first came fatca, now comes the automatic exchange of information: is it just "copy &...

TRANSCRIPT

Regulatory

Serge Garazi – Interim Project Leader “Bank Regulatory”

Update

First, FATCA.Now, the Automatic Exchange of Information- is it just copy & paste?

30 Nov 2015

AEoI after FATCA: just copy&paste? 2

About meEducation

• French-speaking Swiss.• In the Greater Zurich Area for 30 years.• Education:

InformationTechnology

Finance

(Project-)Management

A presentation, based on the combination of IT, Finance and Project-Management.

Ser

ge G

araz

i, 30

Nov

201

5

AEoI after FATCA: just copy&paste? 3

About meProfessional Experience

• Professional Experience:

• Currently:o Board member, VP Operations at Project Management Institute (Switzerland)o Interim Project Leader & Business Analyst «Bank Regulatory»

Ser

ge G

araz

i, 30

Nov

201

5

ABN Amro

T-SystemsDeutsche Telekom

Rothschild Bank

Detecon Consulting

AMSComit

UBSCredit SuisseJulius BaerBNP Paribas

Project Management

Institute

AEoI after FATCA: just copy&paste? 4

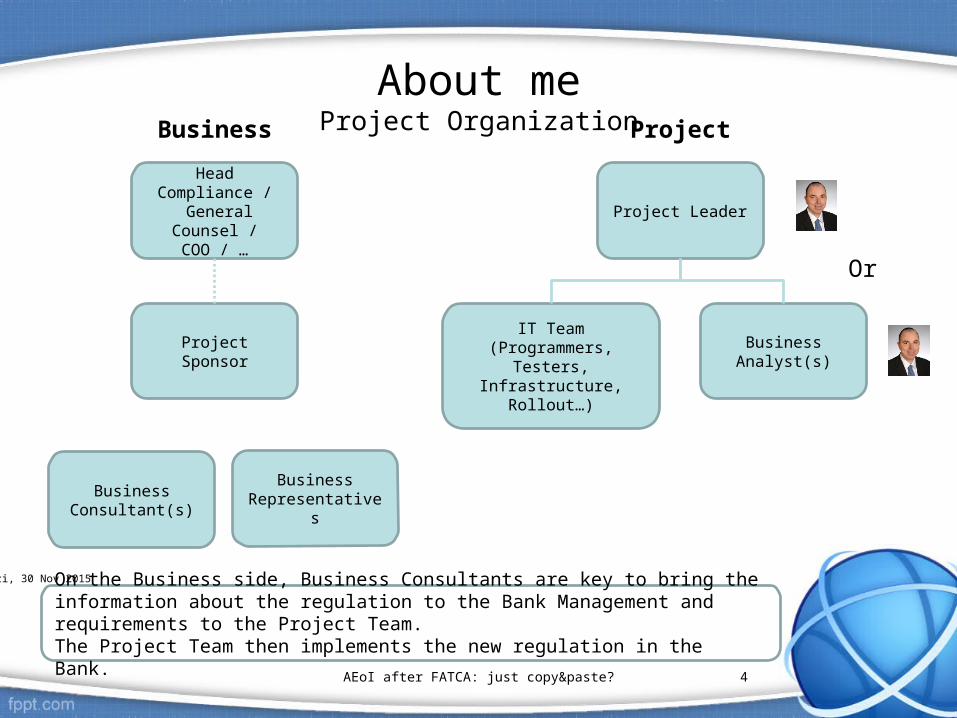

About meProject Organization

On the Business side, Business Consultants are key to bring the information about the regulation to the Bank Management and requirements to the Project Team.The Project Team then implements the new regulation in the Bank.

Head Compliance / General Counsel /

COO / …

Project Sponsor

Business Consultant(s)

BusinessRepresentatives

Project Leader

Business Analyst(s)

IT Team(Programmers, Testers, Infrastructure, Rollout…)

Business Project

Or

Ser

ge G

araz

i, 30

Nov

201

5

AEoI after FATCA: just copy&paste? 5

Welcome on board!

