fitbit presentation

TRANSCRIPT

IsabelOdom,AaronCappelli,JasonBrandner,AnnHauser,SavannahMoss

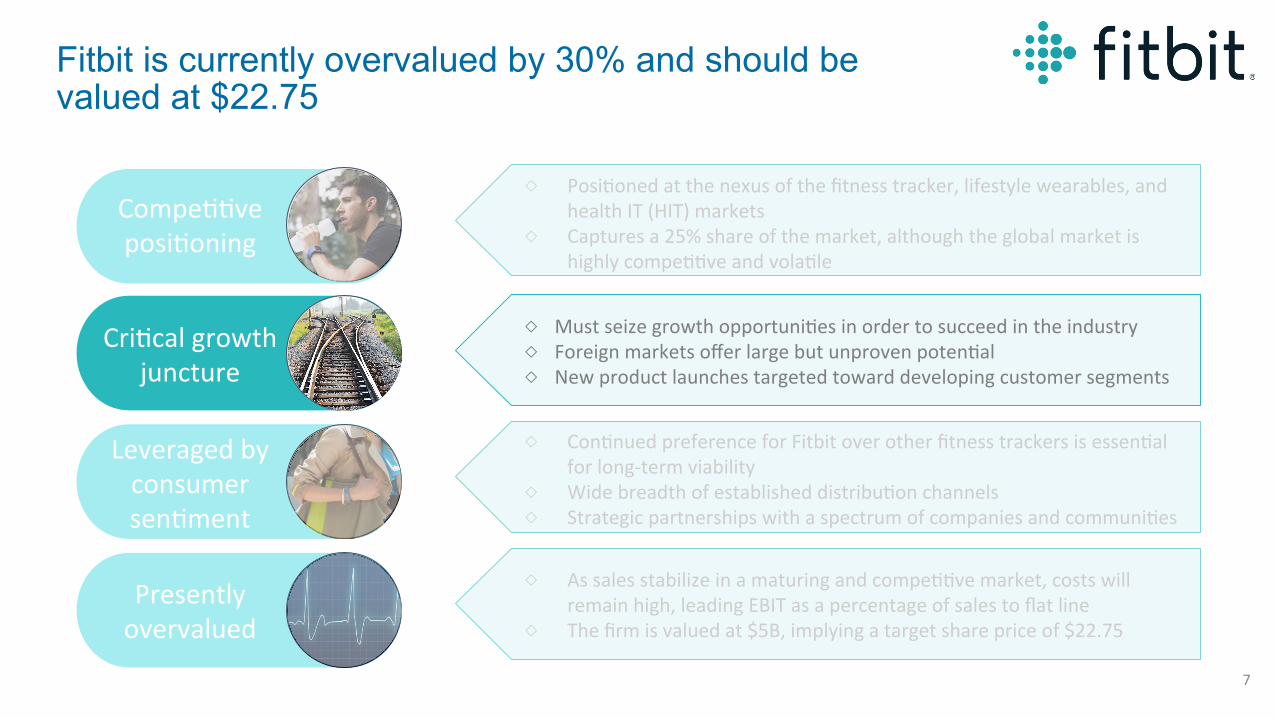

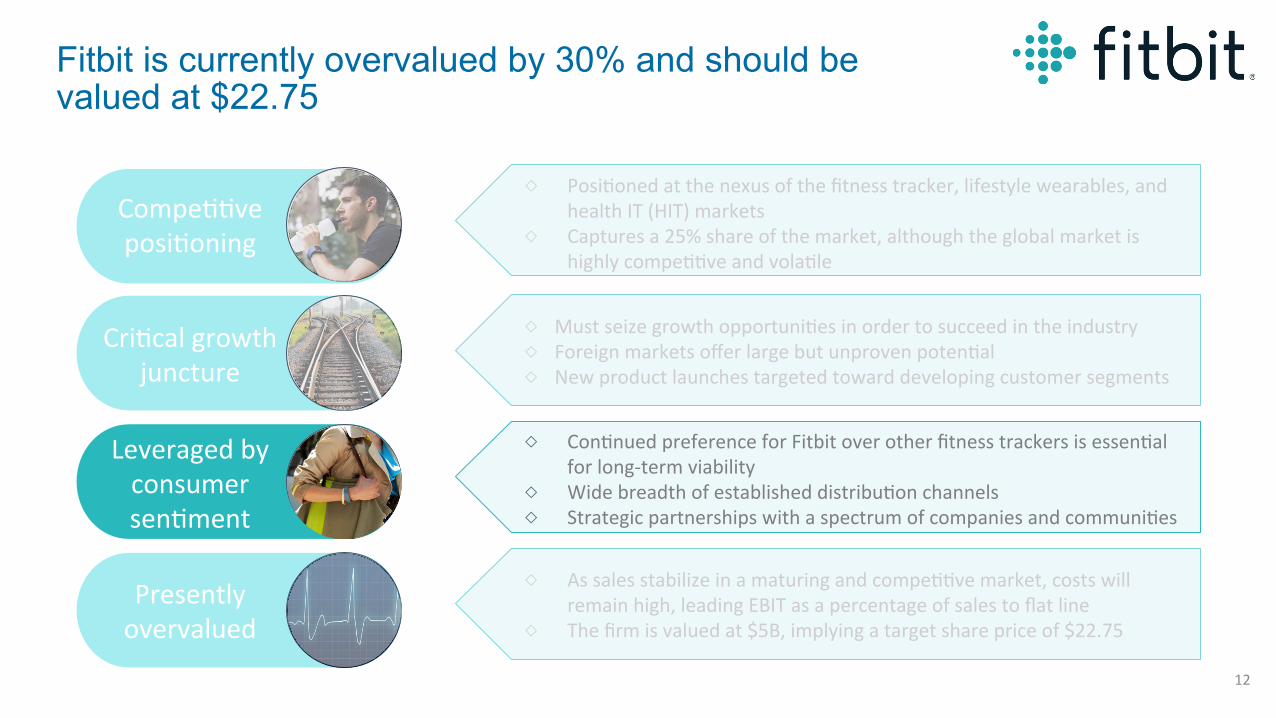

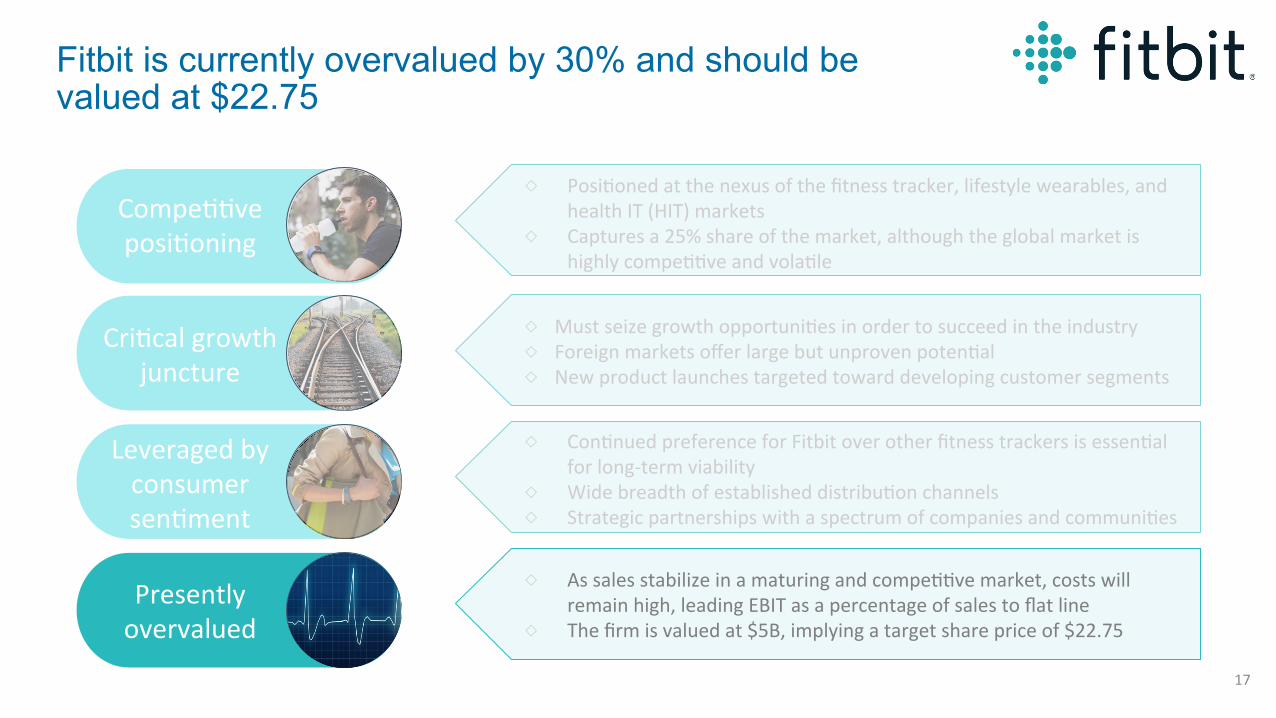

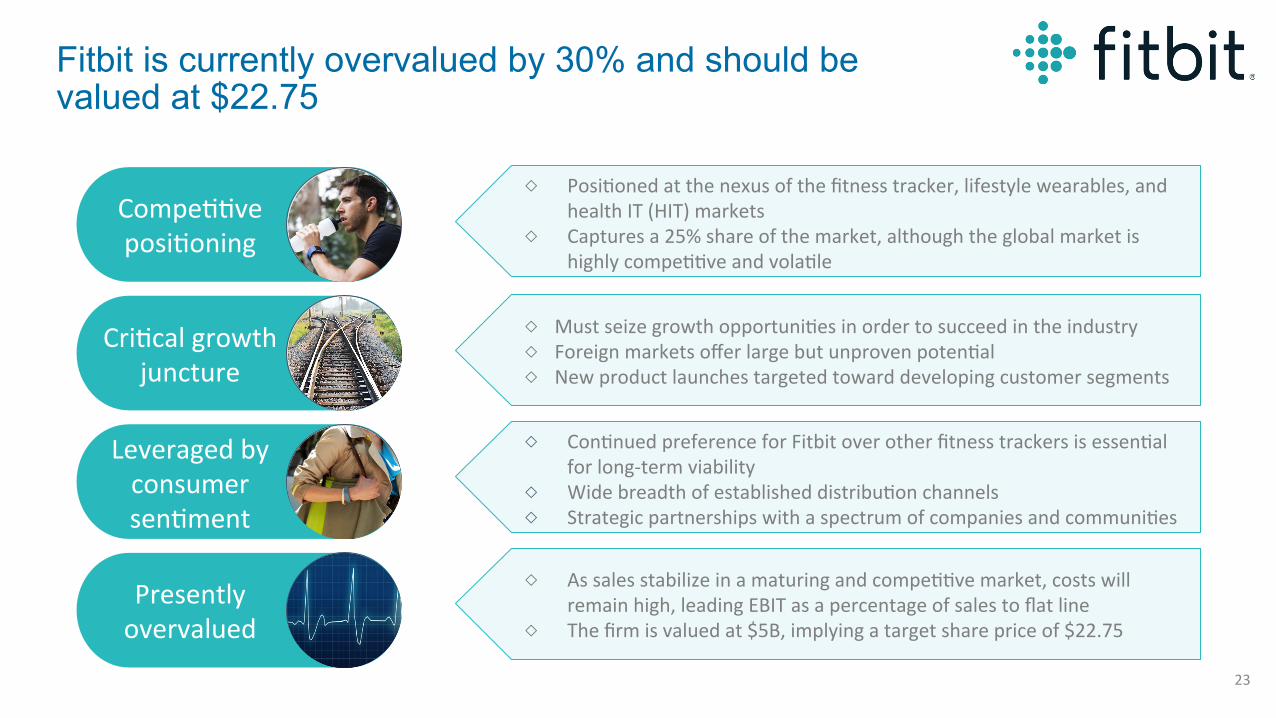

Fitbit is currently overvalued by 30% and should be valued at $22.75

Compe&&veposi&oning

Presentlyovervalued

Cri&calgrowthjuncture

Leveragedbyconsumersen&ment

◇ Posi&onedatthenexusofthefitnesstracker,lifestylewearables,andhealthIT(HIT)markets

◇ Capturesa25%shareofthemarket,althoughtheglobalmarketishighlycompe&&veandvola&le

◇ Con&nuedpreferenceforFitbitoverotherfitnesstrackersisessen&alforlong-termviability

◇ Widebreadthofestablisheddistribu&onchannels◇ Strategicpartnershipswithaspectrumofcompaniesandcommuni&es

