five market trends that are re-shaping c&i energy management and procurement

TRANSCRIPT

Five Trends Re-Shaping C&I Energy Management

Emerging Technology and the Changing Role of Large Energy Users

GTM Research

C&I Customer Network

February 25, 2016

1GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

Steve Propper

Director, Grid Edge

GTM Research

Today’s Presenters

Omar Saadeh

Senior Analyst, Grid Edge

GTM Research

Moderator

Presenter

2GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

Discussion Topics

• Announcing GTM Research’s Grid Edge Customer Network

• Five Trends Re-Shaping Large Commercial and Industrial Energy Management

• Upcoming Program Developments & How to Get Involved

• Q&A

GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

GTM Research’s Grid Edge Customer Network

4GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

GTM’s Grid Edge Research Coverage

5GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

Existing Grid Edge Ecosystem

The current Grid Edge Executive Council consists of more than 100 stakeholders impacting the future electricity system, including:• Utilities• Technology Providers• Regulators & Policy Makers• Trade Organizations• Developers & Integrators• Consulting & Advisory Firms

6GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

Launch of the Grid Edge Customer Network

The world of options for large C&I customers is quickly becomingcomplex – new technologies and investment opportunities abound

Customer Network Members will include:• Big Box and Luxury Retailers• Real-Estate Investment Firms• Cities and Municipalities• Heavy Industry & Manufacturing• Data Centers & Warehouses• Campuses (Hospital, Academia, Etc.)• Other Large Energy Users

Existing market analysis provides insight specifically for:• Energy management and optimization• Building, facility or campus operations• Corporate sustainability efforts• Renewable or alternative energy sources

GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

Five Market Trends Re-Shaping Large C&I Energy Management

8GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

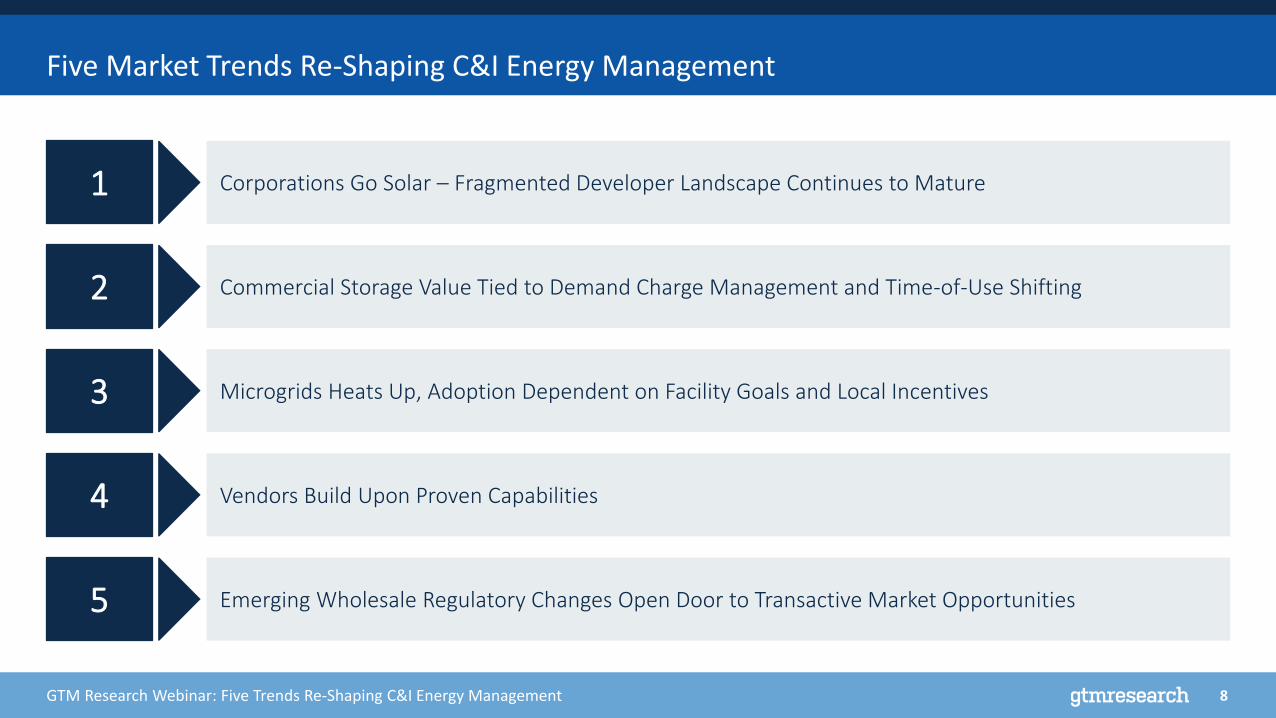

Five Market Trends Re-Shaping C&I Energy Management

1 Corporations Go Solar – Fragmented Developer Landscape Continues to Mature

2 Commercial Storage Value Tied to Demand Charge Management and Time-of-Use Shifting

3 Microgrids Heats Up, Adoption Dependent on Facility Goals and Local Incentives

4 Vendors Build Upon Proven Capabilities

5 Emerging Wholesale Regulatory Changes Open Door to Transactive Market Opportunities

GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

Corporations Go Solar – Fragmented Developer Landscape Continues to Mature

1

10GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

Walmart Leads All Corporations as the Top Solar Adopter

Top 15 Companies by Distributed Solar Capacity (MWdc)

