first half of the fiscal year ending december 31, 2012 ... half of the fiscal year ending december...

TRANSCRIPT

First Half of the Fiscal Year Ending December 31, 2012

Management Report

Lion CorporationItsuo Hama, Representative Director and President, Executive Officer

August 3, 2012

2

3

Basic Policies for FY2012

The first year of “V-1 Plan”Four Strategies

Establish a medium-term growth trajectory/Strengthen earnings platform

1.Qualitative Growth of Domestic Businesses1.Qualitative Growth of Domestic Businesses

2.Quantitative Expansion of Overseas Businesses2.Quantitative Expansion of Overseas Businesses

3.Development of New Business Value3.Development of New Business Value

4.Enhancement of Organizational Learning Capabilities4.Enhancement of Organizational Learning Capabilities

Business Results for the First Half of Fiscal 2012

5

(US$/BBL) (RM/t)

Business Environment for the First Half of 20121. Trends in raw material prices

Crude oil (Dubai) Crude palm oil (Malaysia)

RM3,480/ton

$106/BBL

Jan. to Jun.FY2011 (actual)

(6.9%)

+5.4%

Y-on-YChange(%)

Jan. to Jun.FY2012 (actual)

Expected average annual price at the

beginning of FY2012Raw material

RM3,240/ton

$111/BBL

RM3,200/ton

$100/BBL

Crude palm oil

Crude oil

0

20

40

60

80

100

120

140

1/08 1/09 1/10 1/11 1/120

500

1000

1500

2000

2500

3000

3500

4000

4500

1/08 1/09 1/10 1/11 1/12

6

Stronger yen

Weaker yen

2. Exchange rate fluctuations

¥0.0749

¥2.68

¥81.8

Jan. to Jun.FY2011 (actual)

2.6% (strong yen)¥79.7¥78.0US$

4.5% (strong yen)¥2.56¥2.50Thai Baht

¥0.0650

Expected average annual price at the

beginning of FY2012

¥0.0698

Jan. to Jun.FY2012 (actual)

6.8% (strong yen)Korean Won

Y-on-YChange(%)Currency Currency rate

fluctuations caused a sales decrease

¥1.3 billion

-20

-10

0

10

20

Jan-11

Feb-11

Mar-

11

Apr-

11

May-

11

Jun-11

Jul-

11

Aug-11

Sep-11

Oct-

11

Nov-

11

Dec-11

Jan-12

Feb-12

Mar-

12

Apr-

12

May-

12

Jun-12

US$

Thai Baht

Korean Won

Jan 2011 = standard

Business Environment for the First Half of 2012

7

97

98

99

100

101

102

103

104

FY2007 FY2008 FY2009 FY2010 FY2011 1H FY2012

97

98

99

100

101

102

103

104

105

106

107

Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12

Annual trends Monthly trends in 1H of FY2012(%)(%)

3. Trends in Domestic Home Products Markets Trends in the total of 42 home product markets in which Lion participates (percentage of previous year’s results)

(Source: INTAGE Inc. SRI Survey) *44 markets until FY2010

No. of units

Amount

Unit priceUnit price

No. of units

Amount

Business Environment for the First Half of 2012

8

90

92

94

96

98

100

102

104

106

108

110

FY2007 FY2008 FY2009 FY2010 FY2011 1HFY2012

Unit price

Amount

No. of unit

(%)

4.Monthly Trends in Domestic OTC Drug Markets Trends in the total of 8 OTC Drug markets in which Lion participates (percentage of previous year’s results.)

(Source: Lion)

