first quarter 2018 ncreif indices review · special thanks to kevin scherer, ncreif consultant for...

TRANSCRIPT

First Quarter 2018NCREIF Indices Review

May 10, 2018

Panelist Overview

Jeff Fisher

NCREIF Data & Research Consultant

Will McIntosh

Global Head of Research

USAA Real Estate Company

Special thanks to Kevin Scherer, NCREIF Consultant for Slides from NCREIF Analytics

Disclaimer

Today we will be presenting what we see in the NCREIF data, trends and changes; all comments about future expectations are the personal views of the speakers (and could be wrong!) and not a reflection of a NCREIF opinion or forecast.

Overview

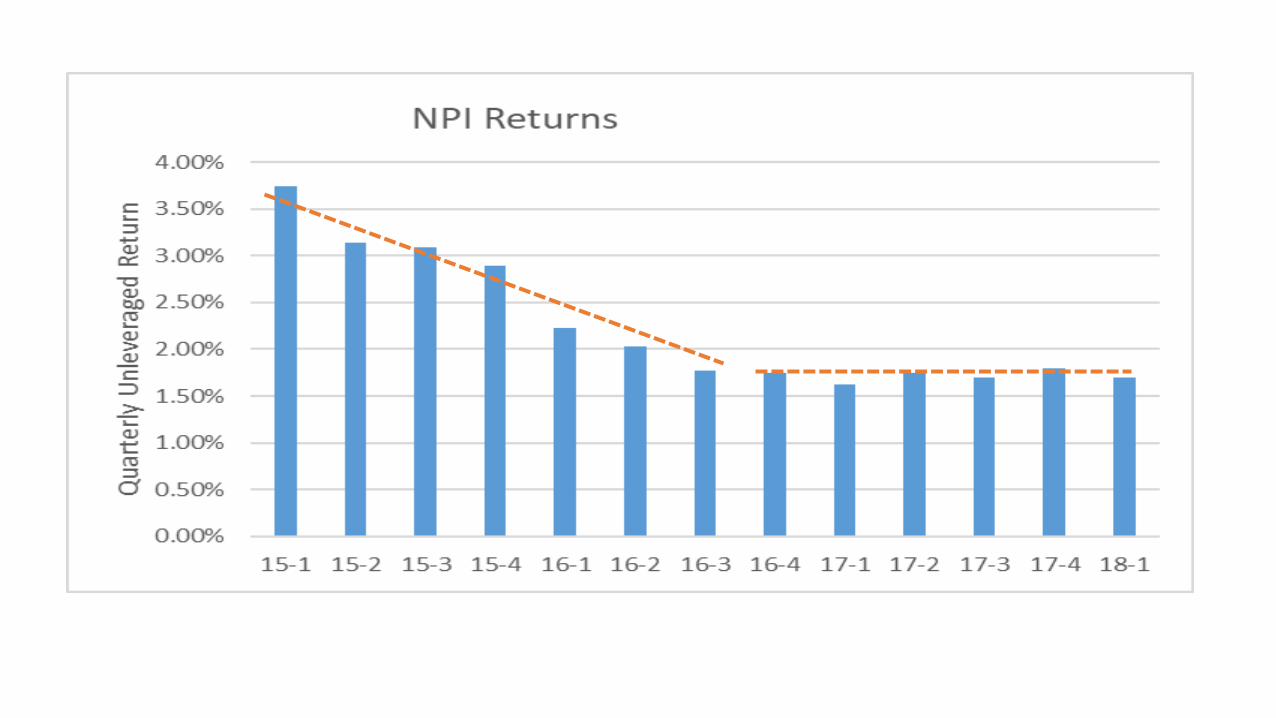

• NPI starts year on slight down tick from 4th quarter 2017

• But up slightly from 1st quarter of 2017

• Volatility of total returns continue at a historic low

• Tale of Two Markets

• Industrial remains by far the top performer

• Retail the worst performer

• Net NFI-ODCE fund inflows = outflows

• Occupancy holding near its 15-year high

• Rental growth strong for undustrial but week for all other sectors

4

NCREIF OverviewFirst Quarter 2018 Index Composition

5

NCREIF Property Index

(NPI)

