finding strategic and cyclical exposure: sector and...

TRANSCRIPT

For financial professional use only. Do not distribute to the public. 1

Finding Strategic and Cyclical Exposure:

Sector and Factor Investing

For financial professional use only. Do not distribute to the public. 2

Housekeeping

‣ Ask Questions

‣ Polls

‣ Survey & Giveaway

• Complete survey for a chance to win a power bank battery

For financial professional use only. Do not distribute to the public. 3

Today’s Presenters

Moderator Panelist Panelist

Tom Lydon Denise Chisholm Darby Nielson

Editor & Publisher Sector Strategist Managing Director of Research

ETF Trends Fidelity Investments Fidelity Investments

Not FDIC Insured May Lose Value No Bank Guarantee

For Investment Professionals

March 2017

Finding Strategic and Cyclical Exposure:

Sector and Factor Investing

Denise Chisholm

Sector Strategist

Darby Nielson

Managing Director of Research

Sector Theme Investing

For Investment Professionals

Where We’ve Been …

Where Are We Going?

For Investment Professionals

Where We’ve Been One of the critical issues facing the market is earnings growth contraction

7

IVA & CCAdj (SAAR, $) % Change—Year to Year

Source: Bureau of Economic Analysis (BEA), as of 9/15

Capital consumption adjustment (CCAdj): the difference between private capital consumption allowances (CCA) and private consumption of

fixed capital (CFC) IVA: Inventory valuation adjustment; SAAR: Seasonally Adjusted Annual Rates.

CORPORATE PROFITS AFTER TAX

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

19

62

19

63

19

65

19

67

19

68

19

70

19

72

19

73

19

75

19

77

19

78

19

80

19

82

19

83

19

85

19

87

19

88

19

90

19

92

19

93

19

95

19

97

19

98

20

00

20

02

20

03

20

05

20

07

20

08

20

10

20

12

20

13

20

15

For Investment Professionals

Profits Have Slowed Sectors can be a great way to play this theme

8

Equity universe is defined as the top 3,000 U.S. stocks by market capitalization; sectors as defined by the Global Industry Classification Standard

(GICS). Source: Haver, as of 12/15.

Alpha: A measure of performance on a risk-adjusted basis. Also referred to as excess return.

SECTOR AVERAGE ALPHA WHEN EARNINGS GROWTH IS DECELERATING

1985 to Present

7.1% 6.0%

2.0% 1.0% 0.5% 0.3%

-0.1% -0.4% -0.8% -1.6%

Co

nsu

me

r S

taple

s

He

alth

Care

Utilit

ies

Ene

rgy

Mate

rials

Co

nsu

me

r D

iscre

tion

ary

Tele

com

mu

nic

ation

s

Fin

an

cia

ls

Indu

str

ials

Tech

no

logy

For Investment Professionals

Potential for Change

9

Corporate Tax Reform?

Potential for Financial Services Deregulation?

For Investment Professionals

Possible Impact on Earnings

10

Corporate Profits is from our internal database defined as the top 3,000 U.S. stocks by market capitalization; sectors as def ined by the Global

Industry Classification Standard (GICS). Source: Haver, as of 12/16.

CORPORATE PROFIT ACCELERATION & GROWTH DURING CORPORATE TAX CUTS

12%

14%

2%

Acceleration During Growth Post Cut Years Before

For Investment Professionals

Tax Reform Implications

11

Equity universe is defined as the top 3,000 U.S. stocks by market capitalization; sectors as defined by the Global Industry Classification Standard

(GICS). Source: Haver, as of 12/16. Defense is an average of staples, healthcare, utilities and telecom sector relative performance. Cyclicals is an

average of energy, industrials, materials, discretionary, technology, and financials relative performance.

AVERAGE SECTOR RETURNS

Higher Corporate Taxes vs. Lower Corporate Taxes

-2%

1%

5%

-1%

Defensive Sectors Cyclical Sectors

Lower Tax Rates Higher Tax Rates

For Investment Professionals

Financial Services Deregulation Implications

12

Equity universe is defined as the top 3,000 U.S. stocks by market capitalization; sectors as defined by the Global Industry Classification Standard

(GICS). Source: Haver, as of 12/16. Defense is an average of staples, healthcare, utilities and telecom sector relative performance. Cyclicals is an

average of energy, industrials, materials, discretionary, technology, and financials relative performance.

