More room (potentially) and storage)– “Good” credit potential

• Disadvantages– Down payment, move-in costs and

insurance costs– Time, money and energy

commitment – Repair and maintenance costs– Utilities not included in mortgage

payment

What does a lender look for?

• Ability to repay• Credit• Down payment• Job Stability

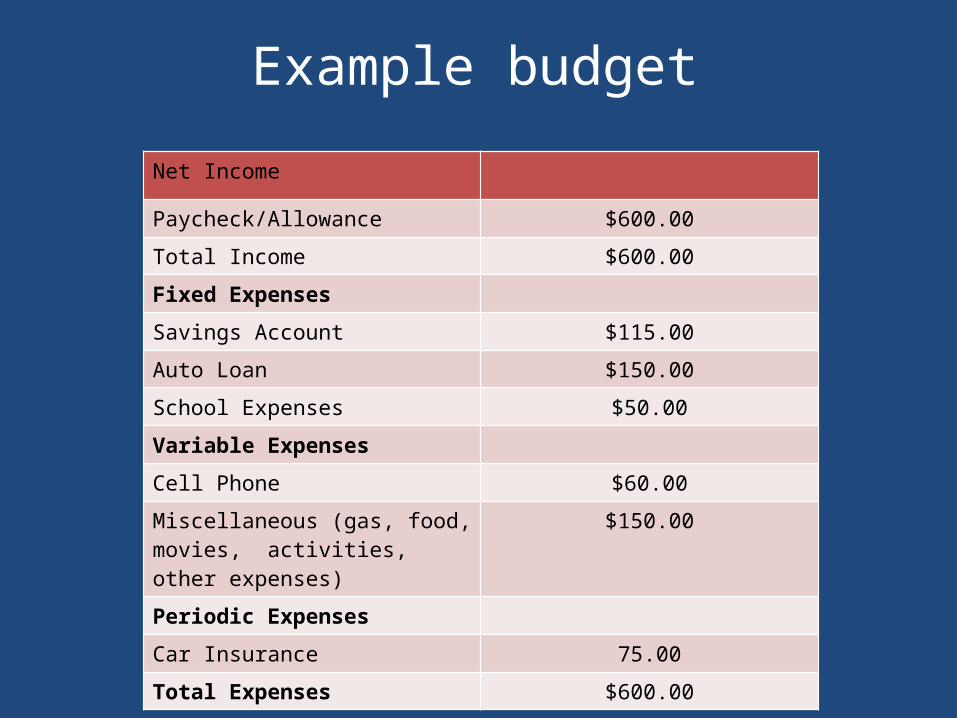

Can you Repay the Loan?

• Lenders and landlords want you to be able to afford a payment.

• In order to allot for a large payment such as housing, you have to know how to budget.

Example budget

Net Income

Paycheck/Allowance $600.00

Total Income $600.00

Fixed Expenses

Savings Account $115.00

Auto Loan $150.00

School Expenses $50.00

Variable Expenses

Cell Phone $60.00

Miscellaneous (gas, food, movies, activities, other expenses)

$150.00

Periodic Expenses

Car Insurance 75.00

Total Expenses $600.00

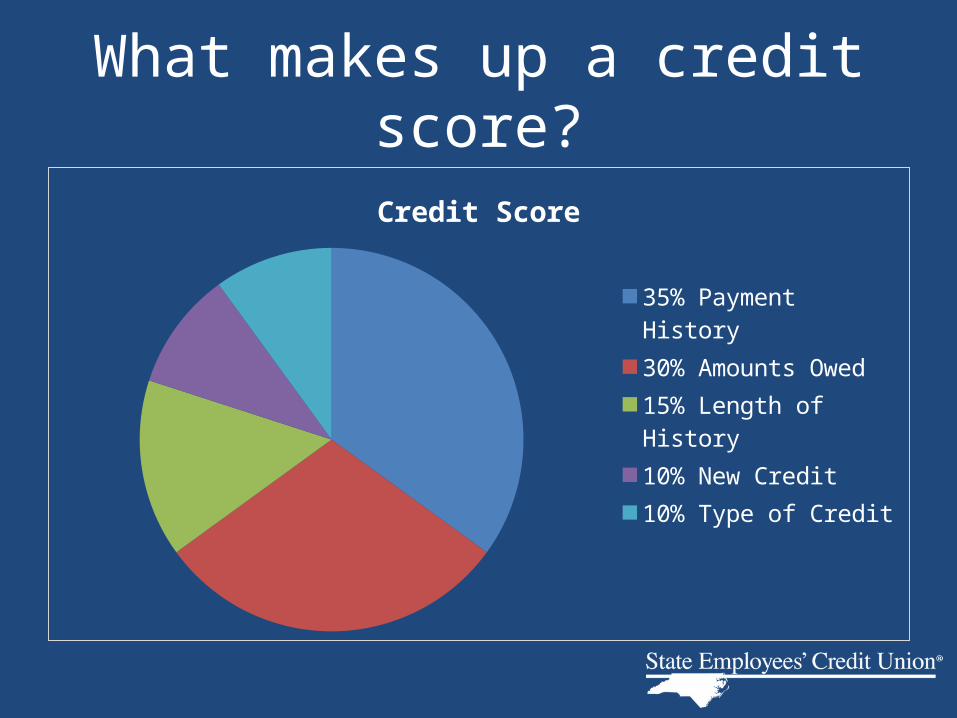

What makes up a credit score?

Credit Score

35% Payment History30% Amounts Owed15% Length of History10% New Credit10% Type of Credit

www.annualcreditreport.com

• Be your own credit manager

• A consumer can get a free credit report from each of the 3 credit bureaus (Equifax, Experian, and Transunion) once a year

• Allows a pro-active approach to monitoring, credit repair, and fraud prevention

Down Payment

• Shows lender your investment in your home• Could take a while to save up for• A larger down payment will help lower your

rate and loan fees• Builds instant equity

Will you have Job Stability?

• Job stability really means income stability.• Longevity with your job shows a steady

income that can support your living expenses.

Lending Terms

• Equity

• Closing

• Discount Points

Lending Terms

• Earnest money• Interest Rate• APR• Escrow• Loan origination fee• Private mortgage insurance (PMI)

Mortgage Payments

• Amount Borrowed

• Interest Rate

• Term

Mortgage Payment Example

Amount Borrowed $120,000

Interest Rate 5%

Monthly Payment $645

Term 30 years

Financing Your Home

• Select your loan type, options include: – Fixed-Rate loan– Adjustable-Rate loan– The Department of Veterans Affairs loan (VA loan)– The Federal Housing Administration loan (FHA

loan)

Fixed Rate Loan

• Interest rate remains the same for a specific term

• Standard 15 and 30 year terms, but different terms are available

Adjustable Rate Loan

• Interest rate can change at a predetermined interval

• Generally lower beginning rates

• Payments may increase or decrease during the life of the loan

The Process

• Pre-Qualification vs. Pre-Approval• Finding a Home (Sales Contract)• Mortgage Application &

Disclosures • Inspections• Closing

Now What?

• Establish a savings account. • Know the difference between saving and

investing. • Work to understand credit cards before you

sign up for one.

This has been a financial institution point of view..

But don’t take our word for it!Contact your financial institution and

find out for yourself!

Stay in the driver seat of your finances and don’t let anyone else take the wheel!

Questions?