fintech existential threat or another tech...

TRANSCRIPT

Fintech – Existential Threat

or Another Tech Bubble?

Alan McIntyre

Global Banking Practice Leader

Scotland Forever!,1881, Lady Butler

Copyright © 2016 Accenture All rights reserved. 2

Twin threats to traditional banking

Copyright © 2016 Accenture All rights reserved.3

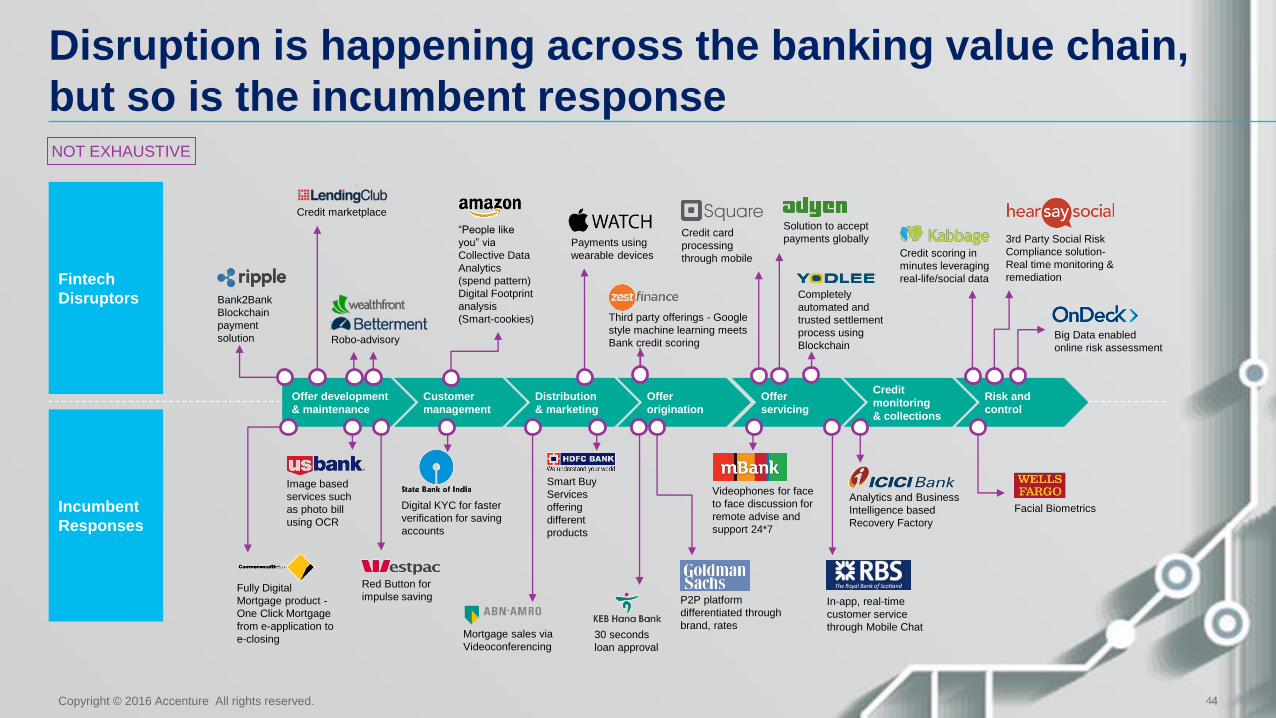

GAAFAFINTECH

4

Customer

management

Distribution

& marketing

Offer

origination

Offer

servicing

Credit

monitoring

& collections

Offer development

& maintenance

Risk and

control

NOT EXHAUSTIVE

Disruption is happening across the banking value chain,

but so is the incumbent response

Copyright © 2016 Accenture All rights reserved. 4

Completely

automated and

trusted settlement

process using

Blockchain

Bank2Bank

Blockchain

payment

solution

“People like

you” via

Collective Data

Analytics

(spend pattern)

Digital Footprint

analysis

(Smart-cookies)

