financing michigan's sustainable agriculture

TRANSCRIPT

FinancingMichigan’sSustainableAgriculture:TheAvailabilityandAccessibilityofCapitalforBeginningFarmers

SusanCocciarelliCSMottGroupforSustainableFoodSystemsatMichiganStateUniversity

December2009

AcknowledgementsAspecialthankyoutoKatieBrandt,GroundswellFarms;PattyCantrell,MichiganLandUseInstitute;andDorothySuput,CarrotProject;fortheirinsightandsupportindevelopingtheRecommendationsportionofthepaper.AndtoKathrynColasanti,DavidConner,LauraGoddeeris,MikeHamm,andSusanSmalley,CSMottGroupforSustainableFoodSystemsatMichiganStateUniversity,forfeedbackandeditingsupport.

TABLEOFCONTENTS

EXECUTIVESUMMARY 4

BACKGROUND 6

ExpandingMichigan’sAgricultureEconomy 6ShrinkingFarmland 6AgingFarmers 7GrowingDemand 8Michigan’sMarketShare 8BeginningFarmers 9AgriculturalProfitability 11TheRoleofCapital 12

CapitalAvailabilityandAccessibilityforBeginningFarmers:MichiganSurveyProject 13CapitalAvailability 13CapitalAccessibility 15LoweringRiskThroughPartnershipsandSupplementaryPrograms 18

Summary 21

ComparingLenderRequirementsandBeginningFarmerAttributes 21Table1 22

FindingsofInstitutionalSupportForBeginningFarmers 23

LimitationsWithinMichigan’sFinancialServicesSector 24

Recommendations 25

REFERENCES 28

APPENDIX 31Surveyrespondents 31Otherfinancialinstitutions 31

MapofRespondents 31

4

ExecutiveSummaryInitiatingafarmenterpriseisoftenanextremelydifficultundertaking,particularlyforfirstgenerationfarmers.Thosewhowishtooperateasmalltomid‐size,diversifiedfarmthatmarketsproductsdirectlytothesurroundingcommunityratherthanalarge,commodityfarmfaceevengreaterchallengesontwolevels:

1. Ourresourceinfrastructureisdesignedtoundergirdourglobalcommoditymarketagriculturalsystem,andthereforerelegatesmallerscalefarmingtoastatusof“niche”or“unconventional”,or“non‐commercial”.

2. Thestatusoffarmoperationsandassetrequirements(includinglandandfinancialcollateral)maypositionthefarmerashighriskbasedonlendingcriteriastructuredaroundlargerscaleagri‐business.

Inarecentstudyofbeginningfarmers,AhearnandNewtonconcludedthatbeginningfarmsareofrecognizedimportancetoagriculturalproductivitygrowthandlandconservationgoalsfortheUnitedStates.1Limitedresearchandanecdotalstudiestellusthatcapitalaccesstailoredtothestartupanddevelopmentoffarmersinsustainableorecologicallyfriendlyfarming,agrowingsectoracrossthecountry,isinadequate.2ThefocusofthispaperistoexploretheextenttowhichprivateandothersourcesofcapitalareavailableinMichigantosupportbeginningfarmers.ThepaperalsooffersrecommendationsthatbuilduponopportunitiesandaddressimpedimentstogrowcapitalinvestmentsinMichigansmallerscale,diversifiedagriculture.

Michigan’seconomyisfacinghugechallenges,withmanufacturingindecline.Agriculture,oneofitsimportantindustries,isgrowing.AccordingtoareportfromMichiganStateUniversity’sProductCenterforAgricultureandNaturalResources,Michiganagricultureexperienceda12percentgrowthin2007,withayearlyeconomicimpactestimatedtobe$71.3billion,anincreaseof$7.6billionfromthe$63.7estimatein2006.3However,Michiganfacesthechallengeofkeepingfarmersinfarmingandshapingafoodsystemthatworksforfarmersandconsumerswhilebolsteringlocalandregionaleconomies.Theagingoffarmersbegsthequestionaboutwhowillfarminthefuture.AstheaverageageofMichiganfarmerscontinuestoincrease–currentlyat56.4years,‐entry‐levelfarmersareneededtoreplacethem.Only5.2%ofMichiganfarmersareundertheageof35.

5

Michiganfarmlandisshrinkingandthecostoffarmablelandisrising;theaveragepriceperfarmlandacrewasnearly60percenthigherin2001thanfiveyearsearlieranddoublethepriceofadecadeearlier.4

WiththedemandfororganicandlocalsourcesoffreshproductincreasinginMichigan,connectingnewerfarmersdirectlywithMichiganmarketsmayhelpmeetthisgrowingdemandforlocallyandsustainablygrownfoodsandstimulateMichigan’sailingeconomy.Inordertoaddresstherolethatcapitalcouldplayinassistingthegrowthofviable,smallerscale,diversifiedfarmoperationsinMichigan,theCSMottGroupforSustainableFoodSystemsatMichiganStateUniversity(MottGroup)surveyedfourteenMichiganfinancialinstitutions,loanfunds,andpublicentitiestogatherinformationabouttherespondents’lendingactivityaswellastheirfamiliarityandengagementwithbeginningfarmers.WefoundthatthereisfinancialcapitalavailableinMichigan,butitsaccessibilitybyfarmersisbasedonseveralvariables:institutionalrepaymentcriteria,lenders’knowledgeaboutsmallerscalesustainablefarming,whetherornotagricultureisanorganizationalpriority,theextenttowhichfinancialinstitutionsmarkettheirproductstopotentialclientele,andgeographicallocation.Anominalnumberoffinancialinstitutions(4of14)wereabletodescribebeginningfarmersbeyondtheUSDAdescription,butsuchfarmersrepresentaverysmallportionoftheiroveralllendingportfolio.Despitethefactthatthemajorityoffinancialinstitutionsrequireadown‐paymentorcollateraltogetanoperationalloan,onlyoneoffersasset‐buildingtoolstoincreasenetworth.

Recommendationsincludeexpandingassetbuildingtoolstobuildnetworthofpromisingbeginningfarmenterprises,clarifyingthelinkbetweenproductionagricultureandeconomicdevelopmentwithinthefinancialservicesindustry,developingstrategiclinkagesbetweenbeginningfarmersandsourcesofcapitalinvestment,andexploringnewvisionsforcapitaldeploymenttoscaleupMichigan’sfoodproduction.

6

BackgroundThefuturehealthandvitalityofagriculture,thefoodsystem,andbothurbanandruralcommunitiesdependsonthesuccessfulentryofallwhowanttopursueafarminglivelihood.Athirdofallfarmlandownersareofretirementage,andoverthenexttwodecadesanestimated400millionacresofU.S.agriculturallandwillbepassedontoheirsorsold.Whileagrowingnumberofyoungpeopleandnewimmigrantswanttoenterfarming,theyfaceamyriadofchallengessuchastherisingcostoffarmland,acriticalshortageoftraining,andlackoffinancing.5Theissueofanewgenerationoffarmershastakencentralstageinthediscussionofnewfarmpoliciesbecause“newfarmersbringskillsetstocomplementandenhancetraditionalmanagementandproductiontechnologies”.6

Toenterfarmingwithouttheexpectationofinheritingland,aspiringfarmersmayhavetobepostponefarminguntiltheyaccumulatesignificantresourcestoacquirenecessaryfarmassets,aprocessthatcantakeyears.7Butbecausethefarmsectordependsonalengthybiologicalprocessthatgeneratesconsiderablephysicalandfinancialrisk,theurgencytofinanceexistsduringthisgestationorstartupperiod.8Financialcapitalhashistoricallybeendifficulttocomebyinthefarmsector,especiallyforbeginningfarmers.

Governmentprogramsdesignedtoencouragebeginningfarmerstoenteragricultureandenhancetheirchancesofsurvivingasviablefarmoperatorshaveemergedfromthe2008FarmBill.Thefocusofthispaper,however,isthequestionofwhetherornotprivateandpublicsourcesofcapitalareavailabletosupportwhathasbeencitednationallyas“theurgentneedtogeneratenew,commerciallyorientedfarmers.”9

ExpandingMichigan’sAgricultureEconomy

SHRINKINGFARMLANDFarmablelandintheU.S.hassteadilydecreasedsince1949,shrinkingby8.4%between1949and2002.10The2007U.S.CensusofAgriculturereportedadeclineinUSfarmlandacresfrom938.3millionin2002to922.1millionin2007,alossof1.7percent.11Michiganisexperiencingbothfarmlandshrinkageandaffordabilityissues.ThetotalnumberofMichiganfarmsdeclinedby2/3between1950and200712andtheAmericanFarmlandtrusthasrankedMichigan9thinthecountryformostthreatenedprimefarmlandduetosprawl.13 TheUSDAreportedinits"AgriculturalLandValuesandCashRents"thatMichigan'sfarmablelandpricesincreased

“Weneedanewgenerationoffarmers.Thisisahugeissue.Whowillgrowourfoodinthefuture?Thisisurgent!ThetimeisNOW!”

JanieHippUSDA

7

morethan7.2percentduring2008toanaveragepriceof$3,700peracre.AccordingtoUSDAstatistics,thelasttimefarmlandvaluesinMichiganexperiencedayear‐to‐yeardeclinewasJanuary1987.14TheFederalReserveBankofChicagoreportedthatMichiganlandpricesincreased13percentfromOct.1,2007,toOct.1,2008.Allofthispointstoaseverelackofaffordablelandfornewfarms,andasituationinwhichaccesstostart‐upcapitalisbecomingmorecritical.

