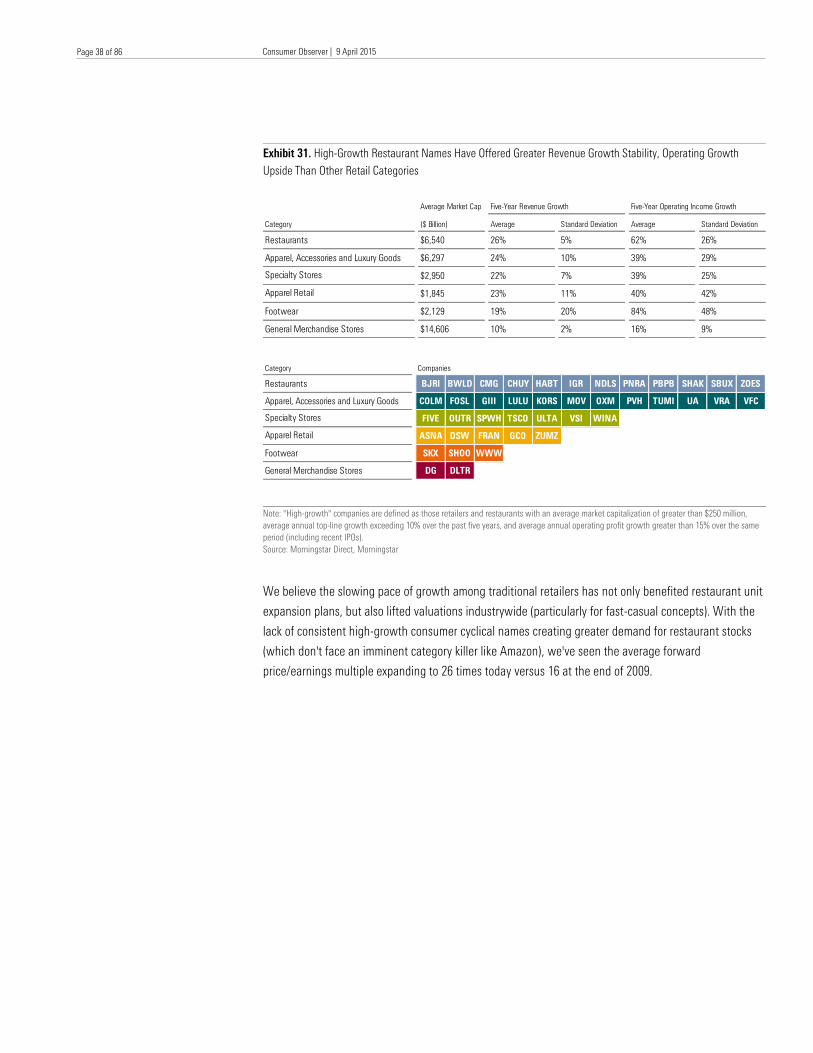

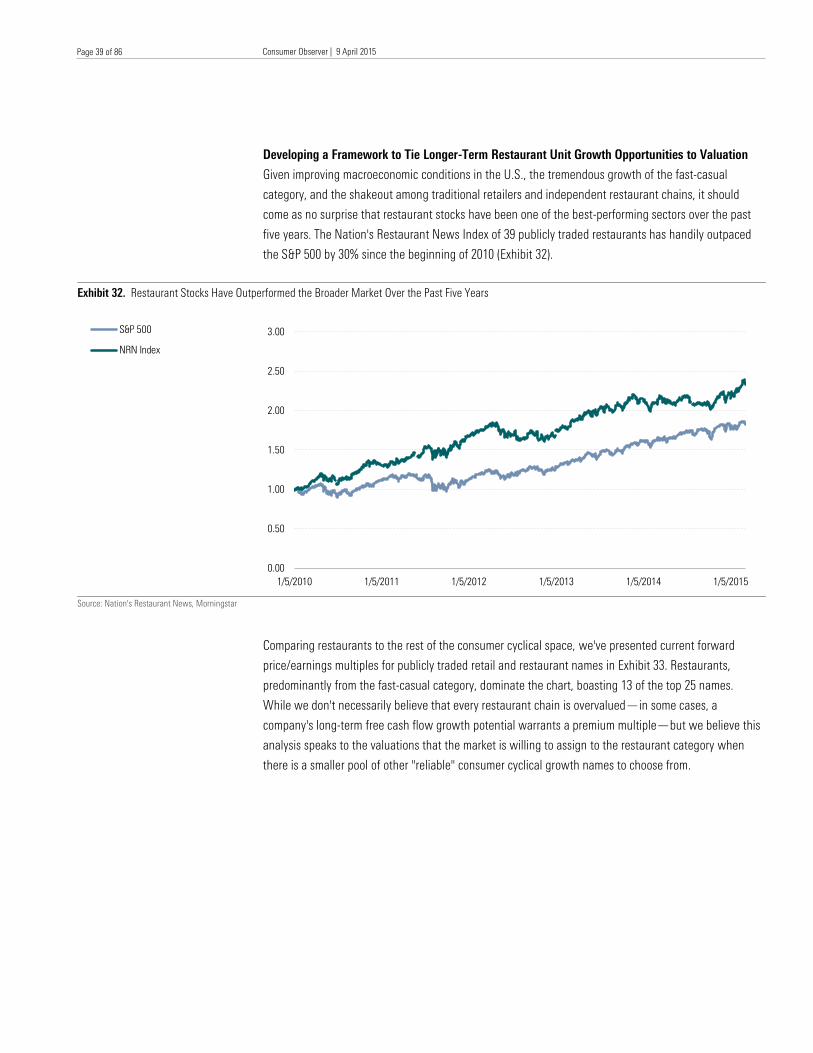

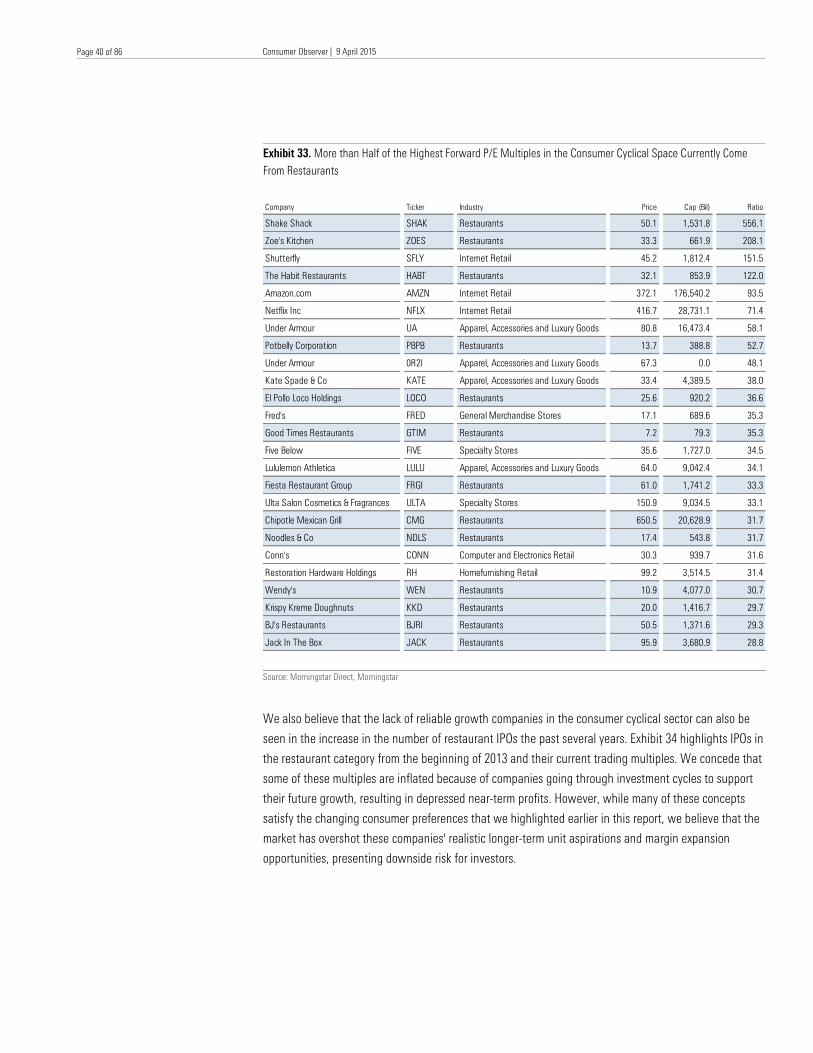

finding restaurant investment opportunities as the...

TRANSCRIPT

?

April 2015

September 2014

Finding Restaurant Investment Opportunities as the Moat-Disruptive Fast-Casual Category Matures

Executive Summary

Restaurants have been one of the most intriguing categories within the consumer space the past several

years, with fast-casual chains like Chipotle and Panera increasingly becoming disruptive forces for both

traditional quick-service and casual-dining restaurant chains. Broadly speaking, we believe that many

fast-casual concepts warrant premium valuations relative to their peers because of the pricing power

inherent in their brands—the impetus for positive moat trends for many players in the space—as well

as a cost-effective model than casual-dining players. However, as many established fast-casual chains

reach maturity at a time when smaller emergent players have relatively easy access to attractive real

estate and inexpensive rents, we believe investors must be cognizant of the potential fast-casual

"bubble" in the market today.

Additionally, increased competition from fast-casual players has triggered many strategic

countermeasures to unlock value across other quick-service and casual-dining restaurant chains. This

includes more straightforward efforts such as localized/regional menu and marketing decisions,

increased customization, mobile ordering, and reimaging efforts leveraging digital platforms but also

more aggressive tactics such as more aggressive franchising/refranchising, real estate transactions, and

spin-offs. In this report, we also examine which strategic actions can realistically unlock shareholder

value, and opportunities where these efforts haven't been priced into the stocks.

Morningstar’s Top Restaurant Investment Ideas

Name/Ticker

Economic

Moat

Moat

Trend

Currency

Fair Value

Estimate

Current

Price

Uncertainty

Rating

Morningstar

Rating

Credit

Rating

Market

Cap(Bil)

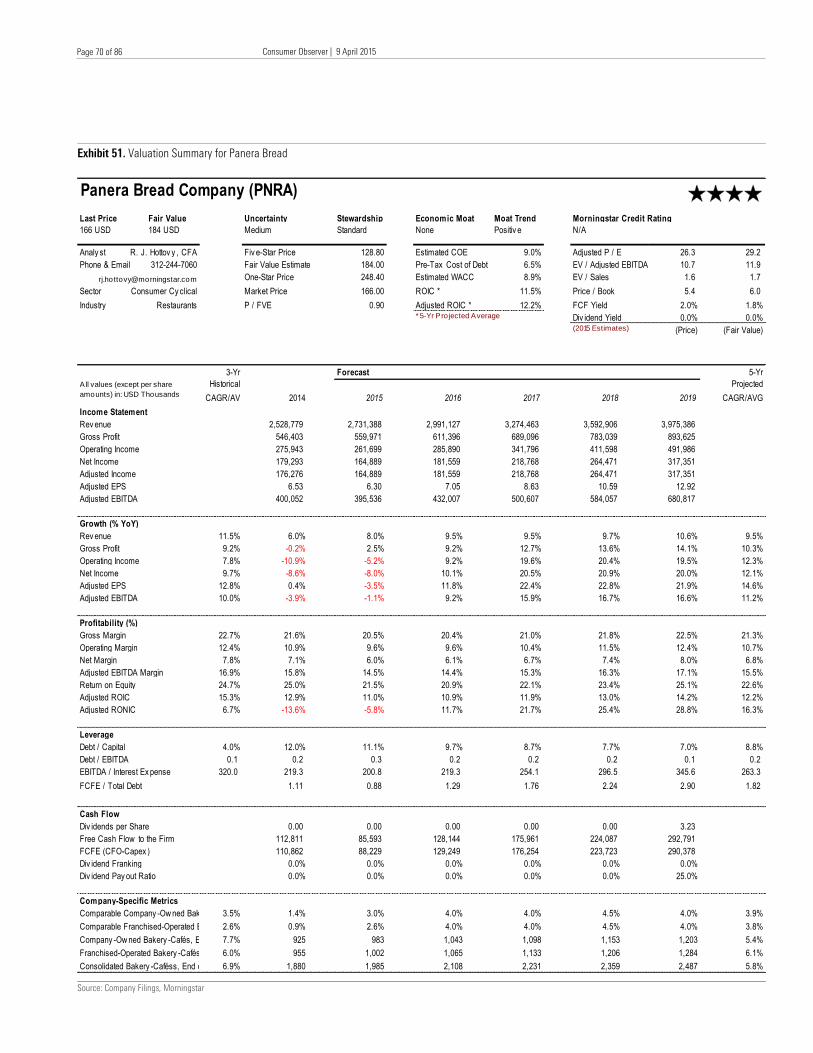

Panera PNRA None Positive USD 184.00 165.97 Medium QQQQ — 4.4

Starbucks SBUX Wide Positive USD 50.00 47.62 Medium QQQ A- 71.4

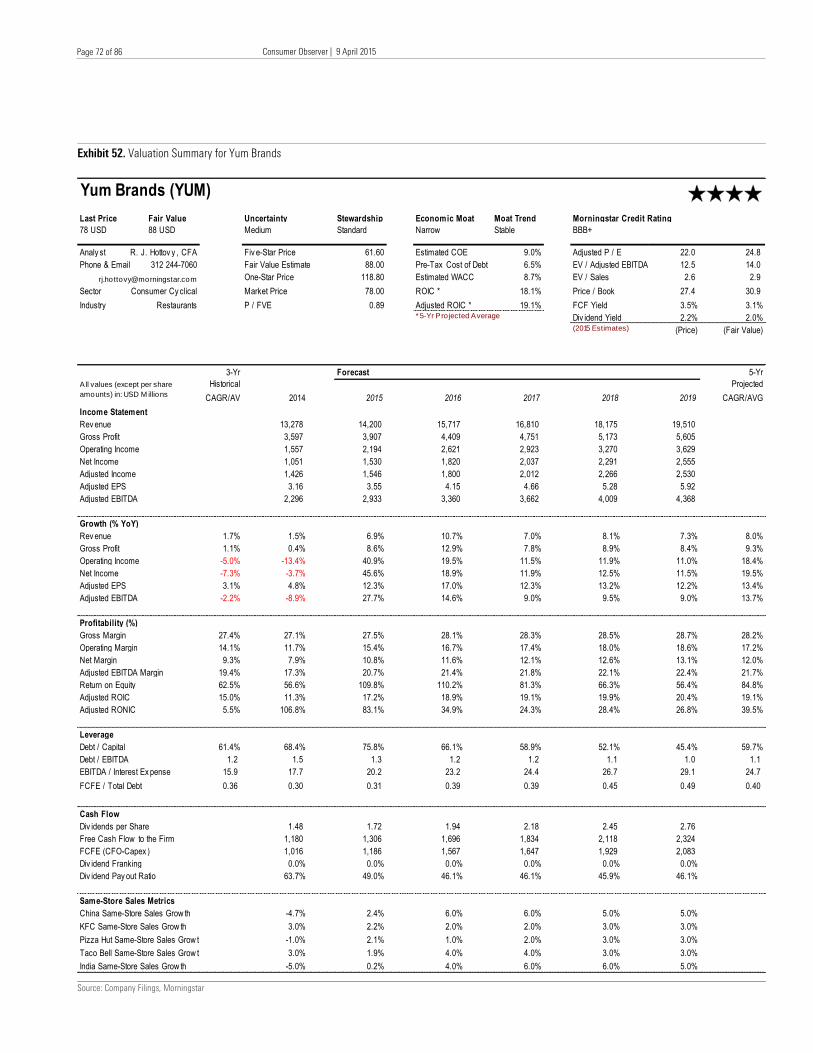

Yum Brands YUM Narrow Stable USD 88.00 78.30 Medium QQQQ BBB 33.9

Contents

2 Key Takeaways

5 Best Ideas

7 Fast-Casual Has Reshaped Preferences

Across the Restaurant Category,

Resulting in Material Changes in

Industry Pricing Power

27 Are There Any Restaurant Investment

Opportunities in a Market Willing to Pay

More Than 500 Times for Shake Shack?

49 Assessing Traditional Restaurants'

Countermeasures to Fast-Casual

Competitive Pressures

67 How Have Restaurant Industry

Changes Reshaped Our Moat Rating

Methodology?