2%

-1%

0%

1%

Less Willing to Lend More Willing to Lend

Average Defensive Sectors Average Cyclical Sectors

AVERAGE SECTOR RETURNS

Banks More Willing to Lend vs. Less

For Investment Professionals

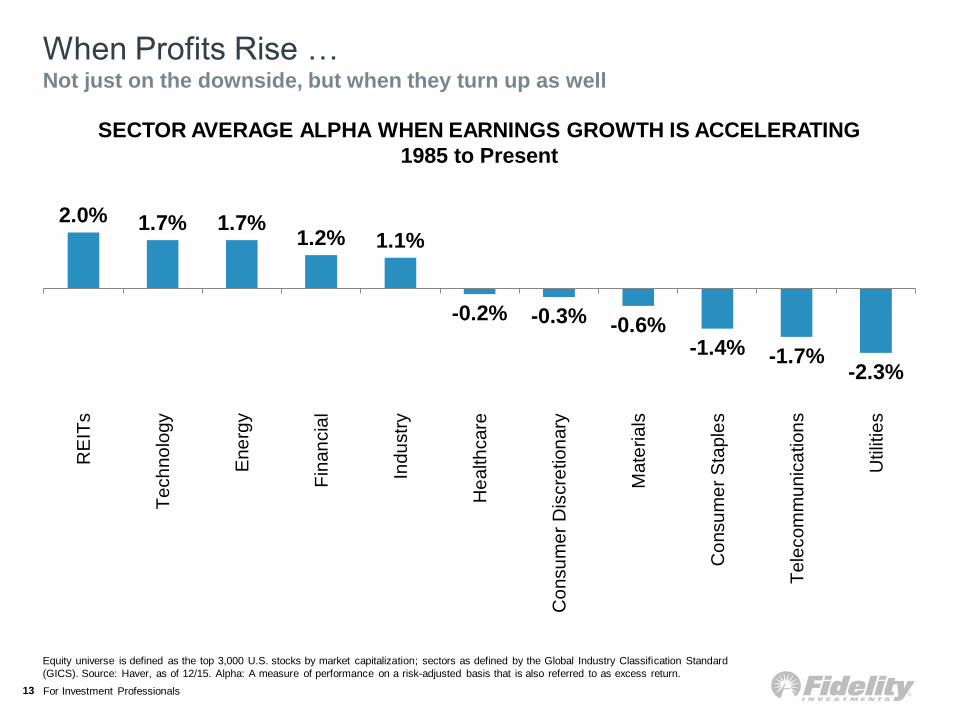

When Profits Rise … Not just on the downside, but when they turn up as well

13

Equity universe is defined as the top 3,000 U.S. stocks by market capitalization; sectors as defined by the Global Industry Classification Standard

(GICS). Source: Haver, as of 12/15. Alpha: A measure of performance on a risk-adjusted basis that is also referred to as excess return.

SECTOR AVERAGE ALPHA WHEN EARNINGS GROWTH IS ACCELERATING

1985 to Present

2.0% 1.7% 1.7% 1.2% 1.1%

-0.2% -0.3% -0.6% -1.4% -1.7%

-2.3%

RE

ITs

Tech

no

logy

Ene

rgy

Fin

an

cia

l

Indu

str

y

He

alth

care

Co

nsu

me

r D

iscre

tion

ary

Mate

rials

Co

nsu

me

r S

taple

s

Tele

com

mu

nic

ation

s

Utilit

ies

For Investment Professionals

Investment Spending Recovery?

14

National Accounts Data in Haver as of 12/31/2016.

REAL GROSS PRIVATE DOMESTIC INVESTMENT (SAAR, CHN.2009$)

% Change–Year to Year

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

62

163

365

166

368

169

371

172

374

175

377

178

380

181

383

184

386

187

389

190

392

193

395

196

398

199

301

102

304

105

307

108

310

111

313

114

316

1

For Investment Professionals

What about Rates?

15

Source: Bureau of Economic Analysis (BEA), as of 12/16; Haver, as of 12/16.

INTEREST RATES AND PROFITS

Odds of Profit Acceleration

58%

36%

Rates Up Rates Down

For Investment Professionals

Fidelity Factor Research

For Investment Professionals

Agenda

17

1. Overview of Factor Investing

2. Factor Usage

A. Strategic Exposure

B. Cyclical Exposure

C. Portfolio Construction

3. Fidelity Factor ETFs

For Investment Professionals

Overview of Factor Investing

For Investment Professionals

Evolution of Factor Analysis Progression of research into the drivers of asset returns

19

Source: Fidelity Investments.

MULTIPLE SYSTEMATIC

RETURN ANOMALIES

SINGLE SOURCE OF

SYSTEMATIC RISK

ASSORTED STRATEGIC

RISK AND RETURN FACTORS

Fama and French develop model accounting

for additional factors, stock characteristics of

size and style, which also drive performance.