NPI Leveraged Property Index

NFI-ODCE (Fund Index – Gross of

Fees)

Farmland Properties

Timberland Properties

Leverage Unlevered 44% 22% Unlevered Unlevered

Quarterly Return

1.7% 1.9% 2.2% 1.3% 0.9%

1 Year Return

7.1% 8.9% 8.1% 7.1% 3.8%

1.7% 2.0%1.3% 0.9%

2.2%

-6.7%

-0.8%

7.1%8.3%

7.1%

3.7%

8.1%

-1.1%

14.0%

6.1% 6.5%

12.1%

4.0%5.1%

6.9%

9.5%

-10%

-5%

0%

5%

10%

15%

20%

NPI NPI Levered Farmland Timberland NFI-ODCE NAREIT S&P 500

Tota

l Re

turn

3/31/2018 1-Yr 10-Yr Avg

Total Returns by Asset Class

Chart: 260

-6%

-1%

4%

9%

14%

19%

2013 2014 2015 2016 2017 2018

Tota

l Re

turn

Agricultural Total Returns

NPI Farmland Timber

Agricultural Total Returns

Annual

Chart: 252

-47%

-37%

-27%

-17%

-7%

3%

13%

23%

33%

2013 2014 2015 2016 2017 2018

NO

I Gro

wth

Agricultural NOI Growth

NPI Farmland Timber

Agricultural NOI Growth

Annual

Chart: 254

Question

• What will be the best performing asset class in 2018?• A. NCREIF Leveraged Returns

• B. Farmland

• C. S&P 500 Stocks

• C. Corporate Bonds

• E. NAREIT Index

9

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

1983 1987 1991 1995 1999 2003 2007 2011 2015

Income Return Appreciation Return Total Return

NPI Returns

Annual

Chart: 261

-72%

-52%

-32%

-12%

8%

28%

48%

1993 1996 1999 2002 2005 2008 2011 2014 2017

Tota

l Re

turn

5th Percentile 25th Percentile 50th Percentile 75th Percentile 95th Percentile

NPI Total Returns by Percentile Distribution

Annual

Chart: 198

14

Note: The Market Value Index (MVI) is an equal-weighted index and excludes expansion capital expenditures.