Restaurant Coverage Universe

69 Panera

71 Yum Brands

73 Starbucks

75 Restaurant Brands International

77 McDonald's

79 Chipotle

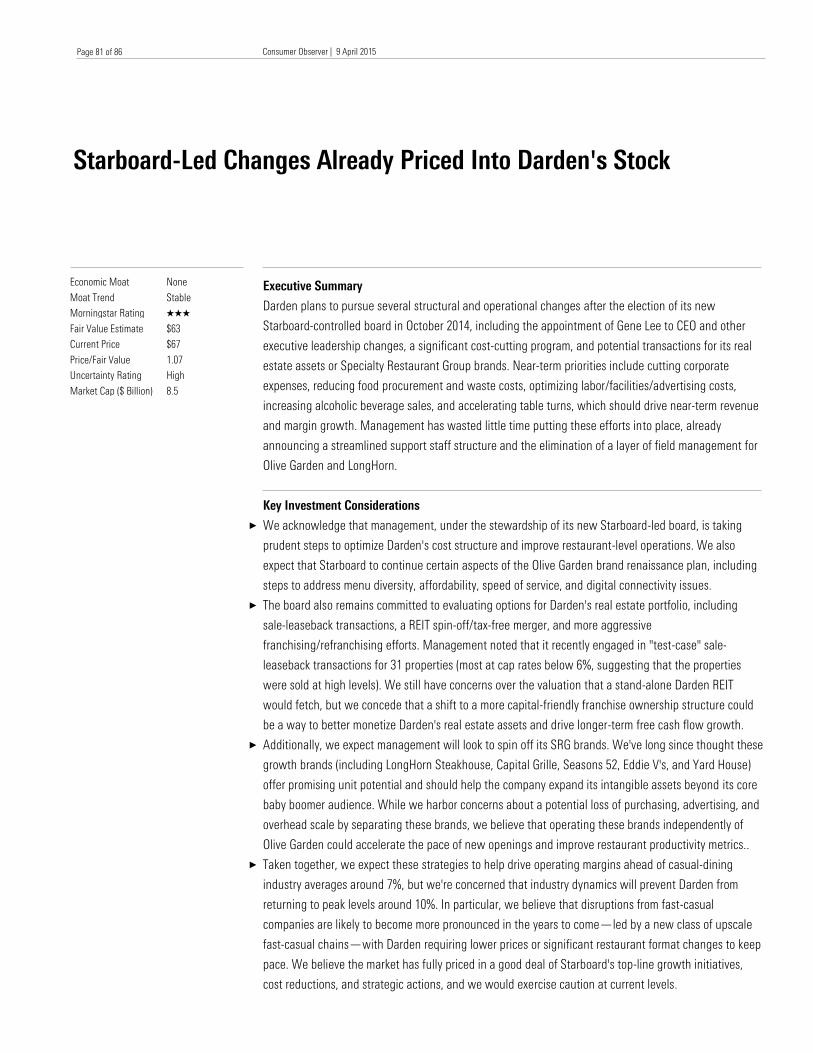

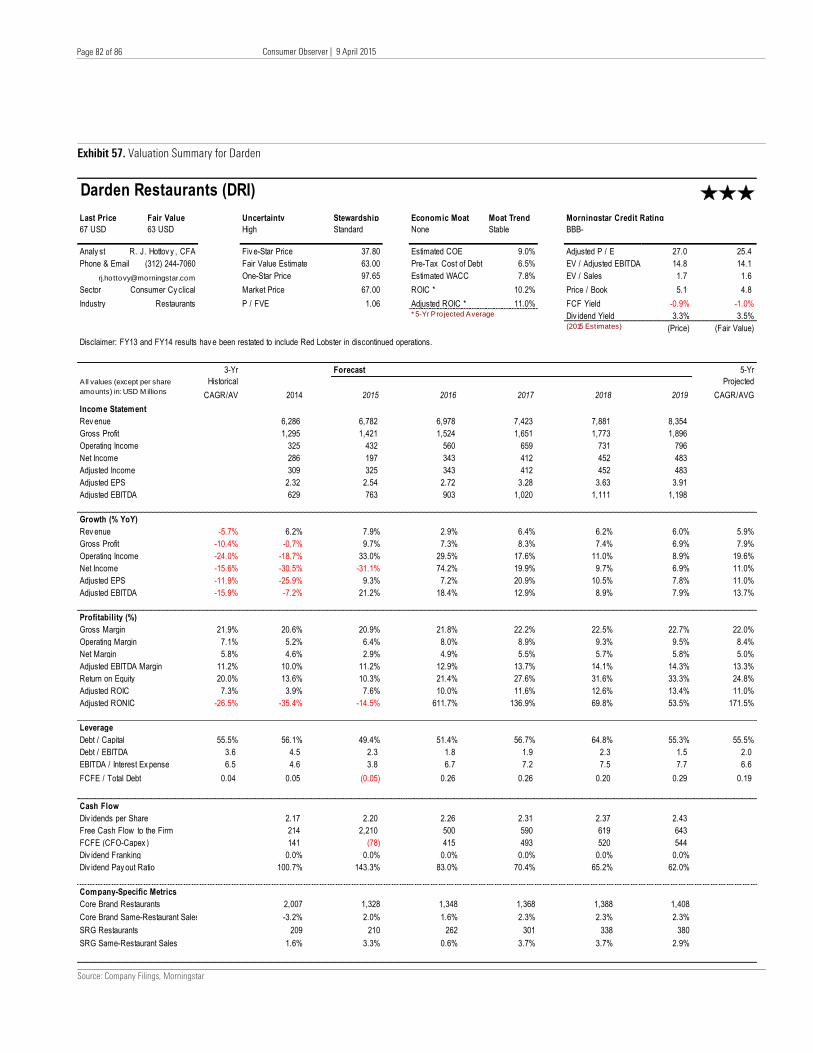

81 Darden

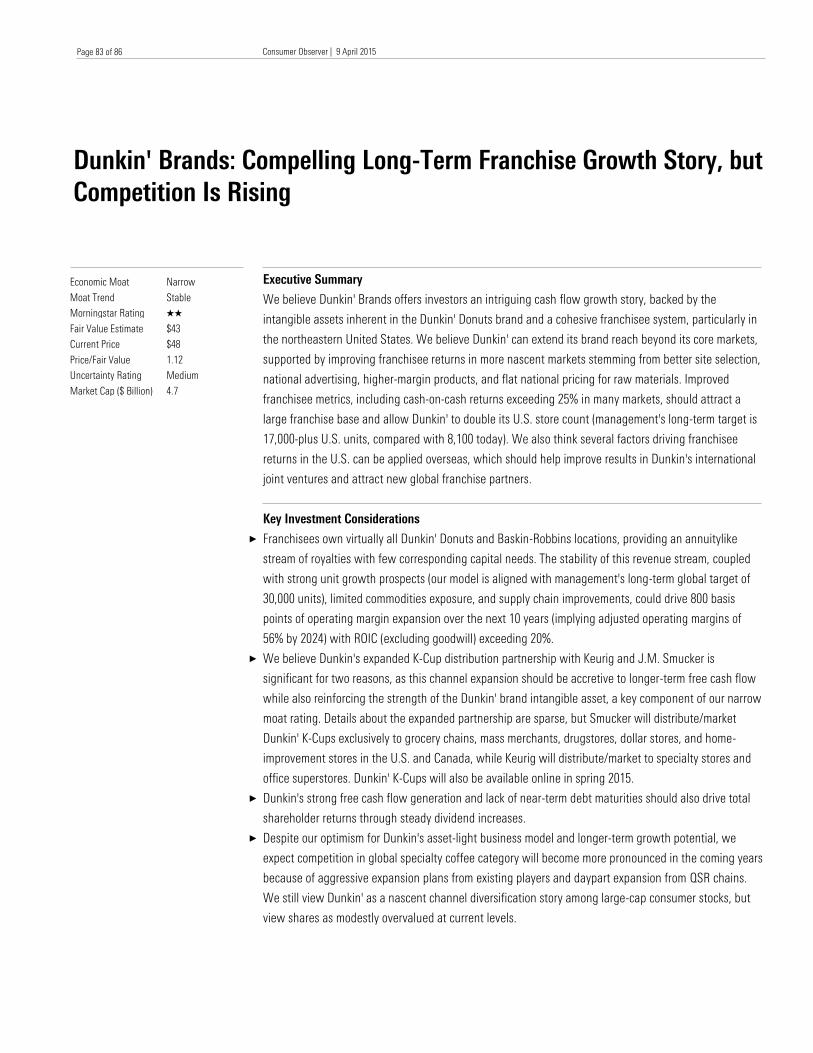

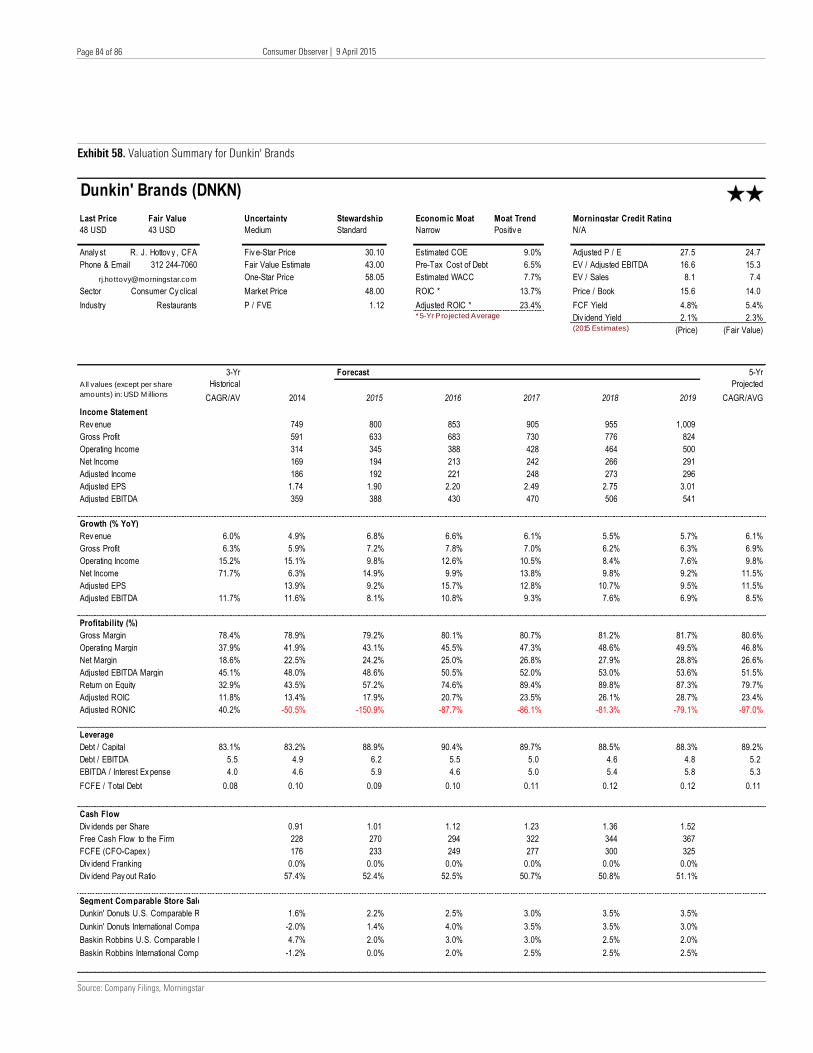

83 Dunkin' Brands

85 Appendix

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 2 of 86

Page 2 of 86

Key Takeaways

Fast-Casual Has Reshaped Preferences Across the Restaurant Category, Resulting in Material

Changes in Industry Pricing Power

× Fast-casual restaurants have better adjusted to changes in consumer behavior during the past several

years, including increased spending power among minority groups and millennials (which has created

demand for a wider variety of flavors, better-for-you products, and locally sourced food), evolving views

about in-restaurant experiences (resulting in consumer calls for customizable menus and faster

throughput), and widespread advances in consumer-facing technologies (leading to mobile-based

ordering, payment, and loyalty programs as well as in-restaurant wireless offerings).

× More important, consumers aren't just willing to visit fast-casual chains more frequently; they're also

willing to pay premium prices for the product and restaurant experience. The companies that have

stayed ahead of changing consumer preferences have also experienced a meaningful increase in

average checks during the past five years, while the increase for traditional quick-service restaurants, or

QSRs, has been more muted. In our view, the increase in average check suggests greater pricing power,

and by extension, a strengthening of the brand intangible asset source that we consider when

evaluating economic moats among retailers and restaurants.

× The ability to adapt to evolving consumer preferences, and the subsequent pricing power, was a key

consideration behind the positive moat trends we've assigned to fast-casual chains such as Chipotle and

Panera as well as Starbucks. Likewise, the inability to react to these changes was a factor in our

negative moat trend for McDonald's and the removal of our narrow moat rating for Darden.

Are There Any Restaurant Investment Opportunities in a Market Willing to Pay 500 Times for

Shake Shack?

× With fast-casual restaurants aligned with changes in consumer dining-out preferences and favorable

retail rent and vacancy trends, we expect the fast-casual category revenue to grow at a compound

annual growth rate (CAGR) of 9.4% during the next five years, taking share from QSRs and casual-dining

restaurants, or CDRs, which we expect to grow 4.1% and 3.7%, respectively.

× The rise of e-commerce has reduced the number of reliable growth concepts among traditional retailers,

which we believe has led to higher valuations across much of the restaurant industry (which now trades

at a forward price/earnings multiple of almost 26 times, up from 16 times five years ago). While some of

this multiple expansion is warranted given the growth potential and the lack of a major disruptive

presence like Amazon, we generally believe the market has overshot the longer-term potential of many

fast-casual concepts such as Noodles & Company, Zoe's Kitchen, and Habit Restaurants.

× Conversely, we find shares of Panera attractive at current levels and believe the market isn't giving the

company enough credit for its longer-term unit growth opportunities (both traditional locations and

delivery and catering hubs) and the cash flow potential of its "Panera 2.0" restaurant remodeling

initiative.

Lead Analyst

R. J. Hottovy, CFA

Consumer Equity Strategist

+1 312-244-7060

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 3 of 86

Page 3 of 86

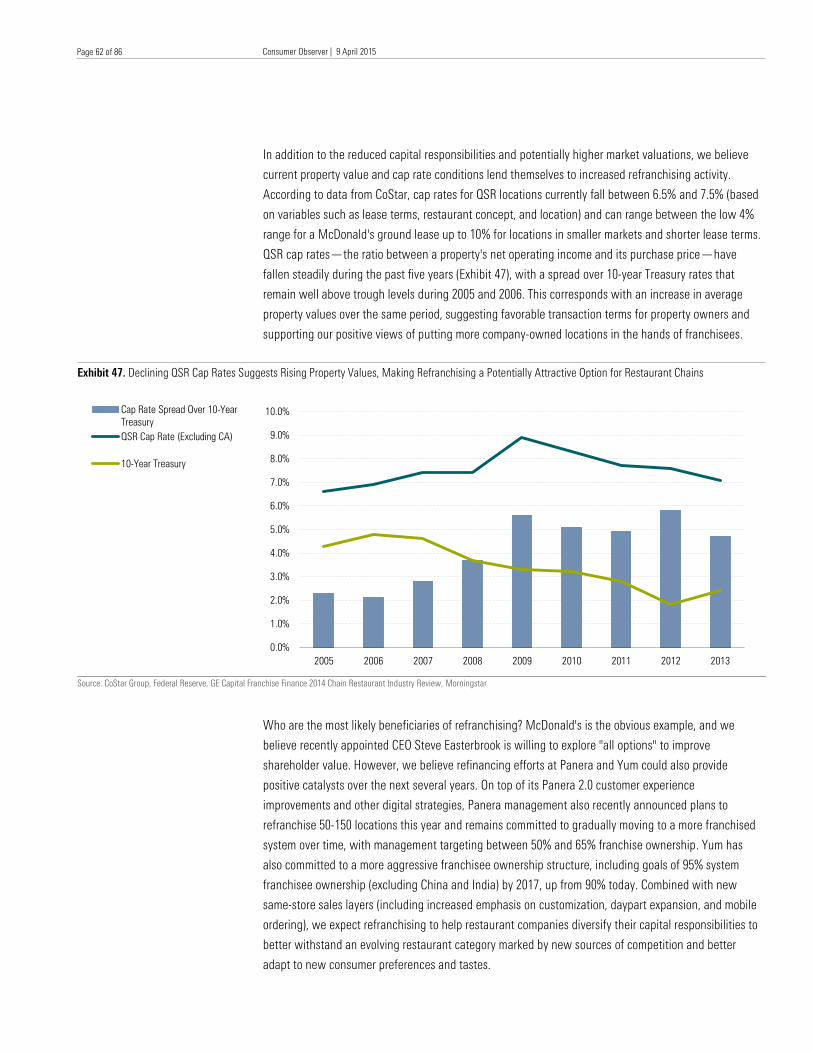

Assessing Traditional Restaurants' Countermeasures to Fast-Casual Competitive Pressures

× We believe consumers' willingness to pay premium prices has been at the heart of the recent QSR

industry movement toward fewer menu items, but more customization options. However, we believe it

will take time for QSRs to realize the benefits of these menu changes, where rationalizing the number of

menu items helps speed up service and customer experience improves over the next year or so followed

by increased awareness and adoption of menu customization options.

× For many traditional restaurant operators, we believe that expansion into other dayparts (breakfast and

snacking, for example), increased adoption of technology to increase throughput via mobile ordering and

payments, and greater delivery/catering alternatives have the potential to improve store productivity

through both increased guest counts and higher average checks. We view each of the Best Ideas that

we've highlighted in this report—Panera, Starbucks, and Yum Brands—as well-positioned to achieve

better utilization trends out of their existing restaurants in the years to come.