14.2

14.32

14.32

14.62

14.94

17.34

17.76

18.44

20.78

41.41

50.21

50.75

60.73

97.54

141.99

0 20 40 60 80 100 120 140 160

Berry Plastics Corp

Verizon

Intel

FedEx

Target

Bed Bath & Beyond

Johnson & Johnson

Hartz Mountain

Macy's

IKEA

Kohl's

Costco

Apple

Prologis

Walmart

Total On-Site Installed Solar Capacity (MWdc)Source: Solar Means Business 2015, SEIA (December 2015)

11GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

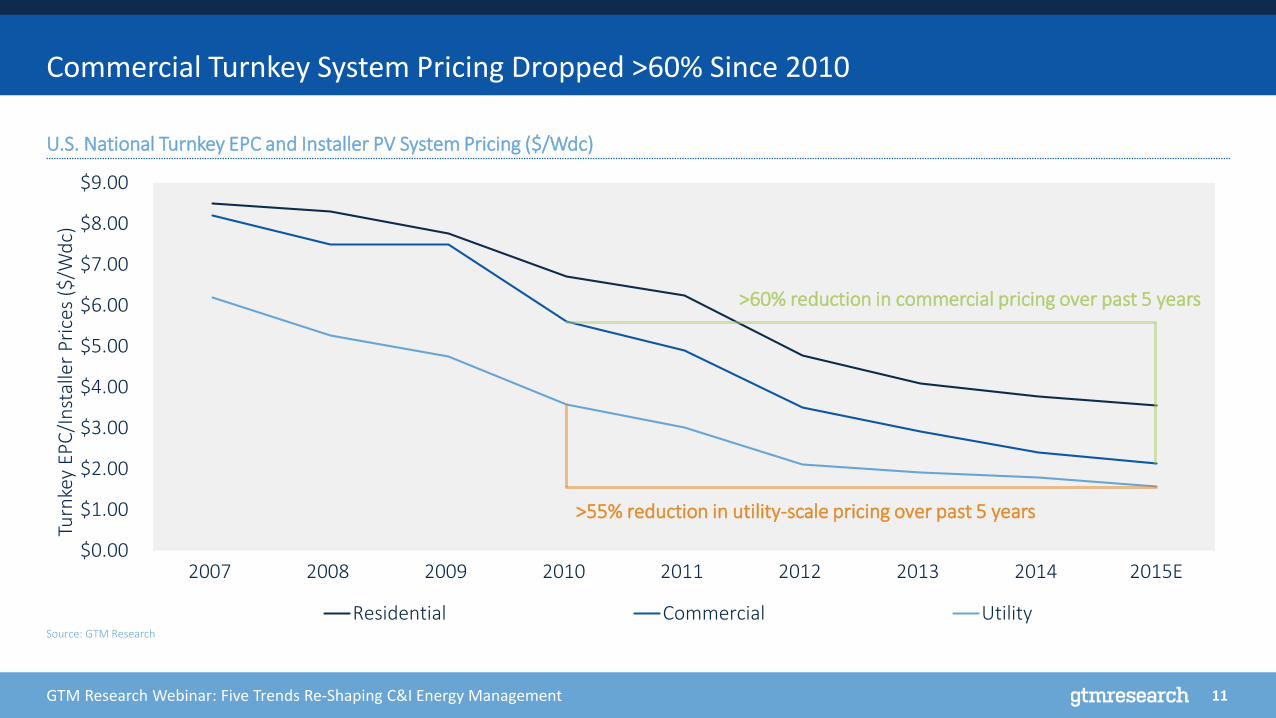

Commercial Turnkey System Pricing Dropped >60% Since 2010

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

2007 2008 2009 2010 2011 2012 2013 2014 2015E

Turn

key

EPC

/In

stal

ler

Pri

ces

($/W

dc)

Residential Commercial UtilitySource: GTM Research

U.S. National Turnkey EPC and Installer PV System Pricing ($/Wdc)

>55% reduction in utility-scale pricing over past 5 years

>60% reduction in commercial pricing over past 5 years

12GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

Shift to Third Party Ownership Expected to Continue

National Commercial Solar Installations by Ownership Structure

Note: The above graphic is based on solar data preceding the announced ITC extension, however, only minor adjustments are expected. Source: GTM Research/SEIA, U.S. Solar Market Insight

13GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

A Fragmented Market; Top 3 Installers Represent Only 27% of the Commercial Market