Business Environment for the First Half of 2012

9

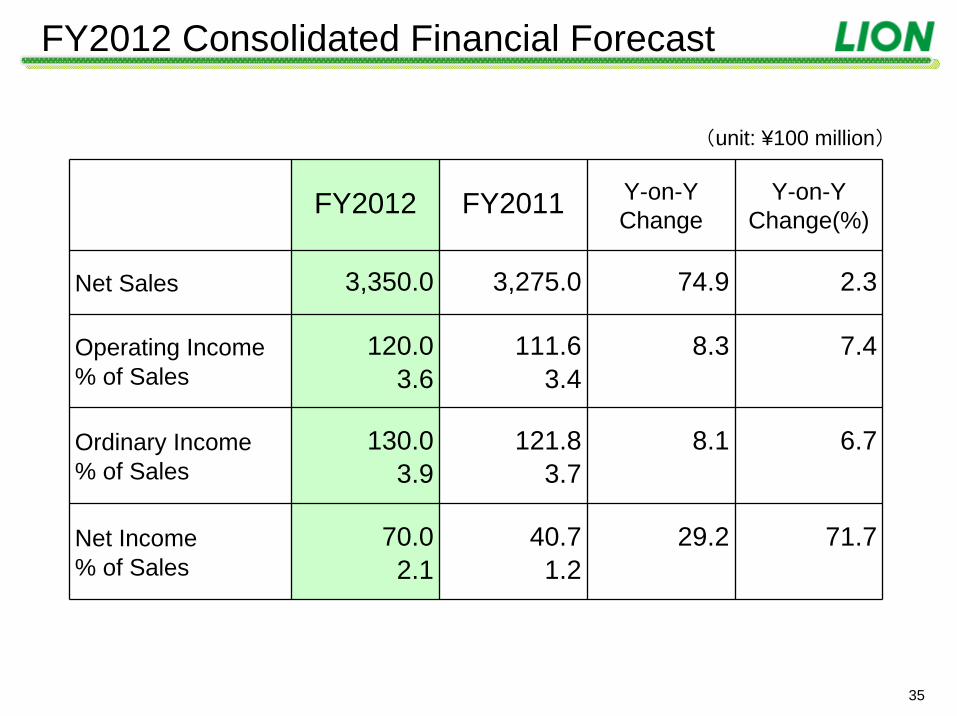

(unit: ¥100 million)

Y-on-YChange

(%)

Y-on-YChange

(%)

Y-on-YChange

15.0

1.0

30.0

1.9

25.0

1.6

1,550.0

Jan.-Jun.FY2012

(forecast)

70.0

2.1

130.0

3.9

120.0

3.6

3,350.0

FY2012(forecast)

Y-on-YChange

FY2011(actual)

Jan.-Jun.FY2011

29.2

8.1

8.3

74.9

71.7

6.7

7.4

2.3

0.4

0.0

40.1

2.7

33.2

2.2

1,514.7

3,025.514.540.7

1.2

Net Income

% of Sales

(25.3)(10.1)121.8

3.7

Ordinary Income% of Sales

(24.8)(8.2)111.6

3.4

Operating Income% of Sales

2.335.23,275.0Net Sales

FY2012 Consolidated Financial Forecast

Full-year revenue and earnings are expected to increase. Although net sales are anticipated to rise, operating income is forecast to decline due to new product releases, brand cultivation and priority investment mainly for proactive advertising to promote Lion’s new corporate message in the first half. Net income is expected to grow due to the absence of a loss on disaster.

Forecast announced on February 10, 2012

10

(22.6)

(5.6)

(10.0)

3.1

Change from forecast

announced on Feb,10, 2012(%)

(3.3)ー11.10.4

0.0

11.6

0.7

Net Income

% of Sales

(1.6)(29.5)(11.8)40.1

2.7

28.3

1.8

Ordinary Income% of Sales

(2.4)(32.3)(10.7)33.2

2.2

22.5

1.4

Operating Income% of Sales

48.75.583.91,514.71,598.7Net Sales

Change from forecast

announced on Feb,10,

2012

Y-on-YChange

(%)

Y-on-YChange

Jan.-Jun.FY2011

Jan.-Jun.FY2012

(unit: ¥100 million)

Financial HighlightsNet Sales and Profits

◇ Net sales exceeded announced figures thanks to favorable domestic and overseas consumerproduct sales

◇Operating income was below announced figures mainly due to increased competition costs, reflecting intensifying competition in stores.

11

Financial HighlightsYear-on-year changes in consolidated operating income

(unit: ¥ 100 million)

33

22

+18

(7)

(1)

(30)

+9

0 10 20 30 40 50 60 70

Operating income for Jan-Jun 2012

Crude oil and vegetable oil

prices

Other expenses

Competition costs

Total cost reduction efforts

(manufacturing and logistics

costs, etc.)

Sales, productmix and others

Operating income for Jan-Jun 2011

Operating income fell ¥1.1. billion year on year due to an increase in competition costs amid intensifying competition in stores. This decrease occurred despite higher sales, comprehensive cost reduction efforts and the absence of loss on disaster following last yearʼs earthquake.

12

Y-on-Ychange(%)

Y-on-Ychange(%)

Net sales Segment income (operating income)

Jan.-Jun.FY2012

Jan.-Jun.FY2011

Y-on-Ychange

Jan.-Jun.FY2012

Jan.-Jun. FY2011

Y-on-Ychange

ConsumerProducts 1,268.1 1,192.7 75.3 6.3 9.3 20.5 (11.2) (54.8)

IndustrialProducts 242.4 249.1 (6.7) (2.7) 0.4 4.6 (4.1) (89.7)

Overseas 283.1 266.8 16.2 6.1 8.7 3.2 5.5 169.4

Other 143.8 117.9 25.8 21.9 4.8 2.7 2.1 77.9

Subtotal 1,937.5 1,826.7 110.7 6.1 23.3 31.1 (7.8) (25.1)

Adjustment (338.7) (311.9) (26.8) - (0.8) 2.0 (2.9) -

Consolidatedtotal 1,598.7 1,514.7 83.9 5.5 22.5 33.2 (10.7) (32.3)

(unit: ¥ 100 million)

Financial Highlights

Consumer Products Business: Despite higher net sales, operating income decreased due to the negative impact of last year’s disaster and intensifying competition.