AGINGFARMERSTheagingoftheU.S.farmerpopulationhasledtoconcernaboutashortageofbeginningfarmers.TheaverageageofU.S.farmoperatorsincreasedfrom55.3in2002to57.1in2007.Thenumberofoperators75yearsandoldergrewby20percentfrom2002,whilethenumberofoperatorsunder25yearsofagedecreased30percent.15InMichigan,thefarmerprofileisbringshomethisurgency:only5.2%ofMichiganfarmersareunderage35,andtheaverageageoftheMichiganfarmersis56.4.Whilebeginningfarmsaremorelikelythanestablishedfarmstobesmallinscaleandoperatedbyyoungeroperators,beginningfarmersarenotnecessarilyyoungfarmers.Beginningfarmersenteragricultureatallages,notjustyoungages.Approximatelyathirdofbeginningfarmersnationallyare55yearsorolder.16Thismeansthatunlesssignificantnumbersofnewpeopleenterfarming,wewillcontinuetofaceadwindlingpopulationoffarmersandwillriskgreaterrelianceonimportedfoods.

Theavailabilityoftrainingisaparallelissue.Manyofthepeoplewhowishtooperateafarmbusinesstodaylackafarmingbackgroundandexperience.ThelackofacomprehensivetrainingprogramfornewfarmerspresentsasignificantbarriertoentryinMichigan.Existingtrainingopportunitiesarescatteredanduncoordinated.Nosingleprogramcoversallcoreproductionandbusinessmanagementcompetenciesalongwithinfrastructuresupporttoassistwithland,capitalandmarketaccess.Yet,thereareindicationsthatagrowingnumberofpeopleareinterestedinorganicand/orsustainablefarminginMichigan.AccordingtoCoriePearce,traininginstructorattheMichiganStateUniversityStudentOrganicFarm(MSUSOF),theone‐yearOrganicCertificateProgram’senrollmenthasincreasedsteadilyoveritsthreeyearsofexistenceandhasawaitinglistfor2010.17Ahugeissue,accordingtoMSUSOFleadinstructor,JeremyMoghtader,iswhetherornotpeoplecompletingtheprogramcanbeginfarmingwithoutaccesstoflexiblecapitaltoobtainland.18

8

GROWINGDEMANDBothWisconsinandIllinoishavecapitalizedongrowingdemandfordifferentiatedagriculturalproductsbypassinglegislationthat plans for expanding and supporting their states’ local and organic food system while overcoming obstacles to increase local and organic food production.19

Sincethelate1990s,U.S.organicproductionhasmorethandoubled,buttheconsumermarkethasgrownevenfaster.Nationally,organicfoodsaleshavemorethanquintupled,increasingfrom$3.6billionin1997to$18.9billionin2007.Morethantwo‐thirdsofU.S.consumersbuyorganicproductsatleastoccasionally,and28percentweekly,accordingtotheOrganicTradeAssociation.Theorganicindustryhasgrownby17to21percenteachyearsince1997,whileoveralldomesticfoodsalesgrewbyonly2to4percentduringthesameperiod.Industryanalystspredictthattheorganicmarketwillcontinuetogrowatarapidpace.Thisfast‐pacedgrowthhasledtoinputandproductshortagesinorganicsupplychains.20

ThereareseveralindicationsthatMichigan’sconsumerdemandformorelocalandorganicallygrownfoodisgrowing.Increasingprevalenceoffarmersmarkets,roadsidestands,pickyourownoperationsandcommunitysupportedagriculturesubscriptionprogramssuggeststhatlocallysourcedfoodisnopassingfad.ThenumberofMichiganfarmersmarketstripledfrom2000to2008.21Michigannowhas85CommunitySupportedAgriculture(CSA)operations,22andcertifiedorganictillableacresincreasedby166%between1997and2005.23BecauseMichigancurrentlyhasonly205organicfarms,ofwhich88%operateonlessthan170acres,thereispotentialtocaptureagreatershareoftheorganicmarket.24

MICHIGAN’SMARKETSHAREMichiganagricultureispoisedforopportunitywithincreasedinterestinlocallygrownfood,growingenthusiasmforfarmmarkets,higher‐valuenicheproducts,opportunitiestobuildprocessingplantsforMichigan‐grownproducts,newfarmingtechnologiesandnewpossibilitiesforseasonextension.25

MSUresearchersestimatethatjust43%ofthefoodswholesaledandretailedinMichiganaregrowninMichigan(Ferris).WithextimatedtotalMichiganretailfoodsalesat$11.602billion,the$6.613billionnon‐Michiganfoodproductssoldrepresentpotentialmarketsformanyfarmersandfoodbusinesses(Petersonetal).

9

A2008statewidestudydemonstratedthepotentialforagriculturetodriveeconomicgrowthinMichigan.AteamofMichiganStateUniversityresearchersledbyDavidConnermeasuredtheeconomicimpactofmeetingFoodGuidePyramidrequirementsforfreshfruitsandvegetables.Theymodeledtheimpactofthefollowingscenario:stateresidentsincreaseconsumptionofallfruitsandvegetablestomeettheguidelinesand,wheninseason,theincreasedconsumptionofthoseitemsabletobegrowninMichiganissourcedfromMichiganfarmers.Thischangewouldresultinaprojectednetincreaseof1,780jobsand$211millioninnewincome.26

ArecentjointreportbytheMichiganLandUseInstitutetheW.E.UpjohnInstituteforEmploymentResearch,andC.S.MottGroupforSustainableFoodSystemsatMSUfurtherrevealsthemarketopportunitiesintransitioningtogrowingandsellingmorefreshvegetablesandfruits:

• Currently74percentofMichiganfruitsand44percentofitsvegetablesaresoldatrelativelylowpricesasingredientsforcanned,frozen,dried,andotherprocessedproducts.

• Thestudy’sprojectionsforupto1,889jobsand$187millioninnew,personalincomecouldwarrantastateeconomicdevelopmentinvestmentofatleast$9.5milliontowardmarketingMichiganfoodsandhelpingfarmsandrelatedbusinessessupplymorefreshmarkets.27

Thestudyassumestwonecessarymarketconditions:theelasticityofdemandforfreshordirectmarketfruits,andvegetables,andthechangeinthelevelofconsumerdemandforfreshordirectmarketfruitsandvegetables.Assumingthattherewouldbesomechangesinpriceandthatthosechangesmightaffectthequantityofproduceconsumerdemand,andthatMichiganwouldmarketMichigan‐grownproduce,themagnitudeofmissingmarketshareinfreshproductrevealsthatnewfarmerscouldhaveamajoreconomicimpactinMichigan.

BEGINNINGFARMERSTheUSDAdefinesbeginningfarmersandranchersasthosewhohaveoperatedafarmorranchfor10yearsorlessaseitherasoleoperatororwithotherswhohavealsooperatedafarmorranchfor10yearsorless.EstablishedbeginningfarmerandrancherprogramshavedifferentiatedbeyondtheUSDAdefinition,determiningthatunderstandingnewerfarmersisthefoundationofeffectiveprogramdesign.28

10

In2001,theNortheastGrowingNewFarmerConsortium(GNF)proposedatypologyofnewfarmersthatwouldenableserviceprovisiontocommerciallyorientedagriculturalproduction.29Thetermnewfarmerencompassesthe“universe”ofpeoplewhoareconsideringbecomingfarmersandthose“beginningfarmers”whohaveactuallybeenfarmingfor10yearsorless.GNFdefinedsix"types"ofnewfarmers.ThesesixGNFfarmertypesaredistinguishedbytheircurrentengagementwith,andcommitmentto,farming.Beginningfarmersintheirfirstthreeyearsofstartupoperationsarestilldiscoveringwhattheyneed,requiringdifferentservicesthanthoseenhancingtheirfarmsaftersixtosevenyearsofoperation.RecognizingstageoffarmoperationsenablesGNFtomoreadequatelyaddresstheneedsoftheirclientsandtoacknowledgetheexperiencegainedduringtheinitialyearsoffarming.30

TheGNFtypologyillustratesdeliberateeffortsbybeginningfarmerprogramstofocusoneducational,experiential,andresourceacquisitiontohelpfarmerstakeadvantageoftherisingconsumerdemandfordirectmarketingofsustainablyproducedfarmproductlocallyandregionally.31GNFdescribesbeginningfarmersashavingacquiredfarmingknowledge,skills,andmanagementexpertise,butbecausemanyarefirstgenerationfarmerslackinglandaccessandthecapitalneededforstartup.

AMottGroupcasestudyoffourMichiganbeginningfarmersrevealedsimilaritiestothedescriptionoftheGNFfarmers.TheseMichiganfarmers,havingcompletedacomprehensivebeginningfarmerprograminsouthwestMichiganandnowenteringtheirfourthyearoffarming,arefirstgeneration,havecollegeeducations,managetheirownfarms,cutcostsbydoingalltheirownlabor,rentedlandbeforeowning,andaretakingadvantageoflocalboomingmarketsforfreshgrownfood.Theyworkedonothers’farms,savedmoney,piecedtogethercapitalfromavarietyofsources,workedofffarm,receivedcontractsupfronttogrowfoodforothers,andinvestedanyprofitintotheirfarmratherthanpaythemselvesthefirsttwoyears.Noneappliedforconventionalfinancing,anticipatingthattheywerenon‐bankable.Twoofthefouranticipate100%oftheirpersonalincomewillcomefromtheircommunitysupportedagriculture(CSA)operationswithinfouryearsofoperationbyaccessingup‐frontconsumerandinstitutionalcontracts.Twotookoverotherfarmers’successfuloperationsandnowderivehalftheirfamilyincomefromthefarm.ThesefarmersrepresentagrowingnumberoffarmersinMichiganwhohavenotreceivedconventionalfinancing.32

11

AGRICULTURALPROFITABILITYThedebateaboutwhetherornotsmallerscaleagricultureisprofitableinfluencesrisk‐aversefinancingforfarmoperations.Incommodityfarming,thepredominantwisdomisthatthelargerthescaleofoperation,themoreprofitablebecausetheytypicallycompeteonthebasisofpriceandgreatersizeoftenmeansgreaterefficiency.