Prices Still Rising

Question

• When will the Market Value Index (MVI) peak for this cycle?• A. Peaked in 2017

• B. 2018

• C. 2019

• D. 2020 or later

15

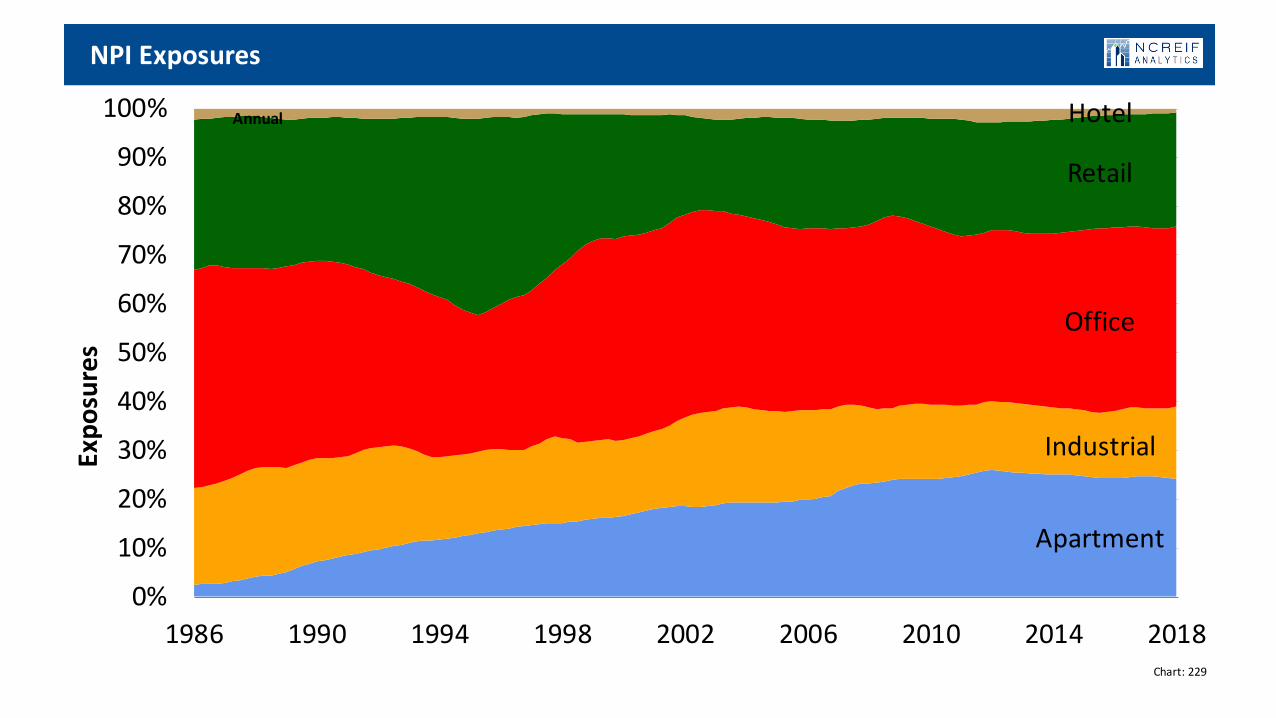

Apartment

Industrial

Office

Retail

Hotel

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1986 1990 1994 1998 2002 2006 2010 2014 2018

Exp

osu

res

NPI Exposures

Annual

Chart: 229

2%

4%

6%

8%

10%

12%

14%

16%

2012 2013 2014 2015 2016 2017 2018

Tota

l Re

turn

Returns by Property Type

NPI Apartment Industrial Office Retail

Returns by Property Type

Annual

Chart: 6

Tale of Two Sectors

Current Quarter Basis Point Total Return Impact by Metro

Apartment Industrial

Office Retail

20

Question

• What will be the best performing property sector in 2018?• A. Apartment

• B. Hotel

• C. Industrial

• D. Office

• E. Retail

21

-8%

-3%

2%

7%

12%

17%

22%

2012 2013 2015 2016 2018

Co

mp

on

en

ts o

f R

etu

rnNPI Components of Return

Cash Yield NOI Growth Cap Rate Change Other Effects Total Return

NPI Components of Return

Annual

Chart: 130

-1%

4%

9%

14%

19%

2011 2012 2013 2014 2015 2016 2017 2018

Tota

l Re

turn

Returns by Consolidated Metro

United New York Los Angeles San Francisco Washington Chicago Boston

Returns by Consolidated Metro

Annual

Chart: 7

-8%

2%

12%

22%

32%

42%

2003 2005 2007 2009 2011 2013 2015 2017

LTV

Rat

io

5th Percentile 25th Percentile 50th Percentile 75th Percentile 95th Percentile

ODCE LTV Ratio by Percentile Distribution

Annual

Chart: 180

Apartment

Industrial

Office

Retail

HotelOther

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1986 1990 1994 1998 2002 2006 2010 2014 2018