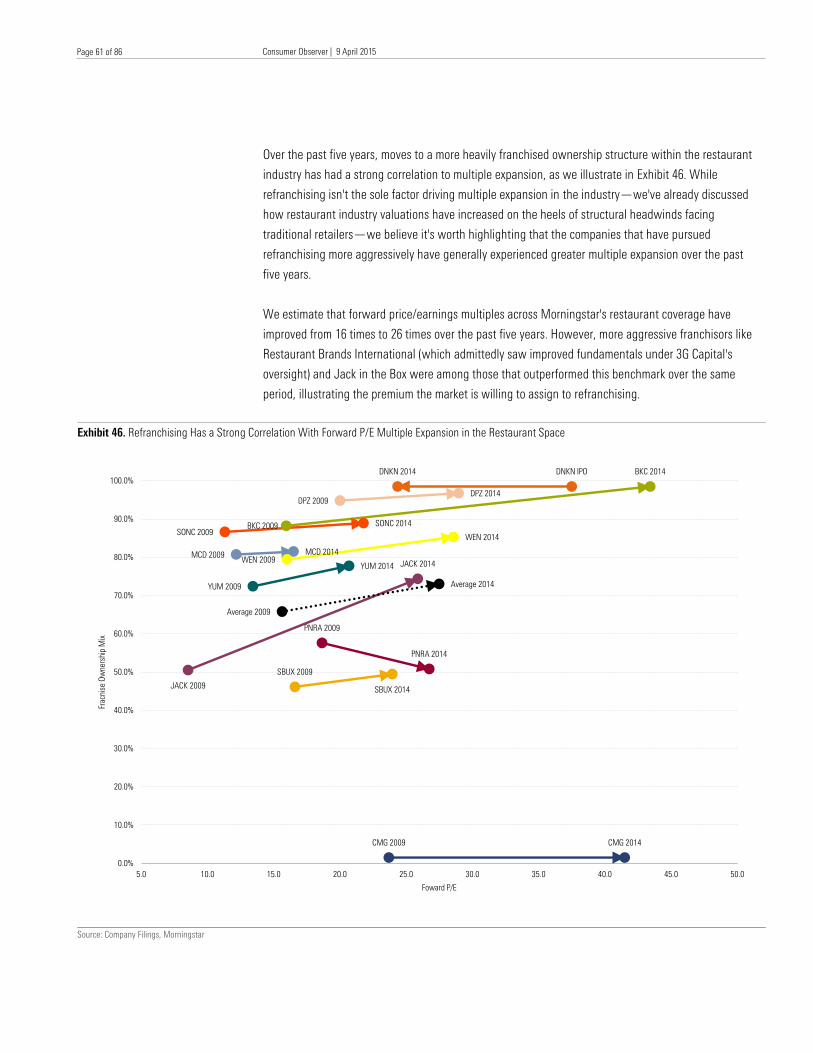

× While refranchising isn't the sole factor driving multiple expansion in the industry, it's noteworthy that

the companies that have pursued refranchising more aggressively have generally experienced greater

multiple expansion over the past five years. We believe McDonald's will probably explore refranchising

options in the near future, as recently appointed CEO Steve Easterbrook has said he is committed to

considering "all options" to improve shareholder value. However, refranchising efforts at Panera and

Yum could also provide positive catalysts over the next several years.

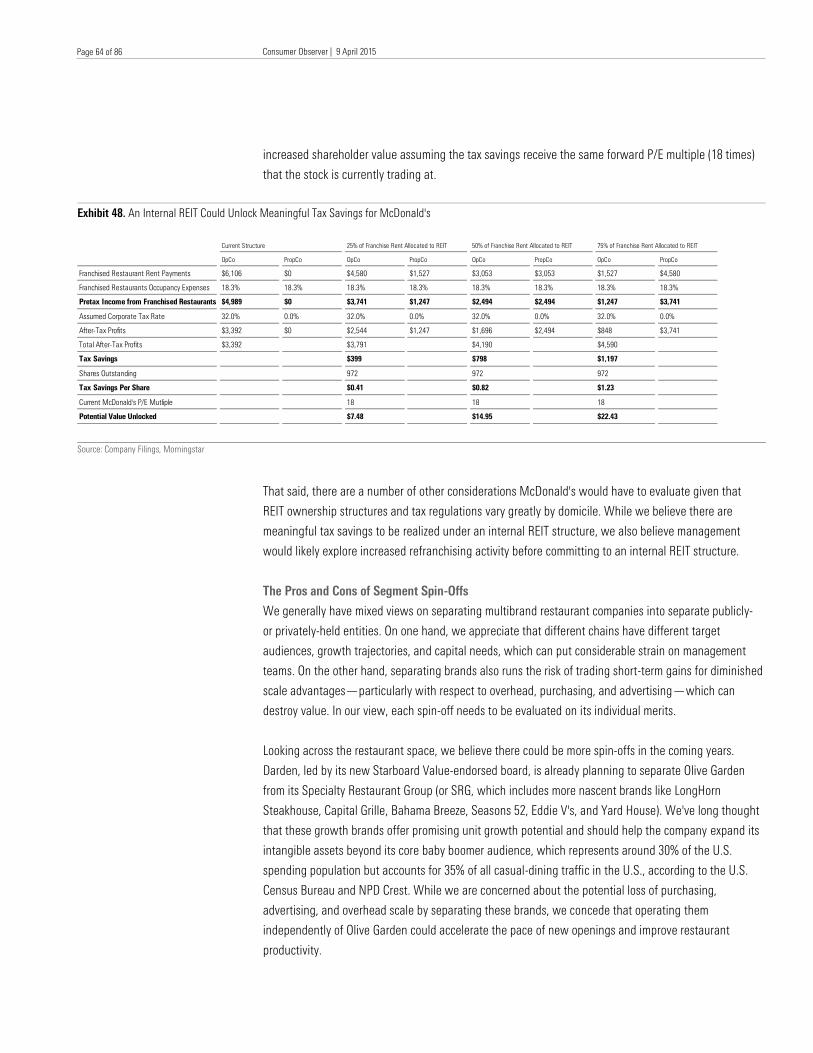

× We believe the market's appetite for potential real estate transactions have increased over the past year

given the current low interest-rate environment and REIT spin-off announcements from other retailer

and restaurant chains. With $39 billion in land and building assets on its balance sheet as of December

2014 and $6.1 billion in rents collected from franchisees last year, McDonald's remains a popular target

for real estate transactions among activist investors and hedge funds. The potential tax savings would

ultimately depend on how much real estate the company was willing to commit to a property company

subsidiary, but because REITs must pay out at least 90% of taxable earnings to shareholders as

dividends and don't pay federal income taxes on income distributed to shareholders, we believe

McDonald's could unlock shareholder value by creating an internal REIT.

× We generally have mixed views on separating multibrand restaurant companies into separate publicly or

privately held entities. On one hand, we appreciate that different chains have different target audiences,

growth trajectories, and capital needs, which can put considerable strain on management teams. On the

other hand, separating brands also runs the risk of trading short-term gains for diminished scale

advantages—particularly with respect to overhead, purchasing, and advertising—which can destroy

value. The idea of separating Yum's China division has some merit, as we've long thought that Yum was

much more than a China growth story and believe that separation would allow investors to tailor their

level of exposure to China and Yum's other emerging markets. Additionally, Yum China is a mostly self-

contained supply chain, distribution, site selection, and advertising ecosystem, and we believe a

separation would be relatively seamless from an operating perspective and would not sacrifice

meaningful scale advantages.

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 4 of 86

Page 4 of 86

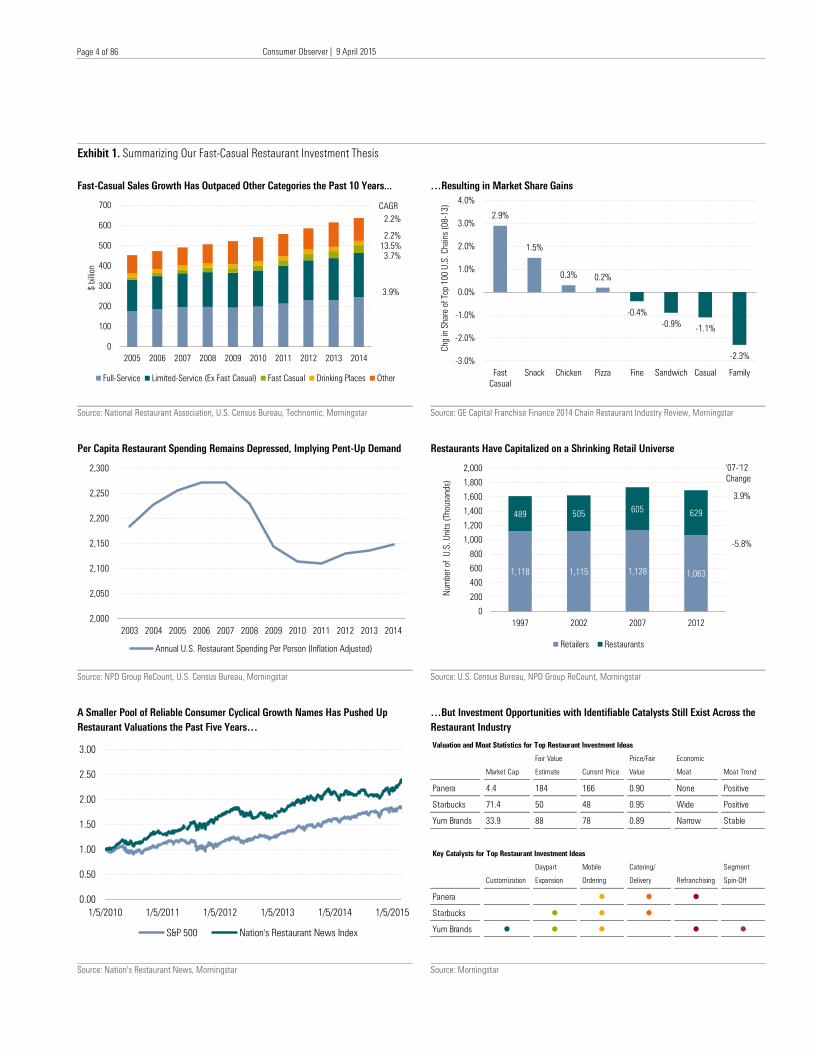

Exhibit 1. Summarizing Our Fast-Casual Restaurant Investment Thesis

Fast-Casual Sales Growth Has Outpaced Other Categories the Past 10 Years... …Resulting in Market Share Gains

Source: National Restaurant Association, U.S. Census Bureau, Technomic, Morningstar Source: GE Capital Franchise Finance 2014 Chain Restaurant Industry Review, Morningstar

Per Capita Restaurant Spending Remains Depressed, Implying Pent-Up Demand Restaurants Have Capitalized on a Shrinking Retail Universe

Source: NPD Group ReCount, U.S. Census Bureau, Morningstar Source: U.S. Census Bureau, NPD Group ReCount, Morningstar

A Smaller Pool of Reliable Consumer Cyclical Growth Names Has Pushed Up

Restaurant Valuations the Past Five Years…

…But Investment Opportunities with Identifiable Catalysts Still Exist Across the

Restaurant Industry

Source: Nation's Restaurant News, Morningstar Source: Morningstar

0

100

200

300

400

500

600

700

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

$ b

illion

Full-Service Limited-Service (Ex Fast Casual) Fast Casual Drinking Places Other

CAGR

2.2%

2.2%

13.5%

3.7%

3.9%

2.9%

1.5%

0.3% 0.2%

-0.4%

-0.9%-1.1%

-2.3%-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

Fast

Casual

Snack Chicken Pizza Fine Sandwich Casual Family

Chg in S

hare o

f Top 1

00

U.S

. C

hain

s (

08

-1

3)

2,000

2,050

2,100

2,150

2,200

2,250

2,300

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Annual U.S. Restaurant Spending Per Person (Inflation Adjusted)

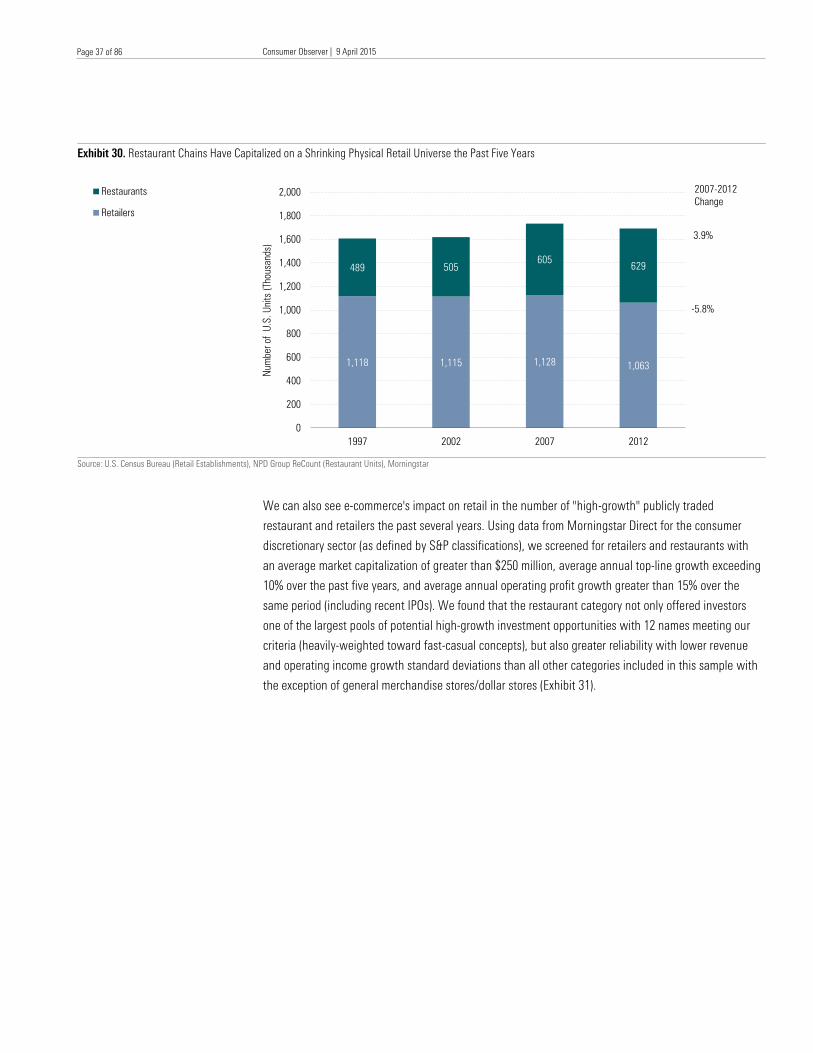

1,118 1,115 1,128 1,063

489 505605

629

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1997 2002 2007 2012

Num

ber o

f U

.S.

Unit

s (

Thousands)

Retailers Restaurants

'07-'12

Change

3.9%

-5.8%

0.00

0.50

1.00

1.50

2.00

2.50

3.00

1/5/2010 1/5/2011 1/5/2012 1/5/2013 1/5/2014 1/5/2015

S&P 500 Nation's Restaurant News Index

Valuation and Moat Statistics for Top Restaurant Investment Ideas

Market Cap

Fair Value

Estimate Current Price

Price/Fair

Value

Economic

Moat Moat Trend

Panera 4.4 184 166 0.90 None Positive

Starbucks 71.4 50 48 0.95 Wide Positive

Yum Brands 33.9 88 78 0.89 Narrow Stable

Key Catalysts for Top Restaurant Investment Ideas

Customization

Daypart

Expansion

Mobile

Ordering

Catering/

Delivery Refranchising

Segment

Spin-Off

Panera l l l

Starbucks l l l

Yum Brands l l l l l

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 5 of 86

Page 5 of 86

Best Ideas

Below, we've highlighted a handful of investment ideas that we believe are well-positioned to capitalize

on the themes we've discussed or are insulated from disruptive changes in the industry. Each company

has a wide or narrow moat and/or a positive moat trend and trades at a discount to our fair value

estimate.

Panera

Accelerating restaurant guest counts give us greater conviction that "Panera 2.0" customer-experience

investments—peak-hour throughput capacity, more accessible prices, new marketing tactics, and digital

ordering—can drive sustainable top-line momentum. We're also optimistic about Panera's new growth

avenues such as delivery and catering hubs, consumer packaged goods, and its usage of mobile devices

and other digital technology to engage with consumers and improve store-level operations, all of which

are poised to become more meaningful cash-flow contributors. The costs of these investments are

expected to weigh on profitability through 2015. However, as comparable transaction trends continue to

improve and customer-experience investments wind down, we believe Panera's longer-term margin

opportunities will become more apparent. Looking beyond 2015, however, our model assumes low- to

mid-single-digit comps (even in light of increased fast-casual competition), resulting in roughly 9%

average annual revenue growth. During that same time horizon, we expect restaurant-level margins to

grow to the 21% range compared with 17.9% in 2014, with operating margins expanding to around 16%

driven by higher-margin menu additions (including a mix shift to the breakfast daypart), increased fixed-

cost leverage, a vertically integrated supply chain, and contribution from catering and delivery

operations.