However,entryratesforsmallfarmbusinessesaresignificantlygreaterthanforotherfarmsizes.Manyofthenewerfarmstart‐upshavechosentocompeteonthebasisofcustomerbenefitsbymarketingadifferentiatedproductsuchaslocalororganic.Withthismarketstrategy,productpriceisafactorbutnottheoverridingfactorandkeepingthebusinesssmallmaybecriticaltosuccess.Enteringfarmersmakesignificantcontributionstoagricultureproduction,accountingforashareoffarmsalesgenerallyhigherthanthatreportedforbeginningmanufacturingindustries.33

Commercialbanksfinance41%ofallfarmdebt(2000),and43%ofallsmallfarmdebt.TheFarmCreditSystemprovides25%offarmcreditnationally.34TheComptrolleroftheCurrencyregulatesagriculturelendingbybanks.TheComptrollerissuestheComptrollerHandbookonthefundamentalsofagriculturalloanunderwritingandadministration,andprovidesguidanceforexaminingthoseactivitiesinnationalbanks.TheHandbook’sAgriculturalLoanClassificationsectionindicatesthattherearenomandatoryrulestodirectexaminersonhowtotreatagriculturalcredit.However,thehandbookdescribesproductioncreditas“perhapsthemostvolatileformofagriculturallending”.35Itisuptotheindividualbanktoestablishareasonableprocesstoanalyzeprojectedcashflow.Closecooperationbetweenlendersandfarmersissuggested.

Thedistinctdifferencebetweensmallandmid‐scalefarming,basedonproductdifferentiationandcommodityfarmingmayposeaninformationandcommunicationgapamongMichiganlenders.Lenderswhorelyoncommodityfarmingmetricstounderwritesmallandmid‐scaleagriculturecreditriskmaybeclosingthedooronfarmmodelsthatarealreadyaddressingfinancialriskmanagement.Suchwerethefindingsina2003studyconductedbytheMinnesotaLandStewardshipProgram.Resultssuggestthatlendersthinkfarmbusinessplansareoftenpoorlywrittenwithlittlesubstantiatingdatatodetermineprofitability.Newerfarmers(0‐3yearsofoperation)havereportedthatlendersarenotconvincedabouttheprofitmarginpotentialonfarmsoperatingonlessthan5acres.AsurveyconductedbytheMinnesotaLandStewardshipProjectof567lenders,agriculturaleducators,andfarmersinWisconsinandMinnesotarevealed

12

that89%ofthefarmersthoughtsustainablefarmingwasequallyormoreprofitablethanconventionalfarming,whileonly35%ofthelendersinthestudythoughtthiswastrue.36AquotebyanOregoncountycommissioneratadebatesponsoredbythelocalFarmBureaureflectstheperspectiveofmanylendinginstitutions:“Tothinkthatsomeoneisgoingtomakealivingonfiveacresisridiculous.That’snotafarm.”37

THEROLEOFCAPITALFarmincomecannotbeignoredasakeyfactorindeterminingthesuccessofthenextgenerationoffarmersandranchers.38Theforemostreasonwhysofewfarmersareyoungisthatstartupcostsinagriculturepresentsabarriertoentry.39Farmingcommonlyrequirescontroloverlandandcapital.Landaccessandtransferprogramsconnectingfarmownerswithnewfarmersareemerging.Yetfinancinglandisamajorchallenge,andbeginningfarmerswithlimitedcollateralhavedifficultyfindingcreditforlandacquisition,equipmentoroperations.

Thegrowthofinnovativeprogramstoaddresscapitalaccesshasemergednationally.TheCarrotProject(TCP)wasestablishedafteramulti‐state,700+farmersurveydeterminedthedifferentfinancialcapitalneedsofgrowersbasedontypeandstageofoperation,accountingforregionaldifferences.TCP’sapproachistofinancefarmersunabletoaccessmoretraditionallendingsourcesbyprovidingsmallloansandtoimproveaccesstofinancialresources.40TheIowaBeginningFarmerTaxCredit,ataxprogramthatprovidesanincentivetocurrentandretiredfarmerswhorentagriculturalassetstoabeginningfarmerwasinitiatedin2007bytheIowaStateUniversityBeginningFarmerCenterandapprovedduringthe2006Iowalegislativesession.Theprogram,administeredbytheIowaAgriculturalDevelopmentAuthority,makestaxcreditsrangingfromfiveto15%availabletoanyeligibleIowataxpayerwhotransfersassetstoa"beginning"farmer.FarmtransferprogramssuchasCaliforniaFarmLinkandtheVermontFarmlinkserveasanintermediarysteptoapplyingforconventionalfinancingbyofferingfarmbusinessplandevelopmentandsmall,initial,operationalloans.41

“Someoftheseyoungpeopledoafantasticjob

ofbeingrealistic.Theyaresharppeople.Theyarenotplanningonstrugglingfor40yearswithnothingtoshowforit.Theyarea

goodinvestmentinthemselvesandforourbankoverthenextfewyears.Andyouknow,I

haven’tlostanickelin11yearsoflendingtostart

upfarmerswhoarerealistic(canproduce

realisticcashflowprojections).”

SmallBankAgricultureLoanOfficer

13

CapitalAvailabilityandAccessibilityforBeginningFarmers:MichiganSurveyProjectInJuly2009,wesurveyedfourteenMichiganfinancialinstitutions,loanfunds,andpublicentities.SignificantagriculturelendinginstitutionsacrossMichiganwereidentified,includingMichiganbanks,creditunions,communitydevelopmentloanfunds,stateagencies,federalandfarmcreditservicesentities.Thesurveytoolcomprisedtwenty‐fivequestionsdesignedtogatherqualitativeandquantitativeinformationabouttherespondents’lendingactivityaswellastheirfamiliarityandengagementwithbeginningfarmers.

Followingthesurvey,interviewsbypersonalvisitsand/ortelephoneconversationswereconductedwithchieflendingofficersrepresentingacrosssectionofconventionalandcommunity‐basedfinancialinstitutionsacrossMichigan.Fromthisseriesof14interviews,wecompiledandanalyzedsurveyresultstoaddressfinancialproductavailabilityandaccessibility(seeappendixforcompletedocumentation).Followingarethemostsalientfindingsfromtheinterviews.

CAPITALAVAILABILITYCapitalavailabilityreferstofinancialproductsofferedspecificallytostart‐upandbeginningfarmers.Keyquestionswereaskedtodeterminebothproductavailabilityandmarketimpetusbehindthesefinancialproducts.ThefollowingsummarizestheresponsesthatbestilluminatethestateoffinancialcapitalavailabilityinMichigan.

1. Mostfinancialinstitutions’conceptsofbeginningfarmersdon’tgobeyondtheUSDAdefinition.

ThemajorityofrespondentsusedtheUSDAdefinitionofbeginningfarmerstodescribethismarketsector.However,someloanofficersinsmallbanksandCEO’sofsmallcreditunionsprovidedaddeddescriptorsbasedonsomeofthenewfarmerstowhomloansweregiven.Thesedescriptorsincluded:collegeeducated,determined,smallerscale,firstgeneration,havevisionandplans,understandrisks,anddirectdeliveryofagricultureproducttothecustomer.

Themajorityoftherespondentsalsodescribedtheirawarenessofamore“localized”foodsystemwhentalkingaboutbeginningfarmers.Respondentsusedsuchdescriptorsforthislocalizedfoodsystemas:newfarmers’markets,urbangardens,CommunitySupported

14

Agriculture(CSA),grocerystoresadvertisinglocalproduce.Nevertheless,knowledgeofsomechangesinagriculturewasbasedmoreonobservationratherthanfirst‐handexperiencelendingtothesenewfarmers.Inotherwords,theknowledgeoflocalfoodwasnotnecessarilyrelatedtothenumberofnewfarmersservedbythemajorityofinstitutions.

2. Beginningfarmerloansdonotrepresentasignificantportionoflendingactivityamongthemajorityoffinancialinstitutions

ExceptfortheFarmServiceAgencyandGreenstoneFarmCreditServiceswhosemissionandregulatoryresponsibilitiesarespecificallywithinagriculture,themajorityoffinancialinstitutionsstatedthatbeginningfarmersarenotanorganizationalpriority.However,inpractice,somesmallbanks,oneloanfundmanager,andbothcreditunionsstatedthattheydidnotdiscriminatebasedonbusinessenterprisetype.Rather,theirpriorityistoworkwithbeginningfarmersonacase‐by‐casebasis.Havingsaidthat,loanstobeginningfarmersrepresentedlessthan5%ofthefinanciallendingportfolioforallfinancialinstitutionrespondentsexceptforGreenStoneFarmCreditServiceandMichiganFarmServiceAgency.BothGreenstoneFarmCreditServiceandtheMichiganFarmServiceAgencyhavemandatestoservicebeginningfarmers.GreenstoneCredithasimplementedaboardapprovedYoung,BeginningandSmallFarmandRanchers(YBS)lendingprogramcomprisedofseparatecomponentsforYBSfarmers.Morerelaxedunderwritingstandardsandloantermshavebeenapprovedforfarmoperatingloans,farmequipmentandintermediatetermloans,andforrealestateloans42.TheMichiganFarmServiceAgencyhasCongressionaltargetsseteachyear.AccordingtotheFarmServiceAgency,thedemandforoperationalloansamongbeginningfarmerswas50%higherin2009thanitwasforthesame6‐monthtimeperiodin2008.