Non-Residential Installers, Q1-Q3 2015

Source: GTM Research U.S. PV Leaderboard Q4 2015

Emerging National Commercial Solar Providers

13%

8%

6%

SolarCity

SunPower

SunEdison

Borrego Solar Systems

G&S Solar

Cenergy Power

Ameresco

EnterSolar

JKB Development

Conergy Projects

All Others

14GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

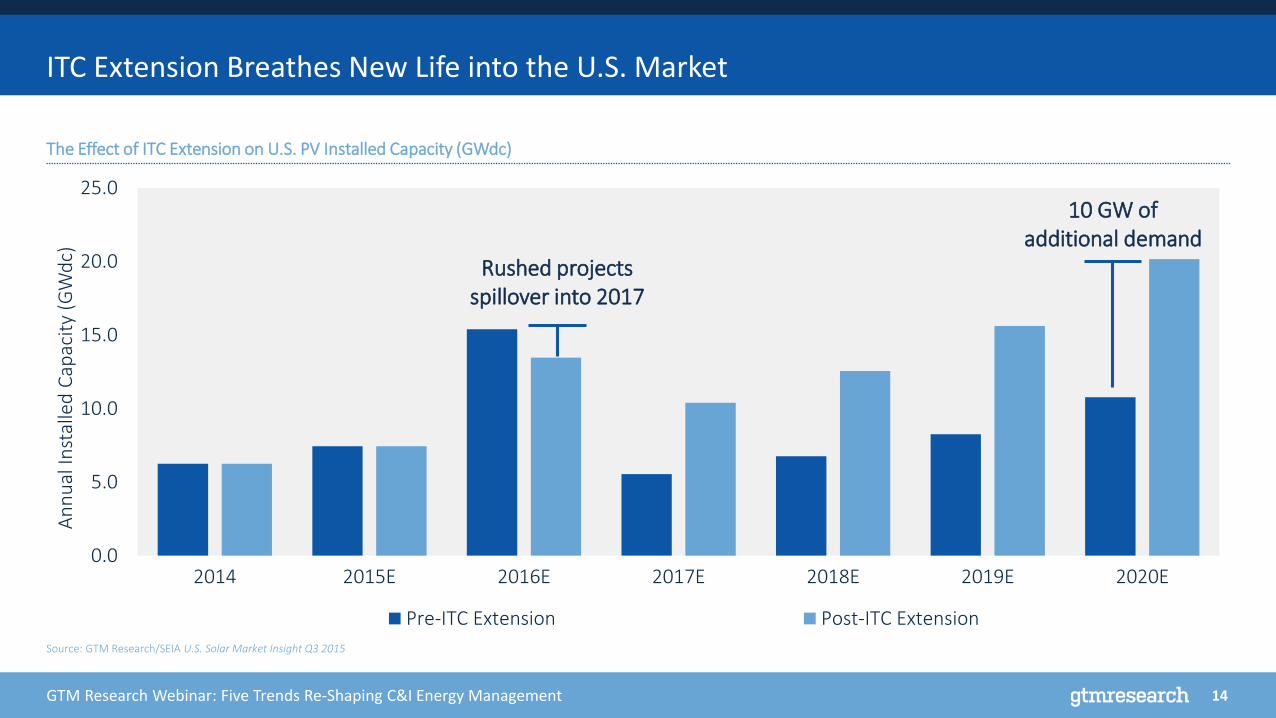

ITC Extension Breathes New Life into the U.S. Market

0.0

5.0

10.0

15.0

20.0

25.0

2014 2015E 2016E 2017E 2018E 2019E 2020E

An

nu

al In

stal

led

Cap

acit

y (G

Wd

c)

Pre-ITC Extension Post-ITC Extension

10 GW of additional demand

Rushed projects spillover into 2017

Source: GTM Research/SEIA U.S. Solar Market Insight Q3 2015

The Effect of ITC Extension on U.S. PV Installed Capacity (GWdc)

GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

Commercial Energy Storage Value Tied to Demand Charge Management and Time-of-Use Shifting

2

16GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

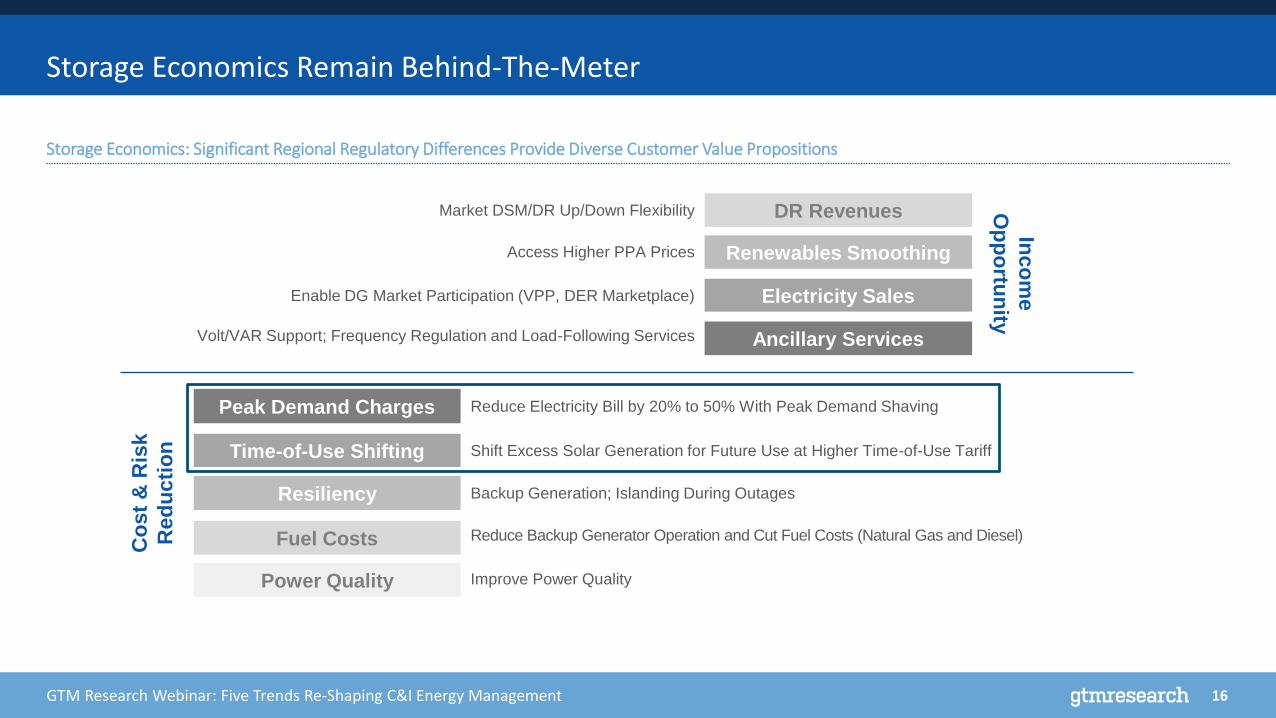

Storage Economics Remain Behind-The-Meter

Storage Economics: Significant Regional Regulatory Differences Provide Diverse Customer Value Propositions