Payments using

wearable devices

Third party offerings - Google

style machine learning meets

Bank credit scoring

3rd Party Social Risk

Compliance solution-

Real time monitoring &

remediation Fintech

Disruptors

Credit scoring in

minutes leveraging

real-life/social data

Robo-advisory

Credit marketplace

Solution to accept

payments globallyCredit card

processing

through mobile

Big Data enabled

online risk assessment

Mortgage sales via

Videoconferencing

Digital KYC for faster

verification for saving

accounts

Analytics and Business

Intelligence based

Recovery Factory

Fully Digital

Mortgage product -

One Click Mortgage

from e-application to

e-closing

Image based

services such

as photo bill

using OCR

Red Button for

impulse saving In-app, real-time

customer service

through Mobile Chat

Facial Biometrics

30 seconds

loan approval

P2P platform

differentiated through

brand, rates

Smart Buy

Services

offering

different

products

Incumbent

Responses

Videophones for face

to face discussion for

remote advise and

support 24*7

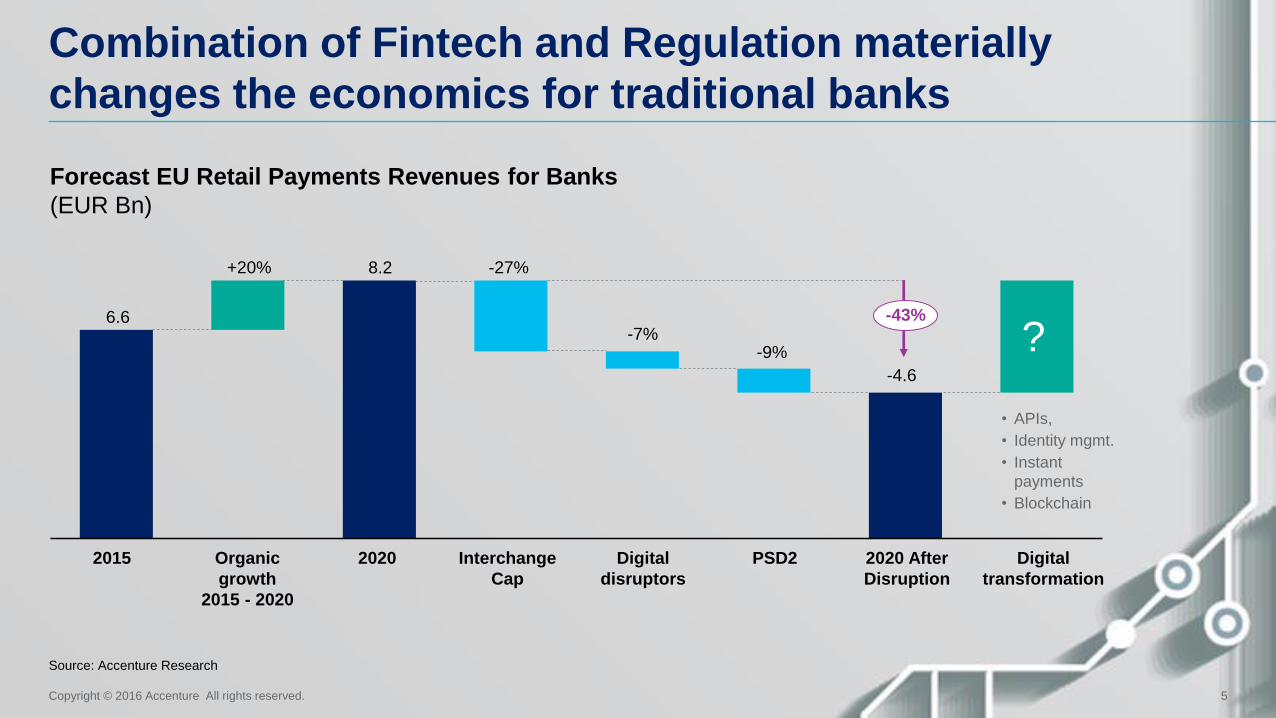

Combination of Fintech and Regulation materially

changes the economics for traditional banks

Copyright © 2016 Accenture All rights reserved. 5

Source: Accenture Research

Forecast EU Retail Payments Revenues for Banks

(EUR Bn)

Organic

growth

2015 - 2020

+20%

6.6

8.2

2015 PSD2

-9%

2020 After

Disruption

Digital

disruptors

-7%

Digital

transformation

Interchange

Cap

-27%

2020

-4.6

-43%

?

• APIs,

• Identity mgmt.

• Instant

payments

• Blockchain

Dual-speed IT

Bureaucratic

Amnesiac

Customer as supplicant

Economically challenged

Poor customer experience

Channel silos not solutions

One stop shop

In my community

Regulated and safe

Transactional trust

A familiar face

Good at complicated

6

Traditional Bank

Copyright © 2016 Accenture All rights reserved.

Customer in control

Simple and elegant

Exciting and new

Low-cost

Adaptive and intelligent

Digital native technology

Digital community and UGC

7

Mobile Bank

Copyright © 2016 Accenture All rights reserved.

Utopian

Basic products

Faceless

Transient?

Unregulated

Equity burn not equity return

Stateless

• Happy customers, regulators and

shareholders

• ‘Digital+’ not ‘Physical+’ mentality

• Uncompromising cross-channel

CustX

• Less branches and people, but

higher stakes

• Phydigital communities

• F2B technology strategy

• On-demand complexity

• Co-opt or scare off Fintech

Traditional

Bank

Mobile

Bank

8Copyright © 2016 Accenture All rights reserved.

Phone

Branch

Sales

force

ATM

Online

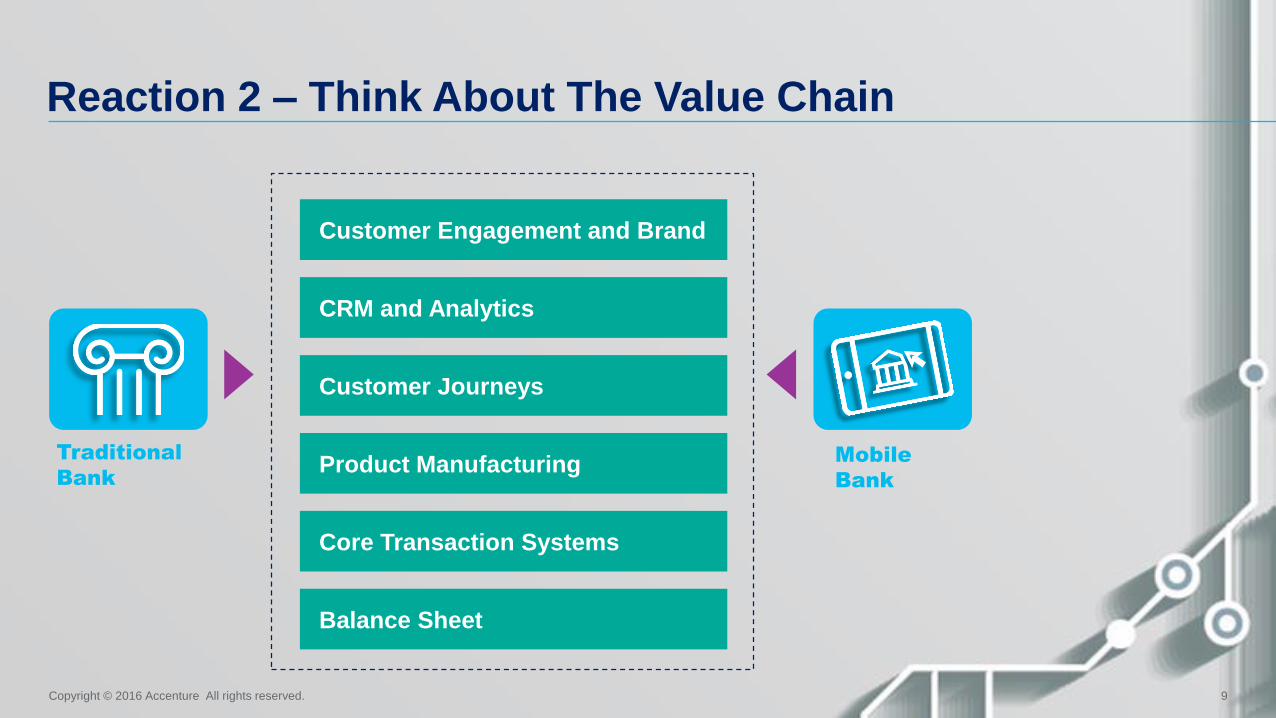

Reaction 1 – Be The Best Version of Yourself

Customer Engagement and Brand

CRM and Analytics

Customer Journeys

Product Manufacturing

Core Transaction Systems

Balance Sheet

Reaction 2 – Think About The Value Chain

9Copyright © 2016 Accenture All rights reserved.

Traditional

Bank

Mobile

Bank

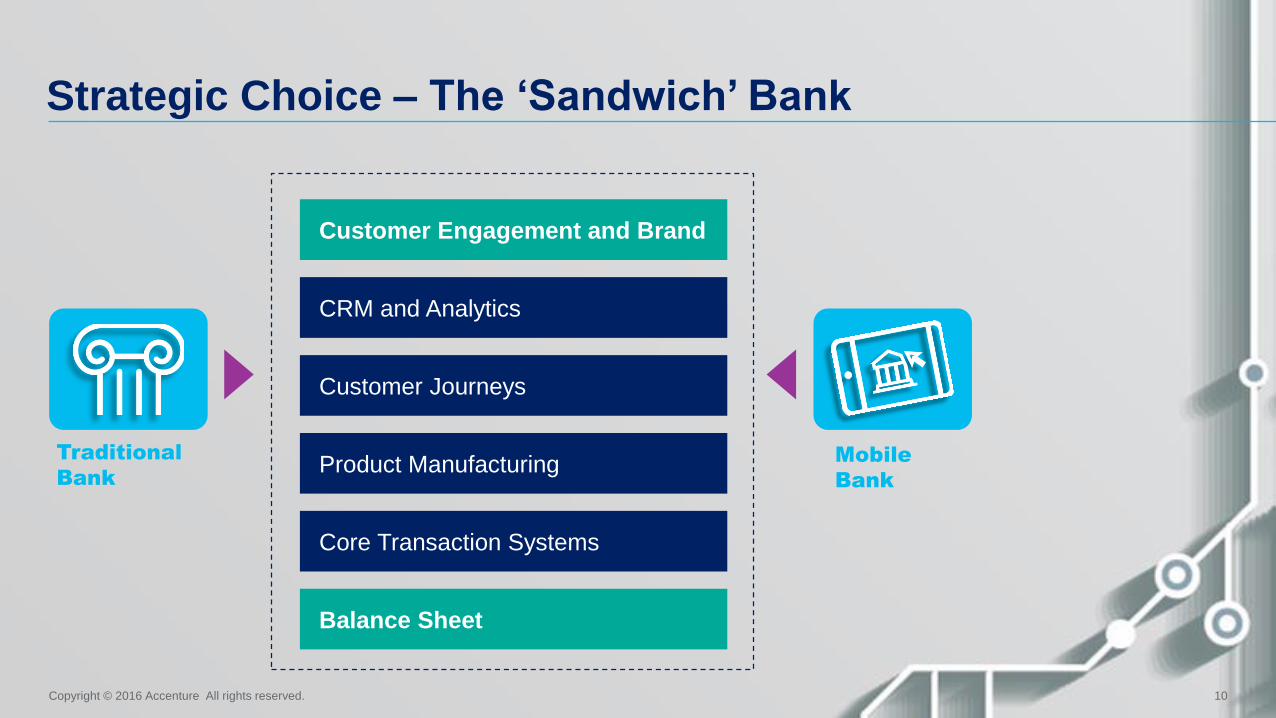

Strategic Choice – The ‘Sandwich’ Bank

10Copyright © 2016 Accenture All rights reserved.

Customer Engagement and Brand

CRM and Analytics

Customer Journeys

Product Manufacturing

Core Transaction Systems

Balance Sheet

Traditional

Bank

Mobile

Bank

11Copyright © 2016 Accenture All rights reserved.

Customer Engagement and Brand

CRM and Analytics

Customer Journeys

Product Manufacturing

Core Transaction Systems

Balance Sheet

Traditional

Bank

Mobile

Bank

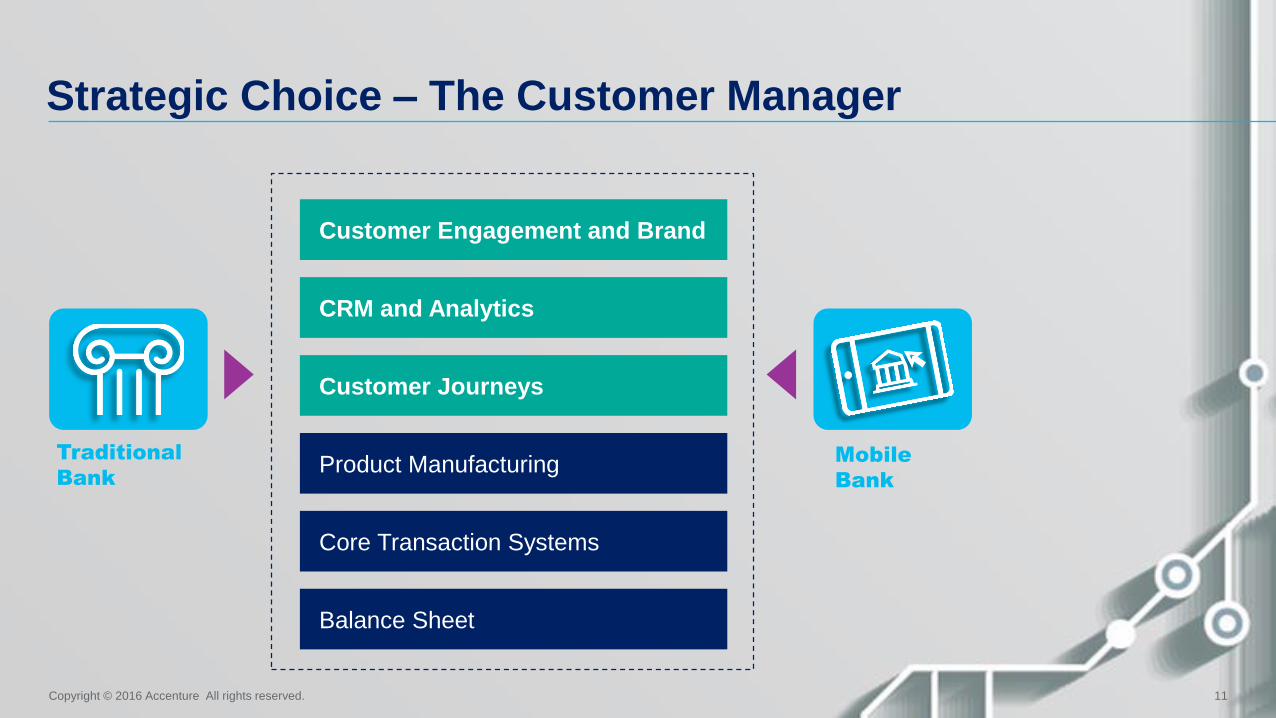

Strategic Choice – The Customer Manager

12Copyright © 2016 Accenture All rights reserved.

Customer Engagement and Brand

CRM and Analytics

Product Manufacturing

Core Transaction Systems

Balance Sheet

Traditional

Bank

Mobile

Bank

Strategic Choice – The Partnership Bank

Customer Journeys

13Copyright © 2016 Accenture All rights reserved.

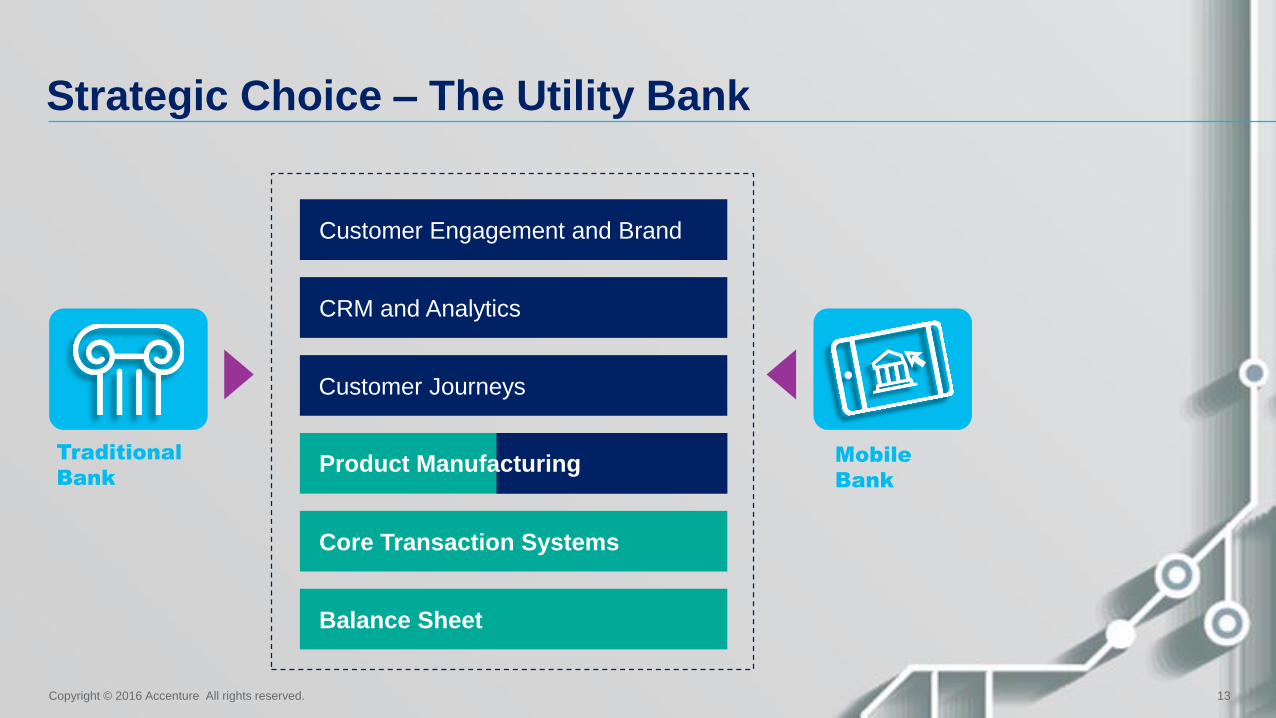

Customer Engagement and Brand

CRM and Analytics

Core Transaction Systems

Balance Sheet

Traditional

Bank

Mobile

Bank

Strategic Choice – The Utility Bank

Customer Journeys

Product Manufacturing

Challenge and opportunity means winners and losers

Innovation

from outside

the banking

sector is

new and

threatening.

14Copyright © 2016 Accenture All rights reserved.

Fintech

capabilities

give banks the

opportunity to

be the best

version of

themselves.

Technology

and regulators

are creating

new business

models that

can be

opportunities

or threats.

The winners in

traditional

banking will

be able to

optimize

across both

dimensions.

Normal VC

rules will apply

to FinTech,

while GAAFA

is more the

existential

threat.

BANKING IS

GETTING A

LOT MORE

INTERESTING

AND

COMPLICATED!