In addition, Panera's refranchising efforts—including plans to refranchise 50-150 locations this year and

expand franchise ownership to 55%-65% of the system over time —comes on the heels of similar

announcements across the industry and could accelerate Panera 2.0 conversions while allowing

management to focus more on brand, menu innovation, and marketing efficacy

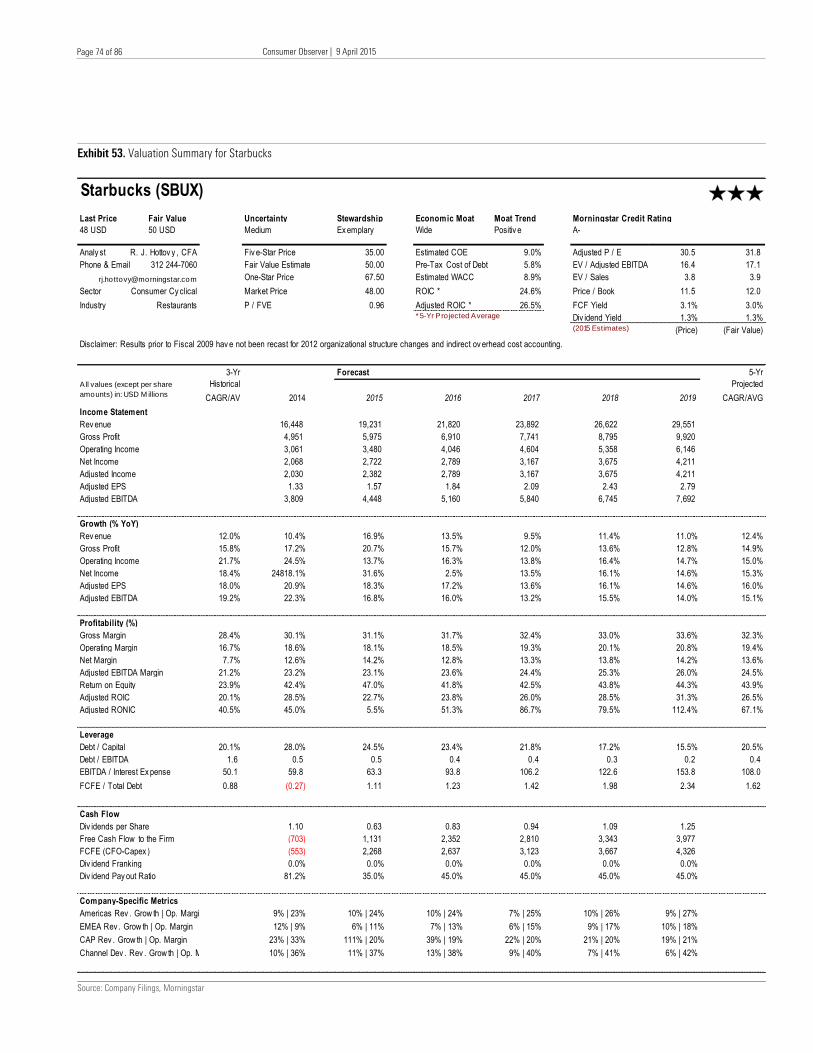

Starbucks

We view Starbucks as one of the most compelling growth stories in the consumer space today, poised

for top-line growth and margin expansion through menu innovations, sustainable cost advantages, and

its evolution into a diversified retail and consumer packaged goods platform. Although it is already the

leading specialty coffee retailer in the U.S., we believe Starbucks has meaningful domestic growth

potential, including new store formats (smaller-format express stores, drive-thrus, beverage trucks, and

square footage reallocation for its premium Starbucks Reserve sub-brand), greater peak-hour capacity,

expanded food offerings, lunch/evening daypart expansion, mobile payments and delivery, and My

Starbucks Rewards usage. At a time when most restaurants and retailers are struggling to stimulate

traffic growth, Starbucks' recent transaction gains suggest that it remains a key consumer destination,

validating the strength of its brand intangible asset.

Starbucks is much more than a retail story, however, and we believe it is just starting to scratch the

surface of its longer-term channel development, brand diversification, and geographic expansion

potential. Many of Starbucks' core retail competitive advantages should extend into these efforts,

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 6 of 86

Page 6 of 86

putting the company in a unique position to capture retail and wholesale market share. Platforms like

VIA Instant coffee and K-Cups should support channel diversification efforts over the medium term, with

nascent brands like Teavana, La Boulange, and Evolution Fresh becoming important cash flow

contributors over an extended horizon. We're also optimistic about mobile, digital, and loyalty program

synergies across the various business lines. Starbucks' international growth opportunities are

undeniable--particularly in China, India, Japan, and Brazil--and we believe best practices from its U.S.

operations can be applied to these regions to drive future growth. Competitive threats exist in both the

retail and wholesale channels, but we believe a wide moat founded on strong brand equity, bargaining

clout with suppliers of all kinds, and an increasingly leverageable model will be enough to stave off

rivals.

Yum Brands

Although rivalry among quick-service restaurants is on the rise globally, we believe Yum Brands offers

investors an intriguing long-term global growth alternative. Our optimism stems from a narrow economic

moat derived from strong brand intangible assets in KFC, Pizza Hut, and Taco Bell as well as a scalable

franchise business model. Although Greg Creed assumed the reins from longtime CEO David Novak at

the beginning of the year, we believe Yum's playbook will remain the same: Combine unit growth and

same-store sales layers to drive systemwide sales, increase operating leverage, and bolster returns on

capital. This approach has served Yum well in the past and should help it withstand an evolving

restaurant category marked by new sources of competition and changing consumer preferences and

tastes.

Yum China comps have remained under pressure in early 2015 amid concerns about improper food

handling practices at one of the region's key beef and poultry suppliers, but we believe its brands can

withstand these issues through quality-assurance marketing and menu revamps. We remain optimistic

about Yum China's long-term potential because of its established distribution infrastructure and local

site-development teams, and we generally find management's division goal of 20% restaurant margins

and 15% normalized operating income growth reachable through low-double-digit unit growth, midteen

system sales growth, and moderate general and administrative expense leverage, partly tempered by

promotional activity and labor cost inflation.

With roughly 40% of Yum's operating income coming from China, the stock is tied to market perceptions

of macro and consumer trends in the region. However, we view Yum as more than a China story and

encourage investors to evaluate Yum's other divisions. With KFC, Pizza Hut, and Taco Bell consolidated

by brand in every region except China and India, we have started to see increased unit and comp growth

with margin expansion via centralized brand support and best-practice sharing across regions. Coupled

with a goal of 95% system franchisee ownership by 2017 (excluding China and India), we view

management's long-term goal of companywide 10% operating income growth as achievable. K

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 7 of 86

Page 7 of 86

Executive Summary

Restaurants have been one of the most dynamic industries within the broader consumer cyclical sector

during the past several years, influenced by a wide range of company, industry, and macroeconomic

factors. Retracing the past five years within the category, we believe many of the beneficiaries of these

industry changes can be found in the fast-casual restaurant category, whose participants offer higher-

quality ingredients and command greater pricing power than traditional quick-service chains but are

more cost-effective to operate than casual-dining restaurants due to smaller formats but higher-

throughput locations lacking a traditional waitstaff. The fast-casual category has been the sweet spot

within the restaurant category in recent years, outpacing the other categories and creating a ripple

effect across much of the restaurant industry, with traditionally more affluent QSR patrons gravitating to

fast-casual chains and the pricing power of many of CDR chains deteriorating as they resort to more

aggressive discounting to remain competitive.

In this section of this report, we examine the industry changes driving the success of fast-casual

restaurants in greater detail, the sustainability of these trends, and the implications for pricing power

(and by extension, economic moats) for the rest of the restaurant industry.

Key Takeaways

× Fast-casual restaurants have better adjusted to changes in consumer behavior the past several years,

including increased spending power among minority groups and millennials (which has created demand

for a wider variety of flavors, better-for-you products, and locally sourced food), evolving views about in-

restaurant experiences (resulting in consumer calls for customizable menus and faster throughput), and

widespread advances in consumer-facing technologies (leading to mobile-based ordering, payment, and

loyalty programs as well as in-restaurant wireless offerings).

× More important, consumers aren't just willing to visit fast-casual chains more frequently; they're also

willing to pay premium prices for the product and restaurant experience. Restaurants that have stayed

ahead of changing consumer preferences have also experienced a meaningful increase in average

checks the past five years, while the increase for traditional QSR players have been more muted. In our

view, the increase in average checks suggests greater pricing power, and by extension, a strengthening

of the brand intangible asset source that we consider when evaluating economic moats among retailers

and restaurants.

× The ability to adapt to evolving consumer preferences and the subsequent pricing power was a key

consideration behind the positive moat trends we've assigned to fast-casual players such as Chipotle

and Panera as well as Starbucks. Likewise, the inability to react to these changes was a factor in our

negative moat trend for McDonald's and the removal of our narrow moat rating for Darden.

Fast-Casual Has Reshaped Preferences Across the Restaurant Category, Resulting in Material Changes in Industry Pricing Power

R. J. Hottovy, CFA

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 8 of 86

Page 8 of 86

Evolving Consumer Preferences Are At the Root of Fast-Casual Restaurant Growth

We attribute much of the success of fast-casual chains the past several years to their ability to adapt to

evolving consumer expectations across the restaurant industry. Many of these consumer changes are

characteristic of larger consumer industry trends, including increased spending power among minority

groups and millennials (which has created demand for a wider variety of flavors, better-for-you products,

and locally sourced food), evolving views about in-restaurant experiences (resulting in consumer calls for

customizable menu offerings products and faster throughput), and widespread advances in consumer-

facing technologies (leading to mobile-based ordering, payment, and loyalty programs as well as in-

restaurant wireless offerings). The impact of these changes among consumer behaviors has been

widespread, leaving many established restaurant players playing catch-up.

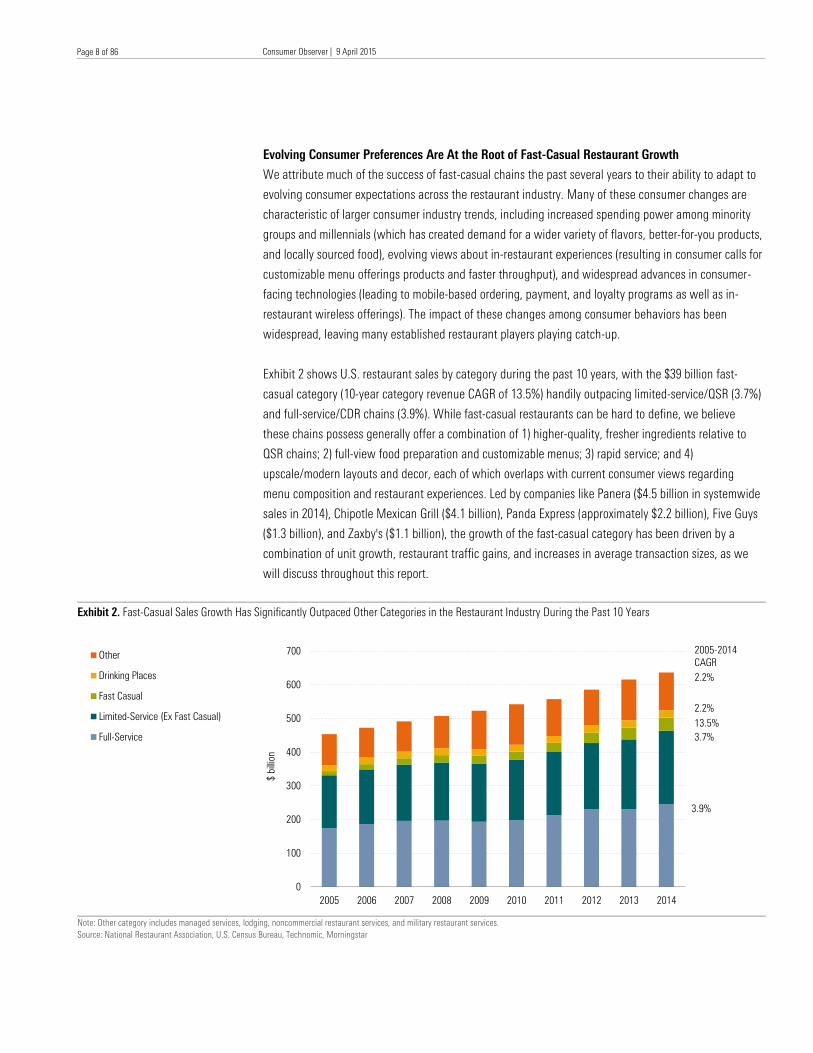

Exhibit 2 shows U.S. restaurant sales by category during the past 10 years, with the $39 billion fast-

casual category (10-year category revenue CAGR of 13.5%) handily outpacing limited-service/QSR (3.7%)

and full-service/CDR chains (3.9%). While fast-casual restaurants can be hard to define, we believe

these chains possess generally offer a combination of 1) higher-quality, fresher ingredients relative to

QSR chains; 2) full-view food preparation and customizable menus; 3) rapid service; and 4)

upscale/modern layouts and decor, each of which overlaps with current consumer views regarding

menu composition and restaurant experiences. Led by companies like Panera ($4.5 billion in systemwide

sales in 2014), Chipotle Mexican Grill ($4.1 billion), Panda Express (approximately $2.2 billion), Five Guys

($1.3 billion), and Zaxby's ($1.1 billion), the growth of the fast-casual category has been driven by a

combination of unit growth, restaurant traffic gains, and increases in average transaction sizes, as we

will discuss throughout this report.

Exhibit 2. Fast-Casual Sales Growth Has Significantly Outpaced Other Categories in the Restaurant Industry During the Past 10 Years

Note: Other category includes managed services, lodging, noncommercial restaurant services, and military restaurant services.

Source: National Restaurant Association, U.S. Census Bureau, Technomic, Morningstar

0

100

200

300

400

500

600

700

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

$ b

illion

Other

Drinking Places

Fast Casual

Limited-Service (Ex Fast Casual)

Full-Service

2005-2014

CAGR

2.2%

2.2%

13.5%

3.7%

3.9%

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 9 of 86

Page 9 of 86

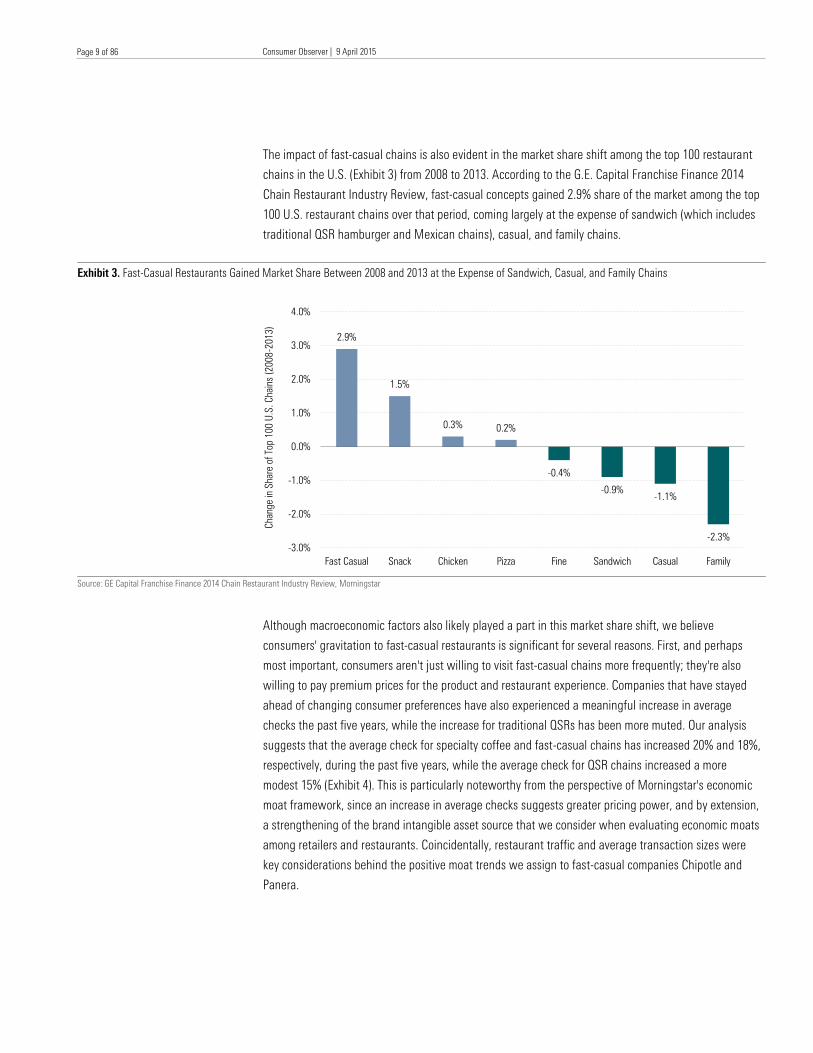

The impact of fast-casual chains is also evident in the market share shift among the top 100 restaurant

chains in the U.S. (Exhibit 3) from 2008 to 2013. According to the G.E. Capital Franchise Finance 2014

Chain Restaurant Industry Review, fast-casual concepts gained 2.9% share of the market among the top

100 U.S. restaurant chains over that period, coming largely at the expense of sandwich (which includes

traditional QSR hamburger and Mexican chains), casual, and family chains.

Exhibit 3. Fast-Casual Restaurants Gained Market Share Between 2008 and 2013 at the Expense of Sandwich, Casual, and Family Chains

Source: GE Capital Franchise Finance 2014 Chain Restaurant Industry Review, Morningstar

Although macroeconomic factors also likely played a part in this market share shift, we believe

consumers' gravitation to fast-casual restaurants is significant for several reasons. First, and perhaps

most important, consumers aren't just willing to visit fast-casual chains more frequently; they're also

willing to pay premium prices for the product and restaurant experience. Companies that have stayed

ahead of changing consumer preferences have also experienced a meaningful increase in average

checks the past five years, while the increase for traditional QSRs has been more muted. Our analysis

suggests that the average check for specialty coffee and fast-casual chains has increased 20% and 18%,

respectively, during the past five years, while the average check for QSR chains increased a more

modest 15% (Exhibit 4). This is particularly noteworthy from the perspective of Morningstar's economic

moat framework, since an increase in average checks suggests greater pricing power, and by extension,

a strengthening of the brand intangible asset source that we consider when evaluating economic moats

among retailers and restaurants. Coincidentally, restaurant traffic and average transaction sizes were

key considerations behind the positive moat trends we assign to fast-casual companies Chipotle and

Panera.