Industrial Products Business: Revenues and earnings declined because of lower industrial demand.Overseas Business: Performance remained favorable (11.0% in terms of real sales based on local

currencies).

Results by business segment

Net sales include internal net sales within and among segments.

13

Consumer Products:Year-on-year change 6.3%

◇Oral Care Products:Y-o-Y change 18.4%Clinica and Dentor Systema brands, under which new products were released, experienced strong sales. Sales of the high-end toothpaste Dent Health rose 109% compared withthe same period of the previous fiscal year.

◇Beauty Care Products : Y-o-Y change (7.3%)Despite firm sales for hand soaps, antiperspirant and deodorant sales fell year on year due to the negative impactof ongoing lower-than-average temperatures.

◇Pharmaceutical Products: Y-o-Y change (3.5%)Sales of insecticides (pharmaceutical products) and eye drops fell compared with the same period of the previous fiscal year because of market shrinkage and intensifying competition in stores.

Results by Business Segment

14

Consumer Products

◇Fabric Care Products : Y-o-Y change 5.2%Although powder laundry detergent sales fell year on year due tointensifying competition in stores, sales were favorable for fabric softenersand liquid laundry detergents.

◇Living Care Products : Y-o-Y change (4.1%)Sales of household cleaners and dishwashing detergents both decreased

year on year because of intensifying competition in stores.

◇Other : Y-o-Y change 17.4%Overall sales increased substantially year on year owing to strong sales of direct-to-consumer products and pet supplies as well as a recovery in giftproduct sales.

Results by Business Segment

15

Industrial Products Busuness: Y-o-Y change (2.7%)In chemical products, sales of activators derived from oils and fats wereimpacted by the strong yen and intensifying competition, whileelectro-conductive carbon sales were weak amid sluggish industrial demand.In detergents for industrial use, sales of alcohol sanitizers for kitchenswere strong.

Overseas Business: Y-o-Y change 6.1%(up 11.0% based on a local currency basis)

Overall sales enjoyed a double-digit increase (local currency basis) thanksto favorable sales of detergents in Thailand and oral care productsin China. Thailand:Sales of Pao laundry detergent and dishwashing detergent were

favorableSouth Korea:Sales were steady mainly due to Chamgreen capturing

the No.1 dishwashing detergent brand share. China:Sales were robust for Systema toothbrushes and and Zact toothpasteHong Kong:Laundry detergent market share increased thanks to the release

of TOP NANOX

Results by Business Segment

Measures for the Second Half of FY2012 and Progress during the First Year of the

“V-1 Plan” Medium-Term Management Plan

17

◇Direct-to-consumer sales business experienced significant growthfor the second consecutive year

1.Qualitative Growth of Domestic Businesses1.Qualitative Growth of Domestic Businesses

2.Quantitative Expansion of Overseas Businesses2.Quantitative Expansion of Overseas Businesses

3.Development of New Business Value3.Development of New Business Value

◇Favorable sales recorded for the “¥10 billion brands”:Oral care: Clinica, Dentor SystemaLaundry detergents: TOPFabric softeners: SOFLAN

◇ Higher sales for super-concentrated and other types ofliquid laundry detergents

◇Overseas Business experienced double-digit sales increases (local currency basis)