Exp

osu

res

NPI-ODCE Exposures

Annual

Chart: 228

2%

4%

6%

8%

10%

12%

14%

16%

18%

2012 2013 2014 2015 2016 2017 2018

Tota

l Re

turn

5th Percentile 25th Percentile 50th Percentile 75th Percentile 95th Percentile

ODCE Total Returns by Percentile Distribution

Annual

Chart: 177

-4%

-2%

0%

2%

4%

6%

8%

1994 1997 2000 2003 2006 2009 2012 2015 2018

Contributions Distributions Net Contributions

ODCE Capital Flows

Annual

Chart: 262

-41%

-21%

-1%

19%

39%

59%

2011 2012 2013 2014 2015 2016 2017

Tota

l Re

turn

5th Percentile 25th Percentile 50th Percentile 75th Percentile 95th Percentile

CEVA Fund Index Total Returns by Percentile Distribution

Annual

Chart: 191

-15%

-10%

-5%

0%

5%

10%

15%

1994 1997 2000 2003 2006 2009 2012 2015 2018

Contributions Distributions Net Contributions

CEVA Capital Flows

Annual

Chart: 265

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

2006 2008 2010 2012 2014 2016 2018

Cap

Rat

eCap Rates by Property Type

NPI Apartment Industrial Office Retail

Cap Rates by Property Type

Annual

Chart: 14

3%

3%

4%

4%

5%

5%

6%

6%

2011 2012 2013 2014 2015 2016 2017 2018

Cap

Rat

eCap Rates by Consolidated Metro

United New York Los Angeles San Francisco Washington Chicago Boston

Cap Rates by Consolidated Metro

Annual

Chart: 15

Question

• What will cap rates be for the nation by the end of 2018?• A. Below 4%

• B. 4% to 5%

• C. 5% to 6%

• D. Above 6%

35

1%

3%

5%

7%

9%

11%

13%

15%

2008 2010 2012 2014 2016 2018

Vac

ancy

Vacancy by Property Type

NPI Apartment Industrial Office Retail

Vacancy by Property Type

Annual

Chart: 21

2%

4%

6%

8%

10%

12%

14%

2011 2012 2013 2014 2015 2016 2017 2018

Vac

ancy

Vacancy by Consolidated Metro

United New York Los Angeles San Francisco Washington Chicago Boston

Vacancy by Consolidated Metro

Annual

Chart: 22

1Q 2018

-13%

-8%

-3%

2%

7%

2008 2010 2012 2014 2016 2018

NO

I Gro

wth

NOI Growth by Property Type

NPI Apartment Industrial Office Retail

NOI Growth by Property Type

Annual

Chart: 23

-12%

-7%

-2%

3%

8%

2011 2012 2013 2014 2015 2016 2017 2018

NO

I Gro

wth

NOI Growth by Consolidated Metro

United New York Los Angeles San Francisco Washington Chicago Boston

NOI Growth by Consolidated Metro

Annual

Chart: 24

Question

• Which property type will have the highest NOI growth in 2018?• A. Apartment

• B. Industrial

• C. Office

• D. Retail

41

21%

31%

41%

51%

61%

71%

81%

2003 2005 2007 2009 2011 2013 2015 2017

Cas

h t

o N

OI R

atio

Cash to NOI Ratio by Property Type

NPI Apartment Industrial Office Retail

Cash to NOI Ratio by Property Type

Annual

Chart: 25

19%

29%

39%

49%

59%

69%

79%

2011 2012 2013 2014 2015 2016 2017 2018

Cas

h t

o N

OI R

atio

Cash to NOI Ratio by Consolidated Metro

United New York Los Angeles San Francisco Washington Chicago Boston

Cash to NOI Ratio by Consolidated Metro

Annual

Chart: 26

1%

3%

5%

7%

9%

11%

13%

15%

2012 2013 2014 2015 2016 2017 2018

Tota

l Re

turn

Apartment Returns by Property Subtype

Apartments Garden Apt Low-Rise Apt Mid-Rise Apt High-Rise Apt

Apartment Returns by Property Subtype

Annual

Chart: 27

Atlanta

Austin

Charlotte

Chicago

Dallas

Denver

Houston

Los Angeles

MiamiMinneapolis

Orlando

Philadelphia

Phoenix

PortlandRaleigh

San Francisco

Seattle

Tampa

Washington, D.C.