Renewables SmoothingAccess Higher PPA PricesIn

co

me

Op

po

rtun

ity

DR RevenuesMarket DSM/DR Up/Down Flexibility

Electricity SalesEnable DG Market Participation (VPP, DER Marketplace)

Ancillary ServicesVolt/VAR Support; Frequency Regulation and Load-Following Services

Co

st

& R

isk

Red

ucti

on

Power Quality Improve Power Quality

Shift Excess Solar Generation for Future Use at Higher Time-of-Use Tariff

Resiliency

Fuel Costs Reduce Backup Generator Operation and Cut Fuel Costs (Natural Gas and Diesel)

Backup Generation; Islanding During Outages

Time-of-Use Shifting

Peak Demand Charges Reduce Electricity Bill by 20% to 50% With Peak Demand Shaving

17GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

Importance of Connecting Value of Energy Storage with Customer Load Profiles

Sample Large Hotel Consumption Profile Sample Hospital Consumption Profile

A large hotel profile generally hastwo distinct peaks and is well suitedfor demand reduction using storage.

Hospitals exhibit relatively flat loadprofiles but do have lengthy periods ofhigh usage throughout much of the day.

Source: EIA, GTM Research, Open EI

18GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

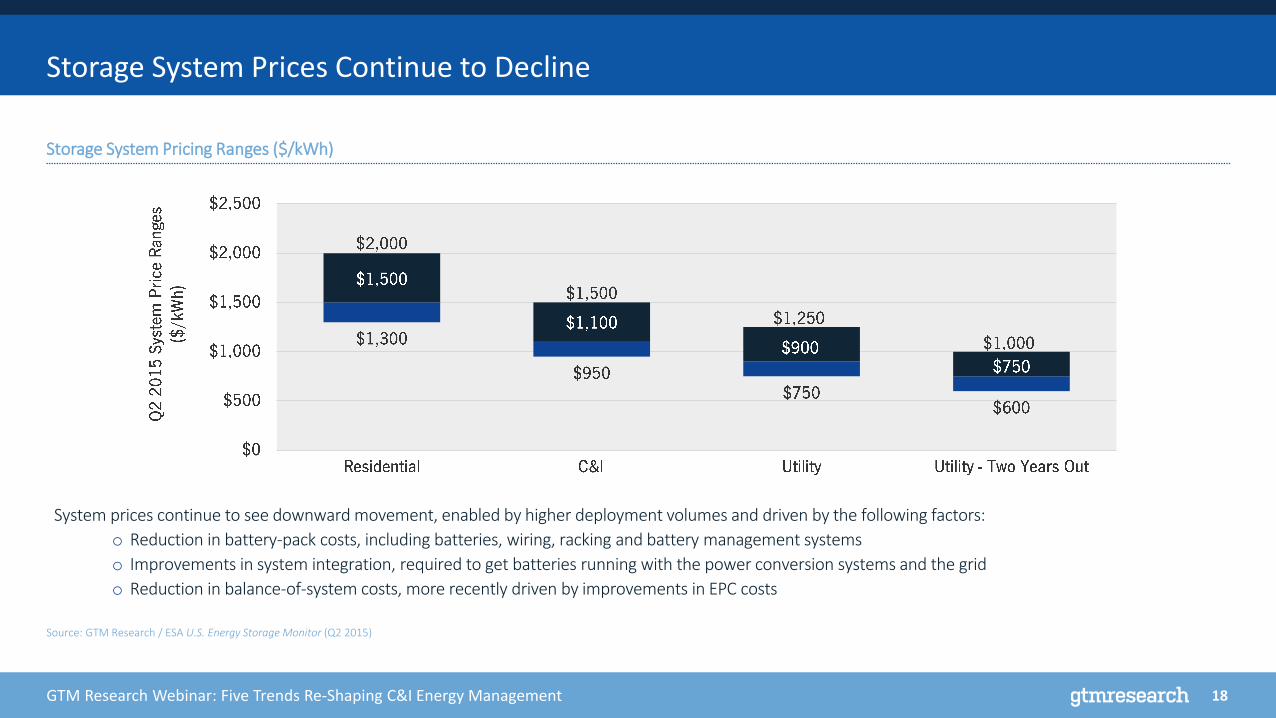

Storage System Prices Continue to Decline

Storage System Pricing Ranges ($/kWh)

System prices continue to see downward movement, enabled by higher deployment volumes and driven by the following factors:

o Reduction in battery-pack costs, including batteries, wiring, racking and battery management systems

o Improvements in system integration, required to get batteries running with the power conversion systems and the grid

o Reduction in balance-of-system costs, more recently driven by improvements in EPC costs

Source: GTM Research / ESA U.S. Energy Storage Monitor (Q2 2015)

GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

Microgrids Heats Up, Adoption Dependent on Facility Goals and Local Incentives

3

20GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

Firstly, What is a Microgrid?