1. Review of the financial crisis2. Regulatory Responses to the Crisis3. FATCA & AEoI

Ser

ge G

araz

i, 30

Nov

201

5

AEoI after FATCA: just copy&paste? 6

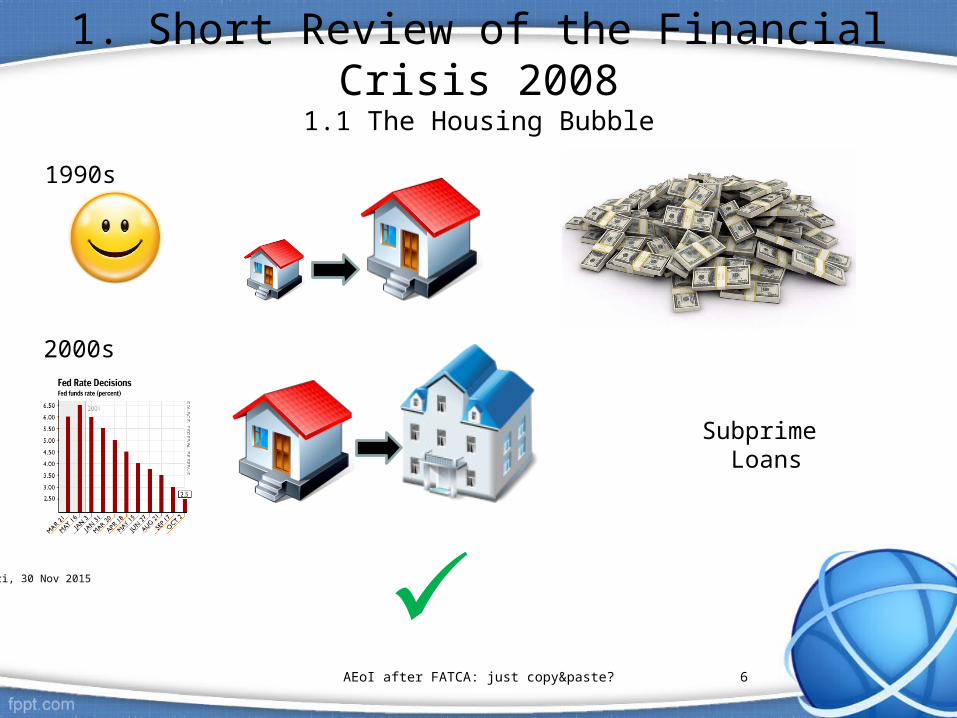

1. Short Review of the Financial Crisis 20081.1 The Housing Bubble

1990s

2000s

Subprime

Loans

Ser

ge G

araz

i, 30

Nov

201

5

AEoI after FATCA: just copy&paste? 7

1. Short Review of the Financial Crisis 20081.2 The Fall

2006

2008

XSer

ge G

araz

i, 30

Nov

201

5

AEoI after FATCA: just copy&paste? 8

1. Short Review of the Financial Crisis 20081.3 The Causes

Deregulation Poor economic policy

Moral hazard

Over-reliance on quantitative models

Excessive leverage

Availability of cheap credit

Dangerous assumptions regarding market dynamics

Undisclosed conflicts of interest

Failure of regulators

Failure of credit rating agencies

Failure of the market

High risk, complex financial products

Lack of transparency

Failures in financial supervision

Failures of corporate governance

Inconsistent action by government

Systemic breakdown in accountability and ethics

Deregulation of OTC Derivatives

High debt

Collapsing mortgage lending standards

Excessive risk-taking

Undisclosed conflicts of interest

Compensation schemes encouraged gambling

Ser

ge G

araz

i, 30

Nov

201

5

Deregulation

AEoI after FATCA: just copy&paste? 9

1. Short Review of the Financial Crisis 20081.4 About Deregulation

2008

“Financial Tsunami”

Ser

ge G

araz

i, 30

Nov

201

5

AEoI after FATCA: just copy&paste? 10

2. Regulatory Responses

2.1 Towards Transparency with OTC Derivatives2.2 Towards Client Protection & Market Efficiency2.3 Towards Bank Resilience

Ser

ge G

araz

i, 30

Nov

201

5

AEoI after FATCA: just copy&paste? 11

2. Regulatory Responses2.1 Towards Transparency in OTC Derivatives

Ser

ge G

araz

i, 30

Nov

201

5

AEoI after FATCA: just copy&paste? 12

2. Regulatory Responses2.1 Towards Transparency in OTC Derivatives

Warren Buffet“derivatives are financial weapons of mass destruction, carrying dangers that, while now latent, are potentially lethal.” (2003)

