five must haves to increase earnings with … must haves sba...five must haves to increase earnings...

TRANSCRIPT

FIVE MUST HAVES TO INCREASE EARNINGS WITH SBA LENDING

Monday, March 2 Presented by Arne Monson, President,

Holtmeyer & Monson

Introductions

Arne Monson President

Holtmeyer & Monson

§ Recognized authority on SBA Lending – working closely with SBA and serving Banks and Small Business since 1982

§ ICBA Preferred Service Provider since 2006

§ 420+ lending customers

§ NAGGL Committee Member

Why SBA Lending?

§ Stay Current With Your Competitors § Get Beneficial Resource For Bank

Commercial Lending Activities § Leverage Various SBA Lending Programs § Gain Tremendous Profits From Secondary

Market § Maximize Profits with a Lender Service

Provider

.

SBA Loan Programs – The Highlights

§ Maximum loan amount – $5,000,000 § Carries up to a 85% guaranty § Maturities range from 10 to 25 Years § Typically pegged to prime rate § Guaranty fees – from 2.00% to

3.75% § Guaranty fees currently waived on

loans of $150,000 or less and Veterans Advantage Program

7 (A) Loan Program

Express Loan Program

§ Maximum loan amount - $350,000 § Carries a 50% guaranty § Maturities range from 1 to 25 years § Lender makes credit decision § Lender must maintain SBA loan

file

504 Loan Program

§ Hybrid financing: fixed assets only § SBA junior security or mortgage

interest § Application processed through

CDC § Maximum debenture $5,000,000

to $5,500,000 § Minimum project funding structure

50%-40%-10%

Opportunities through SBA Lending

§ Make more loans in your local market- compete more effectively

§ Mitigate bank leverage and concentration issues

§ Mitigate collateral risk via SBA enhancements

§ Gain profit potential from non-interest fee income

How To Improve Your Results? The Five Must-Have’s for SBA Lending

$

Must-Have #1 Bank-Wide Support

Bank-Wide Support

§ Senior management, ownership, and BOD must embrace the program

§ Conversational knowledge throughout the organization

§ Budget dedicated and driven – quantifiable

§ Compensation plans reflect SBA lending results

§ Set goals and track results – KPIs/metrics

Must-Have #2 Prospect and Product Awareness

Prospect and Product Awareness

§ Build brand awareness for your bank

§ Who are your best small business prospects based on your current customers/demographics?

§ Referral sources – professional services network

§ Advertising and promotional programs – lunch and learns, small business meetings, etc.

§ Handle “marginal” commercial loan requests

§ Expand commercial lending activities

Lending to Non-Traditional Borrowers

§ Business acquisitions and financing goodwill

§ Start-up businesses § Specialty businesses –

e.g. hotels, restaurants, franchises

§ Term out existing commercial loans and lines of credit

Must-Have #3 Lender/Staff Training and Incentives

Lending and Loan Operations Staff Training

§ Working knowledge of SBA loan programs § Seek out “marginal” credit request § Transaction structuring –

competition and profitability § Incentives provided at the

department and individual level § Equip staff members with tools – calculators,

brochures and program guides

Staff Training : Benefits to Borrower

§ Ability to secure financing on terms and conditions otherwise not available

§ Capitalize fees into loan § Extended term permanent

financing § MAXIMIZE CASH FLOW

Must-Have #4 Secondary Market Opportunities

$

Great Earnings Opportunities Through Secondary Market

§ A very active and lucrative secondary market exists for sale of loan guarantees

§ Pool assemblers acquire individual guarantees at historically high premium levels