GTMR Microgrid Definition:

A microgrid is an independently operable part of the distribution

network, including distributed energy sources, loads and network

assets, that is controlled within clearly defined geographical

boundaries and can operate in grid-connected or islanded mode.

Defining Features:

• Coordinated DER control

• Heat and/or electricity co-optimization

• Islanding capabilities

• Close proximity of generation and load

Source: GTM Research

Customer-Sited Microgrids Can Deploy a Range of Grid-Edge Technologies

Backup Gensets & Uninterruptible Power

Sources

Behind-the-Meter DERs

DER Aggregation & Market Participation

Across Facilities

Control, Management &

OptimizationMicrogrid

21GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

Cost Reduction and Reliability Are Dominant Drivers

University, R&D

Military Installation

City, Community

Public Institution

Commercial

Remote Community

Island

Strong Weak

Cost Reduction High Reliability (Labs, Campus) R&D, Emissions Reduction

High Reliability (Mission-Critical) Cost Reduction Less Risk (Supply, Security), R&D

Reliability (Critical Infrastructure) Energy Policy Targets Defer Investment

Reliability (Public Safety) Cost Reduction Emissions Reduction

Cost Reduction Emissions Reduction Environmental Stewardship

Renewables Integration Investment Deferral Reduce Supply-Chain Risk

Cost Reduction Reduce Supply-Chain Risk Renewables Integration

Medium

Source: GTM Research

Ranking Microgrid Drivers

22GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

The Northeast Commits Close to $500 Million in Microgrid-Related Funding Opportunities

Extreme Weather Triggers State Reliability Initiatives

New York• NYSERDA’s NY Prize to allocate $40M over 3 rounds • $20M commercial microgrid program, RISE-NYC• The state launches a new 10-year, $80M energy

storage program

New Jersey • NJ’s Energy Resiliency Bank to provide $200M in federal

disaster relief funds • $10M, 4-year energy storage program focused on critical

infrastructure

Connecticut • The state’s DEEP microgrid grant and load

program consists of 3 rounds and has committed $78M in total support

Vermont • $12M state- and DOE-supported

microgrid includes solar & storage

Massachusetts• DOER Post-Sandy Resilient Power

Program provides $40M in state solicitation; funded 18 municipal projects

Maryland• Game Changer

Program• Resiliency through

microgrids study

Over the past three years, state-managed funds in the

Northeast U.S. have committed almost $500M in

microgrid-related developments.

Specific Northeast Drivers:

• Extreme weather events and power outages

• PJM’s frequency regulation market

• State policy and incentives (green banks, grid

modernization efforts)

• Favorable rate structures (DR participation, demand-

charge reduction)

23GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

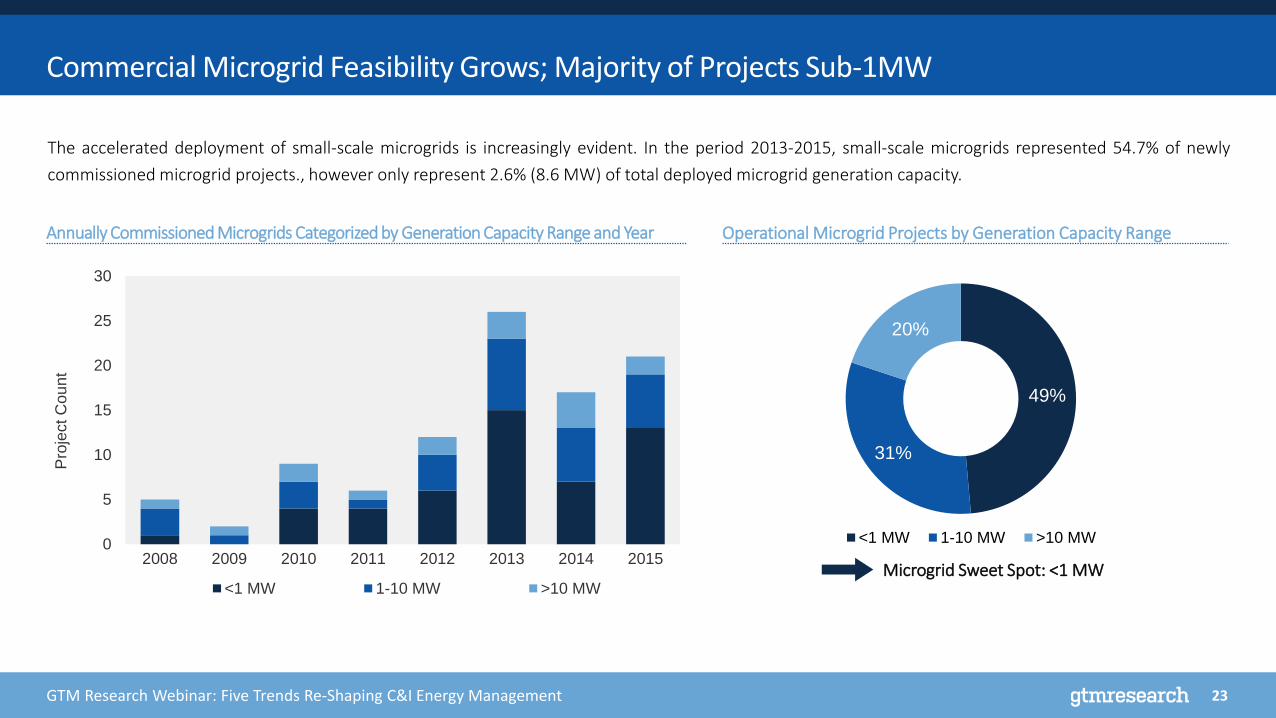

Commercial Microgrid Feasibility Grows; Majority of Projects Sub-1MW

0

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013 2014 2015

Pro

ject C

ou

nt

<1 MW 1-10 MW >10 MW

49%

31%

20%

<1 MW 1-10 MW >10 MW

Microgrid Sweet Spot: <1 MW

The accelerated deployment of small-scale microgrids is increasingly evident. In the period 2013-2015, small-scale microgrids represented 54.7% of newly

commissioned microgrid projects., however only represent 2.6% (8.6 MW) of total deployed microgrid generation capacity.