Capital Asset Pricing Model (CAPM) proposes

return on investment driven by exposure to

single factor, market risk or “beta.”

Substantial research and analysis into many

other strategic factors, which can be used to

explain the components of a stock’s return.

Market

Asset Specific

Market

Asset Specific

Size

Style

Market

Asset Specific

Size

Style

PORTFOLIO PORTFOLIO PORTFOLIO

Momentum

Quality

Value

Volatility

Yield

For Investment Professionals

Evolution of Factor Analysis at Fidelity Fidelity has long history of factor investing, which has evolved significantly over

the last decade since the Quantitative Research team was formed.

20

1965

Fidelity hires first

dedicated Quant

analyst

Background

• Fidelity’s quantitative research capabilities were built to provide fundamentally based factor insights to portfolio managers,

research analysts, and CIOs.

• Factor-based stock selection models were built via collaborations between FMR analysts and PMs with the Quant Research team.

• Factor models incorporate the best stock drivers from both fundamental and quantitative perspectives.

• Evolution resulted in a suite of intuitive, fundamentally-driven models for generating investment ideas and monitoring portfolio exposures.

Fidelity launches its

first quant fund,

Disciplined Equity

Quantitative Research team

formally established to

complement fundamental

capabilities

Global Value and

Momentum multifactor

model researched and

launched

First sector factor

model launched in

collaboration with

fundamental research

Quality and Low

Volatility models

researched and

launched

Research,

development, and

launch of stand-alone

factor products

1988

2006

2007

2008 2013

2016

Source: Fidelity Investments.

For Investment Professionals

Factor Usage

For Investment Professionals

Potential Key Uses of Factor Strategies in a Portfolio Investors seek out factor exposures for return/outcome potential and risk management

22

Strategic Exposure Cyclical Exposure Portfolio Construction

Strategic allocations to factors can

enhance risk-adjusted returns.

Investors may consider exposure to

one or a combination of factors to take

advantage of their potential benefits.

Because factor returns can vary through

time, adjusting factor exposures using a

cyclical framework may help investors

express a market or investment view.

Investors and advisors can use

factor-based strategies to fine-tune

their exposures and better align their

broader portfolios with their intended

investment objectives and risk profiles.

INTENDED OBJECTIVES

For Investment Professionals

Factors Matter Research reveals the return potential of these factors over time

23

Returns are cumulative and assume reinvestment of dividends. Returns do not reflect the performance of any Fidelity index or ETF. Past performance is no

guarantee of future results. Value composite is a combined average ranking of stocks in the equal-weighted top quintile (by book/price ratio) and stocks in

the equal-weighted top quintile (by earnings yield) of the Russell 1000 Index. Momentum returns are the equal-weighted top quintile (by trailing 12-month

returns) of the Russell 1000 Index. Quality returns are the equal-weighted top quintile (by return on equity) of the Russell 1000 index. Low-volatility returns

are yearly returns of the equal-weighted bottom quintile (by standard deviation of weekly price returns) of the Russell 1000 Index. For more detail, see

September 2016 Fidelity Leadership Series “An Overview of Factor Investing”.

Source: Fidelity Investments as of 12/31/15.

CUMULATIVE FACTOR RETURNS VS. THE MARKET, 1985–2015

0%

1000%

2000%

3000%

4000%

5000%

6000%

7000%

8000%

De

c-8

5

De

c-8

7

De

c-8

9

De

c-9

1

De

c-9

3

De

c-9

5

De

c-9

7

De

c-9

9

De

c-0

1

De

c-0

3

De

c-0

5

De

c-0

7

De

c-0

9

De

c-1

1

De

c-1

3

De

c-1

5

Value

Quality Momentum

Low Volatility

Russell 1000

Exposure to

these key strategic

factors has

generated market

outperformance

over time

For Investment Professionals

Factor Definitions Matter

24

Value composite is a combined average ranking of stocks in the

equal-weighted top quintile (by book/price ratio) and stocks in the

equal-weighted top quintile (by earnings yield) of the Russell 1000

Index. Returns shown are yearly returns of this value composite. Past

performance is no guarantee of future results. Source: FactSet, as of

3/31/16.

Earnings yield: last 12 months of earnings per share divided by price

per share. Book/price ratio: the ratio of a company’s reported

accumulated profits to its price per share. Returns shown are yearly

returns of the equal-weighted top quintile (based on these two value

metrics) of the Russell 1000 Index. Past performance is no guarantee

of future results. Source: FactSet, as of 3/31/16.