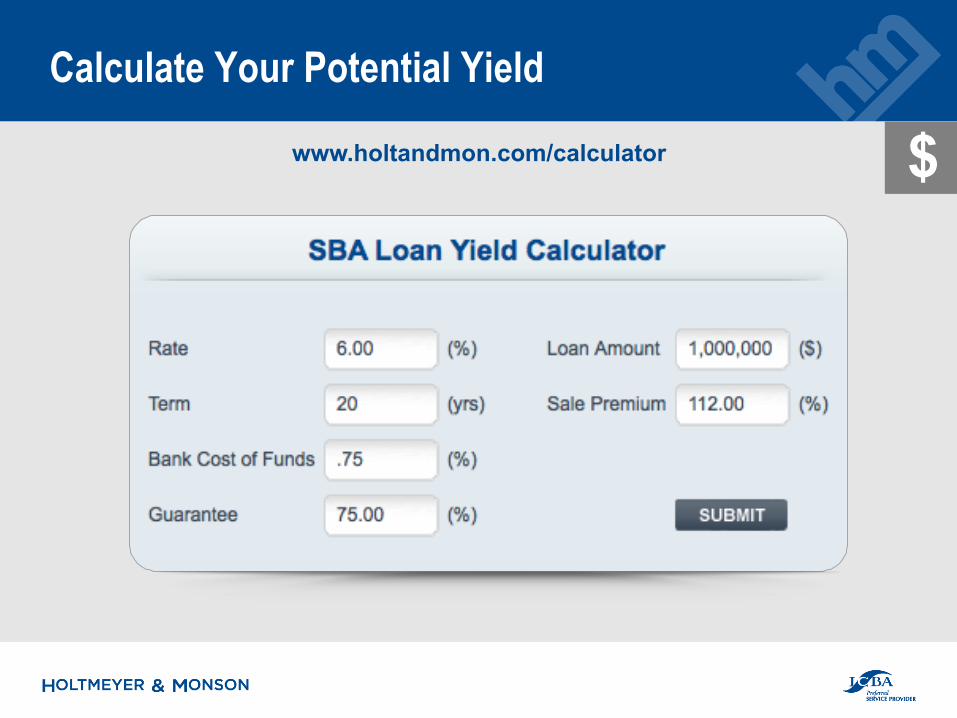

§ Use of a yield calculator

$

Calculate Your Potential Yield

www.holtandmon.com/calculator $

Calculate Your Potential Yield

$www.holtandmon.com/calculator

Calculate Your Potential Yield

$www.holtandmon.com/calculator

Calculate Your Potential Yield

$www.holtandmon.com/calculator

Calculate Your Potential Yield – Year 1

www.holtandmon.com/calculator $

Calculate Your Potential Yield – Year 2

www.holtandmon.com/calculator $

Must-Have #5 SBA and Regulatory Compliance

The nature of the beast… and cannot be minimized.

There are consequences.

Required Resources and Investment

§ Staff dedicated to SBA Lending § Allocated resources to keep up with

the policy and regulatory changes § Knowledge of market conditions § Investment in software platform,

including training - required to do business electronically with SBA

§ The right balance: overhead has to be justified by consistent loan volume

Risks in the SBA Lending Process

§ Loss or repair of SBA guaranty may result from improper loan closing process § Lack of verification of equity injection

§ Failure to perfect required security interest – Example

§ Improper disbursement of loan proceeds

§ Pre-closing authorization modifications

RISK

Most Overlooked Items

§ Credit scoring requirements § Collateral requirements § Credit memo outlines: over or

under $350,000 § Credit bureau reporting requirements § On-going changes to SBA policies and

procedures

!

The Bottom Line in Compliance

§ Lenders must strictly follow SBA procedures to assure compliance with guaranty authorization requirements

§ SBA assumes the role of the largest risk-taker in the transaction

§ Post-closing loan servicing actions and reporting can be cumbersome for lenders

§ SBA loan liquidations and guaranty claims are very specialized – reverse application

The Five Must-Haves

Bank-Wide Support

Prospect and Product Awareness

Lender/Staff Training and Incentives

Secondary Market Opportunities

SBA and Regulatory Compliance

$

There IS help available.

Holtmeyer & Monson Program Features

Holtmeyer & Monson is a full-service SBA Lender Services Provider that focuses solely on the unique opportunity SBA lending presents for community banks.

§ Complimentary Initial Consultation to determine eligibility and program structure.

§ Submission of the Completed Loan Application to the SBA for approval and guarantee issuance.

§ Loan Closing Services with detailed documentation instructions § Securitization and Sale of SBA Guarantee generated from the loan

transaction § SBA Loan Portfolio Management, including payment processing and

remittance, required reporting, and detailed monthly activity reconciliation and reporting.

Why Consider Outsourcing SBA Lending

§ High level of expertise without significant investment

§ Assure agency and regulatory compliance

§ Meet conforming documentation requirements

§ Leverage existing bank personnel

§ Avoid mis-steps which may jeopardize guarantees

Advantages for ICBA Members

§ Reasonable and competitive fee structure

§ 10% off H&M Lender fees for ICBA Members

§ H&M contributes fees in the form of royalties to ICBA

§ NO NET COST TO BANK!

“Now we are able to compete with our larger bank players in the market . . our partnership with Holtmeyer & Monson keeps our expenses down and their expertise provides a level of efficiency that far exceeds our expectations.”

Jenny Scully, Vice President Howard Bank, Rising Sun, MD

“Holtmeyer & Monson helped us add 33% to our normal earnings last year through SBA lending.”

Will Griffin, Jr., President, Brighton Bank, Brighton, TN

Next Steps

§ Contact us to discuss your situation § Calculate your potential SBA

earnings holtandmon.com/calculator

§ Sign up for our e-Newsletter SBA Lending Matters

§ Start getting your “must haves” in order TODAY!

Thank You!

800.340.7304