Annually Commissioned Microgrids Categorized by Generation Capacity Range and Year Operational Microgrid Projects by Generation Capacity Range

24GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

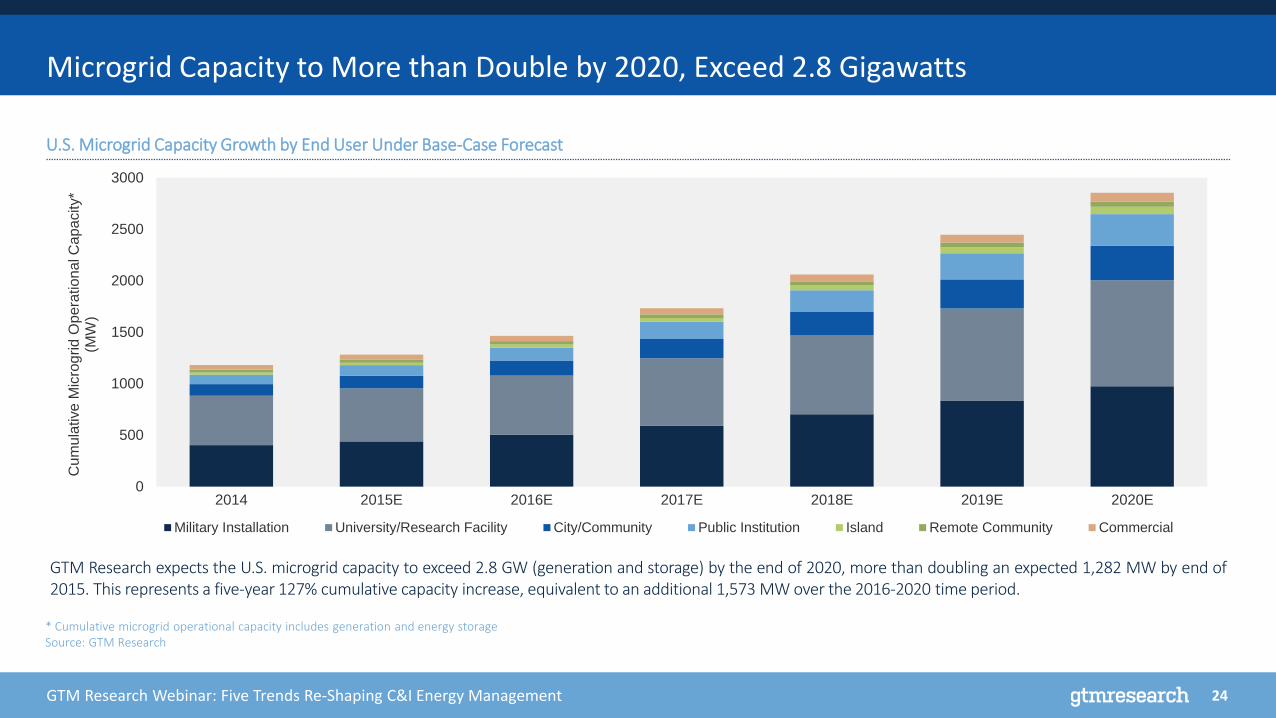

Microgrid Capacity to More than Double by 2020, Exceed 2.8 Gigawatts

0

500

1000

1500

2000

2500

3000

2014 2015E 2016E 2017E 2018E 2019E 2020E

Cu

mu

lative

Mic

rog

rid

Op

era

tion

al C

apa

city*

(MW

)

Military Installation University/Research Facility City/Community Public Institution Island Remote Community Commercial

* Cumulative microgrid operational capacity includes generation and energy storageSource: GTM Research

U.S. Microgrid Capacity Growth by End User Under Base-Case Forecast

GTM Research expects the U.S. microgrid capacity to exceed 2.8 GW (generation and storage) by the end of 2020, more than doubling an expected 1,282 MW by end of2015. This represents a five-year 127% cumulative capacity increase, equivalent to an additional 1,573 MW over the 2016-2020 time period.

GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

Vendors Build Upon Proven Capabilities4

26GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

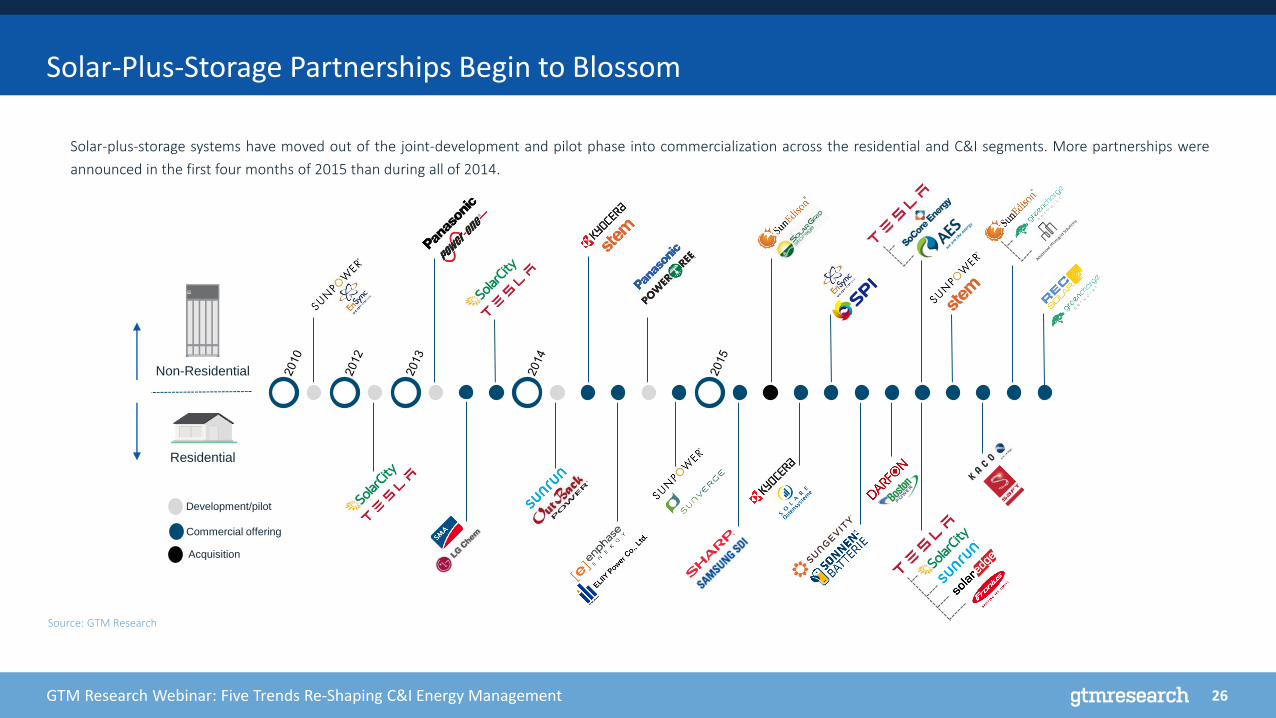

Solar-Plus-Storage Partnerships Begin to Blossom

Solar-plus-storage systems have moved out of the joint-development and pilot phase into commercialization across the residential and C&I segments. More partnerships were

announced in the first four months of 2015 than during all of 2014.

Development/pilot

Commercial offering

Acquisition

Non-Residential

Residential

Source: GTM Research

27GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

Micro-Generator

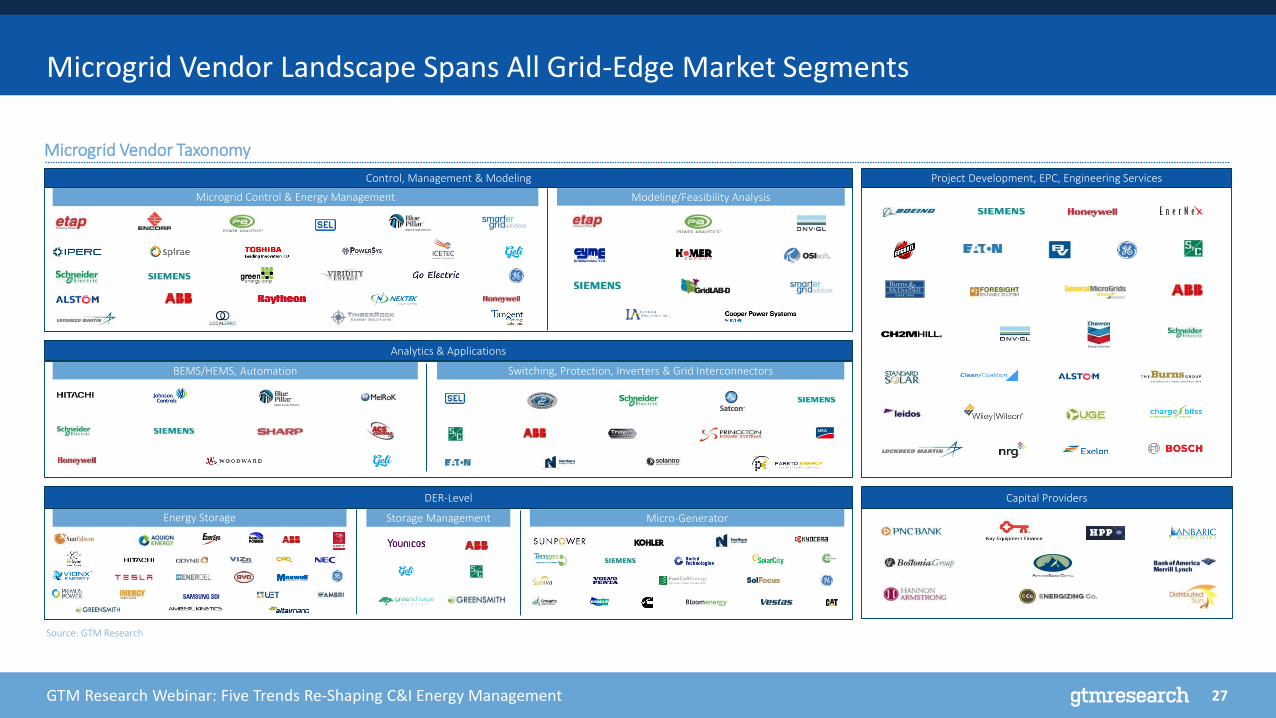

Microgrid Vendor Landscape Spans All Grid-Edge Market Segments

Analytics & Applications

Microgrid Control & Energy Management Modeling/Feasibility Analysis

BEMS/HEMS, Automation Switching, Protection, Inverters & Grid Interconnectors

Energy Storage Storage Management

Project Development, EPC, Engineering Services

Capital Providers

Control, Management & Modeling

DER-Level

Source: GTM Research

Microgrid Vendor Taxonomy

28GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

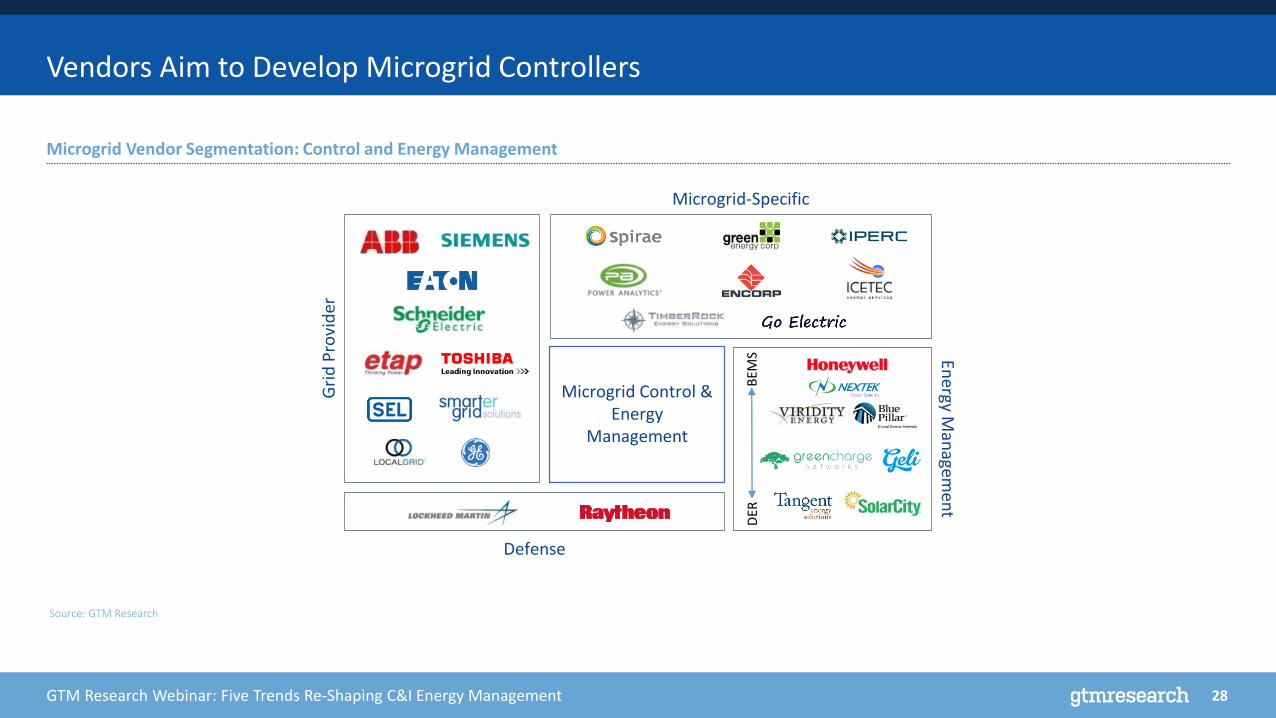

Vendors Aim to Develop Microgrid Controllers

Source: GTM Research

Microgrid Vendor Segmentation: Control and Energy Management

Gri

d P

rovi

der

Microgrid-Specific

Energy M

anagem

ent

Defense

Microgrid Control & Energy

Management

BEM

SD

ER

GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

Emerging Wholesale Regulatory Changes Open Door to Transactive Market Opportunities

5

30GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

Three ISOs Target Increased DER Wholesale Market Participation

CAISO Holds Highest Wholesale Market

Regulatory Transformation:

DER Definition:

3rd-Party Aggregation:

DER Market Rules:

Geographic Dispersion:

DER Telemetry Requirements:

Regulatory Transformation:

DER Definition:

3rd-Party Aggregation:

DER Market Rules:

Geographic Dispersion:

DER Telemetry Requirements:Regulatory Transformation:

DER Definition:

3rd-Party Aggregation:

DER Market Rules:

Geographic Dispersion:

DER Telemetry Requirements:

FavorableUnsupportive

31GTM Research Webinar: Five Trends Re-Shaping C&I Energy Management

Concluding Remarks & Glimpse at What’s to Come

• Distributed Energy Resources increasingly offer opportunities for large C&Is, as system costs decline and

positive cash flows become more clear for some applications

• A fragmented market, with many vendors and third-party intermediaries, is leading to a complex

landscape that many facility and and energy managers have to navigate

• Upcoming Grid Edge Customer Network market analysis will focus on demystifying this market for large

energy users, focusing efforts on synthesizing state and local incentives, comparing technologies and

vendor offerings, and providing deeper economic fundamentals of new investments in DERs (such as

solar, energy storage, co-generation, etc.)

• To learn more or get involved, please visit: http://www.greentechmedia.com/research/subscription/grid-

edge-customer-network

Interested in other GTM Research products and services? Please visit www.gtmresearch.com or contact [email protected]

Thank You!

February 2016