EXCESS RETURNS OF TWO VALUE MEASURES

The performance of a value portfolio can vary

based on how value is defined

EXCESS RETURNS TO A VALUE COMPOSITE

A mix of factors can improve the performance of

a value approach

-30%

-20%

-10%

0%

10%

20%

30%

40%

198

6

198

8

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

201

2

201

4

Book/Price EPLTM

Yearly Excess Return

2015

Avg. Book/Price Avg. Earnings Yield

1.98% 2.91%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

198

6

198

8

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

201

2

201

4

Yearly Excess Return

2015

For Investment Professionals

Factor Performance Cyclicality Most factors are not highly correlated, so diversifying among them may improve

risk-adjusted returns over time

25

Rolling Annual Excess Return

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

Dec-8

6

Dec-8

8

Dec-9

0

Dec-9

2

Dec-9

4

Dec-9

6

Dec-9

8

Dec-0

0

Dec-0

2

Dec-0

4

Dec-0

6

Dec-0

8

Dec-1

0

Dec-1

2

Dec-1

4

Book/Price MomentumValue

Value represented by the equal-weighted top quintile (by book-to price ratio) of the Russell 1000 Index. Momentum represented by the equal-weighted top

quintile (by trailing 12-month returns) of the Russell 1000 Index. Source: FactSet, as of 3/31/16.

For Investment Professionals

Benefits of Factor Diversification Diversifying across multiple factors can help investors achieve more consistent

performance over time

26

Excess Return Tracking Error Info. Ratio

Value 3.4% 5.2% 0.6

Multifactor 1.7% 1.5% 1.2

Yearly Excess Return vs. Broader Market

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

Value Multifactor

Equal-weighted multifactor portfolio includes five factor portfolios: size, value, momentum, quality, and low volatility. Size returns are yearly returns of the equal-weighted bottom quintile

(by market capitalization) of the Russell 1000 Index. Value composite returns are the combined average ranking of stocks in the equal-weighted top quintile (by book/price ratio) and

stocks in the equal-weighted top quintile (by earnings yield) of the Russell 1000 Index. Momentum returns are the equal-weighted top quintile (by trailing 12-month returns) of the Russell

1000 Index. Quality returns are the equal-weighted top quintile (by return on equity) of the Russell 1000 index. Low-volatility returns are yearly returns of the equal-weighted bottom

quintile (by standard deviation of weekly price returns) of the Russell 1000 Index. Excess return: compound average of yearly excess returns versus the equal-weighted Russell 1000

Index from Jan. 1986 through Mar. 2016. Tracking error: measures the variation of performance relative to the broader market (in this case, the equal-weighted Russell 1000 Index).

Information ratio: measures risk-adjusted return (defined as excess return divided by tracking error).

Past performance is no guarantee of future results.

Source: FactSet, as of 3/31/16.

For Investment Professionals

Factor Performance and the Business Cycle Certain factors have tended to perform well in varying market environments;

active factor tilts can help generate alpha throughout the economic cycle.

27

FACTORS AND THE BUSINESS CYCLE

Objective

• Add excess return potential to a

portfolio

Factor Strategy

• Adjust portfolio allocations over

time to increase exposure to

opportunistic factors

Unshaded (white) portions above suggest no clear pattern of over- or underperformance vs. broader market. Double +/– signs indicate that the sector is showing a consistent signal

across all three metrics: full-phase average performance, median monthly difference, and cycle hit rate. A single +/– indicates a mixed or less consistent signal. Value composite is a

combined average ranking of stocks in the equal-weighted top quintile (by book/price ratio) and stocks in the equal-weighted top quintile (by earnings yield) of the Russell 1000 Index.

Momentum returns are the equal-weighted top quintile (by trailing 12-month returns) of the Russell 1000 Index. Quality returns are the equal-weighted top quintile (by return on equity) of

the Russell 1000 index. Low-volatility returns are yearly returns of the equal-weighted bottom quintile (by standard deviation of weekly price returns) of the Russell 1000 Index. Dividend

Yield composite is the equal-weighted top quintile (by dividend yield) or the equal-weighted Russell 1000 Index. For more detail, see September 2016 Fidelity Leadership Series “Putting

Factors to Work.”

Past performance is no guarantee of future results.

Source: Fidelity Investments (AART).

Factor Early Mid Late Recession

Value ++ ++

Dividend Yield ++ ++

Size + +

Momentum ++ +

Quality + +

Low Volatility – – – ++

For Investment Professionals

Factors as Risk Management Tools Adding allocation to a low volatility strategy can help improve a portfolio’s

risk-adjusted return through decreased volatility.