3. Amorelocalizedfoodsystemdoesnottriggeragriculturallendingactivity

Togetinsightaboutinstitutionalplanningtoservenewmarkets,respondentswereaskedabouttheextenttowhichtheylinkedlocalfoodsystemactivitywiththepotentialfornewcustomers.Thoselendinginstitutionsfamiliarwithmorelocalizedfoodsystemsdescribedthefoodsysteminthecontextofproductionmethods(organic,sustainable,highervaluediversifiedproduct),andbymorelocalizedmarkets(farmersmarkets,CommunitySupportedAgriculture,institutionalandrestaurantmarkets).Stateagenciesrespondedthatalthoughthey

15

recognizesuchactivityinotherstates,orsomewhatgenericallyas“thelocalfoodmovement”citedinprint,theyhaven’tdeterminedthatitisagrowingtrendinMichigan.Reasonsgivenwerelackofevidenceoftrueincomegeneration/jobcreation,andthelackoflegislativemandatestoservethissector.

Forthemostpart,thesmallertheinstitution,themoreinclusivetheirdescriptionofobservedfoodsystemactivityatthelocallevel;banksandcreditunionscoulddescribehowtheyareworkingwithindividualbeginningfarmersbasedontheindividuallendingofficers’historyofdirectexperiencewiththissector.Onecreditunionhasdirectexperiencebecauseofapartnershipwithalocalbeginningfarmerprogram.However,themajorityoflendersacknowledgedthattheyareawareoftheincreaseinlocalfoodactivity,citingactivitybyproduct,marketfocus(morelocalanddirect),andsizeoffarmoperations(lessthantenacres).However,theselenderspointedoutthattheirawarenesswasnotnecessarilycausedbyanincreaseddemandforloansfrombeginningfarmersintheirregion.

4. Smallerfinancialinstitutionsarebetterabletotailortheirproducts

WiththeexceptionofFSAandGreenstoneCredit,whichisgovernedbystatute,allinstitutionsrespondedthatnewproductdevelopmentrespondstocustomerneed,thoughcustomersmustbeabletodemonstraterepaymentofanyloanorlineofcredit.Smallbanksandcreditunionsweremostabletotailorproducts,includingsmallamountsofinitialloans,ifbeginningornewfarmerswereabletodemonstrateapositivecashflow.Bothcreditunionsandthecommunitydevelopmentloanfundmanagerstatedthattheybaseproductsonwhatmembersorcustomerspresenttothemasafinancialneedforstartup;however,bothwerequicktopointoutthattheytailorproductsonacasebycasebasis,andthatreturnoninvestmentforboththeclientandtheinstitutionisessential.

CAPITALACCESSIBILITYCapitalaccessibilityreferstotheuser‐friendlinessoreaseofuseoffinancialproductsavailabletonewandbeginningfarmers.Inordertounderstandtheeaseofuse,weaskedquestionsrelatedtotheassessmentofrisk,aswellastheextenttowhichfinancialinstitutionsreachedouttopotentialcustomers.ResponsestothefollowingfoursubjectareasprovidethemostinsightaboutfinancialcapitalaccessibilityamongMichiganfinancialinstitutions.

16

1. Determiningriskassessmentvarieswithfinancialinstitutionalsize,regulatoryresponsibilities,andinternalpolicies

Allinstitutionsdeterminerepaymentcapacitythrougheitherhistoricaland/orprojectedcashflowforstartupfarmers.Thedegreeofspecificityvariesbasedoninstitutionallendingpractices.GovernmentregulationsinfluencebothFSAandGreenStoneFarmCreditServicessuchthattheyareformulaicintheircalculationsofriskwhichinfluencestheextenttowhichtheycanprovideloanstobeginningfarmersthathaveneitherstartupcapitalnorequityintheirfarmbusiness.GreenStoneFarmCreditServices,thelargestlendertobeginningfarmersinMichigan,lendingover$1billion(2008)inMichiganand11Wisconsincounties,utilizesdifferentunderwritingstandardsforbeginningthanforestablishedfarmers.GreenStoneCreditrequiresthatbeginningfarmerapplicantsdemonstrate25%equityintheirbusiness,whichishalfofthestandard50%equitypositionrequiredforfarmbusinessesthatfalloutsidetheUSDAbeginningfarmerdefinition.

Somesmallerbanksservingasmallergeographicarea,creditunions,andloanfundsareabletocalculaterepaymentusingbothcurrentandprojectedcashflowandoff‐farmincome.

Whatdistinguishesthesmallerfinancialinstitutionsfromthelargeragriculturelendersisthemindsetaboutrisk.Thesmallerinstitutionallendersemphasizedthattheycanprovidepersonalizedfinancialservicestohelpbuildthecapacityofafarmerwhopresentspotentiallyviablestart‐uporenhancementplans.Personalizedservicesincludedtailoredfinancialproducts,flexiblepaymentschedules,creditrepair,easeofapplicationprocess,andsometechnicalassistanceinfinancialstatementdevelopment.Althoughlaborintensive,suchpersonalizedservicesultimatelylessenedfinancialrisktotheinstitution.

Agriculture‐basedlendinginstitutionsdidnotseemtohavethesameflexibility;therefore,proofofrepaymentwasparamounttoinstitutionalfinancialprotection.Smallloansmaybethebreadandbutterofsmallerinstitutions,butservicingthosesmallloansisthoughttobealossleaderbylargerfinancialinstitutions.StatedaformeragriculturelendingofficerofasmallerbankinsouthernMichiganthathadrecentlymergedwithalargerbank,“wearenolongerdoingsmallfarmloans.Smallerloansarenotworthanything.Thebankisonlyprovidingsmallerloanstoexistingcustomers.”Accordingtothislendingofficer,hisbank,locatedinacountythatfarms3.5%ofMichigan’stotalfarmacreage,nolongerseesagriculturelendingintheirfuture.

17

2. Thechiefobstacletoextendingfarmcreditcitedbyfinancialinstitutionsistherelatingofcurrentorprojectedcashflowbyfarmoperators.

Accordingtothemajorityofrespondents,unrealisticcashflowprojectionsforstartupfarmsrepresentthechiefobstacleforgettinganykindoffinancialsupportfromlenders.Further,thecommondenominatorforturningdownaloanapplicationwaslackofcashflowthatwouldenablerepayment.

Asecondobstaclewaslackofpersonalcapitalbyastart‐uporbeginningfarmer.ThisisthemajorobstacletoobtainingaloanfromGreenStoneFarmCreditServices:regardlessofsizeoftheoperation,adownpaymentofbetween15%‐25%isstandardforfarmloansfromthem.

Thethirdobstacleislackofbothproductionandfarmmanagementknowledge.Saidonesmallbanklendingofficer,“Iftheymakeamistake,itcanbeaverycostlymistake.Iseeotherlendersmakingloansbasedoncollateral,butthepersonhasnoexperience.So,thelenderwillgettheirmoney,butthefarmerispayingthepricebecausethefarmerdidnotreallyknowwhattheyweredoing.”

Smallerbanksandcreditunionsfactoredintwoadditionalindicatorsoffarmsuccess:theknowledgeaboutthefarmproductandleveloffarmmanagementexperience,aswellasthefarmer’sabilitytoproviderealisticcashflowprojections?Creditunionsalsoconsideredpasthistoryofpersonalcredit,whichtheyviewasawindowintotheperson’scharacter.Theagriculturallenders,GreenstoneandUSDA,bothciteddownpayment,andunrealisticexpectationsbasedonestimatesofproductionasadditionalobstacles.BothUSDAandGreenstoneuseindustrystandardformulastodetermineexpectedreturn.

3. Communitybasedandsmallfinancialinstitutionsplacevalueonlenderrelationshipswithfarmersascosteffectivestrategiesfordeliveringservices

Respondentswereaskedtodescribelenderattributesvaluabletofarmers.Allrespondentscitedthatformingarelationshipwithaborrowerasacomponentofsuccessfullending.Responsesfromsmallbanksandcreditunionsoverwhelminglycitethevalueofbuildingarelationshipwiththeborrowerbyprovidingsomefinancialcounselingaswellasprovidingsometoolsthatenabletheborrowertopresenttheirfarmasabusinessasthemostsignificantattributetheybelieveisvaluedbyfarmers.Oneofthesmallerbank’slendingofficerstatedthattherelationshipwithanewfarmeriskey,andthatheisconcernedaboutthe

18

bank’sfuturerolewithnew,smallerfarmoperationswhenheretires.Creditunionsintermixed“easeofapplication”with“someonethefarmercantalkto”aslenderattributesthattheyconsideredvaluabletotheircustomers.

Asecondattributethatrespondentsthoughtwasinvaluabletoabeginningfarmerwasthelender’sknowledgeaboutagriculture,specifically,knowledgeaboutthetypeofagricultureforwhichtheborrowerisseekingfinancialsupport.Saidonesmallbankloanofficer,“Youngfarmersareopenmindedandtheyareaskingquestions.Theyarenotintofinancingtractors;theywanttosucceedsotheyaskquestions.Theyknowyou;youliveintheircommunity;theyneedustohelpthemthinkabouthowtomakethecashflowsotheyarenotleftwithadebtandnothingtoshowforit,eventhoughtherearelendersouttherethatwouldfinancethetractorwhethertheyneededitornot.”

