flaconi - noah16 london

TRANSCRIPT

Opportunity to become Europe’s Leading Platform for Beauty Products

GET YOUR TICKET TODAY!www.noah-conference.com

2-3Tempodrom, Berlin Old Billingsgate, London

NOV201722-23 JUN2017

SAVE THE DATE

1

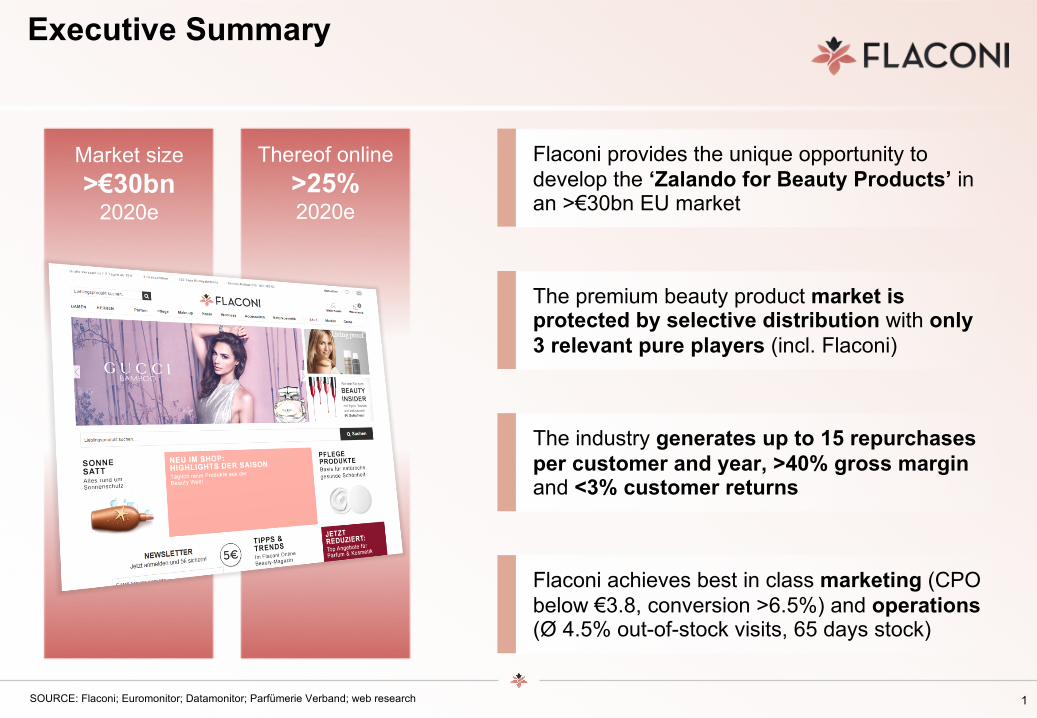

Executive Summary

SOURCE: Flaconi; Euromonitor; Datamonitor; Parfümerie Verband; web research

Market size>€30bn

2020e

Thereof online>25%2020e

Flaconi provides the unique opportunity to develop the ‘Zalando for Beauty Products’ in an >€30bn EU market

The premium beauty product market is protected by selective distribution with only 3 relevant pure players (incl. Flaconi)

The industry generates up to 15 repurchases per customer and year, >40% gross margin and <3% customer returns

Flaconi achieves best in class marketing (CPO below €3.8, conversion >6.5%) and operations(Ø 4.5% out-of-stock visits, 65 days stock)