28

ADDITION OF LOW VOLATILITY: PERFORMANCE AND RISK COMPARISONS

Objective

• Reduce level of risk in a portfolio

while still maintaining return

potential

Factor Strategy

• Factor-based strategies can

complement active funds by

offsetting risk exposures

Large-cap growth fund represented by the median fund by return volatility within the top quintile of 10-year performance in the Morningstar large-cap growth category. Low-volatility

portfolio is the equal-weighted bottom quintile (by standard deviation of weekly price returns) of the Russell 1000 Index. Large-cap growth fund + low vol is an equal-weighted portfolio of

this active large cap growth fund and a low-volatility factor portfolio. Annualized returns from July 2006 through June 2016. Volatility represented by standard deviation (a measure of

return variance). A portfolio with a lower standard deviation exhibits less volatility. For more detail, see September 2016 Fidelity Leadership Series “Putting Factors to Work.”

Past performance is no guarantee of future results.

Source: Fidelity Investments and FactSet, as of 6/30/2016.

Annualized Return and Volatility (%)

July 2006–June 2016

9.2% 8.9%

7.5%

17.2%

14.5% 15.5%

Large-Cap Growth Fund Large-Cap Growth Fund + Low Vol Russell 1000 Index

Annualized Return Volatility

For Investment Professionals

Fidelity Factor ETFs

For Investment Professionals

Fidelity Factor ETFs—Overview Focus on fundamental investment opportunities, leveraging our insights to define

our factor-based strategies

30

FDLO

FDRR

FDMO FQAL

FVAL

FDVV

Aiming to generate higher relative

dividend yield with sector tilts,

subject to constraints, which have

historically delivered higher yield

Targeting higher-yielding

companies with positive correlation

to rising Treasury yields can provide

protection in a rising rate

environment

Focusing on securities, which

generate similar returns as the

broader market over time with less

volatility

Seeking outperforming stocks, which

have had a tendency to continue to

outperform over the medium-term

Prioritizing companies with higher

profitability, stable cash flows, and

good balance sheets, which have

tended to outperform their peers

over time

Capitalizing on cheap stocks, with

low prices relative to fundamentals,

which have historically outperformed

the market over time

Purchase Information

Net Expense Ratio: 0.29%

Stock Exchange: NYSE

Fidelity Brokerage Trading Fees: Commission Free/30-day short-

term trading fee1

Rule-Based Passively Managed Investment Approach

Proprietary Methodology Fidelity Investments

Independent Calculation Agent S&P Dow Jones

Sub-Advisor Geode Capital Management

1 Free commission offer applies to online purchases of Fidelity ETFs in a Fidelity brokerage account with a minimum opening balance of $2,500.

The sale of ETFs on Fidelity’s brokerage platform are subject to an activity assessment fee (of between $0.01 to $0.03 per $1000 of principal) by

Fidelity. Fidelity ETFs traded in Fidelity brokerage accounts are subject to a short-term trading fee by Fidelity, if held less than 30 days.

Source: Fidelity Investments.

FDVV

Fidelity Core

Dividend ETF

FDRR

Fidelity Dividend ETF

for Rising Rates

FDLO

Fidelity Low

Volatility Factor ETF

FDMO

Fidelity Momentum

Factor ETF

FQAL

Fidelity Quality

Factor ETF

FVAL

Fidelity Value

Factor ETF

For Investment Professionals

For financial professional use only. Do not distribute to the public. 31

Questions?

Please submit your questions using the Q&A box.

Glossary

32

Term Definition

12-Month Return Minus 1-Month Return Cumulative 12-month stock return less the prior month’s stock return.

12-Month Earnings Surprise A measure of comparison between the consensus earnings-per-share estimate from 12 months ago and actual

earnings-per-share.

6-Month Average Short Interest A measure of the monthly average number of shares shorted divided by monthly average number of shares traded.

Active Share The percentage of a an index’s weight-adjusted portfolio that differs from another comparison index.

Beta

A historical measure of a fund's sensitivity to market movements and is calculated by comparing the fund's monthly returns,

over 36 months, to those of the market, defined by the fund's benchmark. By definition, the Beta of the market (as measured by

the benchmark) is 1.0. A Beta of less than 1.0 indicates that the fund is less sensitive to the market, while a Beta of more than

1.0 indicates that the fund is more sensitive to the market. The higher the correlation between the fund and the market (as

measured by R-squared), the more meaningful is Beta.

Cash Flow A measure of cash generated by a company, which is calculated adding non-cash charges to net income after taxes.

Correlation to 10-Year Treasury A measure of the correlation of weekly changes in the 10-year Treasury yield with weekly stock returns.