4. Identificationofandmarketingtothenontraditionalfarmersectorisnotcustomary

Customerengagementreferstotheextenttowhichfinancialinstitutionsreachouttonewandbeginningfarmers,marketingproducts,andfacilitatinginteractionwithprospectivecustomers.Animportantfindingisthatover70%offinancialinstitutionssurveyedrelyonwordofmouthreferralsfromcurrentcustomers.Othercustomerengagementstrategiesmentionedincludenewsletters,satisfactionsurveys,andfarmvisits.Theseactivitieswerelimitedtocurrentcustomers,presentationsatstrategicconferences,goingtofarmersmarketstodelivertheirmonthlynewsletter,andgettingreferralsfrompartnersandassociations.

Engagingcustomersisanimportantaspectoffinancialproductaccessibility;iffinancialinstitutionsarerelyingonwordofmouth,reachingbeginningfarmersmaynotbeanorganizationalpriority.Accordingtothespokespersonforamajoragriculturallender,“Wepublishperiodicnewslettersofallfarmloan‐relatedproductinformation.Theymaynothitthosewhodonotparticipateinourdatabase;ifyoudon’tparticipate,youdon’tgettheinformation.”

LOWERINGRISKTHROUGHPARTNERSHIPSANDSUPPLEMENTARYPROGRAMSSeveralquestionsweredesignedtoexploretheextenttowhichfinancialinstitutionswereeithercurrentlyengagedinoropentopartneringwithorganizationsofferingfarmdevelopmentprograms.Integrating

19

supplementaryprogramsorpartneringwithorganizationswhooffertheseprogramsmaylessenafinancialinstitution’sperceptionofriskassociatedwithstartupfarmingoperations.PartnershipandsupplementaryprogramsareintegratedinsomeInternationalFarmTransitionNetwork(IFTN)memberbeginningfarmersandlandtransferprograms.Theseprogramscreatepartnershipsamongmanyorganizations,includingfinancialinstitutions,todevelopnewtransitionandtenurestrategiesthatfacilitatetheentryofthenextgenerationandtheexitofexistingfarmers.BeginningfarmerandlandtransferprogramssuchastheCaliforniaFarmLinkProgramandMinnesotaLandStewardshipprogramusesomeoftheapproachesmentionedbelowwithsuccess.43

1. FinancialInstitutionsrelyprimarilyoninternalprogramsandfundingsourcesforlending

Noneoftherespondentsintentionallycollaboratewithlandtrustsorothergroupsthatareworkingtocreateaccesstofarmableland.GreenStoneFSCreferscustomerstoUSDAResourceandConservationprograms.7ofthe14institutions(50%)referbeginningfarmerstolocalMSUExtension,communitycolleges,andsmallbusinessdevelopmentadministrationprogramsforbusinessplanningassistance.

Encouragingstartuporbeginningfarmerstotakeadvantageoffinancialproductsmaydependontheflexibilityofthefinancialinstitution’scapital.Noneoftherespondentsusephilanthropicfundstosupplementortargetloanproductstospecifictargetborrowers.Oftherespondentswhoofferloanproducts,50%usedepositors’savingsastheonlysourceofavailablecapital.Fiftypercent(50%)borrowmoneythroughnationalloanpools,otherbanks,orthroughbondsandloans.SeverallendersgetFSAloanguarantees.Oneofthefinancialinstitutionssurveyedlendstoanintermediarywhoseroleistoinitiativeandserviceloans.Onecreditunionlendstocooperativesthatservefarmers.Oneentityoffersloanguaranteestofinancialintuitions.

2. Financialinstitutionsdescribethesignificanceofunderutilizedancillaryprogramsandpartnerships

Noneoftherespondentsstrategicallypartnerwithanintermediarytomarkettheirproducts,togeneratemorebeginningfarmercustomers,ortoactasa“feeder”orsteppingstoneprogram.However,CountryHeritageCreditUnionactsasthefinancialinstitutionpartnerinabeginningfarmerprogramthatoffersfinancialincentivestoincreasefarmers’personalsavingsbehavior.Alloftherespondentsstatedthat

20

theycouldseethevalueofstrategicallypartneringwithanintermediary,eachforvariousinstitutionalreasons.

Stateagencies,especiallytheMichiganEconomicDevelopmentCorporation(MEDC),acknowledgedthatintermediaryorpartnershiprelationshipsareinstrumentalforthemtoworkwithincommunities.MEDCreferencedtheirworkintheDetroitareaaroundfreshfoodfinancingasanexplicitexampleofhowstrategicpartnershipsleverageMEDCfunds.MEDCworkswithpartnersacrossthestatetodeterminetheircapacityasafinancialintermediary.

Bothcreditunionscitedworkingwithintermediariesasawaytostrengthentheircapacitytoservebeginningfarmers.FrankenmuthCreditUnionrecentlymergedwithanagriculturecreditunioninSaginaw.Workingdirectlywithabeginningfarmerprogramwouldcreateanavenueforthemtoreachmorefarmersintheirexpandedgeographicarea.CountryHeritageCreditunion,hostingtheAgricultureIndividualDevelopmentAccountsinSWMichigan,referencedthepotentialofstrategicrelationshipswithareapartnerstoexpandservicestonewandbeginningfarmers.

Bothcommunitydevelopmentloanfundsstatedtheywouldwelcomeworkingwithanintermediarythatwouldincreasetheirknowledgeanddevelopmentpotentialinurbanandruralagriculture.

Smallerorcommunitybankswanttoservebeginningfarmerswhocanproducesoundfinancialprojectionsfortheirenterprise.Eachbanksuggestedthatworkingwithanintermediarythatwouldhelpprepareandmightevenprovidesupportivefinancialcapitalwouldbewellreceived.

Bothgovernmentagricultureprogramsstatedthatworkingwithintermediarieswouldbehelpfultotheirprograms.FSAissensitivetothecurrenteconomicconditionsinthebankingindustry;intermediariesthathelpfarmersprepareforviablebusinessoperationsenablethemtopresentlessriskwhenapplyingforproducts.

3. Financialinstitutionsrecognizethevalueofassetbuilding

Assetbuildingismorereadilyachievedwithsupportivefinancialtoolsthathelpthosewithlimitedincomesbuildwealth.Wealthbuildingreferstoclosingthefinancialgapthatpreventsentrepreneursfromtakingadvantageofmainstreamsourcesofcapital.Creditunionsare

21

interestedinenablingpotentialborrowerstomoveforwardalongacreditpath,butwithoutintentionalpartnerships,noneofthefinancialinstitutionsareinvolvedinthisformofequity‐basedincentivesthatshrinkthecapitalgapforstartupandbeginningfarmers.

Althoughallrespondentsunderstoodtheroleassetbuildingcouldplayinremovingobstaclestoobtainingcreditthroughtheirorganizations,onlyonefinancialinstitutionwasinvolvedinanassetbuildinginitiativewithbeginningfarmers.CountryHeritageCreditUnionpartnerswithVanBurenCountyMSUExtensiontoofferlowresourcefarmersamatched‐savingsaccountprogramcalledAgricultureIndividualDevelopmentAccounts.

Althoughothersuggestionsforassetbuildingincludedkeepinginterestratesatlowerthanmarketrateandtechnicalassistancethroughincubatorprogramsthatreduceoveralloperatingexpensesbysharingaccesstoneededequipmentorotherservices,theremainingfinancialinstitutionsdidnotenvisioncreatingprogramsthatyieldeddirectresource‐buildingforbeginningfarmers.

Summary

ResponsestothesurveysuggestthatMichiganfinancialinstitutionswanttoknowtheirbusinessborrower.Financialinstitutionsrelyontheinformationsharedbythefarmer’sbusinessplan,whichdemonstratestheirprojectionofsuccessfulproductandmarketingandshowsthemcurrentassetsandresources.Theyalsowanttoknowthefarmer’sskillset,usuallytranslatedastheexperiencetheborrowerhasinfarmmanagement.Financialinstitutionsuseavarietyoftoolstodeterminewhetherornotthefarmerwillrepayaloan.Forthemajorityoffinancialinstitutionsinterviewed,thefarmer’sproductknowledgeandfarmexperienceareofutmostsignificanceindeterminingthelikelihoodoffarmenterprisesuccess.Networthisalsoimportantintermsofprotectingthefinancialinstitutionagainstunanticipatedloss.