“V-1 Plan” Strategy Implementation and Issues【Achievements】

18

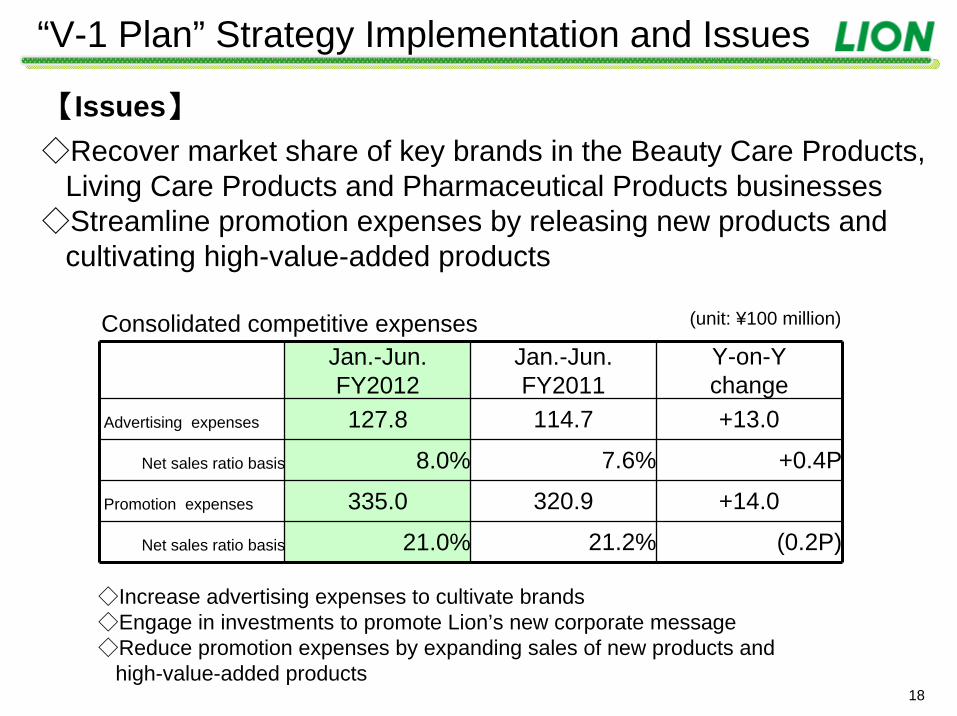

Net sales ratio basis

Promotion expenses

Net sales ratio basis

Advertising expenses

21.0%

335.0

8.0%

127.8

Jan.-Jun.FY2012

21.2%

320.9

7.6%

114.7

Jan.-Jun.FY2011

(0.2P)

+14.0

+0.4P

+13.0

Y-on-Ychange

◇Increase advertising expenses to cultivate brands◇Engage in investments to promote Lion’s new corporate message ◇Reduce promotion expenses by expanding sales of new products and

high-value-added products

◇Recover market share of key brands in the Beauty Care Products,Living Care Products and Pharmaceutical Products businesses

◇Streamline promotion expenses by releasing new products andcultivating high-value-added products

Consolidated competitive expenses (unit: ¥100 million)

【Issues】

“V-1 Plan” Strategy Implementation and Issues

19

Qualitative Growth of Domestic Businesses Oral Care Products

◇Strong sales of new products under the ¥10 Billion Brands:Clinica and Dentor Systema

◇Sales of the high-end toothpaste Dent Health rose 109% compared withthe corresponding period of the previous fiscal year

Dentor SystemaClinica

Toothpaste: Clinica Enamel PearlToothbrush: Clinica Flat Cut

Clinica 3D Cut

Projection comparison129%

Toothbrush:Dentor Systema Haguki PlusSoft type

Projection comparison134%

20

PLALANew releasesin September

platiusLineup expansion

New releases in August

Qualitative Growth of Domestic Businesses Oral Care Products

Issue: Further strengthen products in the mid- to high-end price rangeSecond half initiative: Strengthen toothpaste lineups in the mid- to high-endprice range

21

◇ Strong sales of liquid laundry detergents

Year-on-year comparison 129%(Market growth ratio:111%)

◇Favorable sales of fabric softeners

Year-on-year comparison 112%(Market growth ratio:107%)

Qualitative Growth of Domestic Businesses Fabric Care Products

22

TOP HYGIANew release in July

Kaori to Deodorant no SOFLAN(SOFLAN with Fragrance and Deodorant) Aroma Rich

Fragrance MistNew release in September

Qualitative Growth of Domestic Businesses Fabric Care Products

Issue: Strengthen sales of liquid laundry detergents while regainingmarket share for powder laundry detergents

Second half initiatives:Enhance super-concentrated liquid laundry detergent lineupsCultivate and bolster the SOFLAN brand

23

TOP TOP HYGIAHYGIAInitial shipments (Lion shipping sum)

Projection comparison 153%

Qualitative Growth of Domestic Businesses Fabric Care Products

Released 18, July, 2012

24

Powder detergents35%

Conventionalliquid detergent

35%

Super-concentratedliquid detergents

25%

Super-concentratedliquid detergents

50%

Conventional liquid detergent

15%

Powder detergents30%

Category composition ratio(forecast)FY2012 FY2015

IncreaseIncrease

Become the No.1 company in liquid laundry detergents

Laundry Detergent Market Outlook and Strategy

25

TOP HYGIADetergent that prevents bacteria growth and odors on clothing

TOP NANOXHigh-detergency detergent

Kaori Tsuzuku(Long-Lasting Fragrance) TOP plus Detergent featuring a pleasantly long-lasting fragrance

Pleasant 《Fragrance, softness》

Clean, refreshing《Detergency》

Hygiene & comfort《Antibacterial properties》

Category

Laundry Detergent Market Outlook and Strategy

Offer three super-concentrated detergent varieties to meet consumer detergent needs

26

LOOK Bath Antimold FoggerNew release in September

Qualitative Growth of Domestic Businesses Living care Products

Second half initiative:

Release new LOOK Bath Antimold Fogger

◇ Uses silver ion fog to kill black mold and its spores throughout the bathroom◇ Utilizes fumigation technology cultivated from the development of the Varsan brand

Fumigation technology

Silver ionsterilization+

27

30

40

50

60

70

FY2008 FY2009 FY2010 FY2011 1H

FY2012

Foam

Liquid

(%)

Qualitative Growth of Domestic Businesses Beauty care Products

(Source: INTAGE Inc. SRI Survey, based on monetary amounts)

Second half initiative:Expand lineup of KireiKirei Medicated Foaming Hand Soap (September)

Proportion of sales

28

◇ New products cultivated in the second

◇Continue investing in the marketing of theBUFFERIN brand

Qualitative Growth of Domestic Businesses Pharmaceutical Products

Second half initiative:

29

◇Increase sales channels for electro-conductivecarbon black products for rechargeable battery applications

◇Products experiencing high demand for post-disaster reconstruction: Strengthen sales of Soil stabilizers, repairing materials and superplasticizers for concrete

◇Develop Asian markets: PT. IPPOSHA INDONESIA,LION IDEMITSU COMPOSITES INDIA PVT. LTD

Qualitative Growth of Domestic Businesses Industrial products

Chemical Products

◇ Capture demand from hospitals and othernew users

Detergents for Institutional-Use

Second half initiative:

30

◇Double-digit sales increase (local currency basis)

ThailandPao laundry detergent Favorable sales Year-on-year change

109%

Hong KongNANOX laundry detergentFavorable salesIncreased share of the laundry detergent market

South KoreaChamgreen dishwashing detergent Favorable sales

Captured No. 1 brand sharein the first half of 2012

ChinaSYSTEMA toothbrushFavorable sales

Quantitative Expansion of Overseas Businesses

Year-on-year change

135%

31

Quantitative Expansion of Overseas Businesses

Area expansion(Commence sales in the Philippines and Vietnam)

Boost production capacity

MalaysiaCompletion of laundry detergent

drying towerCommences operations in second half of 2012

PhilippinesSigning ceremony formalizing the

establishment of Peerless LionCommences operations in second half of 2012

32

Development of New Business Value

New product:

Released 17, May

Tomatosu+MilkPeptide Seikatsu

Direct-to-consumer sales channelsRecorded strong sales of such products as Nice rim essence Lactoferrinand accelerate growth in the future

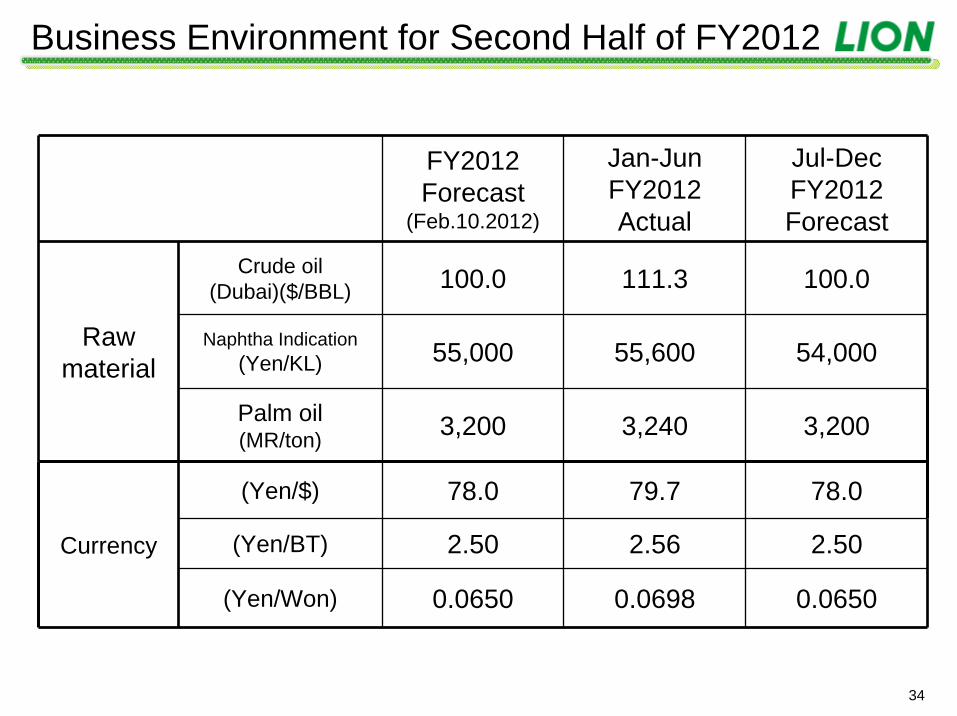

Fiscal 2012 Consolidated Financial Forecast

34

FY2012Forecast

(Feb.10.2012)