Dividend Growth A measure of growth in dividends per share over the last year.

Dividend Yield A measure of trailing dividends over last 12 months divided by price per share.

Earnings-Per-Share (EPS) Growth Measures the growth in reported earnings per share over the specified past time period.

Enterprise Value (EV)-to-EBITDA Enterprise value divided by earnings before interest, tax, depreciation, and amortization.

Free Cash Flow (FCF)

A measure of financial performance calculated as operating cash flow minus capital expenditures. Free cash flow (FCF)

represents the cash that a company is able to generate after laying out the money required to maintain or expand its asset

base.

Free Cash Flow Margin A measure of cash generated after deducting all investments needed to maintain and expand assets divided by total earnings.

Free Cash Flow Stability A measure of the stability of a company’s free cash flows, calculated as a percentage of the last 20 quarters with positive free

cash flow values.

Free Cash Flow Yield

A valuation measure of a stock, which standardizes a company's free cash flow by its market capitalization. Generally, the

lower the ratio, the less attractive the investment and vice versa, with the logic that investors would like to pay as little a price

as possible for as much free cash flow as possible.

For Investment Professionals

Glossary

33

Term Definition

Information Ratio Measures a fund's active return (fund's average monthly return minus the benchmark's average monthly return)

in relation to the volatility of its active returns.

Market Capitalization The total dollar market value of all of a company’s outstanding shares.

Payout Ratio A measure of trailing dividends per share over the past twelve months divided by earnings per share.

Price-to-Book (P/B) Ratio The ratio of a company's current share price to reported accumulated profits and capital.

Price-to-Cash Flow (P/CF) Ratio The ratio of a company's current share price to its trailing 12-months cash flow per share.

Price-to-Earnings (P/E) Ratio

(IBES 1-Year Forecast) The ratio of a company's current share price to Wall Street analysts' estimates of earnings.

Price-to-Earnings (P/E) Ratio Trailing The ratio of a company's current share price to its trailing 12-months earnings per share.

Price-to-Tangible Book Value (TBV) The ratio of a company’s current share price to its total book value, less the value of any intangible assets.

Return on Invested Capital (ROIC) A measure of how effectively a company uses the money (borrowed or owned) invested in its operations, typically expressed

as net income minus dividends divided by total capital (debt plus equity).

Standard Deviation A measure of dispersion of a set of data from its mean.

Volatility-Adjusted 12-Month Return

Minus 1-Month Return

Cumulative 12-month stock return divided by monthly volatility, as measured by standard deviation, less the

prior month’s stock return.

For Investment Professionals

Important Information

For Investment Professionals

Not FDIC Insured. May Lose Value. No Bank Guarantee.

Not NCUA or NCUSIF insured. May lose value. No credit union guarantee.

Unless otherwise disclosed to you, in providing this information, Fidelity is not undertaking to provide impartial investment advice, or to give advice

in a fiduciary capacity, in connection with any investment or transaction described herein. Fiduciaries are solely responsible for exercising

independent judgment in evaluating any transaction(s) and are assumed to be capable of evaluating investment risks independently, both in

general and with regard to particular transactions and investment strategies. Fidelity has a financial interest in any transaction(s) that fiduciaries,

and if applicable, their clients, may enter into involving Fidelity’s products or services.

Views expressed are as of the date indicated, based on the information available at that time, and may change based on market or other

conditions. Unless otherwise noted, the opinions provided are those of the authors and not necessarily those of Fidelity Investments or its affiliates.

Fidelity does not assume any duty to update any of the information.

References to specific investment themes are for illustrative purposes only and should not be construed as recommendations or investment advice.

Investment decisions should be based on an individual’s own goals, time horizon, and tolerance for risk.

This piece may contain assumptions that are “forward-looking statements,” which are based on certain assumptions of future events. Actual events

are difficult to predict and may differ from those assumed. There can be no assurance that forward-looking statements will materialize or that actual

returns or results will not be materially different from those described here.

Past performance is no guarantee of future results.

Investing involves risk, including risk of loss.

Diversification does not ensure a profit or guarantee against loss.

All indices are unmanaged. You cannot invest directly in an index.

Business Cycle Definition

The typical business cycle depicts the general pattern of economic cycles throughout history, though each cycle is different. In general, the typical

business cycle demonstrates the following:

Market Indices

The S&P 500® Index is a market capitalization-weighted index of 500 common stocks chosen for market size, liquidity, and industry group

representation to represent U.S. equity performance. S&P 500 is a registered service mark of Standard & Poor’s Financial Serv ices LLC. Sectors

and industries are defined by the Global Industry Classification Standard (GICS).