ComparingLenderRequirementsandBeginningFarmerAttributes

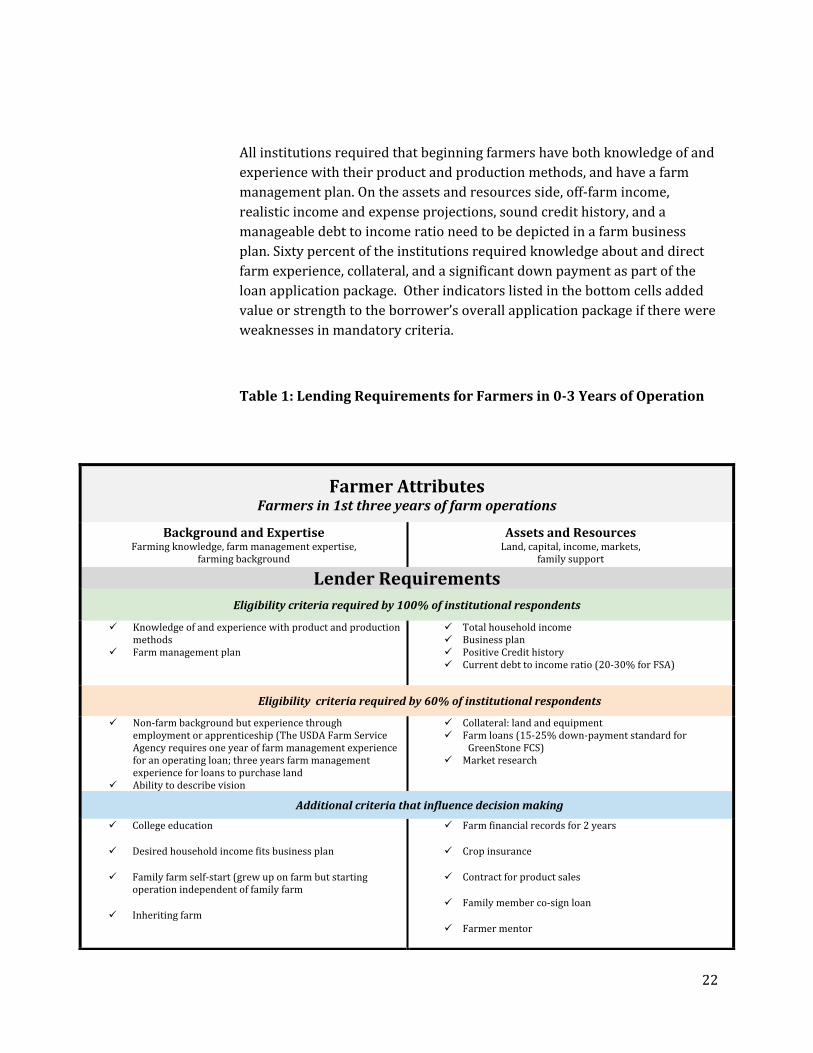

ThelistoflenderrequirementsinTable1isacompilationofrepaymentindicatorsdescribedashavingsomevaluebyfinancialinstitutionsinthestudy.Criteriainfluencinglendingdecision‐makingdifferedbyinstitutions.

22

Allinstitutionsrequiredthatbeginningfarmershavebothknowledgeofandexperiencewiththeirproductandproductionmethods,andhaveafarmmanagementplan.Ontheassetsandresourcesside,off‐farmincome,realisticincomeandexpenseprojections,soundcredithistory,andamanageabledebttoincomerationeedtobedepictedinafarmbusinessplan.Sixtypercentoftheinstitutionsrequiredknowledgeaboutanddirectfarmexperience,collateral,andasignificantdownpaymentaspartoftheloanapplicationpackage.Otherindicatorslistedinthebottomcellsaddedvalueorstrengthtotheborrower’soverallapplicationpackageiftherewereweaknessesinmandatorycriteria.

Table1:LendingRequirementsforFarmersin03YearsofOperation

FarmerAttributesFarmersin1stthreeyearsoffarmoperations

BackgroundandExpertiseFarmingknowledge,farmmanagementexpertise,

farmingbackground

AssetsandResourcesLand,capital,income,markets,

familysupport

LenderRequirementsEligibilitycriteriarequiredby100%ofinstitutionalrespondents

Knowledgeofandexperiencewithproductandproductionmethods

Farmmanagementplan

Totalhouseholdincome Businessplan PositiveCredithistory Currentdebttoincomeratio(20‐30%forFSA)

Eligibilitycriteriarequiredby60%ofinstitutionalrespondents

Non‐farmbackgroundbutexperiencethroughemploymentorapprenticeship(TheUSDAFarmServiceAgencyrequiresoneyearoffarmmanagementexperienceforanoperatingloan;threeyearsfarmmanagementexperienceforloanstopurchaseland

Abilitytodescribevision

Collateral:landandequipment Farmloans(15‐25%down‐paymentstandardfor

GreenStoneFCS) Marketresearch

Additionalcriteriathatinfluencedecisionmaking

Collegeeducation

Desiredhouseholdincomefitsbusinessplan

Familyfarmself‐start(grewuponfarmbutstartingoperationindependentoffamilyfarm

Inheritingfarm

Farmfinancialrecordsfor2years

Cropinsurance

Contractforproductsales

Familymemberco‐signloan

Farmermentor

23

FindingsofInstitutionalSupportforBeginningFarmers

Therecognitionofemergingmorelocalizedfoodsystemsengagingtheircustomerbaseenabledsmallbanks,creditunions,andloanfundentitiestoconsiderthebeginningfarmerasapotentialcustomereventhoughthepercentageoftheiroverallborrowersinthissectorwassmall.Anumberoffinancialinstitutionscoulddescribeattributesofyounger,smaller‐scalebeginningfarmersthatdistinguishedthemfromolder,largerscale,experiencedfarmers.Theseattributespermittedsomesmallbanks,creditunions,andloanfundstoreviewaborrower’sbusinessintentions,makinglendingdecisionsonacase‐by‐casebasis.Statedonebanker,“It’snotsomuchthatthetrendisorganic;it’smoreaboutthetrendinthefarmerprofile.Theyareyoung,collegeeducated,havesomeexperienceworkingonotherfarms,notachildofafarmer,havegoodideasbutnotmuchcollateral,needssmalleramountofmoneyforstartupbuthasnoworkingcapital.Somehavefamilieswhocanhelptheyoungfarmerabsorbsomeoftherisk.Somedonot.”

Smallerbanksandcreditunionsdooffertailoredfinancing,however,abeginningfarmermustmeetcertainskills,knowledge,andincomegenerationrequirements.Themajorityofsmallerlenderslookatrelationshipbuildingaskeytofarmerdevelopment.Thustheytaketimetoassistbeginningfarmerborrowers’effortstostrengthentheirapplicationpackageiffarmersdemonstratecapacityincashflowprojectionsandproduction.Beginningfarmersmayapproachsmallerbanksandcreditunionswithreasonableproductionplansaccompaniedbysomefarmingexperience,yetlackpersonalcapitalorcollateral.Ifoff‐farmincomeisnotsufficienttocoverrepaymentofaloan,somefinancialinstitutionswillworkwiththeprospectiveborrower,butwillnotlendwithoutcapacitytorepay.Thisrelationship‐buildingapproachalignswellwithacommunitybasedfoodsystemsapproachwhereeconomicviabilityacrossthefoodchainisdependentonintentionalrelationships.Localfinanciallendersbecomecriticalcomponentsofthoseintentionalrelationships.

Allrespondentswerewillingtoworkwithintermediarieswhomayactasapipelinefornewcustomers.Evenmorepromisingisthateachofthefinancialinstitutionsinterviewedcoulddescribethepotentialimpactofanintermediaryrelationshipontheirfinancialinstitution.Itisimportanttonotethatintermediarieshavetounderstandhowtoworkwiththefinancialorganization,andbringforwardcreditablecustomersorprojects.

24

LimitationswithinMichigan’sFinancialServicesSector

Relativelylarge,commodityfarmingarethescaleandmanagementstrategymostfamiliartofinancialinstitutionsinterviewedinthisstudy.Adecisionaboutwhetherafarmingoperationhaspotentialtobeeconomicallyviable,i.e.,toprovidealiving,isinfluencedbyperceptionofthelender.Theirlackoffamiliaritywithsmallerscale,diversifiedproductagriculturewasafactorindeterminingtheextenttowhichlendersbelievedfarmerswerecapableofrepayingaloan.

Smallbanksweremorelikelytohaveonepersondesignatedastheagriculturelender.Thestickingpointistheextenttowhichagriculturallendingremainsanorganizationalpriorityuponretirementoftheagricultureloanofficer.Atleasttwoofthefourbankloanofficersthatcontinuetoofferagricultureloanproductsvoicedconcernaboutthelevelofattentionagriculturemightreceivebytheirbankoncetheyretired.Creditunionswerenoticeablydifferentfrombanksinthisregard.Creditunionswereconsistentincitingtheiroverallmissiontoservetheirmembers,whichincludedsmallenterprisedevelopment.Smallorbeginningfarmdevelopmentwasseenasasmallenterprise.Therefore,financialproductscouldbetailoredtothespecificcashflowneedsofenterprise.Inthecaseofagriculture,timingofrepaymentwouldbebasedonsales.Thebankandcreditunionrespondentsweresomewhatgeographicallylimitedtoservingcustomers.Someoftherestrictionswereself‐imposedinordertomaintaindirectcontactwithcustomers.

Economicdevelopment‐orientedentities(bothcommunity‐basedloanfundsandstateagencyMEDC)donotnecessarilyseethelinkbetweenproductionagricultureandeconomicdevelopment.However,economicdevelopmententitiesdidexpressinterestintheeconomicpotentialofpostproductionbusinessdevelopment(processing;distribution)asopportunitiestostimulateMichigan’sfoodsystemeconomy.

Themajorityoftherespondentsdonotmarkettheirfinancialservicesortoolsoutsidetheirexistingcustomerandorganizationalnetworks.Thisisnottosaythatfinancialinstitutionsintervieweddonotmarkettheirproducts;however,marketingtacticssuchasnewsletters,satisfactionsurveys,andpresentationsdidnotencompassawiderangeofaudiences.Ifbeginningfarmersarenotanexistingcustomeroraffiliate,thelikelihoodthattheymaybeunfamiliarwithlocalservicesaregreat.Thisisevenmorelikelywhenbeginningfarmersdonotcomefromafarmingbackground.