◇ Assalesstabilizeinamaturingandcompe&&vemarket,costswillremainhigh,leadingEBITasapercentageofsalestoflatline

◇ Thefirmisvaluedat$5B,implyingatargetsharepriceof$22.75

◇ Mustseizegrowthopportuni&esinordertosucceedintheindustry◇ Foreignmarketsofferlargebutunprovenpoten&al◇ Newproductlaunchestargetedtowarddevelopingcustomersegments

2

Compe&&veposi&oning

Presentlyovervalued

◇ Con&nuedpreferenceforFitbitoverotherfitnesstrackersisessen&alforlong-termviability

◇ Widebreadthofestablisheddistribu&onchannels◇ Strategicpartnershipswithaspectrumofcompaniesandcommuni&es

◇ Assalesstabilizeinamaturingandcompe&&vemarket,costswillremainhigh,leadingEBITasapercentageofsalestoflatline

◇ Thefirmisvaluedat$5B,implyingatargetsharepriceof$22.75

◇ Mustseizegrowthopportuni&esinordertosucceedintheindustry◇ Foreignmarketsofferlargebutunprovenpoten&al◇ Newproductlaunchestargetedtowarddevelopingcustomersegments

Fitbit is currently overvalued by 30% and should be valued at $22.75

Cri&calgrowthjuncture

Leveragedbyconsumersen&ment

◇ Posi&onedatthenexusofthefitnesstracker,lifestylewearables,andhealthIT(HIT)markets

◇ Capturesa25%shareofthemarket,althoughtheglobalmarketishighlycompe&&veandvola&le

3

Fitbit is positioned at the nexus of the fitness tracker, lifestyle wearables, and health IT (HIT) markets

♦Compe&&veposi&oning♦Growthjuncture♦Consumersen&ment♦Valua&on♦

Fitnesstrackers

Lifestylewearables

HealthIT(HIT)

4

Fitbit captures a 25% share of the highly competitive and volatile global wearables market

Globalwearablesmarketshare(2014–16*)Percentoftotalmarket

♦Compe&&veposi&oning♦Growthjuncture♦Consumersen&ment♦Valua&on♦

5Source:Sta&sta(2016)