2.9%

1.5%

0.3%0.2%

-0.4%

-0.9%-1.1%

-2.3%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

Fast Casual Snack Chicken Pizza Fine Sandwich Casual Family

Change in S

hare o

f Top 1

00

U.S

. C

hain

s (

20

08

-2

01

3)

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 10 of 86

Page 10 of 86

Exhibit 4. Increase in Average Transaction Size Suggests Greater Pricing Power Among Fast-Casual Chains, Supporting Positive Moat Trends

Source: Company Filings, Morningstar

Over the next few pages, we will highlight many of the changes in consumer behavior that we've

witnessed across the restaurant industry in recent years, many of which have contributed to the success

of fast-casual restaurants and will likely continue in the years to come. We'll also provide more details

about how these changes have distorted pricing power across the industry, with positive and negative

implications for the brand intangible assets behind our economic moat ratings across our restaurant

coverage universe. We'll also dive into the sustainability of these trends; fast-casual restaurants have

been the sweet spot of the restaurant industry during the past several years with respect to both

fundamentals and market valuations, but we believe the more relevant question for investors is whether

this momentum can continue or will there be disruption as traditional chains adapt to industry changes.

0

2

4

6

8

10

12

TH

I 2

009

TH

I 20

14

DN

KN

20

09

DN

KN

20

14

SB

UX

20

09

SB

UX

20

14

MC

D 2

00

9

MC

D 2

01

4

BK

20

09

BK

20

14

Taco B

ell 2

009

Taco B

ell 2

014

JA

CK

200

9

JA

CK

201

4

KFC

20

09

KFC

20

14

SO

NC

20

09

SO

NC

20

14

WEN

20

09

WEN

20

14

Arby's

200

9

Arby's

201

4

PB

PB

2009

PB

PB

201

4

Chic

k-Fil-A

200

9

Chic

k-Fil-A

201

4

ZO

ES

20

09

ZO

ES

20

14

PN

RA

200

9

PN

RA

201

4

Qdoba 2

009

Qdoba 2

014

CM

G 2

00

9

CM

G 2

01

4

Average C

heck

Average Category

Check 2009

Average Category

Check 2014

Coffee Ö 20%

Quick-Service Ö 15%

Fast-Casual Ö 18%

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 11 of 86

Page 11 of 86

Trend: Backed by Changes in Purchasing Power, Consumers Are Demanding Menu Innovations

and Flavors

At the risk of stating the obvious, we believe taste is still the most important factor when consumers

make restaurant purchase decisions. However, we believe that one of the underrated but also more

impactful changes in restaurant spending trends in recent years is a shift in general taste preferences,

with consumers increasingly demanding nontraditional ingredients, new flavors, and spicier fare. It's

difficult to chalk up these changes to a single factor; instead, we attribute changing consumer tastes to

a number of sources, including greater spending power among minorities, heightened demand for

healthier, or better-for-you, offerings, increased television programming devoted to food, the

globalization of restaurant concepts and sharing menu innovations across borders, and the influence of

social media.

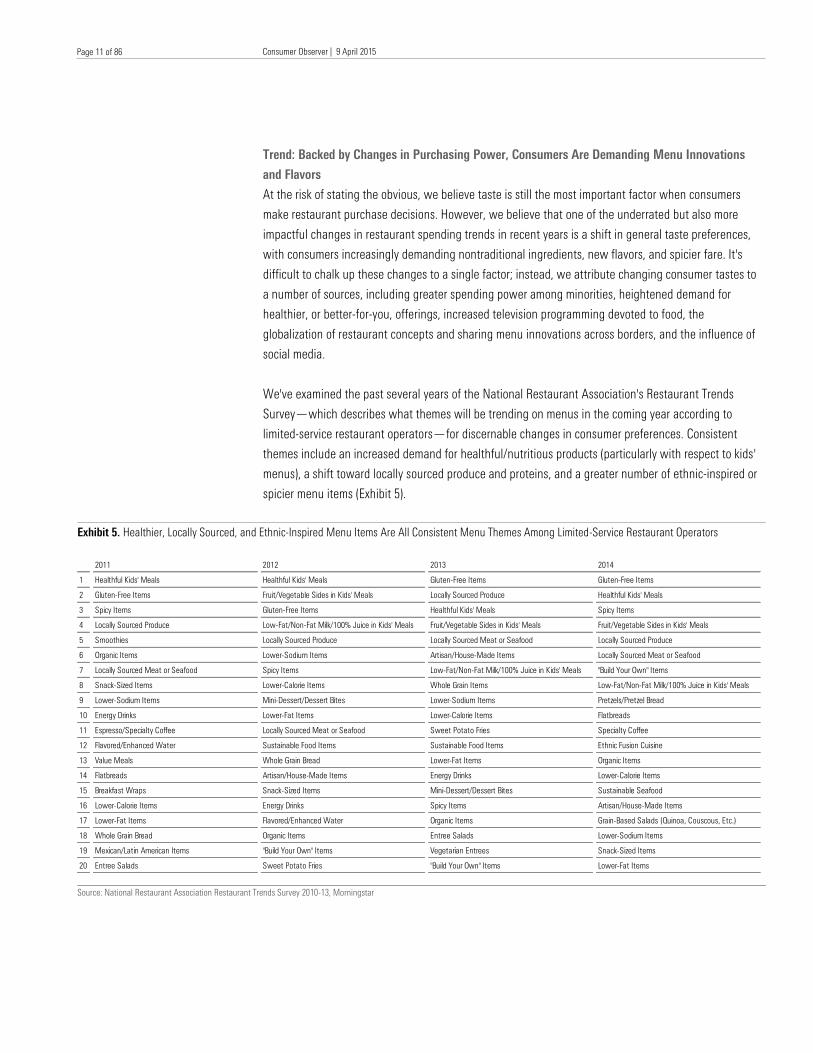

We've examined the past several years of the National Restaurant Association's Restaurant Trends

Survey—which describes what themes will be trending on menus in the coming year according to

limited-service restaurant operators—for discernable changes in consumer preferences. Consistent

themes include an increased demand for healthful/nutritious products (particularly with respect to kids'

menus), a shift toward locally sourced produce and proteins, and a greater number of ethnic-inspired or

spicier menu items (Exhibit 5).

Exhibit 5. Healthier, Locally Sourced, and Ethnic-Inspired Menu Items Are All Consistent Menu Themes Among Limited-Service Restaurant Operators

Source: National Restaurant Association Restaurant Trends Survey 2010-13, Morningstar

2011 2012 2013 2014

1 Healthful Kids' Meals Healthful Kids' Meals Gluten-Free Items Gluten-Free Items

2 Gluten-Free Items Fruit/Vegetable Sides in Kids' Meals Locally Sourced Produce Healthful Kids' Meals

3 Spicy Items Gluten-Free Items Healthful Kids' Meals Spicy Items

4 Locally Sourced Produce Low-Fat/Non-Fat Milk/100% Juice in Kids' Meals Fruit/Vegetable Sides in Kids' Meals Fruit/Vegetable Sides in Kids' Meals

5 Smoothies Locally Sourced Produce Locally Sourced Meat or Seafood Locally Sourced Produce

6 Organic Items Lower-Sodium Items Artisan/House-Made Items Locally Sourced Meat or Seafood

7 Locally Sourced Meat or Seafood Spicy Items Low-Fat/Non-Fat Milk/100% Juice in Kids' Meals "Build Your Own" Items

8 Snack-Sized Items Lower-Calorie Items Whole Grain Items Low-Fat/Non-Fat Milk/100% Juice in Kids' Meals

9 Lower-Sodium Items Mini-Dessert/Dessert Bites Lower-Sodium Items Pretzels/Pretzel Bread

10 Energy Drinks Lower-Fat Items Lower-Calorie Items Flatbreads

11 Espresso/Specialty Coffee Locally Sourced Meat or Seafood Sweet Potato Fries Specialty Coffee

12 Flavored/Enhanced Water Sustainable Food Items Sustainable Food Items Ethnic Fusion Cuisine

13 Value Meals Whole Grain Bread Lower-Fat Items Organic Items

14 Flatbreads Artisan/House-Made Items Energy Drinks Lower-Calorie Items

15 Breakfast Wraps Snack-Sized Items Mini-Dessert/Dessert Bites Sustainable Seafood

16 Lower-Calorie Items Energy Drinks Spicy Items Artisan/House-Made Items

17 Lower-Fat Items Flavored/Enhanced Water Organic Items Grain-Based Salads (Quinoa, Couscous, Etc.)

18 Whole Grain Bread Organic Items Entree Salads Lower-Sodium Items

19 Mexican/Latin American Items "Build Your Own" Items Vegetarian Entrees Snack-Sized Items

20 Entree Salads Sweet Potato Fries "Build Your Own" Items Lower-Fat Items

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 12 of 86

Page 12 of 86

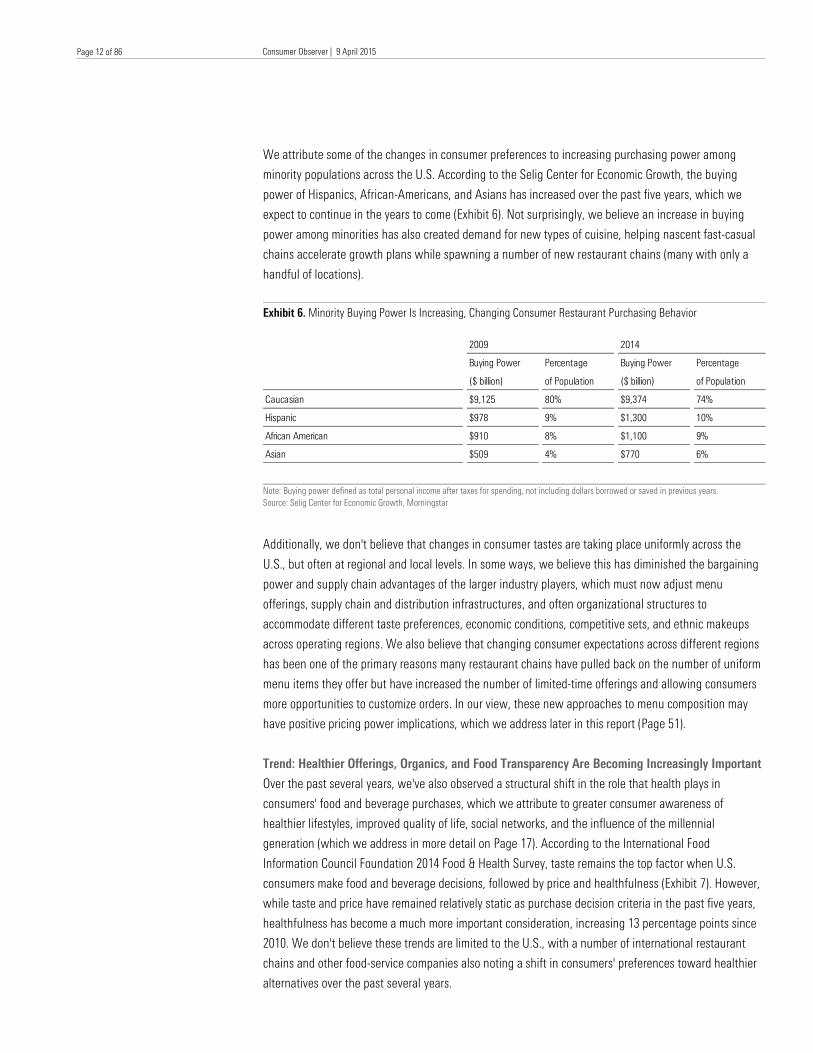

We attribute some of the changes in consumer preferences to increasing purchasing power among

minority populations across the U.S. According to the Selig Center for Economic Growth, the buying

power of Hispanics, African-Americans, and Asians has increased over the past five years, which we

expect to continue in the years to come (Exhibit 6). Not surprisingly, we believe an increase in buying

power among minorities has also created demand for new types of cuisine, helping nascent fast-casual

chains accelerate growth plans while spawning a number of new restaurant chains (many with only a

handful of locations).

Exhibit 6. Minority Buying Power Is Increasing, Changing Consumer Restaurant Purchasing Behavior

Note: Buying power defined as total personal income after taxes for spending, not including dollars borrowed or saved in previous years.

Source: Selig Center for Economic Growth, Morningstar

Additionally, we don't believe that changes in consumer tastes are taking place uniformly across the

U.S., but often at regional and local levels. In some ways, we believe this has diminished the bargaining

power and supply chain advantages of the larger industry players, which must now adjust menu

offerings, supply chain and distribution infrastructures, and often organizational structures to

accommodate different taste preferences, economic conditions, competitive sets, and ethnic makeups

across operating regions. We also believe that changing consumer expectations across different regions

has been one of the primary reasons many restaurant chains have pulled back on the number of uniform

menu items they offer but have increased the number of limited-time offerings and allowing consumers

more opportunities to customize orders. In our view, these new approaches to menu composition may

have positive pricing power implications, which we address later in this report (Page 51).

Trend: Healthier Offerings, Organics, and Food Transparency Are Becoming Increasingly Important

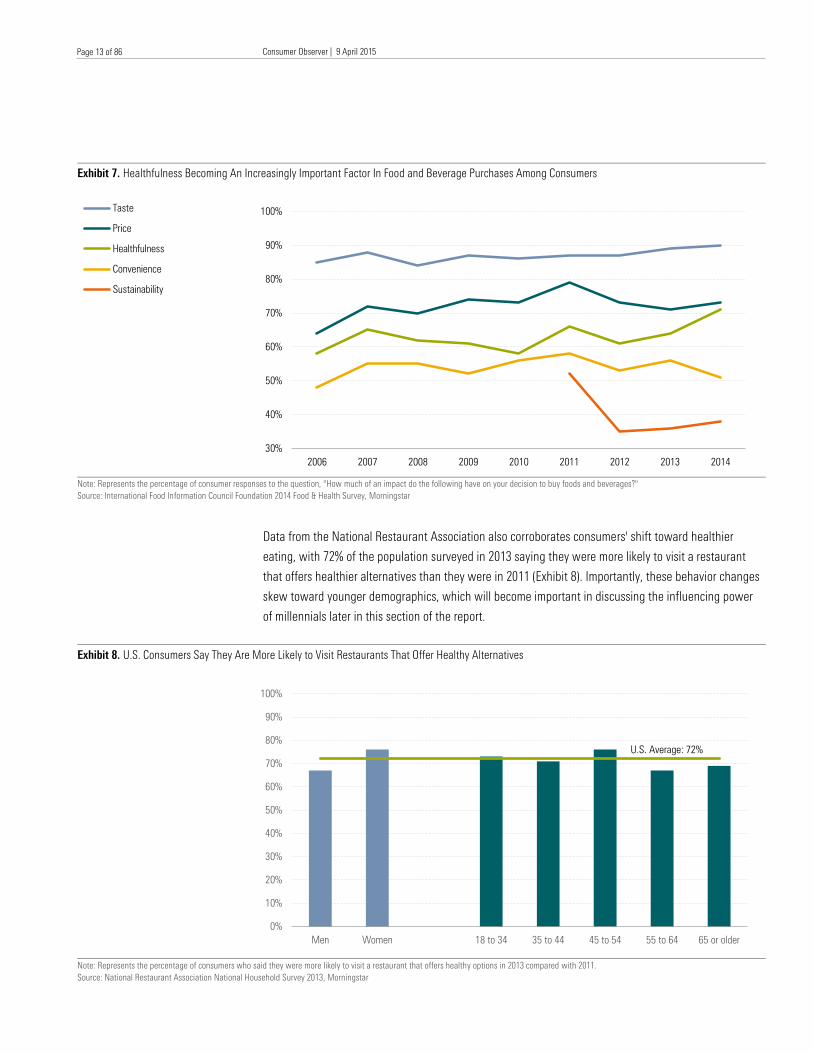

Over the past several years, we've also observed a structural shift in the role that health plays in

consumers' food and beverage purchases, which we attribute to greater consumer awareness of

healthier lifestyles, improved quality of life, social networks, and the influence of the millennial

generation (which we address in more detail on Page 17). According to the International Food

Information Council Foundation 2014 Food & Health Survey, taste remains the top factor when U.S.

consumers make food and beverage decisions, followed by price and healthfulness (Exhibit 7). However,

while taste and price have remained relatively static as purchase decision criteria in the past five years,

healthfulness has become a much more important consideration, increasing 13 percentage points since

2010. We don't believe these trends are limited to the U.S., with a number of international restaurant

chains and other food-service companies also noting a shift in consumers' preferences toward healthier

alternatives over the past several years.

2009 2014

Buying Power

($ billion)

Percentage

of Population

Buying Power

($ billion)

Percentage

of Population

Caucasian $9,125 80% $9,374 74%

Hispanic $978 9% $1,300 10%

African American $910 8% $1,100 9%

Asian $509 4% $770 6%

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 13 of 86

Page 13 of 86

Exhibit 7. Healthfulness Becoming An Increasingly Important Factor In Food and Beverage Purchases Among Consumers

Note: Represents the percentage of consumer responses to the question, "How much of an impact do the following have on your decision to buy foods and beverages?"

Source: International Food Information Council Foundation 2014 Food & Health Survey, Morningstar

Data from the National Restaurant Association also corroborates consumers' shift toward healthier

eating, with 72% of the population surveyed in 2013 saying they were more likely to visit a restaurant

that offers healthier alternatives than they were in 2011 (Exhibit 8). Importantly, these behavior changes

skew toward younger demographics, which will become important in discussing the influencing power

of millennials later in this section of the report.

Exhibit 8. U.S. Consumers Say They Are More Likely to Visit Restaurants That Offer Healthy Alternatives

Note: Represents the percentage of consumers who said they were more likely to visit a restaurant that offers healthy options in 2013 compared with 2011.