25

Inasmuchasfinancialinstitutionssupportthemeritsofassetbuildingasameasuretohelpbeginningfarmersbuildnet‐worth,mostdonotofferequity‐buildingservicesnoristherethebeliefthattheyhavethefinancialwherewithaltoofferthesetoolsaspartoftheircontinuumofavailablefinancialproducts.

Recommendations

Thefollowingrecommendationsbuildonthefindingsofthisstudy.Bytakingthesesteps,wewillworktowardagoaloflong‐termaccesstoarangeoffinancialservicesthatmayservetostimulatesmall‐scaleagriculturestart‐upandexpansionwhilereducingthefinancialvulnerabilityofnewandbeginningMichiganfarmers.

PROBLEM:Mostfinancialinstitutionsuselendingmetricsbasedonthescaleandtypeofproductionwithwhichtheyaremostfamiliarlargescalecommodityagriculture;therefore,theproblemistheextenttowhichtheyunderstanddiversified,smallerscale,andmoredirectmarketfarmingsuchthatcapitalavailabilitycouldbetailoredappropriately.

RECOMMENDATION:TheCSMottGroupforSustainableFoodSystemsatMSUinpartnershipwithorganizationssuchasNorthernInitiatives,MichiganFoodandFarmingSystems,MichiganOrganicFoodandFarmAlliance,andMSU'sStudentOrganicFarmshouldprovideinformationalpresentationsonsmall‐scalefarmstartupandexpansiontailoredtofinancialinstitutionsinfourMichiganregions.Componentsofthesepresentationsshouldinclude:producerandgrowermodelsbysector,marketpotential,supportiveUSDAprograms,modelsofsuccessfulbeginningfarmerandland‐accessprograms,financialpro‐formatemplatesofferedtofarmers,andexamplesofcapitaltoolsthatcouldaccommodatesmallerscale,diversified,product‐focusedfarmoperations.

OUTCOME:Thiswouldintroducefinancialinstitutionstoproduct‐focusedstart‐upfarmingsituationsandprovideabasistoascertaintheinterestleveloffinancialinstitutionsincreatingproductsforthismarket.

PROBLEM:Manylendersarenotfamiliarwithnewerfarmers.Ourstudy,echoingnationalresearch,foundthatthesmallerthefinancialinstitution,thegreatertheimportanceofrelationshipbuildingbetweenthelenderandfarmer.However,themajorityofinstitutionshavelittlecontactwithnewerfarmers,andrefrainfrommarketing

26

theirproductsoutsidetheircurrentcustomerbases.Further,beginningfarmersarenotnecessarilyseekingservicesfrommoreestablishedfinancialinstitutions.

RECOMMENDATION:TheMSUDepartmentofAgriculture,Food,andEconomicResourcesandtheCSMottGroupforSustainableFoodSystemsatMSUshouldconveneagatheringofbeginningandnewerfarmers,representingdiversityofproductandstageoffarmdevelopment,withfinancialinstitutionstodiscussthelinkbetweenfarmenterprisedevelopment,thecapitalneedsoffarmentrepreneurs,andpotentialeconomicimpactregionallyandatstatewide.SuchagatheringmightbepartoforlinkedtotheannualagriculturallendersconferencesponsoredbyMichiganStateUniversity.

OUTCOME:Buildingtoolkitoffinancialcapitalproductsspecificallycreatedforandmarketedtowardbeginningfarmers.

PROBLEM:Allfinancialinstitutionsparticipatinginthisstudyrequireapplicantstosubmitbusinessplans.Atthispoint,therearenobusinessplancoursesinMichiganspecificallytailoredtofarmstartup,andthosecoursesorientedtowardexistingfarmoperationsarenotofferedwithregularity.

RECOMMENDATION:Basedonfeedbackfromfinancialinstitutionsandfarmers,TheMichiganFoodandFarmingSystems,inpartnershipwithMSUExtension,TheCSMottGroup,theMSUStudentOrganicFarm,andTheMichiganLandUseInstitute’sGetFarmingProgramshouldpilotregionallyarobustfarmbusinessplancoursethatenablessmallfarmstartuporenhancement.Tetherthefarmbusinesscoursewithexistingbeginningfarmerprograms,organicfarmcertificateprograms,andland‐accessprograms.ItisourrecommendationthatfarmdevelopmentprogramsinMichiganbestrengthenedthroughtwoavenues:MSUshoulddevelopacademiccourseworktopreparestudentsfordevelopingrealisticbusinessplans.MSUExtensionhasofferedfarmsuccessionprogramsandcouldcontinueleadthiseffortbyintegratingsuccessfulcomponentsoftheInternationalFarmTransitionNetworkmodel.

OUTCOME:Startupfarmsreceivebusinessplanandnetworksupportoverthecourseofthreeyearstomeasurefarmincome.Financialinstitutionsplayakeyroleinproviding“steppingstone”financialcapitaltomatchscaleandstageofoperation.

27

PROBLEM:Despitethefactthatthemajorityoffinancialinstitutionsrequireadownpaymentorcollateraltogetanoperationalloan,onlyoneinstitutionsurveyedoffersassetbuildingtoolsthatenablefarmerstogenerategreaternetworth.AgricultureIndividualDevelopmentAccountshaveasuccessfultrackrecordinaddressinglimitedresourcefarmers’financialnetworth;however,thisassetbuildingtoolislimitedbythesponsoringorganization’sabilitytoraisesufficientfundstomatchthesavingsofparticipatingfarmers.

RECOMMENDATION:Basedonitssuccessfultrackrecord,theCSMottGroupforSustainableFoodSystemsatMSUandlendinginstitutionsofferingarangeoffinancialservicestobeginningfarmersshouldconvenephilanthropicentities,policymakers,andbeginningfarmerprogramstogethertodiscusstheinclusionofAgricultureIDAsaspartofthecontinuumofcapitalavailabilityforstartup,limited‐resourcefarmers.ThesuccessfulAgricultureIDAprogrampilotedinsouthwestMichiganwouldserveasthemodelforregionalexpansion.

OUTCOME:IntegratetheAgricultureIDAswiththefarmbusiness‐planningcourseofferedacrossthestate;createanendowmentformatchfunds.

Closing

ThispaperoffersapreliminaryexplorationoftheextenttowhichprivateandothersourcesofcapitalareavailableinMichigantosupportbeginningfarmers.Onthefinancialinstitutionside,capitalavailabilitybecomesmoreaccessibletobeginningfarmerstotheextentthatbeginningfarmerscanarticulatetheirfarmenterprisesthroughwell‐writtenbusinessplansandfinancialprojectionsthatfitthescaleoftheiroperation.ItisourintenttousethefindingsofthisstudytomoverecommendationsthataddressimpedimentstogrowcapitalinvestmentsinMichigan’ssmallerscale,diversifiedagricultureintoaction.

28

References1Ahearn,M.,andNewton,D.,BeginningFarmersandRanchers,USDAERSEconomicInformationBulletinNumber53,May2009,p.22;www.ers.usda.gov/Publications/EIB53/EIB53.pdf2GettingaHandleontheBarrierstoFinancingSustainableAgriculture:TheGapsBetweenFarmersandLendersinMinnesotaandWisconsin,LandStewardshipProject,June2003;http://www.landstewardshipproject.org/pdf/edsurvey.pdf3Knudson,B,Peterson,H.C.,SecondInterimUpdateontheEconomicImpactofMichigan’sAgri‐FoodandAgri‐EnergySystem,MichiganStateUniversityProductCenterforAgricultureandNaturalResources;http://www.productcenter.msu.edu/strategic.htm4PublicSectorConsultants,Inc.(PSC).2001.MichiganLandResourceProject.AReportPreparedfortheMichiganEconomicandEnvironmentalRoundtable.November2001.http://www.peopleandland.org/resourcelibrary/lbilu/fullreport.pdf.5MichaelFieldsAgriculturalInstitute,TheNextGenerationofFarmers,http://www.michaelfieldsaginst.org/work/policy/newfarmer.shtml6Ahearn,M.,andNewton,D.,BeginningFarmersandRanchers,USDAERSEconomicInformationBulletinNumber53,May2009,p.1;www.ers.usda.gov/Publications/EIB53/EIB53.pdf7Ahearn,M.,andNewton,D.,BeginningFarmersandRanchers,USDAERSEconomicInformationBulletinNumber53,May2009,p.2;www.ers.usda.gov/Publications/EIB53/EIB53.pdf8Gale,H.,“LongitudinalAnalysisofFarmSizeOvertheFarmer’sLifeCycle.”ReviewofAgriculturalEconomics14(Jan.1994):484‐879JanieHipp,NationalProgramLeader,CSREES,USDA,PlenaryPanel,InternationalFarmTransitionNetworkConference,Denver,CO,June11,200910USDAERSAgriculturalResourcesandEnvironmentalIndicators,2006Edition/EIB‐16http://www.ers.usda.gov/publications/arei/eib16/11Formoreinformation,goto:http://www.realtown.com/articles/view/loss‐of‐farmland‐what‐does‐it‐mean#ixzz0NFE2MeMl122007UnitedStatesCensusofAgriculture;http://www.agcensus.usda.gov/Publications/2007/Full_Report/index.asp13FarmingontheEdgereporthttp://www.farmland.org/resources/fote/default.asp14Wittenberg,E.,andHanson,S.,“Farmlandvaluesclimb,farmearningssoften”,http://www.michiganfarmbureau.com/farmnews/transform.php?xml=20090215/farmland.xml152007USDACensusDemographics;http://www.nass.usda.gov/Statistics_by_Subject/Demographics/index.asp16Ahearn,M.,andNewton,D.,BeginningFarmersandRanchers,USDAERSEconomicInformationBulletinNumber53,May2009,p.1;www.ers.usda.gov/Publications/EIB53/EIB53.pdf17InterviewwithCoreiaPearce,StudentOrganicFarm,MichiganStateUniversity,regardingwaitinglistforOrganicCertificateProgram,June200918InterviewwithJeremyMoghtader,AgIDAOrientationMeeting,MSUSOF,August14,2009.

29

19Illinoislegislationhttp://foodfarmsjobs.org/;Wisconsin,http://www.growingproduce.com/americanvegetablegrower/?storyid=40920Greene,C.,Dimiri,C.,Bljing‐Hwan,L.,McBride,W.,Oberholtzer,L.,Smith.,T.,NewReport:EmergingIssuesinUSOrganicIndustry,EconomicInformationBulletin,No(EIB‐55),June2009;www.ers.usda.gov/Publicatios/EIB55http://www.ers.usda.gov/publications/eib55/eib55_reportsummary.html21SeetheLocalDifference:RegionalFoodSystemsBecomeEssentialIngredientForMichiganFuture,MichiganLandUseInstitute,2009www.localdifference.org22Formoreinformation,see:http://www.csafarms.org/23Formoreinformation,see:http://www.moffa.org/f/MI_Organic_Agriculture_Report_March_2007.pdf24PillarandLand4:ThrivingAgriculturetogrowMichiganEconomy,www.peopleandland.org/resourcelibrary/pillars/PAL_Pillar_4.pdf;)MichiganFoodPolicyCouncil.,ReportofRecommendations,preparedforGovernorJenniferGranholm(Lansing,MI:MFPC,October2006)25PillarandLand4:ThrivingAgriculturetogrowMichiganEconomy,www.peopleandland.org/resourcelibrary/pillars/PAL_Pillar_4.pdf26Conner,D.Knudson,W.Hamm,M.andPeterson,C.(2008).TheFoodSystemasanEconomicDriver:StrategiesandApplicationsforMichigan.JournalofHungerandEnvironmentalNutrition3(4)371‐383.27CantrellP.,Conner,D.,Erickcek,G.,Hamm,M.W.,EatFreshandGrowJobs,Michigan,September2006page4.,http://www.mlui.org/farms/fullarticle.asp?fileid=1708628ListeningtoNewFarmers:FindingsfromNewFarmerFocusGroups,theNortheastNewfarmNetwork,NewEnglandSmallFarmInstitute,June200129ListeningtoNewFarmers:FindingsfromNewFarmerFocusGroups,theNortheastNewfarmNetwork,NewEnglandSmallFarmInstitute,June200130ListeningtoNewFarmers:FindingsfromNewFarmerFocusGroups,theNortheastNewfarmNetwork,NewEnglandSmallFarmInstitute,June2001,page531Weise,Elizabeth,“OnTinyPlots,ANewGenerationofFarmersEmerges,USAToday,7/14/200932MichiganNewFarmDevelopment:CaseStudiesfromtheSWMichiganEmergingFarmerProgram,March2009;www.mottgroup,msu.edu33Dunne,T.,Roberts,M,andSamuelson,L.,“PatternsofFirmEntryandexitinUSManufacturingIndustries,RANDJournalofeconomics,vol.19,#4,Winter198834Akhavein,J.,Goldberg,L.,White,L.,“Smallbanks,SmallBusiness,andRelationships:AnEmpiricalStudyofLendingtoSmallFarms”,JournalofFinancialServicesResearch,200426:3245‐261NOTE:FarmCreditSystemprovides25%offarmcreditnationally35ComptrollersHandbook,www.occ.treas.gov/handbook/aglend.pdf36GettingaHandleontheBarrierstoFinancingSustainableAgriculture:TheGapsBetweenFarmersandLendersinMinnesotaandWisconsin,LandStewardshipProject,June2003http://www.landstewardshipproject.org/pdf/edsurvey.pdf37AnAgriculturalMystery;WhyAren’tThereMoreFarmersLikeDavidKnaus.January24,2009,http://columbian.com/article/20090125/NEWS02/701259949

30

38Ruhf,K.Z.,NortheastNewFamers:OpportunitiesforPolicyDevelopment,NewEnglandSmallfarmInstituteJune2001http://growingnewfarmers.org/uploads/uploads/Files/Policy_Background_Paper.pdf39Ahearn,M.,andNewton,D.,BeginningFarmersandRanchers,USDAERSEconomicInformationBulletinNumber53,May2009,p.1;www.ers.usda.gov/Publications/EIB53/EIB53.pdf40TheCarrotProject,FarmersFinancingNeedsAssessment,June2007,[email protected],gotothefollowingwebsites:http://www.uvm.edu/~susagctr/Documents/firstfarmloan.pdf;http://californiafarmlink.org/joomla/index.php?option=com_weblinks&catid=39&Itemid=2342GreenstoneFarmCreditServicesAnnualReport(2008);http://www.greenstonefcs.com/about/company/financial.aspx43SeeInternationalFarmTransitionNetworkwebsiteforlistingofnationalfarmlinkprogramshttp://www.farmtransition.org/netwpart.html;http://www.landstewardshipproject.org/resources‐main.html

http://californiafarmlink.org/joomla/index.php?option=com_content&task=view&id=33&Itemid=47

31

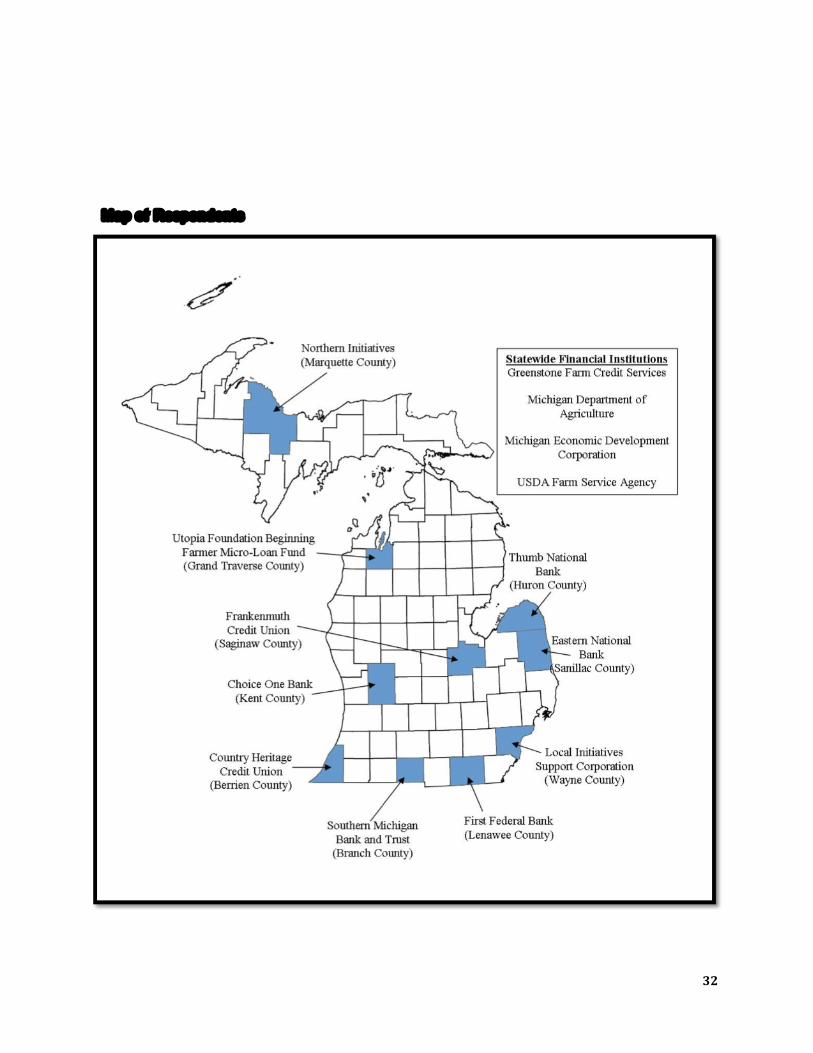

Appendix

SURVEYRESPONDENTSAlloftherespondentswereinterviewed.Twelveorganizationscompletedthesurvey.Twoentitieschosenottocompletethesurvey.

ChoiceOneBank,Sparta,MI(KentCounty)

CountryHeritageCreditUnion,Buchanan,Mi(BerrienCounty)

FrankenmuthCreditUnion,Frankenmuth,MI(SaginawCounty)

GreenStoneFarmCreditServices(statewide)

LocalInitiativesSupportCorporation,Detroit,MI

MichiganDepartmentofAgriculture(statewide)

MichiganEconomicDevelopmentCorporation(statewide)

NorthernInitiatives,Marquette,MI(MarquetteCounty)

SouthernMichiganBankandTrust,Coldwater,MI(Branch)

ThumbNationalBank,Pigeon,MI(Huron)

EasternNationalBank,Crosswell,MI(Sanillac)

USDAFarmServiceAgency(Michigan)(Statewide)

OTHERFINANCIALINSTITUTIONS*UtopiaFoundationBeginningFarmerMicro‐LoanFund,TraverseCity,MI(GrandTraverseCounty)

FirstFederalBank,Morenci,MI(Fulton)

*Metwithorphonedbothinstitutions.Bothsharedsomeinformationbutchosenottoparticipateinthesurveyduetoeitherstageofdevelopment,ornolongerprovidedagriculturelending.

32

MapofRespondents