Ser

ge G

araz

i, 30

Nov

201

5

AEoI after FATCA: just copy&paste? 13

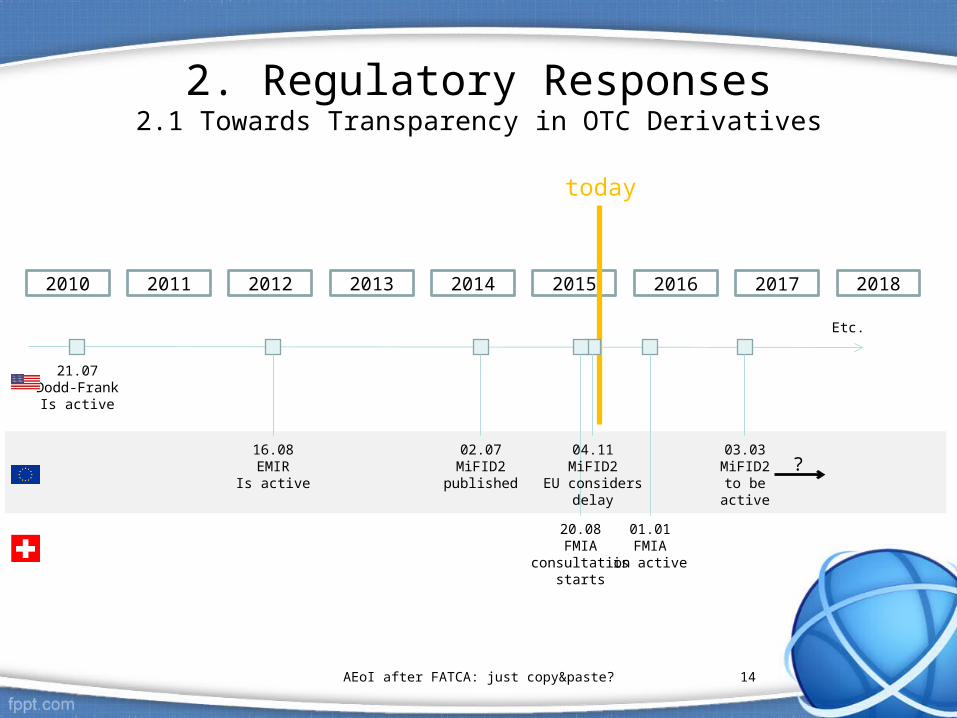

2. Regulatory Responses2.1 Towards Transparency in OTC Derivatives

• Situation:o OTC (over-the-counter) Derivatives were not regulated

• Problems:o No Transparencyo Excessive risk-taking

• Solutions (G-20):o Trade standardized OTC Derivatives on exchangeso Clear OTC Derivatives centrallyo Report OTC Derivatives

• Involved regulations:o USA: Wall Street Reform and Consumer Protection Act (Dodd-Frank Act)o EU:

- European Market Infrastructure Regulation (EMIR)- Markets in Financial Instruments Directive 2 (MiFID2)

o CH: Financial Markets Infrastructure Act FMIA (DE: FinfraG, FR: LFIM)

USD180bn !

Ser

ge G

araz

i, 30

Nov

201

5

AEoI after FATCA: just copy&paste? 14

2. Regulatory Responses2.1 Towards Transparency in OTC Derivatives

2010 2011 2012 2014 20152013 2016 2017 2018

21.07Dodd-Frank

Is active

today

Etc.

16.08EMIR

Is active

20.08FMIA

consultationstarts

01.01FMIA

is active

02.07MiFID2

published

03.03MiFID2to beactive

04.11MiFID2

EU considersdelay

?

AEoI after FATCA: just copy&paste? 15

2. Regulatory Responses2.1 Towards Transparency in OTC Derivatives

IMPORTANT: This book is a very niche and specific piece relevant to a small target audience of potential clients of the Affinity business. Please consider whether it is relevant to you before buying it.

Despite of the seriousness of the subject, … keep having humor!

Ser

ge G

araz

i, 30

Nov

201

5

AEoI after FATCA: just copy&paste? 16

2. Regulatory Responses2.2 Towards Client Protection & Market Efficiency

• Problems:o Loans were given to persons who could not afford themo Conflict of interest between banks’ interests & their Clients’ interestso Banks didn’t understand the products they sold

• Solution:o Rules of conduct for financial intermediaries (e.g. with inducements)o Info requirements about financial institutes and their products and serviceso Suitability and appropriateness tests

• Involved regulations:o USA: Dodd-Frank Acto EU: MiFID2o CH:

- Financial Institution Act FinIA (DE: FINIG, FR: LEFIN) - Federal Financial Services Act FFSA (DE: FIDLEG, FR: LSFIN)

Ser

ge G

araz

i, 30

Nov

201

5

AEoI after FATCA: just copy&paste? 17

2. Regulatory Responses2.2 Towards Client Protection & Market Efficiency

2010 2011 2012 2014 20152013 2016 2017 2018

21.07Dodd-Frank

Is active

today

Etc.

04.11FinSA/FinIA

Draftspublished

01.01FinSA/FinIAare active

02.07MiFID2

published

03.01MiFID2to beactive

02.07MiFID2

EU considersdelay

?

?