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

13%

3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13%

Ap

artm

en

t 1

-Yr

Tota

l Re

turn

s

Apartment 20-Yr Total Returns

Apartment 1-Yr Returns v Long-Term Average

Below LT Avg

Above LT Avg

Chart: 33

-4%

1%

6%

11%

16%

21%

26%

31%

2011 2012 2013 2014 2015 2016 2017 2018

Ap

artm

en

t To

tal R

etu

rnApartment Returns by Consolidated Metro

United New York Los Angeles San Francisco Washington Chicago Boston

Apartment Returns by Consolidated Metro

Annual

Chart: 28

3%

4%

4%

5%

5%

6%

2011 2012 2013 2014 2015 2016 2017 2018

Cap

Rat

eApartment Cap Rates by Consolidated Metro

United New York Los Angeles San Francisco Washington Chicago Boston

Apartment Cap Rates by Consolidated Metro

Annual

Chart: 37

0%

5%

10%

15%

20%

2011 2012 2013 2014 2015 2016 2017 2018

Ind

ust

rial

To

tal R

etu

rnIndustrial Returns by Consolidated Metro

United New York Los Angeles San Francisco Washington Chicago Boston

Industrial Returns by Consolidated Metro

Annual

Chart: 57

3%

5%

7%

9%

11%

13%

15%

2012 2013 2014 2015 2016 2017 2018

Tota

l Re

turnOffice Returns by Property Subtype

Office CBD Off Suburban Off

Office Returns by Property Subtype

Annual

Chart: 77

Atlanta

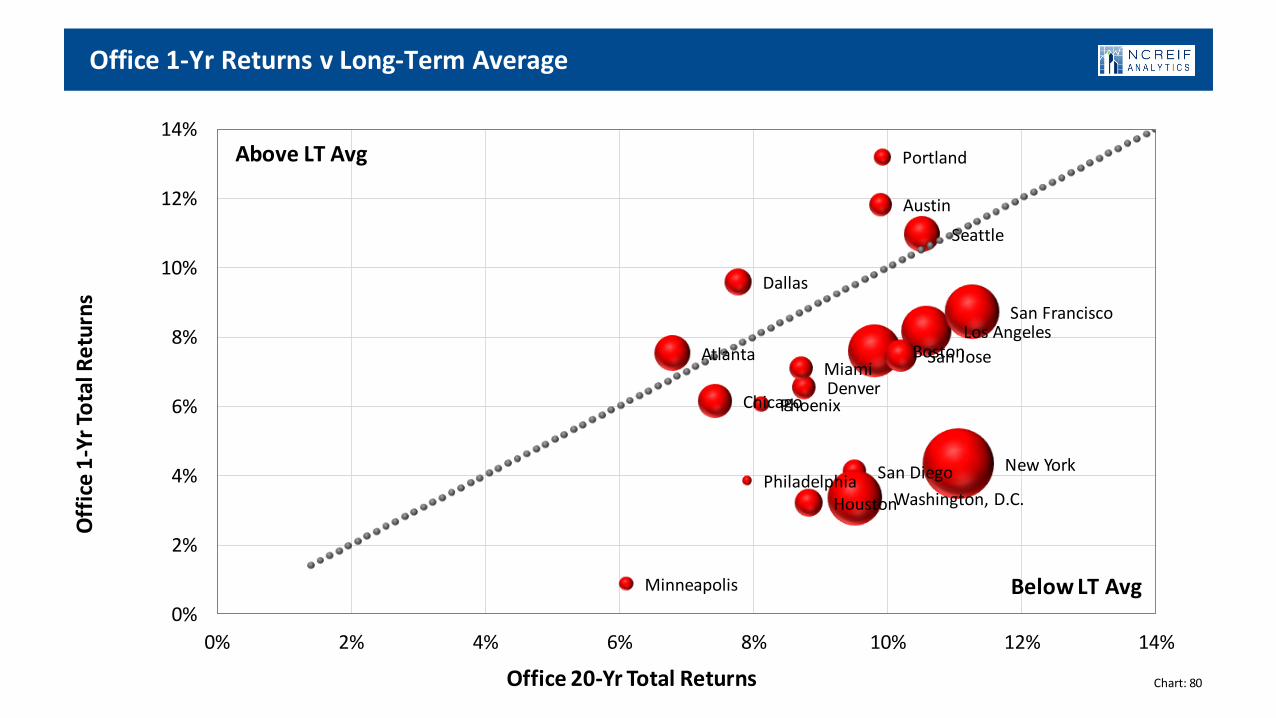

Austin

Boston

Chicago

Dallas

Denver

Houston

Los Angeles

Miami

Minneapolis

New YorkPhiladelphia

Phoenix

Portland

San Diego

San Francisco

San Jose

Seattle

Washington, D.C.

