fiscal deficit and inflation: an empirical analysis for india€¦ · fiscal deficit and inflation:...

TRANSCRIPT

The Romanian Economic Journal

131

Fiscal Deficit and

Inflation: An empirical

analysis for India

Aviral Kumar Tiwari 1 A. P. Tiwari 2

This study examines the linkage between fiscal deficit and inflation in India. The main objective of this study is to examine the factors that are responsible for increasing fiscal deficit in India, by taking into account all factors that can affect the status of fiscal deficit. The study finds that inflation is not at all cause of fiscal deficit. However, government expenditure and money supply are found to be important determinants of mounting fiscal deficit.

Key Words: Budget Deficit, Inflation, Money supply. JEL Classification: C12, E31, E51, H62

1. Introduction

The relationship between budget deficit/fiscal deficit, money growth, government expenditure and inflation has acquired a prominent place in literature on monetary economics. From a theoretical perspective, both the monetarist hypotheses, based originally on the quantitative theory of money, and the fiscal theory of the price level, known as the quantitative theory of government financing of debt, represent the two traditional approaches to understanding what links these macroeconomic variables. Recently, the new Keynesian theory, build

1 Aviral Kumar Tiwari, Management Research Scholar, ICFAI University, Tripura.

Email: [email protected] & [email protected]

2 A. P. Tiwari, Reader, Department of Economics, Vidyant Hindu College, University

of Lucknow, Lucknow. Email: [email protected]

The Romanian Economic Journal

Year XIV, no. 42 December 2011

132

on dynamic general macroeconomic models with imperfect competition, offers an alternative explanation of the dynamics of these variables. Inflation is generally associated with rapid monetary expansion. India’s experience is not different from other countries. Why fiscal policy matters for monetary policy and vice versa is because there is little standing to lowering inflation by monetary measures alone in the presence of soaring budget deficits and public debt (Dahan 1998). Though, instant cause of inflation is associated with money supply, developments in monetary stance are indicative of other sectors of the economy. In India, it is generally argued that fiscal imbalances might have played an important role in explaining price fluctuation. Hence, twin problems of fiscal deficit and inflation have been given a lot of importance in budget of Central government in India. In decade of 2000s the average percentage annual growth rate of inflation was negative. It turned positive in 21st century. In last few years percentage annual growth rate of inflation increased rapidly. Significantly, in 2008-09 it crossed the level of double digit. However, average percentage annual growth rate of fiscal deficit has declined since 1980s to 2000s. But it has increased in 21st century more than twice of that of average percentage annual growth rate 2000th. Estimates reveal that average percentage annual growth rate of money supply has been more or less constant in all the decades. When we consider total government expenditure it is found that it has increased not only in absolute numbers but also in terms of average percentage annual growth rate and percentage annual growth rates1. It is evident from the figure2 1, 2, and 3 that gross fiscal deficit, government expenditure and money supply have increased considerably over years. However, figure 4 indicates that inflation has

1 Detailed estimates of all variables are presented in annexure 1.

2 Figures related to all variables have been presented in annexure 2.

The Romanian Economic Journal

Year XIV, no. 42 December 2011

133

increased up to 1995 and suddenly it has fallen considerably and again it has got momentum since 2000.

Rest of the paper is organized as follows: section 2nd presents review of literature followed by discussion on data source, variables definition and methodology adopted for empirical analysis in section 3rd. In section 4th results of data analysis have been presented followed by conclusions drawn from the empirical analysis in section 5th.

2. Literature review

The relationship between budget deficit, money supply/growth and inflation is a very common debate in economic literature. Lots of economists have analyzed the relationship among these three variables for years by using different countries, different econometric technique and different time period. Most of the studies have analyzed how fiscal deficit and money supply affect inflation which will be evident from the literature review as discussed follows. Very few attempts have been made to analyze the causation running from both ways i.e., how inflation affects fiscal deficit and fiscal deficit affects inflation. (Agheveli and Khan 1978, Miller 1983, Ndebbio 1998 etc.)

Miller (1983) points that fiscal deficit in all cases (whether monetized or not) lead to generate inflationary pressure in the economy. Fischer (1989), by analyzing the relationship between budget deficit and inflation in different countries found that the countries with high inflation have strong relationship among inflation and budget deficit. He noted that high inflation has reducing effect on tax revenue which is known as Tanzi-Olivera Effect. Also, high rate of inflation increases budget deficit by declining seignorage revenue. Shabbir and Ahmed (1994) found that budget deficit has a positive and significant effect on inflation, independent of its indirect effect via money supply that in this case turns out to be minor or negligible.