34 For Investment Professionals

Important Information

The S&P 500 sector indices include the standard GICS sectors that make up the S&P 500 Index. The market capitalization of all S&P 500 sector

indices together composes the market capitalization of the parent S&P 500 Index; each member of the S&P 500 Index is assigned to one (and only

one) sector.

Barclays U.S. Corporate High Yield Bond Index is a market value-weighted index that covers the universe of dollar-denominated, fixed-rate,

non-investment-grade debt.

The Russell 3000® Index measures the performance of the largest 3,000 U.S. companies, representing approximately 98% of the investable U.S.

equity market.

Sectors are defined as follows: Consumer Discretionary: companies that provide goods and services that people want but don’t necessarily need,

such as televisions, cars, and sporting goods; these businesses tend to be the most sensitive to economic cycles. Consumer Staples: companies

that provide goods and services that people use on a daily basis, like food, household products, and personal-care products; these businesses tend

to be less sensitive to economic cycles. Energy: companies whose businesses are dominated by either of the following activities: the construction

or provision of oil rigs, drilling equipment, or other energy-related services and equipment, including seismic data collection; or the exploration,

production, marketing, refining, and/or transportation of oil and gas products, coal, and consumable fuels. Financials: companies involved in

activities such as banking, consumer finance, investment banking and brokerage, asset management, insurance and investments, and real estate,

including REITs. Health Care: companies in two main industry groups: health care equipment suppliers and manufacturers, and providers of health

care services; and companies involved in the research, development, production, and marketing of pharmaceuticals and biotechnology products.

Industrials: companies whose businesses manufacture and distribute capital goods, provide commercial services and supplies, or provide

transportation services. Technology: companies in technology software and services and technology hardware and equipment. Materials:

companies that are engaged in a wide range of commodity-related manufacturing. Telecommunication Services: companies that provide

communications services primarily through fixed-line, cellular, wireless, high bandwidth, and/or fiber-optic cable networks. Utilities: companies

considered to be electric, gas, or water utilities, or companies that operate as independent producers and/or distributors of power.

Information presented herein is for discussion and illustrative purposes only and is not a recommendation or an offer or solicitation to buy or sell

any securities. The views and opinions expressed by the Fidelity speaker are those of their own as of the date of the recording, and do not

necessarily represent the views of Fidelity Investments or its affiliates. Any such views are subject to change at any time based upon market or

other conditions and Fidelity disclaims any responsibility to update such views. These views should not be relied on as investment advice, and

because investment decisions are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Fidelity

product. Neither Fidelity nor the Fidelity speaker can be held responsible for any direct or incidental loss incurred by applying any of the information

offered. Please consult your tax or financial advisor for additional information concerning your specific situation.

The S&P 500 Index is a market capitalization-weighted index of 500 common stocks chosen for market size, liquidity, and industry group

representation to represent U.S. equity performance.

Global Industry Classification Standard (GICS) is a standardized classification system for equities developed jointly by Morgan Stanley Capital

International (MSCI) and Standard & Poor's. The GICS hierarchy begins with 10 sectors and is followed by 24 industry groups, 67 industries, and

147 sub-industries. Each stock that is classified will have a coding at all four of these levels.

35 For Investment Professionals

Important Information

Because of their narrow focus, sector funds tend to be more volatile than funds that diversify across many sectors and companies. Nondiversified

sector funds may have additional volatility because they can invest a significant portion of assets in securities of a small number of individual

issuers. The funds are considered nondiversified and can invest a greater portion of assets in securities of individual issuers than a diversified fund;

thus changes in the market value of a single investment could cause greater fluctuations in share price than would occur in a more diversified fund.

General—Fidelity Factor ETF Risk Disclosure: Stock markets, especially foreign markets, are volatile and can decline significantly in response

to adverse issuer, political, regulatory, market, or economic developments. Foreign securities are subject to interest rate, currency exchange rate,

economic, and political risks. The securities of smaller, less well-known companies can be more volatile than those of larger companies. There is

no guarantee that a factor-based investing strategy will enhance performance or reduce risk. Before investing, make sure you understand how the

fund’s factor investment strategy may differ from more traditional index products. Depending on market conditions, fund performance may

underperform compared to products that seek to track a more traditional index. The return of an index ETF is usually different from that of the index

it tracks because of fees, expenses and tracking error. An ETF may trade at a premium or discount to its Net Asset Value (NAV).