AEoI after FATCA: just copy&paste? 18

2. Regulatory Responses2.3 Towards Bank Resilience

• Problems:o Capital cushion was depleted by moving items off-balance sheeto Liquidity was insufficiently taken care ofo Banks grew so large that they threatened existence of states

• Solutions:o Increase of required capitalo Liquidity requirementso Too big to fail

• Involved regulations:o USA: Dodd-Frank Act, etc.o EU:

- Capital Requirement Directive CRD IV/CRR - Bank Recovery & Resolution Directive (BRRD)

o World- Basel III

o Switzerland- Too big to Fail (TBTF)S

erge

Gar

azi,

30 N

ov 2

015

AEoI after FATCA: just copy&paste? 19

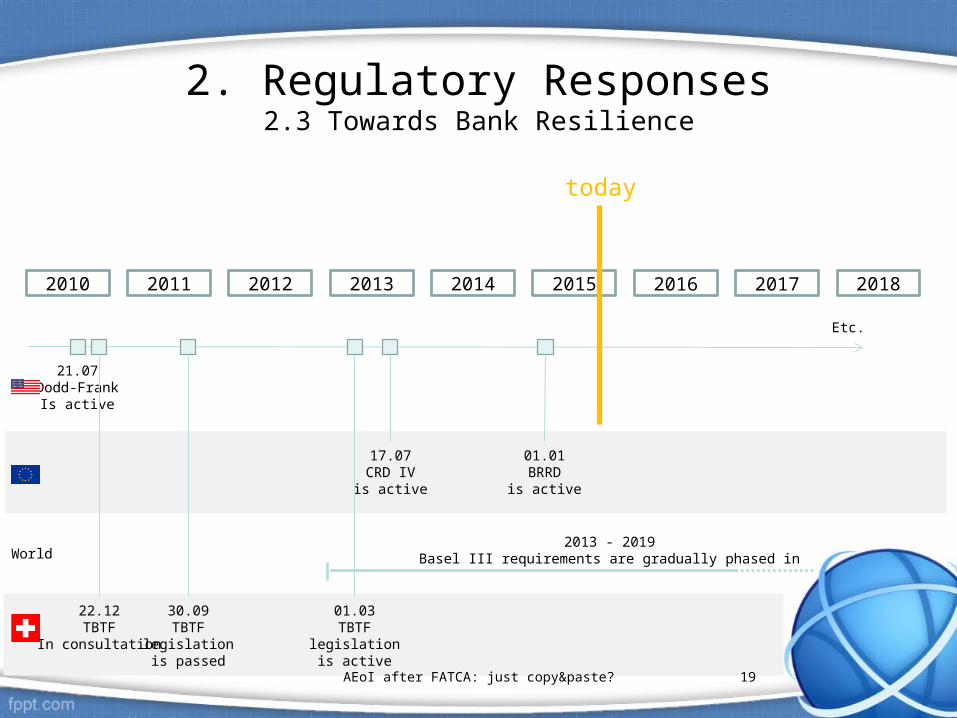

2. Regulatory Responses2.3 Towards Bank Resilience

2010 2011 2012 2014 20152013 2016 2017 2018

21.07Dodd-Frank

Is active

today

Etc.

17.07CRD IVis active

2013 - 2019Basel III requirements are gradually phased in

01.01BRRD

is active

World

22.12TBTF

In consultation

30.09TBTF

legislationis passed

01.03TBTF

legislationis active

AEoI after FATCA: just copy&paste? 20

2. Regulatory Responses2.4 Towards international Tax Compliance

Problem

Solution

Consequence SwissBankingSecrecy

(For outside CH)

(UK-FATCA)

FATCA and AEoI cause the death of the Swiss Banking Secrecy, except for people who are non-US persons and tax-resident only in Switzerland. S