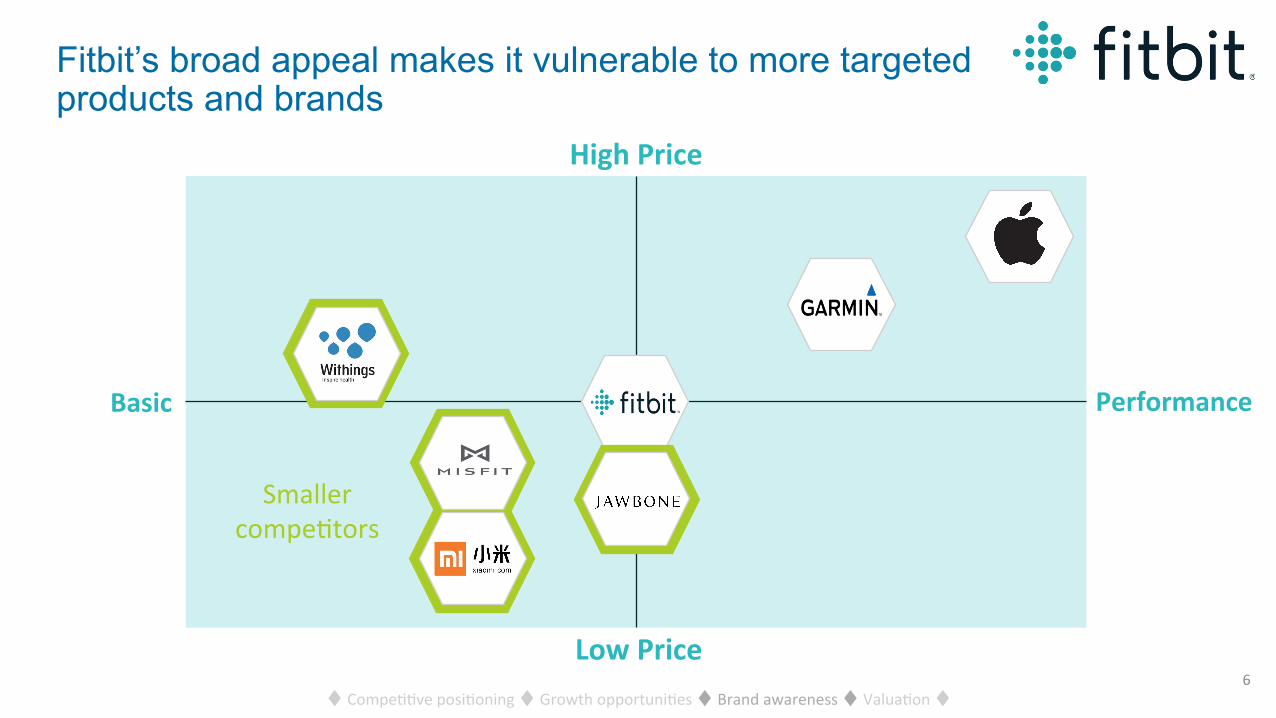

Fitbit’s broad appeal makes it vulnerable to more targeted products and brands

♦Compe&&veposi&oning♦Growthopportuni&es♦Brandawareness♦Valua&on♦

Basic Performance

LowPrice

HighPrice

Smallercompe&tors

6

Compe&&veposi&oning

Presentlyovervalued

◇ Posi&onedatthenexusofthefitnesstracker,lifestylewearables,andhealthIT(HIT)markets

◇ Capturesa25%shareofthemarket,althoughtheglobalmarketishighlycompe&&veandvola&le

◇ Mustseizegrowthopportuni&esinordertosucceedintheindustry◇ Foreignmarketsofferlargebutunprovenpoten&al◇ Newproductlaunchestargetedtowarddevelopingcustomersegments

Fitbit is currently overvalued by 30% and should be valued at $22.75

Cri&calgrowthjuncture

Leveragedbyconsumersen&ment

◇ Con&nuedpreferenceforFitbitoverotherfitnesstrackersisessen&alforlong-termviability

◇ Widebreadthofestablisheddistribu&onchannels◇ Strategicpartnershipswithaspectrumofcompaniesandcommuni&es

◇ Assalesstabilizeinamaturingandcompe&&vemarket,costswillremainhigh,leadingEBITasapercentageofsalestoflatline

◇ Thefirmisvaluedat$5B,implyingatargetsharepriceof$22.75

7

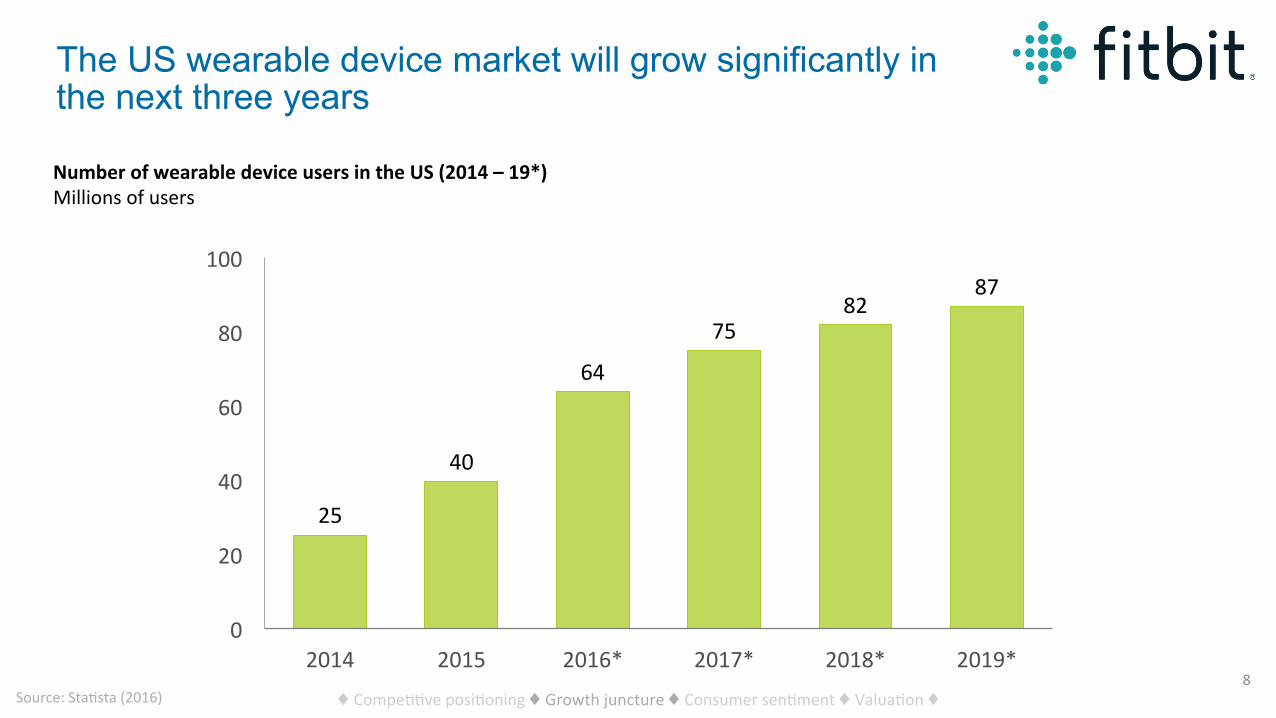

The US wearable device market will grow significantly in the next three years

NumberofwearabledeviceusersintheUS(2014–19*)Millionsofusers

25

40

64

7582

87

0

20

40

60

80

100

2014 2015 2016* 2017* 2018* 2019*

♦Compe&&veposi&oning♦Growthjuncture♦Consumersen&ment♦Valua&on♦

8Source:Sta&sta(2016)

Fitbit must seek out new markets for its products; Foreign market offer large but unproven growth potential

Numberofwearabledevicesinuse(2014,2019*)Millionsofunits

0

40

80

120

160

200

Asia E.Europe LATAM ME/Africa N.America W.Europe♦Compe&&veposi&oning♦Growthjuncture♦Consumersen&ment♦Valua&on♦

9Source:EMarketer(2016)

New products and pricing will increase Fitbit’s access to a number of customer segments

♦Compe&&veposi&oning♦Growthjuncture♦Consumersen&ment♦Valua&on♦

◇ Products:Zip,One,Flex2◇ Pricerange:$50-$90◇ Market:Peopleinterested

inimprovingoverallfitness

EverydayUsers AcRveUsers PerformanceUsers

◇ Products:Alta+ChargeHR◇ Pricerange:$120-$150◇ Market:Ac&vepeoplewho

exerciseregularly;monitorsheartrate

◇ Products:Blaze+Surge◇ Pricerange:$190-$240◇ Market:Performanceand

enduranceathleteswhouseFitbitasadatatool

Increasinglybroadcommercialappeal

10Source:Fitbit(2016)

Fitbit is banking on new product initiatives targeted toward developing into the digital health space

♦Compe&&veposi&oning♦Growthjuncture♦Consumersen&ment♦Valua&on♦

FitbitCorporateWellnessProgram

CorporatePartners

Reducecostsforemployers&employees

Networkingeffectsdriveemployeeengagement

InsuranceAgencies

Reducecostsby$1,300peremployee

11Source:Fitbit(2016)

Compe&&veposi&oning

Presentlyovervalued

◇ Posi&onedatthenexusofthefitnesstracker,lifestylewearables,andhealthIT(HIT)markets

◇ Capturesa25%shareofthemarket,althoughtheglobalmarketishighlycompe&&veandvola&le

◇ Assalesstabilizeinamaturingandcompe&&vemarket,costswillremainhigh,leadingEBITasapercentageofsalestoflatline

◇ Thefirmisvaluedat$5B,implyingatargetsharepriceof$22.75

Dynamicgrowth

opportuni&es

◇ Mustseizegrowthopportuni&esinordertosucceedintheindustry◇ Foreignmarketsofferlargebutunprovenpoten&al◇ Newproductlaunchestargetedtowarddevelopingcustomersegments

◇ Con&nuedpreferenceforFitbitoverotherfitnesstrackersisessen&alforlong-termviability

◇ Widebreadthofestablisheddistribu&onchannels◇ Strategicpartnershipswithaspectrumofcompaniesandcommuni&es

Fitbit is currently overvalued by 30% and should be valued at $22.75

Cri&calgrowthjuncture

Leveragedbyconsumersen&ment

12

52

30

612

0

20

40

60

Nointerest Donotown;consider Own;discon&nued Useregularly

Fitbit faces challenges in capturing 52% of the consumer segment with low purchase intention

Consumerinterestandownership(2016)%ofusers

13

30%ofuserswhopurchaseFitbitsdiscon&nueuse

Source:EMarketer(2016)

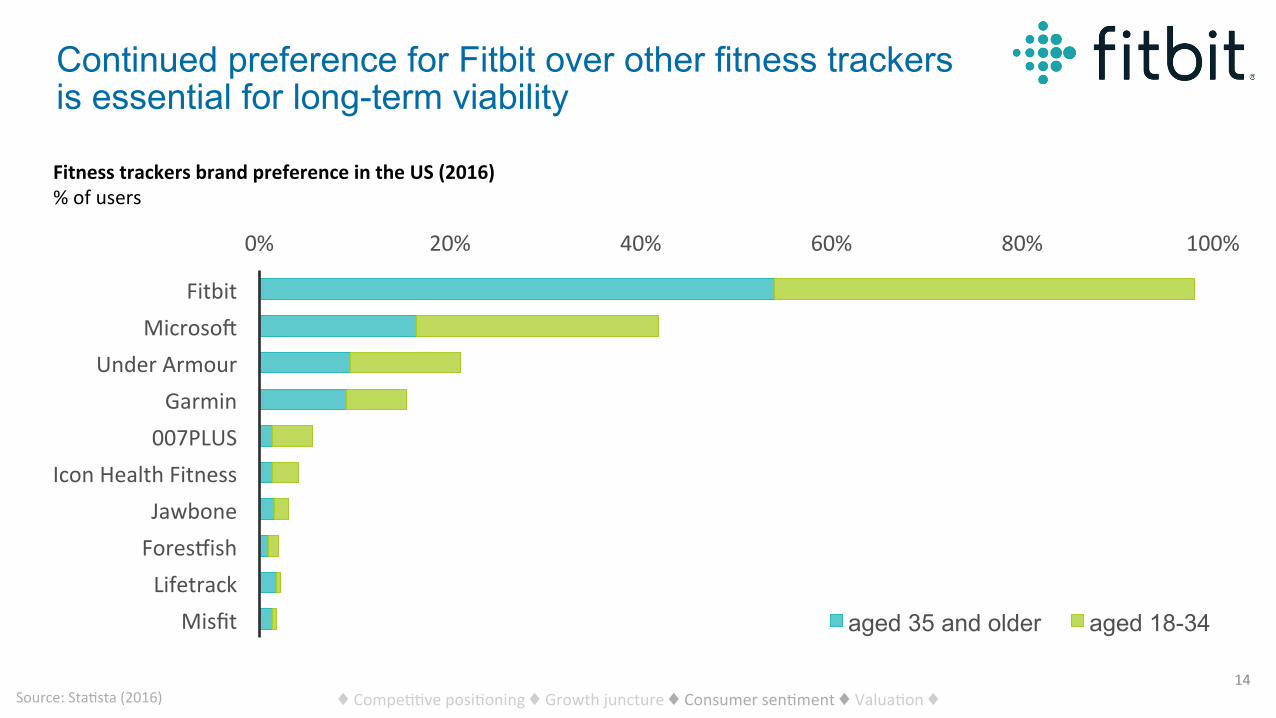

Continued preference for Fitbit over other fitness trackers is essential for long-term viability

♦Compe&&veposi&oning♦Growthjuncture♦Consumersen&ment♦Valua&on♦

0% 20% 40% 60% 80% 100%

FitbitMicrosok

UnderArmourGarmin

007PLUSIconHealthFitness

JawboneForesmishLifetrack

Misfit aged 35 and older aged 18-34

FitnesstrackersbrandpreferenceintheUS(2016)%ofusers

14Source:Sta&sta(2016)

Fitbit has a wide breadth of established distribution channels

Massmerchandisers Specialtystores Onlineretailers

Highdependenceonretailersanddistributers

♦Compe&&veposi&oning♦Growthjuncture♦Consumersen&ment♦Valua&on♦

15

Strategic partnerships with a broad spectrum of companies and communities further establishes brand identity

CommuniRes

Healthcare Companies

Lifestyle

Wellnesscommuni&es Designers

M&A

♦Compe&&veposi&oning♦Growthjuncture♦Consumersen&ment♦Valua&on♦

16

Health

Compe&&veposi&oning

◇ Con&nuedpreferenceforFitbitoverotherfitnesstrackersisessen&alforlong-termviability

◇ Widebreadthofestablisheddistribu&onchannels◇ Strategicpartnershipswithaspectrumofcompaniesandcommuni&es

Dynamicgrowth

opportuni&es

Presentlyovervalued

Fitbit is currently overvalued by 30% and should be valued at $22.75

Cri&calgrowthjuncture

Leveragedbyconsumersen&ment

◇ Assalesstabilizeinamaturingandcompe&&vemarket,costswillremainhigh,leadingEBITasapercentageofsalestoflatline

◇ Thefirmisvaluedat$5B,implyingatargetsharepriceof$22.75

◇ Posi&onedatthenexusofthefitnesstracker,lifestylewearables,andhealthIT(HIT)markets

◇ Capturesa25%shareofthemarket,althoughtheglobalmarketishighlycompe&&veandvola&le

◇ Mustseizegrowthopportuni&esinordertosucceedintheindustry◇ Foreignmarketsofferlargebutunprovenpoten&al◇ Newproductlaunchestargetedtowarddevelopingcustomersegments

17

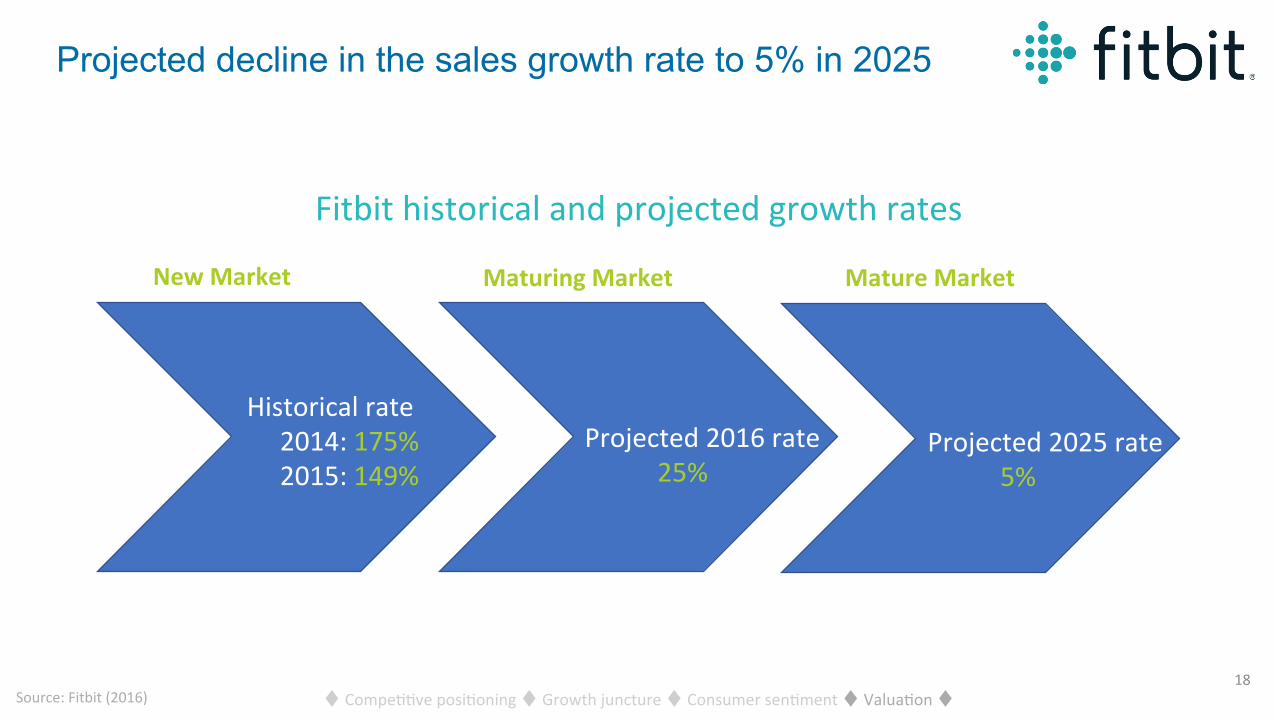

Projected decline in the sales growth rate to 5% in 2025

♦Compe&&veposi&oning♦Growthjuncture♦Consumersen&ment♦Valua&on♦

NewMarket MaturingMarket MatureMarket

Historicalrate2014:175%2015:149%

Projected2016rate25%

Projected2025rate5%

18

Fitbithistoricalandprojectedgrowthrates

Source:Fitbit(2016)

Historical(2013-2015)

ShortTerm(2016*)

LongTerm(2025*)

Salesgrowth 149-175% 25% 5%

COGSasa%ofsales

51-77% 52% 52%

SG&Aasa%ofsales

15-22% 22% 25%

R&Dexpensesasa%ofsales

7-10% 15% 10%

TotaloperaRngexpensesasa%ofsales

78-103% 89% 88%

Underlying assumptions that influence the firm’s projected $6B operating expenses in 2025

♦Compe&&veposi&oning♦Growthjuncture♦Consumersen&ment♦Valua&on♦

19Source:Fitbit(2016)

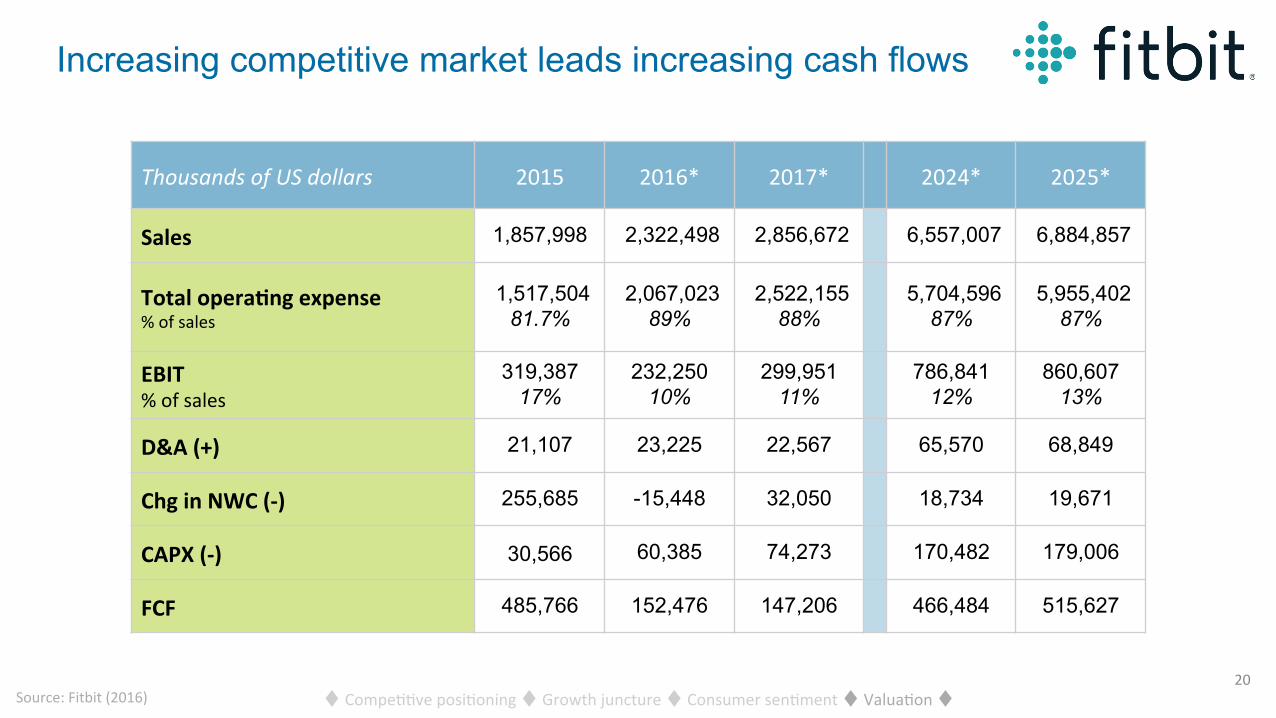

Increasing competitive market leads increasing cash flows

♦Compe&&veposi&oning♦Growthjuncture♦Consumersen&ment♦Valua&on♦

ThousandsofUSdollars 2015 2016* 2017* 2024* 2025*

Sales 1,857,998 2,322,498 2,856,672 6,557,007 6,884,857

TotaloperaRngexpense%ofsales

1,517,504 81.7%

2,067,023 89%

2,522,155 88%

5,704,596 87%

5,955,402 87%

EBIT%ofsales

319,387 17%

232,250 10%

299,951 11%

786,841 12%

860,607 13%

D&A(+) 21,107 23,225 22,567 65,570 68,849

ChginNWC(-) 255,685 -15,448 32,050 18,734 19,671

CAPX(-) 30,566 60,385 74,273 170,482 179,006

FCF 485,766 152,476 147,206 466,484 515,627

20Source:Fitbit(2016)

Fitbit’s unique WACC calculation is due to lack of debt financing and two betas

♦Compe&&veposi&oning♦Growthjuncture♦Consumersen&ment♦Valua&on♦

21Source:Fitbit(2016)

The firm is worth ~$5B, suggesting an appropriate price per share of $22.75

♦Compe&&veposi&oning♦Growthjuncture♦Consumersen&ment♦Valua&on♦

FinancialAssump&ons KeyResults

◇ Riskfreerate:2.86%

◇ Terminalgrowthrate:2.86%

◇ Terminalforecastyear:2025

◇ Beta:

Years1-6:1.85

Years7-10:1.29

◇ WACC:

Years1-6:12.11%

Years7-10:9.31%

$6.9B2025revenue

$860M2025EBIT

$5.04BEnterprisevalue

$22.75Pricepershare

22

Compe&&veposi&oning

Presentlyovervalued

Fitbit is currently overvalued by 30% and should be valued at $22.75

Cri&calgrowthjuncture

Leveragedbyconsumersen&ment

◇ Posi&onedatthenexusofthefitnesstracker,lifestylewearables,andhealthIT(HIT)markets

◇ Capturesa25%shareofthemarket,althoughtheglobalmarketishighlycompe&&veandvola&le

◇ Con&nuedpreferenceforFitbitoverotherfitnesstrackersisessen&alforlong-termviability

◇ Widebreadthofestablisheddistribu&onchannels◇ Strategicpartnershipswithaspectrumofcompaniesandcommuni&es

◇ Assalesstabilizeinamaturingandcompe&&vemarket,costswillremainhigh,leadingEBITasapercentageofsalestoflatline

◇ Thefirmisvaluedat$5B,implyingatargetsharepriceof$22.75

◇ Mustseizegrowthopportuni&esinordertosucceedintheindustry◇ Foreignmarketsofferlargebutunprovenpoten&al◇ Newproductlaunchestargetedtowarddevelopingcustomersegments

23

Appendix

25.Fitbit’sproductline

26.Fitbit’sretailers

27.FitbitSWOTanalysis

28.FitbitEBIT

29.Fitbitmodelsensi&vityanalysis

30.Currentstockprice 24

Fitbit’s product line

25

Fitbit retailers

26

♦Compe&&veposi&oning♦Growthopportuni&es♦Brandawareness♦Valua&on♦

Fitbit SWOT analysis

27

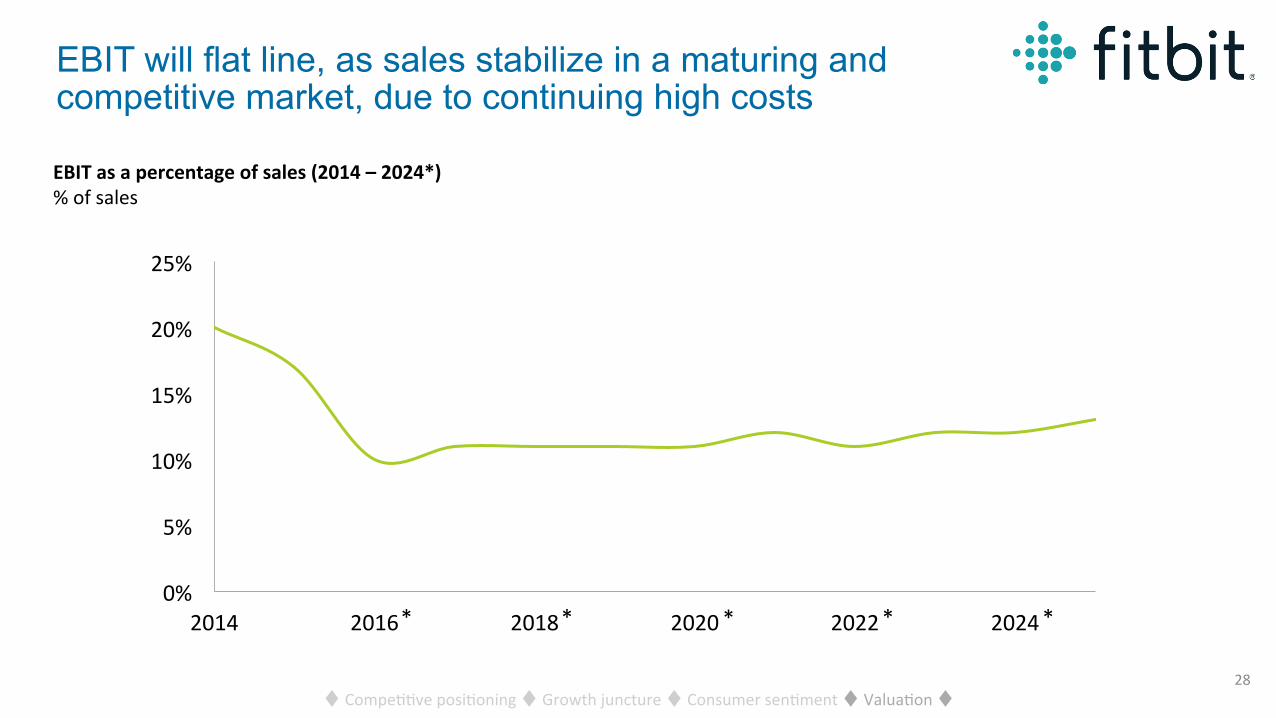

EBIT will flat line, as sales stabilize in a maturing and competitive market, due to continuing high costs

♦Compe&&veposi&oning♦Growthjuncture♦Consumersen&ment♦Valua&on♦

0%

5%

10%

15%

20%

25%

2014 2016 2018 2020 2022 2024

EBITasapercentageofsales(2014–2024*)%ofsales

* * ** *

28

COGSas%ofsales

Equitytototalcap.

SG&Aas%ofsales

R&Das%ofsales

Marketriskpremium

BetaB

Outstandingshares

Sales

Networkingcapital

Riskfreerate

Networkingcapital

Fitbit model sensitivity analysis

29

30

Fitbit’s stock has actually followed our projected trajectory, but to an even greater extent

0

5

10

15

20

25

30

35

Jan Feb March April May June July Aug Sept Oct Nov Dec

Fitbitstockprice(2016)$pershare

Source:GoogleFinance(2016)

$29.59

$7.59

$22.75

Source:EMarketer(2016)