Fidelity Core Dividend ETF: Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer,

political, regulatory, market, or economic developments. Foreign securities are subject to interest rate, currency exchange rate, economic, and

political risks. The securities of smaller, less well-known companies can be more volatile than those of larger companies. There is no guarantee

that a factor-based investing strategy will enhance performance or reduce risk. Before investing, make sure you understand how the fund’s factor

investment strategy may differ from more traditional index funds. Depending on market conditions, fund performance may underperform compared

to funds that seek to track a market capitalization-weighted index. The return of an index ETF is usually different from that of the index it tracks

because of fees, expenses and tracking error. An ETF may trade at a premium or discount to its Net Asset Value (NAV).

Fidelity Dividend ETF for Rising Rates: Stock markets, especially foreign markets, are volatile and can decline significantly in response to

adverse issuer, political, regulatory, market, or economic developments. Foreign securities are subject to interest rate, currency exchange rate,

economic, and political risks. The securities of smaller, less well-known companies can be more volatile than those of larger companies. There is

no guarantee that a factor-based investing strategy will enhance performance or reduce risk. Before investing, make sure you understand how the

fund’s factor investment strategy may differ from more traditional index funds. Depending on market conditions, fund performance may

underperform compared to funds that seek to track a market-capitalization weighted index. The return of an index ETF is usually different from that

of the index it tracks because of fees, expenses and tracking error. An ETF may trade at a premium or discount to its Net Asset Value (NAV).

Fidelity Low Volatility Factor ETF: Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse

issuer, political, regulatory, market, or economic developments. The securities of smaller, less well-known companies can be more volatile than

those of larger companies. There is no guarantee that a factor-based investing strategy will enhance performance or reduce risk. Before investing,

make sure you understand how the fund’s factor investment strategy may differ from more traditional index funds. Depending on market conditions,

fund performance may underperform compared to funds that seek to track a market capitalization-weighted index. The return of an index ETF is

usually different from that of the index it tracks because of fees, expenses, and tracking error. An ETF may trade at a premium or discount to its Net

Asset Value (NAV).

36 For Investment Professionals

Important Information

Fidelity Momentum Factor ETF: Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer,

political, regulatory, market, or economic developments. The securities of smaller, less well-known companies can be more volatile than those of larger

companies. There is no guarantee that a factor-based investing strategy will enhance performance or reduce risk. Before investing, make sure you

understand how the fund’s factor investment strategy may differ from more traditional index funds. Depending on market conditions, fund performance

may underperform compared to funds that seek to track a market capitalization-weighted index. The return of an index ETF is usually different from that

of the index it tracks because of fees, expenses, and tracking error. An ETF may trade at a premium or discount to its Net Asset Value (NAV).

Fidelity Quality Factor ETF: Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer,

political, regulatory, market, or economic developments. The securities of smaller, less well-known companies can be more volatile than those of larger

companies. There is no guarantee that a factor-based investing strategy will enhance performance or reduce risk. Before investing, make sure you

understand how the fund’s factor investment strategy may differ from more traditional index funds. Depending on market conditions, fund performance

may underperform compared to funds that seek to track a market-capitalization weighted index. The return of an index ETF is usually different from that

of the index it tracks because of fees, expenses, and tracking error. An ETF may trade at a premium or discount to its Net Asset Value (NAV).

Fidelity Value Factor ETF: Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political,

regulatory, market, or economic developments. The securities of smaller, less well-known companies can be more volatile than those of larger

companies. Value stocks can perform differently than other types of stocks and can continue to be undervalued by the market for long periods of time.

There is no guarantee that a factor-based investing strategy will enhance performance or reduce risk. Before investing, make sure you understand how

the fund’s factor investment strategy may differ from more traditional index funds. Depending on market conditions, fund performance may

underperform compared to funds that seek to track a market-capitalization weighted index. The return of an index ETF is usually different from that of

the index it tracks because of fees, expenses, and tracking error. An ETF may trade at a premium or discount to its Net Asset Value (NAV).

© 2016 Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its affiliates; (2) may not be

copied or distributed; (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any

damages or losses arising from any use of this information. Morningstar is a registered trademark of Morningstar, Inc., and is not affiliated with Fidelity

Investments.

Third-party trademarks and service marks are the property of their respective owners. All other trademarks and service marks are the property of FMR

LLC or an affiliated company.

Before investing in any mutual fund or exchange traded product, have your client consider its investment objectives, risks, charges, and

expenses. Contact Fidelity for a prospectus, or a summary prospectus if available, containing this information. Have your client read it

carefully.

Fidelity Investments Institutional Services Company, Inc., 500 Salem St., Smithfield, RI 02917.

794494.2.0

37 For Investment Professionals

For financial professional use only. Do not distribute to the public. 38

Thank You