erge

Gar

azi,

30 N

ov 2

015

AEoI after FATCA: just copy&paste? 21

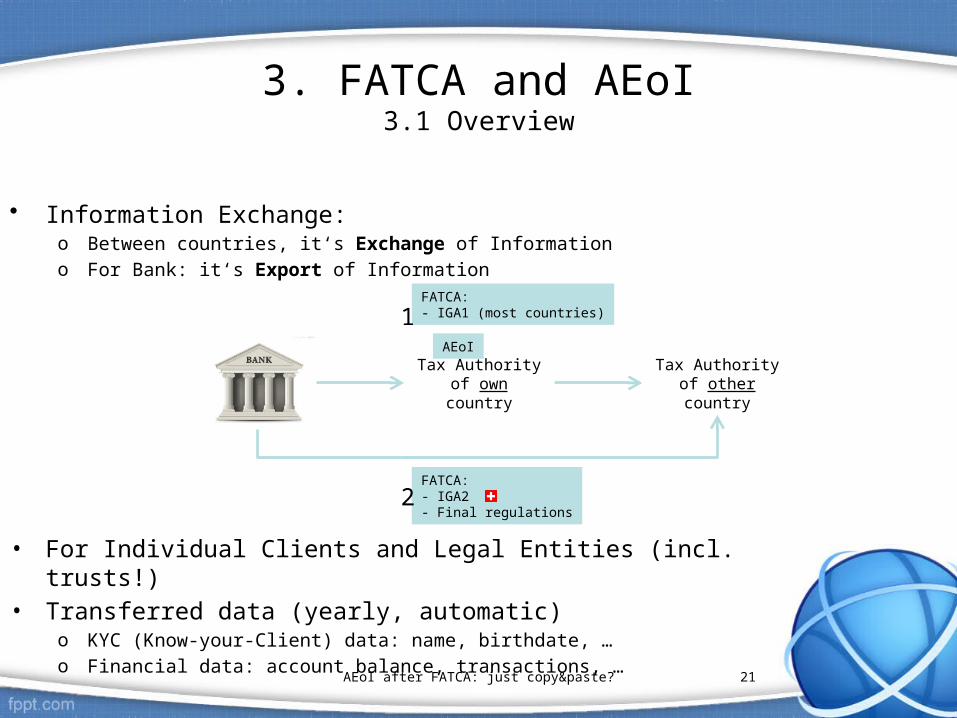

3. FATCA and AEoI3.1 Overview

• Information Exchange:o Between countries, it‘s Exchange of Informationo For Bank: it‘s Export of Information

• For Individual Clients and Legal Entities (incl. trusts!)• Transferred data (yearly, automatic)

o KYC (Know-your-Client) data: name, birthdate, …o Financial data: account balance, transactions, …

Tax Authority of other country

Tax Authority of own country

FATCA: - IGA2 - Final regulations

FATCA: - IGA1 (most countries)

AEoI

1

2

AEoI after FATCA: just copy&paste? 22

3. FATCA and AEoI3.2 FATCA

• «Foreign Account Tax Compliance Act»• US-triggered, applies to the whole world• Obligation to Identify, Report, Withhold• Based on «Nationality++» & Indicia

• Intergovernmental Agreements (IGA)o IGA1 (most countries)o IGA 2 (few countries, e.g. Switzerland)o Final Regulations

https://www.irs.gov/Businesses/Corporations/Foreign-Account-Tax-Compliance-Act-FATCA

FATCA requires that banks around the world report their American Clients to the Internal Revenue Services, in the US.S

erge

Gar

azi,

30 N

ov 2

015

AEoI after FATCA: just copy&paste? 23

3. FATCA & AEoI3.2 FATCA

Impact for Banks– Re-think of business model with US Clients– Classify US Clients and report them to the Internal Revenue Service (IRS)

Impact for Clients – Possibly have to fill up some forms to determine their status– For US-Persons: Have their financial data reported to the IRS

Cost: USD20bn worldwide

(source: Wikipedia)