Source: National Restaurant Association National Household Survey 2013, Morningstar

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014

Taste

Price

Healthfulness

Convenience

Sustainability

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Men Women 18 to 34 35 to 44 45 to 54 55 to 64 65 or older

U.S. Average: 72%

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 14 of 86

Page 14 of 86

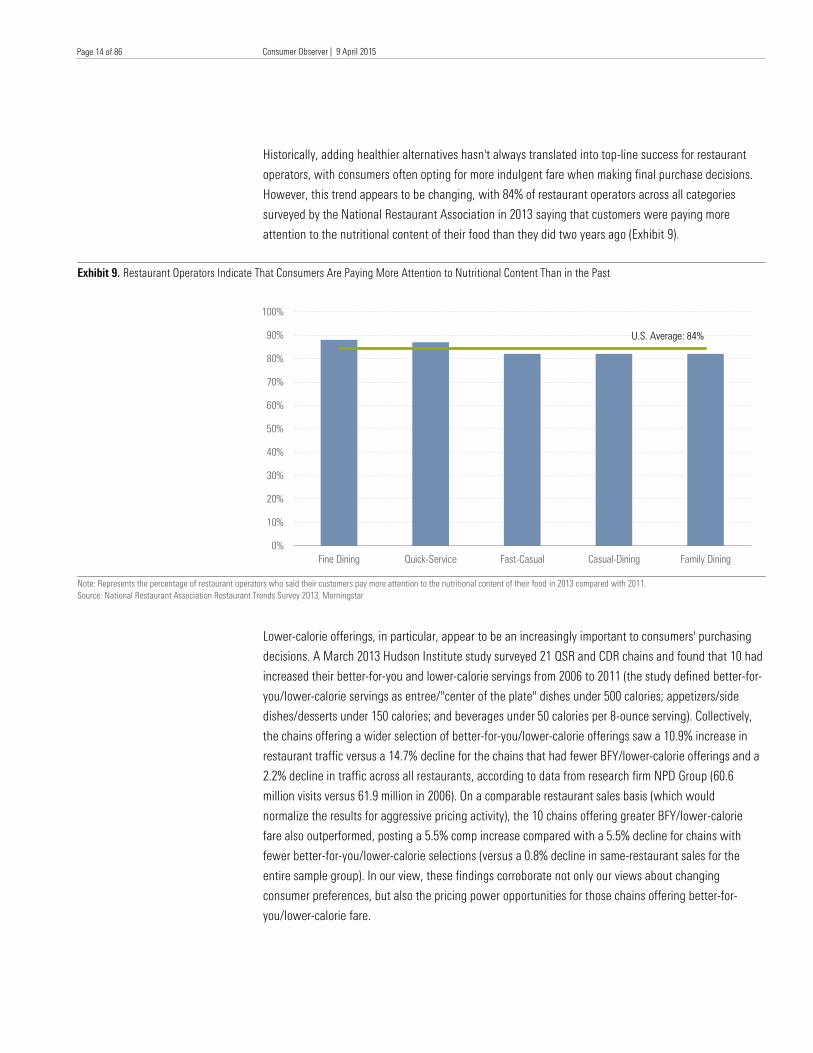

Historically, adding healthier alternatives hasn't always translated into top-line success for restaurant

operators, with consumers often opting for more indulgent fare when making final purchase decisions.

However, this trend appears to be changing, with 84% of restaurant operators across all categories

surveyed by the National Restaurant Association in 2013 saying that customers were paying more

attention to the nutritional content of their food than they did two years ago (Exhibit 9).

Exhibit 9. Restaurant Operators Indicate That Consumers Are Paying More Attention to Nutritional Content Than in the Past

Note: Represents the percentage of restaurant operators who said their customers pay more attention to the nutritional content of their food in 2013 compared with 2011.

Source: National Restaurant Association Restaurant Trends Survey 2013, Morningstar

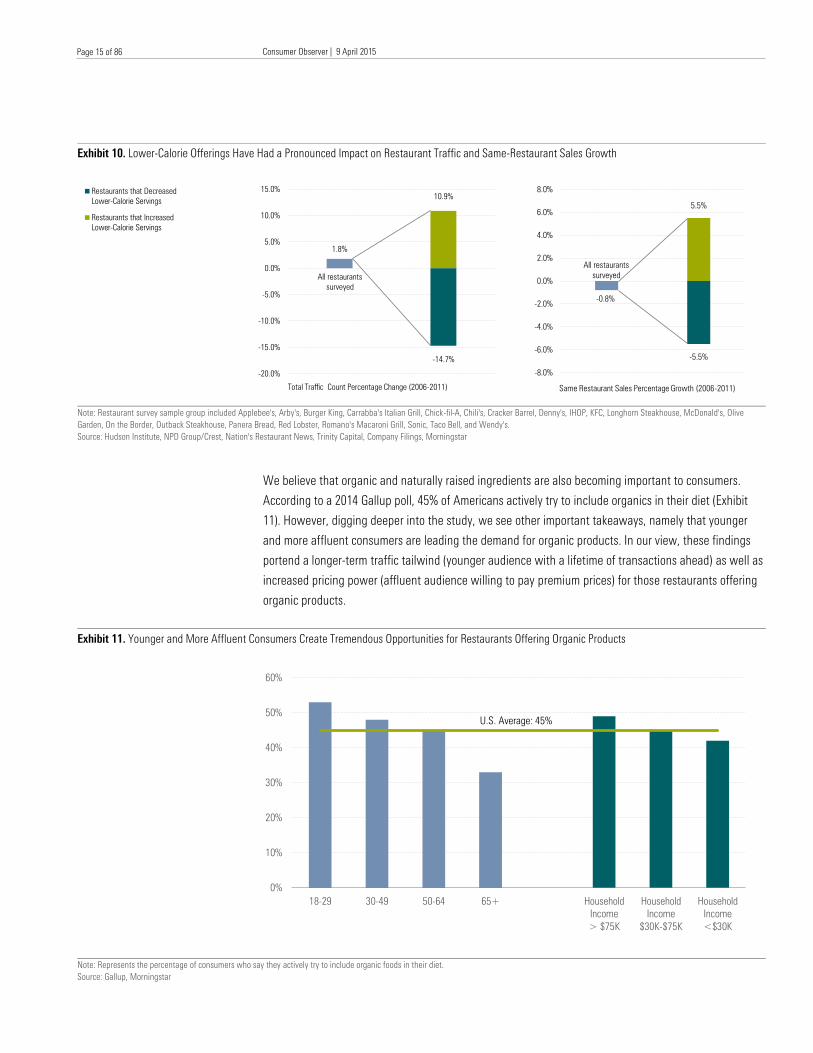

Lower-calorie offerings, in particular, appear to be an increasingly important to consumers' purchasing

decisions. A March 2013 Hudson Institute study surveyed 21 QSR and CDR chains and found that 10 had

increased their better-for-you and lower-calorie servings from 2006 to 2011 (the study defined better-for-

you/lower-calorie servings as entree/"center of the plate" dishes under 500 calories; appetizers/side

dishes/desserts under 150 calories; and beverages under 50 calories per 8-ounce serving). Collectively,

the chains offering a wider selection of better-for-you/lower-calorie offerings saw a 10.9% increase in

restaurant traffic versus a 14.7% decline for the chains that had fewer BFY/lower-calorie offerings and a

2.2% decline in traffic across all restaurants, according to data from research firm NPD Group (60.6

million visits versus 61.9 million in 2006). On a comparable restaurant sales basis (which would

normalize the results for aggressive pricing activity), the 10 chains offering greater BFY/lower-calorie

fare also outperformed, posting a 5.5% comp increase compared with a 5.5% decline for chains with

fewer better-for-you/lower-calorie selections (versus a 0.8% decline in same-restaurant sales for the

entire sample group). In our view, these findings corroborate not only our views about changing

consumer preferences, but also the pricing power opportunities for those chains offering better-for-

you/lower-calorie fare.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Fine Dining Quick-Service Fast-Casual Casual-Dining Family Dining

U.S. Average: 84%

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 15 of 86

Page 15 of 86

Exhibit 10. Lower-Calorie Offerings Have Had a Pronounced Impact on Restaurant Traffic and Same-Restaurant Sales Growth

Note: Restaurant survey sample group included Applebee's, Arby's, Burger King, Carrabba's Italian Grill, Chick-fil-A, Chili's, Cracker Barrel, Denny's, IHOP, KFC, Longhorn Steakhouse, McDonald's, Olive

Garden, On the Border, Outback Steakhouse, Panera Bread, Red Lobster, Romano's Macaroni Grill, Sonic, Taco Bell, and Wendy's.

Source: Hudson Institute, NPD Group/Crest, Nation's Restaurant News, Trinity Capital, Company Filings, Morningstar

We believe that organic and naturally raised ingredients are also becoming important to consumers.

According to a 2014 Gallup poll, 45% of Americans actively try to include organics in their diet (Exhibit

11). However, digging deeper into the study, we see other important takeaways, namely that younger

and more affluent consumers are leading the demand for organic products. In our view, these findings

portend a longer-term traffic tailwind (younger audience with a lifetime of transactions ahead) as well as

increased pricing power (affluent audience willing to pay premium prices) for those restaurants offering

organic products.

Exhibit 11. Younger and More Affluent Consumers Create Tremendous Opportunities for Restaurants Offering Organic Products

Note: Represents the percentage of consumers who say they actively try to include organic foods in their diet.

Source: Gallup, Morningstar

1.8%

10.9%

-14.7%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

Total Traffic Count Percentage Change (2006-2011)

Restaurants that Decreased

Lower-Calorie Servings

Restaurants that Increased

Lower-Calorie Servings

All restaurants

surveyed

5.5%

-0.8%

-5.5%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

Same Restaurant Sales Percentage Growth (2006-2011)

Restaurants that Decreased

Lower-Calorie Servings

Restaurants that Increased

Lower-Calorie Servings

All restaurants

surveyed

0%

10%

20%

30%

40%

50%

60%

18-29 30-49 50-64 65+ Household

Income

> $75K

Household

Income

$30K-$75K

Household

Income

<$30K

U.S. Average: 45%

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 16 of 86

Page 16 of 86

Through its "Food with Integrity" mantra, Chipotle has been at the forefront of the industry movement

toward naturally raised proteins, dairy products from pasture-raised cattle, and organic produce. Though

more costly to source than processed food, these fresh ingredients are a key source of differentiation

and play a part in the brand intangible asset source underpinning our narrow moat rating. Additionally,

by sourcing naturally raised and organic products—often from local ranchers and farmers—Chipotle

has more clout with its suppliers than chains of comparable size (though we have not assigned the

company a cost advantage moat source given its smaller size relative to larger QSR firms).

We believe the success of Chipotle's Food with Integrity has triggered similar movements in the broader

restaurant industry, starting with other fast-casual companies like Panera (whose food-policy statement

advocates removing artificial trans fats, eliminating artificial colors, sweeteners, flavors, and

preservatives, and purchasing only livestock and poultry that have been raised responsibly) and Zoe's

Kitchen but more recently expanding to traditional QSR chains like McDonald's (which recently

announced that it would serve antibiotic-free chicken) and Dunkin' Brands (which announced a

commitment to cage-free eggs and gestation-crate-free pork in the U.S over the next several years).

Given the positive traffic and pricing power implications, we would not be surprised to see organic and

naturally raised ingredients incorporated into menus industrywide in the years to come.

Consumer behavior regarding organic and naturally raised ingredients also substantiate analysis from

Morningstar's February 2015 Consumer Defensive Observer piece "Robust Organic Food Growth Poised

to Bolster Defensive Retailers' Edge, but Could Detract From Consumer Product Firms' Moats," which

concluded that outlets specializing in organic and naturally raised products can extend the pricing power

inherent in brand intangible assets, drive incremental traffic, and bolster economies of scale.

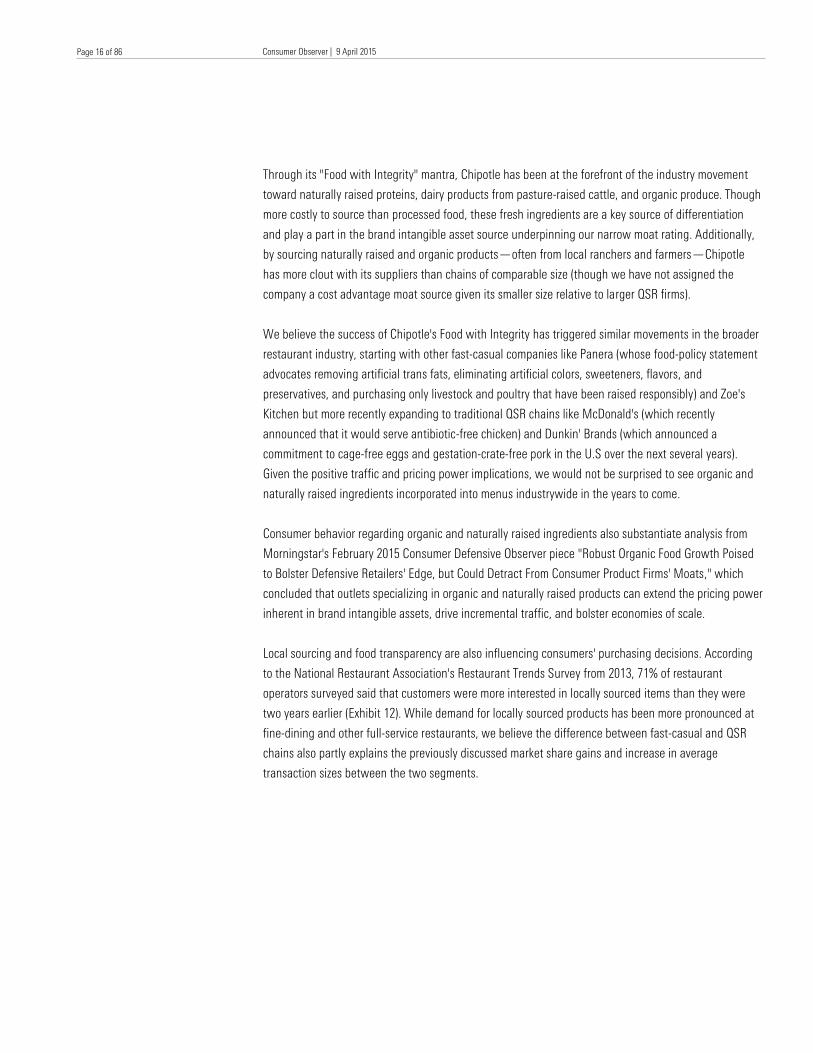

Local sourcing and food transparency are also influencing consumers' purchasing decisions. According

to the National Restaurant Association's Restaurant Trends Survey from 2013, 71% of restaurant

operators surveyed said that customers were more interested in locally sourced items than they were

two years earlier (Exhibit 12). While demand for locally sourced products has been more pronounced at

fine-dining and other full-service restaurants, we believe the difference between fast-casual and QSR

chains also partly explains the previously discussed market share gains and increase in average

transaction sizes between the two segments.

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 17 of 86

Page 17 of 86

Exhibit 12. Restaurant Operator Surveys Indicate That Consumers Are More Interested in Locally Sourced Items Than They Were Two Years Ago

Note: Represents the percentage of restaurant operators who said their customers were more interested in locally sourced items in 2013 compared with 2011.

Source: National Restaurant Association Restaurant Trends Survey 2013, Morningstar

Trend: The Influencing Power of Millennials

We also believe that the generational shift from baby boomer to millennial spending will continue to

have positive implications for some restaurants and negative consequences for others. Not surprisingly,

we expect fast-casual players to remain beneficiaries of millennials' increased spending power, but we

also believe that other traditional restaurant chains have an opportunity to adjust their menus and in-

restaurant experiences to better align with the demands of this critical demographic. In our view,

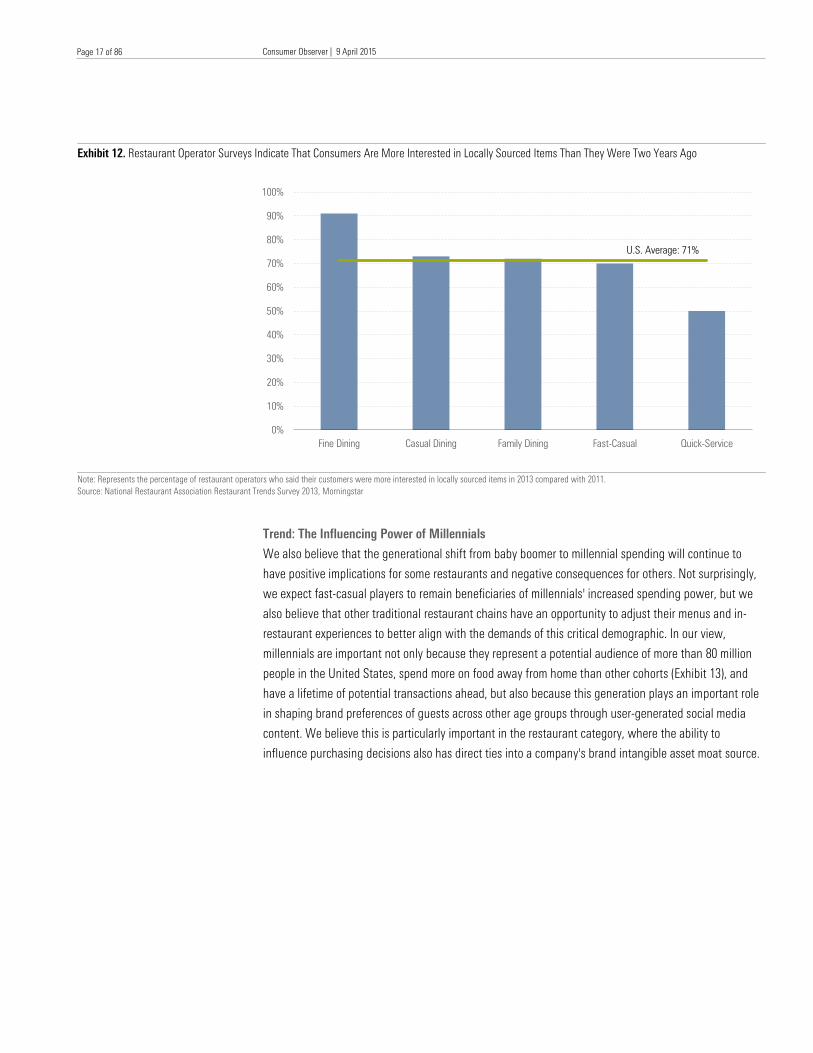

millennials are important not only because they represent a potential audience of more than 80 million

people in the United States, spend more on food away from home than other cohorts (Exhibit 13), and

have a lifetime of potential transactions ahead, but also because this generation plays an important role

in shaping brand preferences of guests across other age groups through user-generated social media

content. We believe this is particularly important in the restaurant category, where the ability to

influence purchasing decisions also has direct ties into a company's brand intangible asset moat source.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Fine Dining Casual Dining Family Dining Fast-Casual Quick-Service

U.S. Average: 71%

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 18 of 86

Page 18 of 86

Exhibit 13. Millennials' Spending on Food Away From Home as a Percentage of Total Food Spending Outpaces Other Generations

Source: U.S. Department of Labor's Bureau of Labor Statistics, Morningstar

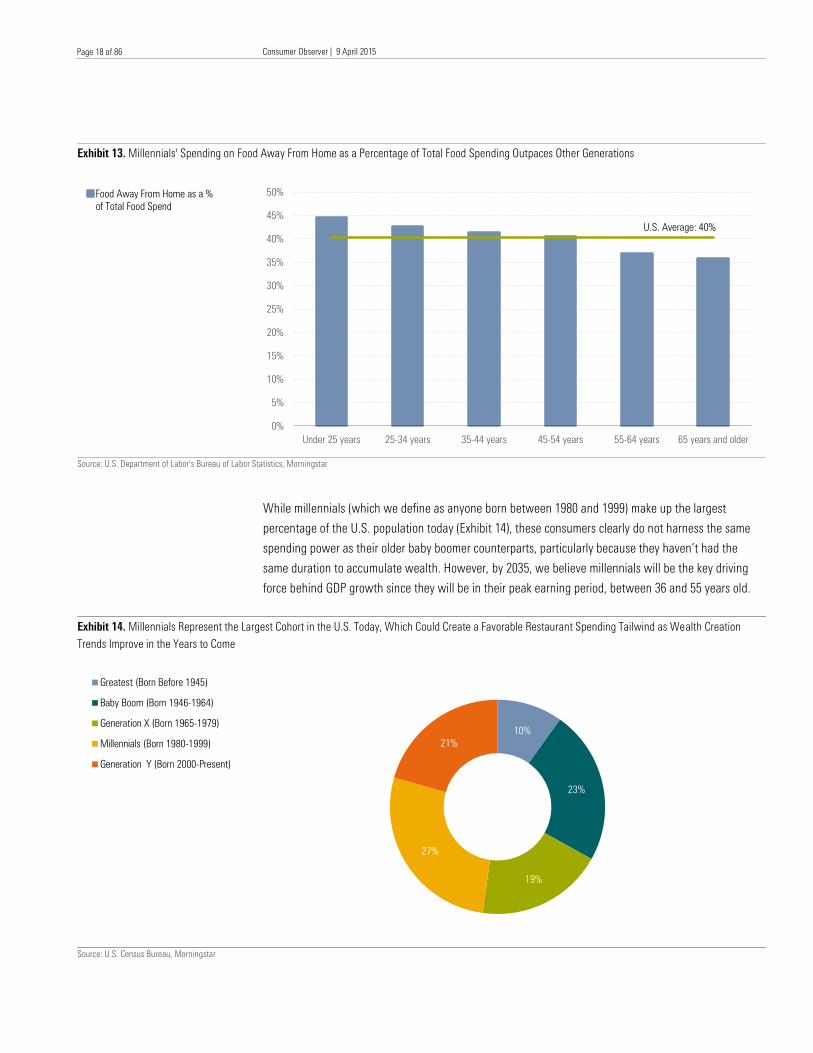

While millennials (which we define as anyone born between 1980 and 1999) make up the largest

percentage of the U.S. population today (Exhibit 14), these consumers clearly do not harness the same

spending power as their older baby boomer counterparts, particularly because they haven’t had the

same duration to accumulate wealth. However, by 2035, we believe millennials will be the key driving

force behind GDP growth since they will be in their peak earning period, between 36 and 55 years old.

Exhibit 14. Millennials Represent the Largest Cohort in the U.S. Today, Which Could Create a Favorable Restaurant Spending Tailwind as Wealth Creation

Trends Improve in the Years to Come

Source: U.S. Census Bureau, Morningstar

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Under 25 years 25-34 years 35-44 years 45-54 years 55-64 years 65 years and older

Food Away From Home as a %

of Total Food Spend

U.S. Average: 40%

10%

23%

19%

27%

21%

Greatest (Born Before 1945)

Baby Boom (Born 1946-1964)

Generation X (Born 1965-1979)

Millennials (Born 1980-1999)

Generation Y (Born 2000-Present)

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 19 of 86

Page 19 of 86

As it pertains to the restaurant industry, the casual-dining category currently holds appeal for baby

boomers, who represent more than 30% of the U.S. spending population (which excludes Generation Y,

or anyone born from 2000 to the present) but account for 35% of all casual-dining traffic in the United

States, according to the U.S. Census Bureau and NPD Group. This is in stark contrast to millennials, who

represent 33% of the spending population but just 24% of casual-dining traffic. This data is also

corroborated by a 2011 study on American millennials conducted by Service Management Group, The

Boston Consulting Group, and Barkley showing that millennials spend a much greater percentage of

total restaurant expenditures at not only fast-casual locations but also fine-dining establishments

(Exhibit 15). In our view, these trends paint a troubling long-term outlook for CDR chains, which have

actually seen fewer visits from millennials over the past five years and are scrambling to address the

problem.

Exhibit 15 Millennials Spend Significantly More at Fast-Casual Restaurants, While Nonmillennials Spend More on Casual Dining

Note: Represents consumers' response to the question, "Of the amount you spend each month [on restaurants], how much do you spend at each type of restaurant?"

Source: American Millennials: Deciphering the Enigma Generation (Service Management Group, The Boston Consulting Group, Barkley), Morningstar

In our view, casual dining's troubles catering to millennials can be traced back to the differences in

consumer expectations we outlined earlier, including increased demand for menu diversity, affordability,

speed of service, and digital connectivity. Most major CDR chains have taken steps to address these

issues over the past two years, including new menu structures accentuated by more entry-level prices or

smaller offerings, nontraditional ingredients, staffing and production changes designed to speed up

service, increased restaurant wireless capabilities, and embracing new technologies such as mobile

payments, text message alerts, or usage of tablets and other handheld in-restaurant devices.

Millennials, to some degree, have also shaped acquisition strategies in this category, with Darden citing

the need to expand beyond the baby boomer generation as a primary reason for acquiring Eddie V's and

Yard House.

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Other

Fine Dining

Fast Casual

Casual Dining

Fast Food

Millennials

Non-Millennials

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 20 of 86

Page 20 of 86

While some of these initiatives will probably improve casual dining's resonance with millennials, we

believe the emergence of fast-casual restaurants has permanently changed the dynamics of the

restaurant industry and will make margin expansion difficult for CDR chains to sustain over an extended

horizon. At its 2013 investor meeting, Darden management noted that the casual-dining guest

experience is not improving fast enough, making premium prices—even after discounting—tougher to

justify. We agree with this sentiment, but we don't expect guest experience improvements to restore the

pricing power these brands once had across all generations. This provides the basis for our negative

moat trend rating for Darden and our generally cautious long-term outlook for much of the casual-dining

industry.

We believe fast-casual restaurants better address the specific demands of millennials, which is the

primary reason that generation spends more eating out than other groups, $174 a month compared with

$153 for nonmillennials, according to the 2011 study detailed in Exhibit 15. We also think there is a

direct correlation between millennial spending and fast-casual restaurant industry growth trends.

In our view, the fast-casual restaurant industry will continue to resonate with millennials in the years to

come. We expect the fast-casual restaurant category to grow nearly 10% during the next five years

because of a compelling consumer value proposition, menu variety, and speed of service as well as unit

economics (lower real estate and labor costs than CDR operators) conducive to accelerated restaurant

opening plans. This exceeds our low-single-digit growth forecast for the broader restaurant industry (we

also discuss our growth forecasts for specific restaurant categories in more detail on Page 47.

The passing of the torch from baby boomers to millennials will also have implications across other

restaurant categories beyond CDRs and fast-casual restaurants. In our view, the fine-dining restaurants

are more likely to benefit from this shift, as millennials have shown a penchant for trading up for special

occasions and bypassing casual dining, which we attribute in part to casual-dining chains' inability to

modify their customer experience for the millennials and the subsequent negativity surrounding many

casual-dining brands. Traditional QSR chains also face some of the brand perception issues that are

plaguing casual-dining restaurants, but we believe these chains will find it easier to modify their menus

and restaurant layouts to more directly align with millennials’ demands (which could create future

pricing opportunities in the process). We've addressed many of these opportunities for traditional QSR

chains in the third section of this report that begins on Page 49.

For additional insights on the potential impact of millennials across several consumer discretionary

categories, please refer to our May 2014 report "Millennials to Power the Next Generation of Leisure

Spending."

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 21 of 86

Page 21 of 86

Trend: Technology Reshaping How Restaurants Reach Customers, Enhance the In-Restaurant

Experience

Almost every restaurant industry investor day presentation we've attended in the past two years has

placed heavy emphasis on the importance of technology in reshaping purchase decisions and enhancing

the customer experience. These innovations include consumer-facing applications (mobile ordering and

payment capabilities, electronic ordering and payments at the table, video menu boards, self-service

kiosks) and front-of-the-house technologies (tablets/handheld devices and other point-of-sale system

software upgrades to manage restaurant throughput levels), and back-of-the-house innovations

(handheld devices to assist with inventory replenishment, special bar-coding to identify food sources,

and other freshness indicators). Technology has also become increasingly relevant to restaurant chains'

marketing plans, with most planning to devote more resources to digital and mobile advertising in 2015,

which has natural marketing synergies with current loyalty programs. In our view, technology

enhancements can help reinforce a restaurant company's brand intangible asset moat source.

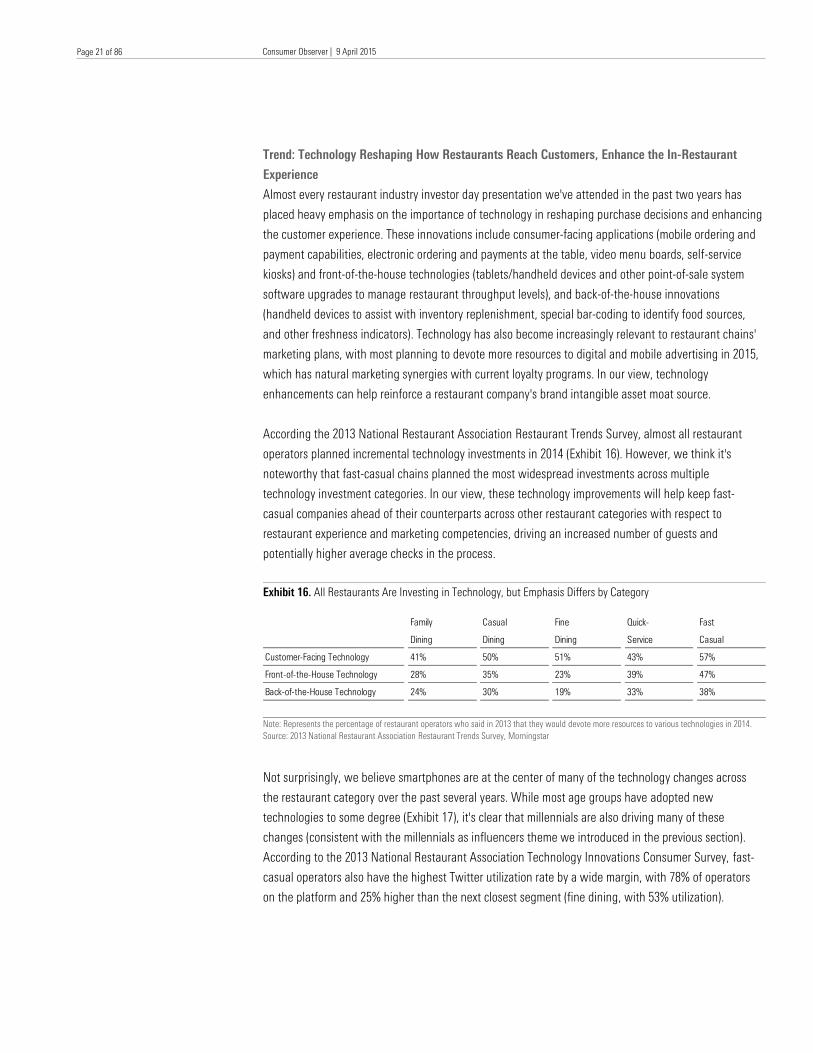

According the 2013 National Restaurant Association Restaurant Trends Survey, almost all restaurant

operators planned incremental technology investments in 2014 (Exhibit 16). However, we think it's

noteworthy that fast-casual chains planned the most widespread investments across multiple

technology investment categories. In our view, these technology improvements will help keep fast-

casual companies ahead of their counterparts across other restaurant categories with respect to

restaurant experience and marketing competencies, driving an increased number of guests and

potentially higher average checks in the process.

Exhibit 16. All Restaurants Are Investing in Technology, but Emphasis Differs by Category

Note: Represents the percentage of restaurant operators who said in 2013 that they would devote more resources to various technologies in 2014.

Source: 2013 National Restaurant Association Restaurant Trends Survey, Morningstar

Not surprisingly, we believe smartphones are at the center of many of the technology changes across

the restaurant category over the past several years. While most age groups have adopted new

technologies to some degree (Exhibit 17), it's clear that millennials are also driving many of these

changes (consistent with the millennials as influencers theme we introduced in the previous section).

According to the 2013 National Restaurant Association Technology Innovations Consumer Survey, fast-

casual operators also have the highest Twitter utilization rate by a wide margin, with 78% of operators

on the platform and 25% higher than the next closest segment (fine dining, with 53% utilization).

Family

Dining

Casual

Dining

Fine

Dining

Quick-

Service

Fast

Casual

Customer-Facing Technology 41% 50% 51% 43% 57%

Front-of-the-House Technology 28% 35% 23% 39% 47%

Back-of-the-House Technology 24% 30% 19% 33% 38%

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 22 of 86

Page 22 of 86

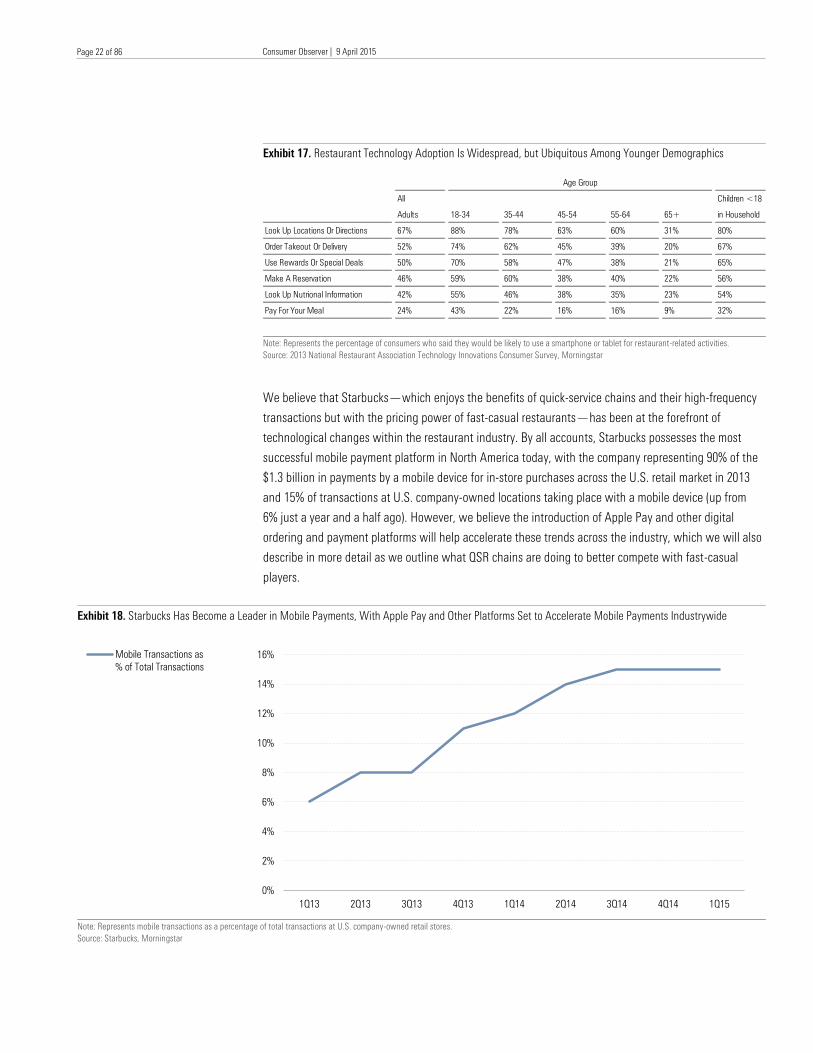

Exhibit 17. Restaurant Technology Adoption Is Widespread, but Ubiquitous Among Younger Demographics

Note: Represents the percentage of consumers who said they would be likely to use a smartphone or tablet for restaurant-related activities.

Source: 2013 National Restaurant Association Technology Innovations Consumer Survey, Morningstar

We believe that Starbucks—which enjoys the benefits of quick-service chains and their high-frequency

transactions but with the pricing power of fast-casual restaurants—has been at the forefront of

technological changes within the restaurant industry. By all accounts, Starbucks possesses the most

successful mobile payment platform in North America today, with the company representing 90% of the

$1.3 billion in payments by a mobile device for in-store purchases across the U.S. retail market in 2013

and 15% of transactions at U.S. company-owned locations taking place with a mobile device (up from

6% just a year and a half ago). However, we believe the introduction of Apple Pay and other digital

ordering and payment platforms will help accelerate these trends across the industry, which we will also

describe in more detail as we outline what QSR chains are doing to better compete with fast-casual

players.

Exhibit 18. Starbucks Has Become a Leader in Mobile Payments, With Apple Pay and Other Platforms Set to Accelerate Mobile Payments Industrywide

Note: Represents mobile transactions as a percentage of total transactions at U.S. company-owned retail stores.

Source: Starbucks, Morningstar

Age Group

All

Adults 18-34 35-44 45-54 55-64 65+

Children <18

in Household

Look Up Locations Or Directions 67% 88% 78% 63% 60% 31% 80%

Order Takeout Or Delivery 52% 74% 62% 45% 39% 20% 67%

Use Rewards Or Special Deals 50% 70% 58% 47% 38% 21% 65%

Make A Reservation 46% 59% 60% 38% 40% 22% 56%

Look Up Nutrional Information 42% 55% 46% 38% 35% 23% 54%

Pay For Your Meal 24% 43% 22% 16% 16% 9% 32%

0%

2%

4%

6%

8%

10%

12%

14%

16%

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

Mobile Transactions as

% of Total Transactions

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 23 of 86

Page 23 of 86

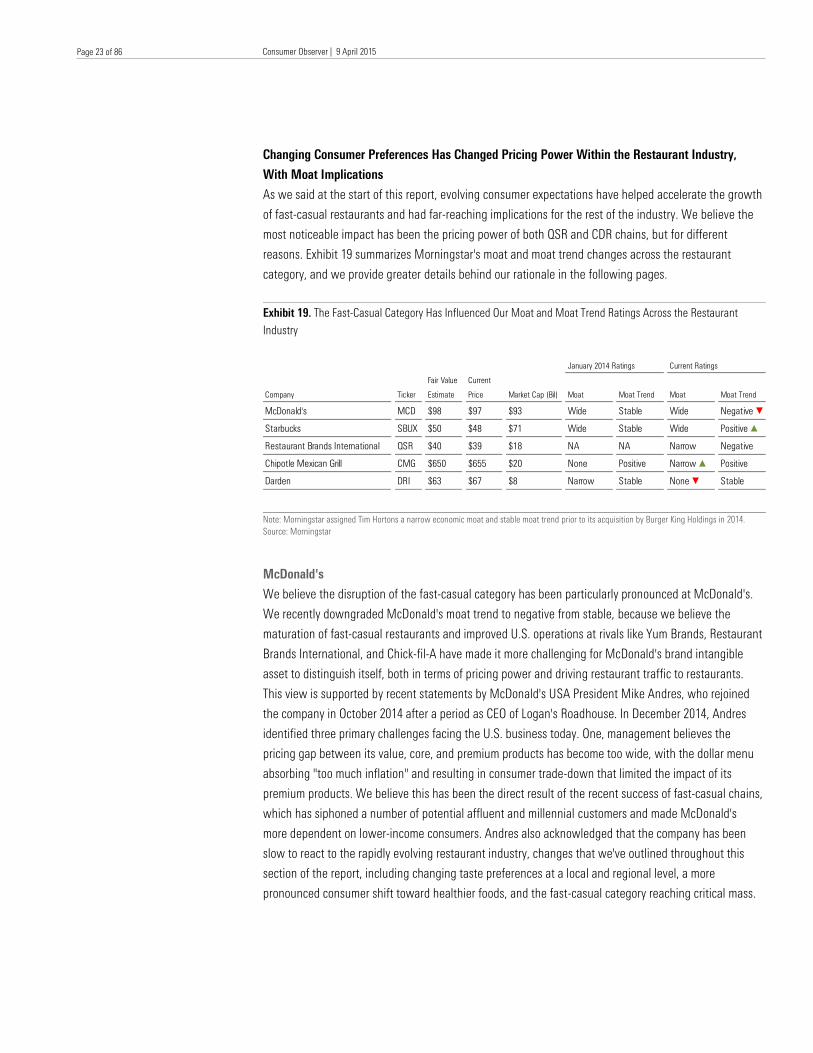

Changing Consumer Preferences Has Changed Pricing Power Within the Restaurant Industry,

With Moat Implications

As we said at the start of this report, evolving consumer expectations have helped accelerate the growth

of fast-casual restaurants and had far-reaching implications for the rest of the industry. We believe the

most noticeable impact has been the pricing power of both QSR and CDR chains, but for different

reasons. Exhibit 19 summarizes Morningstar's moat and moat trend changes across the restaurant

category, and we provide greater details behind our rationale in the following pages.

Exhibit 19. The Fast-Casual Category Has Influenced Our Moat and Moat Trend Ratings Across the Restaurant

Industry

Note: Morningstar assigned Tim Hortons a narrow economic moat and stable moat trend prior to its acquisition by Burger King Holdings in 2014.

Source: Morningstar

McDonald's

We believe the disruption of the fast-casual category has been particularly pronounced at McDonald's.

We recently downgraded McDonald's moat trend to negative from stable, because we believe the

maturation of fast-casual restaurants and improved U.S. operations at rivals like Yum Brands, Restaurant

Brands International, and Chick-fil-A have made it more challenging for McDonald's brand intangible

asset to distinguish itself, both in terms of pricing power and driving restaurant traffic to restaurants.

This view is supported by recent statements by McDonald's USA President Mike Andres, who rejoined

the company in October 2014 after a period as CEO of Logan's Roadhouse. In December 2014, Andres

identified three primary challenges facing the U.S. business today. One, management believes the

pricing gap between its value, core, and premium products has become too wide, with the dollar menu

absorbing "too much inflation" and resulting in consumer trade-down that limited the impact of its

premium products. We believe this has been the direct result of the recent success of fast-casual chains,

which has siphoned a number of potential affluent and millennial customers and made McDonald's

more dependent on lower-income consumers. Andres also acknowledged that the company has been

slow to react to the rapidly evolving restaurant industry, changes that we've outlined throughout this

section of the report, including changing taste preferences at a local and regional level, a more

pronounced consumer shift toward healthier foods, and the fast-casual category reaching critical mass.

January 2014 Ratings Current Ratings

Company Ticker

Fair Value

Estimate

Current

Price Market Cap (Bil) Moat Moat Trend Moat Moat Trend

McDonald's MCD $98 $97 $93 Wide Stable Wide Negative Õ

Starbucks SBUX $50 $48 $71 Wide Stable Wide Positive Ö

Restaurant Brands International QSR $40 $39 $18 NA NA Narrow Negative

Chipotle Mexican Grill CMG $650 $655 $20 None Positive Narrow Ö Positive

Darden DRI $63 $67 $8 Narrow Stable None Õ Stable

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 24 of 86

Page 24 of 86

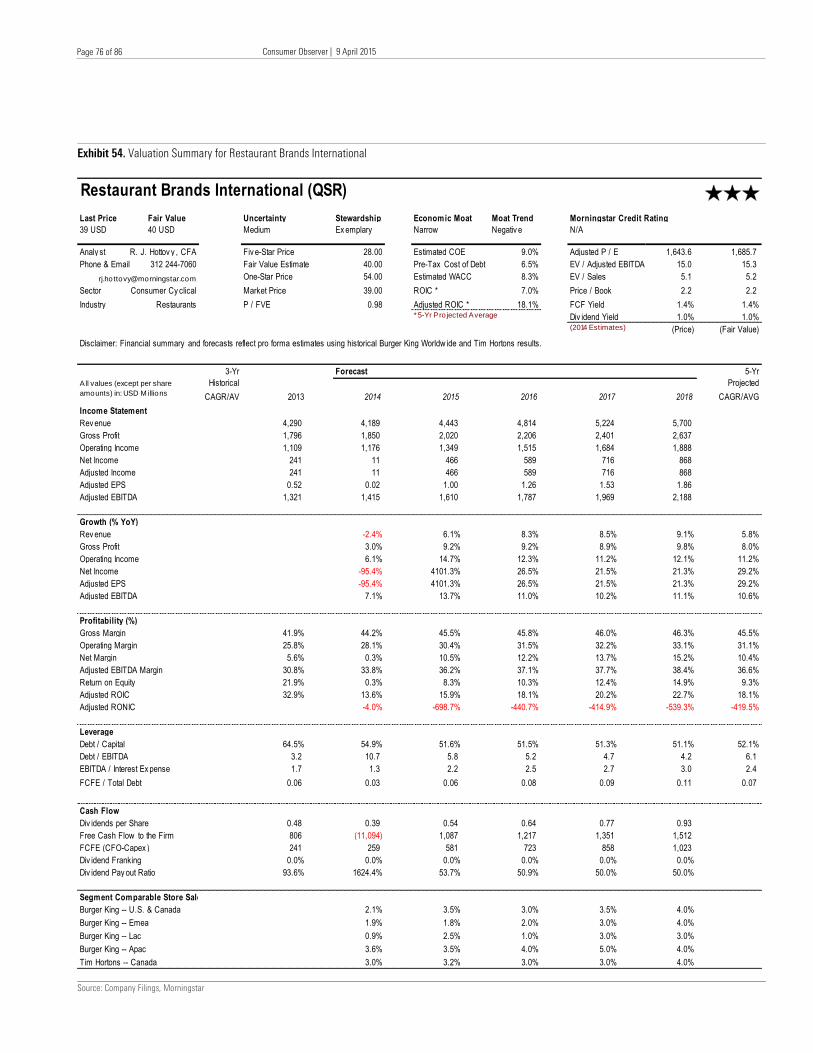

Restaurant Brands International

We've been impressed by improvements in the Burger King system in the past several years under 3G

Capital's stewardship, including stronger relationships with existing franchisees (including the sale of

more than 1,200 company-owned locations to franchisees since 2009, resulting in 99% of the

systemwide restaurants now being operated by franchisees and licensees). In our view, this has placed

restaurant operations in the hands of some of the system's best operators, facilitated accelerated

restaurant remodeling activities (40% of U.S. and Canada Burger King locations have been reimaged at

the end of 2014), and enabled management to focus on brand awareness, menu innovation, and more

effective marketing. In fact, a streamlined menu emphasizing fewer but more impactful products,

daypart expansion (with an emphasis on breakfast and snacking), revamped value platform (two

sandwiches for $5, for example), and remodeled restaurants have reinvigorated the Burger King brand in

recent years—particularly in developed markets such as the U.S.—driving market share gains and

improved franchise-level returns in the process. With additional exterior and interior decor upgrades

planned, new restaurant formats and drive-thru configurations, and adoption of new technologies for

one-to-one marketing and throughput improvements, we anticipate restaurant productivity metrics to

improve in the years to come. Nevertheless, we expect many of the recent structural changes taking

place across the restaurant space to have a more pronounced impact on Burger King's intangible asset

moat source in the years to come, providing the foundation for our negative moat trend rating.

Darden

While fast-casual's impact on QSR chains is undeniable, we believe there are still opportunities for this

category to refine its menu, customer experience, and technology strategies and narrow the pricing gap

with its fast-casual peers over a longer horizon. However, we believe the rise of fast-casual players and

other structural changes within the restaurant industry are more troubling for CDR chains, largely

because of limitations it places on future pricing power/margin expansion. In fact, we removed our

narrow moat rating for Darden in 2014 and no longer view the company's competitive advantages as

sufficient enough to drive excess economic profits over an extended period.

Darden remains the second-largest casual-dining restaurant operator in the United States after selling

Red Lobster, representing approximately 8.5% of the $80 billion domestic casual-dining market. This

places the company behind DineEquity (9% share based on total systemwide sales), but still ahead of

Bloomin' Brands (5% share), Brinker International (3%), and Cheesecake Factory (2%). However, the

casual-dining restaurant industry has become increasingly more competitive in recent years, as we

believe the emergence of fast-casual restaurant concepts has resulted in elevated industry promotional

activity and altering guest experience expectations. In our view, these trends will continue in the years

to come, which will effectively neutralize Darden's brand intangible asset advantages, bargaining power

with suppliers, and marketing and other economies of scale, the combination of which provided the

foundation for our previous narrow moat rating.

Starbucks

At the other end of the spectum, there are examples of restaurant companies that have been able to

adapt to consumer preference and other structural changes within the industry. In our view, Starbucks

provides a prime example. Although the company has admittedly benefited from broader tailwinds

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 25 of 86

Page 25 of 86

fueling the specialty coffee category, we believe the company has taken steps to enhance the brand

intangible asset behind its wide moat rating, resulting in a positive moat trend. This view is validated by

four consecutive years of global comparable-restaurant sales of 5% or greater. Additionally, we believe

that few national/regional restaurant or specialty coffee operators are willing or able to compete with

Starbucks' in-store customer experience, outside a handful of smaller independent coffee chains or

select fast-casual concepts.

We identify several drivers for Starbucks to improve store productivity at new and existing locations,

adding incremental support to our positive moat trend rating. Among the most innovative productivity

initiatives is Mobile Order & Pay, which dovetails nicely with the company's existing digital and loyalty

platforms and could be a game changer across high-frequency retailers and restaurant concepts. The

program, which is expected to be launched nationwide in the U.S. during 2015, allows customers to

place customized beverage and food orders from mobile devices for pickup in a store of their choosing.

We see many benefits from the platform, including more My Starbucks Reward loyalty members, greater

targeted marketing efforts leading to higher food attachment rates and average ticket sizes, increased

purchasing frequency from existing customers, and greater store throughput by effectively eliminating

point-of-sale pain points. Although it may take some time for consumers to adopt this program, we

believe in-store disruptions or the need for a material increase in in-store labor/equipment will be

limited. Management also plans to introduce delivery in 2015, facilitating deliveries in high-density

markets by creating staging areas in unused office buildings and using its existing store locations and

third-party contracted delivery companies in more suburban locations.

Chipotle

With industry-leading comparable sales growth and restaurant-level margins during an increasingly

competitive environment for restaurant operators, we believe Chipotle has carved out a narrow

economic moat. Breaking down Chipotle's recent comparable-restaurant sales trends, we see many

characteristics that validate the strength of its brand intangible asset, which provides the foundation for

our moat rating. Chipotle has averaged 10% comparable-restaurant sales growth the past four years,

driven in large part by traffic growth and only minimal pricing increases. This outpaces traffic for the

broader restaurant category averages—which we peg in the low-single-digit range across all restaurant

categories and low- to mid-single-digit growth for fast-casual concepts—implying market share gains

and helping put Chipotle's brand intangible asset in perspective. However, we believe that recent

transaction growth in the high-single- to low-double-digit range during the past few quarters is

particularly noteworthy, as it comes on top of a 6% increase in menu prices put in place during the

second quarter of 2014 (the first meaningful menu price increase since 2010) as well as an uptick in

catering and add-on orders. In our view, these contributors also provide further evidence of the pricing

power inherent in the brand, a key component when evaluating intangible assets among consumer

companies.

Chipotle's success and compelling unit economics have not gone unnoticed, however, spawning

multiple fast-casual restaurant rivals with aggressive growth aspirations. We anticipate that category

rivalry will escalate and evolve over the next several years (including competition from new entrants as

well as existing quick-service, fast-casual, and casual-dining restaurant operators), forcing firms to

Consumer Observer | 9 April 2015

Healthcare Observer | 14 April 2015

Page 26 of 86

Page 26 of 86

increasingly compete with one another for share through menu innovations, aggressive pricing, and

limited-time offers (not dissimilar to the maturation of the quick-service restaurant industry in the U.S.

over the past decade). Additionally, with retail landlords looking for tenants for unoccupied real estate

and restaurant operators finding themselves with easier access to capital, we anticipate new fast-casual

restaurant entrants will increasingly come to the market.

Nevertheless, we believe Chipotle has separated itself from its fast-casual peers and can defend market

share from new rivals while preserving pricing power. This is in large part due to its "Food with Integrity"

mantra (sourcing naturally raised proteins, dairy products from pasture-raised cattle, and organic

produce, which are more costly but offer a key source of differentiation), upscale restaurant

environments, and uniquely customizable menu structure, each of which enriches Chipotle's brand

intangible asset moat source.

Panera

What about Panera, the largest player in the $39 billion domestic fast-casual industry? In our view,

Panera has exhibited several signs of an emerging intangible asset moat source, resulting in a positive

moat trend. The compelling economics of the fast-casual bakery-cafe concept have attracted a number

of substitutes in recent years, including encroaching competition from traditional quick-service and

casual-dining participants. However, the Panera brand has shown more pricing power than most

restaurant chains, as evidenced by average annual menu price increases of approximately 3% during the

past five years. We believe the Panera brand can maintain its pricing power through its Panera 2.0

initiatives, which are focused on reducing customer friction through additional peak-hour throughput

capacity, labor and production equipment investments, moderating restaurant complexity, implementing

new marketing strategies, and introducing menus that allow for greater portion-size control but also