0%

2%

4%

6%

8%

10%

12%

14%

0% 2% 4% 6% 8% 10% 12% 14%

Off

ice

1-Y

r To

tal R

etu

rns

Office 20-Yr Total Returns

Office 1-Yr Returns v Long-Term Average

Below LT Avg

Above LT Avg

Chart: 80

NPI United States

Atlanta

AustinBoston

ChicagoDallas

Denver

Houston

Los Angeles

Miami

Minneapolis

New York

PhiladelphiaPhoenix

Portland

San Diego

San Francisco

San Jose

Seattle

Washington, D.C.

5%

6%

7%

8%

9%

10%

11%

12%

13%

14%

15%

5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15%

Off

ice

20

-Yr

Tota

l Re

turn

s

Risk (Stdev of Annual Returns)

Office 20-Yr Risk v Return

High Risk / Low Return

Low Risk / High Return

Chart: 78

-3%

2%

7%

12%

17%

22%

2011 2012 2013 2014 2015 2016 2017 2018

Off

ice

To

tal R

etu

rnOffice Returns by Consolidated Metro

United New York Los Angeles San Francisco Washington Chicago Boston

Office Returns by Consolidated Metro

Annual

Chart: 83

3%

3%

4%

4%

5%

5%

6%

6%

7%

7%

2006 2008 2010 2012 2014 2016 2018

Cap

Rat

eOffice Cap Rates by Property Subtype

Office CBD Off Suburban Off

Office Cap Rates by Property Subtype

Annual

Chart: 88

3%

3%

4%

4%

5%

5%

6%

6%

7%

7%

2011 2012 2013 2014 2015 2016 2017 2018

Cap

Rat

eOffice Cap Rates by Consolidated Metro

United New York Los Angeles San Francisco Washington Chicago Boston

Office Cap Rates by Consolidated Metro

Annual

Chart: 85

-2%

3%

8%

13%

18%

2012 2013 2014 2015 2016 2017 2018

Tota

l Re

turnRetail Returns by Property Subtype

Retail Mall Retail Strip Retail Street Retail

Retail Returns by Property Subtype

Annual

Chart: 104

Atlanta

ChicagoDallas

Denver

Houston

Los AngelesMiami

New York

Orlando

Phoenix

San Francisco

Seattle

Washington, D.C.

1%

3%

5%

7%

9%

11%

13%

15%

1% 3% 5% 7% 9% 11% 13% 15%

Re

tail

1-Y

r To

tal R

etu

rns

Retail 20-Yr Total Returns

Retail 1-Yr Returns v Long-Term Average

Below LT Avg

Above LT Avg

Chart: 108

-5%

0%

5%

10%

15%

20%

2011 2012 2013 2014 2015 2016 2017 2018

Re

tail

To

tal R

etu

rnRetail Returns by Consolidated Metro

United New York Los Angeles San Francisco Washington Chicago Boston

Retail Returns by Consolidated Metro

Annual

Chart: 107

2%

3%

4%

5%

6%

7%

2006 2008 2010 2012 2014 2016 2018

Cap

Rat

eRetail Cap Rates by Property Subtype

Retail Mall Retail Strip Retail Street Retail

Retail Cap Rates by Property Subtype

Annual

Chart: 114

2%

7%

12%

17%

22%

2013 2014 2015 2016 2017 2018

Tota

l Re

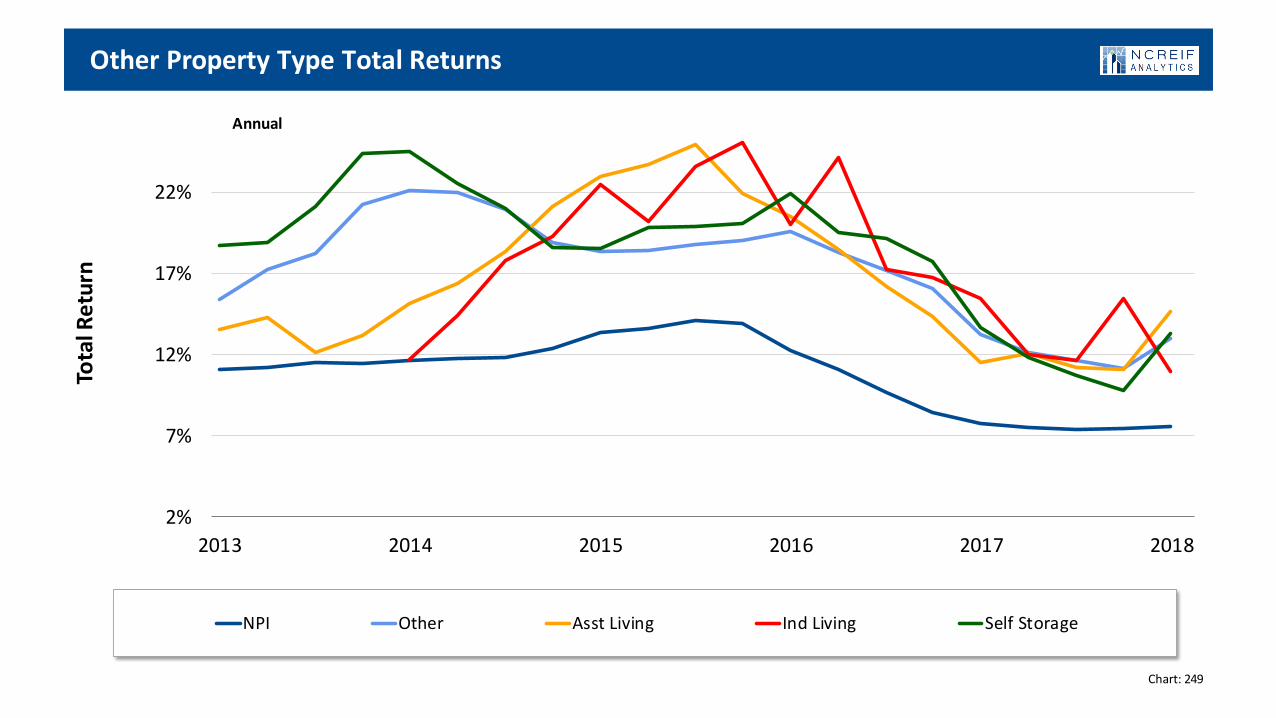

turnOther Property Type Total Returns

NPI Other Asst Living Ind Living Self Storage

Other Property Type Total Returns

Annual

Chart: 249

2.8%

3.3%

3.8%

4.3%

4.8%

5.3%

5.8%

6.3%

6.8%

2013 2014 2015 2016 2017 2018

Cap

Rat

eOther Property Type Cap Rates

NPI Other Asst Living Ind Living Self Storage

Other Property Type Cap Rates

Annual

Chart: 250

-10%

0%

10%

20%

30%

40%

50%

2013 2014 2015 2016 2017 2018

NO

I Gro

wthOther Property Type NOI Growth

NPI Other Asst Living Ind Living Self Storage

Other Property Type NOI Growth

Annual

Chart: 251

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

0

100

200

300

400

500

600

700

800

900

1000

1998 2001 2004 2007 2010 2013 2016

Vo

lum

e (M

il)

Num

ber

of S

ales

Number of Sales Transaction Volume

NPI Transaction Volume

Annual

Chart: 258

Question

• What will the annual NPI total return be for 2018? (Current rolling annual return 7.1%)• A. Below 5%

• B. 5%-to-7%

• C. 7%-to-9%

• D. Above 9%

63

Summary

• Returns below average but stable

• But widening disparity of returns across property sectors

• Cap rate spreads near long-term averages could mitigate

pressure on cap rates from interest rate increases

• NOI growth good for industrial but close to zero for others

• Overall occupancy at historic high driven by industrial

64

Upcoming NCREIF Events

NCREIF Summer Conference 2018Charlotte, NCJune 19–22

Professional Certificate Program in Institutional Real EstateDallas, TXSouthern Methodist UniversityJuly 16–19

Visit www.ncreif.org for more information

65