Ser

ge G

araz

i, 30

Nov

201

5

AEoI after FATCA: just copy&paste? 24

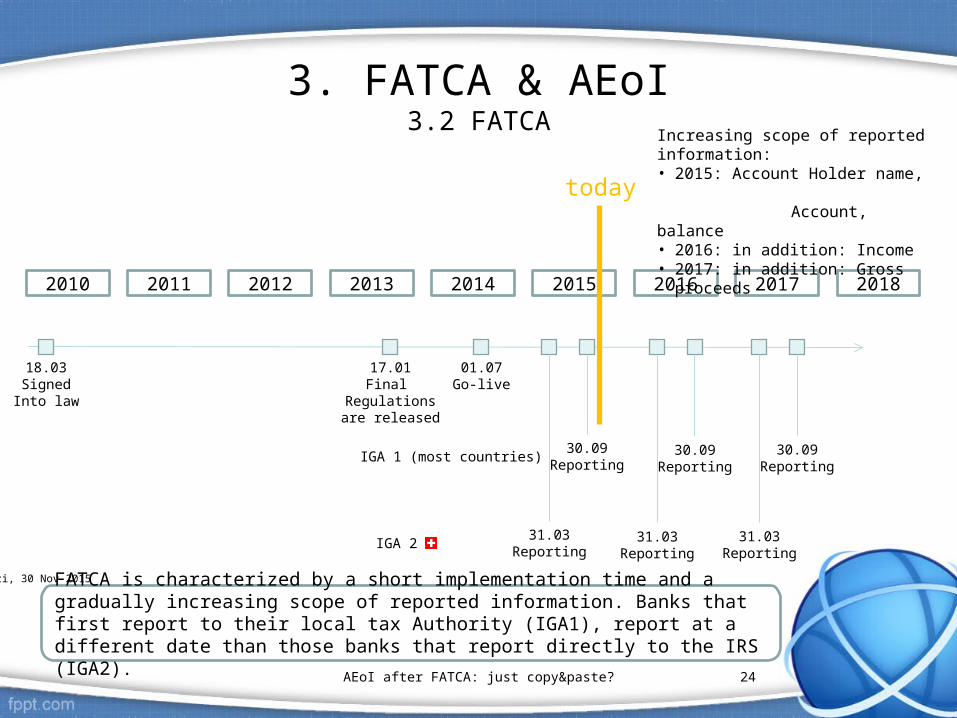

3. FATCA & AEoI3.2 FATCA

2010 2011 2012 2014 20152013 2016 2017 2018

18.03SignedInto law

01.07Go-live

31.03Reporting

today

30.09Reporting

Increasing scope of reported information:• 2015: Account Holder name, Account, balance• 2016: in addition: Income• 2017: in addition: Gross proceeds

17.01Final

Regulationsare released

IGA 1 (most countries)

IGA 2

FATCA is characterized by a short implementation time and a gradually increasing scope of reported information. Banks that first report to their local tax Authority (IGA1), report at a different date than those banks that report directly to the IRS (IGA2).

31.03Reporting

30.09Reporting

31.03Reporting

30.09Reporting

Ser

ge G

araz

i, 30

Nov

201

5

AEoI after FATCA: just copy&paste? 25

3. FATCA & AEoI3.3 AEoI

• “Standard for Automatic Exchange of Financial Information in Tax Matters”• OECD-triggered, targeting the whole world, except USA• Based on bilateral agreements, reciprocal• Obligation to Identify & Report, Withhold• Based on Tax Residence (& indicia)• Made of

o Model Competent Authority Agreemento CRS (Common Reporting Standard)o Commentaries

• 2 main dates per booking center:o Effective date: start of AEoI for the booking center (e.g. Switzerland: 01.01.2017)o Agreement Activation dates: per country pair (booking Center, country X)

o In other languages: o German: Automatischer Informationsaustausch (AIA)o French: Echange Automatique d’Information (EAI)

http://www.oecd.org/tax/Transparency/automaticexchangeofinformation.htm

AEoI after FATCA: just copy&paste? 26

3. FATCA & AEoI3.3 AEoI

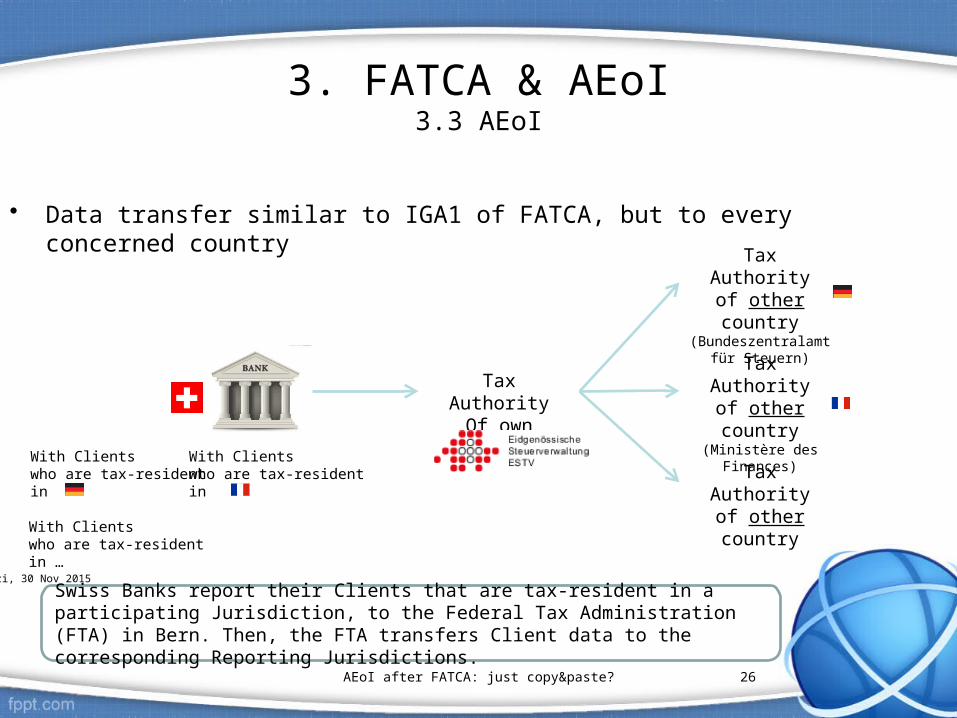

• Data transfer similar to IGA1 of FATCA, but to every concerned country

Tax AuthorityOf own country

Tax Authorityof other country(Bundeszentralamt für

Steuern)

With Clientswho are tax-residentin

Tax Authorityof other country

(Ministère des Finances)

Tax Authorityof other country

Swiss Banks report their Clients that are tax-resident in a participating Jurisdiction, to the Federal Tax Administration (FTA) in Bern. Then, the FTA transfers Client data to the corresponding Reporting Jurisdictions.