Jan-JunFY2012Actual

Jul-DecFY2012Forecast

Rawmaterial

Crude oil (Dubai)($/BBL) 100.0 111.3 100.0

Naphtha Indication(Yen/KL) 55,000 55,600 54,000

Palm oil(MR/ton) 3,200 3,240 3,200

Currency

(Yen/$) 78.0 79.7 78.0

(Yen/BT) 2.50 2.56 2.50

(Yen/Won) 0.0650 0.0698 0.0650

Business Environment for Second Half of FY2012

35

FY2012 FY2011 Y-on-YChange

Y-on-YChange(%)

Net Sales 3,350.0 3,275.0 74.9 2.3

Operating Income% of Sales

120.03.6

111.63.4

8.3 7.4

Ordinary Income% of Sales

130.03.9

121.83.7

8.1 6.7

Net Income% of Sales

70.02.1

40.71.2

29.2 71.7

(unit: ¥100 million)

FY2012 Consolidated Financial Forecast

36

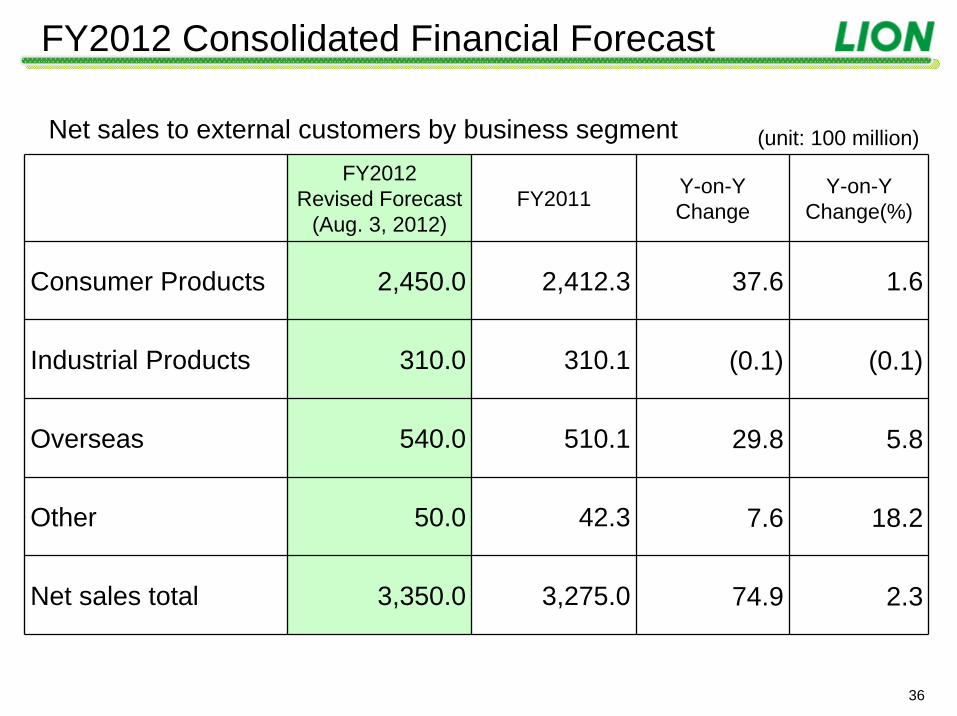

(unit: 100 million)

Y-on-Y Change(%)

FY2012Revised Forecast

(Aug. 3, 2012)FY2011 Y-on-Y

Change

Consumer Products 2,450.0 2,412.3 37.6 1.6

Industrial Products 310.0 310.1 (0.1) (0.1)

Overseas 540.0 510.1 29.8 5.8

Other 50.0 42.3 7.6 18.2

Net sales total 3,350.0 3,275.0 74.9 2.3

Net sales to external customers by business segment

FY2012 Consolidated Financial Forecast

37

Factors Causing Changes in Results Forecasts

◇Increasing costs for market competition due to falling retail prices amid fluctuating economic trends and intensifying competition

◇Intensifying competition among overseas businesses

◇Future Uncertainty caused by high raw material prices and exchange rate fluctuations

FY2012 Consolidated Financial Forecasts

38

Cash Dividends Paid to Shareholders

Payment ratio(Non-consolidated) - 54.7% 47.2% 53.2% 93.0% 65.4% 46.1% 82.4%

FY2004 FY2005 FY2006 FY2007 FY2008 FY2009 FY2010 FY2011 FY2012(Plan)

4 45 5 5

45

5 5 5

5 5 5 5

5 5 5 (5)

0

2

4

6

8

10

12

FY2004 FY2005 FY2006 FY2007 FY2008 FY2009 FY2010 FY2011 FY2012

Year end dividend

Interim dividend

1

(yen)

(Plan)

Dividends per share (annual)

8

109

(10)1010 10 1011

120th Anniversary Commemorative Dividend PaidIn FY2011 as of the year-end: ¥1

The forecasts and projected operating results contained in this

report are based on information available at the time of

preparation, and thus involve inherent risks and uncertainties.

Accordingly, readers are cautioned that actual results may differ

materially from those projected as a result of a variety of factors.

Note: Figures are rounded down to the digits that are displayed.

40

Reference Materials

41

Jan.-Jun.FY2012

Jan.-Jun.FY2011

Y-o-YChange

Y-o-YChange(%)

Net sales 1,598.7 1,514.7 83.9 5.5Cost of sales 693.5 644.2 49.2 7.6

Gross profit 905.1 870.4 34.6 4.0Selling, general and administrativeexpenses 882.6 837.2 45.4 5.4

Operating Income 22.5 33.2 (10.7) (32.3)Non-operating income 10.2 12.2 (1.9) (16.1)Non-operating expenses 4.4 5.3 (0.8) (16.2)

Ordinary income 28.3 40.1 (11.8) (29.5)Extraordinary income ー 0.4 (0.4) ーExtraordinary loss 2.1 33.3 (31.2) (93.7)

Net income before income taxes 26.2 7.2 18.9 261.1Income taxes 8.3 8.7 (0.4) (4.8)Adjustment of income taxes 3.2 (5.0) 8.3 ーMinority interests in earnings ofconsolidated subsidiaries 3.0 3.0 (0.0) (1.8)

Net income 11.6 0.4 11.1 ー

(unit:¥100 million)

Statements of Income (Consolidated)

42

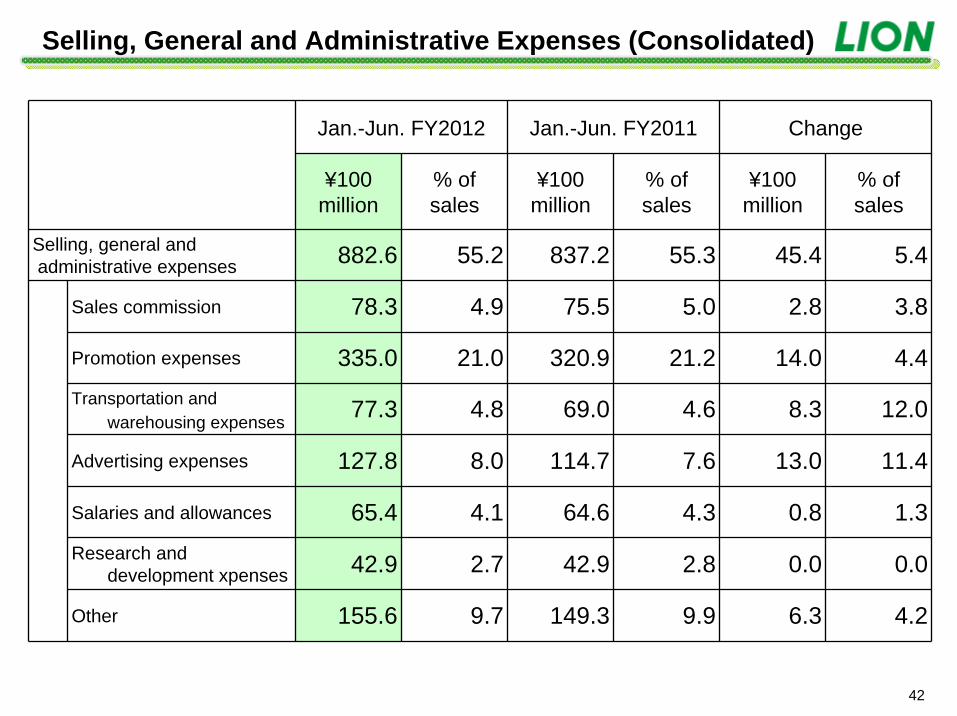

Jan.-Jun. FY2012 Jan.-Jun. FY2011 Change

¥100million

% ofsales

¥100million

% ofsales

¥100million

% ofsales

Selling, general andadministrative expenses 882.6 55.2 837.2 55.3 45.4 5.4

Sales commission 78.3 4.9 75.5 5.0 2.8 3.8

Promotion expenses 335.0 21.0 320.9 21.2 14.0 4.4Transportation and

warehousing expenses 77.3 4.8 69.0 4.6 8.3 12.0

Advertising expenses 127.8 8.0 114.7 7.6 13.0 11.4

Salaries and allowances 65.4 4.1 64.6 4.3 0.8 1.3Research and

development xpenses 42.9 2.7 42.9 2.8 0.0 0.0

Other 155.6 9.7 149.3 9.9 6.3 4.2

Selling, General and Administrative Expenses (Consolidated)

43

Jan.-Jun. FY2012 Jan.-Jun. FY2011

Extraordinary income

Reversal of allowance for doubtful accounts

0.2

Gain on disposal of noncurrent assets

0.2

Total ー Total 0.4

Extraordinary loss

Loss on disposal of noncurrent assets

1.3

Loss on disaster

Loss on disposal of noncurrent assets

28.0

0.3

Impairment loss 0.7 Impairment loss 0.0

. Other 5.0Total 2.1 Total 33.3

Significant Extraordinary Income or Loss (consolidated)

(¥100 million)

44

1H FY2012(Ended Jun 30,

2012)

FY2011(Ended Dec 31,

2011)Change

Current assets 1,251.7 1,272.2 (20.5)

Cash and time deposits 234.2 254.7 (20.5)Notes and accounts receivable-trade 509.5 551.9 (42.3)

Short-term investments 115.9 104.3 11.5

Inventories 322.6 302.5 20.1

Noncurrent assets 1,230.5 1,220.4 10.0

Property, plant and equipment 595.8 585.0 10.7

Intangible assets 195.8 214.8 (19.0)

Investments and other assets 438.8 420.5 18.2

Total assets 2,482.2 2,492.7 (10.5)

Consolidated Balance Sheets (Selected) I(unit: ¥100 million)

45

1H FY2012(Ended Jun. 30, 2012)

FY2011(Ended Dec. 31, 2011) Change

Current liabilities 924.6 946.0 (21.4)Notes and accounts payable-trade 415.0 420.7 (5.7)Short-term loans payable 56.0 51.4 4.6Current portion of long-term loans payable 24.1 24.1 ーAccounts payable-other and accrued expenses 374.2 378.8 (4.6)

Noncurrent liabilities 481.6 494.1 (12.5)Long-term loans payable 238.7 250.8 (12.0)Provision for retirement benefits 191.4 191.5 (0.0)

Capital stock 344.3 344.3 -

Retained earnings 562.6 567.5 (4.8)Treasury stock (165.1) (166.5) 1.4Valuation difference on available-for-sale securities 36.9 30.2 6.7Minority interests 1,075.9 1,052.5 23.4Total liabilities and net assets 2,482.2 2,492.7 (10.5)

Consolidated Balance Sheets (Selected) II(unit: ¥100 million)

46

plan plan

Note: Both capital expenditures and depreciation expenses include amounts for intangible assets.

Capital Expenditures and Depreciation Expenses (consolidated)

Depreciation expensesCapital expenditures(unit:¥100 million)

4051

3926

4562 59 59

60

60

32

5743

60

130

62

485140

6663

0

20

40

60

80

100

120

140

160

180

200

2007 2008 2009 2010 2011 2012 2007 2008 2009 2010 2011 2012

Right of trademarkJul-DecJan-Jun

350

250

304

83

392

106

124 124

79

117 120

63

44

70

120123

47

Consolidated Cash Flow

Jan.-Jun.FY2012

Jan.-Jun.FY2011

Change

Net cash provided by (used in) operating activities 56.8 (98.6) 155.4

Net cash provided by (used in) investment activities (51.5) (53.1) 1.6

Net cash provided by (used in) financing activities (21.1) (48.0) 26.9

Effect of exchange rate change on cash and cash equivalents 0.6 (0.6) 1.2

Net increase (decrease) in cash and cash equivalents (15.1) (200.5) 185.3

Cash and cash equivalents at beginning of period 356.4 445.8 (89.4)

Cash and cash equivalents at end of period 341.2 245.3 95.8

(unit: ¥100 million)

48

Jan.-Jun.FY2012

Jan.-Jun.FY2011

Y-on-YChange

Y-on-Y Change(%)

Consumer Products1,268.1 1,192.7 75.3 6.31,158.8 1,090.4 68.4 6.3

Industrial Products242.4 249.1 (6.7) (2.7)148.0 151.9 (3.9) (2.6)

Overseas283.1 266.8 16.2 6.1267.9 253.1 14.7 5.8

Other143.8 117.9 25.8 21.9

23.9 19.1 4.8 25.1Net sales total 1,937.5 1,826.7 110.7 6.1Sales to external customers total 1,598.7 1,514.7 83.9 5.5

Net sales and sales to external customers

Results by business segment (consolidated)

(unit: ¥100 million)

Upper line: Net sales; Lower line: Sales to external customersNet sales include internal net sales within and among segments.

The forecasts and projected operating results contained in this

report are based on information available at the time of

preparation, and thus involve inherent risks and uncertainties.

Accordingly, readers are cautioned that actual results may differ

materially from those projected as a result of a variety of factors.

Note: Figures are rounded down to the digits that are displayed.