The Romanian Economic Journal

Year XIV, no. 42 December 2011

134

Chaudhary and Ahmad (1995) found that domestic financing of the budget deficit, particularly from the banking system, is inflationary in the long run. The results provide a positive relationship between budget deficit and inflation during acute inflation periods of the seventies. They also find that money supply is not exogenous; rather, it depends on the position of international reserves and fiscal deficit and it has emerged as an endogenous variable. The general conclusion is that the execution of monetary policy is heavily dependent on the fiscal decisions made by the government. In order to control inflationary pressure, government needs to cut the size of budget deficit. Ndungu (1995) has investigated the link among the fiscal deficit, inflation and money supply on one hand and money supply and inflation on the other hand. He found that for the Keynesian economy budget deficit affects growth of monetary base and money supply affects interest and hence inflation. Ikhide (1995) examined the methods of deficit financing and found that whether the deficit is financed by barrowing from banks, from abroad or the public, in most of the cases any way of financing will generate inflationary pressure. Hondroyiannis and Papapetrou (1997) examined the direct and indirect effect of budget deficit on inflation in Greece and found that budget deficit has an indirect raising effect on inflation. However, they also stated that an increase in inflation results in an increase in budget deficit. Kivilcim (1998) has analyzed the long run relationship between budget deficit and inflation in Turkish economy during 1950-1987. He found that a change in budget deficit cause to change in inflation on the same direction. Egeli (2000) examined the relationship among inflation tax, budget deficit and public spending. His result was reverse relation among inflation tax and budget deficit. He also stated that increasing public spending leads to increase in budget deficit. Egeli (2000) concluded that this disequilibrium results from governments’ wrong policies such as using borrowing in order to finance the deficit.

The Romanian Economic Journal

Year XIV, no. 42 December 2011

135

Tanzi (2000) examined the relationship between tax revenue and budget deficit in Latin American countries. He found that in Latin American countries the budget deficit and public deficit increase even after rise in the tax revenue. He stated that this imbalance results from the deficient and inefficient social programs. Vieira (2000) examined the relationship between fiscal deficit and inflation for six major European countries. The author provided a little support for the proposition that budget deficit has been an important contributing factor to inflation in these economies over the last 45 years. On the contrary, where evidence exists of a long-run relationship between inflation and deficits, this evidence is more consistent with the view that it was inflation that contributed to deficits, rather than the reverse. Cevdet et al. (2001) examined the long-run relationship between inflation rate, budget deficit, and real output growth. They conclude that changes in the consolidated budget deficit have no permanent long run effect on the inflation rate and Public Sector Borrowing Requirement (PSBR) from banks does have a long-run relationship with inflation rate.

Catao and Terrones (2003) have shown that there is a strong positive relationship between fiscal deficits and inflation among high-inflation and developing country groups, but not among low-inflation advanced economies. They found that 1 percentage point reduction in the ratio of fiscal deficit to Gross Domestic Product (GDP) typically lowers long-run inflation by 1.5 to 6.0 percentage points, depending on the size of the inflation tax base. Şen (2003) has analyzed the relationship between tax revenue and inflation. Şen (2003) found that high inflation cause to decrease in tax revenue in crisis time and low level of tax revenue cause to tax loss which leads to high budget deficit. He also cross-examines the role of time in the process of tax collection. He concluded that short term tax collection is better than long term tax collection. In the long run the real value of tax revenue tends to decline because of high inflation.

The Romanian Economic Journal

Year XIV, no. 42 December 2011

136

Yabal, Baldemir and Bakimli (2004) made a study to examine the causes about the imbalance between public spending and public revenue in Turkey. They highlighted that the government finances budget deficit by using short term advance money. It also results in the money supply to increase which results in inflation to go up. They concluded that high budget deficit leads high inflation in Turkish Economy. Solomon and Wet (2004) found a strong positive relationship between inflation and budget deficit in Tanzania. They stated that budget deficit has a significant effect on inflation. They also concluded that developing countries should give more importance to inflation because inflation tends to be affected from many economic shocks such as high budget deficit. Therefore, inflation should be controlled by efficient fiscal policies. Agha and Khan (2006) found that inflation in Pakistan is mainly attributable to unsustainable fiscal deficit. Financing of deficit through the banking system from printing of new money and creating interest-bearing debt affects the general price level.