With Clientswho are tax-residentin …

Ser

ge G

araz

i, 30

Nov

201

5

With Clientswho are tax-residentin

AEoI after FATCA: just copy&paste? 27

3. FATCA & AEoI3.3 AEoI

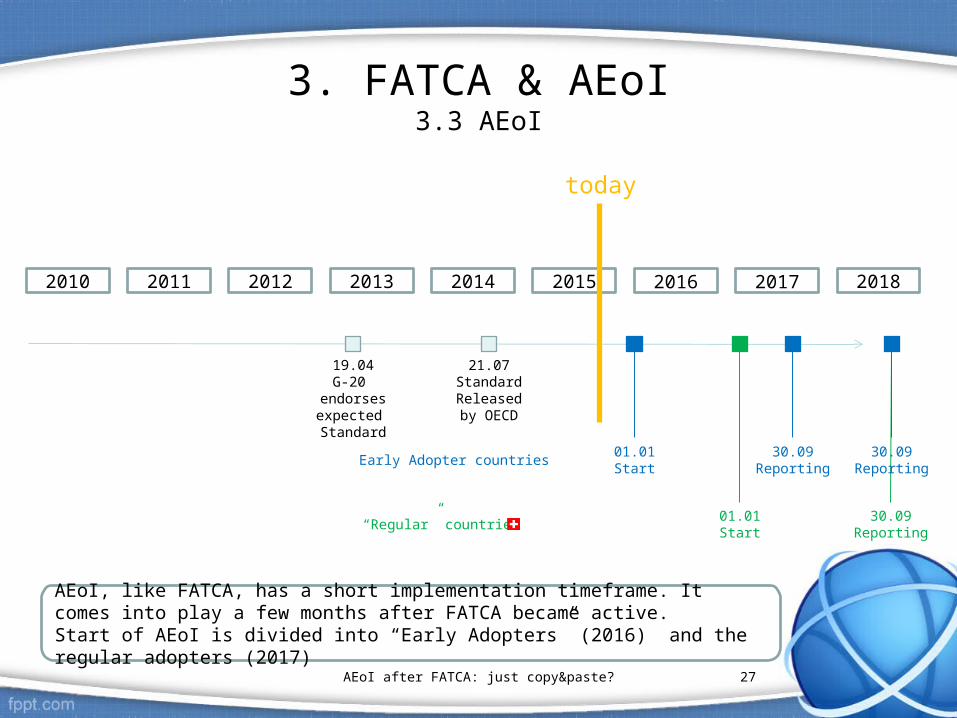

2010 2011 2012 2014 20152013 2016 2017 2018

21.07StandardReleasedby OECD

today

01.01Start

01.01Start

30.09Reporting

19.04G-20

endorsesexpected Standard

Early Adopter countries

“Regular” countries

30.09Reporting

30.09Reporting

AEoI, like FATCA, has a short implementation timeframe. It comes into play a few months after FATCA became active.Start of AEoI is divided into “Early Adopters” (2016) and the regular adopters (2017)

AEoI after FATCA: just copy&paste? 28

3. FATCA & AEoI3.3 AEoI

Impact for Banks– Re-think business model as tax-compliant advising different from tax-not-compliant – Implementation and operational effort to deliver Client-related data to tax authorities– Costs

Impact for Clients– Most were not concerned by FATCA, most will be for CRS– Be reported to every country where tax-resident– New documents (Self-Certification, Documentary Evidence)

Cost: CHF300m-600m for S

witzerland

(source: Swissbanking.org)