2

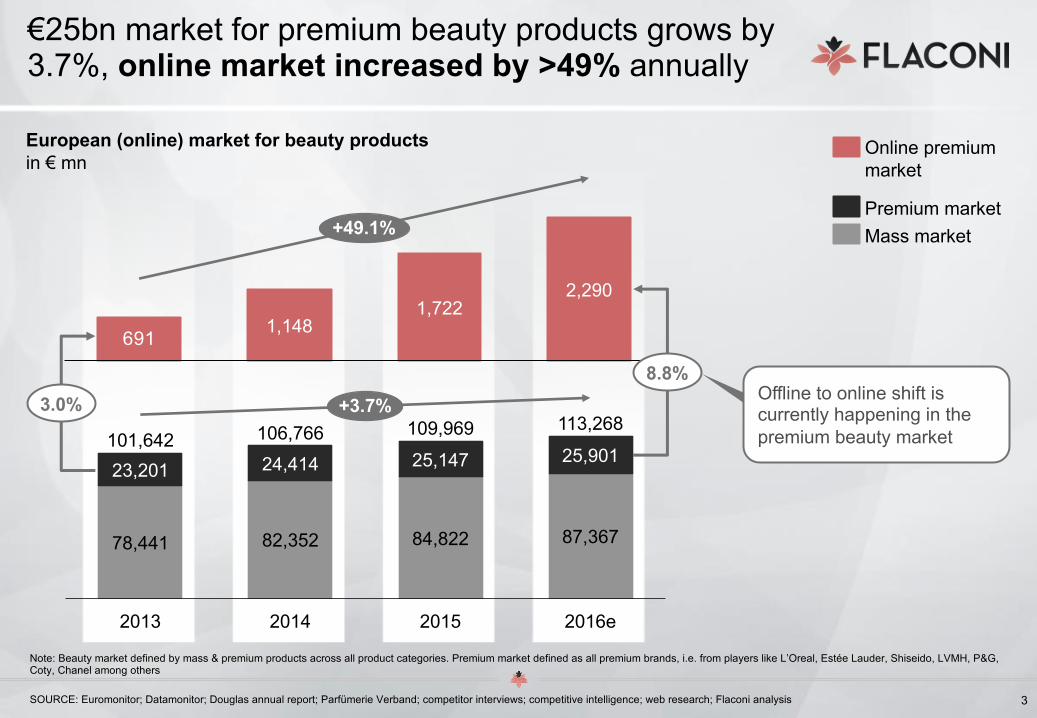

Premium beauty product market in Europe is big, growing & starting to move online

>€25bn marketfor premium beauty products1 in Europe

Up to

15 repurchasesfor beauty products per yearin Germany

Average annual spend of

>€152 for fragrances (€106 facial care, €124 body care)in Germany

71% of women use Perfume & Eau de Toilette every day in Germany

Double digit online growthindicates an offline to online shift is happening

1 Premium market defined as all premium brands, i.e. from players like L’Oreal, Estée Lauder, Shiseido, LVMH, P&G, Coty, Chanel, Hugo Boss among others; no white label drug store products

SOURCE: Euromonitor; Datamonitor; Douglas annual report; Parfümerie Verband; web research; Flaconi analysis

3.7% p.a. growthof beauty market shows robust industry trend

3This copyrighted document is property of the Flaconi GmbH and is disclosed in confidence. 3

€25bn market for premium beauty products grows by 3.7%, online market increased by >49% annually

Note: Beauty market defined by mass & premium products across all product categories. Premium market defined as all premium brands, i.e. from players like L’Oreal, Estée Lauder, Shiseido, LVMH, P&G, Coty, Chanel among others

SOURCE: Euromonitor; Datamonitor; Douglas annual report; Parfümerie Verband; competitor interviews; competitive intelligence; web research; Flaconi analysis

106,766

78,441

25,14724,414

2013

23,201101,642

2014

82,352

2015

113,268

2016e

87,36784,822

25,901

+3.7%109,969

691 1,148

+49.1%

1,7222,290

Premium marketMass market

Online premium market

European (online) market for beauty productsin € mn

3.0%8.8%

Offline to online shift is currently happening in the premium beauty market

4

Company fact sheet

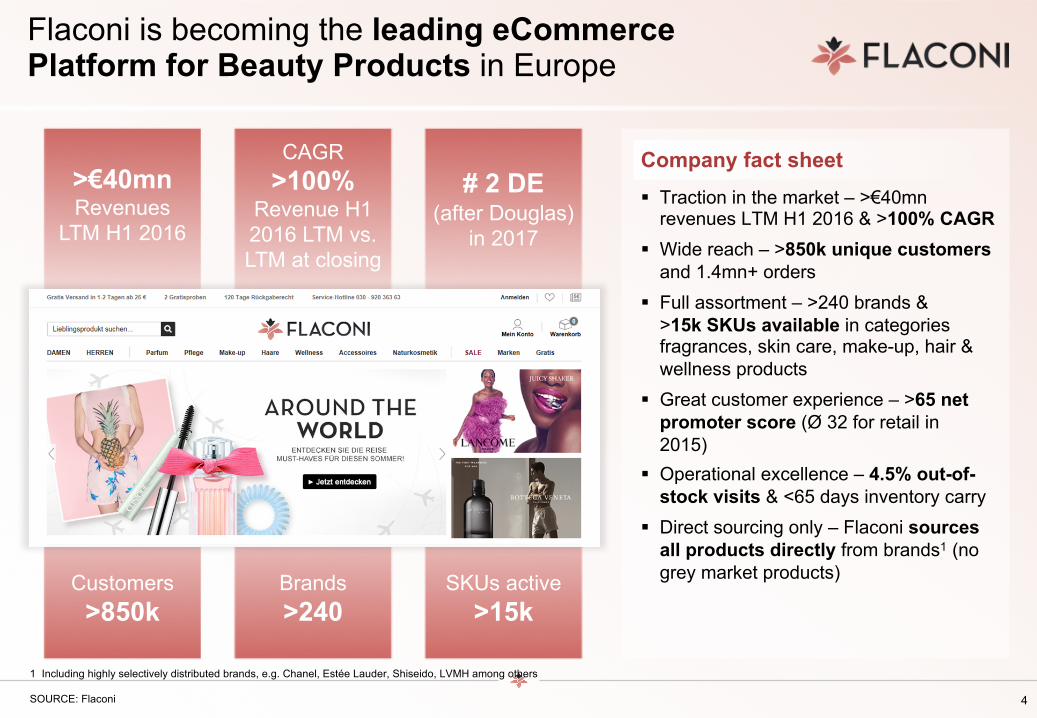

Flaconi is becoming the leading eCommercePlatform for Beauty Products in Europe

>€40mnRevenues

LTM H1 2016

CAGR >100%

Revenue H1 2016 LTM vs. LTM at closing

# 2 DE(after Douglas)

in 2017

Customers>850k

Brands>240

SKUs active>15k

§ Traction in the market – >€40mn revenues LTM H1 2016 & >100% CAGR

§ Wide reach – >850k unique customersand 1.4mn+ orders

§ Full assortment – >240 brands & >15k SKUs available in categories fragrances, skin care, make-up, hair & wellness products

§ Great customer experience – >65 net promoter score (Ø 32 for retail in 2015)

§ Operational excellence – 4.5% out-of-stock visits & <65 days inventory carry

§ Direct sourcing only – Flaconi sources all products directly from brands1 (no grey market products)

1 Including highly selectively distributed brands, e.g. Chanel, Estée Lauder, Shiseido, LVMH among others

SOURCE: Flaconi

5This copyrighted document is property of the Flaconi GmbH and is disclosed in confidence. 5

2009 2011 2010 2012

Flaconi is well positioned to become the ‘Zalando for Beauty Products’

SOURCE: Zalando annual reports; Statista; Flaconi analysis

Revenue development Zalando vs. Flaconi year 1 to 6 after launchindexed to 100% (year 3 after launch)

359

280

205

100

382

327

121100

274

638

Zalando (DACH only)Flaconi (DE only)

2011 2013 2012 2014 2013 2015 2014 2016e

ProSiebenSat.1 acquired Flaconi

2015

Zalando

Flaconi

Category expansionLaunch

Media for equity deal

Operational excellence

§ Skin & hair care§ Fragrances § 2012/13 § 2014/15

§ Shoes § Fashion & sports § 2010/11 § 2012/13

Flaconi #2 online retailer for premium beauty

products

6This copyrighted document is property of the Flaconi GmbH and is disclosed in confidence. 6

TV media support developed Flaconi’s brand awareness to ~50% within 3 years

0

10

20

30

40

50

30.0%

2HY13

29.7%

1HY16

48.1%

2HY15

+62.0%

44.0%

1HY15

39.4%

2HY14

34.9%

1HY14

Awareness grew from 30% in 2HY13 to 48% in 1HY16

1 Top of mind awareness in on-site survey using structured questionnaire

SOURCE: Flaconi; SevenOne Media brand awareness survey 2016 (persons between 18-59 years; n = 1,002)

Brand awareness1

(in %)

2014 2015 20162013

7This copyrighted document is property of the Flaconi GmbH and is disclosed in confidence. 7

Startup Professionalization Scaling

30.7

2014 2016e

11.4

20122011 2017e

9.42.5

2015

0.4

2013

Launch

Flaconi is growing strongly since 2011 & now scaling due to professionalization after P7S1 acquisition

SOURCE: Flaconi 7

in € mn

CAGR 14-16e:>100%

8This copyrighted document is property of the Flaconi GmbH and is disclosed in confidence. 8

Basket size of returning customers (2HY14-2015)in € per order

Returning customers buy Ø 3.4 times and their basket size is >20% bigger than AOV

1 Extrapolated to full 12 month cohort 2 Expanding selection in hair care, skin care & make-up 3 Average order value (excl. taxes) 2015

SOURCE: Flaconi; order baskets and frequency of with at least 2 orders customers between 2HY14-2015

AOV3

€1.43

+14%

2HY15

61.20

1HY15

52.26

2HY14

53.56

2HY15

3.401

1HY15

3.13

2HY14

3.07

+11%

Orders by returning customers (2HY14-2015)in # order of customers (cohort view)

Acquisition by ProSiebenSat.1

Selection expansion2

9

Low competition in Germany as well as Europe due to selective distribution system

Low competition§ Selective distribution

system limits threat of new entrants (‘Amazon protection’)

§ 3 domestic competitors: Douglas, parfumdreams and iParfumerie

§ 2 pure play EU competitors:feelunique, lookfantastic

Limited digital capabilities§ Scattered local retailers lack

skills to digitalize their business

§ Focus on rather ‘bringing store online’ than digital pure play

§ Main competitor Douglas focuses on brick & mortar stores

Note: Online revenue only for Douglas

SOURCE: Flaconi

Offline

Low budget brands

Online

Premium brands

Competition in domestic market

10

Flaconi has opportunities to enter additional EU markets organically & inorganically

Complexity to enter

Easy

Difficult

Organic

M&A priorities

Low High

Market attractiveness

Beauty & care market 2015, in EUR bn.

Online growth beauty & care, YoY 2015, in %

§ Competitive intensity/rivalry

§ Product use differentiation

§ Geographical access (distance)

§ Market size (beauty & care) – total§ Online penetration (beauty & care)§ Market growth rate – online§ Price positioning§ Economic stability

Poland+8.33.5

Austria+9.41.5

Switzerland+9.41.4

Netherlands+9.7 3.1

Italy+9.7

8.9

UK+6.2

15.5

France+4.1

12.6

Nordics+9.3 5.8

Spain &Portugal

+1.4 8.2

Organic growth focus§ Media alliance partners

contacted for potential M4E deals

M&A focus, potential targets§ Nordics§ UK§ Further potential targets to be

screened

SOURCE: Flaconi; Euromonitor; web research

Selected Completed NOAH Transactions

Focus on Leading European Internet companies

Covering over 400 companies across 25 online verticals, a broad range of over 500 investors as well as 100+ online-focused corporates

Deep understanding of industry dynamics

Ability to add value beyond banking advice

Facilitates overall process and minimizes management distraction

NOAH Advisors is globally well connected and has direct access to virtually all key players in the industry

Knowledge of and strong relationships with potential buyers’ key decision makers

Proactively finds and unlocks attractive investment opportunities for leading investors

Annual NOAH Conference in its 8th year

Over 40 years of combined relevant M&A experience

Routine execution of M&A and financing transactions with sizes of several billion euros

24 successfully completed NOAH Advisors transactions underline successful transfer of M&A competencies to the Internet sector

Entrepreneurial mind-set, focused on growing the business and establishing a reputation for excellence

Ability to deliver top results in short time frames

Highly success-based compensation structures align interests of clients and NOAH Advisors, and demonstrate conviction to deliver top results

Creative deal solutions

September 2015

December 2014

September 2014

October 2014

May 2014

Sale of a 70% stake in

to

Exclusive Financial Advisor to Drushim and its Shareholders

Sale of 100% of

for $800m to

Exclusive Financial Advisor to Fotolia and the Selling Shareholders

Sale of 100% of

for €80m to

Exclusive Financial Advisor to Trovit and its Shareholders

Sale of controlling stake in

to

Exclusive Financial Advisor to Facile.it and its Shareholders

sold 100% of

for $228m to a joint venture between

Exclusive Financial Advisor to Yad2 and its Shareholders

Unique Industry Know-How

Unmatched Network and Relationships

Strong Investment Banking Competence

Full Commitment - We Are Entrepreneurs!

EUROPE’S LEADING INTERNET CORPORATE FINANCE BOUTIQUE

September 2016October 2016

May 2016

Investment in

by

Financial Advisor to Oakley Capital

Exclusive Financial Advisor to 10Bis and its Shareholders

®

Marco RodzynekManaging Director & Founder

Jan BrandesManaging Director

Justus LumpeManaging Director

The NOAH Advisors Core Banking Team

Nikhil ParmarDirector

10Bis Drushim

Acquisition of a Majority Stake in

by

from

at a valuation of €300m

Investment in

Exclusive Financial Advisor to KäuferPortal and its Shareholders

by

84% Ownership