3. Data type, data source, variables description, estimation methodology and hypothesis formulation

3.1 Data type, data source variables description, estimation methodology:

This study has used time series data sourced from Handbook of statistics of Reserve Bank of India (RBI). In this study money supply has been measured through the measure of M3 (Broad money), inflation has been measured through consumer price index of all level (following Dritsakis 2004, Rother 2004 and Catão and Terrones 2003)1, gross fiscal deficit has been taken as a measure of deficit and

1 We have employed CPI as it is considered a sufficiently accurate measure of inflation in the literature, where CPI reflects the cost of acquiring a fixed basket of goods and services by the average consumer or "typical consumer". Finally, in an open economy, CPI inflation will in part be determined by price movements of foreign goods. This could occur due to the direct inclusion of such goods in the consumption basket or through their use as intermediate inputs.

The Romanian Economic Journal

Year XIV, no. 42 December 2011

137

government expenditure has been measured by total expenditure of central government. The period 1970-71 to 2008-09 has been taken for analysis in this study. In this study natural log (ln) of all variables has been taken in order to make series of less order of autoregressive i.e., to minimize fluctuations in the series. For empirical analysis log linear multiple regression model has been used which is specified as follows:

ln(Gross Fiscal Deficit)t= α+β1ln(Inflation)t+β2ln(Money Supply)t+β3ln(Government Expenditure)t…………………………………………………………..(1).

3.2. Hypothesis (conjecture) formulation:

H1a: Inflation increases gross fiscal deficit i.e., we expect β1>0.

In general, inflation has raising effect on budget deficit by raising nominal interest rate. According to Fischer Effect, nominal interest rate consists of real interest rate and expected inflation rate. If the inflation expectation increases, it causes to rising nominal interest rate which leads to the public debt to go up. Interest payment covers the big part of public payment in developing countries. If interest rate increases because of inflation, it leads to raise interest payment as well as budget deficit by causing the Debt/GDP ratio to increase and thereby increases fiscal deficit1. There are many other channels

1 In spite of the positive relationship between inflation and budget deficit as stated above, in some cases

inflation and budget deficit move in reverse direction. Inflation tax is important for this. If inflation tax is higher than normal level, as inflation increases people avoid holding money because the cost of holding money is high. Thus, real monetary base tends to decrease as inflation tax correspondingly. Holding money would be a costly activity. Inflation tax would be a type of tax revenue which makes the budget deficit decline. Another type of negative relation between inflation and budget deficit occurs because of public borrowing stocks. If borrowing is not indexed to the inflation, as the inflation rise the real value of public borrowing stocks would decline. As the public borrowing stock fall, budget deficit is expected to decrease.

The Romanian Economic Journal

Year XIV, no. 42 December 2011

138

through which inflation influences the real budget deficit.1The most often cited channel is the “Olivera-Tanzi effect” (Olivera 1967, Tanzi 1977) that deteriorates real budget revenues through lags in tax collection.

H2a: Money supply decreases fiscal deficit i.e., we expect β2<0.

The degree of monetary policy credibility is an important factor that determines the fiscal position. As credible monetary policy implies an independent central bank, it prevents monetization of government debt to a certain degree. Dahan (1998) summarizes the impact of monetary policy on the fiscal stance. The first one is the revenue effect. In the short-run, tight monetary policy may lead to lower output growth and for that reason, tax revenues might reduce, causing a rise in the budget deficit. The second one is the effect on public debt. A tight monetary policy results in higher interest rates, making servicing public debt expensive. With caution, the overall impact would depend on how economic agents formulate their expectations and the degree of credibility of monetary policy. There are two possibilities: (i) the public expects that the monetary authority will fail to achieve the inflation target and eventually abandon the tight policy (ii) the tight policy will bring down inflation (and inflation expectations) once the policy is announced. In the first scenario, tight policy may lead to higher inflation and higher nominal interest rates. In the second scenario, the expected reaction in inflation tends to decrease the nominal interest rate and thus the debt effect is ambiguous. Further the sign of the debt effect is positive if the government is a net borrower and negative if the government is a net lender. The magnitude of the debt effects depends on the level of public debt, the maturity of government bonds and the share of

1 All of the factors in essence are distortional effects of inflation, determined by nominal state institutions. A brilliant overview of the real effects of inflation can be found in Fischer and Modigliani (1979) and Fischer (1989).

The Romanian Economic Journal

Year XIV, no. 42 December 2011

139

flexible interest rate on bonds and the sensitivity of various interest rates. The third one is the effect due to seigniorage. A deceleration in the rate of money creation (through open market operations) leads to an increase in debt creation, resulting in higher budget deficits in subsequent periods.

H3a: Government expenditure increases fiscal deficit i.e., we expect β3>0.

In general, increase in government expenditure (either because of operation of Wagner’s law or otherwise) will increase fiscal deficit if revenue is not generated in the same proportion. However, there are other reasons also due to which government expenditure can increase fiscal deficit even after raise in tax revenue as Tanzi (2000) have found that in Latin American countries that budget deficit and public deficit increase even after rise in the tax revenue due to deficient and inefficient social programs. Ironically, Şen (2003) found that high inflation cause to decrease in tax revenue in crisis time and low level of tax revenue cause to tax loss which leads to high budget deficit. Further, Egeli (2000) also stated that increasing public spending leads to increase in budget deficit. Egeli (2000) concluded that this disequilibrium results from governments’ wrong policies such as using borrowing in order to finance the deficit.

4. Data analysis and empirical findings

Table 1 presents descriptive statistics (in terms of Mean, Median, Standard Deviation (S. D.), Coefficient of Variation (C.V.), Skewness, Kurtosis and Jarque-Bera (J-B) statistics) of variables used for empirical analysis in the present study. From the table 2 it is evident that S. D. of money supply is highest (1.57) and inflation has lowest S. D. (0.51). Since S. D. is not better measure to measure fluctuations in the series therefore C.V. has been calculated which shows that C.V. of fiscal deficit is highest and C.V. of money supply is second highest

The Romanian Economic Journal

Year XIV, no. 42 December 2011

140

while C.V. of inflation is lowest. J-B statistics shows that all variables are having lognormal distribution as data do not support to reject the null hypothesis that variables under consideration have followed normal distribution.

The Romanian Economic Journal

141

Table 1 Descriptive statistics

ln of government expenditure)

ln of consumer price index

ln of gross fiscal deficit Ln of M3

Mean 11.26006 6.063579 10.12453 10.42386 Median 11.43937 5.869297 10.48100 10.35319 Maximum 13.71121 7.230563 12.69623 13.15776 Minimum 8.634798 5.267858 7.249926 7.902118 Standard Deviation (S. D.) 1.496247 0.510076 1.561426 1.566002 Coefficient of variation (C.V.) 13.3613 8.415 15.415 15.0233 Skewness -0.146632 0.709019 -0.387285 0.125631 Kurtosis 1.786685 2.685949 1.89570 1.769939 Jarque-Bera (Probability)

2.531973 (0.281961)

3.427872 (0.180155)

2.956299 (0.228059)

2.561295 (0.277857)

Source: Compiled by the Author’s.

The Romanian Economic Journal

142

Result of regression analysis presented in table 2 shows that inflation is not a significant variable which affects the fiscal deficit in India, while money supply is negatively associated and government expenditure is positively associated with the fiscal deficit. This implies that as money supply increases fiscal deficit will decrease and as government expenditure increases fiscal deficit will increase. Ramsey’s RESET test of omitted variable indicates that all explanatory variables have been included in the model and specification of the model is correct. The estimated value of F-test being insignificant implies that data do not support to reject null hypothesis of omitted variables and misspecification of the model. Data does not support to reject null hypothesis of constant variance implying that heteroskedasticity does not exist. It is evident from Breusch-Pagan test of heteroskedasticity. Durbin-Watson (D-W) value indicates that positive first order autocorrelation does not exist. But problem of multicollinearity is very severe as Variance Inflation Factor (VIF) is very high for the three independent variables.

The Romanian Economic Journal

143

Table 2

Results of regression analysis Dependent Variable: ln of gross fiscal deficit

Variable Coefficient Std. Error (S. E) t-Statistic VIF

Adjusted R-squared (S. E)

Breusch-Pagan for heteroskedasticity

Ramsey’s RESET test

C -2.69337 0.256369 -10.506* 0.993867 (0.122277)

chi2(1) = 9.85 Prob > chi2 = 0.0017

F(3, 32) = 0.32 Prob >F = 0.8119

ln of Government Expenditure 1.918637 0.116578 16.4580*

77.33

ln of consumer price index 0.019723 0.045305 0.435342

75.21 Durbin-Watson (DW) stat= 1.972698

Akaike Information criteria/ Schwarz Information criteria= -1.268136/-1.097515

ln of money supply -0.85436 0.109849 -7.7775*

1.36 F-statistic = 2053.779*

*denotes significant at 1% level. Source: Compiled by the Author’s.

The Romanian Economic Journal

144

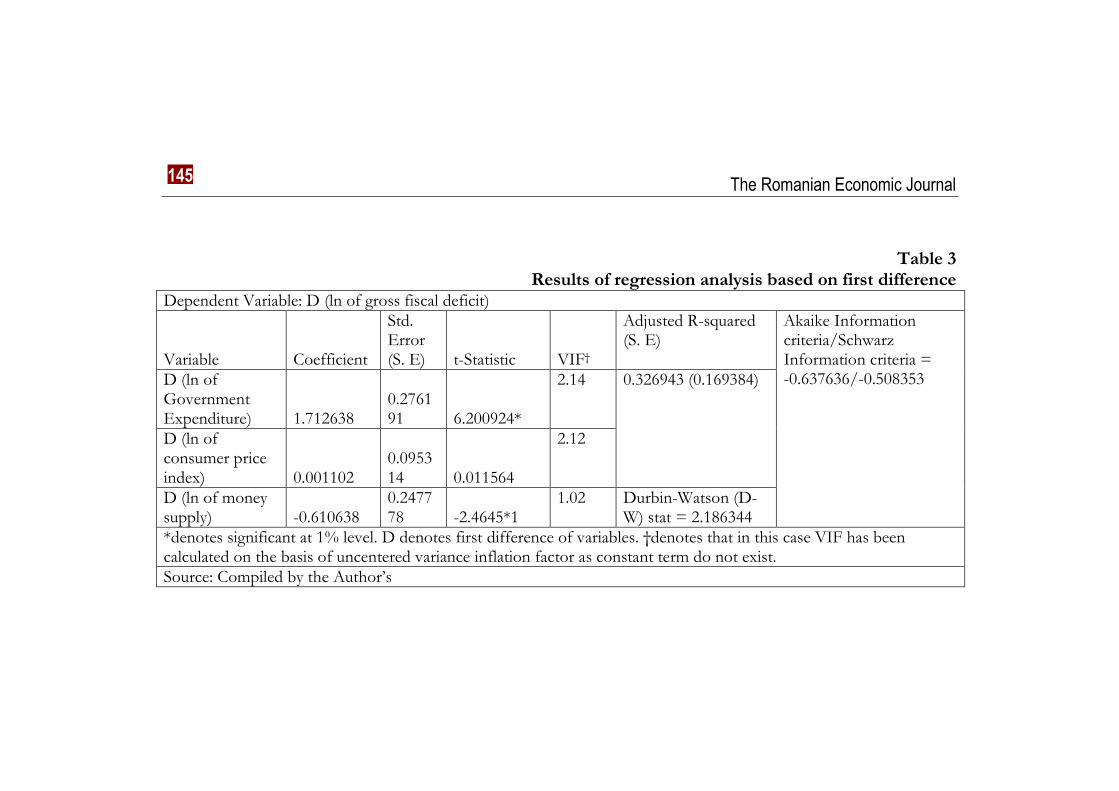

To minimize the problem of multicollinearity first we have done regression analysis using mean deviation of all variables and we found that yet this approach has reduced the VIF1 however, these reduced VIF values were also too high then to avoid problem of multicollinearity on one hand also to avoid the problem of nonstationary property of data (as data used for analysis is time series) for all variables first difference of all variables2 has been taken and then regression analysis has been carried out. Result of the regression analysis of first difference form as presented in table 3 shows similar results as obtained from earlier analysis. In this case we can see that now VIF has considerably declined indicating that a very small degree of multicollinearity exists.

Further, to take into account the time effect, constant term in first difference model has been introduced and again analysis has been carried out. Result has been presented in table 4. It is found that time is also important factor which affects fiscal deficit. In this case also heteroskedasticity, multicollinearity and autocorrelation do not exist. Ramsey’s RESET test indicates that no variable is omitted from the empirical estimation and model is not miss-specified.

1 Results of regression analysis carried out for variables using deviation from mean will be available upon request to the authors. 2 Results of unit root analysis {using (Augmented) Dickey-Fuller (DF/ADF) test statistic and Phillips-Perron (PP) test statistic} have been presented in annexure 3 which shows that all variables are nonstationary in level form and in first difference form they are stationary.

The Romanian Economic Journal

145

Table 3

Results of regression analysis based on first difference Dependent Variable: D (ln of gross fiscal deficit)

Variable Coefficient

Std. Error (S. E) t-Statistic VIF†

Adjusted R-squared (S. E)

Akaike Information criteria/Schwarz Information criteria = -0.637636/-0.508353 D (ln of

Government Expenditure) 1.712638

0.276191 6.200924*

2.14 0.326943 (0.169384)

D (ln of consumer price index) 0.001102

0.095314 0.011564

2.12

D (ln of money supply) -0.610638

0.247778 -2.4645*1

1.02 Durbin-Watson (D-W) stat = 2.186344

*denotes significant at 1% level. D denotes first difference of variables. †denotes that in this case VIF has been calculated on the basis of uncentered variance inflation factor as constant term do not exist. Source: Compiled by the Author’s

The Romanian Economic Journal

Year XIV, no. 42 December 2011

146

Table 4 Results of regression analysis based on first difference with constant Dependent Variable: D (ln of gross fiscal deficit)

Variable Coefficient

Std. Error (S. E) t-Statistic VIF

Adjusted R-squared (S. E)

Breusch-Pagan for heteroskedasticity

Ramsey’s RESET test

C -0.013445 0.100393 -0.1339* 0.307512 (0.171812)

chi2(1) = 2.17 Prob > chi2 = 0.1406

F(3, 31) = 1.97 Prob > F = 0.1394

D (ln of Government Expenditure) 1.772164 0.525410 3.372916

1.12

D (ln of consumer price index) 0.000139 0.096947 0.001429

1.11 Durbin-Watson (DW) stat= 2.195987

Akaike Information criteria/ Schwarz Information criteria= -0.585531/-0.413154

D (ln of money supply) -0.578263 0.348721 -1.658**

1.01 F-statistic = 6.476854*

*and **denotes significant at 1% and 5% level respectively. “D” denotes first difference of variables. Source: Compiled by the Author’s.

The Romanian Economic Journal

147

Finally, actual, fitted (estimated) value of gross fiscal deficit and residual plot has been drawn to show the goodness fit of the model for both specifications i.e., when first difference of all variables is taken for analysis and constant term does not exist and when it exists. Graphs drawn for both specifications show that model fits good and residuals fluctuates around mean zero line.

Figure 5

Goodness fit of the model when first difference of all variables is taken for analysis and constant term is discarded.

The Romanian Economic Journal

Year XIV, no. 42 December 2011

148

Figure 6

Goodness fit of the model when first difference of all variables is taken for analysis and constant term is included.

5. Conclusions

It has been witnessed that over the years particularly in the last decade not only burden of fiscal deficit has increased but also mounting inflation rate. Government expenditure has also increased the pressure of the burden on Central government. As for as money supply is concerned, annual growth rate of money supply has remained more or less constant. However, money supply in absolute terms has increased. The test for stationarity using Augmented Dickey-Fuller (ADF) and Phillip-Perron (PP) test proved that the variables used in this study are nonstationary in their level forms. Result obtained from empirical analysis shows that the important variables which are affecting fiscal deficit are money supply and mounting government expenditure, while inflation does not count for fiscal deficit significantly1. Interestingly, we find from regression

1 In regression analysis testing of hypothesis is done through the testing the significance of coefficients of the variables through t-test. This one can see from the significance of

The Romanian Economic Journal

Year XIV, no. 42 December 2011

149

analysis that money supply is negatively associated and government expenditure is positively associated with the fiscal deficit. This implies that as money supply increases fiscal deficit will decrease and as government expenditure increases fiscal deficit will increase. This implies that while on one hand financing of deficit through the banking system from printing of new money and creating interest-bearing decreases fiscal deficit, on the other hand increasing government expenditure is the main cause of mounting fiscal deficit. This may be due to deficient and inefficient social programs as Tanzi (2000) have found that in Latin American countries disequilibrium between public budget and budget deficit results from governments’ wrong policies such as using borrowing in order to finance the deficit as Egeli (2000) have found. Therefore, to analyses this issue in depth one can go for empirical analysis in this direction for India and also present study can be extended by analyzing the impact of different types of government expenditure and Consumer Price Index (CPI) on fiscal deficit which may give more insights about the problem.

coefficients of respective variables in all regression models employed in the analysis. In all models, coefficients of money supply and government expenditure are significant implying that the data do not supports to accept the null hypothesis, which implies that we can accept the alternative hypothesis. However, data do not provide sufficient evidence to reject or not to accept the null hypothesis for variable inflation in statistical terms.

The Romanian Economic Journal

Year XIV, no. 42 December 2011

150

References

Agheveli B. and Khan, M. S. (1978). Government deficits and inflationary process in developing countries. I.M.F. Staff papers, Vol. 25. Asif Idrees Agha and Muhammad Saleem Khan (2006). An empirical analysis of fiscal imbalances and inflation in pakistan. SBP Research Bulletin, Vol. 2, No. 2. Cevdet A., E.C. Alper, and S. Ozmucur (2001). Budget deficit, inflation and debt sustainbility: Evidence from Turkey (1970-2000). Mim. Istanbul: Bogazici University. Chaudhary, M.A and N.Ahmad. (1995). Money supply, deficit and inflation in Pakistan. Pakistan Development Review, Vol. 34. Dahan M. (1998). The Fiscal Effects of Monetary Policy. IMF Working Paper , 98/66 May. Egeli H. (2000). Gelişmiş ülkelerde bütçe açıkları dokuz eylül. University Social Science Institute Magazin,Vol. 2, No. 4. Fischer S.(1989). The economics of government budget constraint. The World Bank Working Paper, Washington. Fischer S., Modigliani F. (1979). Towards an understanding of the real effects and costs of inflation. Weltwirtschaftliches Archiv Vol. CXIV. Hondroyiannis and Papapetrou (1997). Are budget deficits inflationary? A cointegration approach. Applied Economics Letters, Vol. 4, No. 8. Ikhide S. I. (1995). Must a fiscal deficit be inflationary in a developing African country? Journal of Economic Management, Vol. 2, No. 1. Kesbiç Y., Baldemir E., and Bakımlı E. (2004). Bütçe açıkları ile parasal büyüme ve enflasyon arasındaki ilişki: Türkiye için bir model denemesi. Yönetim ve Ekonomi, Celal Bayar University, Vol. 11, No. 2. Kıvılcım M. (1998) The relationship between inflation and the budget deficit in Turkey. Journal of Business & Economic Statistics, Vol. 16, No. 4.

The Romanian Economic Journal

Year XIV, no. 42 December 2011

151

Luis Catão and Macro E. Terrones (2003). Fiscal deficit and inflation, IMF Working paper, No. 65. Miller P. (1983). Higher deficit policies lead to higher inflation. Federal Reserve Bank of Minneapolis, Winter, 8-19. Ndebbio J. E. (1998). Fiscal deficits and inflationary process in an open economy: The case on Nigeria. The Nigerian Journal of Economics and Social Studies, Vol. 40, No. 3. Ndung’u N. (1995). Government budget deficits and deflation in Kenya: An empirical investigation. African Journal of Economic Policy, Vol. 2, No. 2. Nikolaos Dritsakis (2004). A causal relationship between inflation and productivity: An empirical approach for Romania american. Journal of Applied Sciences, Vol. 1, No. 2. Olivera J.H.G. (1967). Money, prices, and fiscal lags: A note on the dynamics of inflation. Banca Nazionale del Lavoro Quarterly Review, Vol. 20. Philipp C. Rother (2004). Fiscal policy and inflation volatility. Working paper series No. 317 / march 2004. Şen, H. (2003). Olivera - Tanzi Etkisi:Türkiye Üzerine Ampirik Bir Çalışma. Maliye magazine, Vol. 143. Shabbir, T. and A. Ahmed (1994). Are government budget deficit inflationary? Evidence from Pakistan. Pakistan Development Review, Vol. 33. Solomon M. and Wet W. A. (2004). The effect of budget deficit on inflation: The case of Tanzania. SAJEMS NS, Vol.7, No.1. Tanzi V. (1977). Inflation, lags in collection and the real value of tax revenue. IMF Staff Papers, Vol. 24. Tanzi V. (2000). Taxation in Latin America in the last decade. SAJEMS NS, Vol. 7. Vieira C. (2000). Are fiscal deficit inflationary? Evidence for the EU. Department of Economics, Loughborough University UK, Universidade de Evora, Portugal.

The Romanian Economic Journal

152

Annexure 1: Table of Percentage growth rates

Year Percentage annual growth rate of CPI

Percentage annual growth rate of fiscal deficit

Percentage annual growth rate of M3

Percentage annual growth rate of government expenditure

1970-71 1971-72 1.030928 22.65625 14.41023 22.54623 1972-73 10.71429 26.17255 16.35348 14.00174 1973-74 21.19816 -20.4681 19.84577 4.594629 1974-75 34.60076 32.83324 13.61539 20.90533 1975-76 -3.9548 31.58123 12.47529 24.58736 1976-77 -13.8235 25.51997 19.87935 10.32394 1977-78 10.5802 -3.20884 19.9152 13.53884 1978-79 -2.16049 55.16304 20.39124 21.02412 1979-80 9.148265 11.94396 20.19542 1.044442 1980-81 14.16185 29.83417 16.38199 20.07172 Percentage annual average

8.149562

21.20275

17.34634

15.26384

The Romanian Economic Journal

Year XIV, no. 42 December 2011

153

growth rate

1981-82 12.40506 4.42222 17.31939 10.96715 1982-83 5.18018 22.62866 14.58699 21.87216 1983-84 11.34904 22.61221 17.6049 15.40385 1984-85 0.192308 33.66078 18.26576 22.78944 1985-86 4.798464 25.50528 16.58114 20.70499 1986-87 4.761905 20.51423 17.60369 19.46227 1987-88 9.965035 2.664946 17.26252 8.495454 1988-89 12.55962 14.34329 17.28381 15.89487 1989-90 5.367232 15.22815 19.01584 17.44005 1990-91 7.640751 25.25819 16.66402 13.33577 Source: Hand Book of Statistics (RBI) and compiled by the Author’s

The Romanian Economic Journal

156

Annexure 2: Graphical presentation of the variables

Figure 1 = Gross fiscal deficit

Figure 2 = Government expenditure

The Romanian Economic Journal

Year XIV, no. 42 December 2011

157

Figure 3 = Money supply

Figure 4 = Inflation

The Romanian Economic Journal

Year XIV, no. 42 December 2011

158

Annexure 3: Results of unit root analysis

Variables Unit root test statistics Constant

Constant and Trend

DF/ADF (k)†

PP (k)ψ

GOVTEXPENDITURE

----- Yes -1.936782 -1.933716 (3)

D(GOVTEXPENDITURE)

Yes ------ -5.493156* -5.445764*

LCPI ----- Yes -2.037451

-2.037451

D(LCPI) Yes ------ -5.989744* -5.989523* (2)

LGROSSFICIALDEFICIT

----- Yes -2.287080 -2.287080

D(LGROSSFICIALDEFICIT)

Yes ------ -6.083180* -6.029532* (1)

LM3 ----- Yes -1.936611 -1.936611 D(LM3) Yes ---- -6.298259* -6.304654* (2) *denotes significant at 1% level. “k” denotes lag length used to avoid problem of serial correlation. “D” denotes first difference of the variable. “†” denotes maximum lag selection is based on SIC. “ψ” denotes Newey-West using Bartlett kernel method has been used to select appropriate lag length. Critical values of DF/ADF test for level form are -4.219126, -3.533083, -3.198312 at 1%, 5% and 10% level of significance respectively and critical values of DF/ADF test for first difference form are -3.621023, 2.943427, 2.610263 at 1%, 5% and 10% level of significance respectively. Critical values of PP test for level form are -4.219126, -3.533083, -3.198312 at 1%, 5% and 10% level of significance respectively and critical values for PP test for first difference are -3.621023, -2.943427, -2.610263 at 1%, 5% and 10% level of significance respectively.