As for FATCA, the AEoI causes a potential re-think of the Bank’s business model. It then creates both implementation and operational costs for the Bank, without added benefit to either the Bank or its Clients.S

erge

Gar

azi,

30 N

ov 2

015

AEoI after FATCA: just copy&paste? 29

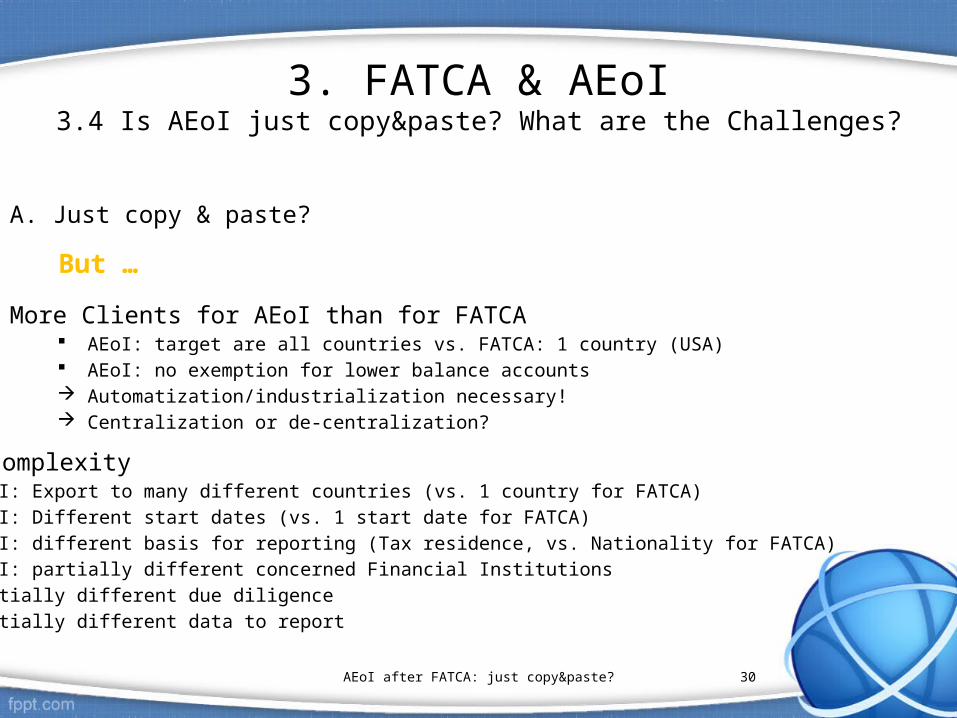

3. FATCA & AEoI3.4 Is AEoI just copy&paste? What are the Challenges?

A. Just copy & paste?

Both are regulations for international tax compliance Both regulations require exporting Client and account information

Yes!

But …

Ser

ge G

araz

i, 30

Nov

201

5

AEoI after FATCA: just copy&paste? 30

3. FATCA & AEoI3.4 Is AEoI just copy&paste? What are the Challenges?

A. Just copy & paste?

More Clients for AEoI than for FATCA AEoI: target are all countries vs. FATCA: 1 country (USA) AEoI: no exemption for lower balance accounts Automatization/industrialization necessary! Centralization or de-centralization?

But …

Higher complexity AEoI: Export to many different countries (vs. 1 country for FATCA) AEoI: Different start dates (vs. 1 start date for FATCA) AEoI: different basis for reporting (Tax residence, vs. Nationality for FATCA) AEoI: partially different concerned Financial Institutions Partially different due diligence Partially different data to report

AEoI after FATCA: just copy&paste? 31

3. FATCA & AEoI3.4 Is AEoI just copy&paste? What are the Challenges?

B) Further Project Management challenges (for regulatory projects): Resources

o Availabilityo Competition of resources

Organizationalo Late definition resp. Clarification of topics, o Tight deadlines

Data & Systemso Different involved systemso Complex (unclean) datao Ensure correctness of reported datao Ensure Traceability/auditability of data change

Ser

ge G

araz

i, 30

Nov

201

5

AEoI after FATCA: just copy&paste? 32

3. FATCA & AEoI3.4 Is AEoI just copy&paste? What are the Challenges?

B) Further Project Management challenges: Knowledge & complexity of business and system processes Reporting: Make or Buy?

Massively higher number of concerned accounts and higher complexity are the two main reasons why AEoI is not just a “copy&paste” of FATCA.Further project management challenges make AEoI even more complex to solve.S

erge

Gar

azi,

30 N

ov 2

015

AEoI after FATCA: just copy&paste? 33

First, FATCA.Now, the Automatic Exchange of Information:

- is it just copy & paste?

Serge GaraziZug, SwitzerlandInterim Project Leader “Bank Regulatory”“Making Change become Reality!”

https://www.xing.com/profile/Serge_Garazi

https://ch.linkedin.com/in/sergegarazi

• Review of the Financial Crisis of 2008• Regulatory Responses to Crisis• FATCA & AEoI: just copy&paste? Which challenges?

Thank you for flying “Regulatory Airlines”!

www.garazi.net Web: